Europe Swimwear Market Size, Share, Trends, & Growth Forecast Report, Segmented By Material, End-User, Distributional Channel, and By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2025 to 2033

Europe Swimwear Market Report Summary

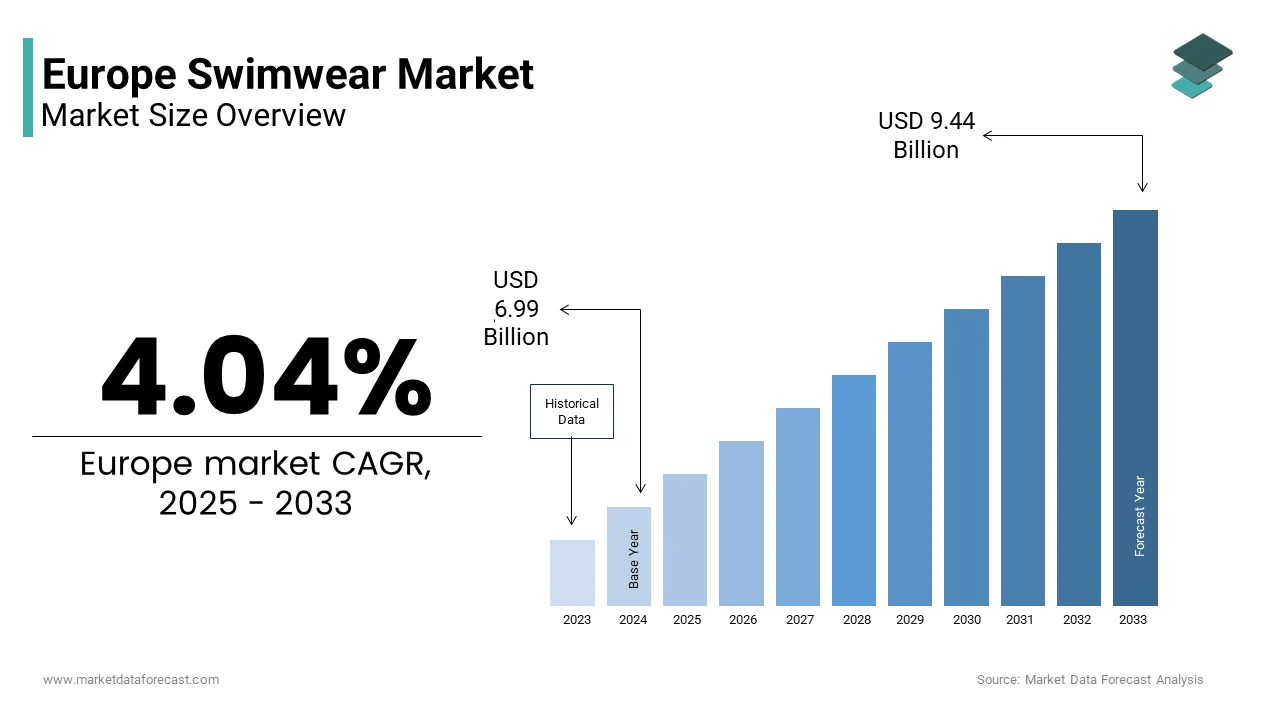

The Europe swimwear market was valued at USD 6.72 billion in 2024, is estimated to reach USD 6.99 billion in 2025, and is projected to expand to USD 9.44 billion by 2033, growing at a CAGR of 4.04% during the forecast period from 2025 to 2033. Market growth is driven by rising beach and leisure tourism, increasing participation in swimming and water sports, and growing consumer interest in fashionable yet functional swimwear. Expanding wellness trends, fitness-oriented lifestyles, and continuous design innovation by leading brands are further supporting market expansion across Europe.

Key Market Trends

- Rising demand for high-performance fabrics such as polyester or nylon blended with spandex due to durability, stretchability, and comfort.

- Growing preference for women’s swimwear is driven by wider style variety, frequent fashion updates, and higher purchase frequency.

- Sustained dominance of offline retail channels, as consumers prefer in-store trials, fit assurance, and premium brand experiences.

- Increasing focus on sustainable and eco-friendly swimwear materials in response to evolving environmental awareness.

Segmental Insights

- By material, the polyester or nylon blended with spandex segment dominated the Europe swimwear market in 2024, supported by its resistance to chlorine, quick-drying properties, and long-lasting performance.

- By end user, the women's segment accounted for 65.5% of the European swimwear market share in 2024, reflecting strong demand across fashion, fitness, and leisure categories.

-

By distribution channel, the offline retail segment held 57.5% of the market share, driven by specialty stores, brand outlets, and department stores.

Regional Insights

The European swimwear market shows consistent growth across major coastal and tourism-driven countries.

- Spain led the market with a 22.3% share in 2024, supported by strong beach tourism and resort wear demand.

- France ranked second, benefiting from premium fashion brands and lifestyle-driven consumption.

- Italy is expected to hold a promising share due to its strong fashion heritage.

- The United Kingdom is projected to register a healthy CAGR, supported by indoor swimming culture and fitness trends.

- Germany is anticipated to maintain a notable share driven by recreational swimming and wellness activities.

Competitive Landscape

The Europe swimwear market is moderately competitive, with global sportswear brands, luxury fashion houses, and specialized swimwear manufacturers actively operating in the region. Key players are focusing on product innovation, sustainable materials, brand collaborations, and omnichannel retail expansion to strengthen market presence. Prominent companies operating in the Europe swimwear market include Haddow Group Plc, Pentland Group PLC, Swimwear Anywhere Inc., Adidas AG, Puma SE, LVMH Moët Hennessy Louis Vuitton, Nike Inc., Boardriders, Inc., Arena Italia S.p.A., and Gap Inc.

Europe Swimwear Market Size

The Europe swimming market size was valued at USD 6.72 billion in 2024 and is anticipated to reach USD 6.99 billion in 2025 and USD 9.44 billion by 2033, growing at a CAGR of 4.04% during the forecast period from 2025 to 2033.

Swimwear includes a diverse range of garments designed for aquatic recreation, sunbathing, and water sports, including bikinis, one pieces, swim trunks, rash guards, and modest swimwear. Unlike purely fashion-driven apparel, swimwear in Europe is deeply intertwined with seasonal tourism, coastal lifestyles, and evolving body positivity norms. Europe’s extensive coastline anchors a vibrant leisure economy. According to the European Environment Agency, these coastal areas support hundreds of millions of beach visits annually, underscoring the scale of demand for swimwear and related apparel. Southern European countries remain tourism powerhouses. As per Eurostat, international arrivals to Spain, France, Italy, and Greece collectively number in the hundreds of millions each year, with coastal experiences among the most sought‑after activities. This influx directly sustains seasonal swimwear purchases and replacements.

Cultural and regulatory shifts also shape demand. For example, France and Spain enforce bans on full‑face coverings at public beaches, indirectly influencing modest swimwear design toward EU‑compliant styles. Meanwhile, the rise of staycations, as mentioned by the European Travel Commission, which notes that domestic holidays account for the majority of summer trips in Germany, has reinforced local consumption even during periods of global travel disruption. His blend of geographic advantage, tourism intensity, and sociocultural evolution positions swimwear not merely as seasonal apparel but as a barometer of leisure, identity, and inclusivity across the European lifestyle landscape.

MARKET DRIVERS

Resurgence of Coastal Tourism and Domestic Staycations

The robust recovery of European coastal tourism and the institutionalization of domestic staycations have significantly revived swimwear demand across the region, which is driving the swimwear market growth in Europe. According to Eurostat, Mediterranean destinations such as Spain, Italy, and Greece collectively welcomed more than 180 million international tourists in 2024, which is the highest level since 2019. As per the European Travel Commission, domestic tourism surged, with a majority of French and German households opting for in‑country vacations, which is reinforcing local demand. These trends translate into direct apparel needs. According to the consumer surveys conducted across EU countries, tourists typically purchase or replace swimwear once per summer season, with families averaging multiple units per trip. Coastal infrastructure supports this behavior. Spain alone maintains hundreds of Blue Flag-certified beaches, according to the Foundation for Environmental Education, which is encouraging repeated beach visits that increase wear and tear on swimwear. As per the European Pool and Spa Association,n Europe added more than 1,000 public swimming facilities between 2022 and 2024, broadening usage beyond coastal areas. This dual engine of international tourism and local leisure ensures consistent annual demand cycles, insulating the market from short-term economic fluctuations and reinforcing swimwear as a seasonal necessity rather than a discretionary luxury.

Influence of Social Media and Celebrity-Driven Fashion Cycles

Digital platforms have dramatically accelerated swimwear trend adoption and purchase frequency across Europe, particularly among consumers aged 16 to 35, which is further fuelling the swimwear market growth in Europe. Instagram and TikTok serve as virtual showrooms where influencers and celebrities debut seasonal styles, often triggering immediate retail spikes. According to a 2024 Eurobarometer special survey on digital consumption, more than 60% of European women aged 18 to 29 reported purchasing swimwear after seeing it on social media, which indicates generational influence. Major brands leverage this dynamic through micro‑influencer partnerships. For example, Spanish label Cea reported a significant sales uplift in its crochet bikini line within two weeks of a single TikTok campaign featuring Mediterranean beach content. Fashion weeks in Milan and Paris now include dedicated swimwear previews, with trends like high leg cuts, retro monokinis, and neutral tones rapidly disseminating across mass and premium segments. The “haul culture” prevalent on YouTube further fuels repeat purchases, with consumers buying multiple styles for vacation content creation. This digital immediacy compresses traditional seasonal planning, compelling retailers to adopt agile inventory systems and limited edition drops. As a result, swimwear has evolved from a functional item into a fast-moving fashion statement, with style obsolescence occurring within months rather than seasons.

MARKET RESTRAINTS

Stringent EU Textile Sustainability and Chemical Regulations

The European Union’s tightening regulatory framework for textiles poses significant compliance burdens on swimwear manufacturers, particularly concerning synthetic fiber content and chemical residues, which are hindering the swimwear market expansion in Europe. Swimwear is predominantly made from polyester and elastane blends and falls under the EU Strategy for Sustainable and Circular Textiles, which mandates digital product passports and minimum recycled content by 2030. According to the European Chemicals Agency, the REACH regulation restricts more than 30 hazardous substances commonly found in dyeing and finishing processes, including certain azo dyes and perfluorinated compounds used for water resistance. In 2024, the European Chemicals Agency added elastane production intermediates to its candidate list for authorization, which is potentially disrupting supply. Compliance requires costly reformulation and supply chain auditing. As per the European Apparel and Textile Confederation, a mid‑sized European swimwear brand spends on average €180,000 annually on chemical testing and certification, which reflects high compliance costs. German customs seized thousands of swimwear units in 2023 for excessive phthalate levels, according to the Federal Institute for Risk Assessment, which is illustrating enforcement. These regulatory pressures increase production costs, delay time to market, and disadvantage smaller players lacking in‑house compliance teams, thereby constraining innovation and accessibility.

High Volatility In Raw Material Costs and Supply Chain Fragmentation

Swimwear producers in Europe face persistent cost instability due to dependence on imported synthetic fibers and fragmented manufacturing networks, which are inhibiting the growth of the European swimwear market. According to the European Man‑Made Fibers Association, more than 85% of polyester and elastane used in EU swimwear is sourced from Asia, primarily China and South Korea, which indicates reliance. ICIS price indices documented that in 2024, polyester staple fiber prices surged by over 25% while elastane costs rose by nearly 20%, driven by global supply constraints. Unlike integrated fashion giants, most swimwear brands operate on short seasonal cycles with limited inventory buffers, which leaves them exposed to spot market fluctuations. Furthermore, production is dispersed across Portugal, Tunisia, Turkey, and Eastern Europe, which is creating logistical complexity. A single collection may involve fabric from Italy, cutting in Romania, and assembly in Morocco. As reported by the Federation of European Sporting Goods Industries, Red Sea shipping disruptions in early 2024 extended lead times by two to three weeks, which is causing stockouts during peak pre‑summer selling windows. This structural fragility undermines pricing stability, limits investment in sustainable materials, and amplifies the risk of missed seasonal opportunities, which is critical in a market where the majority of annual revenue is generated between March and August.

MARKET OPPORTUNITIES

Rise of Inclusive and Adaptive Swimwear Segments

Growing consumer demand for body positivity and accessibility is unlocking new market niches through inclusive sizing, adaptive designs, and culturally sensitive offerings, which is a notable opportunity in the European swimwear market. According to a 2024 YouGov survey across five EU countries, more than 40% of women aged 25 to 45 reported difficulty finding well‑fitting styles in standard retail, highlighting unmet demand. Brands like Pour Moi in the UK and Arena in Italy have expanded size ranges up to 8XL using reinforced seam construction and high support fabrics. Simultaneously, adaptive swimwear for people with disabilities is gaining traction. As per the European Disability Forum, the EU’s 87 million persons with disabilities remain a largely untapped segment, with only a small share of swimwear brands offering adaptive features such as open back designs or magnetic closures. In Sweden and the Netherlands, public pools now mandate accessibility, indirectly driving demand. Additionally, modest swimwear has evolved beyond basic burkinis to fashion‑forward styles compliant with French and Belgian beach dress codes. This diversification aligns with the EU’s non‑discrimination directives and transforms swimwear from a homogeneous product into a spectrum of identity‑affirming solutions.

Integration of Recycled and Bio-Based Performance Fabrics

Innovation in sustainable textile engineering is enabling high-performance swimwear made from certified recycled and bio‑derived materials, which is meeting both regulatory and consumer expectations, and is another potential opportunity in this regional market. Leading European brands now utilize ECONYL regenerated nylon that offers identical stretch and chlorine resistance to virgin nylon. According to the European Textile Research Institute, more than one-third of premium swimwear launches in Western Europe in 2024 incorporated high levels of recycled content, which reflects mainstream adoption. Concurrently, bio‑based elastane from companies like Covestro, which is derived from castor oil, is entering pilot production with comparable recovery properties to petroleum‑based spandex. The German brand Bleed Clothing introduced a swim line in 2024 using bio‑based polyester from algae, achieving a significantly lower carbon footprint verified by TÜV Rheinland, which is demonstrating innovation. These materials satisfy the EU Ecolabel criteria and appeal to eco‑conscious shoppers. As per the European Consumer Organisation, more than half of German and Danish consumers are willing to pay a premium for certified sustainable swimwear, confirming demand. As the EU’s textile eco‑design requirements tighten, such innovations transition from niche differentiators to mainstream necessities, which is positioning sustainability as a core performance attribute rather than an add‑on.

MARKET CHALLENGES

Shortened Product Lifespan and Overconsumption Backlash

Despite sustainability messaging, the fast fashion model has drastically reduced the functional lifespan of swimwear, which is triggering consumer and regulatory pushback against overconsumption and challenging the growth of the European swimwear market. According to a 2024 study by the European Environment Agency, the average European consumer owns more than three swimwear items but uses fewer than two per season, whichresults ins discarding the rest after minimal use. Chlorine, saltwater, and UV exposure degrade elastane fibers within 10 to 15 uses, yet marketing encourages constant style renewal. This disposability conflicts with the EU’s anti‑greenwashing directives. In 2024, the Norwegian Consumer Authority fined an international brand for labeling swimwear as eco‑friendly without substantiating durability claims, which illustrates enforcement. Moreover, synthetic swimwear contributes to microplastic pollution, with each washreleasings thousands of microfibers as measured by the University of Plymouth, prompting calls for mandatory filtration in washing machines under the upcoming EU Ecodesign for Sustainable Products Regulation. As per a 2024 Kantar survey, nearly half of French and Italian respondents expressed guilt over swimwear waste, which shows consumer awareness. This tension between trend velocity and environmental accountability forces brands to balance novelty with longevity, a challenge that risks alienating either fashion‑forward or eco‑conscious segments.

Intensifying Competition from Non-Traditional and Rental Models

The traditional swimwear retail model faces disruption from digital‑native vertical brands and emerging rental or subscription services, which are fragmenting consumer loyalty, compressing margins, and challenging the regional market expansion. According to the European Fashion Retail Observatory, direct‑to‑consumer brands like Sweden’s NA‑KD and France’s Baija capture more than 20% of the under‑30 market, which is leveraging social media and analytics to offer on‑trend styles at lower prices. Simultaneously, swimwear rental platforms such as MyWardrobe HQ in the UK and Dress & Go in Spain are gaining traction among vacationers seeking variety without ownership. As per a Tourism Spain survey in 2024, nearly one-fifth of Spanish tourists aged 20 to 35 rented swimwear for beach holidays, attracted by convenience and reduced packing weight. These models undermine seasonal inventory planning and erode brand control over customer experience. According to Eurostat retail data, department store swimwear sales declined while online specialty stores grew in 2024, reflecting structural change. According to the European E‑Commerce Association, online swimwear purchases have high return rates, averaging nearly 40%, which is adding further pressure. This shift demands rapid adaptation in distribution, pricing, and value proposition challenges exacerbated by the category’s narrow selling window.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 4.04% |

| Segments Covered | By Material, End-User, Distributional Channel, and Country |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | Haddow Group Plc (U.K.), Pentland Group PLC (U.K.), Swimwear Anywhere Inc. (U.S.), Adidas AG (Germany), Puma SE (Germany), LVMH Moët Hennessy Louis Vuitton (France), Nike Inc. (U.S.), Boardriders, Inc. (U.S.), Arena Italia S.p.A. (Italy), Gap Inc. (U.S.) |

SEGMENTAL ANALYSIS

By Material Insights

The polyester or nylon blended with spandex segment dominated the market by accounting for the largest share of the European swimwear market in 2024. The dominance of the segment in this regional market is attributed to the unmatched functional synergy between these polymers. Swimwear must withstand repeated exposure to chlorine, saltwater, UV radiation, and mechanical stretching without losing shape or color, which is a demand met only by high‑tenacity polyester or nylon paired with elastic spandex. According to the European Swimming Federation, millions of Europeans participate in organized swimming programs annually andares creating consistent demand for performance‑oriented blends. Even fashion swimwear incorporates spandex to ensure body conformity and comfort. For instance, these blends retain tensile strength after repeated pool washes, far exceeding alternatives such as cotton or viscose. Polyester/nylon‑spandex blends are expected to remain dominant as durability and performance requirements outweigh sustainability pressures.

The recycled polyester segment is the fastest-growing material segment and is expected to grow at a CAGR of 10.2% over the forecast period, owing to the EU sustainability mandates. According to the European Commission’s Strategy for Sustainable and Circular Textiles, minimum recycled fiber thresholds must be met by 2030. Brands such as Speedo Europe and Arena now offer collections using ECONYL, which is a regenerated nylon sourced from fishing nets and textile waste. According to the Eurobarometer surveys, more than 60% of consumers in Germany and Scandinavia actively seek recycled labels when purchasing apparel. Italian filament producer Aquafil has expanded ECONYL production capacity to meet rising demand. Recycled blends are expected to grow rapidly as EU regulation and consumer preference converge to make circular textiles mainstream.

By End User Insights

Thewomen'sn segment held 65.5% of the European swimwear market share in 2024. The leading position of thewomen'sn segment in this regional market is driven by fashion orientation, variety, and cultural norms. According to Eurostat, women’s apparel consistently accounts for the largest share of EU clothing expenditure. Swimwear for women is treated as a seasonal fashion statement rather than purely functional apparel. Social media, celebrity endorsements, and resort‑wear integration drive rapid trend turnover. Department stores and specialty retailers allocate most swimwear floor space to women’s collections, reflecting higher price points and accessory bundling. Luxury brands such as Eres and La Perla further elevate the category into high fashion, which is influencing silhouettes across the mass market. Women’s swimwear is expected to remain dominant as fashion cycles and cultural drivers sustain recurring purchase behavior.

The kids' swimwear segment is the fastest-growing end‑user category and is predicted to grow at a CAGR of 8.08% over the forecast period in this regional market due to the rising participation in organized aquatic activities. According to the European Swimming Federation, millions of children across the EU participate in formal swimming programs each year. National curricula in Germany, France, and Nordic countries emphasize swimming proficiency by age 10. Family beach holidays also remain a cultural staple. The European Travel Commission reports that a majority of EU households with children take coastal vacations annually. This dual demand fuels higher per‑child consumption compared to adults. Kids' swimwear is expected to grow rapidly as safety standards and leisure culture drive recurring purchases.

By Distribution Channel Insights

The offline retail segment had 57.5% of the European swimwear market share in 2024. The dominating position ofthe offline retail segment in this regional market is driven by the critical importance of fit and tactile evaluation. According to Eurostat retail trade data, apparel sales remain concentrated in physical stores despite e‑commerce growth. Swimwear is among the most fit‑sensitive apparel categories, with consumers preferring in‑store trials to assess stretch, support, and coverage. Department stores such as Galeries Lafayette in France and Selfridges in the UK dedicate extensive seasonal swim sections with fitting rooms and stylist assistance. Specialty retailers leverage lingerie expertise to cross‑sell swimwear with matching apparel. Offline channels are expected to remain dominant as fit sensitivity and experiential shopping sustain in‑store demand.

The online distribution segment is the fastest-growing channel and is expected to register a healthy CAGR of 12.1% over the forecast period, owing to mobile‑first shopping and social commerce. According to the European E‑commerce Association, more than half of online apparel purchases in Europe are made via mobile devices. Instagram and TikTok serve as primary discovery engines, with brands leveraging shoppable posts and influencer campaigns. Augmented‑reality fitting tools piloted by Zalando and ASOS reduce return anxiety, while live commerce events drive higher conversion rates. Online channels are expected to grow rapidly as digital platforms reshape swimwear into a mobile‑first, socially driven category.

COUNTRY ANALYSIS

Spain Swimwear Market Analysis

Spain led the Europe swimwear market with a 22.3% share in 2024. The leading position of Spain in the European market is attributed to its extensive coastline and strong tourism sector. The country’s thousands of kilometers of beaches, many certified with Blue Flag status, attract millions of international visitors annually. Domestic demand is equally robust, with most households purchasing swimwear each year due to cultural emphasis on summer leisure. Local brands capitalize on this demand with rapid trend cycles and resort collections, while the Valencian Community serves as a manufacturing hub supplying both domestic and EU markets. Multi‑generational beach holidays fuel demand across all age groups, reinforcing Spain’s dominance. With its combination of natural advantage, cultural habits, and industrial capacity, Spain is expected to remain Europe’s largest swimwear market.

France Swimwear Market Analysis

France captured thesecond-largestt share of the Europe swimwear market in 2024. The growth of France in the European market can be credited to its role as a global fashion capital and regulatory trendsetter. Luxury houses set design benchmarks that influence mass‑market segments across Europe. French consumers prioritize design and quality, with many willing to pay premium prices for swimwear. National regulations have reshaped modest swimwear toward stylish, compliant designs, while sustainable fashion mandates require environmental labeling for apparel, accelerating the adoption of recycled materials. Domestic demand remains resilient, with women purchasing multiple swimwear items each summer. With its blend of haute couture influence, policy innovation, and consumer sophistication, France is positioned as the qualitative leader in the European swimwear market.

Italy Swimwear Market Analysis

Italy is predicted to account for a promising share of the Europe swimwear market over the forecast period. Factors such as the artisanal quality, premium fabrics, and strong manufacturing heritage are driving the Italian market growth. Specialized mills in regions such as Lake Como and Veneto produce high‑quality materials exclusively for swimwear, supplying both domestic and international luxury brands. Italian swimwear emphasizes craftsmanship and construction, justifying higher price points compared with EU averages. Exports target premium European markets, while domestic demand is fueled by coastal and lake lifestyles. Italy also leads in technical swimwear innovation, with brands dominating competitive swimming through advanced designs. This combination of artisanal heritage, technical excellence, and lifestyle alignment ensures Italy’s premium positioning in the European swimwear market.

United Kingdom Swimwear Market Analysis

The United Kingdom is expected to exhibit a healthy CAGR in the Europe swimwear market during the forecast period due to its leadership in inclusivity and e‑commerce. UK brands pioneered plus‑size and adaptive swimwear, setting benchmarks for accessibility across Europe. The nation also leads in online penetration, with a majority of swimwear sales occurring digitally through agile direct‑to‑consumer brands. British consumers show strong sustainability awareness, driving demand for recycled fabrics. Despite a limited coastline, the UK’s extensive indoor pool culture sustains year‑round demand. Post‑Brexit, UK brands have strengthened EU export partnerships while tailoring collections to domestic diversity. With its focus on inclusivity, digital agility, and functional versatility, the UK remains a progressive and influential market.

Germany Swimwear Market Analysis

Germany is projected to account for a notable share of the Europe swimwear market over the forecast period, owing to the technical rigor and environmental accountability. German consumers prioritize functional attributes such as chlorine resistance and UV protection, driving demand for performance‑oriented brands. The country also leads in sustainable compliance, with eco‑labels mandating strict chemical and recyclability standards. Germany’s strong indoor swimming culture ensures consistent off‑season demand, supported by thousands of public pools and millions of regular users. Retailers enforce supplier codes requiring recycled content and fair labor practices, reinforcing sustainability. With its combination of performance expectations, regulatory adherence, and civic responsibility, Germany is positioned as Europe’s benchmark for quality and sustainable swimwear.

COMPETITIVE LANDSCAPE

Competition in the Europe swimwear market is characterized by a sharp dichotomy between performance-driven functionality and fashion-led aesthetics, with sustainability increasingly serving as the unifying imperative. The landscape features global sportswear giants, heritage European luxury houses, and agile digital native brands, each competing on distinct value propositions. Premium players like Eres and Vilebrequin emphasize craftsmanship and timeless design, while performance brands such as Arena and Speedo leverage technical innovation and athlete endorsements. Meanwhile, direct-to-consumer labels gain share through social media virality, inclusive sizing, and rapid trend response. Regulatory pressures from the EU Strategy for Sustainable Textiles are raising compliance costs and forcing material transparency, favoring brands with traceable supply chains. At the same time, high return rates in e-commerce and short seasonal windows intensify inventory risks. Success in this environment demands a delicate balance of trend agility, functional authenticity, and environmental accountability, making the market highly dynamic and segment-specific.

KEY MARKET PLAYERS

A few of the market players in the Europe swimwear market are

- Haddow Group Plc (U.K.)

- Arena

- Speedo Europe

- Eres

- Pentland Group PLC (U.K.)

- Swimwear Anywhere Inc. (U.S.)

- Adidas AG (Germany)

- Puma SE (Germany)

- LVMH Moët Hennessy Louis Vuitton (France)

- Nike Inc. (U.S.)

- Boardriders, Inc. (U.S.)

- Arena Italia S.p.A. (Italy)

- Gap Inc. (U.S.)

Top Players In The Market

- Arena is a premier European swimwear brand with deep roots in competitive swimming and a strong presence across performance and fashion segments. Originally founded in France and now headquartered in Italy, the company supplies FINA-approved competition suits to national teams and elite athletes while also offering lifestyle collections for recreational swimmers. Arena contributes significantly to the global market through its technical innovation in hydrodynamic fabrics and compression engineering. In 2024, Arena launched a new eco performance line made entirely from ECONYL regenerated nylon, achieving full certification under the Global Recycled Standard. The brand also expanded its inclusive sizing to 6XL across core European markets, responding to body positivity trends. These initiatives reinforce Arena’s dual identity as a performance leader and a responsible lifestyle brand.

- Speedo Europe, operating under Pentland Brands, remains a dominant force in both competitive and consumer swimwear across the continent. Known for pioneering technologies such as Fastskin and Endurance+ chlorine-resistant fabric, Speedo serves everyone from Olympic athletes to school swimming programs. The company plays a pivotal role in global swim education initiatives and collaborates with national federations to promote water safety. In 2024, Speedo Europe introduced a fully circular swimwear collection featuring mono material construction for easier recyclability and partnered with municipal pools in Germany and the Netherlands to collect end-of-life suits for material recovery. It also enhanced its digital fitting tool to reduce online returns. These actions demonstrate Speedo’s commitment to innovation, sustainability, and accessibility in a rapidly evolving market.

- Eres, a Paris-based luxury swimwear and lingerie maison, exemplifies French elegance and craftsmanship in the premium European swimwear segment. Renowned for its minimalist silhouettes, matte fabrics, and precision tailoring, Eres caters to a discerning clientele seeking timeless design over fleeting trends. The brand’s influence extends globally through collaborations with high-end retailers and its integration into resort wear collections. In 2024, Eres transitioned its entire swim line to 100% recycled Italian nylon while maintaining its signature soft hand feel and color depth. It also launched a made-to-order service in select European boutiques to minimize overproduction. By aligning artisanal quality with circular principles, Eres reinforces its position as a benchmark for sustainable luxury in the swimwear industry.

Top Strategies Used by the Key Market Participants

Key players in the Europe swimwear market focus on integrating certified recycled materials such as ECONYL and Repreve to meet EU sustainability mandates and consumer expectations. They invest in digital fitting technologies and virtual try-on tools to reduce online return rates and enhance customer experience. Brands are expanding size inclusivity and adaptive designs to address body diversity and accessibility demands across age and ability spectrums. Strategic collaborations with sports federations and environmental organizations bolster credibility in performance and eco claims. Additionally, companies adopt made-to-order or small batch production models to minimize waste and align with circular fashion principles while maintaining premium positioning.

MARKET SEGMENTATION

This research report on the Europe swimwear market is segmented and sub-segmented into the following categories.

By Material Type

- Polyester/Nylon

- Spandex

By End-user Type

- Men

- Women

- Kids

By Distribution Channel Type

- Online

- Offline

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe swimwear market?

The Europe swimwear market includes the retail and online sale of swimwear apparel such as bikinis, one-piece swimsuits, trunk shorts, rash guards, and related beachwear for men, women, and children.

What drives growth in the Europe swimwear market?

Market growth is driven by rising disposable incomes, increasing tourism and beach vacations, growing fitness and active lifestyle trends, and fashion innovations in swimwear design.

Which swimwear styles are popular in Europe?

Bikinis, one-piece suits, tankinis, board shorts, and athleisure swimwear are among the most popular styles, reflecting fashion preferences and occasion-based usage.

How does seasonality affect the Europe swimwear market?

Swimwear sales peak during spring and summer months, aligned with holiday seasons, warmer weather, and increased travel to coastal and resort destinations.

Which countries lead swimwear consumption in Europe?

Countries such as Italy, France, Spain, and the United Kingdom are major markets due to strong beach culture, fashion awareness, and tourism activity.

What role do online channels play in swimwear sales?

E-commerce and social commerce platforms are crucial, offering wider style options, sizing tools, virtual try-ons, and direct-to-consumer brands that drive market penetration.

How do fashion trends influence the swimwear market?

Trends like sustainable fabrics, bold prints, mix-and-match separates, and inclusive sizing influence consumer preferences and product launches.

What are key challenges in the swimwear market?

Seasonal demand, returns due to fit issues, price competition, and supply chain disruptions are key challenges.

Are sustainable swimwear products gaining traction?

Yes, eco-friendly swimwear made from recycled materials, biodegradable fabrics, and low-impact dyes is rising in popularity among eco-conscious consumers.

What is the future outlook for the Europe swimwear market?

The market is expected to grow steadily with expanding tourism, fashion innovation, omni-channel retail strategies, and increased focus on sustainability.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com