Europe Psilocybin Market Size, Share, Trends & Growth Forecast Report Segmented By Application (Depression, Anxiety, Post-Traumatic Stress Disorder, Substance Abuse, Obsessive-Compulsive Disorder), Formulation, Therapeutic Setting, Patient Demographics, And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe), Industry Analysis From 2026 To 2034

Europe Psilocybin Market Size

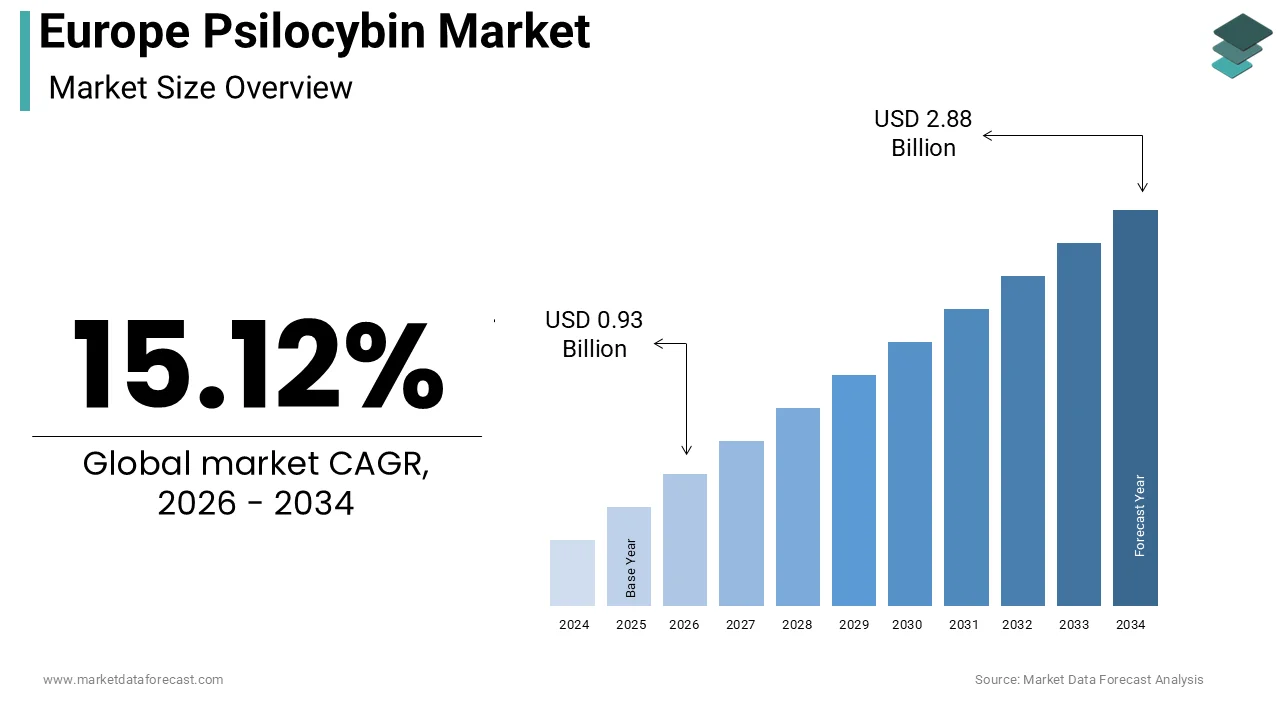

The Europe psilocybin market size was calculated to be USD 0.81 billion in 2025 and is anticipated to be worth USD 2.88 billion by 2034, from USD 0.93 billion in 2026, growing at a CAGR of 15.12% during the forecast period.

Psilocybin is a naturally occurring psychedelic compound produced by more than 200 species of fungi, commonly known as "magic mushrooms" or "shrooms". This market is currently transitioning from a prohibited substance framework toward a regulated medical paradigm, driven by rigorous clinical investigations into its efficacy for treating severe mental health disorders such as treatment-resistant depression and end-of-life anxiety. The European landscape is characterized by a complex patchwork of national regulations, yet a unified scientific momentum is building across the continent. According to the WHO Regional Office for Europe, mental health conditions affect a substantial portion of the population, with conditions like anxiety and depression seeing a notable surge following recent global crises. This has created a critical demand for integrated care systems that go beyond traditional pharmaceutical treatments to include social and community-based support. Furthermore, the European Medicines Agency has begun engaging with sponsors regarding the regulatory pathways for psychedelic-assisted psychotherapy, signaling a shift in official oversight. Eurostat data identifies intentional self-harm as a primary driver of mortality among young and middle-aged adults. The high impact of these deaths, particularly among men in their twenties, underscores the urgent need for early intervention and breakthrough prevention strategies tailored to the unique stressors of modern life. The European Commission has adopted a comprehensive approach to mental health, prioritizing the development of novel digital tools and cross-border research consortia. These initiatives aim to address the severe shortage of specialized professionals by leveraging technology to complement face-to-face clinical interactions. The region hosts numerous academic institutions, including Imperial College London and University Hospital Zurich, which are pioneering randomized controlled trials. This convergence of high unmet medical needs, evolving regulatory dialogues, and robust academic research defines the nascent but rapidly evolving operational environment for the psilocybin industry in Europe.

MARKET DRIVERS

Escalating Prevalence of Treatment-Resistant Mental Health Disorders

The alarming rise in treatment-resistant depression and other refractory psychiatric conditions is the primary factor propelling the Europe psilocybin market. These are conditions that fail to respond to conventional antidepressants and cognitive behavioral therapies. Current standard-of-care antidepressant medications often require weeks to exhibit effects and demonstrate significant non-response rates, leaving a large portion of patients without effective relief. According to the World Health Organization, depression is a leading cause of disability in Europe, affecting a vast number of people, with a significant subset classified as treatment-resistant. Clinical data emerging from European centers suggests that psilocybin-assisted therapy can induce rapid and sustained remission in these difficult-to-treat populations, often after just one or two sessions. The European Psychiatry Association has noted a growing consensus among clinicians regarding the limitations of existing monoaminergic drugs, fostering openness to investigating serotonergic psychedelics. Furthermore, the economic burden of mental illness in the European Union is estimated to be over six hundred billion Euros annually, prompting healthcare systems to seek more efficient interventions rather than relying solely on long-term maintenance therapies. This desperate clinical need for mechanisms that offer rapid neuroplasticity and symptom relief drives intense investment and research activity, positioning psilocybin as a potential paradigm shift in psychiatric care.

Robust Academic Research Infrastructure and Public Funding Support

The presence of world-class academic research institutions and increasing public funding dedicated to exploring the therapeutic potential of psychedelics within the region further drives the growth of the Europe psilocybin market. Unlike other regions where research may be primarily industry-led, Europe boasts a strong tradition of publicly funded neuroscience research that lends significant credibility to psilocybin studies. As per the European Commission, the Horizon Europe program has allocated substantial grants to consortia investigating novel mental health treatments, including several projects focused on psychedelic compounds and their mechanisms of action. Institutions such as the University of Zurich and King's College London are conducting landmark Phase 2 and Phase 3 trials that adhere to rigorous Good Clinical Practice standards, generating high-quality data essential for regulatory approval. The European Research Council continues to support basic science inquiries into how psilocybin affects brain connectivity and neuroplasticity, providing the foundational knowledge required for drug development. Additionally, the establishment of dedicated centers for psychedelic research, such as the Centre for Psychedelic Research at Imperial College London, creates hubs of expertise that attract global talent and investment. This strong academic backbone not only validates the scientific premise of psilocybin therapy but also accelerates the translation of laboratory findings into clinical applications, fueling market growth.

MARKET RESTRAINTS

Stringent Regulatory Classification and Legal Prohibitions

The strict classification of psilocybin as a Schedule I controlled substance is the biggest restraint for the European psilocybin market. This regulation, spanning international and national laws, severely limits research and commercial activities. Under the United Nations Single Convention on Narcotic Drugs, which binds European nations, psilocybin is categorized as having no accepted medical use and a high potential for abuse, creating formidable legal barriers to cultivation, possession, and administration. Researchers must navigate a labyrinthine process of obtaining special licenses from national health ministries and drug enforcement agencies, a procedure that can delay study initiation by months or even years. The European Medicines Agency requires extensive safety data before considering any approval, yet the current legal status makes gathering this data exceptionally difficult and costly. This regulatory rigidity stifles innovation, deters private investment due to legal uncertainty, and prevents the establishment of standardized manufacturing protocols, thereby slowing the overall maturation of the market.

Social Stigma and Historical Association with Recreational Drug Use

The pervasive social stigma and negative public perception associated with psilocybin also impede the expansion of the Europe psilocybin market. This is rooted in its historical classification as a hallucinogenic drug of abuse rather than a legitimate medicine. Decades of prohibitionist rhetoric and cultural associations with the counterculture movements of the 1960s have created deep-seated skepticism among policymakers, healthcare providers, and the general public regarding the safety and validity of psychedelic therapies. As per a survey, a significant majority of citizens in several European countries still view all psychedelic substances as dangerous and lacking therapeutic value, which influences political will and funding priorities. This stigma manifests in hesitancy among physicians to prescribe or recommend such treatments and reluctance among insurance providers to cover them, even if approved. The fear of reputational damage causes many pharmaceutical companies to approach the sector with extreme caution, limiting the capital influx necessary for large-scale development. Furthermore, patient recruitment for clinical trials can be hampered by fears of being labeled as drug users, despite the medical context. Overcoming this deeply ingrained cultural barrier requires extensive education and advocacy efforts, which slow the acceptance and integration of psilocybin into mainstream healthcare systems.

MARKET OPPORTUNITIES

Development of Proprietary Synthetic Analogs and Novel Formulations

Developing proprietary synthetic analogs of psilocybin and novel formulations offers a lucrative avenue for the Europe psilocybin market expansion. This approach allows companies to secure intellectual property rights while circumventing natural variability. Natural psilocybin derived from fungi faces challenges related to batch consistency and patentability, whereas synthetic variants can be chemically modified to optimize pharmacokinetics, reduce side effects, and shorten the duration of the psychedelic experience. Companies are exploring prodrugs that offer improved bioavailability or formulations such as rapid-dissolve tablets and intravenous solutions that provide precise dosing control essential for clinical settings. These innovations enable the creation of "designer" psychedelics that retain therapeutic efficacy while offering commercial advantages through exclusivity. Furthermore, the ability to tailor the duration of action allows for more flexible therapy sessions, potentially reducing the resource intensity of treatment delivery. Market participants can establish robust moats against competition by focusing on chemical innovation. This positions them as leaders in the next generation of precision psychiatry medicines.

Integration into Digital Therapeutics and Hybrid Care Models

The integration of psilocybin therapy with digital therapeutics and hybrid care models opens the door to scale treatment delivery and enhance patient outcomes across the region's diverse healthcare landscape, which is expected to boost the expansion of the Europe psilocybin market. Traditional psychedelic-assisted psychotherapy is resource-intensive, requiring hours of therapist time, but digital platforms can facilitate preparation, monitoring, and integration phases remotely, making the therapy more accessible and cost-effective. Startups are developing virtual reality environments to guide patients through the psychedelic experience and AI-driven algorithms to analyze session data for personalized insights. This technological synergy allows for the standardization of therapeutic protocols and the potential for remote supervision by clinicians, addressing the shortage of trained therapists. Additionally, digital platforms can collect real-world evidence at scale, further validating efficacy and supporting reimbursement negotiations. Companies can leverage Europe's advanced digital infrastructure to create scalable business models. These models will democratize access to digital health services, unlocking a massive addressable market.

MARKET CHALLENGES

Critical Shortage of Trained Therapists and Standardized Protocols

The acute shortage of qualified therapists trained in psychedelic-assisted psychotherapy obstructs the growth of the Europe psilocybin market. Furthermore, this is compounded by a lack of universally standardized treatment protocols. Effective psilocybin therapy relies heavily on the "set and setting," requiring skilled professionals to guide patients through intense psychological experiences, yet current training programs are limited in capacity and scope. As per sources, there is currently no unified certification framework for psychedelic therapists across the EU, leading to inconsistencies in care quality and safety standards. The intensive nature of the therapy, which often involves multiple hours of preparation, dosing, and integration per patient, creates a bottleneck that limits the number of individuals who can be treated simultaneously. Without a scalable workforce, the commercial viability of psilocybin clinics remains constrained, regardless of regulatory approval. Furthermore, the absence of consensus on dosing regimens, music selection, and therapeutic techniques complicates multi-center clinical trials and hinders regulatory acceptance. Addressing this human capital deficit requires significant investment in educational infrastructure and the development of accredited training curricula, a process that is time-consuming and complex, given the varying national regulations on psychotherapy practice.

Complex Reimbursement Landscapes and Payer Skepticism

Navigating the fragmented and complex reimbursement landscapes across European nations challenges the commercial success of psilocybin therapies and the overall expansion of the Europe psilocybin market. Payers remain skeptical about the cost-effectiveness of high-ticket, one-time interventions. Unlike chronic medications that generate recurring revenue, psilocybin therapy is envisioned as a short-course treatment, which complicates the economic modeling for national health services and private insurers accustomed to traditional payment structures. As per research, health technology assessment bodies in countries like Germany, France, and the UK demand robust long-term data on the durability of response and quality-adjusted life years before agreeing to reimburse novel psychiatric treatments. The high upfront cost of developing and delivering these therapies, combined with the need for specialized facilities and staff, raises concerns about affordability within strained public health budgets. Additionally, the variation in healthcare financing models across Europe means that a therapy approved in one country might face insurmountable reimbursement hurdles in another, fragmenting the market. Convincing payers to cover these innovative treatments requires compelling health economic data that is currently scarce, creating a significant barrier to widespread patient access and market penetration.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 15.12% |

| Segments Covered | By Application, Formulation, Therapeutic Setting, Patient Demographics, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Compass Pathways, atai Life Sciences, MindMed, Cybin Inc., Field Trip Health, GH Research, Small Pharma, Numinus Wellness, Beckley Psytech, MAPS (Multidisciplinary Association for Psychedelic Studies) |

SEGMENTAL ANALYSIS

By Application Insights

The depression segment was the largest segment in the Europe psilocybin market and occupied a 42.7% share in 2025. This position of the segment is attributed to the severe global crisis of treatment-resistant depression and the compelling clinical evidence demonstrating rapid and sustained remission rates following psilocybin-assisted therapy. A top reason for this dominance is the staggering prevalence of major depressive disorder across Europe, particularly the subset of patients who fail to respond to multiple lines of conventional antidepressants, creating a desperate demand for novel mechanisms of action. Traditional therapies often require weeks to months to show efficacy and carry significant side effect burdens, whereas early-phase clinical trials conducted at institutions like Imperial College London have shown that psilocybin can produce rapid antidepressant effects within hours or days. The European Psychiatry Association has increasingly recognized the limitations of monoaminergic drugs, fostering a clinical environment ripe for psychedelic interventions. The sheer volume of suffering individuals, combined with the economic burden of depression, drives intense research focus and investment into this specific indication, securing its leading market position. An additional factor is the advanced stage of clinical development for psilocybin in treating depression compared to other indications, with numerous Phase 2 and Phase 3 trials actively recruiting patients across major European hubs. The regulatory pathway for depression is becoming clearer as agencies like the European Medicines Agency engage in scientific advice procedures with sponsors developing psilocybin formulations specifically for this condition. Landmark studies published in prestigious journals have demonstrated that a single dose of psilocybin combined with psychological support can lead to remission in a notable share of patients with treatment-resistant depression, providing a strong evidence base for future approval. Furthermore, patient advocacy groups across Germany, France, and the UK are lobbying aggressively for access to these therapies, creating political pressure to accelerate approvals. The convergence of robust data, advanced trial stages, and strong stakeholder support ensures that depression remains the cornerstone of the European psilocybin market.

The Post-Traumatic Stress Disorder (PTSD) segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 18.5% during the forecast period due to rising awareness of trauma-related disorders among veterans and civilians, coupled with emerging data suggesting psilocybin's unique ability to facilitate emotional processing and memory reconsolidation. Also, the rapid expansion of the PTSD segment is driven by the increasing recognition of trauma prevalence across Europe, particularly among military veterans, refugees, and survivors of violence, who often suffer from chronic symptoms unresponsive to traditional therapies. Current treatments, such as selective serotonin reuptake inhibitors and exposure therapy, have limited success rates, with a portion of patients failing to achieve meaningful improvement, creating a vast unmet need. Preliminary research suggests that psilocybin can help patients process traumatic memories without the overwhelming fear response, offering a potential breakthrough for this difficult-to-treat population. Governments across Europe are increasingly prioritizing veteran mental health, with initiatives in the UK and Germany specifically funding research into alternative therapies for PTSD. The urgent societal need to address the long-term impacts of trauma on individuals and communities is propelling significant investment and clinical interest, driving the fastest growth in this application sector. A further key driver is the unique mechanistic profile of psilocybin, which appears to enhance neuroplasticity and facilitate the reconsolidation of traumatic memories, offering a biological advantage over existing pharmacological options. Unlike standard anxiolytics that may suppress symptoms, psilocybin promotes a state of heightened brain connectivity that allows patients to revisit and reframe traumatic experiences in a therapeutic setting. The scientific validation is attracting substantial venture capital and pharmaceutical interest, with several biotech companies launching dedicated programs to investigate psilocybin for trauma-related disorders. The European Research Council has also granted funding to explore the neural mechanisms underlying psychedelic-assisted psychotherapy for PTSD, further legitimizing the field. The promise of a curative rather than palliative approach to trauma, supported by growing mechanistic evidence, is accelerating the adoption of psilocybin for PTSD, making it the fastest-growing application segment.

By Formulation Insights

The Capsule segment held the majority share of 45.6% of the Europe psilocybin market in 2025. This supremacy of the segment is driven by the precision dosing capabilities, ease of administration, and alignment with current clinical trial protocols that favor solid oral dosage forms for standardized delivery. A main contributor to the prevalence of capsules is the critical need for exact dosing in clinical research and future therapeutic applications, where variability in drug absorption can significantly impact safety and efficacy outcomes. Psilocybin derived from natural mushrooms varies widely in potency, making synthetic psilocybin encapsulated in precise milligram amounts the gold standard for scientific rigor. As per the European Medicines Agency guidelines on clinical trial management, strict control over dosage uniformity is mandatory for regulatory approval, and capsules offer the most reliable method to ensure each patient receives the intended amount of active ingredient. Most landmark studies conducted in Europe, including those at King's College London, utilize gelatin or vegetarian capsules to administer psilocybin, establishing this format as the benchmark for data generation. The familiarity of capsules to both clinicians and patients reduces administration errors and simplifies logistics in hospital and clinic settings. Furthermore, capsules protect the compound from degradation due to light and moisture, ensuring stability during storage and transport. This combination of scientific necessity, regulatory compliance, and operational convenience secures the leading position of the capsule segment. Key to this segment is also the high level of patient compliance and psychological acceptability associated with capsule ingestion, which mimics the familiar experience of taking conventional medication and reduces anxiety related to the treatment process. For many patients, especially those unfamiliar with psychedelics, swallowing a pill feels more medicalized and controlled than consuming raw mushrooms or liquids, helping to establish a therapeutic "set and setting" conducive to positive outcomes. The psychological framing is crucial in minimizing pre-dose anxiety, which can otherwise interfere with the therapeutic journey. Additionally, capsules are tasteless and odorless, avoiding the potentially unpleasant sensory experience of consuming fungal material, which can be a barrier for some individuals. The ease of integration into standard pharmacy dispensing systems also facilitates future commercial distribution. The capsule format aligns with patient preferences and existing healthcare workflows. As a result, it maintains its dominance in the market.

The Liquid segment is expected to exhibit a noteworthy CAGR of 16.8% from 2026 to 2034, owing to the advantages of rapid onset of action, flexible titration capabilities, and the development of novel intravenous and sublingual formulations for acute care settings. The swift expansion of the liquid segment is largely fueled by the pharmacokinetic advantage of liquid formulations, which allow for faster absorption and quicker onset of effects compared to solid oral dosage forms, a critical factor in controlled clinical environments. In therapeutic settings, the ability to titrate the dose in real-time based on patient response is invaluable, allowing clinicians to adjust the intensity of the experience to ensure safety and optimize therapeutic benefit. As per pharmacological studies, liquid psilocybin administered sublingually or intravenously can reach peak plasma concentrations significantly faster than capsules, enabling more precise control over the duration and depth of the psychedelic state. This flexibility is particularly important for patients with varying metabolic rates or those who may have difficulty swallowing pills. Furthermore, liquid formulations facilitate the development of microdosing regimens where precise small volumes are required, expanding the potential user base beyond macrodose therapy. The adaptability of liquids to different routes of administration, including nasal sprays currently under investigation, adds to their versatility. These clinical advantages make liquid formulations increasingly attractive for next-generation therapeutic protocols, driving their rapid adoption. A further point supporting this segment is the aggressive innovation in intravenous and other novel liquid delivery systems by biotechnology companies seeking to differentiate their products and secure intellectual property rights. Several European and global firms are developing sterile injectable psilocybin solutions designed for hospital use, aiming to bypass first-pass metabolism and achieve 100 percent bioavailability. Intravenous administration allows for an extremely predictable pharmacokinetic profile, which is highly desirable for regulatory approval and insurance reimbursement. Additionally, liquid formats enable the creation of ready-to-use kits for emergency psychiatric care or rapid intervention scenarios, broadening the scope of application beyond scheduled therapy sessions. The potential for combining liquid psilocybin with other intravenous medications in a hospital setting also opens new therapeutic avenues. This wave of technological advancement and the pursuit of proprietary delivery mechanisms are propelling the liquid segment to become the fastest-growing category in the market.

By Therapeutic Setting Insights

The Outpatient segment dominated the Europe psilocybin market and captured a 55.8% share in 2025. This prominence of the segment is supported by the cost-effectiveness of ambulatory care, the structure of current clinical trials, and the preference for treating patients in less restrictive environments that promote autonomy. The main reason behind the dominance of the outpatient setting is the compelling economic argument for delivering psilocybin therapy outside of expensive inpatient facilities, which aligns with the budget constraints of European national health services. Inpatient care involves high overhead costs for room, board, and 24-hour nursing, whereas outpatient clinics can deliver the same therapeutic protocol with a fraction of the resources, making the treatment more scalable and affordable. As per sources, healthcare payers across the EU are increasingly prioritizing ambulatory care models to reduce hospital congestion and lower overall expenditure, a trend that strongly favors outpatient psychedelic therapy. Current clinical trials are predominantly designed as day-case procedures where patients arrive, undergo the session, and return home after monitoring, establishing a precedent for future commercial delivery. The typical psilocybin session lasts 6 to 8 hours, fitting comfortably within a standard clinic operating day without requiring overnight stays. This efficiency allows for higher patient throughput and lower per-patient costs, which is essential for achieving widespread accessibility and securing reimbursement. The economic viability of the outpatient model ensures its position as the primary setting for psilocybin administration. This segment is also built up by the therapeutic advantage of administering psilocybin in a comfortable, non-clinical outpatient environment that fosters a sense of safety and openness, which is crucial for the psychological work involved. The "set and setting" principle dictates that the physical environment profoundly influences the patient's experience, and outpatient clinics are often designed to resemble living rooms rather than hospital wards to reduce anxiety and encourage introspection. As per guidelines from the European Federation of Psychologists' Associations, a relaxed and homelike atmosphere is recommended to facilitate the deep emotional processing required for successful outcomes, something that sterile inpatient units may struggle to provide. Patients often feel more empowered and less stigmatized when visiting a community clinic compared to being admitted to a psychiatric ward, improving recruitment and retention rates. Furthermore, the ability to return to one's home environment after the session aids in the integration process, allowing patients to immediately apply insights to their daily lives. The alignment of the outpatient setting with best practices for psychedelic therapy and patient preferences solidifies its leading market share.

The residential treatment segment is predicted to witness the highest CAGR of 19.2% between 2026 and 2034. This acceleration is driven by the emergence of specialized retreat centers offering immersive multi-day programs, the demand for comprehensive holistic care, and the need for intensive support for severe cases. The rapid growth of the residential treatment segment is primarily fueled by the rise of dedicated wellness retreats and specialized clinics in Europe that offer immersive, multi-day psilocybin experiences integrated with extensive preparatory and integration therapies. These facilities, particularly in countries with more lenient regulations like the Netherlands and Switzerland, provide a contained environment where patients can disconnect from daily stressors and focus entirely on their healing journey. The residential model allows for continuous monitoring and support over several days, enabling deeper therapeutic work that may not be possible in a single-day outpatient visit. This immersive approach appeals to individuals with complex trauma or severe addiction who require a stable and supportive environment for extended periods. The premium nature of these services, often bundled with yoga, meditation, and nutritional counseling, creates a high-value market segment that is expanding rapidly as legal frameworks evolve to accommodate such facilities. Following this, the segment is backed by the necessity for residential care in treating patients with severe comorbidities or high suicide risk who require 24-hour medical supervision and intensive multidisciplinary support. For individuals with profound treatment-resistant depression or co-occurring substance use disorders, the structured environment of a residential facility offers a level of safety and care intensity that outpatient settings cannot match. The ability to manage acute psychological reactions immediately and provide round-the-clock therapeutic integration enhances patient safety and outcomes. Furthermore, insurance providers and public health systems are beginning to recognize the value of intensive residential interventions for reducing long-term healthcare utilization among the most vulnerable populations. The growing acknowledgment of the need for tiered care options, where residential treatment serves the most critical patients, is propelling this segment to the highest growth rate in the market.

By Patient Demographics Insights

The adult segment led the total Europe psilocybin market and accounted for a substantial share in 2025 because of the high prevalence of mental health disorders in the working-age population, the current focus of clinical research on adult cohorts, and regulatory restrictions limiting access for minors. Apart from these, a key factor for this segment is the disproportionately high incidence of depression, anxiety, and substance use disorders among adults aged 18 to 64, who constitute the majority of individuals seeking mental healthcare in Europe. As per studies, mental health conditions are the leading cause of disability among adults in the EU, with millions requiring effective interventions to maintain employment and quality of life. This demographic is also the primary focus of current clinical trials, as regulatory bodies generally require extensive safety data in adults before approving studies involving adolescents or the elderly. The economic impact of untreated mental illness in this group, including lost productivity and healthcare costs, creates a strong imperative for governments and insurers to support innovative treatments like psilocybin therapy. Furthermore, adults are more likely to have the financial means and autonomy to seek out private treatment options or participate in clinical research. The convergence of high disease burden, research focus, and economic urgency ensures that adults remain the largest consumer group for psilocybin therapies. Also helping this market is the stringent regulatory and ethical framework governing clinical research and medical treatment for minors, which currently limits the expansion of psilocybin therapy into younger demographics. European regulations require extensive safeguards and parental consent for pediatric trials, slowing the pace of development for adolescent indications compared to adult studies. As per research, the majority of approved investigational medicinal product dossiers for psychedelics specify adult inclusion criteria exclusively, reflecting a cautious approach to introducing these compounds to developing brains. Ethical concerns regarding the potential impact of psychedelics on cognitive development and emotional maturity further restrict access for children and teenagers. Consequently, the market is naturally skewed towards the adult population, where the risk-benefit profile is better understood and regulatory pathways are more established. The adult segment still commands the vast majority of market activity and revenue. This trend will continue until more robust safety data becomes available for younger age groups.

The veterans segment is estimated to register the fastest CAGR of 21.4% over the forecast period. This surge of the segment is propelled by targeted government initiatives to address the mental health crisis among military personnel, the high prevalence of PTSD in this group, and the specific suitability of psilocybin for trauma processing. The swift growth of the veteran segment is primarily attributed to increasing recognition from European governments of the severe mental health challenges faced by military personnel, leading to dedicated funding and pilot programs for alternative therapies like psilocybin. Countries such as the United Kingdom and Germany have launched specific task forces to explore non-traditional treatments for veterans suffering from combat-related PTSD, acknowledging the failure of conventional approaches for many service members. Pilot schemes funded by state budgets are now underway to evaluate psilocybin-assisted therapy in veteran populations, creating a structured pathway for market entry. The strong political will to support those who have served, combined with the visible societal cost of veteran suicide and homelessness, accelerates the adoption of innovative treatments. This top-down support creates a unique and rapidly expanding niche within the broader psilocybin market. Further boosting this segment is the emerging evidence suggesting that psilocybin is particularly effective in treating combat-related PTSD and moral injury, conditions that are prevalent among veterans and notoriously difficult to treat with standard medications. The unique mechanism of psilocybin, which facilitates the processing of deeply entrenched traumatic memories and fosters a sense of connectedness, addresses the core symptoms of moral injury and isolation often experienced by soldiers. Veteran advocacy groups across Europe are actively campaigning for access to these therapies, amplifying the demand and influencing policy decisions. The specific alignment of psilocybin's therapeutic effects with the unique psychological wounds of warfare makes it a highly sought-after intervention for this demographic. The combination of high unmet need, proven efficacy, and strong advocacy is propelling the veteran segment to become the fastest-growing demographic in the market.

REGIONAL ANALYSIS

United Kingdom Psilocybin Market Analysis

The United Kingdom outperformed other countries in the Europe psilocybin market by capturing a share of 28.8% in 2025. This dominance of the UK market is driven by its pioneering academic research, progressive regulatory engagement, and the presence of world-renowned institutions driving the global psychedelic renaissance. The UK is home to the Centre for Psychedelic Research at Imperial College London, which has conducted some of the most influential clinical trials on psilocybin for depression and end-of-life anxiety, setting the global standard for scientific rigor. As per research, the country has granted multiple licenses for the cultivation and manufacture of psilocybin for research purposes, creating a favorable environment for drug development. The government's Life Sciences Vision strategy explicitly identifies mental health innovation as a priority, fostering collaboration between academia, industry, and the NHS. Furthermore, the presence of numerous biotech startups in the "Golden Triangle" of London, Oxford, and Cambridge has attracted significant venture capital investment into the sector. The British public discourse on psychedelics is also more advanced, with mainstream media coverage reducing stigma and increasing patient awareness. According to sources, the UK receives a disproportionate share of European funding for psychedelic research, cementing its status as the primary hub for innovation and commercialization in the region.

Switzerland Psilocybin Market Analysis

Switzerland followed closely behind in the Europe psilocybin market and accounted for a 18.4% share in 2025. This expansion is attributed to its long history of psychedelic research, flexible regulatory framework for compassionate use, and high-quality clinical infrastructure. The Swiss market is characterized by early access programs and a sophisticated healthcare system willing to integrate novel therapies. Switzerland has a unique regulatory pathway that allows physicians to apply for compassionate use permits to administer psilocybin to patients with severe, treatment-resistant conditions, effectively creating an early market for therapeutic use. The country hosts renowned universities like the University of Zurich, which continues to lead research into the neurobiology of psychedelics, maintaining Switzerland's reputation as a scientific powerhouse. The high purchasing power of the Swiss population and the coverage provided by supplementary health insurance for experimental treatments also support a robust private market. Furthermore, Switzerland's neutrality and stability make it an attractive location for international clinical trials and headquarters for psychedelic biotech firms. According to research, there is growing professional acceptance of psychedelic-assisted therapy, facilitating smoother integration into clinical practice. This blend of regulatory flexibility, scientific excellence, and economic strength sustains Switzerland's leading role.

Germany Psilocybin Market Analysis

Germany holds a noteworthy position in the European market due to its large population, robust pharmaceutical industry, and evolving regulatory landscape that is increasingly open to cannabinoid and psychedelic medicines. The German market is known for a strong emphasis on evidence-based medicine and rigorous clinical validation. As Europe's largest economy, Germany represents a massive addressable market for mental health treatments, with a high prevalence of depression and anxiety creating urgent demand for new solutions. The recent legalization of cannabis for medical and recreational use in Germany has paved the way for a broader acceptance of scheduled substances for therapeutic purposes, signaling a potential shift for psilocybin. The presence of major pharmaceutical companies and a strong biotech sector in cities like Berlin and Munich provides the industrial capacity necessary for scaling production and distribution. Furthermore, the German healthcare system's statutory insurance model offers a clear pathway for future reimbursement once efficacy is proven, attracting significant investor interest. According to studies, professional interest in psychedelic research is surging, with new networks forming to advance the field. This combination of market size, industrial capability, and regulatory evolution positions Germany as a key growth engine.

Netherlands Psilocybin Market Analysis

The Netherlands expanded steadily in the regional market owing to its unique legal status regarding psilocybin truffles, a thriving wellness tourism sector, and a progressive cultural attitude towards psychedelics. The Dutch market serves as a living laboratory for safe consumption and harm reduction practices. Unlike most other European nations, the Netherlands permits the sale of psilocybin-containing truffles through licensed "smart shops," creating a unique quasi-legal market that generates revenue and normalizes usage under regulated conditions. The country attracts thousands of medical tourists annually seeking guided psilocybin experiences, contributing significantly to the local economy and fostering a wealth of practical knowledge on set and setting. This existing infrastructure provides a solid foundation for the transition to fully medicalized models as clinical evidence accumulates. Furthermore, Dutch research institutions like Maastricht University are actively engaged in studying the effects of microdosing and macrodosing, contributing valuable data to the global scientific community. According to a source, the Netherlands leads Europe in harm reduction strategies related to psychedelics, enhancing public safety and acceptance. This unique legal and cultural environment gives the Netherlands a distinct and influential position in the market.

Denmark Psilocybin Market Analysis

Denmark is predicted to grow notably in the regional market from 2026 to 2034 due to its progressive social welfare model, strong commitment to mental health innovation, and emerging biotech cluster focused on neuroscience. The Danish market is notable for its holistic approach to healthcare and willingness to pilot new treatments. Denmark's comprehensive public healthcare system places a high priority on mental well-being, creating a supportive environment for the introduction of breakthrough therapies like psilocybin for treatment-resistant depression. The country is home to a growing number of life science startups in Copenhagen, often referred to as "Medicon Valley," which are increasingly focusing on novel psychiatric drug development. The Danish culture of trust in public institutions and high levels of social cohesion facilitate the implementation of structured clinical programs and community-based integration support. Furthermore, Denmark's participation in cross-border European research initiatives ensures that it remains at the forefront of scientific advancements in the field. This forward-thinking approach and strong public health infrastructure define Denmark's emerging role in the European landscape.

COMPETITION OVERVIEW

The competition in the Europe psilocybin market is characterized by a dynamic mix of established biopharmaceutical companies and agile startups vying to lead the emerging field of psychedelic medicine. The landscape is currently defined by a race to complete pivotal clinical trials and secure first-mover advantage for regulatory approval in indications like treatment-resistant depression. Rivalry centers heavily on the quality of clinical data, the uniqueness of proprietary formulations, and the ability to navigate complex regulatory environments across different European nations. Companies differentiate themselves through vertical integration strategies that control everything from cultivation to clinical delivery, ensuring supply chain security and product consistency. Collaboration often coexists with competition as firms join forces with academic centers to share research costs and access specialized patient populations. The high barriers to entry created by stringent regulations and the need for specialized therapeutic infrastructure limit the number of viable competitors. Success depends on demonstrating superior safety profiles, establishing robust reimbursement models, and building trusted brands that can overcome the historical stigma associated with psychedelic substances.

KEY MARKET PLAYERS

A few major players of the Europe psilocybin market include

- Compass Pathways

- Atai Life Sciences

- Mindmed

- Cybin Inc

- Field Trip Health

- Gh Research

- Small Pharma

- Numinus Wellness

- Beckley Psytech

- Maps (Multidisciplinary Association For Psychedelic Studies)

Top Strategies Used by the Key Market Participants

Key players in the Europe psilocybin market primarily focus on advancing clinical trials to generate robust data required for regulatory approval and reimbursement. Companies frequently invest in vertical integration to secure reliable supply chains for high-quality raw materials and synthetic active ingredients. Strategic partnerships with academic institutions and hospital networks serve as a crucial tactic to facilitate patient recruitment and enhance scientific credibility. Participants actively engage with regulatory bodies like the European Medicines Agency to shape guidelines and clarify pathways for psychedelic-assisted psychotherapy. Developing proprietary formulations and novel derivatives allows firms to secure intellectual property rights and differentiate their products from natural alternatives. Additionally, firms emphasize building comprehensive therapist training programs to ensure standardized care delivery and address the critical shortage of qualified professionals in the field.

Leading Players in the Europe Psilocybin Market

- Compass Pathways stands as a pioneering mental health care company dedicated to accelerating patient access to evidence-based psilocybin therapy for treatment-resistant depression. The organization operates globally but maintains a significant footprint in Europe through its headquarters in London and an extensive clinical trial network across the continent. Compass recently initiated large-scale Phase 3 trials in multiple European countries to validate the efficacy and safety of its proprietary synthetic psilocybin formulation known as COMP360. Their strategic focus involves collaborating with leading academic institutions and regulatory bodies to establish robust clinical guidelines and reimbursement pathways. By developing a comprehensive therapeutic model that includes therapist training and digital support tools, Compass aims to standardize care delivery. This holistic approach positions the company as a global leader in transforming psychiatric care and ensuring that innovative treatments reach patients who have exhausted existing options.

- Champignon Brands Inc. operates as a life sciences company with a strong emphasis on the research and development of psilocybin based therapeutics through its European subsidiaries and partnerships. The company leverages its expertise in fungal cultivation and extraction to produce high-quality raw materials for clinical studies and future commercial products. Champignon recently expanded its operational capabilities by securing licenses for the cultivation and processing of psilocybin containing mushrooms in jurisdictions with favorable regulatory frameworks within Europe. Their strategy focuses on vertical integration to control the entire supply chain from spore to finished pharmaceutical product. By investing in advanced extraction technologies and establishing strategic alliances with European research centers, the company aims to accelerate the drug development pipeline. This commitment to scientific rigor and supply chain security strengthens their position as a key contributor to the emerging global psychedelic medicine industry.

- MindMed is a leading biopharmaceutical company focused on discovering and developing novel psychedelic-inspired medicines to treat brain health disorders with a significant presence in the European market. The company utilizes its proprietary drug discovery platform to create optimized derivatives of classic psychedelics, including psilocybin, aimed at improving efficacy and reducing side effects. MindMed recently advanced several clinical programs in Europe targeting anxiety and addiction while engaging proactively with European regulators to define clear approval pathways. Their approach involves generating robust clinical data to support regulatory submissions and building a scalable manufacturing infrastructure for their novel compounds. By fostering collaborations with top-tier European hospitals and research organizations, MindMed ensures access to diverse patient populations for its trials. This dedication to innovation and strategic partnership enables the company to lead the charge in bringing safe and effective psychedelic therapies to patients worldwide.

RECENT HAPPENING NEWS

- In late 2024, Beckley Psytech made significant progress with its short-acting psychedelic pipeline. In December 2024, the company announced positive topline results from its Phase 2a study of ELE-101 (intravenous psilocin) for Major Depressive Disorder, demonstrating rapid-acting potential.

MARKET SEGMENTATION

This research report on the Europe psilocybin market has been segmented and sub-segmented based on application, formulation, therapeutic setting, patient demographics & region.

By Application

- Depression

- Anxiety

- Post-Traumatic Stress Disorder

- Substance Abuse

- Obsessive-Compulsive Disorder

By Formulation

- Liquid

- Tablet

- Capsule

- Powder

- Injection

By Therapeutic Setting

- Inpatient

- Outpatient

- Residential Treatment

- Community-Based Programs

By Patient Demographics

- Adults

- Adolescents

- Elderly

- Veterans

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is driving the growth of the Europe psilocybin market?

Rising mental health awareness, increasing clinical trials, and supportive regulatory changes are key growth drivers.

2. What are the major applications of psilocybin?

It is primarily used in treating depression, anxiety, PTSD, and addiction disorders.

3. What are the key market trends?

Growing investments in psychedelic therapies and increasing partnerships between biotech firms and research institutes.

4. Who are the key players in the Europe psilocybin market?

Major players include Compass Pathways, atai Life Sciences, MindMed, and Cybin Inc.

5. What challenges does the market face?

Strict regulations, social stigma, and high costs of clinical trials are major challenges.

6. What opportunities exist in this market?

Expansion into new therapeutic areas and increasing acceptance of mental health treatments offer strong opportunities.

7. What role do clinical trials play in this market?

Clinical trials are crucial for validating safety, efficacy, and gaining regulatory approvals.

8. What is the future outlook of the Europe psilocybin market?

The market is expected to grow significantly due to ongoing research and evolving regulations.

9. What are the risks associated with psilocybin use?

Potential risks include psychological distress if used without supervision.

10. What industries are benefiting from this market growth?

Pharmaceuticals, biotechnology, and mental healthcare sectors are the primary beneficiaries.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com