Europe Specialty Chemicals Market Size, Share, Trends and Growth Forecasts Research Report, Segmented By Product and Country – Industry Analysis (2026 to 2034)

Europe Specialty Chemicals Market Report Summary

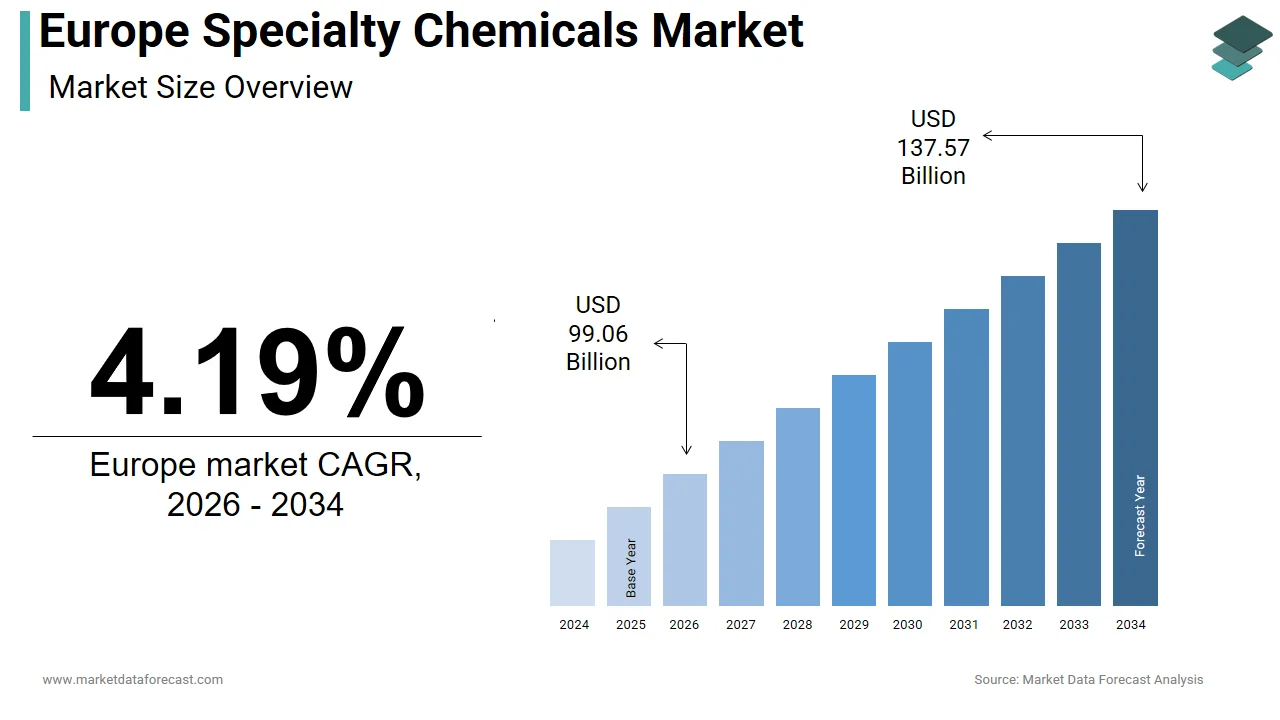

The Europe specialty chemicals market was valued at USD 95.08 billion in 2025, is estimated to reach USD 99.06 billion in 2026, and is projected to grow to USD 137.57 billion by 2034, registering a CAGR of 4.19% from 2026 to 2034. Market growth is driven by stringent EU environmental regulations, rising demand for high-performance materials, and the region’s strategic focus on sustainability, circular economy integration, and technological sovereignty. Specialty chemicals remain critical enablers across automotive, construction, electronics, agriculture, personal care, and advanced manufacturing applications.

Key Market Trends

-

Accelerated shift toward green chemistry and bio-based formulations driven by EU sustainability mandates.

-

Rising demand for high-purity and performance chemicals in semiconductors, renewable energy, and electric mobility.

-

Increasing adoption of chemical recycling and circular feedstock integration.

-

Growing influence of green public procurement on construction, coatings, and cleaning chemicals.

-

Intensifying competition from Asian specialty chemical suppliers offering cost-competitive alternatives.

Segmental Insights

-

Based on product:

-

The polymers & plastic additives segment held the largest share at 18.2%, driven by regulatory pressure on recyclability, packaging sustainability, and performance enhancement across automotive and consumer goods.

-

-

Fastest-growing segment:

-

The electronic chemicals segment is expected to register the fastest CAGR, supported by the European Chips Act, expansion of semiconductor fabs, and rising demand for ultra-high-purity materials.

-

Regional Insights

The Europe specialty chemicals market is witnessing steady growth across major industrial economies, supported by advanced manufacturing clusters, strong regulatory frameworks, and innovation-driven ecosystems.

- Germany led the market, supported by its integrated chemical parks, automotive and industrial demand, and skilled workforce pipeline.

- France holds a strong position due to leadership in agrochemicals, cosmetics actives, and electronic materials, backed by state-led industrial policy.

- The United Kingdom remains influential in life sciences, advanced materials, and specialty pharmaceutical intermediates, supported by strong research output despite regulatory divergence.

- Italy is expanding steadily, driven by fine chemicals for pharmaceuticals, textiles, and construction additives aligned with its manufacturing heritage.

Competitive Landscape

The Europe specialty chemicals market is characterized by layered competition among multinational leaders, regional innovators, and niche specialists. Large players leverage scale, regulatory expertise, and integrated production to dominate high-barrier segments, while mid-sized and niche firms focus on application-specific innovation and sustainability-led differentiation. Regulatory complexity under REACH and the Chemicals Strategy for Sustainability both protects incumbents and raises entry barriers. Increasing competition from Asian suppliers and the rise of bio-based startups are reshaping pricing power and innovation strategies across the region.

Prominent companies operating in the Europe specialty chemicals market include BASF SE, Akzo Nobel N.V., Bayer AG, Eastman Chemical Company, The Dow Chemical Company, Solvay, Chemtura Corporation, DuPont, Albemarle Corporation, Clariant AG, Chevron Phillips Chemical Company, Ashland Inc., Huntsman Corporation, INEOS Group AG, Evonik Industries AG, and Syngenta AG.

Europe Specialty Chemicals Market Size

The Europe specialty chemicals market was valued at USD 95.08 billion in 2025, is estimated to reach USD 99.06 billion in 2026, and is projected to reach USD 137.57 billion by 2034, growing at a CAGR of 4.19% from 2026 to 2034.

The specialty chemicals are high-value formulations engineered for specific performance functions across diverse industrial and consumer applications, including agrochemicals, electronic materials, construction additives, personal care actives, and advanced polymers. In 2025, the sector operates under intensifying regulatory scrutiny and sustainability imperatives that redefine innovation trajectories. According to Eurostat, over 170000 chemical substances are registered under the EU’s REACH regulation, with nearly 4500 classified as substances of very great concern as per the European Chemicals Agency. The region hosts more than 28000 chemical enterprises, the vast majority of which are small and medium-sized enterprises deeply integrated into localized value chains, as documented by the European Commission’s Industrial Ecosystems Report. Furthermore, the EU imported 38% of its key organic chemical intermediates from outside the bloc in 2023 as per the Joint Research Centre, underscoring strategic dependencies that influence supply resilience and innovation sovereignty in specialty segments.

MARKET DRIVERS

Stringent EU Environmental Regulations Are Catalyzing Green Chemistry Innovation

The European Union’s regulatory architecture is the single most powerful force reshaping specialty chemicals demand toward sustainable alternatives. The increasing environmental regulations from the government bodies are greatly influencing the growth of the Europe specialty chemicals market. The Chemicals Strategy for Sustainability, launched in 2020, aims to eliminate all non-essential uses of substances of very great concern by 2030. This has accelerated the adoption of bio-based surfactants, with the European Bioplastics Association confirming that bio-based specialty chemical output grew by 14% year on year in 2024. The EU’s Ecolabel criteria now cover 23 product groups requiring formulations to meet strict aquatic toxicity and biodegradability thresholds. Additionally, the Industrial Emissions Directive mandates best available techniques for chemical plants, leading to a 22% reduction in VOC emissions from specialty chemical facilities between 2020 and 2024. These regulations function not as barriers but as innovation mandates compelling formulators to embed circularity and non-toxicity into molecular design from inception.

Growth in High-Tech Manufacturing Is Elevating Demand for Performance Chemicals

Europe’s strategic push toward technological sovereignty is driving robust demand for specialty chemicals in semiconductors, renewable energy, and electric mobility. The growing high-tech manufacturing is elevating demand for performance chemicals, which is expected to boost the growth of the Europe specialty chemicals market. The European Chips Act allocated €43 billion through 2030 to rebuild wafer fabrication capacity, directly boosting demand for high-purity photoresists, etchants, and CMP slurries. Similarly, the EU’s Net Zero Industry Act targets 40% domestic manufacturing of solar photovoltaics by 2030, requiring advanced encapsulants anti anti-reflective coatings, and conductive inks. In electric vehicles, specialty electrolyte binders and thermal interface materials are crucial, with 2.8 million battery electric vehicles sold in the EU in 2024 as per the European Automobile Manufacturers Association. The need for high-performance battery chemicals has surged.

MARKET RESTRAINTS

Raw Material Volatility and Geopolitical Dependencies Impair Cost Stability

The increasing concern from unstable access to feedstocks exacerbated by geopolitical fragmentation is restricting the growth of the Europe specialty chemicals market. Over 60% of the EU’s benzene and toluene key aromatics for performance polymers and agrochemicals are derived from imported crude oil and naphtha, with Russia historically supplying 28% of pre-2022 volumes, as per the recent survey. Although diversification has reduced Russian crude imports to under 5% by 2024, alternative sources from the Middle East and the United States have increased freight and refining costs by 19%. Moreover, the EU relies on China for 98% of its rare earth elements essential for catalysts and phosphors, as documented by the European Raw Materials Alliance. Export controls imposed by China in 2023 caused europium oxide prices to spike by 320% within six months, per the Joint Research Centre. This dependency forces specialty formulators to absorb cost shocks or reformulate under time pressure. Additionally, the EU’s carbon border adjustment mechanism adds compliance complexity for imported intermediates, further distorting input economics. These structural vulnerabilities constrain R&D predictability and erode margins, particularly for small and medium enterprises lacking hedging capabilities.

Labor and Skills Shortages Hamper Innovation and Operational Continuity

The acute shortage of skilled personnel across research, manufacturing, and regulatory compliance functions is also limiting the growth of the Europe specialty chemicals market. The European Chemical Industry Council reported in 2024 that 44% of chemical companies in Germany, France, and Italy faced unfilled technical positions in process engineering and analytical chemistry. The shortage directly impacts innovation velocity; companies like Clariant and Evonik have delayed pilot plant launches due to the inability to staff advanced control rooms. Furthermore, regulatory complexity under REACH and CLP demands specialized toxicology and data management expertise, which is increasingly outsourced at premium costs.

MARKET OPPORTUNITIES

Circular Economy Mandates Are Unlocking New Revenue from Chemical Recycling

The EU’s binding targets for circularity are transforming waste streams into strategic feedstock sources for specialty chemicals, with is sole purpose of creating new opportunities for the growth of Europe's specialty chemicals market. Companies like BASF and LyondellBasell now operate commercial pyrolysis and depolymerization units in Germany and the Netherlands, converting mixed plastic waste into naphtha and monomers for high-purity applications. The EU’s End of Waste criteria, finalized in 2023, legally recognize outputs from approved chemical recycling processes as a virgin equivalent, enabling use in food contact and medical applications. Additionally, the European Commission’s Innovation Fund granted €280 million in 2024 to seven chemical recycling projects focused on polyurethanes and composites. These initiatives not only reduce fossil dependency but also create premium-priced circular product lines meeting corporate sustainability commitments from brands like L’Oréal and Siemens.

Expansion of Green Public Procurement Is Creating Institutional Demand Pull

Europe’s public sector is emerging as a powerful catalyst for sustainable specialty chemicals, through mandatory green procurement criteria are also steadily propelling the growth of Europe's specialty chemicals market. The EU’s revised Green Public Procurement framework, effective from 2024, requires all public construction projects to use building materials with Environmental Product Declarations and low embodied carbon. As per the European Commission, public procurement accounts for 14% of EU GDP or approximately €2.1 trillion annually. This has directly boosted demand for bio-based adhesives, low VOC coatings, and flame retardants free of halogenated compounds. In France, the Elan Law mandates that public buildings incorporate at least 30% bio-sourced materials by 2025, driving a 33% year-on-year increase in bio polyol sales for insulation foams, according to the French Environment and Energy Management Agency. Similarly, Germany’s federal procurement guidelines now exclude cleaning formulations containing phosphates or alkylphenol ethoxylates, benefiting producers of enzymatic and plant-derived alternatives.

MARKET CHALLENGES

Intensifying Global Competition Is Compressing Pricing Power

European specialty chemical producers face mounting pressure from well-capitalized Asian competitors offering comparable performance at significantly lower prices. The intensifying global competition is likely to prompt Chinese firms such as Wanhua Chemical and Zhenjiang Denka have expand their European footprint by establishing technical service centers and local blending facilities, reducing import barriers. According to the recent study, Chinese exports of specialty polymers to the EU grew by 29% in 2024, while average unit values declined by 11% indicating aggressive pricing strategies. Simultaneously, Indian companies like Atul and PI Industries leverage lower regulatory compliance costs to supply agrochemical intermediates and dyes at margins unattainable for EU-based manufacturers. The European Chemical Industry Council noted that European producers lost over 12% of the industrial surfactant market to Asian imports between 2021 and 2024. Unlike commodity chemicals, where scale dictates cost, specialty segments are vulnerable because performance differentials can be narrow and certification timelines lengthy.

Fragmented Regulatory Implementation Across Member States Delays Market Access

The disparities in national enforcement of chemical regulations create commercial inefficiencies and fragmentation, which will also decline the growth of the Europe specialty chemicals market in the coming years. While REACH is a single regulatory framework, its implementation varies notably in classification, labeling, and enforcement timelines. A specialty adhesive approved in the Netherlands may require reformulation for sale in Poland due to divergent interpretations of non-intentionally added substances. This regulatory asymmetry increases compliance costs, where a 2024 study by the European Chemical Industry Council found that SMEs spend on average €180000 annually managing cross-border regulatory discrepancies. Moreover, national restrictions under Article 114 of the TFEU, such as France’s ban on endocrine disruptors in cleaning products or Sweden’s stricter aquatic toxicity thresholds, force companies to maintain multiple product variants. These barriers delay pan-European launches by 6 to 9 months on average as per industry surveys, undermining the single market’s core promise and disadvantaging smaller players lacking legal infrastructure.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product and County. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | BASF SE, Akzo Nobel N.V., Bayer AG, Eastman Chemical Company, The Dow Chemical Company, Solvay, Chemtura Corporation, DuPont, Albemarle Corporation, Clariant AG, Chevron Philips Chemical Company, Ashland Inc., Huntsman Corporation, INEOS Group AG, Evonik Industries AG, Syngenta AG, and Others. |

SEGMENTAL ANALYSIS

By Product Insights

The polymers & plastic additives segment was the largest by accounting for 18.2% of the Europe specialty chemicals market share in 2024, with their pervasive use across automotive, packaging, construction, and consumer goods, where performance enhancement and regulatory compliance intersect. The EU’s Packaging and Packaging Waste Regulation mandates that all plastic packaging placed on the market by 2030 must be reusable or recyclable in an economically viable manner. This has intensified demand for compatibilizers, impact modifiers, and stabilizers that enable mechanical recycling of mixed plastic streams. As per the European Environment Agency, over 14 million tonnes of post-consumer plastic packaging were collected in 2024, requiring advanced additives to maintain material integrity across cycles. Companies like Clariant and BASF have commercialized additive masterbatches that increase recycled content tolerance in polyolefins by up to 50% without compromising mechanical properties, as verified by the Fraunhofer Institute for Process Engineering. Additionally, the EU’s restriction on microplastics adopted in 2023 accelerated the adoption of polymer-bound additives that prevent particle leaching. These regulatory tailwinds transform additives from passive components into enablers of circularity, ensuring sustained demand even as virgin plastic use declines.

The electronic chemicals segment is expected to register the fastest CAGR of 9.7% throughout the forecast period. The European Chips Act committed €43 billion in public and private funding through 2030 to double the EU’s semiconductor production share to 20%. This has triggered a wave of fab construction, including Intel’s €30 billion facility in Germany and STMicroelectronics’ 300 mm plant in Italy. Each new fab requires approximately 500 to 700 tonnes of high-purity electronic chemicals annually, including photoresists, etchants, CMP slurries, and ultrapure solvents. Localized supply is further mandated by the Chips Act’s resilience clause, requiring critical materials to have secure EU-based sources. Companies like Merck and Solvay have responded by expanding ISO Class 1 cleanroom production in France and Belgium, ensuring sub-part-per-trillion impurity levels. This policy-driven industrial renaissance transforms electronic chemicals from niche inputs into strategic national assets.

COUNTRY LEVEL ANALYSIS

Germany Specialty Chemicals Market Analysis

Germany was the top performer in the Europe specialty chemicals market with 24.3% of the share in 2024, with its integrated chemical cluster, advanced engineering base, and stringent environmental governance. The nation hosts Europe’s largest chemical parks in Ludwigshafen and Marl, housing over 150 chemical companies with shared infrastructure and R&D facilities. The automotive and machinery sectors consume 31% of all specialty polymers and lubricants, which provide a stable downstream demand. Furthermore, Germany’s dual vocational training system produces over 22000 chemical technicians annually, ensuring skilled labor continuity.

France Specialty Chemicals Market Analysis

France specialty chemicals market growth is likely to grow with the high-value segments, including agrochemicals, cosmetics actives, and electronic materials, driven by strong state-led industrial policy. In agrochemicals, France remains Europe’s largest agricultural producer with 26 million hectares under cultivation according to Agreste, requiring advanced crop protection chemicals despite regulatory tightening. The country also leads in green chemistry patents with 28% of EU filings in enzyme catalysis, as documented by the European Patent Office. The integration of chemical innovation with agriculture, luxury, and digital industries creates a uniquely diversified specialty chemicals ecosystem.

United Kingdom Specialty Chemicals Market Analysis

The United Kingdom specialty chemicals market in 2025, according to the Chemical Industries Association. Despite Brexit-related trade friction, the UK maintains leadership in life science chemicals, advanced materials, and specialty pharmaceutical intermediates. Over 70% of the UK’s chemical exports go to the EU, yet regulatory divergence under UK REACH has increased compliance costs. Nevertheless, the UK’s strength in research remains unmatched; it produces 16% of global chemistry publications despite having only 1% of the world’s population, as per the Royal Society of Chemistry. In 2025, the UK government launched the Industrial Decarbonisation Strategy, allocating £380 million to support low-carbon chemical manufacturing, including hydrogen-based ammonia synthesis. The Cambridge and Teesside clusters specialize in biocatalysis and CO2 utilization technology, with companies like Johnson Matthey scaling electrochemical processes for green surfactants.

Italy Specialty Chemicals Market Analysis

Italy specialty chemicals market growth is likely to have significant growth opportunities with fine chemicals for pharmaceuticals, textile auxiliaries, and construction additives aligned with its manufacturing heritage. Italy is Europe’s second-largest textile producer with over 45000 companies requiring dyeing auxiliaries, finishing agents, and sustainable fiber treatments as per Sistema Moda Italia. In pharmaceuticals, Italy hosts major API manufacturers supplying 18% of Europe’s generic drug intermediates, according to the European Generic Medicines Association. The 2024 National Recovery and Resilience Plan allocated €2.1 billion to green chemistry, including enzymatic synthesis and waterless dyeing technologies. Additionally, Italy’s construction sector, stimulated by the Superbonus 110% tax incentive, drove a 14% increase in demand for concrete superplasticizers and waterproofing admixtures in 2024.

COMPETITIVE LANDSCAPE

Competition in the Europe specialty chemicals market is characterized by a tripartite dynamic among multinational leaders, regional innovators, and agile niche specialists. Global players like BASF, Solvay, and Clariant leverage scale, integrated production, and deep regulatory expertise to dominate high-barrier segments such as electronic chemicals and catalysts. However, they face intensifying pressure from mid-sized European firms like Evonik Lanxess and Arkema that excel in tailored solutions for construction, automotive, and healthcare. Simultaneously, Asian giants such as Wanhua Chemical and DIC Corporation are expanding European technical service centers and local blending operations to offer cost-competitive alternatives, particularly in polymers and coatings. Regulatory complexity under REACH and the Chemicals Strategy for Sustainability acts as both shield and sword, favoring incumbents with compliance infrastructure while constraining smaller entrants. The market is further fragmented by the rise of bio-based startups leveraging EU innovation grants to commercialize novel fermentation-derived molecules. This layered competition drives continuous reinvention where technological leadership must be balanced with sustainability credentials, circular integration, and rapid response to policy shifts. Differentiation now hinges less on chemical composition alone and more on embedded services, digital connectivity, and verified environmental performance across the value chain.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe specialty chemicals market include

- BASF SE

- Akzo Nobel N.V

- Bayer AG

- Eastman Chemical Company

- The Dow Chemical Company

- Solvay

- Chemtura Corporation

- DuPont

- Albemarle Corporation

- Clariant AG

- Chevron Philips Chemical Company

- Ashland Inc.

- Huntsman Corporation

- INEOS Group AG

- Evonik Industries AG

- Syngenta AG

TOP PLAYERS IN THE MARKET

- BASF is a German multinational and a cornerstone of the European specialty chemicals industry with extensive global operations across more than 90 countries. The company supplies advanced materials, catalysts, construction chemicals, and nutrition solutions underpinned by integrated Verbund production sites. In recent years, BASF has intensified its focus on sustainable chemistry, launching bio-based polyamides and recyclable polymer additives compliant with EU circular economy mandates. The company inaugurated a new catalytic conversion pilot plant in Ludwigshafen in early 2024, dedicated to transforming plastic waste into feedstock, reinforcing its leadership in chemical recycling and aligning with the EU’s Chemicals Strategy for Sustainability.

- Solvay is a Belgium-headquartered innovator specializing in high-performance materials, specialty surfactants, and advanced formulations for electronics and healthcare. The company plays a pivotal role in Europe’s technological sovereignty, supplying ultra-pure chemicals for semiconductor manufacturing and battery materials for electric mobility. To strengthen its regional position, Solvay completed the spin-off of its soda ash division in 2023 to focus exclusively on specialty segments. In 2024, it expanded its fluoropolymer production capacity in Italy to support next-generation lithium battery binders and launched a digital formulation platform enabling faster co-development with industrial customers across automotive and renewable energy sectors.

- Clariant is a Swiss specialty chemicals leader renowned for its catalysts, additives, and sustainable solutions across packaging, textiles, and personal care. The company contributes significantly to global green chemistry through its EcoTain-certified product portfolio, which meets stringent life cycle assessment criteria. In Europe, Clariant has deepened its circular economy initiatives by scaling up its Licocene recycling enhancers and launching colorant masterbatches derived from bio-based feedstocks. In 2024, the company commissioned an innovation center in Frankfurt focused on CO2-reduced polymer additives and partnered with major packaging converters to validate the recyclability of multi-layer films using its AddWorks solutions, enhancing compliance with EU plastic regulations.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Leading participants in the Europe specialty chemicals market are pursuing integrated strategies centered on sustainability, regulatory alignment, and technological differentiation. Companies are divesting commodity assets to concentrate on high-margin specialty segments with defensible intellectual property. They are investing in localized production of bio-based and recyclable chemistries to meet EU green mandates and reduce supply chain risk. Strategic collaborations with end users in automotive electronics and construction enable co-development of application-specific formulations. Digitalization of R&D through AI-driven molecular design and formulation platforms accelerates time to market. Additionally, firms are establishing closed-loop partnerships with recyclers and utilities to secure circular feedstocks and support industrial decarbonization pathways.

MARKET SEGMENTATION

This research report on the Europe specialty chemicals market has been segmented and sub-segmented into the following categories.

By Product

- Agrochemicals

- Polymers & Plastic Additives

- Construction Chemicals

- Electronic Chemicals

- Cleaning Chemicals

- Surfactants

- Lubricants & Oilfield Chemicals

- Specialty Coatings

- Paper & Textile Chemicals

- Food Additives

- Adhesives & Sealants

- Others

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

1. Which end-use industries drive the europe specialty chemicals market?

Construction, automotive, electronics, personal care, food additives, and healthcare are key sectors boosting the europe specialty chemicals market through demand for advanced formulations

2. How important is sustainability in the europe specialty chemicals market?

Sustainability is central to the europe specialty chemicals market, with strong focus on green chemistry, bio-based products, and cleaner production to meet regulatory and consumer expectations

3. Which region leads within the europe specialty chemicals market?

Western Europe leads the europe specialty chemicals market thanks to mature industries in germany, france, and the uk, supported by advanced technology and strong industrial bases

4. Why is eastern europe growing fast in the europe specialty chemicals market?

Eastern Europe shows the fastest growth in the europe specialty chemicals market due to rapid urbanization, infrastructure projects, and expanding manufacturing and household goods demand

5. What product types dominate the europe specialty chemicals market?

Agrochemicals, construction chemicals, personal care actives, flavors, fragrances, dyes, pigments, and water treatment chemicals dominate the europe specialty chemicals market

6. How do regulations affect the europe specialty chemicals market?

Strict EU regulations on safety and environment raise compliance costs but also favor innovative, eco-friendly solutions in the europe specialty chemicals market

7. What role do personal care actives play in the europe specialty chemicals market?

Personal care active ingredients form a leading segment in the europe specialty chemicals market, supported by rising demand for effective, natural, and sustainable cosmetics

8. How is green and bio-based chemistry shaping the europe specialty chemicals market?

Shift to bio-based and eco-friendly chemistries is reshaping the europe specialty chemicals market, creating opportunities in renewable materials and low-impact processes

9. How does the automotive industry influence the europe specialty chemicals market?

The automotive sector drives the europe specialty chemicals market via need for coatings, lightweight composites, lubricants, and performance additives with heat and UV resistance

10. What growth opportunities exist in the europe specialty chemicals market?

Opportunities in the europe specialty chemicals market include green products, high-performance materials, personalized personal care, and advanced electronics and healthcare uses

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com