Europe Red Clover Market Size, Share, Trends & Growth Forecast Report By Form, By End-User Industry, and By Country (Germany, France, United Kingdom, Netherlands, Denmark & Rest of Europe) – Industry Analysis and Forecast, 2026 to 2034

Europe Red Clover Market Size

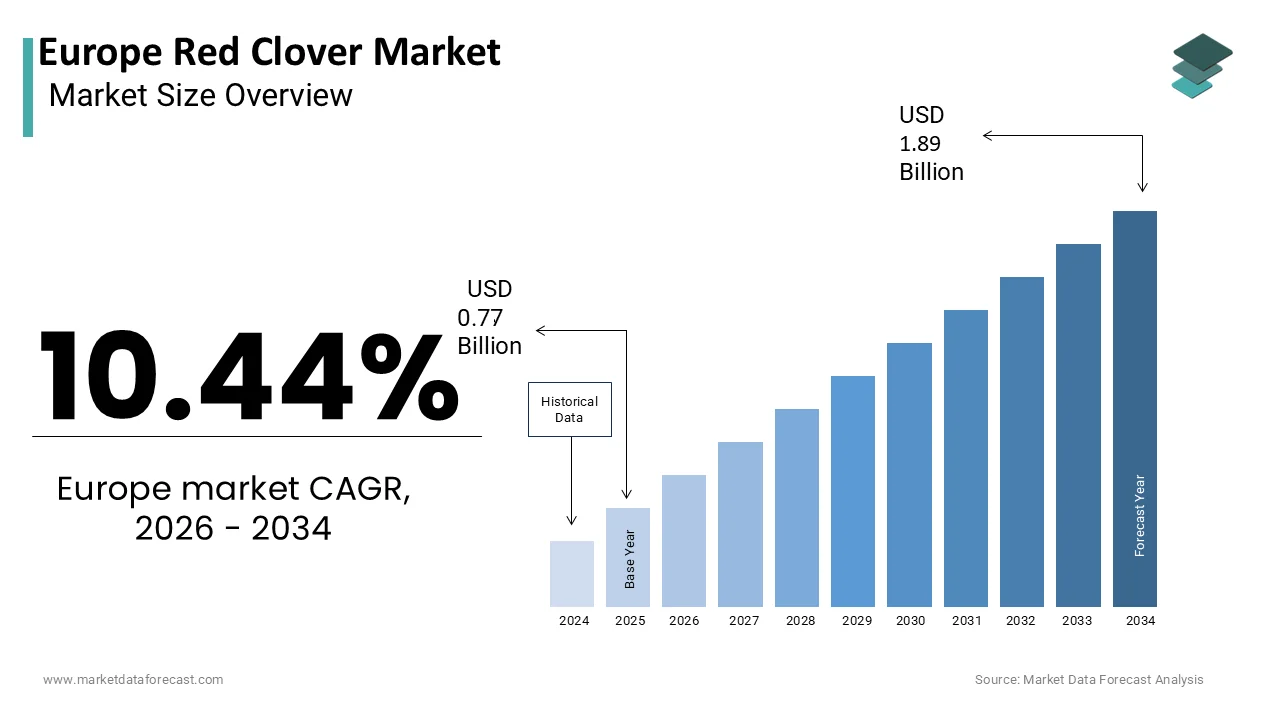

The Europe red clover market was valued at USD 0.77 billion in 2025, is estimated to reach USD 0.85 billion in 2026, and is projected to reach USD 1.89 billion by 2034, growing at a CAGR of 10.44% from 2026 to 2034.

The red clover is the cultivation, processing,g and distribution of Trifolium pratense,se a perennial legume widely utilized for livestock, forage, soil enrichment,t and increasingly for phytoestrogen extraction in nutraceuticals. This agricultural sector plays a pivotal role in sustainable farming systems due to the plant’s ability to fix atmospheric nitrogen, thereby reducing the dependency on synthetic fertilizers. As per Eurostat data from 2024, approximately 3.5 million hectares of temporary grasslands in the European Union included leguminous species, with red clover being a dominant component in Northern and Central European rotations. According to the Food and Agriculture Organization of the United Nations, the adoption of legume-based cropping systems has increased by 12% since 2020, driven by environmental policies. The European Commission’s Farm to Fork Strategy explicitly promotes the expansion of protein crops to enhance food security and biodiversity. The dual utility of red clover as both an agronomic asset and a source of bioactive compounds defines a dynamic market landscape. Regulatory support for nitrogen-fixing crops, combined with rising demand for natural health solutions,s creates a robust foundation for growth.

MARKET DRIVERS

Government Mandates for Nitrogen Reduction and Sustainable Agriculture

The stringent environmental regulations aimed at reducing nitrogen pollution are accelerating the growth of Europe red clover market. The European Union’s Nitrates Directive and the broader Green Deal framework impose strict limits on synthetic fertilizer usage to protect water quality and reduce greenhouse gas emissions. Red clover’s natural ability to fix nitrogen makes it an essential tool for farmers seeking compliance without sacrificing soil fertility. Farmers integrate red clover into crop rotations to replenish soil nutrients naturally, thereby lowering input costs and meeting regulatory standards. The Common Agricultural Policy provides direct payments for eco schemes that include legume cultivation, further incentivizing adoption. In France, over 200000 hectares of new legume cover crops were established in 20,23 supported by government subsidies, as noted by the French Ministry of Agriculture. This policy-driven shift ensures consistent demand for red clover seeds and biomass. The alignment of agricultural practices with environmental goals creates a stable market environment. Additionally, the push for carbon farming initiatives recognizes the soil carbon sequestration potential of legumes. These regulatory and financial incentives collectively drive the expansion of red clover cultivation across Europe.

Rising Demand for Natural Phytoestrogens in Menopause Management

The growing consumer preference for natural remedies in women’s health is greatly influencing the growth of Europe red clover market. Red clover is rich in isoflavones, such as biochanin A and formononetin, which act as phytoestrogens and are widely used to alleviate menopausal symptoms like hot flashes and night sweats. As per the European Menopause and Andropause Society, the number of women seeking non-hormonal treatments for menopause increased by 20% in 2023 due to safety concerns associated with hormone replacement therapy. This shift has spurred pharmaceutical and nutraceutical companies to incorporate red clover extracts into their product portfolios. Clinical studies validating the efficacy of red clover isoflavones have enhanced consumer confidence and medical endorsement. Regulatory approvals for novel food ingredients containing red clover extracts have streamlined market entry for new products. Manufacturers are investing in standardized extraction technologies to ensure consistent potency and quality. The trend toward preventive healthcare and wellness further boosts demand. Retailers expand their shelves with red clover-based tea capsules and tinctures.

MARKET RESTRAINTS

Susceptibility to Persistent Fungal Diseases

The vulnerability of red clover to persistent fungal diseases, such as clover rot and powdery mildew, is a primary factor hampering the growth of Europe red clover market. These pathogens can severely reduce biomass yield and seed quality, leading to economic losses for farmers and processors. As per the European Journal of Plant Pathology, incidence rates of Sclerotinia trifoliorum, the causative agent of clover rot, have increased by 10% in wetter regions of Northern Europe since 2020. Climate change-induced changes in precipitation patterns create favorable conditions for fungal proliferation. The lack of resistant varieties limits the effectiveness of chemical control measures, especially in organic farming systems where synthetic fungicides are prohibited. Farmers may hesitate to include red clover in rotations due to the risk of stand failure. The cost of managing disease through cultural practices such as extended crop rotations reduces overall farm productivity. Seed producers face challenges in maintaining high germination rates and purity standards. This volatility discourages widespread adoption, particularly among small-scale growers. Research into breeding resistant strains is ongoing, but progress is slow.

Limited Persistence and Short Productive Lifespan

The limited persistence and short productive lifespan of red clover compared to other forage legumes is additionally limiting the growth of Europe red clover market. Red clover typically maintains high productivity for only two to three years, after which yields decline significantly due to crown rot and winter kill. As per the Grassland Society of Northern Europe, the average productive life of a red clover ley is 2.5 years, necessitating frequent reseeding. This short lifecycle increases establishment costs and labor requirements for farmers. Frequent disturbance of soil for reseeding can also lead to carbon release and soil structure degradation, counteracting some environmental benefits. Farmers often prefer longer-lasting alternatives, such as white clover or alfalfa, which offer greater longevity despite potentially lower initial yields. The logistical burden of regular reseeding discourages adoption in intensive livestock systems where a continuous forage supply is important.

MARKET OPPORTUNITIES

Expansion into Plant-Based Protein Ingredients

The development of red clover as a source of plant-based protein is likely to pose a new opportunity for the growth of Europe red clover market. As the demand for alternative proteins grows, red clover leaves are being processed into protein concentrates and isolates for use in meat analogues and dietary supplements. Red clover protein offers a complete amino acid profile and is rich in antioxidants, making it attractive to health-conscious consumers. In 2024, several pilot plants in the Netherlands began commercial-scale extraction of red clover protein, demonstrating technical feasibility, according to a study. This diversification adds value to the crop beyond traditional forage uses. Farmers can harvest red clover specifically for protein extraction, creating a new revenue stream. The sustainability credentials of red clover align with the environmental goals of food manufacturers. Regulatory approval for the novel food status of red clover protein in the EU would further accelerate market entry.

Integration in Regenerative Agriculture and Carbon Farming

The integration of red clover into regenerative agriculture and carbon farming schemes is another attribute to enhance the growth of Europe red clover market. Regenerative practices focus on restoring soil health and sequestering carbon, where red clover plays a key role due to its deep root system and nitrogen-fixing capabilities. Red clover improves soil structure and water retention, enhancing resilience to climate extremes. Agri tech companies are developing monitoring tools to quantify carbon storage, enabling precise verification for credits. This financial incentive encourages wider adoption of red clover in arable rotations. The synergy between biodiversity enhancement and carbon capture appeals to corporate sustainability goals. Food companies are sourcing ingredients from regenerative farms to meet zero targets. The alignment with global climate goals ensures long-term support. Red clover becomes a strategic asset in the transition to climate-smart agriculture.

MARKET CHALLENGES

Competition from Established Alternative Legumes

Intense competition from established alternative legumes, such as alfalfa and white clover, is a challenge for the growth of Europe red clover market. Alfalfa offers higher protein content and longer persistence, while white clover integrates better into permanent grasslands. As per the European Feed Manufacturers Federation, alfalfa imports into the EU remained stable at 4 million tons in 202,3 indicatina g strong preference for this alternative. Farmers often choose alfalfa for high-intensity dairy operations due to its superior yield stability. White clover is preferred in grazing systems for its tolerance to frequent defoliation. Red clover struggles to compete in these specific niches due to its agronomic limitations. The established supply chains and knowledge base for alfalfa and white clover create barriers to entry for red clover. Seed companies invest more in breeding programs for these dominant species, limiting innovation for red clover. Market inertia makes it difficult to shift farmer preferences. Price competitiveness is another factor, as alfalfa meal often offers better value per unit of protein. Red clover must differentiate itself through unique benefits,s such as ease of establishment or specific health properties.

Regulatory Hurdles for Novel Food Approvals

The complex regulatory hurdles for novel food approvals for processed extracts and protein ingredients also inhibit the growth of Europe red clover market. The European Food Safety Authority requires rigorous safety assessments for new food sources, which are time-consuming and costly. As per the European Commission, the average time for novel food authorization exceeds 18 months,s creating uncertainty for investors. These delays hinder product launches and market entry for innovative companies. Small and medium-sized enterprises often lack the resources to navigate the complex regulatory landscape. The classification of red clover extracts as medicinal products in some member states adds another layer of complexity. Harmonization of regulations across the EU is incomplete, leading to fragmented market access. In Germany, red clover supplements face stricter labeling requirements than in other countries. This inconsistency increases compliance costs for manufacturers. The precautionary principle in EU food law can stifle innovation. Companies must balance regulatory compliance with commercial viability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Form, End-User Industry, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Barenbrug Group, NOW Foods, Swanson Health Products, Nature’s Way Products, LLC, Gaia Herbs, LLC, Frontier Co-op, Starwest Botanicals, Herb Pharm LLC, Indigo Herbs Ltd., Mountain Rose Herbs, Bio Botanica Inc., Bioforce AG |

SEGMENTAL ANALYSIS

By Forms Insights

The raw form segment was accounted in holding a significant share of the Europe red clover market in 2025 owing to the extensive use of raw red clover as high-quality forage for ruminant livestock, particularly dairy cattle. Raw red clover is valued for its high protein content, digestibility, and palatability,y which directly contribute to improved milk production and animal health. As per the European Milk Board, the inclusion of legume-based forages, such as red clover, in dairy diets increased milk yield by an average of 5% in 2023. Farmers prefer raw form,s including hay and silage, because they require minimal processing and retain the nutritional integrity of the plant. The cost-effectiveness of producing raw forage on the farm reduces dependency on imported protein feeds such as soybean meal. Regulatory incentives for reducing the carbon footprint of livestock farming further encourage the use of home-grown legumes. The simplicity of harvesting and storing raw red clover makes it accessible to farmers of all scales.

The processed form segment is expected to witness the fastest CAGR of 8.2% from 2026 to 2034, with the surging demand for standardized nutraceutical extracts used in women’s health supplements. Processed red clover extracts are rich in isoflavones, which are clinically proven to alleviate menopausal symptoms such as hot flashes and mood swings. As per the European Menopause and Andropause Society, the usage of phytoestrogen supplements increased by 25% among women aged 45 to 60 in 2023. Consumers prefer processed forms such as capsules, tablets, ts, and tinctures due to their convenience, precise dosage,e and consistent potency. In the United Kingdom, om sales of red clover extract supplements grew by 18% in 2,024 according to the British Herbal Medicine Association. Pharmaceutical and nutraceutical companies are investing in advanced extraction technologies to produce high purity isoflavone concentrates. Regulatory approvals for novel food ingredients containing red clover extracts have facilitated market entry for new products. The aging population in Europe creates a large and growing target demographic for these health solutions. Marketing campaigns emphasizing natural and safe alternatives to hormone replacement therapy drive consumer interest. This shift toward preventive healthcare and wellness ensures robust growth for processed red clover products.

The integration of processed red clover into functional food and beverage applications accelerates the growth of this segment. Food manufacturers are incorporating red clover extracts and powders into products such as teas, smoothies, and health bars to enhance their nutritional profile and appeal to health-conscious consumers. Processed forms allow for easier incorporation into diverse food matrices without affecting taste or texture significantly. These products cater to the trend of functional beverages that offer health benefits beyond basic nutrition. The versatility of processed red clover enables innovation in product development,t attracting a broader consumer base. Retailers are expanding their shelves with value-added red clover products targeting specific health needs. The convenience of ready-to-consume formats appeals to busy urban consumers. Investment in research and development by food companies continues to uncover new applications for red clover ingredients. This diversification beyond traditional supplements drives the accelerated expansion of the processed segment.

By End User Industries Insights

The agricultural industry segment was the largest by holding a prominent share of the Europe red clover market in 2025, owing to the fundamental role of red clover in sustainable livestock feeding systems, ms particularly for dairy and beef production. Red clover provides high-protein in an alternative to imported soybean meal, reducing feed costs and environmental impact. Dairy farmers rely on red clover silage to maintain high milk yields and quality while adhering to environmental regulations. The ability of red clover to thrive in temperate climates makes it a reliable feed source across Northern and Central Europe. Government subsidies for protein crops under the Common Agricultural Policy further incentivize their cultivation. The agricultural sector’s consistent and large volume requirements ensure steady market stability. The shift toward local and sustainable feed sources strengthens the position of red clover in agriculture. This foundational demand supports the majority of red clover production and trade in Europe.

The pharmaceutical industry segment is projected to expand at a CAGR of 9.5% from 2026 to 2034, with the increasing clinical validation of the efficacy of red clover isoflavones in managing menopausal symptoms and improving bone health. Recent studies have demonstrated that standardized red clover extracts can significantly reduce the frequency and severity of hot flashes without the risks associated with hormone replacement therapy. As per the European Journal of Clinical Nutrition, a meta-analysis published in 2023 confirmed the safety and effectiveness of red clover isoflavones, leading to greater medical endorsement. Pharmaceutical companies are developing prescription and over-the-counter medications containing red clover extracts to meet this demand. The aging female population in Europe creates a substantial market for these therapeutic solutions. Regulatory bodies are streamlining approval processes for botanical drugs, facilitating faster market entry.

COUNTRY LEVEL ANALYSIS

Germany Red Clover Market Analysis

Germany was the top performer in the Europe red clover market by capturing 22.5% of the share in 2025. The strong agricultural sector and stringent environmental regulations promoting sustainable farming practices are greatly influencing the growth of the market in Germany. Germany is also a major consumer of red clover extracts for pharmaceutical and nutraceutical applications, driven by a health-conscious population. The presence of leading pharmaceutical companies facilitates the development and distribution of red clover-based products. Strict fertilizer laws encourage farmers to adopt nitrogen-fixing crops, reducing reliance on synthetic inputs. The well-established organic farming sector further boosts demand for red clover in crop rotations. Germany’s robust research infrastructure supports innovation in red clover breeding and extraction technologies. The combination of agricultural policy and health trends ensures strong market growth.

France Red Clover Market Analysis

France red clover market was ranked second, holding 18.4% of the market share in 2025. The significant livestock industry and growing interest in plant-based medicines are leveraging the growth of the market. France is a leading producer of high-quality red clover seeds and forage for domestic and export markets. The pharmaceutical sector in France is also adopting red clover extracts for menopause management, reflecting changing consumer preferences. The government’s support for agroecology promotes the integration of legumes in cropping systems. French consumers are increasingly seeking natural health solutions,s driving retail sales of red clover products. The country’s diverse agricultural landscape allows for widespread red clover cultivation. Strong cooperative structures among farmers facilitate efficient production and distribution. France’s commitment to sustainability and health ensures its prominent position in the market.

United Kingdom Red Clover Market Analysis

The United Kingdom red clover market growth is likely to grow with the strong tradition of grassland farming and increasing focus on sustainable agriculture. As per the Department for Environment,nt Food and Rural Affairs, the area of temporary grasslands containing legumes increased by 8% in 2023. Red clover is widely used in livestock feed,eed particularly in Scotland and Wales, where dairy and sheep farming are prevalent. The pharmaceutical and supplement industry in the UK is a significant consumer of red clover extract,s driven by an aging population. Consumer awareness of natural remedies for menopause is high,gh leading to robust retail sales. Government initiatives such as the Environmental Land Management schemes encourage legume cultivation for soil health.

Netherlands Red Clover Market Analysis

The Netherlands red clover market growth is driven by intensive dairy farming and innovative agricultural practices. As per the study, the use of red clover in dairy rations increased by 15% in 2023 to reduce protein imports. In 2024, pilot projects for red clover protein production received significant investment, according to Wageningen University. Strict environmental regulations on nitrogen emissions drive the adoption of nitrogen-fixing crops. Dutch farmers are early adopters of sustainable practices, integrating red clover into precision farming systems. The pharmaceutical industry in the Netherlands utilizes red clover extracts for various health applications. The country’s strategic location and logistics infrastructure facilitate efficient trade.

Denmark Red Clover Market Analysis

Denmark's red clover market growth is likely to grow with a highly developed organic farming sector and strong environmental policies. Denmark is a leader in organic dairy production, relying heavily on red clover for feed. The government’s ambitious climate goals promote legume cultivation to reduce greenhouse gas emissions. Danish consumers are highly aware of sustainable and natural health products, ts driving demand for red clover supplements. The country’s research institutions are actively studying the benefits of red clover in sustainable agriculture. Strong cooperation between the farmers, researchers, and policymakers supports market development.

COMPETITIVE LANDSCAPE

The competition in the Europe red clover market is characterized by a mix of specialized seed breeders,s agricultural cooperatives, es and botanical extract suppliers vying for dominance through quality and innovation. Major players compete based on genetic performance, sustainability credentials,s and product purity rather than price alone. Established firms leverage their extensive research and development capabilities to introduce new cultivars that address climate challenges. Smaller niche players focus on organic and heirloom seeds, appealing to environmentally conscious farmers. Regulatory compliance regarding seed certification and novel food approvals serves as a significant barrier to entry, ensuring that only reputable firms can thrive. Collaborative efforts between breeders and farmers are common to optimize cultivation practices. The rise of plant-based proteins adds anotherlayer of competitionn, encouraging innovation in processing technologies. Companies that successfully integrate sustainability and scientific validation gain a competitive edge.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global Europe Red Clover Market include

- Barenbrug Group

- NOW Foods

- Swanson Health Products

- Nature’s Way Products, LLC

- Gaia Herbs, LLC

- Frontier Co-op

- Starwest Botanicals

- Herb Pharm LLC

- Indigo Herbs Ltd.

- Mountain Rose Herbs

- Bio Botanica Inc.

- Bioforce AG

TOP PLAYERS IN THE MARKET

- DLF Seeds is a leading global supplier of grass and clover seeds with a significant presence in the Europe red clover market. The company contributes to the global market by breeding high-yielding and disease-resistant red clover varieties that enhance livestock productivity. DLF focuses on sustainable agriculture and recently launched new seed mixes optimized for nitrogen fixation and soil health. The company has invested in research facilities across Europe to develop climate-resilient cultivars. These initiatives strengthen its market position by offering superior genetic solutions to farmers. DLF continues to lead through innovation and commitment to sustainability, ensuring long-term growth with trust among European agricultural stakeholders who value quality and environmental responsibility in their farming practices.

- Barenbrug Group is a major player in the forage and turf seed industry with strong involvement in the Europe red clover market. The company plays a vital role in providing high-quality red clover seeds for both conventional and organic farming systems. Barenbrug contributes to the global market by developing innovative varieties that improve feed efficiency and animal health. Recent actions include the expansion of its production capacity in Northern Europe to meet growing demand. The company has also partnered with agricultural institutions to promote the benefits of legume-based cropping systems. These efforts strengthen its market position by ensuring a reliable supply and technical support. Barenbrug focuses on sustainability and farmer education to drive adoption.

- Martin Bauer Group is a prominent supplier of botanical extracts with a significant footprint in the Europe red clover market for nutraceutical applications. The company is involved in sourcing and processing red clover into standardized extracts rich in isoflavones for women’s health products. Martin Bauer contributes to the global market by ensuring high purity and consistency in its botanical ingredients. Recent actions include the implementation of advanced extraction technologies to enhance product potency and efficacy. The company has also strengthened its supply chain transparency to meet strict regulatory standards. These strategies strengthen its market position by delivering premium quality ingredients to pharmaceutical and supplement manufacturers. Martin Bauer emphasizes sustainable sourcing and scientific validation.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe red clover market primarily employ genetic innovation and sustainable sourcing to maintain a competitive advantage. Companies invest in breeding programs to develop varieties with higher yield, disease resistance, and nutritional value. This strategy ensures differentiation and meets the evolving needs of farmers and processors. Another major strategy involves vertical integration to control quality from seed production to the final extract. Manufacturers establish direct relationships with growers to secure a consistent supply and reduce costs. Strategic partnerships with research institutions help validate health benefits and improve agronomic practices. Additionally, companies focus on digital platforms to provide technical support and market insights to customers. These combined approaches enable key participants to build strong brands and capture value in a growing market while addressing environmental and regulatory challenges effectively.

MARKET SEGMENTATION

This research report on the europe red clover market is segmented and sub-segmented into the following categories.

By Form

- Raw

- Processed

By End-User Industry

- Agricultural

- Pharmaceutical

By Country

- Germany

- France

- United Kingdom

- Netherlands

- Denmark

- Rest of Europe

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com