Europe Renal Dialysis Market Size, Share, Trends, & Growth Forecast Report By End User (In center dialysis, Home dialysis), Type, Modality and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

Europe Renal Dialysis Market Report Summary

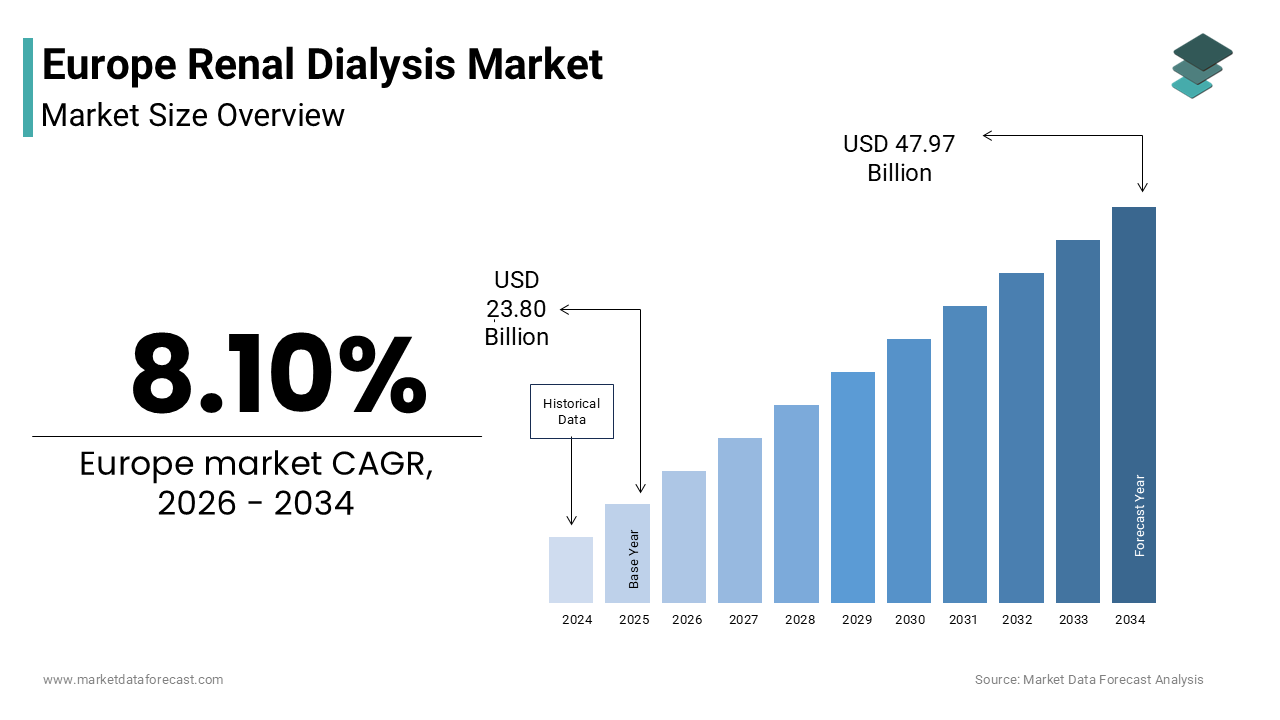

The Europe renal dialysis market was valued at USD 23.80 billion in 2025, is expected to reach USD 25.72 billion in 2026, and is projected to grow to USD 47.97 billion by 2034, registering a CAGR of 8.10% from 2026 to 2034. The market growth is driven by the rising prevalence of chronic kidney diseases, increasing incidence of diabetes and hypertension, and the growing aging population across Europe. Additionally, advancements in dialysis technologies and the expansion of home-based treatment modalities are further supporting market expansion.

Key Market Trends

- Rising prevalence of chronic kidney disease (CKD) driven by diabetes and hypertension

- Increasing adoption of home dialysis and remote monitoring solutions

- Integration of AI and digital health technologies in dialysis care

- Growing demand for patient-centric and decentralized treatment models

- Increasing focus on sustainability and eco-friendly dialysis solutions

Segmental Insights

- Based on end-user, the in-center dialysis segment held the dominant share of the Europe renal dialysis market in 2025. This dominance is driven by the availability of specialized infrastructure, skilled professionals, and the need for continuous medical supervision for complex patients.

- Based on type, the hemodialysis segment accounted for the largest share of the market in 2025, owing to its effectiveness in rapid toxin removal and suitability for patients with severe kidney conditions.

- Based on modality, the conventional hemodialysis segment dominated the market due to established clinical protocols and favorable reimbursement structures across Europe.

Regional Insights

The Europe renal dialysis market is witnessing strong growth across major countries due to rising disease burden and healthcare investments.

- Germany led the market with 26.8% share in 2025, driven by advanced healthcare infrastructure, high dialysis center density, and strong reimbursement systems.

- United Kingdom held a significant share due to increasing adoption of home dialysis and strong support from the National Health Service.

- France is experiencing steady growth with universal healthcare coverage and high adoption of advanced dialysis techniques like hemodiafiltration.

- Italy is expanding due to its aging population and increasing prevalence of kidney diseases.

- Spain is growing rapidly with investments in dialysis infrastructure and increasing focus on peritoneal dialysis adoption.

Competitive Landscape

The Europe renal dialysis market is highly competitive, with global healthcare companies and regional providers focusing on innovation, service expansion, and integrated care models. Companies are investing in home dialysis technologies, digital health platforms, and sustainable solutions to strengthen their market position. Strategic partnerships, acquisitions, and vertical integration are key strategies adopted by market participants. Key players in the Europe renal dialysis market include Fresenius Medical Care AG & Co. KGaA, Baxter International Inc., B. Braun Melsungen AG, Nipro Corporation, Nikkiso Co., Ltd., Asahi Kasei Corporation, Medtronic plc, DaVita Inc., Becton, Dickinson and Company, Toray Industries, Inc., JMS Co., Ltd., Diaverum, and Dialife SA.

Europe Renal Dialysis Market Size

The Europe renal dialysis market size was valued at USD 23.80 billion in 2025 and is anticipated to reach USD 25.72 billion in 2026 from USD 47.97 billion by 2034, growing at a CAGR of 8.10% during the forecast period from 2026 to 2034

The renal dialysis is healthcare dedicated to the artificial filtration of blood for patients suffering from end stage renal disease and acute kidney injury. This ecosystem includes hemodialysis, peritoneal dialysis, and related consumables, serving as a life sustaining bridge or permanent solution when native kidney function fails. As per statistics from the Organisation for Economic Co operation and Development, the prevalence of diabetes and hypertension, the two primary drivers of kidney failure, has risen by 15% over the last decade in major European nations. Furthermore, the aging demographic profile exacerbates this scenario, with the European Commission projecting that the population aged 65 and older will constitute nearly 30% of the total by 2050, significantly increasing the incidence of renal decline. Current clinical audits reveal that only about 25% of eligible patients receive timely pre emptive transplant evaluations, leaving the vast majority dependent on dialysis modalities. The integration of home-based therapies is gaining traction, yet in center treatments remain dominant due to infrastructure limitations.

MARKET DRIVERS

Escalating prevalence of diabetes and hypertension drives exponential patient volume

The surging incidence of diabetes mellitus and systemic hypertension serves is propelling the growth of Europe renal dialysis market. These two comorbidities are responsible for nearly 70% of all new cases of end stage renal disease by creating a relentless pipeline of patients requiring life sustaining filtration. As per data from the International Diabetes Federation, the number of adults living with diabetes in Europe is projected to reach 68 million by 2045, representing a significant increase from current figures and directly correlating with higher rates of diabetic nephropathy. Hypertension prevalence is equally alarming, with the European Society of Cardiology reporting that over 45% of the adult population in countries like Germany and Spain suffers from uncontrolled high blood pressure, a leading cause of glomerular damage. The pathophysiology of these conditions leads to progressive and irreversible loss of kidney function, often necessitating dialysis initiation within a decade of diagnosis. Furthermore, the sedentary lifestyles and dietary habits prevalent in Western Europe contribute to obesity, which further exacerbates renal stress. Clinical registries indicate that the average age of dialysis initiation is decreasing slightly due to earlier onset of type 2 diabetes in younger populations, extending the duration of treatment required per patient.

Aging demographic profile intensifies the burden of chronic kidney disease

The rapidly aging population structure, as advanced age is intrinsically linked to the physiological decline of kidney function and the accumulation of comorbidities is additionally elevating the growth of Europe renal dialysis market. The kidneys naturally lose filtering capacity over time, and the elderly population exhibits a significantly higher susceptibility to acute kidney injury and chronic progression towards organ failure. As per demographic projections from Eurostat, the proportion of individuals aged 80 and above in the European Union is expected to double by 2050, creating a massive cohort highly vulnerable to renal complications. Data from the European Renal Association reveals that the incidence rate of end stage renal disease in individuals over 75 is nearly four times higher than in those under 65, where the stark correlation between longevity and renal dependency. Older patients often present with complex medical histories including cardiovascular disease and frailty, making them poor candidates for transplantation and thus heavily reliant on long term dialysis. Additionally, the polypharmacy common in geriatric care increases the risk of drug induced nephrotoxicity, further accelerating the need for renal replacement therapy.

MARKET RESTRAINTS

Severe shortage of skilled nephrology professionals limits service scalability

The acute scarcity of specialized nephrologists, dialysis nurses, and trained technicians required to operate complex filtration systems safely is declining the growth of Europe renal dialysis market. The delivery of high-quality dialysis care demands a highly skilled multidisciplinary team, yet workforce planning in many European nations has failed to keep pace with the rising patient population. As per workforce analyses conducted by the European Renal Best Practice initiative, several member states face a deficit of up to 30% in qualified dialysis nursing staff, leading to burnout and increased turnover rates among existing employees. The training pipeline for nephrologists is lengthy and rigorous, resulting in a slow replenishment rate that cannot match the exponential growth in patient numbers. In rural areas of Eastern and Southern Europe, the situation is even more dire, with some regions having fewer than one specialist per 100000 inhabitants, forcing patients to travel excessive distances for care. This labor shortage directly caps the number of treatment slots available, creating waiting lists and compromising the quality of care through rushed procedures or inadequate monitoring. Furthermore, the physical and emotional demands of the job deter new entrants, exacerbating the gap.

High operational costs and reimbursement disparities restrict access

The substantial financial burden associated with establishing and maintaining dialysis facilities, coupled with fragmented reimbursement policies is also hindering the growth of Europe renal dialysis market. Dialysis is an expensive therapy requiring costly machinery, water treatment plants, and continuous consumption of disposables, placing a heavy strain on national healthcare budgets. As per health economic data from the European Observatory on Health Systems and Policies, the annual cost of treating a single hemodialysis patient can exceed 60000 euros, a figure that varies wildly depending on the country and setting. While Western European nations generally offer comprehensive coverage, countries in Eastern Europe often struggle with limited public funding, leading to restricted access or lower quality standards for patients reliant on state support. Reimbursement rates for home dialysis, which is often more cost effective in the long run, are frequently insufficient to cover the initial setup and training costs, discouraging both providers and patients from adopting this modality. Private insurance schemes often impose strict caps or exclusions for certain advanced therapies, forcing patients into suboptimal treatment paths. The lack of harmonized pricing and funding mechanisms creates a fragmented landscape where geographic location dictates the quality and availability of care.

MARKET OPPORTUNITIES

Expansion of home dialysis modalities offers significant growth potential

The strategic shift toward expanding home dialysis modalities, particularly peritoneal dialysis and home hemodialysis to decentralize care and improve patient quality of life is creating new opportunities for the growth of Europe renal dialysis market. Home based therapies empower patients to manage their treatment schedules, offering greater flexibility and autonomy while reducing the burden on overcrowded in center facilities. As per clinical guidelines from the European Renal Association, increasing the uptake of home dialysis to 30% of the total patient population could result in substantial cost savings for healthcare systems while improving clinical outcomes. Technological advancements have made home machines more user friendly, compact, and connected, allowing for remote monitoring by clinicians which enhances safety and adherence. Governments in countries like Sweden and the Netherlands are increasingly incentivizing home therapy adoption through favorable reimbursement structures and dedicated training programs. The COVID 19 pandemic further accelerated this trend by highlighting the risks of congregate settings and the resilience of decentralized care models. Manufacturers are responding by developing integrated digital platforms that facilitate real time data transmission and telehealth consultations, making home care viable for a broader range of patients. This transition not only addresses capacity constraints but also aligns with the growing patient preference for treating chronic conditions in the comfort of their own homes, opening a vast avenue for revenue growth and service innovation.

Integration of artificial intelligence and remote monitoring technologies

The incorporation of artificial intelligence and advanced remote monitoring technologies into dialysis workflows is additionally enhancing the growth of Europe renal dialysis market. AI algorithms can analyze vast amounts of patient data to personalize dialysis prescriptions, adjusting parameters such as ultrafiltration rates and dialysate composition in real time to minimize adverse events. As per research published in the Journal of Nephrology, the implementation of AI driven decision support systems has been shown to reduce hospitalization rates by up to 20% by predicting hypotensive episodes and other complications before they occur. Remote monitoring devices enable clinicians to track patient vitals and machine performance from a distance, facilitating proactive interventions and reducing the need for frequent in person visits. This technological integration is particularly valuable for managing the growing home dialysis population, ensuring safety and compliance without constant physical supervision. Furthermore, predictive analytics can optimize inventory management and staff scheduling, improving operational efficiency for dialysis centers. The ability to aggregate data across networks allows for benchmarking and continuous quality improvement, driving better overall standards of care.

MARKET CHALLENGES

Complex regulatory landscape for medical device approval creates delays

Navigating the intricate and evolving regulatory landscape for medical devices, aiming to introduce innovative dialysis technologies is one of the major challenges for the growth of Europe renal dialysis market. The implementation of the European Union Medical Device Regulation has intensified the requirements for clinical evidence, post market surveillance, and traceability, extending the time and cost required for product approval. The heightened scrutiny disproportionately affects smaller companies and startups lacking the resources to conduct extensive trials and maintain rigorous documentation standards. The variability in interpretation among different notified bodies across member states further complicates the harmonization of market entry strategies by leading to uncertainty and fragmented launch plans. Additionally, the requirement for unique device identification and stringent cybersecurity measures for connected dialysis machines adds layers of complexity to product development. These regulatory headwinds create an environment of uncertainty that can stifle innovation and slow the introduction of novel therapeutic solutions.

Environmental sustainability concerns regarding dialysis waste management

The environmental impact of dialysis treatments in the massive volume of plastic waste and water consumption generated by each session is additionally to impede the growth of Europe renal dialysis market. A single hemodialysis session produces approximately 2.5 kilograms of clinical waste, primarily consisting of single use plastics, tubing, and dialyzers, contributing significantly to the healthcare carbon footprint. As per estimates from the European Environment Agency, the dialysis sector is responsible for hundreds of thousands of tons of non-biodegradable waste annually across Europe, raising concerns among policymakers and environmental groups. Furthermore, conventional hemodialysis requires large quantities of ultrapure water, with each treatment consuming up to 500 liters, placing a strain on local water resources especially in drought prone regions. The energy intensity of running dialysis machines and water treatment plants further exacerbates the environmental burden. There is increasing pressure from regulators and society for healthcare providers to adopt sustainable practices, such as recycling programs, eco-friendly materials, and water conservation technologies. However, the strict infection control standards inherent to dialysis make it difficult to reduce single use items without compromising patient safety. Balancing the imperative for sterile, safe care with the urgent need for environmental stewardship requires significant investment in research and infrastructure by posing a complex operational and ethical challenge for market participants.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 9.23% |

| Segments Covered | By End-user, Type, Modality and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | Fresenius Medical Care AG & Co. KGaA, Baxter International Inc., B. Braun Melsungen AG, Nipro Corporation, Nikkiso Co., Ltd., Asahi Kasei Corporation, Medtronic plc, DaVita Inc., Becton, Dickinson and Company, Toray Industries, Inc., JMS Co., Ltd., Diaverum, and Dialife SA. |

SEGMENTAL ANALYSIS

By End User Insights

The in-center dialysis segment was accounted in holding a dominant share of Europe renal dialysis market in 2025 owing to the extensive network of dedicated dialysis clinics and hospital units equipped to manage complex medical needs under constant professional supervision. Many patients with end stage renal disease present with severe cardiovascular instability or multiple comorbidities that make unsupervised home treatment risky. As per data from the European Renal Association, over 75% of incident dialysis patients in Europe initiate therapy in a clinical setting due to the need for immediate medical intervention during potential adverse events like hypotension or arrhythmias. The presence of trained nephrologists and nurses allows for real time adjustment of ultrafiltration rates and electrolyte balance, which is critical for frail elderly populations who constitute a growing demographic. Furthermore, the logistical burden of storing supplies and managing waste at home deters many patients, making the turnkey solution of visiting a center more appealing. National health systems in countries like Germany and France have historically invested heavily in building large scale dialysis centers, creating a physical infrastructure that reinforces this model. The psychological comfort of being surrounded by medical staff and peer support groups within these facilities further cements patient preference, ensuring that in center care remains the standard of care for the vast majority of the European patient population.

The home dialysis segment is likely to grow at a fastest CAGR of 6.8% throughout the forecast period owing to the rapid expansion of home dialysis is the proactive push by European governments and health authorities to alleviate the crushing financial and capacity burden on traditional dialysis centers. As per directives from the European Kidney Health Alliance, several nations including the Netherlands and Sweden have implemented national targets aiming for 30% of all dialysis patients to be treated at home within the next decade. These governments are introducing favorable reimbursement tariffs that cover the full cost of home machine installation, water treatment modifications, and ongoing telehealth support, removing previous financial barriers. The economic argument is compelling, as studies indicate that home dialysis can reduce overall treatment costs by up to 20% compared to in center care by minimizing staffing requirements and facility overheads. Health ministries are actively funding educational campaigns to inform patients about these benefits, while simultaneously pressuring providers to develop robust home care programs.

By Type Insights

The hemodialysis segment held a significant share of the Europe renal dialysis market in 2025 with its unmatched ability to rapidly clear toxins and manage fluid overload, making it the preferred choice for patients with little to no residual kidney function or those experiencing acute metabolic crises. Unlike peritoneal dialysis which relies on slower continuous exchange, hemodialysis utilizes high flux membranes and precise blood pumps to achieve significant solute removal in short sessions. As per clinical guidelines from the European Best Practice Guidelines, hemodialysis is indicated as the first line therapy for patients with severe uremic symptoms, hyperkalemia, or significant volume overload where immediate correction is life-saving. The capability to customize dialysate composition and ultrafiltration profiles allows clinicians to tailor treatments for complex patients with cardiovascular instability, a common comorbidity in the European renal population. Data from registry analyses shows that patients initiated on hemodialysis have lower early mortality rates in the first 90 days compared to other modalities by reinforcing clinician confidence in prescribing it for fragile new starters. The robustness of the technique in handling difficult cases ensures that it remains the backbone of renal care services.

The peritoneal dialysis segment is swiftly growing at an anticipated CAGR of 5.4% from 2025 to 2034. The growth of the segment is likely to grow with the superior ability to preserve residual kidney function compared to hemodialysis, a factor strongly linked to better long term survival and quality of life. The continuous nature of peritoneal dialysis provides a more physiological clearance of toxins and fluids, avoiding the hemodynamic swings associated with intermittent hemodialysis that can damage remaining nephrons. As per longitudinal studies published in the Journal of the American Society of Nephrology, patients maintained on peritoneal dialysis retain measurable urine output for significantly longer periods, which correlates with reduced dietary restrictions and improved phosphate control. European nephrologists are increasingly prioritizing this "kidney first" approach, especially for younger patients and those with significant residual function at initiation. Guidelines from the European Renal Association now explicitly recommend considering peritoneal dialysis as the initial modality of choice for eligible patients to maximize this benefit. The preservation of native function also delays the need for more aggressive interventions and improves responsiveness to future transplantation.

By Modality Insights

The conventional hemodialysis segment was the largest by capturing a dominant share of the Europe renal dialysis market with its clinical protocols and the alignment of these schedules with existing reimbursement frameworks across Europe. For over fifty years, the thrice weekly regimen has been the global gold standard, resulting in a vast body of evidence supporting its efficacy and safety profile. As per coding and billing regulations in most European health systems, reimbursement rates are explicitly structured around the three session per week model, creating a rigid financial incentive for providers to adhere to this schedule. Deviating from this norm to offer alternative modalities often requires special approvals or faces uncertain compensation, discouraging innovation at the provider level. The operational workflow of dialysis centers is optimized for this rhythm, allowing for efficient staff rostering, machine utilization, and patient transport logistics. Training curricula for nurses and technicians are exclusively focused on this modality, creating a workforce deeply proficient in conventional methods but less experienced with alternatives.

The nocturnal hemodialysis segment is expected to register a fastest CAGR of 7.2% in coming years with the robust clinical data demonstrating its superiority in improving patient survival, cardiovascular health, and overall quality of life compared to conventional schedules. As per findings from the FHN Nocturnal Trial and subsequent European observational studies, patients on nocturnal regimens report significantly reduced fatigue, fewer dietary restrictions, and lower medication burdens, particularly for phosphate binders and antihypertensives. The gentle, prolonged removal of fluids eliminates the cramping and hypotension often experienced after short conventional sessions, allowing patients to wake up feeling refreshed rather than exhausted. This dramatic improvement in well being has sparked strong patient advocacy and demand, pushing clinicians to consider it for eligible candidates. The ability to work full time and engage in social activities during the day without the interruption of midday treatments is a transformative lifestyle benefit that appeals strongly to the working age population.

REGIONAL ANALYSIS

Germany Renal Dialysis Market Analysis

Germany was the largest contributor in the Europe renal dialysis market by holding 26.8% of share in 2025 with a highly dense network of specialized outpatient dialysis centers, a strong tradition of nephrology excellence, and a generous reimbursement system that supports high frequency treatments. The growth of segment is likely to grow with the unique structure of the German healthcare system, which encourages the proliferation of independent nephrologist owned practices that operate dedicated dialysis units, ensuring widespread geographic access. As per data from the German Society of Nephrology, Germany has one of the highest numbers of dialysis stations per capita in the world, facilitating easy access for its large elderly population. Furthermore, Germany is a hub for medical device manufacturing by hosting headquarters of major global players which fosters early adoption of cutting-edge technologies like hemodiafiltration. The cultural emphasis on rigorous clinical standards and frequent treatment sessions aligns perfectly with the conventional hemodialysis model, sustaining high volumes.

United Kingdom Renal Dialysis Market Analysis

The United Kingdom was ranked second by capturing 18.6% of Europe renal dialysis market share in 2025 with the National Health Service, which focuses heavily on cost efficiency and the strategic expansion of home dialysis to manage capacity constraints. The active implementation of national policies aimed at increasing the proportion of patients treated at home, supported by robust telehealth infrastructure and patient education programs is also boosting the growth of the market. The UK also faces a significant burden of diabetic kidney disease, which drives steady demand for renal replacement therapies across all regions. The presence of world leading research institutions and clinical trials in nephrology further enhances the sophistication of care delivery. The tension between limited capital for new brick and mortar centers and the need to treat a growing population has accelerated the adoption of innovative home models by making the UK a dynamic and evolving market leader.

France Renal Dialysis Market Analysis

France renal dialysis market growth is esteemed to grow steadily throughout the forecast period with a hybrid system combining large hospital based units with a thriving sector of private autonomous dialysis centers, all underpinned by a universal health coverage model. The high prevalence of hypertension and cardiovascular disease, which leads to a significant incidence of end stage renal disease requiring intensive management is bolstering the growth of market in this country. As per statistics from the French Biomedicine Agency, France maintains a very high rate of hemodiafiltration usage, a premium form of hemodialysis, reflecting the clinical preference for high efficiency clearance methods. The reimbursement framework is highly supportive, covering the full cost of treatment and associated transport, which encourages regular attendance and adherence to prescribed schedules. The country also boasts a strong network of nephrology training programs, ensuring a steady supply of skilled professionals to staff its numerous facilities. Recent government initiatives have begun to promote peritoneal dialysis more aggressively to address regional disparities in access, but hemodialysis remains the cornerstone of care.

Italy Renal Dialysis Market Analysis

Italy renal dialysis market growth is expected to grow with its aging population, which is driving a consistent and growing demand for dialysis services. Data from the Italian Society of Nephrology indicates that Italy has a notably high prevalence of diabetic nephropathy, necessitating complex care protocols that sustain market activity. The national health service provides universal coverage, though bureaucratic hurdles can sometimes delay the initiation of home programs. However, there is a growing movement towards standardizing care pathways nationwide to reduce geographical inequities. The strong presence of academic medical centers drives research and the adoption of novel therapies, particularly in the field of vascular access management.

Spain Renal Dialysis Market Analysis

Spain renal dialysis market growth is likely to grow with a strong public health system and an increasing focus on integrating dialysis care with transplant programs. The growth of the segmnent is driven by the strategic investment in modernizing dialysis infrastructure, with many autonomous communities upgrading facilities to include advanced water treatment systems and digital monitoring tools. According to the Spanish Society of Nephrology, there is a concerted effort to increase the utilization of peritoneal dialysis, leveraging its cost effectiveness and suitability for the country geography, which includes many island and rural populations. The public funding model ensures broad access, although waiting times for certain procedures can vary by region. The collaborative efforts between public hospitals and private providers are enhancing capacity and introducing innovative care models.

COMPETITIVE LANDSCAPE

The competitive landscape of the Europe renal dialysis market is characterized by intense rivalry among established multinational corporations and specialized regional providers striving for dominance through innovation and service excellence. Market leaders leverage their extensive distribution networks and integrated care models to maintain strong relationships with large hospital groups and national health services. Competition is fierce in the area of home dialysis where companies vie to offer the most user friendly and connected devices that empower patients. Regulatory compliance acts as a significant barrier to entry but also serves as a battleground where firms compete on the speed and ease of adhering to stringent European safety standards. Price competition remains relevant for commoditized consumables while value based selling dominates for high capital equipment and services. Strategic collaborations with academic institutions for clinical trials further differentiate players by validating efficacy.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe renal dialysis market include

- Fresenius Medical Care AG & Co. KGaA

- Baxter International Inc.

- B. Braun Melsungen AG

- Nipro Corporation

- Nikkiso Co., Ltd.

- Asahi Kasei Corporation

- Medtronic plc

- DaVita Inc.

- Becton, Dickinson and Company (BD)

- Toray Industries, Inc.

- JMS Co., Ltd.

- Diaverum

- Dialife SA

Top Players in the Europe Renal Dialysis Market

Fresenius Medical Care

Fresenius Medical Care stands as the global leader in integrated dialysis products and services, playing a pivotal role in shaping renal care standards across Europe. The company operates an extensive network of outpatient dialysis clinics and supplies a comprehensive portfolio of dialyzers, machines, and concentrates to hospitals worldwide. In Europe, Fresenius Medical Care actively drives the transition toward home therapies by launching next generation portable hemodialysis devices and digital health platforms that enable remote patient monitoring. Recent actions include the strategic expansion of its value based care programs which partner with payers to improve outcomes while reducing costs. The firm also invests heavily in sustainability initiatives to reduce the environmental footprint of dialysis treatments through water conservation technologies.

Baxter International

Baxter International is a renowned global healthcare company with a profound impact on the Europe renal dialysis market through its leadership in peritoneal dialysis solutions and acute kidney injury therapies. The company provides a wide range of automated peritoneal dialysis cyclers, manual exchange systems, and critical care continuous renal replacement therapy devices. In Europe, Baxter focuses on empowering patients to manage their condition at home by developing user friendly interfaces and connected health ecosystems that facilitate seamless data sharing with clinicians. Recent strategic moves involve the introduction of advanced biocompatible dialysis fluids designed to preserve residual kidney function and reduce long term complications. The corporation has also strengthened its European supply chain resilience to ensure uninterrupted access to life saving therapies amidst global logistical challenges.

B. Braun Melsungen AG

B. Braun Melsungen AG operates as a leading German medical technology company with a significant presence in the Europe renal dialysis sector through its high quality hemodialysis systems and consumables. The company offers a robust portfolio including hemodialysis machines, high flux dialyzers, and bloodline sets that are widely used in hospitals and dialysis centers throughout the region. In Europe, B. Braun emphasizes safety and precision by integrating advanced monitoring features and ergonomic designs into its equipment to minimize clinical errors and enhance operator comfort. Recent actions include the launch of sustainable dialysis products made from recycled materials and the development of digital solutions for real time treatment documentation and analysis. The firm actively participates in educational initiatives to train healthcare professionals on best practices for vascular access management and infection control.

Top Strategies Used by Key Market Participants

Key players in the Europe renal dialysis market primarily employ strategic acquisitions and partnerships to expand their product portfolios and penetrate new geographic regions effectively. Companies invest heavily in research and development to introduce innovative home dialysis devices and digital health platforms that enhance patient autonomy and clinical outcomes. Market participants focus on vertical integration by operating their own dialysis clinics to secure steady demand for their medical devices and consumables. Educational initiatives and training programs for nephrologists and nurses are widely used to build brand loyalty and promote the adoption of proprietary technologies. Firms also prioritize sustainability by developing eco-friendly products and processes to align with stringent European environmental regulations. Expanding manufacturing capabilities within Europe helps companies mitigate supply chain risks and ensure consistent product availability.

MARKET SEGMENTATION

This research report on the Europe renal dialysis market has been segmented and sub-segmented based on the following categories.

By End-user

- In center dialysis

- Home dialysis

By Type

- Hemodialysis

- Peritoneal

- Others

By Modality

- Conventional hemodialysis

- Short daily hemodialysis

- Nocturnal hemodialysis

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com