Europe Scented Candles Market Size, Share, Trends, & Growth Forecast Report By Category (Mass, Premium),Material, Distribution Channel and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2025 to 2033

Europe Scented Candles Market Report Summary

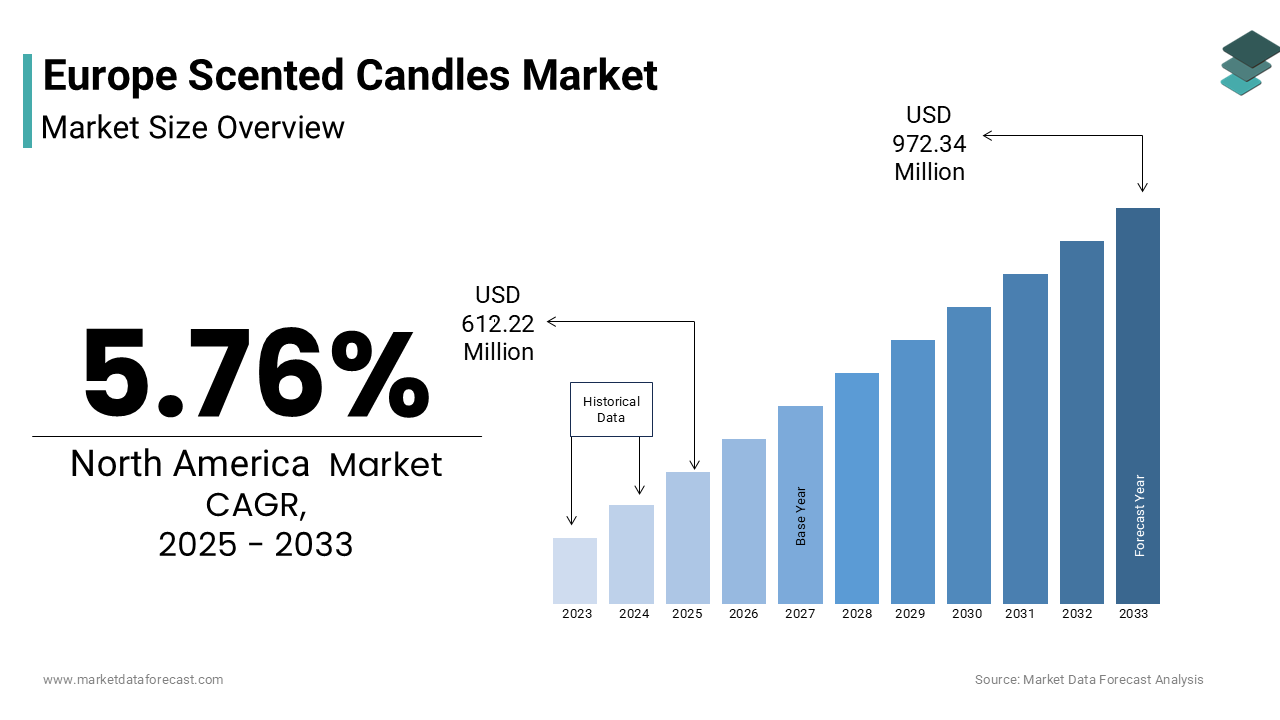

The Europe scented candles market was valued at USD 587.39 million in 2024, is anticipated to reach USD 612.22 million in 2025, and is projected to reach USD 972.34 million by 2033, growing at a CAGR of 5.76% during the forecast period from 2025 to 2033. The growth of the Europe scented candles market is driven by rising consumer focus on home ambiance, mental well-being, and aromatherapy-based lifestyle products. Increasing time spent indoors, the expansion of premium home fragrance gifting culture, and growing demand for wellness-oriented and sustainable candles are further fueling market growth. Moreover, regulatory-driven ingredient transparency, the shift toward plant-based waxes, and the revival of artisanal and heritage-inspired fragrances are reshaping product innovation and consumer preferences across Europe.

Key Market Trends

- Rising adoption of scented candles as aromatherapy tools supporting stress relief, relaxation, and mental wellness.

- Growing popularity of premium and luxury scented candles positioned as lifestyle and gifting products.

- Increasing demand for sustainable and biodegradable waxes, including soy, rapeseed, and blended formulations.

- Expansion of online and direct-to-consumer channels offering personalized scent discovery and curated collections.

- Revival of artisanal craftsmanship and regional heritage scents, leveraging European botanical identity.

Segmental Insights

- Based on category, the mass segment was the largest and held a significant share of the Europe scented candles market in 2024. The dominance of this segment is attributed to wide availability, affordable pricing, and strong presence across hypermarkets and supermarkets, where candles are frequently purchased as everyday home ambiance products.

- Based on material, the blended wax segment accounted for the largest share of the Europe scented candles market in 2024. This segment’s leadership is driven by its ability to balance cost efficiency, burn performance, and sustainability perception by combining paraffin with plant-based waxes.

- Based on distribution channel, the hypermarkets and supermarkets segment was the largest, occupying a prominent share of the Europe scented candles market in 2024. The dominance of this segment stems from high impulse purchasing, extensive shelf visibility, and integration of scented candles into routine household shopping.

Regional Insights

- The Europe scented candles market is witnessing steady growth across major economies, supported by home lifestyle trends, strong gifting traditions, and rising wellness awareness.

- France was the largest contributor, accounting for a significant share of the Europe scented candles market in 2024, driven by its deep-rooted fragrance heritage, access to premium essential oils, and strong presence of luxury candle brands.

- The United Kingdom continues to perform strongly, fueled by established gifting culture, increasing emphasis on mental well-being, and widespread adoption of aromatherapy-based home products.

- Germany remains a key market, supported by strong environmental awareness, preference for sustainable and allergen-transparent products, and growing adoption of plant-based wax candles.

- Italy is emerging as a high-value market, driven by design-centric consumption, aesthetic vessel preferences, and integration of scented candles into broader luxury lifestyle and interior décor narratives.

Competitive Landscape

The Europe scented candles market is characterized by the presence of global fragrance brands, regional artisans, and mass-market retailers competing on the basis of olfactory differentiation, sustainability credentials, pricing, and brand storytelling. Leading companies are focusing on premiumization, refillable packaging, transparent ingredient disclosure, and digital engagement through e-commerce platforms. Strategic collaborations with wellness experts, interior designers, and lifestyle influencers are strengthening brand positioning. Prominent players in the Europe scented candles market include Yankee Candle (Newell Brands), Village Candle, DW Home, Scentsy, Inc., Bath & Body Works, LLC, Bridgewater Candle Company, IKEA Group, L’Occitane International S.A., The Body Shop International Limited, and Voluspa.

Europe Scented Candles Market Size

The europe scented candles market size was valued at USD 587.39 million in 2024 and is anticipated to reach USD 612.22 million in 2025 from USD 972.34 million by 2033, growing at a CAGR of 5.76% during the forecast period from 2025 to 2033.

Scented candles have evolved beyond simple illumination to become integral elements of home ambiance wellness rituals and sensory lifestyle experiences. These products typically consist of natural or synthetic waxes infused with fragrance oils and are engineered to deliver consistent aroma diffusion over extended burn cycles. According to Eurostat, European households reported increased time spent indoors during evening hours in 2023, a behavioral trend amplified by hybrid work models and rising energy costs that discourage external leisure. This domestic anchoring has elevated home environment quality as a priority, with olfactory comfort playing a measurable psychological role. As per the European Commission’s 2023 Quality of Life Survey, many respondents identified ambient scent as a key factor in perceived home relaxation. Furthermore, national regulations such as France’s AGEC Law now mandate transparency in ingredient labeling for all home fragrances, driving formulation shifts toward certified essential oils and biodegradable carriers.

MARKET DRIVERS

Rising Emphasis on Mental Well Being and Aromatherapy Integration

The growing recognition of mental health as a public priority has significantly elevated demand for scented candles as accessible aromatherapy tools. The rising emphasis on mental well being and aromatherapy integration is majorly elevating the growth of Europe scented candles market. According to the World Health Organization, mental health disorders affect over 84 million people in the European Union with anxiety and stress related conditions showing a 22% increase, since 2020. In response, consumers are increasingly adopting non-clinical sensory interventions including olfactory stimulation through candles infused with lavender bergamot and eucalyptus. This scientific validation has spurred mainstream adoption with retailers like Sephora and Douglas dedicating entire sections to “wellness candles” formulated in collaboration with aromatherapists. Additionally, the European Candle Association reported that new candle launches in 2023 featured wellness centric claims such as “calming” “grounding” or “mindfulness enhancing.”

Expansion of Premium Home Fragrance Gifting Culture

Gifting behavior has emerged as a powerful structural driver of scented candle consumption, across Europe particularly during holidays and personal milestones. The expansion of premium home fragrance gifting culture is additionally elevating the growth of Europe scented candles market. In the United Kingdom, the tradition of “hostess gifts” has institutionalized candle gifting with adults reporting they carry a scented candle, when visiting private homes,, as confirmed by the UK Office for National Statistics. Similarly, in France, the cultural norm of “cadeau de remerciement” or thank you gifts has made luxury candles from brands like Diptyque and Cire Trudon staple tokens of appreciation. A 2024 survey by Eurofound found that European companies included scented candles in their end of year employee care kits.

MARKET RESTRAINTS

Stringent EU Regulations on Fragrance Allergen Disclosure

The European Union’s rigorous allergen labeling requirements under the Cosmetics Regulation EC 1223 2009, which also applies to scented candles due to their skin proximity during handling. The stringent EU regulations on fragrance allergen disclosure is restricting the growth of Europe scented candles market. According to the Scientific Committee on Consumer Safety, 26 specific fragrance substances are classified as potential allergens requiring mandatory declaration, when present above certain thresholds 0.01% in leave on products and 0.001% in aerosols though candles fall into a gray-area interpreted broadly by national authorities. As a result, manufacturers must reformulate popular scents like lily of the valley or oakmoss which contain restricted materials, such as hydroxycitronellal or atranol. This regulatory fragmentation forces brands to maintain multiple formulations increasing compliance costs high and delaying product launches. While intended to protect consumer health these rules inadvertently limit olfactory creativity and heritage scent reproduction in the European market.

Limited Availability of Certified Sustainable Waxes

The shortage of domestically produced certified sustainable waxes, such as soy palm or rapeseed is also degrading the growth of Europe scented candles market. According to the European Commission, many soy wax used in European candle making is imported from the United States and Brazil raising concerns about deforestation linkage and carbon footprint. The EU Deforestation Regulation, which came into force in December 2024 now requires full geolocation traceability for all soy based products further complicating supply chains. Beeswax though locally available is constrained by pollinator decline. Paraffin derived from petroleum remains the most cost effective and consistent option but faces increasing consumer rejection of German buyers, now actively avoid paraffin, as per GfK’s 2023 home care survey. This raw material gap between sustainability aspiration and supply reality forces many brands to compromise on either cost performance or environmental claims creating a persistent tension in product development.

MARKET OPPORTUNITIES

Integration of Smart Home Compatible Scent Systems

The emergence of ambient fragrance with smart home technology with a high potential opportunity for premium scented candle innovation. The integration of smart home compatible scent systems is major opportunity for the growth of Europe scented candles market. As per the European Smart Home Observatory, households in Germany, France, and the Netherlands, connected device such as voice assistants or automated lighting. This ecosystem creates a natural entry point for programmable scent delivery systems that integrate with existing platforms. In 2023, Swedish startup Aromajoin launched a Wi Fi enabled candle warmer compatible with Amazon, Alexa, and Google Home by allowing users to schedule scent diffusion or adjust intensity via smartphone. Similarly, the German brand Skandinavisk introduced its “Hygge Link” line in early 2024 featuring NFC enabled candles that trigger personalized lighting and music settings when lit.

Revival of Artisanal Craftsmanship in Regional Heritage Scents

The growing consumer preference for authenticity and local identity is driving demand for regionally inspired scented candles rooted in European botanical and cultural heritage. The revivial of artisanal craftsmanship in regional heritage scents is also elevating the growth of Europe scented candles market. According to the European Cultural Heritage Platform, many consumers aged 25 to 45 express willingness to pay a premium for products reflecting local terroir or artisanal tradition. This trend has revitalized niche producers using native ingredients, such as lavender from Provence heather from the Scottish Highlands or pine resin from the Black Forest. Similarly, Sweden’s “Duft av Sverige” initiative supports small batch producers using wild foraged botanicals like cloudberry and birch tar. Retailers like Selfridges and KaDeWe, now curate “European Fragrance Trails” collections highlighting these regional narratives.

MARKET CHALLENGES

Volatility in Essential Oil Pricing Due to Climate Induced Crop Failures

The acute input cost instability due to climate related disruptions in essential oil supply chains is one of the challenges for the growth of Europe scented candles market. Many premium fragrances rely on plant derived oils, such as lavender rosemary and citrus whose yields are highly sensitive to weather extremes. According to the European Environment Agency, prolonged droughts in Southern Europe reduced lavender harvests in France and Spain in 2023 compared to the 5 year average. Similarly, unseasonal frosts in Sicily damaged bergamot orchards leading to drop in 2024 output and corresponding price spikes. Since, natural oils can constitute up to a premium candle’s raw material cost these fluctuations directly impact profitability. Small batch producers lacking hedging mechanisms are particularly vulnerable.

Consumer Skepticism Toward Greenwashing in Sustainability Claims

The rising consumer distrust regarding environmental and ethical claims made by candle brands, which is additionally to decline the growth of Europe scented candles market. According to the European Consumer Organisation, EU shoppers believe that “natural” or “eco-friendly” labels on home fragrances are misleading or insufficiently verified. The European Commission’s 2023 sweep of online candle retailers found that made unsubstantiated claims about biodegradability or carbon neutrality. In response, countries like the Netherlands and Belgium have introduced stricter national guidelines requiring proof of sustainability assertions. This regulatory scrutiny combined with social media scrutiny amplifies reputational risk for brands lacking transparent supply chains. Consequently, even legitimate sustainable producers face uphill battles in consumer trust requiring costly certifications like COSMOS or Cradle to Cradle to stand out.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Analysed | By Category, Material, Distribution Channe and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Analysed | United Kingdom, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, and the Czech Republic. |

| Market Leaders Profiled | Yankee Candle (Newell Brands), Village Candle, DW Home, Scentsy, Inc., Bath & Body Works, LLC, Bridgewater Candle Company, IKEA Group, L’Occitane International S.A., The Body Shop International Limited, and Voluspa |

SEGMENTAL ANALYSIS

By Category Insights

The mass segment was the largest by accounting for a dominant share of the Europe scented candles market in 2024 with the broad accessibility consistent pricing and integration into everyday retail routines across diverse socioeconomic groups. As per a study, many European households purchase home care or ambiance products at least once per month with mass candles priced between two and eight euros representing a low commitment trial for scent exploration. Retailers like Carrefour Tesco and Edeka have amplified this trend by dedicating permanent shelf space to seasonal and evergreen scents such as vanilla and ocean breeze ensuring year-round visibility. The European Retail Roundtable reported that in 2023 private label scented candles grew, across major supermarket chains driven by margin optimization and consumer trust in store brand quality.

The premium segment is projected to grow at fastest CAGR of 12.8% from 2025 to 2033 from rising consumer willingness to invest in curated sensory experiences as extensions of personal identity and well-being. The “home as sanctuary” mindset intensified by hybrid work models is also driving the growth of Europe scented candles market. As per the European Commission’s 2023 Quality of Life Survey, urban professionals now allocate dedicated budgets for home ambiance with premium candles seen as justified self-care expenditures. Brands like Diptyque Jo Malone and Byredo have leveraged storytelling and olfactory artistry to position candles as collectible lifestyle objects rather than consumables. Limited editions such as Guerlain’s “Parisian Nights” collection sold out across Europe within 72 hours of launch in November 2023 demonstrating pent up demand for experiential luxury.

By Material Insights

The blended wax formulations segment was the largest by holding 51.2% of the Europe scented candles market share in 2024. These blends typically combine paraffin with soy palm or rapeseed wax to balance cost performance and sustainability perception. A primary driver is functional optimization pure soy waxes often suffer from poor scent throw and frosting while pure paraffin faces consumer resistance. Blends deliver consistent burn quality strong fragrance load and smooth aesthetic at a moderate price point. Under the EU Deforestation Regulation, which mandates traceability for pure soy and palm inputs blends containing less than regulated wax can bypass stringent documentation requirements. This loophole has been widely adopted by mid-tier brands seeking to claim “partially plant based” status without full supply chain overhauls.

The soy wax segment is anticipated to witness a fastest CAGR of 15.3% throughout the forecast period owing to the escalating consumer demand for biodegradable non toxic home products aligned with circular economy principles. As per the European Consumer Organisation, many shoppers aged 18 to 35 actively seek candles labeled “100% plant based” with soy being the most recognized vegetable wax. France’s AGEC Law introduced in 2023 requires all home fragrance products sold in the country to disclose wax composition and banned paraffin in municipal procurement by 2025 accelerating soy adoption, among public sector suppliers. Companies like Skåne Candles in Sweden and Lumière Noire in Belgium, now source certified EU grown soy achieving full traceability from field to jar.

By Distribution Channel Insights

The hypermarkets and supermarkets segment was the largest by holding 47.6% of the Europe scented candles market share in 2024 from their role as one stop destinations for routine household replenishment, where candles are purchased alongside groceries cleaning supplies and personal care items. A primary driver is impulse visibility, candles are strategically placed in high traffic zones, such as seasonal aisles checkout perimeters and home care sections. Additionally, extended operating hours and nationwide footprint ensure accessibility across urban rural and suburban demographics.

The online stores segment is likely to register a fastest CAGR of 18.6% from 2025 to 2033 with the emergence of digital discovery personalized curation and direct to consumer brand building. A key driver is the ability to offer extensive scent libraries and detailed ingredient transparency features impossible in physical retail. Niche brands like Melt Candle Co in the UK and Nez Sens in France, use e commerce platforms to showcase olfactory notes burn duration and sustainability credentials through immersive storytelling. As per the European Digital Consumer Panel, online candle buyers cite “access to unique scents not available locally” as their primary motivation. Companies like Scent Trunk and Cierge Club offer monthly curated boxes with personalized scent profiles based on user preferences driving repeat engagement and customer lifetime value.

REGIONAL ANALYSIS

France Scented Candles Market Analysis

France was the largest contributor of the Europe scented candles market by holding 22.4% of share in 2024 with its centuries old olfactory heritage, where scent is considered an art form rather than a commodity. Grasse the historic perfume capital supplies over 60% of Europe’s premium fragrance oils ensuring unparalleled access to high quality raw materials. National brands like Diptyque and Cire Trudon leverage this legacy to command global prestige, while small batch artisans benefit from the “Savoir Faire” certification that validates traditional candle making techniques. The French Ministry of Culture designated candle craftsmanship as part of the nation’s intangible cultural heritage in 2023 further institutionalizing its value. Additionally, France enforces the strictest ingredient disclosure laws in Europe under the AGEC Law compelling brands to innovate with transparent formulations.

The United Kingdom Scented Candles Market Analysis

The United Kingdom was ranked second by holding 18.7% of the Europe scented candles market share in 2024. Its distinct profile is shaped by deeply embedded gifting customs and the rapid mainstreaming of wellness rituals. The tradition of bringing a hostess gift to private gatherings has normalized candle gifting with many adults reporting they carry a scented candle, when visiting homes according to the UK Office for National Statistics. Simultaneously, the National Health Service’s 2023 mental well-being initiative endorsed non-pharmaceutical stress relief methods including ambient scenting encouraging household adoption. British brands like Jo Malone, NEOM, and Bamford have pioneered wellness focused collections with therapeutic claims validated by aromatherapy institutes.

Germany Scented Candles Market Analysis

Germany scented candles market growth is likely to grow with the dual commitment to environmental rigor and value conscious consumption. Over 80% of German consumers check wax composition before purchase with paraffin facing near total rejection in urban centers, as per survey. This has driven mass adoption of rapeseed and blended plant-based waxes with Aldi and Lidl offering certified sustainable candles under two euros. Simultaneously, Germany enforces the EU’s most stringent allergen labeling through the Federal Institute for Risk Assessment requiring full quantitative disclosure of all fragrance ingredients above 0.001%. This transparency standard has elevated consumer trust in domestically produced candles. The country also leads in refillable and reusable candle systems companies like LUMBR and Stadtklang offer ceramic vessels with replaceable wax inserts reducing single use waste.

Italy Scented Candles Market Analysis

Italy scented candles market growth is likely to grow with the prominent growth opportunities in next coming years. Its candle culture is inseparable from the nation’s design heritage, where fragrance is experienced as a multisensory art object. Italian consumers prioritize vessel aesthetics burn quality and olfactory complexity over price with 60% willing to pay premium for hand blown glass or ceramic containers. Brands like Acqua di Parma and Santa Maria Novella integrate candles into broader lifestyle narratives linking scent to regional terroir and historical apothecary traditions. The Milan Design Week has featured candle installations since 2022 with collaborations between perfumers and architects redefining ambient experience. Unlike Northern European countries, Italy’s consumption peaks during summer months when open windows and terraces enhance scent diffusion. This design led emotional consumption model makes Italy a high value aesthetic benchmark within the European landscape.

Sweden Scented Candles Market Analysis

Sweden scented candles market growth is anticipated to grow steadily with the minimalist design principles extreme environmental standards and early adoption of circular business models. Swedish consumers exhibit the highest preference for unscented or subtly fragranced candles in Europe with favoring strong aromas. This has elevated demand for clean burning rapeseed and beeswax blends with transparent sourcing. Brands like Skandinavisk and Byredo emphasize “hygge” and “lagom” philosophies coziness without excess through muted palettes and functional simplicity. Sweden also leads in regulatory innovation, where the Swedish Environmental Protection Agency introduced mandatory carbon footprint labeling for all home fragrances in 2023 requiring lifecycle assessments from raw material to disposal.

COMPETITIVE LANDSCAPE

The Europe scented candles market features layered competition spanning global luxury houses regional artisans and mass market retailers. At the premium end brands differentiate through olfactory uniqueness vessel design and cultural narrative with French and British houses setting global benchmarks. Mid-tier players compete on sustainability credentials including wax composition refillability and carbon footprint transparency often certified by EU eco labels. The private labels and value brands dominate through price accessibility and retail integration particularly in hypermarkets. Competition is further intensified by regulatory complexity around allergen disclosure and deforestation free sourcing which raises compliance costs and favors established players. Digital channels have lowered entry barriers for niche brands yet also increased consumer scrutiny on greenwashing.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe Scented Candles Market include

- Yankee Candle (Newell Brands)

- Village Candle

- DW Home

- Scentsy, Inc.

- Bath & Body Works, LLC

- Bridgewater Candle Company

- IKEA Group

- L’Occitane International S.A.

- The Body Shop International Limited

- Voluspa (Cognac Gourmand)

Top Players in the Europe Scented Candles Market

Diptyque SAS

Diptyque SAS is a French luxury fragrance house renowned for its artisanal scented candles that blend olfactory artistry with minimalist design. The company exports its products to over seventy countries and is credited with pioneering the premium home fragrance segment globally. In Europe Diptyque maintains a strong presence through its boutiques in Paris London Milan and Stockholm as well as selective department store partnerships. The brand launched its “Les Essences” refillable candle system featuring reusable vessels and compostable wax inserts to align with circular economy principles. Diptyque enhanced its traceability platform by publishing full ingredient disclosure for all fragrances including allergen concentrations in compliance with EU regulatory expectations. Its integration of heritage craftsmanship with modern sustainability practices continues to define luxury standards in the global scented candle market.

Jo Malone London (Estée Lauder Companies)

Jo Malone London a subsidiary of the Estée Lauder Companies is a leading British brand known for its elegant and versatile scented candles that emphasize layering and seasonal storytelling. The brand operates in over fifty European markets through standalone stores online channels and premium retail partnerships. Jo Malone introduced its “Home for the Holidays” collection featuring recycled glass vessels and FSC certified packaging reinforcing its environmental commitments. The company also expanded its personalization service in key European cities allowing customers to engrave candle lids with bespoke messages. The brand launched a digital scent profiling tool on its European e commerce platform to enhance discovery and reduce return rates. By combining British aesthetic refinement with scalable luxury accessibility Jo Malone maintains a distinctive position in both mass premium and gifting segments across the continent.

Skandinavisk ApS

Skandinavisk ApS is a Danish Swedish brand that has become synonymous with Nordic minimalism and sustainable home fragrance across Europe. The company crafts scented candles using locally sourced rapeseed wax essential oils and reusable vessels inspired by Scandinavian landscapes and cultural concepts such as hygge and friluftsliv. Skandinavisk exports to over forty countries and is recognized for its transparent supply chain and carbon neutral certification. The brand launched its “Refill Circle” program in Germany France and the Netherlands enabling customers to return empty jars for sterilization and reuse. Skandinavisk introduced a new line of candles formulated with wild foraged botanicals from Nordic forests certified by the Nordic Ecolabel.

Top Strategies Used by the Key Market Participants

Key players in the Europe scented candles market focus on premiumization through storytelling heritage and sensory design while advancing sustainability via refillable systems biodegradable waxes and transparent ingredient disclosure. They invest in direct to consumer e commerce platforms with personalized scent recommendations and digital engagement tools. Strategic collaborations with interior designers and wellness experts enhance brand positioning beyond mere fragrance. Companies also align with EU regulatory frameworks by adopting allergen transparency and deforestation free sourcing. Additionally, they leverage seasonal and limited edition launches to drive urgency and gifting appeal across both physical and online retail channels.

MARKET SEGMENTATION

This research report on the europe scented candles market has been segmented and sub–segmented into the following categories.

By Category

- Mass

- Premium

By Material

- Blended Wax

- Paraffin Wax

- Soy Wax

- Others

By Distribution Channel

- Hypermarkets & Supermarkets

- Specialty Stores

- Online Stores

- Convenience Stores

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What are scented candles?

Scented candles are candles infused with fragrance oils or essential oils to provide aroma and enhance indoor ambiance.

What is driving the Europe scented candles market growth?

Growth is driven by rising demand for home décor products, wellness trends, stress relief solutions, and increased time spent indoors.

Which materials are commonly used in scented candles in Europe?

Common materials include paraffin wax, soy wax, blended wax, beeswax, and plant-based waxes.

What are the key applications of scented candles?

Scented candles are widely used for home décor, aromatherapy, relaxation, gifting, and hospitality settings.

Which countries dominate the Europe scented candles market?

Germany, France, the UK, Italy, and Spain are major contributors due to strong retail and lifestyle product demand.

How does sustainability impact the Europe scented candles market?

Sustainability drives demand for eco-friendly waxes, natural fragrances, recyclable packaging, and clean-burning candles.

What types of fragrances are popular in Europe?

Floral, vanilla, citrus, woody, herbal, and seasonal scents such as cinnamon and pine are highly popular.

Which category dominates the Europe scented candles market?

The mass segment dominates due to affordability, wide availability, and frequent household usage.

What is the fastest-growing segment in the market?

The premium scented candles segment is growing rapidly due to demand for luxury home fragrances and lifestyle branding.

What is the future outlook for the Europe scented candles market?

The market is expected to grow steadily, supported by wellness trends, sustainability focus, and premium product demand.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com