Europe Primer Market Size, Share, Trends & Growth Forecast Report By Material, By Application, By End-Use Industry, and By Country (Germany, France, Italy, United Kingdom, Spain & Rest of Europe) – Industry Analysis and Forecast, 2026 to 2034

Europe Primer Market Size

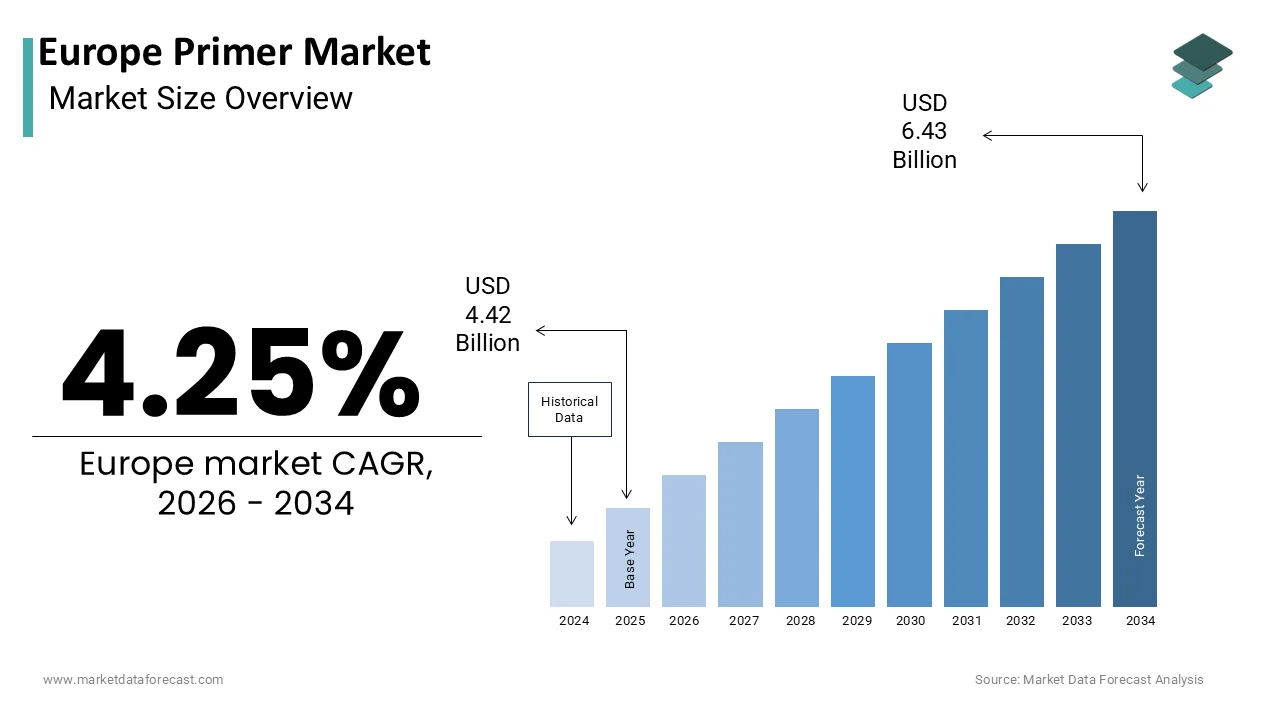

The Europe primer market was valued at USD 4.42 billion in 2025, is estimated to reach USD 4.61 billion in 2026, and is projected to reach USD 6.43 billion by 2034, growing at a CAGR of 4.25% from 2026 to 2034.

The primer is focusing on preparatory coatings applied to substrates before the final topcoat. These formulations are engineered to enhance adhesion provide corrosion resistance and seal porous surfaces ensuring the longevity and aesthetic quality of the final finish. Primers are indispensable in construction automotive manufacturing and industrial maintenance sectors where surface integrity is paramount. The market operates under stringent regulatory frameworks that dictate chemical composition and environmental impact. The automotive industry also drives demand with vehicle production requiring precise surface preparation for durability and visual appeal. According to the European Automobile Manufacturers Association passenger car production in the EU reached 10.5 million units in 2023, underscoring the sustained need for high performance primers. Environmental regulations such as the Industrial Emissions Directive influence product development by limiting volatile organic compound emissions. The European Environment Agency notes that industrial solvent use remains a key target for emission reductions prompting a shift towards water borne and high solids primer technologies. This regulatory landscape combined with industrial activity defines the operational context of the Europe primer market. The integration of advanced polymers and nano materials further enhances primer performance addressing specific challenges such as humidity resistance and thermal stability.

MARKET DRIVERS

Expansion of Automotive Production and Electric Vehicle Manufacturing

The resurgence of automotive production and the rapid transition to electric vehicles is majorly escalating the growth of Europe primer market. Original equipment manufacturers require advanced primer systems to ensure corrosion protection and adhesion for increasingly complex vehicle structures. The shift towards electric vehicles introduces new material combinations including aluminum and composite panels which necessitate specialized primer formulations to ensure proper bonding and durability. As per the International Energy Agency, electric car sales in Europe surpassed 2 million units in 2023 accounting for more than 20% of total car sales. This transition drives innovation in primer technologies such as cathodic electrocoats that provide uniform coverage and superior corrosion resistance for battery enclosures and chassis components. The lightweighting trend in automotive design further amplifies demand for high performance primers that can adhere to diverse substrates without adding significant weight. Additionally, the average age of vehicles on European roads is increasing leading to higher demand for automotive refinish primers in the aftermarket sector. Manufacturers are investing in research and development to create eco-friendly primer solutions that meet stringent environmental standards while delivering exceptional performance. The combination of increased production volumes and technological advancements in vehicle design sustains strong demand for automotive primers in the European market.

Revitalization of Construction Infrastructure Through Renovation Initiatives

The extensive renovation of existing infrastructure and building stock for protective and decorative primers is greatly influencing the growth of Europe primer market. Governments are implementing aggressive energy efficiency and preservation targets that require upgrading building envelopes, which often involves surface preparation and priming before applying final coatings. According to the survey, the Renovation Wave strategy aims to double the annual energy renovation rate of residential and non-residential buildings by 2030. This initiative necessitates the use of high performance primers that provide moisture resistance and enhance adhesion for insulation systems and facade coatings. As per Eurostat, the building stock in the European Union is energy inefficient creating a vast addressable market for renovation related products. The demand for anti-corrosive primers has risen as property owners seek to protect structural elements from weathering and decay. Additionally, the restoration of historical buildings requires specialized primers that preserve architectural integrity while providing modern protection. The construction industry’s recovery post pandemic has further amplified this trend with increased investment in both public and private projects. Manufacturers are responding by developing low volatile organic compound primer formulations that meet stringent environmental standards while offering superior sealing properties. The integration of smart primers that can indicate structural stress or moisture ingress also adds value to renovation projects.

MARKET RESTRAINTS

Stringent Environmental Regulations on Volatile Organic Compounds

The strict environmental regulations limiting the use of volatile organic compounds pose a significant restraint to the Europe primer market. Regulatory frameworks, such as the Industrial Emissions Directive and the National Emission Ceilings Directive impose tight restrictions on solvent based primer products which have traditionally been favored for their superior penetration and drying characteristics. According to the European Environment Agency, emissions of volatile organic compounds from industrial processes must be reduced by 40% by 2030 compared to 2005 levels. This mandate forces manufacturers to reformulate products using water borne or high solids technologies which can be more expensive and technically challenging to produce. As per the European Chemicals Agency, the registration and evaluation of new chemical substances under the Registration Evaluation Authorization and Restriction of Chemicals regulation add considerable time and cost to product development. Small and medium sized enterprises often struggle to comply with these complex regulatory requirements due to limited resources for research and testing. The transition away from solvents can also impact the performance of primers in terms of drying time and adhesion leading to customer resistance in professional applications. Additionally varying national implementations of European directives create a fragmented regulatory landscape that complicates cross border trade. Compliance costs are passed on to consumers potentially reducing demand in price sensitive segments. The continuous tightening of environmental standards requires ongoing investment in cleaner technologies, which constrains profit margins and limits the availability of certain high performance solvent based primers in the market.

Volatility in Raw Material Prices and Supply Chain Disruptions

Fluctuations in the prices of key raw materials, such as epoxy resins acrylics and zinc dust is limiting the growth of Europe primer market. These inputs are essential for producing high quality protective primers and their prices are influenced by global supply dynamics energy costs and geopolitical tensions. According to the International Monetary Fund, global commodity prices experienced significant volatility in recent years affecting the cost structure of chemical manufacturers. As per study, producer prices for chemicals in the European Union increased by over 20% in 2022 driven by higher energy and feedstock costs. The reliance on imported raw materials exposes European manufacturers to currency exchange rate risks and supply chain disruptions. Disruptions in logistics due to port congestion or labor strikes can lead to delays and inventory shortages impacting production schedules. The energy intensive nature of primer manufacturing further amplifies the impact of rising electricity and natural gas prices. Manufacturers face difficulties in passing on these increased costs to customers who are sensitive to price changes. This margin pressure discourages investment in new capacity and innovation. Additionally, the scarcity of certain specialty additives can limit product availability and hinder the development of new formulations. The unpredictability of input costs complicates long term planning and strategic decision making for industry participants.

MARKET OPPORTUNITIES

Development of Bio Based and Sustainable Primer Solutions

The development of bio-based and sustainable primer solutions is solely to promote new opportunities for the growth of Europe primer market. Consumers and industries are increasingly seeking environmentally friendly alternatives to traditional petroleum-based products. According to the European Bioplastics Association, the production capacity for bio based plastics in Europe is expanding rapidly driven by demand for sustainable materials. This trend extends to primers where bio based resins derived from renewable resources such as vegetable oils and plant sugars are gaining traction. As per the survey, the Circular Economy Action Plan promotes the use of sustainable products and materials in construction and manufacturing. Companies that innovate in this space can differentiate themselves and capture market share among eco conscious buyers. Bio based primers often offer comparable performance to conventional products while reducing carbon footprint and dependency on fossil fuels. Regulatory incentives for green products further support this transition. Partnerships with agricultural suppliers and biotechnology firms facilitate the sourcing of raw materials. The introduction of certifications for bio based content enhances consumer trust and market acceptance. Additionally the development of self priming coatings that combine primer and topcoat functions reduces material usage and application time.

Integration of Smart and Functional Primer Technologies

The integration of smart and functional primer technologies is likely to impact positively on the growth of Europe primer market. These advanced primers provide additional benefits beyond adhesion and corrosion protection such as self healing sensing or anti microbial capabilities. According to the study, self healing coatings can automatically repair micro cracks extending the lifespan of protected structures. Smart primers can monitor structural health by changing color in response to stress or corrosion providing early warning signals for maintenance. As per the European Innovation Partnership on Smart Cities and Communities, the deployment of intelligent infrastructure is a priority for many European cities driving demand for innovative materials. Anti microbial primers are also gaining popularity in healthcare and food processing facilities due to hygiene concerns. The aerospace and marine sectors utilize functional primers to reduce drag and improve fuel efficiency. Research and development investments in nanotechnology enable the creation of primers with precise molecular structures for enhanced performance. Collaborations between material scientists and end users accelerate the commercialization of these technologies. The ability to offer customized solutions for specific challenges allows manufacturers to command premium prices.

MARKET CHALLENGES

Intense Competition from Low Cost Imports

The intense competition from low cost imports is posing as a major challenge for the growth of Europe primer market. Manufacturers in Asia and other regions often benefit from lower labor and raw material costs allowing them to offer products at competitive prices. According to the World Trade Organization, global trade in chemical products has increased with emerging markets becoming significant exporters. European manufacturers must contend with these price advantages, while adhering to stricter environmental and safety regulations that increase production costs. The presence of counterfeit or substandard products in the market further exacerbates the challenge undermining brand reputation and consumer trust. Small and medium sized enterprises are particularly vulnerable to this competition as they lack the economies of scale to absorb cost disparities. The fragmentation of the European market with varying national preferences and standards complicates efforts to achieve uniform pricing and distribution strategies. Additionally, the appreciation of the euro against other currencies can make European exports less competitive and imports more attractive. However, this strategy requires continuous investment in research and development which may be constrained by margin pressures. The influx of affordable alternatives limits the pricing power of European manufacturers and restricts market share growth.

Complexity of Application and Surface Preparation Requirements

The complexity of application and surface preparation is additionally declining the growth of Europe primer market. Proper primer performance is heavily dependent on thorough surface cleaning and profiling which can be labor intensive and costly. According to the European Federation of Corrosion, inadequate surface preparation is cited as the primary cause of coating failure in industrial applications. As per the International Organization for Standardization, strict guidelines such as ISO 8501 define surface cleanliness standards that must be met before primer application. Achieving these standards often requires specialized equipment and skilled labor, which may not be readily available in all regions. The variability of substrate conditions in renovation projects further complicates the selection and application of appropriate primers. Moisture content temperature and humidity levels must be carefully monitored to ensure proper curing and adhesion. Failure to adhere to these protocols can result in premature coating failure leading to costly repairs and reputational damage for contractors. Consumer awareness about proper surface preparation remains low in the DIY segment leading to improper handling and unsatisfactory results. Regulatory uncertainty regarding future waste management requirements for surface preparation debris creates risks for long term planning. Companies must invest in educational programs and user friendly products to mitigate these challenges. However, the high costs associated with training and compliance constrain profitability and hinder the adoption of advanced primer technologies in certain sectors.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Material, Application, End-Use Industry, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Akzo Nobel N.V., PPG Industries, Inc., Sherwin-Williams Company, BASF SE, Axalta Coating Systems Ltd., Jotun Group, Hempel A/S, Kansai Paint Co., Ltd., Nippon Paint Holdings Co., Ltd., DAW SE, Tikkurila Oyj, Asian Paints Limited |

SEGMENTAL ANALYSIS

By Material Insights

The epoxy resins segment was the largest by holding 42.3% of the Europe primer market share in 2025 with the exceptional adhesion chemical resistance and durability that epoxy based primers provide to various substrates particularly metal and concrete. According to the European Federation of Corrosion, the annual cost of corrosion in Europe is estimated at over 100 billion euros prompting industries to invest in high performance protective coatings like epoxy primers. As per the study, epoxy resins are favored for their ability to form strong cross-linked networks that resist moisture and chemicals ensuring long term asset protection. The construction sector also contributes significantly to demand with epoxy primers used to seal concrete floors and prepare surfaces for heavy duty coatings. The versatility of epoxy formulations allows them to be tailored for specific environmental conditions, such as high humidity or temperature fluctuations. Additionally, the automotive industry utilizes epoxy primers for cathodic electrocoating providing uniform coverage and superior rust prevention for vehicle bodies. The established manufacturing infrastructure for epoxy resins in Europe ensures consistent supply and quality.

The biocides segment is projected to witness a fastest CAGR of 6.5% from 2026 to 2034 with the increasing regulatory focus on hygiene and the prevention of microbial growth in coatings. The heightened awareness of indoor air quality and health safety following recent global health crises. According to the study, the approval and use of biocidal active substances are strictly monitored ensuring that only safe and effective products enter the market. As per the survey, healthcare associated infections remain a significant concern driving hospitals and clinics to adopt antimicrobial surface treatments including primers. The construction industry is also integrating biocides into primers to prevent mold and algae growth on exterior facades particularly in humid climates. As per the European Environment Agency, climate change is expected to increase humidity levels in certain regions exacerbating microbial risks on building surfaces. Innovations in nano silver and organic biocide technologies offer enhanced efficacy with lower environmental impact. Regulatory incentives for sustainable and healthy building materials further support the adoption of biocide infused primers. The expansion of the food and beverage industry in Europe also drives demand for hygienic coating solutions.

By Applications Insights

The metal application segment was the largest by holding 48.3% of the Europe primer market share in 2025 with the need for corrosion protection in automotive industrial machinery and infrastructure sectors. According to the European Automobile Manufacturers Association, passenger car production in the EU reached 10.5 million units in 2023 each requiring multiple layers of primer for durability. Industrial facilities also rely heavily on metal primers for maintaining equipment and structures exposed to harsh chemicals and weather conditions. The maritime sector contributes significantly to demand with ships and offshore platforms requiring robust anti corrosive primers. Epoxy and zinc rich primers are preferred for their superior barrier properties and cathodic protection capabilities. The aging infrastructure in Europe necessitates regular maintenance and repainting of metal bridges and pipelines further sustaining demand. Regulatory standards such as ISO 12944 specify rigorous requirements for protective paint systems on steel structures driving the adoption of high-quality metal primers.

The plastic application segment is expected to exhibit a fastest CAGR of 7.2% from 2026 to 2034 with the increasing use of plastics in automotive and consumer electronics industries. The automotive industry’s shift towards lightweight materials to improve fuel efficiency and reduce emissions is fuelling the growth of the segment. As per Plastics Europe, the production of plastics in Europe remains robust with significant volumes used in packaging and electronics that often require decorative or functional coatings. Consumer electronics manufacturers utilize plastic primers to achieve high gloss finishes and durable surfaces for devices such as smartphones and laptops. Innovations in flame retardant and conductive primers also open new application areas in electrical components. The development of water borne plastic primers aligns with environmental regulations reducing volatile organic compound emissions. The versatility of plastics in design and manufacturing drives continuous innovation in primer formulations to meet diverse aesthetic and performance requirements.

By End-Use Industry Insights

The building and construction segment was the largest by holding 50.3% of the Europe primer market share in 2025 with the extensive use of primers in residential commercial and infrastructure projects for surface preparation and protection. The European Union’s Renovation Wave strategy aims to improve the energy efficiency of buildings. According to the European Commission, over 75% of the building stock in the EU is energy inefficient creating a vast market for renovation activities that include priming and painting. As per Eurostat, the construction sector accounts for 9% of the EU gross domestic product indicating its significant economic impact and material consumption. Primers are essential for ensuring the adhesion and durability of exterior and interior coatings on concrete wood and metal surfaces. The restoration of historical buildings also requires specialized primers to preserve architectural integrity. Public infrastructure projects such as bridges and tunnels further drive demand for high performance protective primers. The growing trend towards sustainable construction encourages the use of low volatile organic compound and bio based primers. Regulatory frameworks promoting green building certifications support the adoption of environmentally friendly primer solutions.

The automotive segment is projected to fastest CAGR of 5.8% from 2026 to 2034 with the recovery of vehicle production and the transition to electric mobility. The increasing production of electric vehicles, which require specialized primers for battery enclosures and lightweight components. According to the European Automobile Manufacturers Association, electric vehicle sales in Europe are growing rapidly requiring new coating technologies to meet performance and safety standards. As per the International Energy Agency, the push for lighter vehicles to improve energy efficiency has increased the use of high performance primers on aluminum and composite materials. Automotive original equipment manufacturers are adopting multi-layer coating systems that offer superior durability and scratch resistance. The demand for customized colors and effects also drives innovation in automotive refinish primers. The average age of vehicles on European roads is increasing leading to higher demand for repair and maintenance primers in the aftermarket sector. Regulatory pressures to reduce emissions from coating processes have accelerated the adoption of water borne and powder primer technologies in automotive plants.

COUNTRY LEVEL ANALYSIS

Germany Primer Market Analysis

Germany was the top performer in the Europe primer market by accounting 22.4% of the share in 2025 with its robust automotive and industrial sectors. The presence of major automotive manufacturers, who require advanced primer solutions for vehicle production is also driving the growth of the market in this country. According to the German Federal Ministry for Economic Affairs and Climate Action, the automotive sector is investing heavily in electric vehicle production which increases demand for specialized protective primers. As per the German Paint and Printing Ink Industry Association the shift towards water borne and powder primers is accelerating due to strict environmental regulations. The industrial sector in Germany also contributes significantly to demand with ongoing maintenance projects for machinery and infrastructure. The Energiewende policy promotes sustainable building practices encouraging the use of low volatile organic compound primers. Germany’s strong industrial base supports the production and consumption of high quality primers for diverse applications. The country’s focus on innovation drives the development of smart and functional primers. Regulatory frameworks, such as the Technical Instructions on Air Quality Control enforce stringent emission limits fostering the adoption of cleaner technologies.

France Primer Market Analysis

France ranks as the second largest market for primers in Europe with an approximate share of 14% in 2023 influenced by its strong construction sector and aesthetic preferences. The French government’s MaPrimeRenov scheme, which provides financial incentives for energy efficient home improvements, including exterior insulation and painting. As per the French Paint Industry Federation, there is a growing preference for eco labeled primers that meet strict environmental and health standards. The French consumers place high value on aesthetics leading to demand for premium finishes and custom colors. The tourism industry contributes to market growth through the maintenance and renovation of hotels and historic buildings. Regulatory initiatives such as the Anti Waste Law for a Circular Economy promote the use of sustainable packaging and recyclable materials in the paint industry. France’s commitment to reducing carbon emissions drives the adoption of low volatile organic compound formulations.

Italy Primer Market Analysis

Italy primer market held second position by holding 11.3% of share in 2025 with its vibrant construction and furniture industries. The Superbonus tax credit scheme, which although modified has stimulated extensive renovation activities, including facade painting and insulation. According to the Italian National Institute of Statistics, the construction sector has shown resilience with significant activity in the residential renovation segment. Italian manufacturers are known for their innovation in color trends and texture effects appealing to discerning consumers. The tourism sector also contributes to demand through the maintenance of hospitality facilities and historic sites. Regulatory efforts to improve energy efficiency in buildings support the use of reflective and insulating primers.

United Kingdom Primer Market Analysis

The United Kingdom primer market growth is likely to grow with steady demand for architectural primers driven by home improvement trends and rental property maintenance. The UK government’s commitment to improving energy efficiency in homes, which often involves exterior repainting and insulation upgrades. According to the Office for National Statistics, the housing sector remains active with significant spending on repairs and improvements. As per the British Coatings Federation, there is a growing trend towards sustainable and low odor primers among consumers concerned about indoor air quality. The automotive and aerospace industries in the UK also contribute to demand for high performance industrial primers. Regulatory standards, such as the Control of Volatile Organic Compounds in Paints Regulations enforce limits on solvent content driving the adoption of water borne technologies.

Spain Primer Market Analysis

Spain primer market growth is likely to have prominent growth opportunities in coming years with significant demand for exterior primers due to the country’s warm climate and exposure to sunlight. The renovation of tourist accommodations and residential properties, which requires durable and weather resistant primers is also fuelling the growth of market. According to the Spanish National Statistics Institute, the construction sector has recovered strongly with increased investment in housing and hospitality projects. As per the study, there is a high demand for anti-algae and UV resistant primers that protect buildings from harsh environmental conditions. The automotive industry in Spain is also a major consumer of primers with several large manufacturing plants operating in the country. Spanish consumers prefer bright and vibrant colors influencing product development and marketing strategies. Government initiatives to improve energy efficiency in buildings support the use of thermal insulation primers.

COMPETITIVE LANDSCAPE

The competition in the Europe primer market is characterized by the presence of established multinational corporations and specialized regional producers. Market leaders compete on the basis of product quality innovation and sustainability credentials. The high regulatory barriers related to environmental compliance create significant advantages for companies with advanced research and development capabilities. Competitive dynamics are influenced by raw material costs and energy prices which impact production expenses. Companies differentiate themselves through eco friendly formulations and digital customer services. Price competition is moderate as customers prioritize performance and environmental standards over lowest cost. Strategic alliances with construction and automotive industries strengthen market positions and ensure stable demand. The shift towards sustainable building and transportation drives innovation and collaboration among market participants. Regulatory frameworks play a crucial role in shaping competitive landscapes by setting standards for emissions and waste. Companies that adapt quickly to changing regulations and consumer preferences gain a competitive advantage.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global Europe Primer Market include

- Akzo Nobel N.V.

- PPG Industries, Inc.

- Sherwin-Williams Company

- BASF SE

- Axalta Coating Systems Ltd.

- Jotun Group

- Hempel A/S

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- DAW SE

- Tikkurila Oyj

- Asian Paints Limited

TOP LEADING PLAYERS IN THE MARKET

- AkzoNobel is a global leader in paints and coatings with a significant presence in the Europe primer market through its decorative and performance coatings divisions. The company offers a wide range of primers for architectural automotive and industrial applications emphasizing sustainability and innovation. Recent actions include expanding its portfolio of low volatile organic compound and bio based primers to meet stringent environmental regulations. AkzoNobel invests heavily in research and development to create advanced formulations that enhance adhesion and corrosion resistance. The company strengthens its market position by collaborating with construction and automotive partners to develop customized solutions. Their commitment to circular economy principles drives the introduction of recyclable packaging and efficient application technologies. AkzoNobel’s strategic focus on digitalization improves customer engagement and supply chain efficiency ensuring reliable product availability across European markets.

- PPG Industries is a major player in the Europe primer market providing high performance coating solutions for automotive aerospace and industrial sectors. The company leverages its global expertise to deliver innovative primer technologies that ensure superior surface preparation and protection. Recent strategies involve increasing production capacity for water borne and powder primers to align with sustainability goals. PPG invests in advanced manufacturing processes to reduce energy consumption and waste generation. The company collaborates with original equipment manufacturers to develop lightweight and durable primer systems for electric vehicles. PPG’s focus on digital tools enhances customer service and technical support strengthening relationships with key clients. Their extensive distribution network ensures timely delivery of high quality primer products to diverse industries.

- BASF SE is a leading chemical company that significantly influences the Europe primer market through its raw material supply and proprietary coating formulations. The company provides essential resins additives and pigments that enable the production of high-performance primers. Recent actions include expanding its portfolio of sustainable raw materials such as bio-based solvents and recycled polymers for primer formulations. BASF invests in research and development to create innovative solutions that improve primer efficiency and environmental profile. The company collaborates with formulators and manufacturers to develop next generation primers for various applications including automotive and construction. BASF’s commitment to sustainability drives the adoption of circular economy practices within the industry. Their strategic partnerships and technical expertise strengthen their market position.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe primer market primarily focus on sustainability and innovation to address environmental concerns and regulatory requirements. Companies invest in developing low volatile organic compound and bio-based primers to meet strict emission standards. Strategic acquisitions and partnerships expand product portfolios and geographic reach. Digitalization of supply chains enhances operational efficiency and customer engagement. Manufacturers prioritize research and development to create high performance primers for emerging applications such as electric vehicles and smart buildings. Compliance with environmental regulations is maintained through continuous improvement in production processes. Companies also engage in consumer education to promote the benefits of sustainable primers. These strategies enable participants to maintain competitiveness and achieve long term growth in the European region.

MARKET SEGMENTATION

This research report on the europe primer market is segmented and sub-segmented into the following categories.

By Material

- Epoxy Resins

- Acrylic Resins

- Polyurethane

- Biocides

- Alkyd

- Other Materials

By Application

- Metal

- Concrete

- Wood

- Plastic

- Other Substrates

By End-Use Industry

- Building & Construction

- Automotive

- Industrial Machinery

- Marine

- Aerospace

- Other End-Use Industries

By Country

- Germany

- France

- Italy

- United Kingdom

- Spain

- Rest of Europe

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com