Europe Speaker Market Size, Share, Trends, & Growth Forecast Report By Type (Portable Speakers, Soundbars, Floor Standing Speakers, Subwoofers, Bookshelf Speakers, Others), Connectivity, Application and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

Europe Speaker Market Report Summary

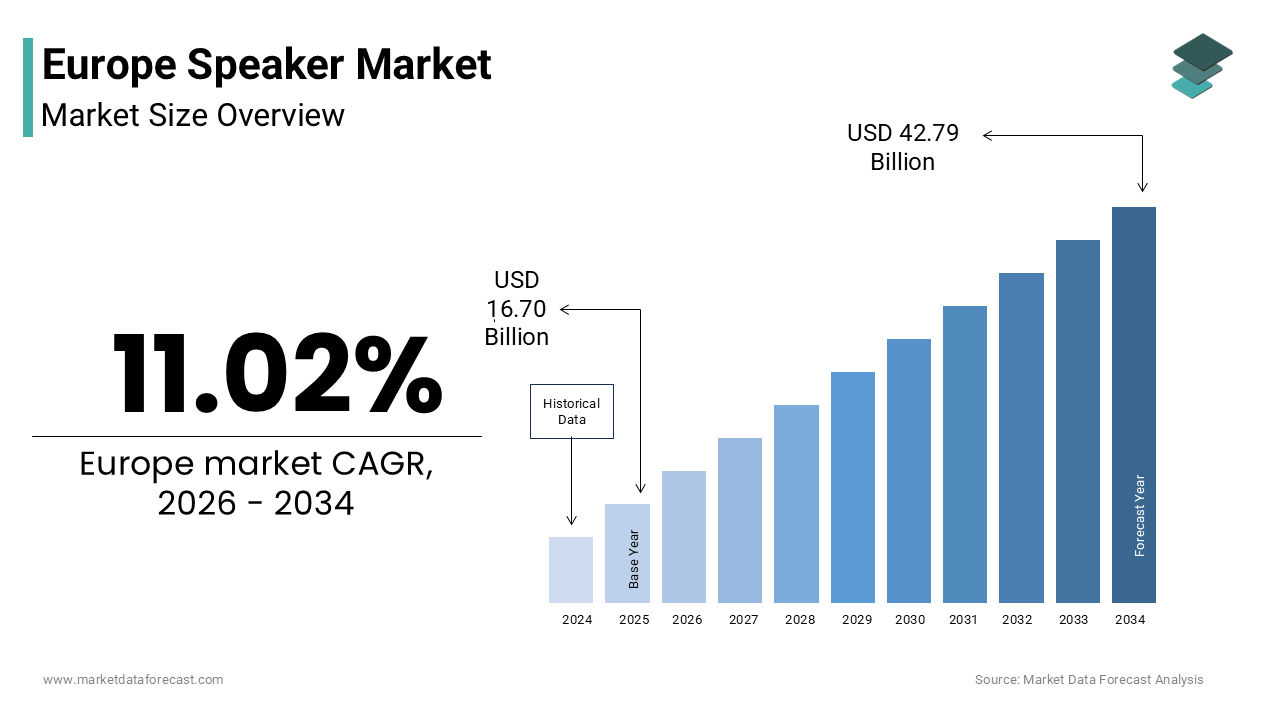

The Europe speaker market was valued at USD 16.70 billion in 2025, is expected to reach USD 18.55 billion in 2026, and is projected to grow to USD 42.79 billion by 2034, registering a CAGR of 11.02% from 2026 to 2034. The market growth is driven by the rising adoption of high-resolution audio streaming, increasing integration of smart home ecosystems, and growing demand for wireless and portable audio solutions. Additionally, strong digital connectivity and evolving consumer preferences for premium sound quality and sustainable products are further accelerating market expansion across Europe.

Key Market Trends

- Increasing demand for high-resolution and immersive audio formats (Dolby Atmos, spatial audio)

- Rising adoption of smart speakers and voice-controlled home ecosystems

- Growth of portable and outdoor speaker usage is driven by lifestyle trends

- Expansion of wireless connectivity and multi-room audio systems

- Increasing focus on sustainability, repairability, and eco-friendly materials

Segmental Insights

- Based on type, the soundbars segment held the largest share of 42.1% in 2025. This dominance is driven by the increasing adoption of slim televisions, which require external audio solutions to enhance sound quality.

- Based on connectivity, the wireless segment dominated the market with 64.2% share in 2025, driven by the widespread use of smartphones, streaming platforms, and preference for cable-free setups.

- Based on application, the home entertainment segment accounted for 58.7% of the market share in 2025, driven by increasing consumption of streaming content and demand for cinematic audio experiences at home.

Regional Insights

The Europe speaker market is expanding across key countries, supported by strong consumer demand, technological advancements, and lifestyle trends.

- Germany led the market with 26.3% share in 2025, driven by its strong automotive sector, advanced manufacturing base, and high demand for premium audio systems.

- United Kingdom held the second-largest share, supported by a strong music culture, early adoption of smart home devices, and a dynamic retail environment.

- France is witnessing steady growth due to demand for luxury and aesthetically designed audio products along with strong home cinema adoption.

- Italy is growing with increasing demand for designer speakers and the integration of modern audio systems in renovated living spaces.

- Spain is expected to expand rapidly due to outdoor lifestyle trends, tourism-driven demand, and rising adoption of portable speakers.

Competitive Landscape

The Europe speaker market is highly competitive, with global electronics companies and specialized audio brands competing on innovation, design, and ecosystem integration. Companies focus on wireless technologies, smart home compatibility, and sustainability to strengthen their market position. Strategic collaborations with automotive manufacturers and streaming platforms are further shaping the competitive landscape Key players in the Europe speaker market include Sony Group Corporation, Samsung Electronics Co., Ltd., LG Electronics Inc., Bose Corporation, Harman International Industries, Inc., Apple Inc., Amazon.com, Inc., Google LLC, Sonos, Inc., Panasonic Holdings Corporation, Philips (Koninklijke Philips N.V.), and Yamaha Corporation.

Europe Speaker Market Size

The Europe speaker Market size was valued at USD 16.70 billion in 2025 and is anticipated to reach USD 18.55 billion in 2026 from USD 42.79 billion by 2034, growing at a CAGR of 11.02% during the forecast period from 2026 to 2034.

A speaker refers to an electronic device that converts electrical signals into audible sound waves. This market encompasses a broad range of products, from everyday consumer electronics like portable Bluetooth speakers to specialized professional systems for live events and high-end audiophile equipment. This market is currently undergoing a paradigm shift driven by the convergence of high-resolution audio streaming, smart home integration, and stringent environmental regulations specific to the region. Unlike other global markets where volume often dictates trends, the European landscape is uniquely characterized by a discerning consumer base that prioritizes acoustic fidelity, sustainable manufacturing, and data privacy within connected audio ecosystems. According to Eurostat, 93% of households in the European Union had internet access in 2023 (rising to 94.2% in 2024), creating a robust infrastructure for streaming services that directly fuels the demand for high-quality playback hardware. Furthermore, the European Commission's Ecodesign for Sustainable Products Regulation (ESPR) entered into force in July 2024, establishing a framework to set rigorous sustainability requirements. Meanwhile, specific new rules adopted in 2023 for smartphones and tablets are already compelling manufacturers to improve durability, repairability, and battery longevity ahead of their 2025 implementation. Data from the International Telecommunication Union (ITU) indicates that internet use in Europe reached 91% of the population in 2024, with mobile broadband penetration exceeding 100 subscriptions per 100 inhabitants, facilitating the ubiquitous use of wireless audio devices across the continent. This intersection of advanced digital connectivity, regulatory pressure for circular economy practices, and a cultural appreciation for premium sound positions the region as a critical testing ground for next-generation audio technologies.

MARKET DRIVERS

Surge in High-Resolution Audio Streaming and Content Consumption

The exponential growth of lossless audio streaming services and immersive content formats drives demand for high-fidelity reproduction hardware.

The rapid adoption of high-resolution audio streaming platforms and the proliferation of immersive content formats, such as Dolby Atmos and spatial audio, are among the key reasons behind the growth of the Europe speaker market. This necessitates advanced speaker systems capable of reproducing nuanced soundscapes. European consumers are increasingly subscribing to premium tiers of music and video services that offer lossless and hi-res audio, rendering standard compression-compatible speakers inadequate for the full experience. According to the International Federation of the Phonographic Industry (IFPI), the number of paid music streaming subscriptions in Europe has continued its rapid expansion, with the region remaining a critical market for digital revenue. While standard audio tiers dominate, there is a gradual, emerging interest in high-resolution "lossless" formats among audiophiles. This shift is further amplified by the rise of 4K and 8K video content on platforms like Netflix and Disney Plus, which often include object-based audio tracks that demand multi-channel soundbar setups or surround sound systems to unlock their potential. The European Audiovisual Observatory reveals that subscription video-on-demand (SVOD) has achieved mass-market status, with the vast majority of European households now subscribing to at least one streaming service. This ubiquitous access to cinema-quality content is a key driver for the complimentary sales of enhanced home audio systems. The gap between standard built-in audio and external speakers is widening as more content is mixed for immersive formats. This shift is forcing both audiophiles and casual listeners to upgrade their gear to truly experience modern media.

Integration of Smart Home Ecosystems and Voice Control

The widespread deployment of interconnected smart home devices and voice assistants transforms speakers into central control hubs for domestic automation.

The deepening integration of speakers into comprehensive smart home ecosystems also fuels the expansion of the Europe speaker market. Here, they act as both audio output devices and primary voice-controlled interfaces for lighting, heating, security, and appliances. The European market has seen a surge in the adoption of platforms like Amazon Alexa, Google Assistant, and Apple HomeKit, making smart speakers an essential entry point for home automation. According to research, the installed base of smart home technology in Europe is growing exponentially, driven by the widespread adoption of connected appliances and security systems. Within this ecosystem, smart speakers continue to serve as a central control hub for many households. This utility extends beyond convenience; in an aging society, voice-controlled speakers provide critical accessibility features for elderly residents, allowing them to manage their environment and summon assistance without physical exertion. Reports derived from the European Commission's Digital Economy and Society Index (DESI) metrics suggest that while engagement with digital services is high, the specific use of voice assistants is establishing itself as a regular interaction model for a distinct segment of the population, reflecting a shift toward hands-free technology in daily life. Furthermore, the ability of modern speakers to act as intercoms and security monitors adds layers of functionality that justify their presence in every room. Interoperability standards like Matter are finally reducing fragmentation. As a result, the speaker’s role as the smart home's central hub will grow, fueling sustained demand across all price points.

MARKET RESTRAINTS

Stringent Environmental Regulations and Raw Material Constraints

Rigorous European Union sustainability mandates and scarcity of critical raw materials increase production costs and limit design flexibility.

An increasingly complex regulatory landscape is restricting the growth of the Europe speaker market. This shift is driven by the EU's Ecodesign for Sustainable Products Regulation and the Critical Raw Materials Act. These regulations impose strict requirements on material sourcing, recyclability, and repairability. Also, these regulations mandate that manufacturers design products with easily replaceable batteries and components, use recycled content, and provide detailed digital product passports, all of which significantly increase research and development expenditures and manufacturing complexity. According to the European Centre for Strategic Management of Critical Raw Materials, the EU imports over 90 percent of its rare earth elements, such as neodymium and dysprosium, which are essential for high-performance speaker magnets, leaving the supply chain vulnerable to geopolitical tensions and price volatility. Advocacy for Right-to-Repair legislation is driving a shift in electronic manufacturing. While these laws aim to extend product lifespans, they require manufacturers to adjust their design and assembly processes to ensure components are accessible, which can present a significant operational challenge for smaller enterprises. The requirement to phase out certain hazardous substances while maintaining acoustic performance creates a technical barrier, slowing down the introduction of innovative designs. Regulatory and supply chain pressures will continue to constrain market growth and profitability. This will persist until stable domestic sources are established or viable synthetic alternatives are perfected.

Acoustic Challenges in Urban Living Environments

The prevalence of compact living spaces and strict noise pollution ordinances in European cities limit the adoption of high-volume and large-format speaker systems.

The unique architectural and demographic reality of the region’s urban centers is further hindering the expansion of the Europe speaker market. High population density, compact housing units, and stringent noise control regulations restrict the usage of powerful or large-scale audio systems. A significant portion of the European population resides in apartments with thin walls and shared communal spaces, making the operation of high-fidelity floor-standing speakers or subwoofers at optimal volumes socially and legally problematic. According to the European Environment Agency, exposure to environmental noise remains a major health concern, with at least 100 million citizens affected, prompting many municipalities to enforce strict quiet hours and decibel limits that discourage the use of robust audio equipment. Data from Eurostat emphasizes that a significant portion of the European population resides in urban environments characterized by limited living space. The trend toward smaller, city-center apartments is driving a market preference for compact, high-efficiency audio solutions over traditional, large-format speaker installations. This spatial constraint forces consumers to prioritize compact, low-profile solutions like soundbars or portable Bluetooth speakers, which may compromise on acoustic depth and dynamic range compared to traditional hi-fi setups. The inability to fully utilize the capabilities of high-end audio gear in typical living conditions dampens the incentive for enthusiasts to invest in premium large-format systems, thereby capping the growth potential of the upper market segment.

MARKET OPPORTUNITIES

Expansion of Spatial Audio and Immersive Sound Technologies

The advent of object-based audio formats and 3D sound processing offers a transformative opportunity for premium multi-channel and soundbar systems.

The rapid commercialization of spatial audio and immersive sound technologies is providing major growth areas for the Europe speaker market. These innovations promise to revolutionize home entertainment by delivering three-dimensional soundscapes that mimic real-world acoustics. Unlike traditional channel-based audio, spatial audio uses object-based rendering to place sounds precisely in a 3D space, requiring specialized speaker configurations such as upward-firing drivers, satellite speakers, and advanced digital signal processing to achieve the intended effect. According to various sources, European consumers are increasingly investing in home cinema systems compatible with object-based audio formats. This trend is heavily supported by the growing library of immersive content provided by global streaming services and modern gaming hardware. This technology appeals strongly to the European desire for cinematic experiences at home, particularly in regions where visiting public cinemas may be less frequent due to geographic or economic factors. Data from the European Broadcasting Union indicates that an increasing number of live sports and cultural events are being broadcast in immersive formats, creating a fresh demand for upgrading legacy stereo systems. The shift to immersive audio is a major market opportunity, fueled by expanding content libraries and cheaper hardware. Manufacturers can now differentiate themselves by mastering superior acoustic engineering and software integration.

Growth of Portable and Outdoor Audio Lifestyles

The rising trend of outdoor socialization and mobile lifestyles creates lucrative demand for rugged, weather-resistant, and highly portable speaker solutions.

The escalating popularity of outdoor activities, al fresco dining, and mobile social gatherings offers a substantial opportunity for the Europe speaker market. This is driven by demand for durable, weather-proof, and battery-powered audio devices. Europeans increasingly value work-life balance and outdoor leisure, leading to a surge in camping, beach trips, park gatherings, and garden parties where portable audio is essential for ambiance. The European Outdoor Group (EOG) indicates that while the market has entered a period of stabilisation, there remains a clear preference for durable and weather-resistant consumer electronics. This has sustained interest in high-performance portable audio devices designed for use in rugged environments. The integration of solar charging capabilities and extended battery life in newer models further enhances their appeal for off-grid adventures, aligning with the region's strong environmental consciousness. Data from the European Travel Commission reveals that domestic tourism within Europe reached record levels in 2023, with travelers seeking compact entertainment solutions for road trips and holiday rentals. Additionally, the trend of "balcony culture" in dense urban areas has created a niche for compact, aesthetically pleasing outdoor speakers that comply with noise regulations while providing quality sound. This shift towards mobile and outdoor living expands the addressable market beyond the living room, opening new revenue streams for manufacturers who can blend durability, portability, and acoustic performance.

MARKET CHALLENGES

Complexity of Recycling Composite Audio Materials

The intricate combination of plastics, metals, fabrics, and electronic components in modern speakers poses a significant challenge to circular economy goals.

The technical difficulty of recycling the complex, composite materials used in modern construction is a major challenge for the European speaker market. This difficulty conflicts directly with the European Union’s ambitious zero-waste and circular economy targets. Modern speakers often integrate molded plastics, metal grilles, fabric coverings, foam surrounds, and embedded electronics into a single sealed unit, making separation and material recovery economically unviable with current industrial processes. According to the European Electronic Waste Recyclers Association, less than 20 percent of small consumer audio devices are effectively recycled, with the majority ending up in landfills or incinerators due to the high cost of delamination and component sorting. The new Ecodesign regulations mandate higher recycling rates and the use of mono-materials, yet achieving this without compromising acoustic damping properties or aesthetic appeal remains a formidable engineering hurdle. The Joint Research Centre of the European Commission indicates that the energy required to separate bonded materials in speakers often exceeds the energy saved by recovering the raw inputs, creating an environmental paradox. The market faces persistent regulatory scrutiny and reputational risks regarding its environmental footprint. This will continue until breakthroughs in chemical recycling or design-for-disassembly methodologies are widely adopted.

Fragmentation of Wireless Connectivity Standards

The lack of universal alignment in wireless audio protocols and codec support creates consumer confusion and limits interoperability between devices.

The escalating challenge of fragmentation in wireless connectivity standards and audio codecs impedes the expansion of the Europe speaker market. This creates significant compatibility issues and hinders the seamless user experience expected in a connected ecosystem. Bluetooth is everywhere, but the audio world is actually pretty confusing right now thanks to a mix of codecs like aptX and LDAC, plus Wi-Fi options like AirPlay and Chromecast. Because of this, you'll often find that not all speakers work perfectly with every device. The Bluetooth Special Interest Group (SIG) continues to drive the adoption of new standards, such as Auracast, to improve the wireless audio experience. However, the vast diversity of hardware and software versions in the market can still lead to occasional user frustration regarding seamless device pairing and feature support. Reports from the European Consumer Organisation (BEUC) suggest that consumers frequently encounter difficulties when integrating smart audio equipment into their existing digital ecosystems. These issues are often linked to software compatibility and the limited lifespan of firmware updates, which can prematurely affect the functionality of otherwise working hardware. This fragmentation forces manufacturers to license multiple technologies, increasing bill of materials costs, while consumers face the risk of purchasing hardware that may become obsolete or incompatible with future devices. The slow rollout of unified standards like Auracast promises relief, but the transition period prolongs market uncertainty and complicates product development strategies for companies trying to cater to a diverse range of user ecosystems.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 11.02% |

| Segments Covered | By Type, Connectivity, Application and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | Sony Group Corporation, Samsung Electronics Co., Ltd., LG Electronics Inc., Bose Corporation, Harman International Industries, Inc., Apple Inc., Amazon.com, Inc., Google LLC, Sonos, Inc., Panasonic Holdings Corporation, Philips (Koninklijke Philips N.V.), and Yamaha Corporation. |

SEGMENTAL ANALYSIS

By Type Insights

In 2025, the soundbars segment maintained dominance in the Europe speaker market and accounted for a 42.1% share. This segment dominates because the rapid decline of traditional receivers and the rise of ultra-slim TVs require external audio solutions. It is further fueled by the high demand for user-friendly, compact audio systems designed for European homes. Apart from these, a key driver for the dominance of soundbars is the unavoidable trade-off in modern television manufacturing where screens have become increasingly thin, leaving insufficient internal volume for high-quality speakers, thus creating a critical need for external audio solutions. As manufacturers prioritize 4K and 8K resolution panels with minimal bezels, the acoustic performance of built-in speakers has degraded significantly, often producing tinny sound with no bass response, which fails to match the visual fidelity of the content. The soundbar offers the most practical solution by delivering a substantial upgrade in dialogue clarity and dynamic range without the complexity of multi-component systems. A study indicates that streaming services now deliver content with higher bitrates and surround sound formats, making the limitations of TV speakers even more apparent. This technological divergence between visual excellence and audio inadequacy ensures that soundbars remain the default choice for enhancing the home viewing experience across the continent. A further key factor sustaining the market share of soundbars is their compact form factor and sleek design, which align perfectly with the spatial constraints and aesthetic preferences of European urban housing. With a significant portion of the European population residing in apartments and homes with limited floor space, bulky traditional speaker stacks and large receivers are often impractical or visually intrusive. Soundbars eliminate the need for extensive wiring and multiple speaker placements, offering a clutter-free setup that appeals to design-conscious consumers. Furthermore, the integration of wireless subwoofers allows users to place bass modules out of sight while still enjoying rich low frequencies. This combination of space-saving utility and aesthetic harmony cements the soundbar as the leading speaker type in the region.

The outdoor speakers segment is estimated to register the fastest CAGR of 11.4% during the forecast period due to the rising trend of al fresco living, the expansion of smart garden ecosystems, and advancements in weather-resistant materials that enable durable year-round installation. This segment is growing fast mostly because of the cultural shift towards outdoor living, where Europeans increasingly treat gardens, balconies, and patios as extensions of their indoor living spaces for dining, socializing, and relaxation. The post-pandemic era has intensified this trend, with homeowners investing heavily in landscaping and outdoor amenities to create private entertainment zones, driving demand for audio solutions capable of withstanding external elements. Consumers are seeking immersive experiences for backyard parties, summer dinners, and poolside gatherings, moving beyond portable Bluetooth units to permanent, high-fidelity installations. Research emphasizes that domestic tourism and staycations reached record levels, prompting households to upgrade their private outdoor environments to rival commercial venues. The availability of solar-powered and battery-operated outdoor speakers further facilitates this adoption by removing the barrier of complex electrical wiring in garden settings. As the concept of the "outdoor room" becomes standard in European real estate, the demand for specialized audio hardware designed for these environments will continue to surge. Also supporting this segment is the significant technological progress in materials science, enabling speakers to withstand harsh European weather conditions ranging from freezing winters to intense summer UV exposure. Modern outdoor speakers now utilize advanced polymers, marine-grade stainless steel, and UV-stabilized coatings that prevent degradation, rust, and color fading, ensuring long-term reliability and reducing replacement costs. These durability enhancements give consumers confidence to install speakers permanently in exposed locations without fear of damage from rain, snow, or humidity. Various sources indicate that extreme weather events have become more frequent, necessitating robust equipment that can endure such variability. Manufacturers are also integrating self-healing coatings and corrosion-resistant drivers specifically engineered for coastal and alpine regions. This evolution in build quality transforms outdoor speakers from seasonal novelties into permanent infrastructure investments, driving sustained growth and higher average selling prices in this rapidly expanding category.

By Connectivity Insights

The wireless connectivity segment led the Europe speaker market and captured a 64.2% share in 2025. This leading position of the segment is attributed to the ubiquity of smartphones, the proliferation of high-speed Wi-Fi networks, and the consumer preference for cable-free setups that offer flexibility and ease of use. The proliferation of wireless connectivity is largely sustained by the pervasive adoption of smartphones and the dominance of streaming platforms. These factors have made wired connections obsolete for the majority of daily listening scenarios. Consumers expect seamless, instant connectivity between their mobile devices and audio systems, utilizing protocols like Bluetooth, Wi-Fi, and AirPlay to stream content from services such as Spotify, Apple Music, and Tidal without physical tethering. According to studies, paid music streaming subscriptions in Europe reached a significant level in 2023, with a large share of listening hours occurring on mobile devices. This behavioral shift necessitates speakers that can easily pair with handheld sources, allowing users to move freely around their homes while maintaining uninterrupted audio playback. The convenience of casting music from any room and the ability to control playback via voice assistants further reinforce the preference for wireless solutions. As content consumption becomes increasingly mobile-centric, the demand for speakers that integrate effortlessly into this digital ecosystem ensures wireless technology remains the market leader. Further boosting this segment is the strong consumer desire for minimalist interiors and the freedom to place speakers anywhere without the constraint of proximity to power outlets or audio sources. European design trends heavily favor clean lines and uncluttered spaces, making the elimination of visible cables a priority for homeowners and interior designers alike. Wireless speakers allow users to position audio units in optimal acoustic locations or move them between rooms for different activities, such as taking music from the kitchen to the garden, without rewiring. The advancement of battery technology, offering longer playtimes on single charges, further supports this trend by decoupling speakers from fixed power sources. This alignment with modern lifestyle needs and design preferences secures the leading position of wireless speakers in the European market.

The wired segment is anticipated to witness the fastest CAGR of 8.2% over the forecast period owing to the resurgence of high-fidelity audiophile culture, the professional installation sector, and the need for latency-free connections in gaming and studio environments. One key factor helping this segment is the renewed interest among audiophiles and music enthusiasts in lossless, high-resolution audio reproduction, which often requires the stability and bandwidth of physical connections to achieve maximum fidelity. While wireless technologies have improved, purists argue that wired connections using high-quality cables eliminate potential compression, interference, and latency issues inherent in wireless transmission, delivering the purest possible sound signal. The availability of high-resolution audio files and streaming tiers has heightened awareness of audio quality gaps, prompting serious listeners to revert to wired setups for their main systems. Data from Yole Intelligence suggests that the market for high-end DACs (Digital-to-Analog Converters) and interconnects is expanding rapidly, supporting the infrastructure needed for wired speaker configurations. This niche but lucrative segment values performance over convenience, ensuring steady growth for wired solutions as consumers seek to unlock the full potential of their high-end audio collections. Also helping this segment is the persistent demand in professional installation sectors and competitive gaming communities where reliability, synchronization, and zero latency are non-negotiable. In commercial spaces, cinemas, and large-scale home theater installations, wired connections ensure synchronized audio across multiple zones without the risk of dropouts or interference that can plague wireless networks. Besides, the esports and competitive gaming sectors require absolute audio precision with no lag, making wired headsets and monitor speakers the preferred choice for serious gamers who cannot afford even millisecond delays. Furthermore, new building regulations in some European countries mandate structured cabling for new constructions, facilitating wired audio integration. These professional and performance-driven requirements ensure that wired connectivity remains a vital and growing segment despite the wireless boom.

By Application Insights

The home entertainment application segment held the majority share 58.7% of the Europe speaker market in 2025. Factors such as the centrality of media consumption in daily life, the upgrade cycle triggered by large-screen TV adoption, and the desire for cinematic experiences within the home are supporting the supremacy of this segment. A main reason for the segment's success is the massive shift in consumption habits towards streaming video services and binge-watching, which has transformed the living room into the primary venue for movie and series consumption. As households cancel traditional cable subscriptions in favor of platforms like Netflix, Disney Plus, and Amazon Prime Video, the expectation for theater-quality audio to accompany high-definition visuals has skyrocketed. The abundance of high-quality content, often mixed in Dolby Atmos or surround sound formats, creates a compelling need for upgraded speaker systems to fully appreciate the production value. The inadequacy of built-in TV speakers for dialogue clarity and immersive effects forces consumers to invest in soundbars and surround systems. This deep integration of streaming into daily routines ensures that home entertainment remains the largest application area for speakers across the continent. Following this, the segment is backed by the widespread adoption of large-screen televisions exceeding 55 inches and the proliferation of 4K and 8K content, which creates a disproportionate mismatch with internal TV audio capabilities. As screen sizes increase to fill living room walls, the physics of thin panel design prevents the inclusion of adequate speakers, resulting in audio that feels disconnected from the expansive visual experience. Consumers purchasing these premium displays are increasingly aware that the audio experience lags behind the visual fidelity, prompting immediate upgrades to external speaker systems to restore balance. The desire to replicate the cinema experience at home, especially for sports and blockbuster movies, drives continuous investment in multi-channel audio setups. This symbiotic relationship between large display adoption and audio enhancement secures the leading position of the home entertainment segment.

The automotive application segment is likely to experience the fastest CAGR of 13.5% from 2026 to 2034. This explosive growth of the segment is fuelled by the electrification of vehicle fleets, the transformation of cars into "third living spaces," and the integration of sophisticated premium audio brands as standard features in new models. A key reason this segment is doing well is the rapid transition to electric vehicles (EVs), which lack the engine noise of internal combustion cars, thereby exposing road, wind, and tire noise that must be actively managed through advanced audio systems. In EVs, speakers are not only used for entertainment but also play a critical role in Active Noise Cancellation (ANC) systems that generate anti-phase sound waves to silence unwanted frequencies, creating a serene cabin environment. The absence of engine masking noise also means that music playback must be of higher fidelity to satisfy passengers, driving the inclusion of more speakers and higher wattage amplifiers. Also, the dual requirement for noise management and enhanced audio quality ensures that the automotive sector becomes the fastest-growing application for speaker technology. A further point supporting this is the strategic trend of automakers partnering with prestigious audio brands to differentiate their vehicles and elevate the interior experience to that of a luxury lounge. Car manufacturers are increasingly marketing their vehicles as "third living spaces" where occupants can enjoy concert-hall quality sound, leading to the standard inclusion of branded systems from companies like Bang & Olufsen, Bose, Meridian, and Burmester even in non-luxury segments. The premiumization strategy appeals to European consumers who spend significant time commuting and view high-quality audio as a essential comfort feature rather than a luxury extra. Automakers are adding more speakers, subwoofers, and 3D audio capabilities to meet intense market competition and consumer expectations. Consequently, the automotive speaker market is experiencing substantial volume growth.

REGIONAL ANALYSIS

Germany Speaker Market Analysis

Germany was the top performer in the Europe speaker market and occupied a share of 26.3% in 2025. The demand for speakers in Germany is credited to its powerful automotive sector, which drives massive demand for advanced in-vehicle speaker systems, and a consumer base that prioritizes technical specifications and sound accuracy in home audio purchases. The country's leading position is built on its status as Europe's biggest economic power, its prominence in automotive engineering, and a rich, deeply rooted culture of audio appreciation. Moreover, the country is home to renowned audio brands and a dense network of specialized hi-fi retailers who cater to a discerning clientele willing to invest in premium equipment. Furthermore, the German tradition of "HiFi" culture ensures a steady market for high-end standalone speakers and amplifiers, with consumers viewing audio equipment as a long-term investment. The strong industrial base also supports the development of cutting-edge speaker technologies, from automotive ANC systems to professional installation gear. This combination of automotive strength, cultural appreciation for sound, and economic power ensures Germany remains the primary engine of the European speaker market.

United Kingdom Speaker Market Analysis

The United Kingdom was the second largest market speakers in Europe and accounted for a 18.5% share in 2025. This growth of the UK market is driven by its vibrant music heritage, early adoption of smart home technologies, and a robust retail sector that promotes innovative audio products. The UK market owes its strength to a rich musical heritage and a vibrant live music scene. Consequently, this environment fosters intense consumer engagement with audio quality, driving substantial demand for both professional and consumer speakers. The country is a leader in smart home adoption, with British consumers quickly embracing voice-controlled speakers and multi-room audio ecosystems from brands like Sonos and Amazon. Additionally, the competitive retail landscape, including major electronics chains and online platforms, ensures wide availability and aggressive promotion of the latest speaker technologies. The prevalence of music festivals and home entertainment culture further stimulates sales of portable and party speakers. This blend of musical passion, technological readiness, and retail dynamism positions the UK as a critical and dynamic market for speakers in Europe.

France Speaker Market Analysis

France plays a major role in the Europe speaker market due to its strong luxury goods sector, government support for cultural industries, and a growing emphasis on home cinema and aesthetic design. France's market strength is supported by its reputation as a global center for luxury and design, which influences the speaker market towards high-end, aesthetically pleasing products that double as furniture pieces. French consumers often prioritize the visual integration of speakers into their decor, driving demand for designer brands and custom installation solutions that blend seamlessly with interior styles. According to sources, the government's support for the audiovisual sector encourages the consumption of high-quality content, indirectly boosting the market for premium playback equipment. The country also has a strong tradition of home cinema, with many households investing in comprehensive surround sound systems to enjoy films in privacy. The presence of historic audio brands and a sophisticated consumer base that values craftsmanship ensures a steady demand for premium speaker solutions. This fusion of design consciousness, cultural policy, and home entertainment trends keeps France as a pivotal market in Western Europe.

Italy Speaker Market Analysis

Italy grew steadily in the European market owing to its global leadership in industrial design, which extends to the audio sector where speakers are often treated as art objects, commanding premium prices for their aesthetic and acoustic qualities. It is characterized by its world-renowned design heritage, a passion for music and opera, and increasing adoption of smart audio solutions in modern living spaces. Italian consumers have a deep appreciation for music, from classical opera to modern pop, fostering a culture that values high-fidelity reproduction and emotional engagement with sound. The trend towards renovating historic homes with modern technology has also spurred demand for discreet, high-performance in-wall and invisible speakers that preserve architectural integrity. In addition, the strong influence of Italian design houses entering the audio market adds a unique local flavor that distinguishes it from other regions. This intersection of artistic heritage, musical passion, and modernization ensures Italy remains a key growth market for speakers in Southern Europe.

Spain Speaker Market Analysis

Spain is likely to expand significantly in the European market from 2026 to 2034 due to its lifestyle-oriented culture where social gatherings, outdoor dining, and beach activities are central to daily life, driving robust demand for portable, rugged, and weather-resistant speakers. It is distinguished by its vibrant social culture, booming tourism industry, and increasing demand for portable and outdoor audio solutions for hospitality and residential use. The country's massive tourism sector also contributes significantly, with hotels, resorts, and restaurants investing heavily in commercial audio systems to enhance guest experiences in pools, terraces, and common areas. Furthermore, the growth of the rental market and holiday homes has stimulated demand for easy-to-install wireless audio systems that can be moved or upgraded easily. The popularity of music festivals and nightlife also sustains a market for professional PA and party speakers. This combination of climatic advantages, tourism-driven commercial demand, and a socially active population ensures Spain remains a vital and evolving market for speakers in the region.

COMPETITIVE LANDSCAPE

The competition in the Europe speaker market is characterized by intense rivalry among established global brands and agile local specialists vying for dominance in specific segments like smart home audio and automotive sound systems. Large multinational corporations leverage their extensive distribution networks and strong brand recognition to secure prime shelf space in major electronics retailers and partnership deals with car manufacturers across the continent. This trend towards integrated ecosystems creates high barriers to entry for smaller firms unless they possess highly differentiated acoustic technologies or unique design aesthetics that appeal to discerning European tastes. The competitive landscape is further complicated by stringent European Union safety regulations and emerging sustainability mandates which demand rigorous testing and certification before market approval. Companies must therefore invest significantly in research and development to demonstrate superior sound quality and environmental compliance while navigating complex procurement processes. Innovation speed and the ability to provide localized customer support are critical differentiators that determine market success. Furthermore, strategic alliances between speaker makers and streaming service providers have become essential for accessing exclusive content features to accelerate product adoption. The market remains dynamic with continuous entries of sustainable and smart audio solutions challenging traditional standards and reshaping competitive dynamics across the region.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe speaker market include

- Sony Group Corporation

- Samsung Electronics Co., Ltd.

- LG Electronics Inc.

- Bose Corporation

- Harman International Industries, Inc.

- Apple Inc.

- Amazon.com, Inc.

- Google LLC

- Sonos, Inc.

- Panasonic Holdings Corporation

- Philips (Koninklijke Philips N.V.)

- Yamaha Corporation

Top Players in the Europe Speaker Market

Sonos Inc

Sonos Inc stands as a global pioneer in wireless multiroom audio with a profound impact on the European speaker landscape through its seamless ecosystem of smart speakers and soundbars. The company contributes significantly to the global market by setting industry standards for high fidelity streaming and intuitive user interfaces that integrate diverse music services. Recently Sonos has strengthened its position by launching next generation portable speakers featuring advanced Bluetooth connectivity and improved battery life specifically tailored for European outdoor lifestyles. The firm actively collaborates with major European retailers to create immersive listening rooms that showcase the versatility of their multiroom setups. These strategic initiatives ensure their technology remains at the forefront of home audio innovation while addressing the growing consumer demand for flexible and high quality wireless sound solutions across the continent.

Harman International Industries Inc

Harman International Industries Inc operates as a leading innovator in connected audio solutions with a dominant presence in the European market particularly within automotive and premium home entertainment sectors. The company contributes globally by delivering sophisticated speaker systems branded under JBL, Bang and Olufsen, and Mark Levinson that define luxury audio experiences. Their recent actions to solidify market presence include expanding partnerships with European electric vehicle manufacturers to integrate custom tuned sound systems into new car models. Harman has also invested heavily in developing sustainable manufacturing processes using recycled materials to align with strict European environmental regulations. The firm frequently engages in collaborations with music festivals and events to demonstrate the power of their professional grade audio equipment. By focusing on acoustic excellence and brand prestige Harman enhances value for customers seeking superior sound quality. These efforts demonstrate their commitment to driving technological advancement and maintaining leadership in the competitive European arena.

Bose Corporation

Bose Corporation is a specialized audio technology company that has established itself as a key player in the European market through its focus on noise cancellation and compact speaker designs. The company makes a substantial global contribution by providing innovative soundbars and portable speakers that deliver immersive audio in small form factors ideal for urban living spaces. Their recent strategy to strengthen their European position involves introducing smart home speakers with enhanced voice assistant integration and spatial audio capabilities tailored for modern apartments. Bose has also expanded its retail footprint across major European cities to offer personalized fitting sessions and acoustic consultations. The firm continues to invest in research and development for proprietary algorithms that optimize sound performance in various room environments. By maintaining a dedicated focus on user experience and acoustic clarity Bose addresses the evolving needs of consumers who prioritize quality and convenience. Their persistent innovation in noise management and miniaturization ensures they remain a vital partner for individuals seeking premium audio solutions.

Top Strategies Used by Key Market Participants

Key players in the Europe speaker market predominantly employ strategic product differentiation and sustainability integration to secure supply chains and meet escalating regional demand for eco-friendly audio solutions. Companies frequently invest millions in developing speakers made from recycled plastics and biodegradable materials to comply with strict European Union environmental regulations and appeal to conscious consumers. Another major strategy involves forming deep collaborative partnerships with automotive original equipment manufacturers and smart home platform providers to co-develop customized audio systems that ensure perfect compatibility and seamless user experiences. Market participants also focus heavily on expanding their direct-to-consumer online channels to offer wider variety and competitive pricing while gathering valuable customer data for future product development. Investment in research and development remains a cornerstone strategy as firms strive to achieve breakthroughs in spatial audio processing and wireless connectivity standards. Additionally, companies pursue targeted acquisitions of niche software startups to rapidly incorporate advanced voice control and room calibration algorithms into their existing hardware platforms. These combined approaches allow industry leaders to navigate complex regulatory landscapes while maintaining a competitive edge in this rapidly evolving technological sector.

RECENT MARKET DEVELOPMENTS

- In September 2023, Sonos, a wireless audio specialist, launched the Move 2 portable speaker with significantly enhanced 24-hour battery life in Germany and globally. This product launch allows Sonos to better cater to outdoor lifestyles and strengthen its European speaker market presence.

- In June 2023, Harman International, a connected audio leader, deepened its automotive ties when Volvo Cars, a major Swedish electric vehicle manufacturer, revealed the Volvo EX30 featuring a custom Harman Kardon soundbar system. This partnership allows Harman International to secure key automotive contracts and strengthen its European market presence.

- In September 2023, JBL (Harman), a leading audio brand, executed a high-profile brand activation during Paris Fashion Week in France, showcasing its latest audio-wearables. This marketing move allowed the brand to enhance customer engagement and strengthen its European speaker market presence (Note: Bose closed its European retail stores in 2020).

- In November 2024, Sonos, a global innovator, launched its "Elves of Sound" global marketing campaign to promote its home theater and multiroom audio capabilities for the festive season. This initiative allowed Sonos to demonstrate audio quality to a wider audience and strengthen its European market presence.

- In January 2024, Harman Professional, a premium audio provider, appointed Exhibo and Adagio Italia as new strategic distributors in Italy. This restructuring is anticipated to allow Harman International to streamline operations, improve product availability, and strengthen its European speaker market presence.

MARKET SEGMENTATION

This research report on the Europe renal dialysis market has been segmented and sub-segmented based on the following categories.

By Type

- Portable Speakers

- Soundbars

- Floor Standing Speakers

- Subwoofers

- Bookshelf Speakers

- Others

By Connectivity

- Wired

- Wireless

By Distribution Channel

- Online

- Offline

By Application

- Home Entertainment

- Office

- Automotive

- Commercial Spaces

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com