Europe Selective Laser Sintering Market Size, Share, Trends, and Growth Forecasts Research Report, Segmented By Material, Application, Industry and Country – Industry Analysis (2026 to 2034)

Europe Selective Laser Sintering Market Report Summary

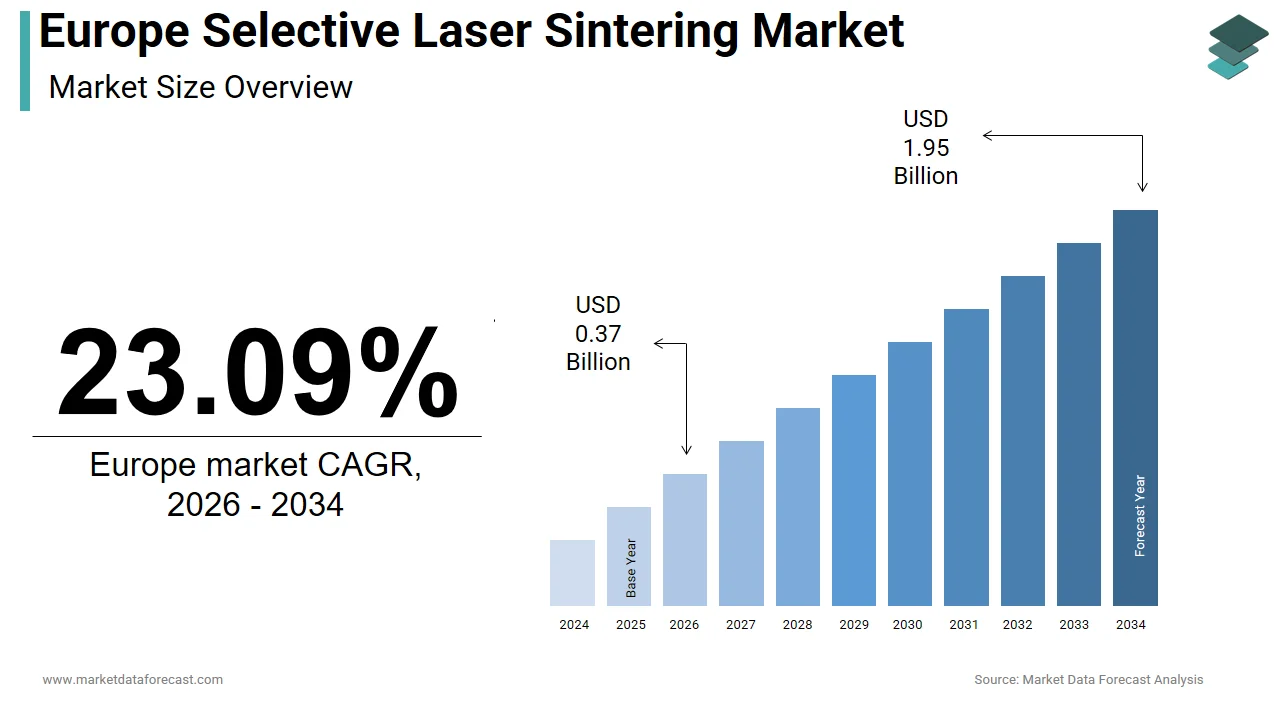

The Europe selective laser sintering (SLS) market was valued at USD 0.30 billion in 2025, is estimated to reach USD 0.37 billion in 2026, and is projected to reach USD 1.95 billion by 2034, growing at a CAGR of 23.09% from 2026 to 2034. Market growth is driven by the rapid adoption of additive manufacturing technologies across industries such as automotive, aerospace, and healthcare. SLS enables the production of complex, lightweight, and high-performance components, making it a preferred solution for prototyping and end-use manufacturing. Increasing investments in industrial automation, digital manufacturing, and sustainable production processes are further accelerating market expansion across Europe.

Key Market Trends

- Rising adoption of additive manufacturing and 3D printing technologies.

- Increasing demand for lightweight and complex component production.

- Growth in automotive and aerospace applications.

- Expansion of rapid prototyping and on-demand manufacturing.

- Advancements in materials and printing technologies.

Segmental Insights

- Based on material, the nylon segment dominated the Europe SLS market by capturing 64.3% share in 2025, driven by its durability, flexibility, and cost-effectiveness.

- Based on application, the tooling segment led the market with 41.6% share in 2025, supported by demand for rapid prototyping and manufacturing tools.

- Based on industry, the automotive segment held the largest share of 34.3% in 2025, driven by the need for lightweight components and design flexibility.

Regional Insights

The Europe SLS market is witnessing strong growth across leading industrial economies.

- Germany is expected to maintain its leadership position, supported by strong investments in industrial automation and engineering excellence.

- The United Kingdom is poised to strengthen its presence through advanced research capabilities and focus on high-value manufacturing.

- France is projected to grow steadily due to investments in industrial modernization and sustainable transport solutions.

Competitive Landscape

The Europe selective laser sintering market is highly competitive, with companies focusing on technological innovation, material development, and expanding industrial applications. Strategic partnerships and investments in advanced manufacturing technologies are key competitive strategies.

Prominent companies operating in the Europe selective laser sintering market include 3D Systems Corporation, EOS GmbH, Farsoon Technologies, SLM Solutions Group AG, Prodways Group, Formlabs Inc., Sinterit Sp. z o.o., Renishaw Plc, Materialise NV, Sintratec AG, Sharebot S.r.l., and Ricoh Company Ltd.

Europe Selective Laser Sintering Market Size

The Europe selective laser sintering market was valued at USD 0.30 billion in 2025, is estimated to reach USD 0.37 billion in 2026, and is projected to reach USD 1.95 billion by 2034, growing at a CAGR of 23.09% from 2026 to 2034.

The Europe selective laser sintering market is poised for steady expansion over the next several years as industrial sectors increasingly prioritize additive manufacturing for complex production needs. This technology is distinct for its ability to produce complex geometries without the need for support structures, making it indispensable for aerospace, automotive, and healthcare applications. The region serves as a global hub for industrial innovation driven by strong engineering traditions and rigorous quality standards. According to Eurostat, the manufacturing sector accounted for approximately 15% of the European Union's gross value added in 2023, indicating the economic importance of advanced production techniques. As per a report by the European Commission, investment in research and development within the manufacturing sector increased by 8% year on year, reflecting a strategic shift towards digitalization and automation. The adoption of Industry 4.0 principles has accelerated the integration of selective laser sintering into mainstream production lines. According to the Fraunhofer Institute, over 60% of German manufacturing companies have implemented at least one additive manufacturing technology in their processes. The regulatory environment under the European Green Deal also promotes sustainable manufacturing practices, encouraging the use of materials that minimize waste. This technological landscape positions selective laser sintering as a critical enabler of lightweighting and customization trends across key European industries.

MARKET DRIVERS

Aerospace Industry Demand for Lightweight and Complex Components

The European aerospace sector is expected to remain a dominant force in driving selective laser sintering adoption as manufacturers seek to meet aggressive sustainability and weight-reduction targets. Selective laser sintering allows for the creation of intricate lattice structures and consolidated parts that significantly reduce component weight without compromising structural integrity. As per the European Aviation Safety Agency, the aviation industry aims to reduce carbon emissions by 50% by 2050 compared to 2005 levels, driving the adoption of lightweight materials. Airbus and other major manufacturers utilize selective laser sintering to produce bracketry, ducting, and interior components that are up to 40% lighter than traditionally manufactured counterparts. According to the Aerospace Technology Institute, investments in advanced manufacturing technologies in the UK alone exceeded 1 billion pounds in 2023 to support sustainable flight initiatives. The ability to consolidate multiple parts into single units reduces assembly time and potential failure points enhancing overall aircraft reliability. Furthermore, the technology enables rapid prototyping of new designs accelerating the development cycle for next generation aircraft. The European Union’s Clean Sky Joint Undertaking further supports these efforts by funding projects that integrate additive manufacturing into aero engine and airframe production. This sustained focus on efficiency and sustainability ensures consistent demand for selective laser sintering services and equipment within the European aerospace supply chain.

Automotive Sector Transition Towards Electric Vehicle Production

The European automotive industry is likely to witness sustained demand for selective laser sintering as the transition toward electric vehicle production intensifies over the next few years, which is another key market driver. Electric vehicles require lightweight components to offset the heavy weight of battery packs, thereby extending driving range and improving energy efficiency. Selective laser sintering facilitates the production of complex heat exchangers, battery housings, and custom interior parts that are difficult to achieve with traditional subtractive methods. As per the European Automobile Manufacturers Association, electric car sales in the EU reached 2.3 million units in 2023, representing a substantial share of the total market. Major automakers such as BMW and Volkswagen have integrated selective laser sintering into their production lines to create functional prototypes and end-use parts. According to the International Energy Agency, the push for electrification requires a 30% reduction in vehicle body weight to maintain performance standards. This technology allows for the use of high-performance polymers and metal alloys that offer superior strength-to-weight ratios. Additionally, the flexibility of selective laser sintering supports mass customization, enabling manufacturers to offer personalized vehicle features without significant tooling costs. The European Commission’s alternative fuels infrastructure regulation further incentivizes the adoption of efficient manufacturing processes to meet stringent emission targets. Consequently, the automotive sector’s evolution towards electrification and customization drives robust growth in the selective laser sintering market.

MARKET RESTRAINTS

High Initial Investment and Operational Costs

The substantial initial investment required for selective laser sintering equipment and the high operational costs associated with material handling pose significant restraints to market expansion in Europe. Industrial-grade selective laser sintering machines often cost between 200,000 and 1 million euros, depending on build volume and laser capabilities, which creates a high barrier to entry for small and medium-sized enterprises. As per a study by the European Investment Bank, access to finance for capital-intensive technologies remains a challenge for 20% of manufacturing firms, particularly those lacking extensive collateral. Furthermore, the cost of specialized powders such as polyamide 12 and metal alloys is significantly higher than traditional raw materials due to limited suppliers and strict quality control requirements. According to the Fraunhofer Institute, material costs can account for up to 50% of the total production expense in additive manufacturing processes. The need for controlled environments, including inert gas atmospheres and precise temperature regulation, further increases energy consumption and operational overheads. Post-processing steps such as powder removal, surface finishing, and heat treatment add additional labor and equipment costs. These financial burdens discourage widespread adoption, particularly among smaller manufacturers who operate on thin margins. Although long-term benefits exist, the upfront capital expenditure and ongoing operational expenses limit the speed at which selective laser sintering can be integrated into broader European manufacturing bases.

Limited Material Availability and Standardization Issues

The limited availability of qualified materials and the lack of standardized certification protocols are further impeding the expansion of the Europe selective laser sintering market. While the range of printable materials is expanding, it remains narrow compared to traditional manufacturing options, restricting the applicability of the technology in certain high-performance sectors. As per the European Committee for Standardization, there are currently fewer than 20 internationally recognized standards for additive manufacturing materials, leading to inconsistencies in quality and performance verification. This lack of standardization complicates the qualification process for critical applications in aerospace and medical devices, where regulatory approval is mandatory. According to the European Medicines Agency, the validation of additively manufactured medical implants requires extensive clinical data, which is costly and time-consuming to generate. Furthermore, the dependency on proprietary powder formulations from specific machine manufacturers creates vendor lock-in situations, limiting competition and keeping prices elevated. The recycling of unused powder is also constrained by degradation issues, which affect mechanical properties after multiple uses. According to a study by the University of Cambridge, powder reuse rates are limited to five to ten cycles before quality deteriorates significantly. These material constraints and regulatory hurdles slow down the adoption rate and limit the scalability of selective laser sintering operations across diverse European industries.

MARKET OPPORTUNITIES

Expansion into Medical and Dental Applications

The medical and dental sectors in Europe are set to provide significant opportunities for selective laser sintering as personalized healthcare solutions become the standard over the coming years. The technology enables the production of custom surgical guides, implants, and prosthetics that match individual anatomical structures, improving surgical outcomes and patient comfort. As per the European Federation of National Associations of Orthopaedics and Traumatology, the number of joint replacement surgeries in Europe is expected to increase by 25% by 2030 due to an aging population. Selective laser sintering allows for the creation of porous titanium implants that promote osseointegration, reducing recovery times and rejection risks. According to the European Society for Biomaterials, the market for additive-manufactured medical devices is growing at a rate of 15% annually. In dentistry, the technology is widely used for producing crowns, bridges, and aligner molds with high precision and efficiency. The European General Data Protection Regulation facilitates the secure handling of patient data required for custom design workflows. Furthermore, reimbursement policies in countries like Germany and France are increasingly covering additively manufactured medical devices, encouraging hospital adoption. The ability to produce complex geometries that mimic natural bone structures offers a competitive advantage over traditional casting methods. This convergence of demographic trends, technological capability, and regulatory support creates a fertile ground for selective laser sintering advancements in the European healthcare sector.

Integration with Industry 4.0 and Digital Manufacturing Ecosystems

Integration with Industry 4.0 technologies is expected to drive higher operational efficiency and process reliability for European manufacturers in the near future, which is another potential opportunity for the European selective laser sintering market. By connecting selective laser sintering machines to Internet of Things platforms, manufacturers can monitor production parameters in real time, predict maintenance needs, and optimize build schedules remotely. As per the European Commission’s Digital Decade policy programme, 75% of European companies are expected to adopt cloud computing and artificial intelligence by 2030, facilitating smarter manufacturing processes. Digital twins allow for the simulation of sintering processes before physical production, reducing material waste and improving first-time yield rates. According to the Platform Industry 4.0, connected factories can achieve productivity gains of up to 20% through data-driven decision-making. The use of blockchain technology ensures traceability of materials and processes, which is crucial for quality assurance in regulated industries. Furthermore, automated powder handling systems integrated with robotic arms streamline post-processing tasks, reducing manual labor and exposure to hazardous materials. The European Union’s Horizon Europe program funds projects that develop interoperable standards for digital manufacturing, fostering collaboration across borders. This digital transformation enhances the competitiveness of European manufacturers by enabling flexible, responsive, and efficient production models. Consequently, the synergy between selective laser sintering and digital technologies unlocks new value propositions and operational efficiencies.

MARKET CHALLENGES

Stringent Environmental and Safety Regulations

Stringent environmental and safety regulations regarding powder handling and emissions is a major challenge to the Europe selective laser sintering market. The fine particles used in the process pose respiratory hazards, requiring specialized ventilation systems and personal protective equipment to ensure worker safety. As per the European Agency for Safety and Health at Work, exposure to ultrafine particles is a recognized occupational risk necessitating strict adherence to workplace safety directives. Compliance with the Registration, Evaluation, Authorisation, and Restriction of Chemicals regulation adds complexity to the sourcing and disposal of polymer powders and chemical agents. According to the European Environment Agency, industrial facilities must implement rigorous waste management protocols to prevent environmental contamination from unused powders and support materials. The energy intensity of the sintering process also faces scrutiny under the European Green Deal, which mandates reductions in industrial carbon footprints. Manufacturers must invest in energy-efficient machines and renewable energy sources to meet these sustainability targets. Furthermore, the transport of hazardous materials is subject to strict logistical regulations, increasing supply chain costs. Non-compliance can result in severe fines and operational shutdowns, posing significant financial risks. These regulatory pressures require continuous investment in safety infrastructure and environmental monitoring systems, challenging the profitability and operational flexibility of selective laser sintering providers in Europe.

Skilled Labor Shortage and Technical Expertise Gap

The shortage of skilled labor is likely to remain a primary bottleneck for European companies looking to scale their selective laser sintering capabilities in the next few years, which is further challenging the expansion of the European selective laser sintering market. Operating these complex machines requires specialized knowledge in materials science, computer-aided design, and process optimization, which is not widely available in the current workforce. As per the European Centre for the Development of Vocational Training, there is a projected deficit of 1.2 million digital specialists in the EU by 2025, affecting advanced manufacturing sectors disproportionately. The learning curve for mastering selective laser sintering parameters such as laser power, scan speed, and layer thickness is steep, requiring extensive training and experience. According to the German Engineering Federation, 45% of manufacturing companies report difficulties in finding qualified personnel for additive manufacturing roles. This skills gap leads to suboptimal machine utilization, increased error rates, and longer production cycles. Educational institutions are struggling to keep pace with technological advancements, resulting in a mismatch between graduate skills and industry needs. Furthermore, the retention of trained employees is challenging due to high demand and competitive salaries. Companies must invest heavily in internal training programs and partnerships with universities to bridge this gap. Until the workforce pipeline is strengthened, the lack of technical expertise will remain a bottleneck for the widespread adoption and efficient operation of selective laser sintering technologies in Europe.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Material, Application, Industry, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled |

|

SEGMENTAL ANALYSIS

By Material Insights

The nylon segment dominated the market by accounting for 64.3% of the European market share in 2025. The dominance of the nylon segment in the European market is primarily driven by the exceptional mechanical properties, chemical resistance, and cost-effectiveness of polyamide powders, particularly PA12 and PA11. Nylon offers an ideal balance of strength, flexibility, and durability, making it suitable for a wide range of applications from functional prototypes to end use parts. As per the European Plastics Converters association, polyamide based materials represent the most widely used polymers in industrial additive manufacturing due to their established processing parameters and reliable performance. The automotive sector extensively utilizes nylon for producing under the hood components, interior trim, and ducting systems which require heat resistance and structural integrity. According to a study by the Fraunhofer Institute for Laser Technology, nylon parts produced via selective laser sintering exhibit isotropic properties that are comparable to injection molded parts but with greater design freedom. The availability of recycled nylon powders also supports sustainability goals which are critical in the European market. Furthermore, the mature supply chain for nylon powders ensures consistent quality and competitive pricing compared to specialized engineering plastics. This combination of performance, reliability, and economic viability solidifies nylon as the cornerstone material for selective laser sintering operations across Europe.

However, the metal segment is on the rise and is estimated to grow at a promising CAGR of 19.4% over the forecast period in the European selective laser sintering market due to the increasing demand for high performance lightweight components in the aerospace and automotive industries. Selective laser sintering of metals such as titanium, aluminum, and steel enables the production of complex geometries that are impossible to achieve with traditional manufacturing methods. As per the European Aviation Safety Agency, the aerospace industry is aggressively adopting metal additive manufacturing to reduce aircraft weight and improve fuel efficiency with some components being up to 50% lighter than conventional counterparts. Airbus and Boeing have integrated metal sintered parts into their latest aircraft models driving significant demand for qualified metal powders. In the automotive sector, the shift towards electric vehicles necessitates lightweight battery housings and motor components to extend range. According to the European Automobile Manufacturers Association, investment in metal additive manufacturing technologies by European automakers increased by 25% in 2023. The ability to consolidate multiple metal parts into single units reduces assembly time and improves structural integrity. Furthermore, the development of new metal alloys with enhanced thermal and mechanical properties expands the potential applications of selective laser sintering. This strong industrial pull from high value sectors accelerates the adoption of metal materials in the European market.

By Application Insights

The tooling segment accounted for 41.6% of the European market share in 2025. The growth of the tooling segment in the European market can be credited to the ability of selective laser sintering to produce complex molds, jigs, fixtures, and patterns rapidly and cost effectively. Traditional tooling methods often involve lengthy lead times and high costs associated with machining and casting whereas additive manufacturing allows for direct digital fabrication. As per the European Tool and Mold Makers Association, the adoption of additive manufacturing for tooling has reduced lead times by up to 70% enabling faster product launches. Automotive and aerospace companies extensively use sintered tools for assembly line fixtures and inspection gauges which require high precision and durability. According to BMW Group, the use of selective laser sintered tools in their production facilities has improved ergonomic conditions for workers and increased operational efficiency. The technology allows for the integration of conformal cooling channels in injection molds which enhances cycle times and part quality. This capability is particularly valuable in high volume manufacturing where even small reductions in cycle time result in significant cost savings. Furthermore, the design freedom offered by selective laser sintering enables the creation of lightweight tools that are easier to handle and install. These operational benefits make tooling the primary application area for selective laser sintering in Europe.

On the other hand, the robotics segment is expected to grow at the fastest CAGR of 21.6% over the forecast period in the European market owing to the increasing demand for lightweight and customized components in automated systems. Selective laser sintering allows for the production of complex robotic parts such as grippers, joints, and housing structures with optimized geometry that reduces weight and improves dynamic performance. As per the International Federation of Robotics, sales of industrial robots in Europe increased by 10% in 2023 with a growing emphasis on collaborative robots that operate alongside humans. Lightweight components are essential for collaborative robots to ensure safety and energy efficiency. According to KUKA, a leading robotics manufacturer, the use of additive manufactured parts has reduced the weight of robotic arms by up to 30% enhancing their payload capacity and speed. The ability to customize grippers for specific tasks without expensive tooling makes selective laser sintering ideal for flexible manufacturing environments. Furthermore, the integration of sensors and wiring within printed structures simplifies assembly and improves reliability. The European Union’s strategy for digital transformation encourages the adoption of advanced robotics in manufacturing, logistics, and healthcare. This policy support combined with technological advantages drives the rapid adoption of selective laser sintered components in the robotics sector.

By Industry Insights

The automotive segment led the market by accounting for 34.3% of the European market share in 2025. The dominance of automotive segment in the European market is driven by the sector’s intense focus on vehicle lightweighting to improve fuel efficiency and meet stringent emission regulations. Selective laser sintering enables the production of complex lightweight components such as air ducts, brackets, and interior parts that reduce overall vehicle weight. As per the European Automobile Manufacturers Association, the average weight of electric vehicles is significantly higher than conventional cars necessitating aggressive lightweighting strategies for other components. Major automakers like BMW, Volkswagen, and Mercedes Benz have integrated selective laser sintering into their production workflows for both prototyping and end use parts. According to BMW Group, the use of additive manufacturing has allowed for the production of over 1 million parts annually demonstrating scalability. The technology also supports mass customization allowing customers to personalize interior elements and accessories without disrupting production lines. The ability to produce tools and fixtures in house further enhances manufacturing efficiency and reduces lead times. The automotive sector’s large volume and continuous innovation cycle create sustained demand for selective laser sintering services. This strategic alignment with industry goals solidifies the automotive sector as the primary driver of the European selective laser sintering market.

However, the medical devices segment is anticipated to register a CAGR of 21.2% over the forecast period in the European market owing to the increasing demand for personalized implants and surgical solutions. Selective laser sintering enables the production of patient specific implants that match individual anatomical structures, improving surgical outcomes and recovery times. As per the European Federation of National Associations of Orthopaedics and Traumatology, the number of joint replacement surgeries is rising due to an aging population creating a strong demand for customized orthopedic implants. Titanium and polymer implants produced via selective laser sintering offer superior biocompatibility and osseointegration properties. According to the European Society for Biomaterials, additive manufactured implants show significantly better long term stability compared to traditional devices. The technology also facilitates the production of complex surgical guides and instruments that enhance precision during procedures. Regulatory frameworks in Europe are evolving to support the approval of personalized medical devices with the European Medicines Agency providing clearer guidelines for additive manufacturing. This regulatory clarity encourages investment and innovation in the sector. Furthermore, the ability to produce small batches of specialized devices cost effectively makes selective laser sintering ideal for niche medical applications. The combination of demographic trends, technological capabilities, and regulatory support drives the rapid expansion of the medical devices segment.

COUNTRY LEVEL ANALYSIS

Germany Selective Laser Sintering Market Analysis

Germany is expected to maintain its leadership position in the Europe selective laser sintering market for the foreseeable future, supported by continuous investment in industrial automation and advanced engineering. The country is home to leading machine manufacturers and material suppliers who drive innovation in additive manufacturing. As per the German Engineering Federation, the adoption of additive manufacturing technologies in German industry has grown by 15% annually. The presence of major automotive companies such as BMW, Volkswagen, and Daimler creates substantial demand for lightweight and customized components. Germany’s Fraunhofer Institute is a global leader in additive manufacturing research providing critical expertise and development support. The government’s High Tech Strategy 2025 prioritizes digital manufacturing and Industry 4.0 initiatives fostering a conducive environment for technology adoption. According to the Federal Ministry for Economic Affairs and Climate Action, significant funding is allocated to research and development in advanced production technologies. The strong vocational training system ensures a skilled workforce capable of operating and maintaining selective laser sintering equipment. Furthermore, the country’s central location in Europe facilitates efficient distribution and service networks. This combination of industrial strength, technological leadership, and supportive policy positions Germany as the dominant market for selective laser sintering in Europe.

United Kingdom Selective Laser Sintering Market Analysis

The United Kingdom is poised to strengthen its market presence over the coming years by leveraging its advanced research capabilities and focus on high value manufacturing. The UK is home to major aerospace manufacturers such as Rolls Royce and BAE Systems which extensively utilize selective laser sintering for engine components and structural parts. As per the Aerospace Technology Institute, investment in additive manufacturing technologies in the UK exceeds 500 million pounds supporting innovation and commercialization. The presence of leading universities and research centers such as the University of Sheffield’s Advanced Manufacturing Research Centre drives technological advancements. The government’s Industrial Strategy includes specific provisions for promoting advanced manufacturing and digital technologies. According to Make UK, the manufacturing sector is increasingly adopting additive manufacturing to enhance competitiveness and sustainability. The UK’s strong intellectual property framework encourages innovation and attracts international investment. Furthermore, the National Health Service is exploring the use of additive manufacturing for personalized medical devices creating new market opportunities. The country’s focus on high value manufacturing and research excellence sustains its prominent role in the European selective laser sintering landscape.

France Selective Laser Sintering Market Analysis

France is projected to see steady growth in its selective laser sintering market as the country continues to invest heavily in industrial modernization and sustainable transport solutions. Companies such as Airbus, Safran, and Renault are key adopters of selective laser sintering technologies for producing lightweight and complex components. As per the French Ministry of Economy, the France 2030 investment plan allocates significant funds to advanced manufacturing and digital technologies. The presence of specialized research institutions such as the Institut Carnot supports the development of new materials and processes. According to the Union des Industries et Métiers de la Métallurgie, the adoption of additive manufacturing in the French metallurgical sector is accelerating. The country’s focus on sustainability and carbon neutrality drives the demand for lightweighting solutions in transportation. Furthermore, the healthcare sector is increasingly utilizing additive manufacturing for prosthetics and surgical instruments. The French government’s support for startups and innovation clusters fosters a dynamic ecosystem for additive manufacturing. This combination of industrial demand, policy support, and research capability drives the growth of the selective laser sintering market in France.

Italy Selective Laser Sintering Market Analysis

Italy is expected to experience continued development in its selective laser sintering market by capitalizing on its strong reputation for luxury goods and high-end automotive engineering. The country is known for its design excellence and manufacturing prowess particularly in the production of high performance vehicles and fashion accessories. As per the Italian National Institute of Statistics, the manufacturing sector contributes significantly to the national economy with a growing emphasis on digital transformation. Companies such as Ferrari and Lamborghini utilize selective laser sintering for prototyping and producing custom components. The footwear and eyewear industries also adopt the technology for mass customization and rapid product development. According to Confindustria, the main association representing manufacturing and service companies, there is increasing investment in Industry 4.0 technologies. The government’s National Recovery and Resilience Plan includes provisions for digital innovation and sustainable manufacturing. Furthermore, the presence of specialized machine builders and material suppliers supports the local ecosystem. The focus on high quality and customized production aligns well with the capabilities of selective laser sintering. This industrial structure and policy support sustain the growth of the market in Italy.

Sweden Selective Laser Sintering Market Analysis

Sweden is likely to see increased adoption of selective laser sintering as its industrial giants continue to prioritize circular economy principles and digitalized production. The country is home to major industrial companies such as Volvo and Scania which are early adopters of additive manufacturing for lightweighting and efficiency improvements. As per Statistics Sweden, the manufacturing industry is a key driver of economic growth with significant investment in research and development. The Swedish government’s innovation agency Vinnova supports projects focused on sustainable production and digitalization. According to the Swedish Association of Mechanical Engineering, the adoption of additive manufacturing is increasing particularly in the automotive and aerospace sectors. The country’s strong environmental regulations encourage the use of technologies that reduce material waste and energy consumption. Furthermore, the healthcare sector is exploring additive manufacturing for personalized medical devices. The presence of leading universities and research institutes fosters collaboration and innovation. Sweden’s focus on sustainability and technological advancement positions it as a key player in the European selective laser sintering market.

COMPETITIVE LANDSCAPE

The competition in the Europe selective laser sintering market is intense and characterized by the presence of established global manufacturers alongside innovative regional specialists. Major players leverage their technological expertise and extensive product portfolios to dominate the landscape while niche firms compete on specialized materials and customized services. The market exhibits high barriers to entry due to the significant investment required for research and development and proprietary technology protection. Companies differentiate themselves through machine performance material quality and software capabilities. Strategic collaborations with end users in aerospace automotive and medical sectors are common as they seek to validate applications and accelerate adoption. The emphasis on sustainability and circular economy principles drives competition in eco friendly materials and energy efficient processes. Intellectual property rights play a crucial role in maintaining competitive advantages leading to ongoing innovation in laser technology and powder formulations. Price competition is moderate as customers prioritize quality and reliability over cost for critical industrial applications. Service and support capabilities are key differentiators with companies investing in local teams to ensure rapid response times. This dynamic environment fosters continuous improvement and technological advancement benefiting the broader additive manufacturing ecosystem in Europe.

X`KEY MARKET PLAYERS

The leading companies operating in the Europe selective laser sintering market include:

- 3D Systems Corporation

- EOS GmbH

- Farsoon Technologies

- SLM Solutions Group AG

- Prodways Group

- Forlabs Inc.

- Sinterit sp z.o.o.

- Renishaw Plc

- Materialise NV

- Sintratec AG

- Sharebot S.r.l.

- Ricoh Company Ltd.

TOP PLAYERS IN THE MARKET

- EOS GmbH is a global technology leader in industrial additive manufacturing with its headquarters located in Germany. The company specializes in selective laser sintering systems for polymers and metals serving diverse industries such as aerospace automotive and healthcare. EOS recently expanded its material portfolio by introducing new high performance polyamide powders that enhance part durability and surface quality. The company also launched updated software solutions to streamline workflow integration and improve process reliability for industrial users. EOS continues to invest in research and development to advance laser technology and build chamber capabilities. Its strong focus on sustainability includes initiatives to reduce energy consumption and promote powder recycling. By maintaining rigorous quality standards and offering comprehensive customer support EOS strengthens its position as a trusted partner for industrial additive manufacturing. These strategic actions reinforce its commitment to innovation and operational excellence in the European and global markets.

- SLM Solutions Group AG is a prominent provider of metal additive manufacturing solutions based in Germany with a significant presence in the selective laser sintering sector. The company offers advanced systems for producing complex metal components used in aerospace energy and medical applications. SLM Solutions recently enhanced its machine connectivity features to support Industry 4.0 requirements enabling real time monitoring and data analysis. The company also expanded its service network across Europe to provide faster technical support and training to customers. SLM Solutions focuses on developing open material platforms that allow users to choose from a wide range of qualified powders. This flexibility attracts manufacturers seeking cost effective and versatile production options. The company collaborates with research institutions to drive innovation in metal processing technologies. By prioritizing customer centric innovations and robust service infrastructure SLM Solutions solidifies its reputation as a key player in the European additive manufacturing landscape.

- Materialise NV is a leading software and additive manufacturing service provider headquartered in Belgium with extensive expertise in selective laser sintering. The company offers comprehensive software suites that optimize build preparation nesting and support generation for various additive technologies. Materialise recently updated its Magics software platform with enhanced algorithms for improved part quality and reduced material waste. The company also expanded its manufacturing facilities in Europe to increase production capacity for polymer and metal parts. Materialise focuses on delivering end to end solutions including design consulting prototyping and serial production. Its strong emphasis on regulatory compliance supports clients in medical and aerospace sectors who require certified processes. The company actively participates in industry consortia to establish standards for additive manufacturing. By combining advanced software tools with high quality manufacturing services Materialise strengthens its market position and drives the adoption of selective laser sintering technologies across Europe.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe selective laser sintering market primarily focus on expanding their material portfolios to include high performance polymers and specialized metal alloys. Companies invest heavily in research and development to enhance machine precision speed and reliability for industrial applications. Strategic partnerships with automotive and aerospace manufacturers facilitate the integration of additive manufacturing into serial production lines. Firms emphasize software integration to streamline workflows and enable seamless data exchange between design and production stages. Sustainability initiatives such as powder recycling programs and energy efficient machines are prioritized to meet environmental regulations. Expansion of service networks ensures timely technical support and maintenance for customers across the region. Training and certification programs are launched to address the skilled labor shortage and promote best practices. These multifaceted strategies enable companies to maintain competitive advantages and drive widespread adoption of selective laser sintering technologies in the European industrial sector.

MARKET SEGMENTATION

This research report on the Europe selective laser sintering market has been segmented and sub-segmented into the following categories.

By Material

- Metal

- Nylon

By Application

- Tooling

- Heavy Equipment & Machinery

- Robotics

By Industry

- Consumer Goods

- Automotive

- Medical Devices

- Aerospace & Aeronautics

- Others

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is the Europe selective laser sintering market?

The Europe selective laser sintering market uses laser technology to fuse polymer powders for 3D printing complex parts in prototyping and low-volume production.

How does the Europe selective laser sintering market function?

The Europe selective laser sintering market works by selectively sintering powder layers with lasers to create functional prototypes and end-use components.

What drives growth in the Europe selective laser sintering market?

The Europe selective laser sintering market grows due to Industry 4.0 adoption, automotive prototyping, aerospace lightweighting, and sustainable manufacturing initiatives.

Which countries lead the Europe selective laser sintering market?

Germany leads the Europe selective laser sintering market, followed by the UK and France, supported by strong manufacturing bases and R&D investment.

What materials define the Europe selective laser sintering market?

The Europe selective laser sintering market primarily uses nylon powders, polyamides, and engineering polymers suited for functional prototyping and production parts.

What applications shape the Europe selective laser sintering market?

The Europe selective laser sintering market serves automotive, aerospace, consumer goods, medical devices, and tooling applications requiring complex geometries.

How does regulation influence the Europe selective laser sintering market?

EU manufacturing standards and sustainability regulations shape the Europe selective laser sintering market by promoting powder recyclability and emission controls.

What trends affect the Europe selective laser sintering market?

The Europe selective laser sintering market sees growth in multi-material printing, faster build speeds, automated powder handling, and Industry 4.0 integration.

What challenges face the Europe selective laser sintering market?

The Europe selective laser sintering market faces high equipment costs, powder recyclability limits, surface finish requirements, and skilled operator shortages.

How does automotive fit the Europe selective laser sintering market?

Automotive prototyping drives the Europe selective laser sintering market through rapid tooling, lightweight components, and functional testing parts.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com