Europe Small Wind Turbine Market Size, Share, Trends & Growth Forecast Report Segmented By Axis Type (Horizontal Axis Wind Turbine, Vertical Axis Wind Turbine), And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe), Industry Analysis From 2026 To 2034

Europe Small Wind Turbine Market Report Summary

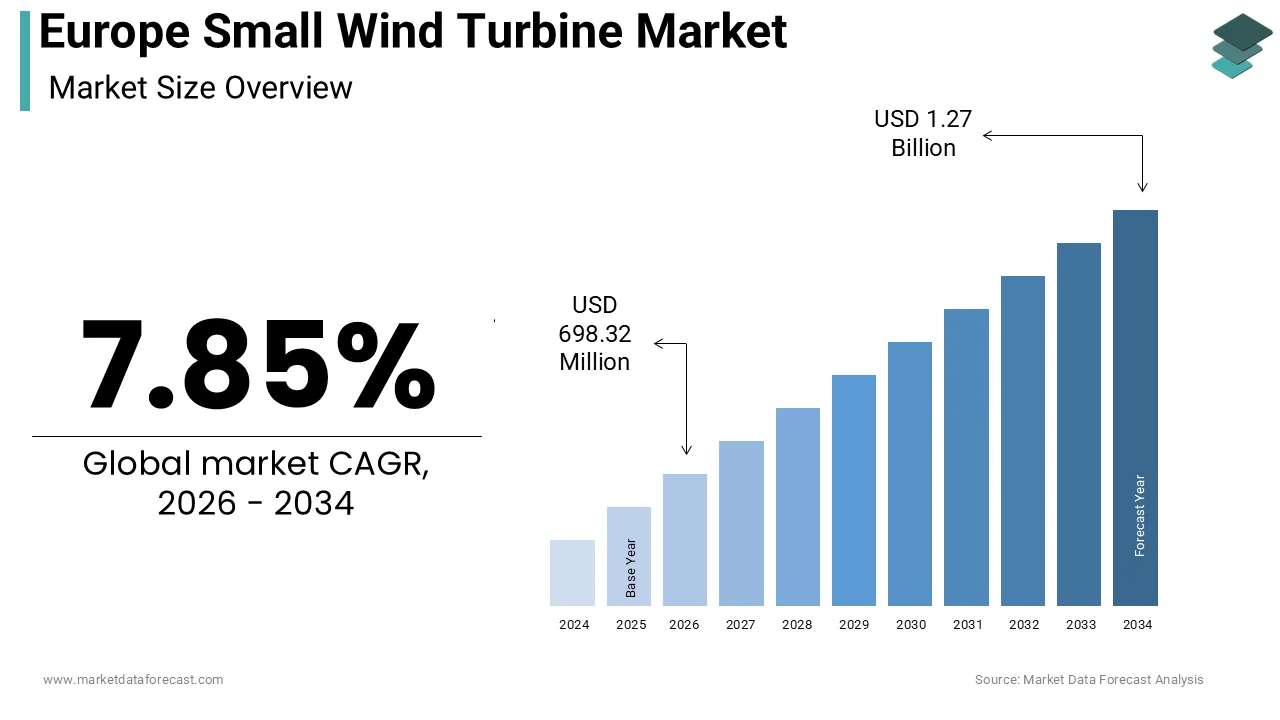

The Europe small wind turbine market was valued at USD 647.49 million in 2025 and is projected to reach USD 1.27 billion by 2034, growing from USD 698.32 million in 2026 at a CAGR of 7.85% during the forecast period. Market growth is driven by increasing demand for decentralized renewable energy solutions, rising energy costs, and supportive government policies promoting clean energy adoption. Small wind turbines are gaining traction in rural, residential, and off-grid applications due to their ability to provide localized power generation and reduce dependence on centralized energy systems.

Key Market Trends

- Rising adoption of decentralized and off-grid renewable energy systems

- Increasing government incentives and subsidies for small wind installations

- Growing demand for hybrid renewable systems (wind + solar)

- Expansion of rural electrification and energy independence initiatives

- Technological advancements are improving the efficiency and durability of turbines

Segmental Insights

- Based on axis type, the horizontal axis wind turbines segment dominated the Europe small wind turbine market in 2025, driven by higher efficiency and widespread commercial adoption.

Regional Insights

- United Kingdom led the Europe small wind turbine market in 2025 by holding 24.1% of the regional market share, supported by strong renewable energy policies and rural adoption.

- Germany ranked second with 20.2% share in 2025, driven by advanced renewable infrastructure and technological expertise

- France holds a notable share, supported by government incentives and growing interest in energy independence

- Italy is witnessing steady growth due to favorable regulations and diverse geographical conditions.

- Spain is anticipated to expand significantly during the forecast period, driven by increasing adoption in rural and coastal areas

Competitive Landscape

- The Europe small wind turbine market is moderately competitive, with companies focusing on innovation, efficiency improvements, and expansion of small-scale renewable solutions. Market players are investing in hybrid systems, smart energy integration, and cost-effective turbine designs to enhance adoption.

- Prominent players in the Europe small wind turbine market include Siemens Gamesa Renewable Energy, Vestas Wind Systems A/S, Nordex SE, Enercon GmbH, Bergey Windpower Co, Kingspan Group plc, SD Wind Energy Ltd, Ryse Energy, Aeolos Wind Energy Ltd, Eocycle Technologies Inc, Fortis Wind Energy, Endurance Wind Power, XZERES Corp, Kestrel Renewable Energy, and Superwind GmbH.

Europe Small Wind Turbine Market Size

The Europe small wind turbine market size was calculated to be USD 647.49 million in 2025 and is anticipated to be worth USD 1.27 billion by 2034, from USD 698.32 million in 2026, growing at a CAGR of 7.85% during the forecast period.

Small wind turbines (SWTs) are compact, decentralized wind energy systems designed for small-scale electricity generation, typically producing between 500 Watts (W) and 100 kilowatts (kW). These decentralized energy solutions are primarily deployed in rural residential, agricultural, and small commercial settings to supplement grid electricity or provide off-grid power. Unlike large-scale utility wind farms, small wind turbines operate in a complex wind environment,s often characterized by turbulence and variable directions, necessitating robust engineering and adaptive control systems. The region’s commitment to energy independence and decarbonization drives interest in distributed generation technologies. According to the European Environment Agency, the building sector accounts for 40 percent of final energy consumption in the European Union, highlighting the potential for on-site renewable integration. Furthermore, Eurostat's 2024 housing statistics indicate that 82% of the population in rural areas live in houses (compared to only 27% in cities), suggesting a significantly higher technical potential for rooftop solar and small-scale renewable installations due to higher private property ownership and available roof space. The National Renewable Energy Laboratory (NREL) notes that distributed wind energy systems can improve grid resiliency and reduce transmission and distribution losses by generating power directly behind the meter or close to local electrical loads. Regulatory frameworks such as the European Green Deal encourage citizen energy communities, which often utilize small wind technology. However, the market faces scrutiny regarding noise and visual impact. The European Wind Energy Association emphasizes the need for standardized certification to ensure reliability and safety. As electricity prices remain volatile, consumers seek long-term cost stability through self-generation. This market segment thus represents a critical component of the broader renewable energy landscape, offering localized resilience and contributing to national climate targets through decentralized power production.

MARKET DRIVERS

Rising Electricity Prices and Energy Security Concerns Accelerate Adoption

Surging electricity prices and heightened concerns regarding energy security serve as primary growth enablers for the Europe small wind turbine market. The geopolitical instability following recent conflicts has disrupted natural gas supplies, leading to unprecedented volatility in energy markets. Rising electricity prices across the European Union, which saw significant increases in 2023, are driving the adoption of small-scale wind technology as a cost-stabilization measure, according to Eurostat. This financial pressure motivates homeowners and small businesses to seek alternative sources of power that offer long-term cost predictability. Small wind turbines enable users to generate their own electricity, thereby reducing reliance on the central grid and mitigating exposure to fluctuating utility rates. For instance, in the United Kingdom, the Energy Price Guarantee has prompted a surge in inquiries for domestic renewable solutions. The UK Department for Energy Security and Net Zero shows a marked increase in certified renewable installation sites. Additionally, the desire for energy independence is strong in rural areas where grid infrastructure may be less reliable. European Commission reports indicate rising investment in on-site generation by agricultural businesses to enhance energy resilience. Small wind systems complement solar photovoltaic arrays by producing power during windy nights and winter months when solar output is low. This hybrid approach ensures a more consistent energy supply. Consequently, the economic imperative to reduce energy bills, combined with the strategic goal of energy autonomy, drives significant demand for small wind technology in the European market.

Government Incentives and Supportive Policy Frameworks Stimulate Investment

Robust government incentives and supportive policy frameworks significantly stimulate investment in the Europe small wind turbine market. Various European nations have implemented financial mechanisms such as feed-in tariffs, tax credits, and grants to encourage the deployment of distributed renewable energy. According to the European Commission, the Renewable Energy Directive II mandates that member states simplify permitting procedures for small-scale renewable projects. This regulatory support reduces administrative barriers and accelerates project timelines. For example, in Germany, the Renewable Energy Sources Act provides guaranteed payments for electricity fed into the grid from small wind installations. The German Federal Ministry for Economic Affairs and Climate Action highlights that a significant number of decentralized wind units are integrated into the national grid, supported by long-term financial frameworks that ensure consistent returns for operators. In France, national subsidy programs enable residents to significantly offset the initial purchase price of approved sustainable energy systems through direct financial assistance and tax-related incentives. The French Environment and Energy Management Agency observes that financial support schemes have fostered a steady upward trend in the adoption of residential and agricultural wind systems over the last several years. Additionally, the European Union’s Cohesion Policy funds rural development projects that include renewable energy components. The European Agricultural Fund for Rural Development shows that substantial portions of the multi-year rural budget are dedicated to supporting energy modernization and the deployment of clean power sources in farming communities. These financial supports lower the initial capital burden and improve the return on investment for users. Consequently, the alignment of national policies with EU climate goals creates a favorable environment for the expansion of the small wind turbine sector.

MARKET RESTRAINTS

Complex Permitting Processes and Zoning Restrictions Hinder Deployment

Complex permitting processes and stringent zoning regulations constitute a major restraint to the growth of the Europe small wind turbine market. Despite EU directives aimed at simplifying approvals, local municipalities often impose rigorous requirements regarding height, noise and visual impact. The European Wind Energy Association identifies that securing the necessary approvals for small-scale turbines involves a timeline that varies significantly across the continent, with local administrative requirements often extending the process over several years. This prolonged timeline increases project costs and discourages potential investors. For instance, in the Netherlands, strict landscape protection laws limit the installation of turbines in certain rural zones. The Dutch government notes that a considerable portion of smaller wind energy proposals fail to receive approval because they do not align with local land-use regulations or existing spatial planning frameworks. Similarly, in Italy, heritage conservation rules restrict installations near historical sites, which are prevalent in many regions. The Italian Ministry of Cultural Heritage and Activities requires specialized environmental and aesthetic reviews for renewable installations proposed near sensitive historical or natural sites, which often extends the overall development schedule. Furthermore, noise regulations vary widely across countries, with some requiring sound levels below 40 decibels at property boundaries. The World Health Organization guidelines on environmental noise influence these local standards, making compliance challenging for manufacturers. The lack of harmonized regulations across Europe creates uncertainty for developers and consumers. In addition, the European Consumer Organisation reports that a large segment of the public chooses to discontinue their transition to sustainable home power due to the overwhelming complexity of administrative paperwork and local approval requirements. Consequently, the fragmented and often restrictive regulatory landscape impedes the widespread adoption of small wind technology.

High Initial Capital Costs and Extended Payback Periods Deter Consumers

The high initial capital costs associated with SWTs and the resulting extended payback periods act as a significant deterrent for many potential consumers, which hampers the expansion of the Europe small wind turbine market. Unlike solar photovoltaic systems, which have seen dramatic price reduction,s small wind turbines involve complex mechanical components and require professional installation on tall towers. According to the International Renewable Energy Agency, the average installed cost for a small wind turbine in Europe ranges from 3000 to 5000 euros per kilowatt. This upfront investment is substantially higher than that for equivalent solar capacity. For a typical 5-kilowatt system, the total cost can exceed 20000 euros. Leading regional financial institutions indicate that the time required for a small wind project to recover its initial investment through energy savings varies widely based on local wind speeds and the prevailing cost of grid power. This long horizon poses a financial risk for homeowners and small businesses, particularly in an economic environment characterized by inflation and uncertain future energy prices. Additionally, maintenance costs for moving parts such as bearings and blades add to the lifetime expense. Technical assessments from the German Agricultural Society suggest that ongoing service and repair costs represent a consistent annual percentage of the original project funding. Many consumers lack access to affordable financing options specifically tailored for small wind projects. Studies note that while sustainability-focused lending is growing, specialized credit products tailored specifically for residential wind technology remain relatively limited among traditional commercial lenders. Consequently, the high barrier to entry and prolonged return on investment limit the market appeal of small wind turbines compared to other renewable technologies.

MARKET OPPORTUNITIES

Integration with Hybrid Renewable Energy Systems Enhances Value Proposition

The integration of SWTs with hybrid renewable energy systems presents a significant opportunity for the growth of the Europe small wind turbine market. Combining wind technology with solar photovoltaics and battery storage creates a resilient and reliable power supply that mitigates the intermittency of individual sources. Regional solar industry bodies observe that combining multiple local power sources with storage significantly raises the proportion of generated energy used directly on-site rather than exported to the grid. Small wind turbines complement solar panels by generating electricity during nighttime and cloudy or windy conditions when solar output is minimal. This synergy is particularly valuable in Northern European countries where wind resources are abundant but solar irradiance is seasonal. For instance, in Sweden, the combination of wind and solar ensures a more consistent energy profile throughout the year. The Swedish Energy Agency notes a steady and significant year-over-year increase in the adoption of multi-technology power systems as consumers seek to diversify their local energy production. Additionally, advancements in smart inverters and energy management systems allow for optimized dispatch of stored energy. These technologies enable users to maximize savings by using stored power during peak tariff periods. The European Battery Alliance highlights that the declining cost of lithium-ion batteries further enhances the economic viability of hybrid systems. Furthermore, off-grid applications in remote islands and mountainous regions rely heavily on hybrid setups for energy security. Regional island energy programs show that a substantial number of isolated power systems are now including small-scale wind to complement solar generation and ensure a more stable energy supply. Consequently, the trend towards integrated energy solutions opens new avenues for small wind turbine manufacturers to expand their market reach.

Technological Advancements in Vertical Axis and Low Wind Speed Designs

Technological advancements in vertical axis wind turbines VAWTs and low wind speed designs provide substantial prospects for the Europe small wind turbine market. Traditional horizontal-axis turbines require consistent and strong winds, which are not available in all urban and suburban locations. VAWT, however, can capture wind from any direction and operate efficiently in turbulent airflow typical of built environments. Research from the Fraunhofer Institute for Wind Energy Systems indicates that recent innovations in vertical-axis technology have enhanced performance and energy capture during periods of lower air movement. These innovations make small wind technology viable for rooftop installations in cities where space is limited and wind patterns are complex. For example, in Denmark, pilot projects in Copenhagen have demonstrated the effectiveness of silent VAWTs on commercial buildings. The Danish Energy Agency notes that urban wind potential is significantly underutilized due to technological limitations. Additionally, the development of direct drive generators eliminates the need for gearboxes, reducing maintenance requirements and noise levels. The European Research Council has funded several projects focused on materials science to create lighter and more durable blades. These improvements enhance the aesthetic appeal and acceptability of small wind turbines in residential areas. Information from carbon reduction advisory groups suggests that equipment designed for quieter operation is becoming increasingly popular among consumers who are sensitive to the acoustic impact of residential energy systems. Furthermore, the integration of Internet of Things sensors enables predictive maintenance and performance monitoring. Consequently, technological innovation expands the applicability of small wind turbines to new segments and locations, driving market growth.

MARKET CHALLENGES

Public Perception Issues Regarding Noise and Visual Impact Persist

Persistent public perception issues regarding noise and visual impact pose a serious challenge to the Europe small wind turbine market. Despite technological improvements, many residents associate wind turbines with industrial-scale facilities and perceive them as intrusive to the landscape. Survey data on public attitudes indicates that a notable segment of the population remains hesitant about the aesthetic changes to local landscapes resulting from the installation of wind energy systems near residential areas. Noise generation, although reduced in modern models remains a complaint, particularly in quiet rural areas. The World Health Organization guidelines state that continuous noise levels above 45 decibels can cause sleep disturbance and annoyance. Some older or poorly maintained turbines exceed this threshold, leading to community opposition. For instance, in France, several local councils have banned small wind installations due to resident complaints. The French Ministry of Ecological Transition reports that social acceptance is a key barrier to decentralized renewable energy. Additionally, the flicker effect caused by rotating blades can be disturbing to nearby inhabitants. The German Federal Immission Control Act imposes strict limits on shadow casting, which restricts installation possibilities. Misinformation and lack of awareness about the benefits of small wind technology exacerbate these perceptions. Studies observe that critical public discourse regarding energy projects frequently receives more attention than the successful integration of these systems into local communities. Furthermore, the lack of standardized certification for noise and visual impact creates inconsistency in product performance. Data from the European Consumer Organisation indicates that trust in manufacturer claims is low among potential buyers. Consequently, addressing social acceptance through education and stricter quality standards remains a critical challenge.

Supply Chain Vulnerabilities and Raw Material Price Volatility

Supply chain vulnerabilities and raw material price volatility are also major obstacles for manufacturers in the Europe small wind turbine market. The production of wind turbines relies heavily on critical materials such as rare earth elements for permanent magnets, steel for towers, and copper for wiring. According to the European Raw Materials Alliance, the EU depends on imports for around 98 percent of its rare earth needs, making the supply chain susceptible to geopolitical disruptions. Recent global events have highlighted the fragility of these supply lines, leading to delays and increased costs. Research found that the cost of industrial metals remains volatile, creating challenges for equipment manufacturers trying to maintain stable production costs. Additionally, the semiconductor shortage impacted the production of control systems and inverters essential for turbine operation. A study notes that while past supply constraints caused significant delays, the availability of critical electronic parts continues to influence manufacturing schedules. These disruptions force manufacturers to hold higher inventory levels tying up capital and increasing storage costs. Furthermore, the transition to sustainable sourcing adds complexity to procurement processes. The European Commission’s Critical Raw Materials Act aims to secure domestic supply, but implementation will take time. Small and medium-sized enterprises lack the bargaining power of larger corporations to secure favorable contracts. Multiple surveys suggest that a majority of specialized equipment builders experienced significant disruptions in receiving necessary parts and materials during recent global logistical challenges. Consequently, the instability in material availability and pricing constrains production capacity and profitability, hindering market growth.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.85% |

| Segments Covered | By Axis Type, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Siemens Gamesa Renewable Energy, Vestas Wind Systems A/S, Nordex SE, Enercon GmbH, Bergey Windpower Co., Kingspan Group plc, SD Wind Energy Ltd., Ryse Energy, Aeolos Wind Energy Ltd., Eocycle Technologies Inc., Fortis Wind Energy, Endurance Wind Power, XZERES Corp., Kestrel Renewable Energy, Superwind GmbH |

SEGMENTAL ANALYSIS

By Axis Type Insights

The horizontal axis wind turbines dominated the Europe small wind turbine market and accounted for a substantial share in 2025. This dominance of the segment is mainly driven by its superior aerodynamic efficiency and higher energy yield compared to vertical-axis counterparts. The performance advantage makes them the preferred choice for rural and agricultural applications where maximizing power output is critical for economic viability. The mature manufacturing ecosystem for horizontal-axis turbines in Europe ensures reliable supply chains and competitive pricing. For instance, Germany and Denmark host several leading manufacturers who have refined blade design and generator technology over decades. Additionally, the widespread availability of technical expertise for installation and maintenance supports their adoption. Installers are more familiar with the structural requirements and electrical integration of horizontal-axis systems, reducing deployment risks. Consequently, the combination of higher efficiency, established supply chains, and standardized certification sustains the leadership of horizontal axis wind turbines in the European market. The cost-effectiveness and scalability of horizontal-axis wind turbines further reinforce their market leadership. Economies of scale in production have significantly reduced the unit cost of horizontal-axis turbines, making them more accessible to residential and commercial users. This reduction is attributed to advancements in material science, such as the use of lightweight composite blades and improved manufacturing techniques. For example, the use of carbon fiber reinforced polymers has allowed for longer blades that capture more wind without proportionally increasing weight or cost. Furthermore, horizontal axis turbines are available in a wide range of capacities from 1 kilowatt to 100 kilowatt,s allowing users to select systems that precisely match their energy needs. This scalability is particularly beneficial for farms and small industrial facilities that require customized solutions. Additionally, the modular nature of these systems facilitates easy expansion if energy demand increases. Consequently, the economic advantages and flexibility of horizontal-axis turbines ensure their continued dominance in the European small wind market.

However, the vertical axis wind turbines segment is predicted to witness the highest CAGR of 11.5% from 2026 to 2034 due to its suitability for urban environments where wind directions are turbulent, and space is limited. Unlike horizontal axis turbines, vertical axis models can capture wind from any direction without the need for a yaw mechanism,s making them ideal for rooftop installations in cities. Their compact and often artistic designs appeal to architects and building owners who prioritize aesthetics. For instance, in the Netherlands, several municipal buildings in Amsterdam have installed sculptural vertical-axis turbines that serve both functional and decorative purposes. Additionally, vertical axis turbines operate at lower rotational speeds, resulting in reduced noise emissions, which is crucial for densely populated areas. The World Health Organization guidelines on environmental noise favor these quieter models for residential zones. Consequently, the ability to integrate seamlessly into urban infrastructure and meet aesthetic and noise constraints drives the rapid expansion of this segment. Technological advancements in vertical-axis wind turbine design significantly contribute to their accelerated growth. Recent innovations have addressed historical issues related to low starting torque and efficiency, improving their performance in low wind speed conditions typical of urban areas. These improvements make them viable in regions previously considered unsuitable for wind energy. For example, in Sweden, researchers have developed helical blade designs that reduce vibration and enhance stability. Additionally, the integration of smart control systems allows vertical axis turbines to optimize blade pitch and generator load in real time, maximizing energy capture. These technological strides are supported by government grants for innovative renewable energy technologies. Furthermore, the modular design of many vertical-axis turbines simplifies transportation and installation, reducing logistical costs. Consequently, continuous innovation and ease of deployment fuel the rapid growth of the vertical axis segment.

REGIONAL ANALYSIS

United Kingdom Small Wind Turbine Market Analysis

The United Kingdom led the Europe small wind turbine market and captured a 24.1% share in 2025. This position of the UK market is attributed to its exceptional wind resources and strong policy support for decentralized energy. According to the UK Met Office, the average wind speed in the UK is among the highest in Europe, particularly in Scotland and coastal regions, making it ideal for wind energy generation. The UK government’s Smart Export Guarantee scheme provides financial incentives for households and businesses that export surplus electricity to the grid. Moreover, the government identifies that a substantial number of small-scale wind energy units have been deployed nationwide, contributing to the country’s decentralized power capacity. Additionally, the rural landscape of the UK, with its numerous farms and remote properties, offers ample space for installation. Agricultural advocacy groups note that a meaningful proportion of farming enterprises have integrated wind power into their operations to offset rising utility expenses and improve financial sustainability. The presence of established manufacturers and installers further supports market growth. The national trade body for wind power emphasizes that the sector supports thousands of jobs in manufacturing, installation, and maintenance, particularly benefiting rural and regional employment markets. Furthermore, the UK’s commitment to achieving net zero emissions by 2050 drives investment in diverse renewable technologies. The Committee on Climate Change indicates that distributed wind energy plays a crucial role in decarbonizing the heating and transport sectors through electrification. Consequently, the combination of favorable natural conditions, supportive policies, and industrial capacity solidifies the United Kingdom’s position as the dominant market for small wind turbines in Europe.

Germany Small Wind Turbine Market Analysis

Germany was the second largest country in the Europe small wind turbine market and occupied a share of 20.2% in 2025. This growth of the German market is supported by the country’s Energiewende policy, which prioritizes the transition to renewable energy sources. According to the German Federal Ministry for Economic Affairs and Climate Action, small wind turbines are recognized as a key component of the decentralized energy strategy. National renewable energy legislation offers financial frameworks—such as market premiums and targeted support for smaller units—that help stabilize the economic outcomes for investors in decentralized wind technology. Information from the German Wind Energy Association suggests that the deployment of smaller wind units has maintained a consistent and significant upward trend, driven by a growing demand for energy independence. The agricultural sector is a major contributor, with many farmers installing turbines to power irrigation systems and barns. The German Agricultural Society notes that a substantial number of farming operations have integrated wind power into their business models to reduce dependence on external energy providers and lower carbon footprints. Additionally, the industrial sector utilizes small wind turbines for onsite power generation to reduce carbon footprints. The Confederation of German Industries emphasizes the role of self-generated renewable energy in meeting corporate sustainability goals. Germany’s robust engineering sector supports the development of high-quality and efficient turbines. Companies like Enercon and Nordex have influenced global standards for small wind technology. Furthermore, public awareness campaigns have increased acceptance of small wind projects in rural communities. The German Environment Agency notes that community-owned wind projects have enhanced social acceptance. Consequently, the strong regulatory framework, industrial strength, and agricultural demand maintain Germany’s significant presence in the European market.

France Small Wind Turbine Market Analysis

France holds a notable share of the Europe small wind turbine market due to government incentives and a growing interest in energy independence among rural households. The French Environment and Energy Management Agency notes that while previous tax-based incentives have expired, new national grant programs now offer direct financial support to homeowners for specific sustainable energy upgrades. This financial support has stimulated demand, particularly in regions with consistent wind patterns such as Brittany and Normandy. The French Wind Energy Association observes a steady upward trend in the adoption of decentralized wind technology as more domestic users seek to diversify their energy sources. Additionally, the French government’s Multiannual Energy Program aims to increase the share of renewable energy in final consumption to 33 percent by 2030. This target encourages the deployment of diverse renewable technologies, including small wind. The agricultural sector in France is also adopting wind energy to power livestock facilities and processing units. The French Ministry of Agriculture highlights that a growing number of agricultural operations are incorporating wind power to improve their energy autonomy and reduce long-term costs. Furthermore, the rise of citizen energy communities has facilitated collective investments in small wind projects. The French National Federation of Local Public Energy Companies highlights that community-owned turbines enhance local engagement and acceptance. Despite some regulatory hurdles related to heritage sites, the market continues to expand. Consequently, the combination of fiscal incentives, policy targets, and community involvement drives the growth of the small wind turbine market in France.

Italy Small Wind Turbine Market Analysis

Italy is moving ahead steadfastly in the Europe small wind turbine market owing to its diverse geography and supportive regulatory framework. The country’s extensive coastline and mountainous regions offer varied wind resources suitable for small-scale applications. According to the Italian National Agency for New Technologies, Energy and Sustainable Economic Development, small wind turbines are increasingly used in off-grid locations such as islands and remote villages. National building renovation incentives have heightened public awareness of sustainable home technology, leading to increased exploration of various decentralized power options. Trade organizations for wind energy note a marked increase in public curiosity regarding small-scale systems following the introduction of major national sustainability initiatives. Additionally, the agricultural sector in southern Italy utilizes small wind turbines for water pumping and irrigation. Agricultural unions observe that many farms in the wind-rich southern regions are increasingly adopting wind power technology to stabilize their energy requirements. The tourism industry also contributes to demand, with hotels and resorts installing turbines to enhance their sustainability credentials. The Italian Federal Union of Public Tourism Professionals indicates that eco-friendly certifications are becoming a competitive advantage. Furthermore, local manufacturing capabilities support the supply of specialized turbines designed for Mediterranean wind conditions. The Italian Ministry of Economic Development promotes research and development in small wind technology through grants. Consequently, the unique geographical advantages, policy incentives, and sector-specific demands sustain Italy’s position in the European market.

Spain Small Wind Turbine Market Analysis

Spain is likely to expand notably in the Europe small wind turbine market from 2026 to 2034 due to growing adoption in rural and coastal areas. The country’s abundant wind resources, particularly in regions like Galicia and Andalusia, provide a favorable environment for small wind energy. The Spanish government’s Recovery Transformation and Resilience Plan includes funding for renewable energy projects in rural areas. The agricultural sector is a key driver with olive groves and vineyards utilizing small wind turbines for irrigation and processing. Additionally, the tourism sector in coastal regions is adopting wind energy to power hotels and recreational facilities. Furthermore, the decline in battery storage costs has made hybrid wind-solar systems more attractive. Consequently, the combination of natural resources, government support, and sector-specific applications supports the steady growth of the small wind turbine market in Spain.

COMPETITION OVERVIEW

The competition in the Europe small wind turbine market is characterized by a mix of established manufacturers and innovative startups striving for technological superiority and market share. Leading companies differentiate themselves through product reliability, efficiency, and aesthetic design, particularly for urban applications. The market sees intense rivalry between horizontal and vertical-axis turbine producers, each targeting specific customer segments based on site conditions and preferences. Price competition is moderate as buyers prioritize long-term performance and return on investment over initial cost. Brands with strong certification portfolios and proven track records gain a competitive edge in securing public and private contracts. Collaboration with research institutions drives innovation in materials and control systems, enhancing product capabilities. The fragmentation of the market allows niche players to thrive by specializing in unique applications such as marine or off-grid solutions. Regulatory compliance serves as a barrier to entry, ensuring that only high-quality products remain. Intellectual property protection is crucial for safeguarding proprietary technologies. Overall, the competitive landscape is dynamic with companies continuously adapting to changing regulatory environments and consumer demands for sustainable energy solutions.

KEY MARKET PLAYERS

A few major players of the Europe small wind turbine market include

- Siemens Gamesa Renewable Energy

- Vestas Wind Systems A/S

- Nordex SE

- Enercon GmbH

- Bergey Windpower Co

- Kingspan Group plc

- SD Wind Energy Ltd

- Ryse Energy

- Aeolos Wind Energy Ltd

- Eocycle Technologies Inc

- Fortis Wind Energy

- Endurance Wind Power

- XZERES Corp

- Kestrel Renewable Energy

- Superwind GmbH

Top Strategies Used by the Key Market Participants

Key players in the Europe small wind turbine market primarily focus on technological innovation and product differentiation to maintain a competitive advantage. Companies invest in research and development to improve efficiency in low wind speeds and reduce noise emissions. Strategic partnerships with local installers and energy service companies enhance market penetration and customer support. Manufacturers also emphasize certification and compliance with international standards to build trust and facilitate regulatory approval. Diversification into hybrid systems combining wind, solar, and storage addresses intermittency issues. Marketing efforts highlight sustainability and energy independence, appealing to environmentally conscious consumers. After-sales service and maintenance contracts provide recurring revenue streams and ensure long-term customer satisfaction. Expansion into emerging applications such as electric vehicle charging stations creates new growth opportunities. These strategies collectively drive resilience and adaptation in the evolving European renewable energy landscape.

Leading Players in the Europe Small Wind Turbine Market

- Ampair Wind Power Ltd is a prominent manufacturer based in the United Kingdom specializing in robust and reliable small wind turbines for diverse applications. The company contributes significantly to the global market by exporting high-quality horizontal axis turbines known for their durability in harsh marine and rural environments. Ampair strengthens its market position through continuous innovation in blade design and generator efficiency, ensuring optimal performance in low wind speeds. Recent actions include the launch of the Ampair 600 model, which features improved aerodynamics and reduced noise levels. The company actively collaborates with system integrators to provide comprehensive off-grid energy solutions. By focusing on long term reliability and minimal maintenance requirements, Ampair has built a strong reputation among residential and commercial users. Their commitment to sustainable manufacturing practices aligns with European environmental standards, enhancing brand loyalty. Additionally, Ampair provides extensive technical support and training for installers, ensuring proper deployment and operation. This customer-centric approach, combined with product excellence, solidifies their leadership in the European small wind sector.

- Windside Production Ltd from Finland is a leading innovator in vertical-axis wind turbine technology, renowned for its silent and aesthetically pleasing designs. The company plays a crucial role in the global market by providing solutions for urban and architectural applications where noise and visual impact are critical concerns. Windside strengthens its market position by targeting niche segments such as telecommunications towers, lighthouses, and historic buildings. Recent initiatives include the development of new composite materials that enhance durability while reducing weight. The company’s turbines are widely used in remote monitoring stations across Europe due to their ability to operate in turbulent wind conditions. Windside actively participates in research projects funded by the European Union to advance small wind technology. Their focus on quality and precision engineering has earned them certifications that facilitate market access in stringent regulatory environments. By emphasizing unique design and operational silence, Windside differentiates itself from competitors. This strategic focus on specialized applications and technological advancement ensures their continued relevance and growth in the European market.

- Eocycle Technologies Inc although headquartered in Canada, has established a significant presence in the European small wind turbine market through strategic partnerships and localized distribution. The company contributes to the global market by offering innovative vertical-axis turbines designed for easy installation and low maintenance. Eocycle strengthens its market position in Europe by collaborating with local energy providers and engineering firms to deploy units in commercial and industrial settings. Recent actions include the introduction of the EO 10 model, which features a direct drive generator eliminating the need for gearboxes. This design reduces mechanical failure risks and lowers operational costs. The company focuses on demonstrating the economic viability of small wind through pilot projects in France and the United Kingdom. Eocycle also invests in digital monitoring tools that allow users to track performance in real time. By addressing common pain points such as maintenance complexity, Eocycle appeals to business customers seeking reliable renewable energy sources. Their adaptive strategy and focus on user-friendly technology support their expanding footprint in the European region.

MARKET SEGMENTATION

This research report on the Europe small wind turbine market has been segmented and sub-segmented based on axis type & region.

By Axis Type

- Horizontal Axis Wind Turbine

- Vertical Axis Wind Turbine

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What are the key drivers of the market?

Key drivers include rising renewable energy adoption, supportive government policies, and increasing demand for off-grid power solutions.

2. What are the main applications of small wind turbines?

Applications include residential power generation, farms, remote areas, telecom towers, and small businesses.

3. What types of small wind turbines are available?

The main types are horizontal-axis wind turbines (HAWT) and vertical-axis wind turbines (VAWT).

4. Which segment dominates the market?

Horizontal-axis wind turbines dominate due to higher efficiency and widespread adoption.

5. What trends are shaping the market?

Key trends include hybrid renewable systems (wind + solar), smart monitoring systems, and improved turbine efficiency.

6. What challenges does the market face?

Challenges include high initial costs, regulatory barriers, and inconsistent wind availability.

7. What role does technology play in this market?

Technological advancements improve turbine efficiency, reduce maintenance costs, and enhance performance in low-wind conditions.

8. How does the market support sustainability goals?

Small wind turbines help reduce carbon emissions and support decentralized clean energy generation.

9. What opportunities exist in the Europe small wind turbine market?

Opportunities include rural electrification, smart grid integration, and increasing demand for energy independence.

10. Which countries lead the market in Europe?

The UK, Germany, and Denmark are leading markets due to strong renewable energy initiatives.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com