Europe Seed Market Size, Share, Trends, COVID-19 Impact & Growth Forecast Report, Segmented By Seed Trait, Crop Type and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

Europe Seed Market Size

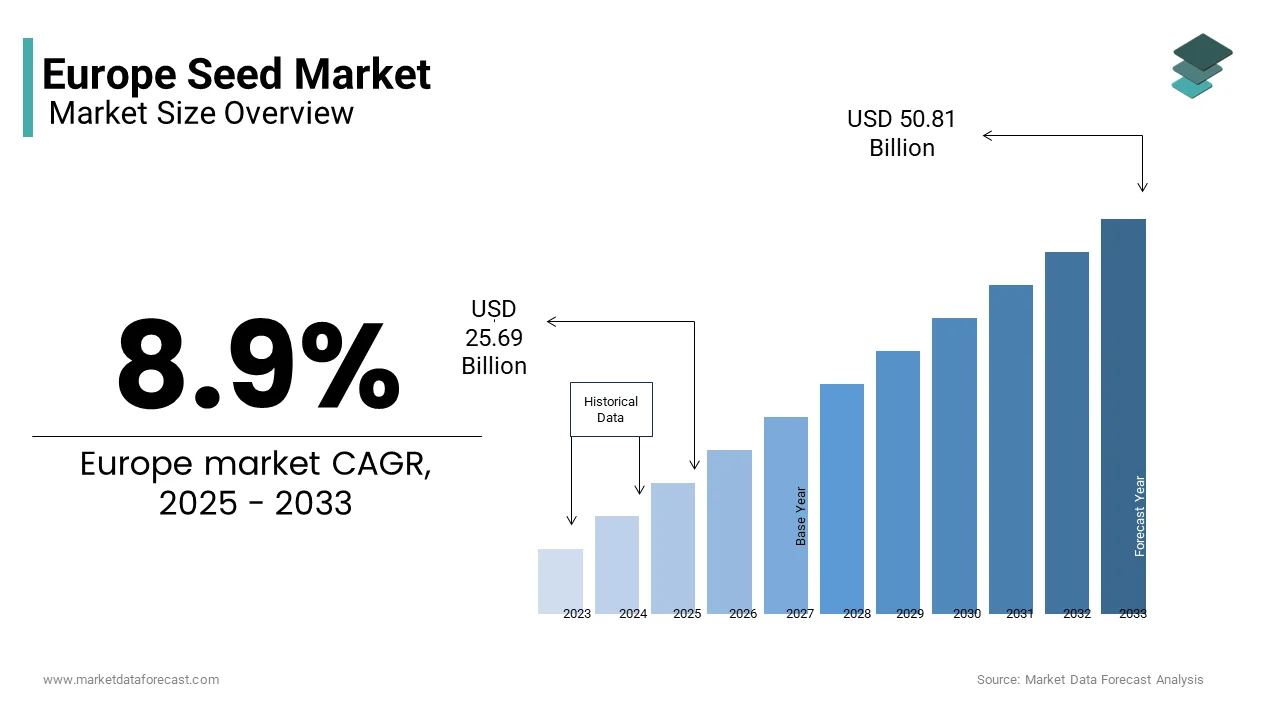

The European seed market was valued at USD 25.69 billion in 2025 and is anticipated to reach USD 27.98 billion in 2026, from USD 55.34 billion by 2034, growing at a compound annual growth rate (CAGR) of 8.9% during the forecast period from 2026 to 2034.

The seeds serve as the foundational input for food security, biodiversity conservation, and sustainable land management. Unlike commodity trading, the European seed sector operates under a highly regulated framework governed by the EU Common Catalogue of Varieties and national seed certification schemes that ensure genetic purity, germination viability, and phytosanitary safety. Furthermore, the European Commission’s Farm to Fork Strategy targets a 50 % reduction in chemical pesticide use by 2030, intensifying demand for resilient seed varieties with built-in tolerance to pests and climate stress.

MARKET DRIVERS

EU Policy Mandates for Sustainable Agriculture Drive Demand for Advanced Seed Varieties

The European Union’s binding sustainability directives for innovation and adoption of advanced seed technologies are one of the major factors propelling the growth of theEuropeane Seed Market. As per the European Commission’s Farm to Fork Strategy, the EU aims to reduce synthetic fertilizer use by 20 % and expand organic farming to 25% of agricultural land by 2030. According to the European Environment Agency, over 140,000 farms transitioned to organic certification between 2020 and 2023, which is creating acute demand for organically produced seeds compliant with Regulation (EU) 2018/848. Additionally, the EU’s Sustainable Use of Pesticides Regulation incentivizes genetic solutions over chemical interventions, accelerating breeding programs for fungal-resistant wheat and potato lines. Public research institutions like Wageningen University have partnered with seed companies to develop climate-resilient maize hybrids suitable for Southern Europe’s warming conditions.

Rising Consumer Demand for Diverse and Nutrient-Dense Crops Stimulates Specialty Seed Innovation

The dietary patterns are reshaping crop portfolios and fueling demand for specialty and nutrient-enhanced seed varieties, which will additionally enhance the growth of thEuropeanpe Seed Market. As per the European Food Information Council, over 68% of consumers in Western Europe now prioritize nutritional density and crop diversity when purchasing fresh produce, driving interest in heritage grains, leafy greens, and biofortified vegetables. Similarly, demand for plant-based proteins has spurred the development of high-yielding faba bean and lentil varieties; the French National Institute for Agricultural Research released three new protein-dense pea cultivars in 2023 with 25 % higher lysine content.

MARKET RESTRAINTS

Stringent GMO Regulations Limit Access to Advanced Breeding Technologies

The world’s most restrictive regulatory regimes for genetically modified organisms, which indirectly impede the adoption of next-generation breeding tools, are restraining the growth of the European seed market. As per Directive 2001/18/EC, any seed developed using transgenic techniques is subject to a decade-long approval process, with near-zero commercial cultivation permitted. Consequently, European farmers lack access to disease-resistant or climate-adaptive varieties widely available in North and South America. For instance, while CRISPR-edited wheat with improved mildew resistance is field tested in the United States, equivalent European trials remain confined to laboratories.

Fragmented National Seed Certification Systems Increase Compliance Costs

The significant disparities in national seed certification procedures create operational inefficiencies and elevate entry barriers for seed companies, which is solely degrading the growth of the European seed market. As per the European Commission’s 2023 evaluation of Regulation (EU) 2016/1039, 14 member states maintain additional national requirements beyond EU minimum standards for seed labeling, testing intervals, and field inspection protocols. In Germany, for example, cereal seed lots must undergo three separate germination tests before certification, whereas in Spain only two are required. These inconsistencies force multinational seed firms to maintain country-specific documentation and testing schedules, increasing administrative costs by an estimated 18%, according to the International Seed Federation.

MARKET OPPORTUNITIES

Expansion of Digital Seed Platforms Enhances Farmer Access and Traceability

The emergence of digital seed marketplaces and traceability systems to modernize seed distribution and strengthen farmer engagement is setting up new opportunities for the growth of the European seed market. As per the European Digital Agriculture Observatory, over 40 digital seed platforms were operational in 2023, connecting breeders directly with growers through mobile applications that provide variety recommendations, soil matching, and delivery tracking. Platforms like eSeed in France and Seed2Farm in the Netherlands integrate agronomic data from Copernicus satellites and national soil databases to suggest optimal seed choices based on real-time field conditions.

Revival of Agrobiodiversity Initiatives Creates Niche Markets for Heritage and Landrace Seeds

The policy-driven and consumer-led efforts to conserve agricultural biodiversity are unlocking commercial potential for heritage and landrace seed varieties, which will additionally elevate the growth of the European seed market. As per the European Commission’s Biodiversity Strategy for 2030, member states are required to establish gene banks and support on-farm conservation of traditional cultivars, many of which possess unique adaptations to local climates and soils. In Spain, the Catalan Institute of Agrifood Research released five revived heirloom wheat lines in 2023 tailored for artisanal bread making, with seed sales growing by 35 % annually. Seed saver networks like Kokopelli in France distribute over 2,000 open-pollinated varieties, supported by EU rural development funds.

MARKET CHALLENGES

Climate-Induced Yield Volatility Threatens Seed Production Stability

The seed production across Europe faces increasing disruption from climate extremes that compromise both quantity and quality of propagation material, which is more likely to pose a challenge for the growth of the European seed market. Even controlled environment seed multiplication is vulnerable; energy costs for climate-regulated greenhouses surged by 130 % in Germany between 2021 and 2022, per the German Farmers’ Association, which is forcing some producers to scale back operations.

Intellectual Property Enforcement Gaps Undermine Breeder Investment Returns

Weak enforcement of plant variety protection rights across parts of Europe discourages long-term investment in seed research and development, which will additionally inhibit the growth of the European seed market in the coming years. As per the Community Plant Variety Office, over 40 % of infringement complaints between 2020 and 2023 originated from Eastern and Southern member states, where unauthorized seed saving and resale remain prevalent. The EU’s Plant Reproduction Material Law permits limited farm saving for certain crops, but inconsistent national implementation creates loopholes exploited by informal seed traders. While the EU Plant Variety Rights system grants 25 to 30 years of protection, the collection of royalties relies on national authorities with varying capacity and political will.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 8.9% |

| Segments Covered | By Seed Trait, Crop Type, and Country Analysis |

| Various Analyses Covered | Global, Regional, and Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | Germany, UK, France, Italy, Spain |

| Market Leaders Profiled | Biochar Products Inc., Diacarbon Energy Inc., Agri-Tech Producers LLC, Genesis Industries, Green Charcoal International, Vega Biofuels Inc., The Biochar Company, Cool Planet Energy Systems Inc., Full Circle Biochar, and Pacific Pyrolysis Pty Ltd. |

SEGMENT ANALYSIS

By Seed Trait Insights

The herbicide-tolerant seeds segment accounted in holding 52.3% of thEuropeanpe seed market share in 2024, with the need for efficient weed control in large-scale arable farming, particularly in cereal and oilseed production systems, where labor scarcity and rising input costs necessitate chemical solutions. As per the French National Institute for Agricultural Research, over 85 % of sunflower acreage in France now uses imidazolinone-tolerant hybrids, reducing reliance on mechanical weeding and lowering fuel consumption by 18 % per hectare. National agronomic advisory services actively promote these varieties as part of integrated weed management strategies under the EU’s Sustainable Use of Pesticides Directive.

The “Other Stacked Traits” segment is projected to expand at a CAGR of 9.6 % throughout the forecast period with the EU’s Farm to Fork Strategy, which mandates simultaneous reductions in chemical inputs and yield volatility, compelling breeders to develop multi-trait solutions through advanced conventional methods. In Germany, KWS Saat developed a winter wheat line combining Fusarium head blight resistance with improved water use efficiency, now cultivated on over 120,000 hectares. Public funding under Horizon Europe has allocated 120 million euros since 2021 to multi-trait breeding consortia, accelerating commercialization.

By Crop Insights

The grain seeds segment was the largest and held 48.3% of thEuropeanpe seed market share in 2024, with the continent’s vast cereal production base, which includes whea barleyroatsy o, and rye cultivated across over 50 million hectares of arable land. Policy support further reinforces demand; the Common Agricultural Policy allocates direct payments to farmers who use officially registered varieties, incentivizing certified seed adoption.

The fruit and vegetable seed segment is expected to grow at a CAGR of 11.2% during the forecast period, with the rising consumer demand for fresh produce, urban agriculture trends, and policy support for dietary diversification. Protected cultivation is expanding rapidly; the Netherlands alone added 1,200 hectares of greenhouse vegetable area in 2022, requiring specialized grafted and hybrid seeds.

COUNTRY-LEVEL ANALYSIS

France Market Analysis

France's seed market held 23.2% of the share in 2024, with its status as the EU’s top cereal and oilseed producer and a global hub for seed research and breeding. According to the French Ministry of Agriculture, over 11 million hectares of land are dedicated to cereal cultivation, requiring more than 1.2 million tons of certified seed annually. France’s GEVES seed certification agency is one of the most active in Europe, registering over 500 new varieties in 2023 alone. The integration of public research institutions like INRAE with private breeders creates a robust innovation ecosystem, ensuring France remains the epicenter of European seed development and distribution.

Germany Market Analysis

Germany was ranked second by capturing 18.2% of thEuropeanpe seed market share in 2024 with its advanced agricultural technology adoption and stringent seed quality standards. As per the German Federal Office of Agriculture and Food, over 95 % of cereal and oilseed farmers use certified seeds, supported by mandatory documentation under the Seed Marketing Act. The country is a leader in winter crop breeding, with KWS Saat and Deutsche Saatveredelung developing high-yielding wheat and rye varieties adapted to Central European climates.

Italy Market Analysis

Italy's seed market growth is driven by the strong demand for vegetable, fruit, and durum wheat seeds aligned with its culinary and export agricultural identity. As per the Italian National Institute of Statistics, Italy is the EU’s largest producer of tomatoes and artichokes, requiring over 3,500 tons of specialized vegetable seed annually.

Spain Market Analysis

Spain's seed market growth is likely to grow with its extensive horticultural sector and adaptation to Mediterranean climate challenges. Spain also leads in sunflower seed production, with herbicide-tolerant hybrids covering 75 % of the 800,000-hectare crop as per the Spanish Oilseed Association.

COMPETITIVE LANDSCAPE

The European seed market features a competitive landscape shaped by a mix of large multinational corporations, cooperative breeders, and specialized regional players. Companies like Limagrain KWS and Bayer dominate through extensive research infrastructure, a broad crop portfolio, and deep integration with European agricultural policies. These firms leverage decades of breeding expertise and compliance with strict EU seed certification and phytosanitary regulations to maintain trust among farmers and regulators. Simultaneously, agile niche breeders focus on organic heritage and vegetable seed, catering to urban agriculture and gourmet markets. Competition intensifies around sustainability with firms racing to deliver multi-trait varieties that reduce chemical inputs and enhance climate resilience. Regulatory constraints on biotechnology limit the use of transgenic tools but spur innovation in advanced conventional breeding.

KEY MARKET PLAYERS

A few of the market players in theEuropeane seed market include

- Monsanto

- Syngenta

- Limagrain

- KWS SAAT SE & Co KGaA

- KWS

- Bayer CropScience

- DLF-Trifolium

Top Players in the Market

- Limagrain is a leading European agricultural cooperative headquartered in France with a strong global footprint in cereal, vegetable, and forage seed. The company operates through subsidiaries such as Vilmorin Mikado and LG Seed, delivering region-specific seed solutions across Europe, North America, and Africa. Limagrain emphasizes non-GM breeding and sustainable agriculture, aligning with EU regulatory standards. Recently, the company launched a portfolio of climate-resilient wheat and barley varieties developed using marker-assisted selection to address drought and heat stress in Southern Europe. It also expanded its digital seed advisory platform, offering farmers real-time agronomic recommendations based on soil and weather data.

- KWS SAAT is a German-based global seed company specializing in sugar beet cereals and oilseed crops with a significant presence across Europe and the Americas. The company is renowned for its advanced breeding programs in winter wheat, ry, and hybrid rye, leveraging genomic selection and digital phenotyping. KWS has strengthened its European position by introducing multi-trait seed varieties that combine disease resistance with nitrogen use efficiency, supporting the EU’s Farm to Fork objectives. In recent years, the company invested in automated seed processing facilities in Germany and Poland to enhance quality control and scalability. KWS also collaborates with universities on climate adaptation research and participates in EU-funded projects on sustainable intensification. Its commitment to conventional breeding and digital agriculture positions KWS as a key enabler of resilient European crop production.

- Bayer Crop Science, a division of Bayer AG, is a major player in the European seed market, offering a diverse portfolio of vegetable and field crop seeds under brands such as De Ruiter and Nunhems. The company integrates seed technology with digital farming tools through its Climate FieldView platform, enabling precision planting and performance tracking. Recently, the company launched biofortified tomato and pepper varieties rich in vitamins and antioxidants, targeting health-conscious consumers. Bayer also expanded its seed treatment offerings with biologicals to reduce chemical inputs.

Top Strategies Used by the Key Market Participants

Key players in thEuropeanpe seed market pursue several strategic approaches to maintain competitiveness and comply with regional regulations. They invest heavily in non-genetically modified breeding technologies such as marker-assisted selection and genomic prediction to develop climate-resilient and input-efficient varieties. Companies prioritize digital integration by offering seed selection platforms linked to soil weather and yield data, enhancing farmers ' decision-making. Strategic collaborations with public research institutions and participation in EU-funded agricultural projects accelerate innovation while ensuring policy alignment. Expansion of organic and low-input seed portfolios addresses the growing demand driven by the Farm to Fork Strategy. Additionally, firms strengthen supply chain reliability through localized seed production and advanced processing facilities to meet stringent EU certification standards and reduce import dependency.

MARKET SEGMENTATION

This research report on the European seed market has been segmented and sub-segmented into the following categories.

By Seed Trait

- Herbicide Tolerant

- Insect Resistant

- Other Stacked Traits

By Crop Type

- Oilseed

- Soybean

- Sunflower

- Cotton

- Canola

- Grain Seed

- Corn

- Wheat

- Rice

- Millet Crops

- Fruit & Vegetable

- Tomato

- Melon

- Carrot

- Onion

- Pepper

- Lettuce

- Other Seed

- Alfalfa

- Turf

- Clover & Forage Plants

- Flower Seed

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the expected value of the seed market in Europe in 2025?

The Europe seed market is predicted to be worth USD 25.69 billion in 2025.

What are the key challenges faced by the Europe seed market?

Concerns over genetic engineering, the need for large-scale investments in research and development, and addressing the complexities of international trade are some of the key challenges to the Europe seed market.

What are the future growth prospects and emerging trends in the Europe seed market?

The advancements in biotechnology, increased adoption of precision agriculture, and a continued focus on sustainable and climate-smart farming practices are some of the emerging trends in the Europe seed market.

What factors are driving growth in the Europe seed market?

Increasing demand for high-yield, climate-resilient, and disease-resistant crop varieties—alongside EU farm-to-fork sustainability goals—is accelerating innovation and adoption of advanced seeds across the region.

Which crops dominate the European seed market?

Cereals (wheat, barley, maize), oilseeds (rapeseed, sunflower), and vegetables (tomato, lettuce, carrot) lead in terms of volume and value, reflecting Europe’s diverse agricultural landscape and strong food processing sector.

How is the EU’s Green Deal affecting seed development?

The Farm to Fork Strategy aims to reduce chemical pesticides and promote organic farming, pushing breeders to develop non-GMO, organic-compliant, and biodiversity-enhancing seed varieties through conventional and new genomic techniques.

Are genetically modified (GM) seeds used in Europe?

GM seed cultivation remains highly restricted—only one GM maize variety (MON810) is approved in limited countries—making Europe one of the most regulated markets globally for biotech seeds.

What role does organic farming play in seed demand?

With the EU targeting 25% organic farmland by 2030, demand for certified organic seeds is rising, though supply gaps persist due to limited breeding programs and certification complexities.

Who are the leading seed companies in Europe?

Key players include Bayer (through its Crop Science division), BASF, Syngenta (part of ChemChina), KWS SAAT, and Limagrain—renowned for R&D in hybrid seeds, digital agronomy, and sustainable traits.

How is climate change influencing seed innovation?

Breeders are prioritizing drought tolerance, heat resistance, and early-maturing traits to help farmers adapt to erratic weather patterns, water scarcity, and shifting growing seasons across Southern and Eastern Europe.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com