Europe Semiconductor Intellectual Property Market Size, Share, Trends & Growth Forecast Report By IP Source, By Design IP, By Vertical, and By Country (Germany, United Kingdom, France, Italy, Netherlands & Rest of Europe) – Industry Analysis and Forecast, 2026 to 2034

Europe Semiconductor Intellectual Property Market Size

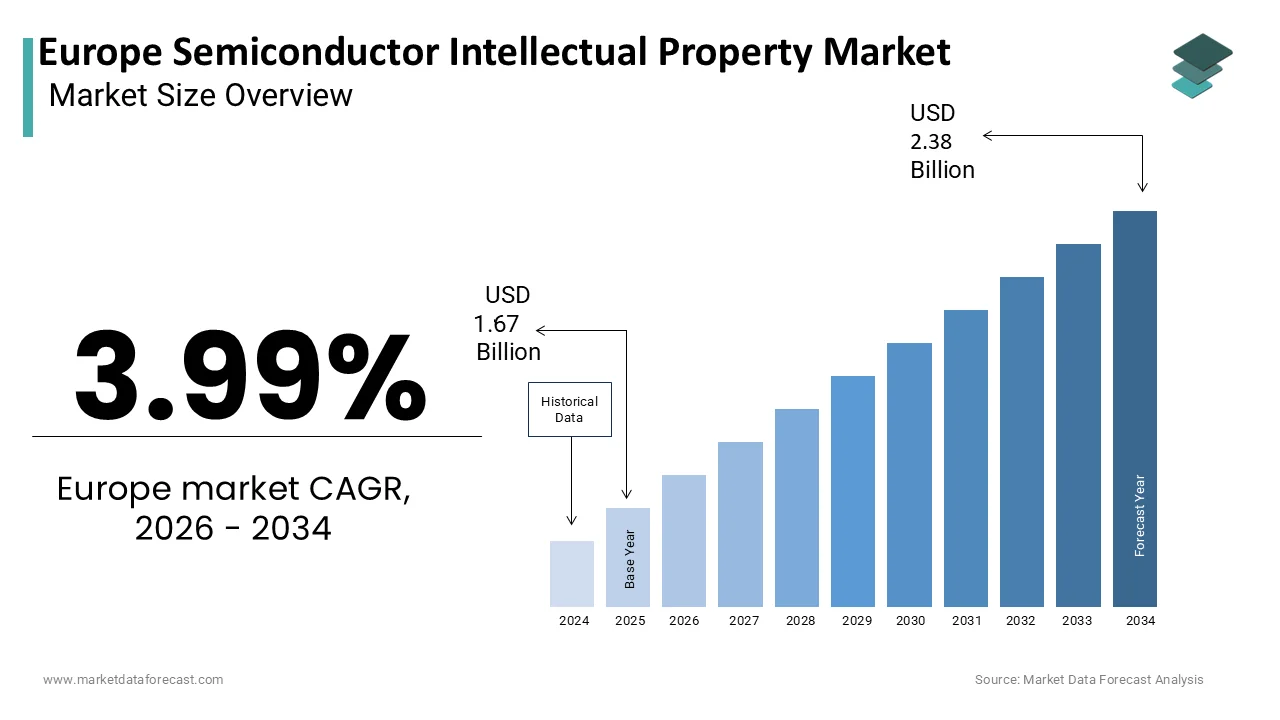

The Europe semiconductor intellectual property market was valued at USD 1.67 billion in 2025, is estimated to reach USD 1.74 billion in 2026, and is projected to reach USD 2.38 billion by 2034, growing at a CAGR of 3.99% from 2026 to 2034.

Semiconductor Intellectual Property (IP) refers to pre-designed, reusable building blocks or components, such as logic designs, layouts, or circuits, used to create integrated circuits (ICs) and systems-on-chip (SoCs). These assets enable chip designers to accelerate time to market by integrating verified functional units rather than designing every transistor from scratch. In the European context, this market is pivotal for supporting the region’s strong automotive, industrial, and telecommunications sectors. As per Eurostat, the ICT manufacturing sector specifically accounted for roughly 0.5-1.2% of gross value added in various Member States as of 2024/2025, while total high-tech product sales reached €414 billion in 2024. Furthermore, the European Commission reports that the semiconductor industry provides approximately 455,000 direct high-skill jobs, with a looming shortage of 350,000 workers expected by 2030. The market is characterized by a shift towards specialized architectures, including RISC-V open source frameworks, which offer flexibility and cost efficiency for custom applications. Regulatory initiatives such as the European Chips Act aim to double the EU’s global share of semiconductor production to 20 percent by 2030, indirectly stimulating demand for indigenous intellectual property solutions. However, current projections from the European Court of Auditors suggest the actual share will only reach approximately 11.7% due to intense global competition. This legislative push encourages local innovation and reduces dependency on non-European suppliers. Consequently, companies are increasingly investing in proprietary designs to secure supply chains and meet specific performance requirements for electric vehicles and edge computing devices. The ecosystem involves a complex interplay between independent intellectual property vendors, integrated device manufacturers, and fabless design houses, all striving to balance innovation with rigorous compliance standards.

MARKET DRIVERS

Expansion of the Automotive Electronics Sector

The rapid expansion of the automotive electronics sector serves as a primary driver for the Europe semiconductor intellectual property market. Modern vehicles are increasingly defined by their software and electronic content, with advanced driver assistance systems, infotainment, and powertrain management requiring sophisticated integrated circuits. As per the European Automobile Manufacturers Association (ACEA), a modern electric vehicle (EV) integrates approximately 1,300 to 3,000 semiconductor units, a density that is doubling as Europe shifts toward Level 3/4 autonomous driving and software-defined vehicles. This proliferation of chips necessitates robust and reliable intellectual property cores for processing, connectivity, and safety functions. European automakers prioritize functional safety standards such as ISO 26262, driving demand for pre-verified intellectual property that meets these stringent requirements. Licensing established cores reduces the risk of design errors and accelerates certification processes. Additionally, the shift towards software-defined vehicles requires flexible and updatable hardware architectures, which intellectual property providers address through modular and scalable solutions. The integration of artificial intelligence for real-time decision making further increases the complexity of chip designs, prompting manufacturers to rely on specialized neural network processing units. By leveraging licensed intellectual property, automotive suppliers can focus on differentiation features while ensuring baseline reliability. This strategic reliance on external design assets fuels sustained growth in the semiconductor intellectual property market, aligning with the broader electrification and digitalization trends in the European automotive industry.

Growth of Industrial Internet of Things Applications

The growth of Industrial Internet of Things applications significantly propels the expansion of the Europe semiconductor intellectual property market. Industries are increasingly adopting smart sensors, predictive maintenance systems, and automated control units to enhance operational efficiency and productivity. Based on European Commission digital targets, the number of total IoT connections in Europe is projected to approach 1 billion by 2030, with industrial high-performance computing (Edge AI) driving the highest demand for low-power IP blocks. These devices require specialized intellectual property cores for wireless connectivity, data processing, and energy management. The diversity of industrial applications, ranging from manufacturing robotics to smart grid infrastructure, demands customizable solutions that can be tailored to specific environmental and performance constraints. Intellectual property providers offer a wide range of interfaces and processor architectures that enable designers to create application-specific integrated circuits efficiently. The need for real-time data processing at the edge further stimulates demand for high-speed serial interfaces and memory controllers. Additionally, the emphasis on security in industrial networks drives the integration of hardware-based security modules, which are often sourced as licensed intellectual property. By providing verified and optimized building blocks, intellectual property vendors help industrial equipment manufacturers reduce development cycles and ensure interoperability. This alignment with the digital transformation of European industry sustains the robust demand for semiconductor design assets.

MARKET RESTRAINTS

High Licensing Costs and Royalty Structures

High licensing costs and complex royalty structures for premium semiconductor IP act as a major barrier to the Europe semiconductor intellectual property market. This is particularly challenging for small and medium-sized enterprises. Developing advanced cores requires substantial research and development investment, which providers recoup through upfront fees and ongoing royalties based on chip sales. According to industry cost models cited by the European Semiconductor Industry Association (ESIA) members, the design cost for an advanced 5nm SoC has escalated to over €500 million, with IP licensing and verification now consuming approximately 30–40% of total R&D expenditure. For smaller design houses, these costs can be prohibitive, limiting their ability to access state-of-the-art technologies. The cumulative effect of licensing multiple cores for a single chip can erode profit margins, making it difficult to compete with larger integrated device manufacturers that have internal libraries. Additionally, the unpredictability of royalty payments based on volume forecasts creates financial uncertainty for startups and niche players. Negotiating favorable terms often requires significant legal and technical expertise, adding to the administrative burden. Some companies may opt for older or less efficient technologies to avoid high costs, potentially compromising product performance. This financial barrier restricts innovation and limits the diversity of participants in the market. Consequently, the high entry cost remains a persistent challenge, slowing the adoption of advanced intellectual property solutions among resource-constrained entities in the European semiconductor ecosystem.

Shortage of Skilled Semiconductor Design Engineers

A critical shortage of skilled semiconductor design engineers poses a substantial hurdle to the Europe semiconductor intellectual property market. The complexity of modern chip design requires specialized knowledge in architecture, verification, and physical implementation, skills that are in short supply across the continent. Per Cedefop and the EU Digital Decade 2025 assessment, Europe faces a deficit of 1.2 million ICT professionals, with the semiconductor industry specifically requiring 350,000 additional workers by 2030 to meet Chips Act production targets. This talent gap hinders the ability of companies to effectively integrate and customize licensed intellectual property cores. Even with access to high-quality design assets, organizations lack the human capital to optimize these components for specific applications. The aging workforce in the traditional semiconductor hubs of Europe further exacerbates the problem, as experienced engineers retire without sufficient replacements entering the field. Universities and training institutions struggle to keep pace with the rapid evolution of design tools and methodologies. This scarcity drives up labor costs and extends project timelines, reducing the overall efficiency of the design process. Companies may delay new product launches or limit the scope of their designs due to resource constraints. The inability to scale engineering teams in line with market demand limits the growth potential of both intellectual property providers and their customers. This human resource constraint remains a fundamental bottleneck for the industry.

MARKET OPPORTUNITIES

Adoption of Open Source RISC-V Architecture

The adoption of the open-source RISC-V instruction set architecture offers a significant opportunity for the Europe semiconductor intellectual property market. RISC-V offers a modular and extensible framework that allows designers to customize processor cores without the restrictive licensing fees associated with proprietary architectures like ARM. According to RISC-V International, the ecosystem is scaling rapidly, with global core shipments projected to surpass 16 billion by 2025. Europe is a major driver of this growth through the EuroHPC JU and the European Processor Initiative (EPI), which utilize RISC-V to achieve technological sovereignty. European companies are increasingly leveraging RISC-V to develop application-specific processors for automotive, industrial, and aerospace applications. This shift enables greater flexibility and control over the design process, fostering innovation in niche markets. Intellectual property providers are responding by offering enhanced RISC-V cores with added features for security, performance, and efficiency. The open nature of the architecture encourages collaboration and community-driven development, accelerating the creation of new design assets. Additionally, the European Union’s support for open standards aligns with the principles of RISC V, providing a favorable regulatory environment. By embracing this architecture, European firms can reduce dependency on foreign technology providers and build a resilient domestic supply chain. This strategic move opens new revenue streams for intellectual property vendors who specialize in RISC-V extensions and verification services, driving market growth.

Integration of Artificial Intelligence in Edge Devices

The integration of artificial intelligence in edge devices provides a potential prospect for the Europe semiconductor intellectual property market. As industries move towards decentralized data processing, there is a growing demand for chips capable of running machine learning algorithms locally. As per sources, the European edge computing market is expanding at a significant rate through 2027, with specific demand for AI-optimized IP in industrial and automotive sectors driving higher value-per-socket for IP providers. This trend requires specialized intellectual property cores for neural network processing, image recognition, and natural language understanding. Intellectual property providers are developing optimized accelerator blocks that deliver high performance with low power consumption, essential for battery-operated edge devices. The ability to license these AI-specific cores allows chip designers to quickly incorporate advanced capabilities into their products without extensive in-house development. Furthermore, the need for real-time decision-making in critical applications drives the demand for deterministic and reliable AI hardware. European companies are well-positioned to lead in industrial AI applications, creating a strong domestic market for these specialized design assets. By focusing on edge AI intellectual property, vendors can capture value from the expanding Internet of Things ecosystem. This technological shift enables the creation of smarter, more responsive devices, reinforcing the strategic importance of semiconductor intellectual property in the European digital economy.

MARKET CHALLENGES

Complexity of Intellectual Property Integration and Verification

The complexity of integrating and verifying multiple intellectual property cores within a single system on chip is a major challenge for the Europe semiconductor intellectual property market. Modern chips often combine dozens of heterogeneous blocks, including processors, memory controllers, and interface protocols, each from different vendors. As per Synopsys, verification accounts for up to 70 percent of the total design cycle time, highlighting the immense effort required to ensure proper functionality. Integrating these diverse components requires rigorous testing to identify compatibility issues, timing violations, and power conflicts. The lack of standardized interfaces and documentation among different intellectual property providers complicates this process, leading to prolonged development schedules. Errors discovered late in the design flow can result in costly respins, delaying time to market, and increasing expenses. Additionally, the increasing frequency and complexity of chips exacerbate these challenges, requiring advanced verification tools and methodologies that are expensive and difficult to master. Small and medium-sized design houses often lack the resources to perform comprehensive verification, increasing the risk of field failures. The fragmentation of the intellectual property ecosystem further hinders seamless integration, forcing designers to act as system integrators. This technical burden acts as a significant barrier to efficient chip development, limiting the speed at which new products can be introduced to the market.

Geopolitical Tensions and Supply Chain Vulnerabilities

Geopolitical tensions and supply chain vulnerabilities further hamper the Europe semiconductor intellectual property market. The global semiconductor industry is highly interconnected, with design, manufacturing, and packaging often occurring in different regions. Recent trade restrictions and export controls have disrupted this flow, creating uncertainty for European companies that rely on international collaborations. As per the European External Action Service, geopolitical instability has highlighted the risks of dependency on non-European technologies, prompting calls for greater strategic autonomy. However, achieving self-sufficiency is difficult given the dominance of foreign players in certain intellectual property segments. European firms face challenges in accessing advanced design tools and manufacturing processes due to regulatory barriers. Additionally, the threat of intellectual property theft and cyber espionage remains a concern, requiring robust security measures that add to operational costs. The fragmentation of global standards and regulations further complicates cross-border business operations. Companies must navigate a complex web of compliance requirements, which can delay product launches and increase legal risks. The uncertainty surrounding future trade policies discourages long-term investment in collaborative projects. These geopolitical factors create an unstable operating environment, hindering the growth and innovation potential of the European semiconductor intellectual property sector.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By IP Source, Design IP, Vertical, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Arm Holdings plc, Synopsys, Inc., Cadence Design Systems, Inc., Imagination Technologies Group plc, CEVA, Inc., Rambus Inc., Lattice Semiconductor Corporation, VeriSilicon Holdings Co., Ltd., Alphawave IP Group plc, Silvaco, Inc., eMemory Technology Inc., Dolphin Design SAS |

SEGMENTAL ANALYSIS

By IP Source Insights

The licensing segment was the largest segment in the Europe semiconductor intellectual property market and captured a 65.7% share in 2025. This supremacy of the segment is attributed to the fundamental business model of independent intellectual property vendors who generate immediate revenue through upfront licensing fees before any chips are manufactured. As per sources, the escalating cost of research and development for advanced processor cores, often exceeding hundreds of millions of dollars per node, necessitates substantial initial capital recovery, a financial model primarily supported by upfront licensing fees. The main driver for this segment is the need for chip designers to secure access to proven and verified design blocks without long-term financial uncertainty. Licensing agreements allow companies to integrate complex functionalities such as central processing units or graphics processors into their system-on-chip designs efficiently. This model is particularly attractive for startups and small design houses that lack the resources to develop these components from scratch. Additionally, licensing provides legal protection and technical support, ensuring that the intellectual property is implemented correctly. The predictability of upfront costs helps organizations manage their budgets effectively during the design phase. Furthermore, the rapid pace of technological innovation requires frequent updates to intellectual property libraries, which are often included in licensing packages. This continuous access to state-of-the-art designs reinforces the preference for licensing over royalty-based models in the early stages of product development. Consequently, the licensing segment remains the cornerstone of revenue for intellectual property providers in Europe.

The royalty segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 14.8% during the forecast period due to the increasing volume of semiconductor shipments across various end-use industries, particularly automotive and consumer electronics. As per a study, the number of connected IoT devices globally is projected to reach approximately 24 billion by 2027, with the European market accounting for a multi-billion unit share. This massive installed base drives high-volume production, generating significant recurring royalty streams for IP holders. A key driver is the shift towards high-volume manufacturing of integrated circuits that incorporate licensed intellectual property. Unlike licensing fees, which are one-time payments, royalties provide recurring revenue based on the number of units sold. This model aligns the interests of intellectual property providers with the commercial success of their customers. As chips become more complex and expensive to produce, the value of the embedded intellectual property increases, justifying higher royalty rates. Additionally, the adoption of standard architectures such as ARM and RISC-V in mass market applications ensures a steady flow of royalty income. The growth of the Internet of Things and edge computing sectors further amplifies this trend, as billions of low-cost sensors and microcontrollers require licensed cores. Intellectual property vendors are increasingly focusing on royalty-bearing agreements to capture long-term value from successful products. This structural shift towards volume-driven revenue models accelerates the growth of the royalty segment in the European market.

By Design IP Insights

The processor IP segment held the majority share of 40.3% of the Europe semiconductor intellectual property market in 2025 because of the critical role of central processing units and microcontrollers in virtually all electronic devices. As per the European Commission, the demand for high-performance computing capabilities in automotive and industrial applications has surged, necessitating advanced processor cores. A key force behind the growth of this segment is the increasing complexity of system-on-chip designs, which require powerful and efficient processing units to handle multiple tasks simultaneously. Automotive manufacturers, for instance, rely on sophisticated processor IP for advanced driver assistance systems and infotainment platforms. The shift towards electric vehicles has further increased the need for specialized controllers that manage battery systems and powertrain operations. Additionally, the rise of artificial intelligence at the edge requires neural network processing units, which are often licensed as part of the processor IP portfolio. Companies prefer to license proven processor architectures to reduce development time and ensure reliability. The availability of diverse instruction set architectures, including ARM and RISC-V, provides designers with flexibility in choosing the right core for their specific application. This versatility and the indispensable nature of processing power solidify the Processor IP segment as the market leader in Europe.

The interface IP segment is expected to exhibit a noteworthy CAGR of 15.2% from 2026 to 2034, owing to the escalating demand for high-speed data transmission and connectivity in modern electronic systems. As per International Data Corporation, global data creation is expected to reach 180 zettabytes by 2025, driving the need for faster interfaces such as PCIe, USB, and Ethernet. The primary driver is the proliferation of data centers and cloud computing infrastructure in Europe, which requires high-bandwidth interconnects to manage massive data flows. Additionally, the adoption of 5G technology in telecommunications networks necessitates advanced interface IP for base stations and user equipment. The integration of multiple heterogeneous components in system-on-chip designs also increases the demand for reliable and standardized interfaces. Interface IP ensures seamless communication between processors, memory, and peripheral devices, which is critical for overall system performance. The emergence of new standards such as PCIe 5.0 and 6.0 further stimulates the market, as designers upgrade their architectures to support higher speeds. Automotive applications, including vehicle-to-everything communication, also contribute to this growth by requiring robust and low-latency interfaces. The continuous evolution of connectivity standards and the increasing importance of data throughput drive the rapid expansion of the Interface IP segment in the European market.

By Vertical Insights

The automotive segment led the Europe semiconductor intellectual property market and accounted for a 35.2% share in 2025. This leading position of the segment is attributed to the profound transformation of the automotive industry towards electrification, autonomy, and connectivity. As per research, the average value of semiconductor content in a car has more than doubled in the last 10 years, reaching over $600, reflecting the increasing reliance on connectivity, safety, and electrification. The segment lead is secured by the stringent safety and reliability requirements mandated by regulations such as ISO 26262. Automotive manufacturers require pre-verified intellectual property cores that meet these rigorous standards to ensure functional safety in critical applications like braking and steering systems. The development of advanced driver assistance systems and autonomous driving features demands high-performance processing units and specialized accelerators, which are often sourced as licensed IP. Additionally, the shift towards software-defined vehicles requires flexible and updatable hardware architectures, prompting automakers to invest in customizable intellectual property solutions. The presence of major European automotive OEMs and tier one suppliers further strengthens the market ecosystem. These companies collaborate closely with intellectual property vendors to develop tailored solutions that enhance vehicle performance and user experience. The sustained investment in electric vehicle platforms and smart mobility initiatives ensures that the automotive sector remains the largest consumer of semiconductor intellectual property in Europe.

The industrial segment is predicted to witness the highest CAGR of 16.5% over the forecast period. This rapid expansion of the segment is fueled by the ongoing digital transformation of manufacturing processes and the adoption of Industry 4.0 technologies. As per the European Commission, the Horizon Europe program has allocated €14 billion for 2026-2027 to drive research in digital and industrial technologies. The primary driver is the need for real-time data processing and control in smart factories, which requires robust and reliable intellectual property cores. Industrial applications such as predictive maintenance, quality inspection, and supply chain optimization rely on sensors and controllers that incorporate licensed IP for connectivity and processing. The emphasis on energy efficiency and sustainability also drives the adoption of low-power intellectual property solutions for industrial IoT devices. Additionally, the resurgence of manufacturing in Europe, supported by government initiatives, creates new opportunities for semiconductor design. Companies are increasingly focusing on edge computing capabilities to reduce latency and improve operational efficiency. The diversity of industrial applications, ranging from aerospace to medical devices, further contributes to the growth of this segment. By leveraging specialized intellectual property, industrial equipment manufacturers can accelerate product development and enhance competitiveness. These factors collectively drive the robust growth of the Industrial segment in the European semiconductor intellectual property market.

COUNTRY LEVEL ANALYSIS

Germany Semiconductor Intellectual Property Market Analysis

Germany outperformed other countries in the Europe semiconductor intellectual property market and accounted for a 28.6% share in 2025. This growth of the German market is driven by a strong industrial base, particularly in the automotive and manufacturing sectors, which are heavy consumers of advanced semiconductor designs. German companies are known for their emphasis on engineering excellence and quality, driving the demand for high-reliability intellectual property cores. As per the Federal Statistical Office (Destatis), the automotive industry accounts for approximately 4.5% to 4.7% of the country’s gross value added (GVA) (and roughly 5% of GDP according to industry reports), highlighting its significance as a driver for semiconductor demand. The main driver for the market in Germany is the presence of major automotive original equipment manufacturers and tier one suppliers who are actively developing electric and autonomous vehicles. These companies require sophisticated processors and interface intellectual property to meet stringent safety and performance standards. Additionally, the German government’s support for semiconductor research and development through initiatives like the European Chips Act further stimulates the market. The country hosts several leading research institutes and design centers that collaborate with intellectual property vendors to innovate new solutions. The focus on industrial automation and Industry 4.0 also drives demand for specialized embedded systems. Furthermore, the strong ecosystem of semiconductor equipment and material suppliers supports the overall growth of the industry. These factors collectively sustain Germany’s position as the largest and most influential market for semiconductor intellectual property in Europe.

United Kingdom Semiconductor Intellectual Property Market Analysis

The United Kingdom was the second-largest player in the Europe semiconductor intellectual property market and held a 22.1% share in 2025. The market in the UK has a vibrant ecosystem of fabless design houses and intellectual property vendors, particularly in the Cambridge and Southampton clusters. British companies are leaders in processor architecture and specialized chip design, contributing significantly to global innovation. As per the Office for National Statistics (ONS), the UK’s digital sector contributed approximately £160 billion in GVA in 2023, showing a growth of 0.6% from the previous year, while specific high-growth segments like AI are projected to expand faster. One of the major drivers of the market is the presence of world-class universities and research institutions that produce a steady stream of skilled engineers and innovative technologies. The UK is home to several prominent intellectual property providers who specialize in processor cores and connectivity solutions. The strong focus on artificial intelligence and machine learning applications further drives demand for specialized design assets. Additionally, the government’s National Semiconductor Strategy aims to strengthen the domestic supply chain and support design capabilities. The collaboration between academia and industry fosters a culture of innovation, attracting investment from global players. The UK’s expertise in compound semiconductors and photonics also complements the digital design sector. These dynamics maintain the UK’s status as a key hub for semiconductor intellectual property development and licensing in Europe.

France Semiconductor Intellectual Property Market Analysis

France occupies a significant position in the Europe semiconductor intellectual property market due to strong government initiatives promoting technological sovereignty and strategic autonomy in critical sectors. French enterprises, particularly in aerospace, defense, and telecommunications, are increasingly investing in indigenous semiconductor designs to reduce dependency on foreign suppliers. As per Bpifrance, the French deep tech ecosystem is expanding, with €2.8 billion raised by startups in 2024 and 385 new deep tech startups created, supported by the "France 2030" investment plan. The primary driver for the market is the presence of major integrated device manufacturers and research centers such as CEA Leti, which play a crucial role in advancing semiconductor technologies. The French government’s France 2030 investment plan allocates substantial funds to semiconductor research and production, stimulating demand for local intellectual property solutions. Additionally, the strong automotive and industrial sectors in France drive demand for specialized embedded systems and safety-critical cores. The country’s focus on open source architectures like RISC-V aligns with its strategic goals, fostering a collaborative ecosystem for design innovation. Furthermore, the integration of French companies into European collaborative projects enhances their access to cutting-edge technologies. These factors contribute to the steady growth and strategic importance of the semiconductor intellectual property market in France.

Italy Semiconductor Intellectual Property Market Analysis

Italy witnessed a consistent growth in the Europe semiconductor intellectual property market owing to a strong presence in specialized semiconductor applications, particularly in automotive and industrial electronics. Italian companies are known for their expertise in analog and mixed signal design, which complements the digital intellectual property market. The main accelerator for the market is the presence of major semiconductor manufacturers and design centers that collaborate with intellectual property vendors to develop custom solutions. The automotive sector, with companies like STMicroelectronics having a significant footprint, drives demand for reliable and efficient processor and interface IP. Additionally, the growing focus on smart manufacturing and automation in Italy creates opportunities for industrial IoT applications. The government’s support for digital transformation and innovation further facilitates market growth. Furthermore, the integration of Italian research institutions into European semiconductor initiatives enhances the country’s capabilities in advanced design. These factors contribute to the emerging potential of the semiconductor intellectual property market in Italy, with steady growth expected in specialized niches.

Netherlands Semiconductor Intellectual Property Market Analysis

The Netherlands is anticipated to expand notably in the Europe semiconductor intellectual property market over the forecast period due to its pivotal role in the global semiconductor equipment supply chain and a growing design ecosystem. Dutch companies are leaders in lithography and testing equipment, which supports the broader semiconductor industry. The primary driver for the market is the presence of major technology companies and research institutes such as IMEC and TNO, which collaborate on advanced semiconductor projects. The Netherlands is also home to a vibrant startup scene focused on chip design and intellectual property development. The government’s commitment to maintaining the country’s position as a tech hub drives investment in education and infrastructure. Additionally, the strong collaboration with neighboring countries like Germany and Belgium fosters a regional ecosystem for semiconductor innovation. The focus on sustainability and energy-efficient technologies also influences the direction of intellectual property development. These factors support the dynamic growth of the semiconductor intellectual property market in the Netherlands, positioning it as a critical node in the European semiconductor landscape.

COMPETITIVE LANDSCAPE

The competition in the Europe semiconductor intellectual property market is intense and characterized by the presence of global giants alongside specialized regional players. Major corporations leverage their extensive portfolios and integrated toolchains to offer comprehensive solutions that span from design to verification. Differentiation is increasingly achieved through performance metrics, power efficiency, and support for advanced connectivity standards. The rise of open source architectures like RISC-V introduces new competitive dynamics, challenging traditional proprietary models. Companies are forming strategic ecosystems with foundries and software vendors to ensure compatibility and accelerate adoption. Innovation in artificial intelligence and machine learning accelerators serves as a key battleground for technological leadership. Customer support and technical expertise are critical factors influencing purchasing decisions, particularly for complex system-on-chip designs. Regulatory pressures regarding security and sustainability also shape competitive strategies, prompting providers to embed compliance features directly into their IP. Mergers and acquisitions are common as firms seek to expand their capabilities and market reach. The ability to deliver reliable, scalable, and secure IP solutions quickly remains the primary determinant of success in this dynamic and technologically driven market environment.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global Europe Semiconductor Intellectual Property Market include

- Arm Holdings plc

- Synopsys, Inc.

- Cadence Design Systems, Inc.

- Imagination Technologies Group plc

- CEVA, Inc.

- Rambus Inc.

- Lattice Semiconductor Corporation

- VeriSilicon Holdings Co., Ltd.

- Alphawave IP Group plc

- Silvaco, Inc.

- eMemory Technology Inc.

- Dolphin Design SAS

TOP LEADING PLAYERS IN THE MARKET

- Arm Limited remains a dominant force in the Europe semiconductor intellectual property market, providing the foundational architecture for most mobile and embedded processors globally. The company contributes significantly to the global ecosystem by licensing its energy-efficient designs to major chipmakers. Arm has recently strengthened its position by expanding its automotive portfolio with high-performance computing platforms tailored for software-defined vehicles. These initiatives support European automakers in developing advanced driver assistance systems. The company also focuses on enhancing security features within its core to meet stringent regulatory standards. By fostering strong partnerships with foundries and electronic design automation vendors, Arm ensures seamless integration for its customers. Its continuous investment in research and development drives innovation in artificial intelligence and edge computing. Arm’s commitment to open standards and collaboration solidifies its role as a critical enabler of digital transformation across various industries in Europe and worldwide.

- Synopsys Inc. is a leading provider of electronic design automation tools and semiconductor intellectual property, playing a crucial role in the European market. The company offers a comprehensive portfolio of interface and processor IP that accelerates chip design cycles. Synopsys contributes to the global market by integrating its IP solutions with its design software, creating a unified workflow for engineers. Recently, the company has strengthened its position by launching advanced interface IP solutions supporting next-generation connectivity standards such as PCIe 6.0. These innovations address the growing demand for high-speed data transfer in data centers and automotive applications. Synopsys also emphasizes security by embedding hardware root of trust features into its IP blocks. Its strategic acquisitions and partnerships expand its technological capabilities and market reach. By providing verified and silicon-proven IP, Synopsys helps European designers reduce time to market and mitigate risks. This holistic approach reinforces its leadership in the semiconductor IP landscape.

- Cadence Design Systems Inc. is a key player in the Europe semiconductor intellectual property market, offering a wide range of customizable processor and interface IP. The company contributes to the global market by enabling complex system-on-chip designs through its robust Tensilica processor families. Cadence has recently strengthened its position by enhancing its AI accelerator IP to support machine learning workloads at the edge. This move aligns with the increasing adoption of artificial intelligence in industrial and consumer devices across Europe. The company also focuses on delivering low-power and high-performance solutions for automotive and mobile applications. Cadence collaborates closely with foundries to ensure optimal performance and manufacturability of its IP. Its integration of IP with verification and validation tools provides customers with a streamlined design experience. Cadence continuously innovates and expands its portfolio to maintain a competitive edge. This strategy supports the evolving needs of the European semiconductor industry.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe semiconductor intellectual property market predominantly employ strategies focused on innovation and strategic partnerships to maintain a competitive advantage. Companies invest heavily in research and development to create advanced processors and interface IP that meet emerging standards such as PCIe 6.0 and USB4. Integration of artificial intelligence capabilities into IP cores is a major focus to address the growing demand for edge computing. Providers are increasingly adopting platform-based approaches that combine IP with electronic design automation tools for seamless workflows. Strategic alliances with foundries ensure silicon-proven results and faster time to market. Expansion into specialized verticals like automotive and industrial IoT allows firms to capture niche opportunities. Emphasis on security features within IP block addresses is raising cybersecurity concerns. Licensing models are evolving to offer greater flexibility and cost efficiency for customers. These strategies collectively drive growth and enhance the value proposition in a rapidly changing technological landscape.

MARKET SEGMENTATION

This research report on the europe semiconductor intellectual property market is segmented and sub-segmented into the following categories.

By IP Source

- Licensing

- Royalty

By Design IP

- Processor IP

- Interface IP

By Vertical

- Automotive

- Industrial

By Country

- Germany

- United Kingdom

- France

- Italy

- Netherlands

- Rest of Europe

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com