Europe Supercapacitors Market Size, Share, Growth, Trends Research Report, Segmented By Type, Material, Application, And By Region (U.K France, Germany, Spain, Italy, Sweden, Russia and Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis Forecasts (2026 to 2034)

Europe Supercapacitors Market Report Summary

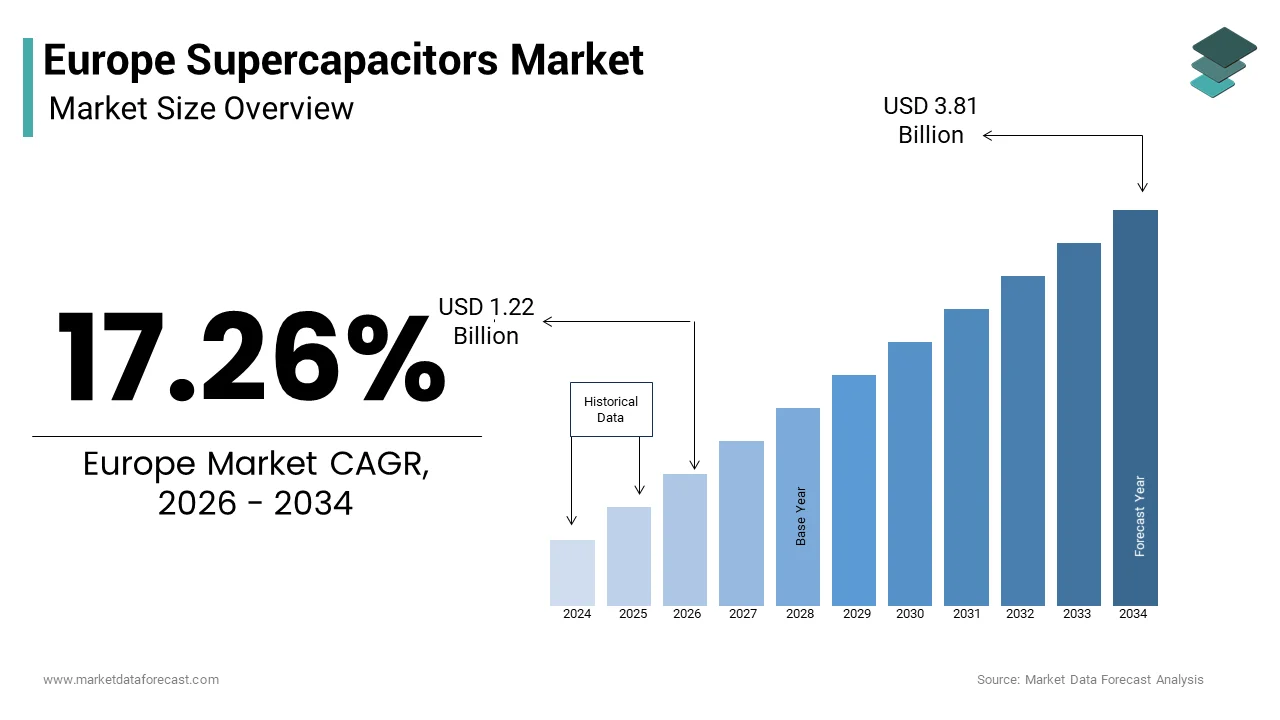

The Europe supercapacitors market was valued at USD 1.04 billion in 2025, is estimated to reach USD 1.22 billion in 2026, and is projected to reach USD 3.81 billion by 2034, growing at a CAGR of 17.26% during the forecast period from 2026 to 2034. The growth of the Europe supercapacitors market is driven by increasing demand for energy-efficient storage solutions, rising adoption of electric and hybrid vehicles, and the growing need for rapid charging and high-power delivery technologies. Advancements in energy storage systems and expanding applications across automotive, industrial, and renewable energy sectors are further accelerating market growth.

Key Market Trends

- Rising adoption of supercapacitors in electric and hybrid vehicles for energy recovery and power stabilization.

- Increasing demand for high-performance energy storage solutions with fast charging and long lifecycle capabilities.

- Growing use of supercapacitors in renewable energy systems for grid stabilization and backup power applications.

- Advancements in materials such as graphene and carbon-based composites enhancing performance and efficiency.

- Expansion of industrial and consumer electronics applications driving demand for compact and reliable energy storage devices.

Segmental Insights

- Based on type, the double layer capacitors segment dominated the Europe supercapacitors market in 2025. The segment’s leadership is attributed to its high power density, long cycle life, and widespread usage in various energy storage applications.

- Based on material, carbon-based materials accounted for a significant share of the Europe supercapacitors market in 2025. Their dominance is driven by excellent conductivity, cost-effectiveness, and suitability for high-performance energy storage solutions.

- Based on application, the automotive segment held 38.7% of the Europe supercapacitors market share in 2025. The segment’s growth is supported by the increasing adoption of electric vehicles and the need for efficient energy management systems.

Regional Insights

The Europe supercapacitors market demonstrates strong growth across key countries.

- Germany led the market by accounting for 28.3% of the share in 2025, supported by its advanced automotive industry and strong focus on energy storage technologies.

- The United Kingdom followed with 16.8% of the market share, driven by increasing investments in renewable energy and electric mobility.

- France holds a significant position due to its extensive nuclear and renewable energy infrastructure. Italy is witnessing steady growth supported by its manufacturing sector.

- Spain is expected to register notable growth during the forecast period due to increasing adoption of clean energy technologies.

Competitive Landscape

The Europe supercapacitors market is highly competitive, with key players focusing on innovation, material advancements, and strategic collaborations to strengthen their market presence. Companies are investing in next-generation energy storage technologies and expanding their production capabilities to meet growing demand. Prominent players in the Europe supercapacitors market include Cap-XX, UCAP Power (Maxwell Technologies), Knowles Electronics, LLC (Cornell Dubilier), XS Power Batteries (Ioxus), Skeleton Technologies Inc., KYOCERA Corporation (KYOCERA AVX Components Corporation), Tecate Group, VINATech Co. Ltd., Nippon Chemi-Con Corp., TDK Corporation, Murata Manufacturing Co., Ltd., LS Materials, Eaton, Yunasko, FastCAP Ultracapacitors Corporation, Panasonic Corporation, and Nanoramic Laboratories.

Europe Supercapacitors Market Size

The Europe super capacitors market size was valued at USD 1.04 billion in 2025 and is anticipated to reach USD 1.22 billion in 2026 to reach USD 3.81 billion by 2034, growing at a CAGR of 17.26% during the forecast period from 2026 to 2034.

A supercapacitor (also known as an ultracapacitor) is a high-capacity energy storage device that bridges the gap between a standard capacitor and a rechargeable battery. This technology is increasingly critical for the continent's strategic transition toward electrification, renewable energy integration, and industrial automation under the European Green Deal. Unlike batteries which store energy chemically, supercapacitors store energy electrostatically, making them indispensable for applications requiring instant bursts of power or frequent regenerative braking. According to the European Climate Law, the European Union has legally committed to reducing net greenhouse gas emissions by at least 55% by 2030 compared to 1990 levels, a target that Eurostat data monitoring confirms will necessitate the massive deployment of efficient energy storage systems in transport and grid infrastructure. Furthermore, SolarPower Europe reports that the European Union installed a record 56 gigawatts (55.9 GW) of new solar photovoltaic capacity in 2023 (while the International Energy Agency estimates this figure closer to 61 GW), creating an urgent need for buffering solutions to manage intermittency and stabilize grid frequency. The European Commission has also identified advanced energy storage as a key strategic value chain, fostering research into next generation materials like graphene to reduce dependency on imported battery technologies. This convergence of regulatory mandates, renewable expansion, and the push for sustainable mobility positions the region as a pivotal hub for the adoption and innovation of supercapacitor technologies.

MARKET DRIVERS

Accelerated Electrification of Public Transport and Heavy Duty Vehicles

The aggressive shift toward electric buses, trams, and heavy duty trucks drives unprecedented demand for high power density energy storage capable of handling regenerative braking.

The rapid electrification of public transportation and heavy-duty logistics is greatly encouraging the growth of the Europe supercapacitors market. This trend demands kinetic energy capture during braking to maximize range and efficiency. Unlike passenger cars, buses and trucks undergo frequent stop start cycles in urban environments, generating substantial amounts of waste heat and energy that supercapacitors can recover almost instantaneously due to their superior power density compared to lithium ion batteries. According to ACEA, registrations of electric city buses are increasing rapidly across the European Union, as many urban centers implement zero-emission zones and fleet targets to meet climate goals. The International Association of Public Transport emphasizes that cities like London, Paris, and Berlin are increasingly deploying hybrid electric buses that utilize supercapacitor banks to handle peak power demands during acceleration, thereby reducing the size and cost of the main battery pack. Data from the European Environment Agency indicates that transport accounts for nearly 25 percent of EU greenhouse gas emissions, prompting strict regulations that accelerate the retirement of diesel fleets. The unique capability of supercapacitors to endure hundreds of thousands of charge cycles without degradation makes them the ideal solution for these high intensity applications, ensuring sustained market growth as public transit authorities modernize their fleets to meet climate targets.

Integration of Renewable Energy Sources and Grid Stabilization Needs

The expanding share of intermittent renewable energy in the power mix necessitates fast responding storage solutions for frequency regulation and voltage support.

The region is integrating higher proportions of variable renewable energy sources like wind and solar, which creates a critical need for grid stability, and thereby fuels the expansion of the Europe supercapacitors market. This shift is because these sources cause supply fluctuations that threaten reliability. Supercapacitors offer millisecond response times for frequency regulation and voltage support, capabilities that traditional batteries and fossil fuel peaker plants cannot match effectively, making them vital for maintaining the balance of the European power network. Data from ENTSO-E shows that renewable sources now account for a significant portion of Europe's power generation. This shift has introduced new complexities for grid operators, who must now manage higher levels of variability and ensure sufficient ramping resources are available to balance the system. The International Renewable Energy Agency notes that frequency deviations caused by sudden changes in wind speed or cloud cover require immediate injection or absorption of power, a task perfectly suited for supercapacitor modules deployed at substations and wind farms. Data from the European Commission's Action Plan for Grids emphasizes the need for flexible assets to support the decarbonized grid, with billions of euros allocated for smart grid technologies. As the continent moves away from synchronous generators provided by coal and gas plants, the inertia of the grid decreases, heightening the reliance on fast acting storage like supercapacitors to prevent blackouts and ensure power quality. This structural shift in energy architecture ensures a robust and growing demand for supercapacitor based stabilization systems across the region.

MARKET RESTRAINTS

High Cost Per Watt Hour Compared to Lithium Ion Batteries

The significantly higher cost per unit of energy stored limits the adoption of supercapacitors to niche applications where power density outweighs energy capacity requirements.

The economic disparity between supercapacitors and lithium ion batteries regarding energy density and cost per watt hour inhibits the growth of the Europe supercapacitors market. This restricts their use to specific roles rather than as standalone energy sources. While supercapacitors excel in delivering high power, they store significantly less energy per unit of weight and volume compared to modern batteries, making them prohibitively expensive for applications requiring long duration discharge or extended range. According to the International Council on Clean Transportation, the cost of lithium ion battery packs in Europe dropped to $115–$139 euros per kilowatt hour in 2023, whereas supercapacitors remain substantially higher when calculated on an energy basis, often exceeding 1000 euros per kilowatt hour. This cost structure forces system designers to limit supercapacitor usage to hybrid configurations where they only handle peak loads, preventing them from capturing the broader mass market for energy storage. Data from the European Association for Storage of Energy indicates that for stationary storage applications requiring hours of backup power, investors overwhelmingly prefer battery technologies due to their superior economics. The inability of supercapacitors to compete on price for energy intensive tasks means their market potential remains capped unless breakthroughs in material science drastically reduce production costs or increase energy density. Until this gap narrows, widespread adoption beyond automotive and grid smoothing applications will remain challenging.

Dependence on Imported Critical Raw Materials and Supply Chain Vulnerabilities

Reliance on non-European sources for activated carbon precursors and specialized electrolytes creates supply chain risks and exposes the market to geopolitical instability.

The heavy dependence of the region’s manufacturers on imported critical raw materials holds back the expansion of the Europe supercapacitors market. This is particularly true for high purity activated carbon derived from coconut shells or specialized polymers, and advanced electrolytes which are predominantly sourced from Asia. The lack of domestic refining and processing capabilities for these essential components leaves the European supercapacitor supply chain vulnerable to export restrictions, logistical bottlenecks, and price volatility driven by geopolitical tensions. According to the European Commission's Critical Raw Materials assessments, the EU faces a total reliance on external markets for natural graphite and other critical inputs. This high level of import dependency is a primary driver behind the European Chips Act and related legislation aimed at securing more diverse and domestic supply chains. A study emphasizes that the global semiconductor supply chain remains highly concentrated, making the European market susceptible to disruptions in the delivery of critical electronic components and specialized chemical inputs. This reliance complicates the goal of strategic autonomy championed by the European Commission, as local manufacturers struggle to secure consistent and affordable supplies of high quality materials needed for performance grade supercapacitors. The European market faces persistent risks of production delays and margin compression due to a lack of robust domestic upstream industries and diversified sourcing. As a result, its ability to scale rapidly and meet growing domestic demand is significantly hindered.

MARKET OPPORTUNITIES

Emergence of Hybrid Energy Storage Systems in Industrial Automation

The development of combined battery and supercapacitor systems offers a transformative opportunity to optimize efficiency and extend lifespan in robotics and manufacturing.

The rapid adoption of hybrid energy storage systems within the industrial automation sector creates major possibilities for the growth of the Europe supercapacitors market. These systems combine the high energy density of batteries with the high power density of supercapacitors for optimal performance. As European industries embrace Industry 4.0 and deploy vast numbers of automated guided vehicles, robotic arms, and port cranes, the need to manage peak power spikes without oversizing battery packs becomes critical for operational efficiency and cost reduction. According to the International Federation of Robotics, Europe installed over 95000 industrial robots in 2023, many of which operate in high cycle environments where frequent acceleration and deceleration strain conventional battery systems. By integrating supercapacitors, these machines can draw burst power from the supercapacitor bank during high load events, reducing thermal stress on the battery and extending its overall lifecycle by 30% to 50%. Data from the European Manufacturing Survey indicates that downtime due to battery failure or replacement is a top concern for facility managers, driving interest in hybrid architectures that enhance reliability. The European Commission's Digital Europe Programme further supports such innovations by funding projects that improve industrial energy efficiency. As manufacturers seek to maximize uptime and reduce total cost of ownership, the demand for hybrid systems incorporating supercapacitors is poised to surge, opening a lucrative avenue for market growth.

Advancements in Graphene Based Supercapacitor Technologies

Breakthroughs in graphene and other nanomaterials promise to dramatically increase energy density and unlock new applications in consumer electronics and aerospace.

Ongoing research and development into graphene-based supercapacitors are setting the stage to overcome current limitations in energy density, which is likely to promote the expansion of the Europe supercapacitors market. These advancements could revolutionize the market by enabling applications previously reserved for batteries. Graphene, with its exceptional surface area and conductivity, allows for the creation of supercapacitors that can store significantly more energy while maintaining rapid charge discharge capabilities, making them viable for portable electronics, drones, and even aviation. According to the European Patent Office (EPO), there is intense innovation activity surrounding graphene-based energy storage. Much of this progress is supported by large-scale initiatives like the Graphene Flagship, which fosters collaboration between European academic institutions and the private sector to develop next-generation storage materials. These advancements could enable electric aircraft to utilize supercapacitors for takeoff and landing phases, reducing weight and emissions, a sector where the European aerospace industry is a global leader. Research suggests that the demand for supercapacitors made from advanced materials is set for steady long-term growth. As production processes mature and costs continue to decline, these components are expected to capture a larger share of the industrial and transport sectors.The ability to manufacture flexible and transparent supercapacitors also opens doors for wearable technology and smart textiles, areas where European fashion and tech sectors are highly influential. These next-generation materials are transitioning from laboratory prototypes to commercial products. As they do, they will expand the addressable market significantly beyond traditional industrial and automotive uses.

MARKET CHALLENGES

Complexity of Recycling Composite Electrochemical Components

The intricate combination of organic electrolytes, metal foils, and porous carbon materials poses significant challenges to circular economy goals and waste management.

The technical difficulty of recycling their complex composite materials hinders the growth of the European supercapacitor market. This issue conflicts directly with the European Union’s ambitious circular economy and zero-waste targets.Supercapacitors consist of tightly wound layers of aluminum foil, activated carbon electrodes, separators, and organic or aqueous electrolytes that are difficult to separate efficiently using current mechanical or pyrometallurgical processes. According to the European Electronic Waste Recyclers Association, less than 10 percent of supercapacitors are currently recycled effectively, with the majority ending up in landfills or incinerators due to the lack of specialized industrial facilities capable of recovering high purity materials. The new Ecodesign for Sustainable Products Regulation mandates higher recyclability scores and the use of recycled content, pressuring manufacturers to develop design for disassembly approaches that do not compromise performance. Data from the Joint Research Centre of the European Commission indicates that the energy required to recycle current supercapacitor designs often exceeds the value of the recovered materials, creating an economic disincentive for waste management operators. Standardized recycling protocols and economically viable chemical recovery methods have not yet been established. As a result, the industry faces regulatory scrutiny and reputational risks that could hinder market acceptance in sustainability-focused regions.

Standardization Gaps in Safety and Performance Metrics

The lack of unified international standards for testing, safety certification, and performance characterization creates market fragmentation and slows adoption.

The escalating challenge of fragmented standardization regarding safety protocols, testing methodologies, and performance metrics further impedes the expansion of the Europe supercapacitors market. This lack of uniformity creates uncertainty for system integrators and slows down widespread adoption across diverse sectors. Unlike the well established standards for lithium ion batteries, the supercapacitor industry lacks universally accepted criteria for evaluating cycle life, leakage current, and thermal runaway risks under various operating conditions, leading to inconsistencies in product quality and reliability claims. The International Electrotechnical Commission (IEC) continues to refine global standards for testing and specifying supercapacitors in transport and industrial applications. However, the inconsistent adoption of these standards across different European industries can lead to technical confusion for engineers who are specifying components for mission-critical systems. Data from the European Committee for Standardization reveals that divergent national regulations regarding the transport and disposal of supercapacitors containing organic electrolytes add layers of compliance complexity for manufacturers operating in multiple jurisdictions. This lack of clarity forces original equipment manufacturers to conduct extensive internal validation testing, increasing time to market and development costs. Furthermore, the absence of clear safety benchmarks for emerging high voltage modules hinders their integration into sensitive infrastructure like medical devices and aviation systems. Until a cohesive framework of standards is fully implemented and enforced across the EU, market growth may be hampered by caution and incompatibility issues.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 17.26% |

| Segments Covered | By Type, Material, Application, Country |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | Cap-XX (Australia), UCAP POWER (Maxwell Technologies) (South Korea), Knowles Electronics, LLC (Cornell Dubilier) (U.S.), XS Power Batteries (Ioxus) (U.S.), Skeleton Technologies Inc. (Estonia), KYOCERA CORPORATION (KYOCERA AVX Components Corporation) (U.S.), Tecate Group (U.S.), VINATech Co. Ltd. (Korea), Nippon Chemi-Con Corp. (Japan), TDK Corporation (Japan), Murata Manufacturing Co., Ltd. (Japan), LS Materials (South Korea), Eaton (Ireland), Yunasko (France), FastCAP Ultracapacitors Corporation (U.S.), Panasonic Corporation (Japan), Nanoramic Laboratories (U.S.) |

SEGMENTAL ANALYSIS

By Type Insights

The double layer capacitors segment led the Europe supercapacitors market and captured a substantial share in 2025. This leading position of the segment is driven by its mature manufacturing technology, exceptional cycle life exceeding one million cycles, and widespread adoption in applications requiring rapid charge discharge capabilities without chemical degradation. Double Layer Capacitors (EDLCs) spearhead the market because they can endure millions of charge-discharge cycles with minimal loss. This unparalleled longevity makes them indispensable for industrial applications involving frequent power cycling. Unlike batteries that degrade chemically over time, EDLCs store energy electrostatically, ensuring consistent performance in harsh environments such as port cranes, elevators, and uninterruptible power supplies where reliability is paramount. The total cost of ownership for these systems is significantly lower over a decade of operation because replacement frequencies are drastically reduced. This proven track record of longevity ensures that industries reliant on continuous operation prioritize EDLCs, securing their leading market position across the continent. Also supporting this segment is its superior power density, which allows them to deliver and absorb massive bursts of energy in milliseconds, a capability essential for stabilizing power grids and supporting vehicle acceleration. In applications like wind turbine pitch control or electric bus acceleration, the system requires immediate power injection that batteries cannot provide quickly enough without suffering damage or efficiency losses. Their ability to operate efficiently at extreme temperatures ranging from minus 40 to plus 65 degrees Celsius further enhances their utility in outdoor infrastructure. This unique combination of speed and robustness makes EDLCs the default solution for high power demands, cementing their dominance in the current market landscape.

The hybrid capacitors segment is estimated to register the fastest CAGR of 14.2% from 2026 to 2034 owing to its unique ability to bridge the gap between the high energy density of batteries and the high power density of supercapacitors, enabling new applications in electric mobility and long duration backup. Rapid segment gains are also caused by its architectural design which combines a battery type electrode with a capacitor type electrode, offering significantly higher energy density than traditional EDLCs while retaining fast charging capabilities. This balance is crucial for electric vehicles and hybrid buses that need to store more energy for range extension without sacrificing the ability to capture regenerative braking energy efficiently. By providing up to five times the energy storage of standard EDLCs, hybrid capacitors allow designers to optimize vehicle architecture for both performance and efficiency. This technological advantage positions them as the ideal solution for the next generation of electrified transport, driving their rapid market expansion. Further boosting this segment is its ability to operate at higher voltages and wider temperature ranges compared to conventional supercapacitors, unlocking applications in aerospace and remote infrastructure. Hybrid designs often utilize advanced electrolytes and asymmetric electrodes that enable operating voltages up to 3.8 volts per cell, increasing the total energy storage capacity of the module without adding extra cells. Furthermore, their lower self discharge rate compared to EDLCs makes them suitable for backup power applications where the device must remain charged for extended periods without maintenance. These enhanced operational characteristics expand the addressable market into high value sectors that were previously inaccessible to standard supercapacitors, fueling their status as the fastest growing segment.

By Material Insights

The carbon based materials dominated the Europe supercapacitors market and occupied a significant share in 2025. This prominence of the segment is supported by the abundance of carbon precursors, the well established activation processes for creating high surface area electrodes, and the cost effectiveness of activated carbon compared to exotic alternatives. The supremacy of carbon based materials, particularly activated carbon, is fundamentally driven by their ability to achieve extremely high specific surface areas exceeding 2000 square meters per gram, which is critical for maximizing the electrostatic storage capacity of double layer capacitors. The porous structure of activated carbon provides ample sites for ion adsorption, directly correlating to higher capacitance values per unit volume. The inherent electrical conductivity of graphitic carbon structures also minimizes internal resistance, allowing for efficient high power delivery. As the demand for energy storage grows, the proven track record of carbon materials in delivering reliable performance ensures they remain the cornerstone of supercapacitor production, securing their leading market position. Following this, the segment is backed by its relatively low cost and the existence of mature, global supply chains that can meet the volumetric demands of the expanding European market. Unlike metal oxides or conducting polymers which require complex synthesis and rare raw materials, activated carbon can be produced from abundant biomass waste products, keeping production costs competitive. The scalability of carbon activation processes allows manufacturers to ramp up production quickly to meet surging demand without prohibitive capital expenditure. This economic advantage ensures that carbon remains the material of choice for mass market applications, maintaining its substantial share of the European supercapacitors landscape.

The Composite Materials segment is anticipated to witness the fastest CAGR of 16.5% over the forecast period. This explosive growth is propelled by the integration of graphene, carbon nanotubes, and metal oxides into carbon matrices to overcome the limitations of single material electrodes, offering synergistic improvements in energy density and conductivity. The primary engine for the rapid expansion of composite materials is their ability to combine the high surface area of carbon with the pseudocapacitive properties of metal oxides or the superior conductivity of nanomaterials, resulting in electrodes that outperform individual components. By embedding manganese dioxide or ruthenium oxide nanoparticles into a carbon nanotube framework, manufacturers can achieve specific capacitances that are double or triple those of pure activated carbon while maintaining high power delivery. According to sources, research collaborations in Europe have demonstrated composite electrodes with energy densities approaching those of lead acid batteries, a breakthrough that opens new markets in electric mobility. These materials address the critical energy density gap that has historically limited supercapacitor adoption, making them highly attractive for next generation devices. As production techniques for these composites mature, their ability to deliver superior performance drives their rapid uptake in high value applications. This segment is also built up by the emergence of flexible and stretchable supercapacitors enabled by polymer carbon composites, which are essential for the booming wearable technology and smart textile sectors in Europe. Traditional rigid carbon electrodes cannot withstand the bending and stretching required for wearable devices, whereas composites incorporating conductive polymers and graphene sheets offer mechanical flexibility without compromising electrical performance. The ability to print these materials onto flexible substrates using roll to roll processing further accelerates their adoption in mass production. This alignment with the trends in miniaturization and flexible electronics ensures that composite materials will continue to grow at the fastest rate within the European market.

By Application Insights

The Automotive application segment was the largest segment in the Europe supercapacitors market and accounted for 38.7% share in 2025 because of the aggressive electrification of transport, the necessity for regenerative braking systems in heavy duty vehicles, and the implementation of start stop technologies to meet emission standards. Besides these, the segment's lead is based on the widespread deployment of regenerative braking systems in electric and hybrid buses, trucks, and trains across Europe, where supercapacitors are the optimal technology for capturing kinetic energy. During braking events, vehicles generate massive power spikes that batteries cannot absorb quickly enough without degradation, whereas supercapacitors can capture up to 90 percent of this energy in seconds. A study reveals that the inclusion of supercapacitors in heavy duty truck hybrids has increased fuel efficiency, a significant saving for logistics operators facing high diesel costs. The ability to release this stored energy instantly during acceleration reduces the load on the main engine or battery, extending component life and reducing emissions. This functional necessity in modern green transportation ensures that the automotive sector remains the largest consumer of supercapacitors in the region. A further point supporting this segment is the stringent European Union emission regulations that mandate the use of efficient start stop systems in internal combustion engine vehicles to reduce idle emissions. Supercapacitors are increasingly used to power these systems because they can deliver the high current required to restart the engine instantly even in cold weather, a task where traditional lead acid batteries often struggle. The durability of supercapacitors under frequent cycling conditions makes them ideal for urban driving patterns characterized by constant stopping and starting. As emission norms tighten further with the Euro 7 standards, the reliance on supercapacitors to ensure reliable and efficient engine management will continue to grow, solidifying the automotive segment's leading position.

The Energy application segment is likely to experience the fastest CAGR of 15.8% between 2026 and 2034. This swift expansion of the segment is attributed to the massive expansion of renewable energy installations, the urgent need for grid frequency regulation, and the development of smart microgrids across the continent. Key to this segment is also the critical role supercapacitors play in maintaining grid stability amidst the increasing volatility caused by intermittent renewable energy sources like wind and solar. As conventional synchronous generators are phased out, the grid loses inertia, requiring fast acting assets to balance supply and demand within milliseconds to prevent blackouts. Research shows that supercapacitors are uniquely suited for this task due to their sub second response times, outperforming traditional gas peaker plants and even large scale batteries in speed. The European Commission's Clean Energy Package incentivizes the deployment of such flexible resources, driving utilities to invest heavily in supercapacitor based stabilization units. As the share of renewables climbs toward 50%, the demand for these rapid response systems will accelerate, making energy the fastest growing application sector. The segment is seeing more growth from the essential use of supercapacitors in the pitch control systems of modern wind turbines, which are vital for safety and efficiency in Europe's extensive offshore wind farms. Pitch control systems must adjust blade angles instantly during high winds or grid faults to prevent mechanical damage, requiring a reliable power source that can operate in extreme temperatures and deliver high power bursts. The harsh marine environment of offshore farms favors the robustness of supercapacitors over other storage technologies. Europe continues to lead the world in offshore wind development. This, along with the mandatory inclusion of supercapacitors in new turbines, is driving significant volume growth in the energy sector.

COUNTRY LEVEL ANALYSIS

Germany Supercapacitors Market Analysis

Germany outperformed other countries in the Europe supercapacitors market and accounted for a 28.3% share in 2025 owing to its status as Europe's industrial powerhouse, hosting a dense concentration of automotive manufacturers, renewable energy projects, and advanced engineering firms that drive demand for high performance energy storage. Germany’s ambitious Energiewende has accelerated the transition to renewable energy and electric vehicles. Consequently, this has created a massive market for supercapacitor technology in both the grid and automotive sectors.The country is home to global automotive giants like Volkswagen, BMW, and Mercedes Benz who are integrating supercapacitors into their hybrid and electric fleets to enhance efficiency and regenerative braking capabilities. Furthermore, Germany leads Europe in wind energy installation, particularly offshore, where supercapacitors are critical for turbine pitch control systems. The presence of leading research institutes like Fraunhofer fosters innovation in graphene and hybrid capacitor technologies. This combination of industrial might, policy support, and technological leadership ensures Germany remains the primary engine of the European supercapacitors market.

United Kingdom Supercapacitors Market Analysis

The United Kingdom was the second largest country in the Europe supercapacitors market and held a 16.8% share in 2025. This position of the UK market is driven by its world leading offshore wind sector, strong aerospace industry, and government initiatives to decarbonize public transport networks. The UK's strong market standing is largely attributable to its position as the global leader in offshore wind energy, where supercapacitors are indispensable for the reliable operation of turbine control systems in harsh marine environments. The country hosts some of the largest offshore wind farms in the world, creating a sustained and high volume demand for ruggedized energy storage solutions. Additionally, the UK's robust aerospace industry, including companies like Rolls Royce and BAE Systems, utilizes supercapacitors for aircraft emergency systems and more electric aircraft architectures. The government's zero emission bus mandate also stimulates the market for electric public transport equipped with regenerative braking systems. This convergence of renewable energy ambition, aerospace innovation, and green transport policy positions the UK as a critical and dynamic market for supercapacitors.

France Supercapacitors Market Analysis

France secures a significant spot in the Europe supercapacitors market due to its extensive nuclear and renewable energy grid, strong railway electrification programs, and strategic investments in next generation energy storage materials. The modernization of the SNCF national railway network is a key factor supporting France's market strength. This system extensively employs supercapacitors for tramways and hybrid trains to recover braking energy and reduce electricity consumption. The country is a pioneer in deploying trams with onboard energy storage that eliminate the need for overhead catenaries in historic city centers, driving significant demand for high power density modules. Furthermore, France's commitment to grid stability through its nuclear and renewable assets necessitates advanced frequency regulation solutions where supercapacitors excel. The presence of major chemical and material science companies also supports the development of advanced carbon and composite materials for supercapacitors. This blend of transport innovation, grid modernization, and material science expertise ensures France remains a pivotal market in Western Europe.

Italy Supercapacitors Market Analysis

Italy witnessed a steady expansion in the regional market owing to its robust manufacturing sector, extensive use of supercapacitors in port automation and logistics, and growing adoption in renewable energy integration. Its market presence is driven by its status as a major logistics hub in the Mediterranean, where ports like Genoa and Trieste utilize supercapacitor equipped automated guided vehicles and ship to shore cranes to improve efficiency and reduce emissions. The intensive cycling nature of port operations makes supercapacitors the ideal energy storage solution for handling equipment, driving steady demand from the industrial sector. According to sources, the logistics and warehousing sector invested heavily in electrification in 2023, with supercapacitors being a key component of new automated systems. Additionally, Italy's sunny climate has spurred massive solar photovoltaic installations, creating a need for buffering solutions to manage intermittency and stabilize local grids. The country's strong automotive design and niche EV manufacturing also contribute to demand. This fusion of industrial automation, renewable expansion, and specialized manufacturing keeps Italy as a key growth market in Southern Europe.

Spain Supercapacitors Market Analysis

Spain is likely to grow notably in the European market from 2026 to 2034 because of its aggressive solar energy expansion, modernization of public transport fleets, and increasing focus on green hydrogen production which utilizes supercapacitors for process stability. The country’s market trajectory is influenced by its status as one of Europe's sunniest nations, leading to a boom in solar photovoltaic capacity that requires effective energy management and grid stabilization solutions provided by supercapacitors. The country is rapidly deploying large scale solar parks that integrate storage to smooth output fluctuations, creating a fertile ground for energy application growth. Furthermore, major cities like Madrid and Barcelona are upgrading their bus fleets to electric and hybrid models equipped with regenerative braking systems, boosting the automotive segment. The emerging green hydrogen sector also utilizes supercapacitors to manage the variable power loads of electrolyzers. This combination of solar leadership, urban transport modernization, and emerging hydrogen economy ensures Spain remains a vital and evolving market for supercapacitors in the region.

COMPETITIVE LANDSCAPE

The competition in the Europe supercapacitors market is characterized by intense rivalry among established multinational corporations and agile specialized firms vying for dominance in high growth segments like electric mobility and grid stabilization. Large global players leverage their extensive patent portfolios and mature manufacturing networks to secure long term supply agreements with major automotive and industrial clients across the continent. This trend towards integrated energy storage solutions creates high barriers to entry for smaller firms unless they possess highly differentiated graphene technologies or proprietary dry electrode processes. The competitive landscape is further complicated by stringent European Union safety regulations and emerging sustainability mandates which demand rigorous testing and certification before market approval. Companies must therefore invest significantly in research and development to demonstrate superior power density and environmental compliance while navigating complex procurement processes. Innovation speed and the ability to provide localized technical support are critical differentiators that determine market success. Furthermore, strategic alliances between supercapacitor manufacturers and battery producers have become essential for developing hybrid systems that optimize both energy and power metrics. The market remains dynamic with continuous entries of advanced material solutions challenging traditional carbon based standards and reshaping competitive dynamics across the region.

KEY MARKET PLAYERS

A few of the market players that are dominating the Europe supercapacitors market are

- Cap-XX (Australia)

- UCAP POWER (Maxwell Technologies) (South Korea)

- Knowles Electronics, LLC (Cornell Dubilier) (U.S.)

- XS Power Batteries (Ioxus) (U.S.)

- Skeleton Technologies Inc. (Estonia)

- KYOCERA CORPORATION (KYOCERA AVX Components Corporation) (U.S.)

- Tecate Group (U.S.)

- VINATech Co. Ltd. (Korea)

- Nippon Chemi-Con Corp. (Japan)

- TDK Corporation (Japan)

- Murata Manufacturing Co., Ltd. (Japan)

- LS Materials (South Korea)

- Eaton (Ireland)

- Yunasko (France)

- FastCAP Ultracapacitors Corporation (U.S.)

- Panasonic Corporation (Japan)

- Nanoramic Laboratories (U.S.)

Top Players In The Market

- Maxwell Technologies LLC, now a subsidiary of Tesla Inc, stands as a global pioneer in dry electrode technology and ultracapacitor solutions with a profound impact on the European automotive and renewable energy sectors. The company contributes significantly to the global market by providing high power density energy storage modules essential for regenerative braking systems in electric buses and grid stabilization applications. Recently Maxwell has strengthened its position by integrating its dry electrode manufacturing processes with European battery gigafactories to produce hybrid storage units that combine batteries and supercapacitors. The firm actively collaborates with major European commercial vehicle manufacturers to deploy next generation start stop systems that reduce emissions and fuel consumption. These strategic initiatives ensure their technology remains at the forefront of energy efficiency while addressing the critical demand for rapid charge discharge capabilities across the continent's electrified transport network.

- Skeleton Technologies GmbH operates as a leading innovator in curved graphene based supercapacitors with a dominant presence in the European market particularly within heavy duty transportation and industrial automation sectors. The company contributes globally by delivering ultra high power energy storage devices that offer superior cycle life and temperature resilience compared to traditional carbon based solutions. Their recent actions to solidify market presence include expanding production capacity at their factory in Germany to meet surging demand from electric truck and train manufacturers across the EU. Skeleton Technologies has also invested heavily in research partnerships with European universities to develop advanced graphene materials that increase energy density without compromising power performance. The firm frequently engages in pilot projects with railway operators to replace diesel engines with hybrid electric drives powered by their supercapacitor modules. By focusing on sustainable graphene sourcing and high performance engineering Skeleton Technologies enhances value for customers seeking reliable and eco friendly energy storage. These efforts demonstrate their commitment to driving technological advancement and maintaining leadership in the competitive European arena.

- Panasonic Industry Co Ltd is a specialized electronic components manufacturer that has established itself as a key player in the European market through its extensive portfolio of gold capacitors and electric double layer capacitors for diverse industrial applications. The company makes a substantial global contribution by supplying compact and reliable supercapacitors used in smart metering, automotive electronics, and backup power systems for critical infrastructure. Their recent strategy to strengthen their European position involves launching new high voltage supercapacitor series designed specifically for harsh automotive environments and renewable energy inverters compliant with strict EU regulations. Panasonic has also expanded its distribution network and technical support centers across major European nations to ensure rapid delivery and integration assistance for local clients. The firm continues to invest in developing hybrid capacitor technologies that bridge the gap between traditional batteries and supercapacitors for longer duration backup needs. By maintaining a dedicated focus on quality consistency and miniaturization Panasonic addresses the evolving needs of consumer electronics and industrial IoT sectors. Their persistent innovation in material science ensures they remain a vital partner for industries seeking robust and efficient energy storage solutions.

Top Strategies Used By Key Market Participants

Key players in the Europe supercapacitors market predominantly employ strategic product innovation and vertical integration to secure supply chains and meet escalating regional demand for high performance energy storage. Companies frequently invest millions in developing graphene based electrodes and hybrid capacitor architectures to achieve higher energy densities that compete with lithium ion batteries while retaining fast charging capabilities. Another major strategy involves forming deep collaborative partnerships with automotive original equipment manufacturers and railway operators to co-develop customized energy storage modules that address specific application requirements like regenerative braking and start stop systems. Market participants also focus heavily on expanding their manufacturing facilities within the European Union to comply with local content regulations and reduce logistics costs associated with importing heavy components. Investment in research and development remains a cornerstone strategy as firms strive to achieve breakthroughs in cycle life and operating temperature ranges. Additionally, companies pursue targeted acquisitions of specialized material science startups to rapidly incorporate novel conductive polymers and activated carbon sources into their existing production platforms. These combined approaches allow industry leaders to navigate complex regulatory landscapes while maintaining a competitive edge in this rapidly evolving technological sector.

MARKET SEGMENTATION

This research report on the Europe supercapacitors market is segmented and sub-segmented into the following categories.

By Type

- Double Layer Capacitors

- Pseudocapacitors

- Hybrid Capacitors

By Material

- Carbon & metal oxide

- Conducting Polymers

- Composite Materials

By Application

- Automotive

- Consumer Electronics

- Energy

- Industrial

- Healthcare

- Others (Aerospace & Defense, etc.)

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

Frequently Asked Questions

What defines the supercapacitors market in Europe?``

It involves energy storage devices that deliver rapid charge and discharge for high-power applications.

Why are supercapacitors gaining attention across Europe?

They offer faster charging and longer lifecycle compared to traditional batteries.

How can supercapacitors be explained in simple terms?

They are devices that store and release energy quickly without relying on chemical reactions like batteries.

Which industries are driving demand for supercapacitors?

Automotive, renewable energy, electronics, and industrial sectors are major adopters.

What role do electric vehicles play in this market?

They use supercapacitors for energy recovery and power support in hybrid systems.

How do supercapacitors differ from conventional batteries?

They provide higher power density but lower energy storage capacity.

What technological advancements are shaping this market?

Improvements in materials like graphene are enhancing performance and efficiency.

Why is sustainability important in the supercapacitors market?

They are environmentally friendly due to longer lifespan and reduced waste.

How does renewable energy integration influence demand?

Supercapacitors help stabilize energy supply in solar and wind systems.

What challenges does this market face in Europe?

High production costs and limited energy density can restrict wider adoption.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com