Europe Urban Air Mobility Market Size, Share, Trends and Growth Forecasts Research Report, Segmented By Vehicle Type, Range, Operation, End User, and Country – Industry Analysis (2026 to 2034)

Europe Urban Air Mobility Market Summary

The Europe Urban Air Mobility Market is experiencing rapid growth, driven by strong policy support for sustainable transport, rising urban congestion, and increasing demand for low-emission mobility solutions. The market is shaped by the European Green Deal, multimodal transport planning, and advancements in electric vertical take-off and landing (eVTOL) aircraft. Key growth factors include smart city initiatives, medical logistics demand, and regulatory frameworks for unmanned air traffic management, while air taxis and air ambulances are leading adoption across the region.

Market Size & Growth

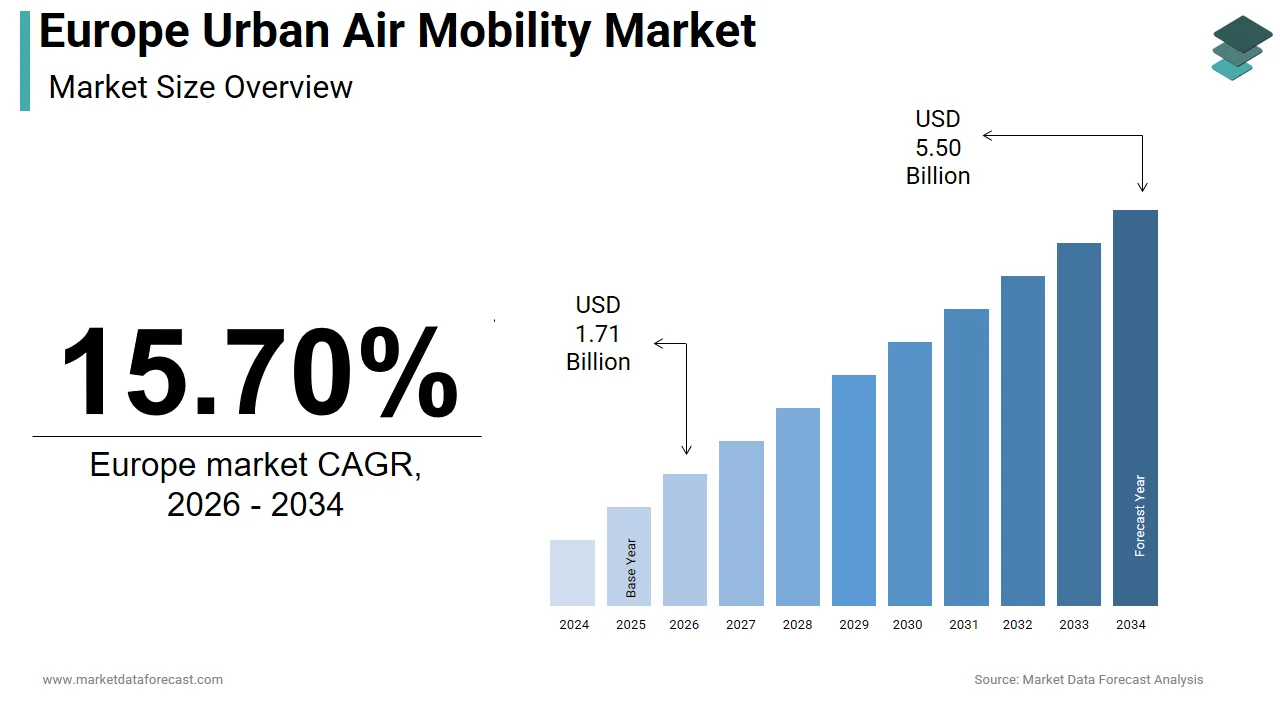

- Valued at USD 1.48 billion in 2025, with projected growth to USD 5.50 billion by 2034.

- CAGR estimated at 15.70% for the 2026 to 2034 period.

Key Drivers

- Sustainable Urban Mobility Plans: EU policies integrating urban air mobility into decarbonized transport strategies.

- Traffic Congestion: Rising delays in road transport encouraging alternative aerial solutions.

- Medical & Emergency Logistics: Growing use of aerial systems for time-critical healthcare deliveries.

- Government Support: Increased funding for low-altitude electric aviation infrastructure and trials.

Leading Segments

- Vehicle Type: Air Taxis, Air Ambulance, Last-Mile Delivery.

- Range: Intracity and Intercity operations.

- End Users: Ridesharing Companies, Hospitals & Medical Agencies.

Key Trends

- Green Aviation: Focus on zero-emission, battery-powered eVTOL aircraft.

- Vertiport Development: Integration of landing hubs with rail and multimodal transport corridors.

- Autonomous Operations: Growing trials of unmanned and hybrid aerial systems.

- Medical Applications: Expansion of air ambulances and sample delivery services.

Major Players

- Airbus SE, Volocopter, Lilium Aviation GmbH, Ehang, Safran SA, Textron Inc., Uber Technologies Inc., Aurora Flight Sciences.

Europe Urban Air Mobility Market Size

The size of the Europe urban air mobility market was worth USD 1.48 billion in 2025. The regional market is anticipated to grow at a CAGR of 15.70% from 2026 to 2034 and be worth USD 5.50 billion by 2034 from USD 1.71 billion in 2026.

Urban air mobility (UAM) is a safe and efficient air transportation system for highly automated aircraft to carry passengers or cargo at low altitudes in urban and suburban areas. Unlike conventional aviation, urban air mobility in Europe is fundamentally shaped by stringent environmental mandates, dense population geographies, and integrated multimodal transport planning. A defining characteristic is its alignment with the European Green Deal, which prioritizes zero-emission mobility solutions to alleviate ground congestion and reduce urban CO2 output. According to sources, a significant majority of the population lives within urban environments. Key metropolitan regions experience considerable annual delays in road transit. An increase in the establishment of regulatory frameworks for managing unmanned aerial traffic is apparent. A number of member states have initiated participation in designated air traffic corridors for unmanned systems. These foundational policy and demographic conditions position urban air mobility not as a futuristic concept but as an emerging pillar of Europe’s sustainable urban logistics and passenger transit strategy.

MARKET DRIVERS

Integration into EU Sustainable Urban Mobility Plans

The region’s binding commitment to decarbonize urban transport has embedded UAM into formal city planning frameworks, which acts as a key accelerator for the Europe urban air mobility market. The European Commission’s revised Guidelines on Sustainable Urban Mobility Plans now explicitly recognize low-altitude electric aviation as a complementary layer for emergency services, medical logistics, and last-mile freight in cities exceeding one million inhabitants. Several cities in a specific region have integrated potential aerial transport into their urban development plans for the coming decade. Major urban centers are setting aside dedicated areas within their land use planning for future aerial mobility infrastructure. A substantial share of recent funding for urban transport innovation has focused on developing aerial mobility systems, with a preference for quiet, battery-powered operations. Ground delivery vehicles are identified as contributors to urban carbon emissions, suggesting potential regulatory shifts to move certain types of cargo to electric air transport. This institutional anchoring ensures urban air mobility is evaluated not in isolation but as part of integrated and multimodal decarbonization strategies.

MARKET RESTRAINTS

Public Acceptance and Noise Sensitivity in Densely Populated Areas

Significant social resistance rooted in acoustic impact concerns, despite technological progress, restricts the growth of the Europe urban air mobility market. Urban population densities in Europe are higher compared to other continents, indicating a greater number of residents could be close to low-altitude air traffic routes. Extensive exposure to existing urban sound sources appears to lower tolerance for additional noise from aerial transport. A significant number of city residents express reservations about integrating new air transport systems into communities unless strict noise performance criteria are achieved. Current prototypes of vertical flight aircraft generate sound levels during specific flight phases that may surpass noise thresholds preferred by many urban residents. These acoustical realities constrain flight corridors, operational hours, and vertiport siting, which directly limit commercial scalability in the very environments urban air mobility aims to serve.

MARKET OPPORTUNITIES

Medical and Emergency Logistics in Remote and Island Communities

The region’s geographic diversity, including thousands of islands and mountainous regions, creates new opportunities for the Europe urban air mobility market. Numerous island territories are identified as geographically isolated regions where traditional transportation methods face limitations due to environmental conditions and infrastructure constraints. A significant portion of these islands operates without local diagnostic imaging capabilities, necessitating the movement of patients to larger medical facilities. Regional initiatives are exploring the integration of urban air mobility to facilitate the distribution of essential medical supplies and equipment to remote maritime areas. Aerial drone technology is being utilized in pilot programs to expedite the transfer of biological samples between islands and mainland laboratories. Preliminary trials indicate that autonomous flight can substantially decrease transit times for medical deliveries while ensuring the stability of sensitive materials. These time-critical applications bypass infrastructure gaps while aligning with EU health equity mandates by offering a socially justifiable entry point for aerial mobility adoption.

Development of Vertiport Infrastructure Along Existing Transport Corridors

Strategic co-location of takeoff and landing sites with established multimodal hubs offers a scalable infrastructure opportunity, which is expected to drive the expansion of the Europe urban air mobility market. Regulatory requirements have been established to ensure major railway stations and intermodal freight terminals in the region integrate infrastructure for future aerial mobility operations. A number of rail hubs across several nations have proactively set aside space for vertiports, utilizing existing operational resources like security protocols, power supply, and passenger logistics. Moreover, a functional, modular vertiport prototype has been introduced at a major transport hub, demonstrating the potential to manage a specific volume of electric vertical take-off and landing vehicle (eVTOL) movements hourly and providing integrated maintenance and passenger processing capabilities. Financial commitments have been secured to support the development of vertiports along a primary transportation corridor, with priority given to locations near high-speed rail stops. This infrastructure synergy minimizes land acquisition costs, accelerates permitting, and embeds aerial mobility into daily commuter patterns rather than treating it as a standalone novelty.

MARKET CHALLENGES

Regulatory Fragmentation Across National Airspace Authorities

Operational uncertainty in unmanned aircraft use persists because European Union Aviation Safety Agency rules, while common, are implemented unevenly across member states. This hinders the expansion of the Europe urban air mobility market. Germany and France boast national U-space service providers, whereas Italy and Spain are still bound by legacy ATC procedures, which cannot support dynamic low-altitude routing for drones. The limited implementation of standardized low-altitude airspace corridors suggests that comprehensive regional coverage remains incomplete. Discrepancies in national operational requirements continue to hinder the commercial feasibility of long-range aerial transport. Variations in altitude restrictions and communication standards necessitate multiple administrative approvals for single journeys spanning different jurisdictions. Diverse emergency protocols across borders create logistical complexities for operators managing integrated flight paths. The absence of a unified regulatory framework for unmanned traffic management impacts the efficiency of cross-border transitions. This patchwork governance undermines the economic case for scalable networks, as operators must develop country-specific compliance stacks rather than pan-European solutions. Urban air mobility (UAM) will be limited to localized pilot programs until comprehensive regulatory and operational standards are fully integrated.

Limited Battery Energy Density Constraining Range and Payload

Current lithium-ion battery technology imposes strict operational boundaries on electric aerial vehicles, which directly affects service viability in the region’s varied topography, and thereby negatively impacts the Europe urban air mobility market. The operational scope for most certified eVTOL aircraft is currently characterized by a practical range that supports intracity and short-range regional air mobility. Current range capabilities typically fall below the distances required for established intercity routes within the same geographic region. The present energy storage capacity of commercially used aviation batteries indicates that achieving extended range missions would necessitate a compromise in safety margins. A specific increase in battery energy density is a key requirement for facilitating operations that can reliably cover longer distances. Observations from operations in cold climate areas indicate a measurable reduction in effective range, linked to the power demands for maintaining optimal battery temperatures. These physical limitations restrict urban air mobility to short-hop urban or airport shuttle roles, preventing integration into broader regional air networks and delaying the path to profitability for operators.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Vehicle type, Range, Operation, End User, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Textron Inc., Uber Technologies Inc., Airbus SE, Ehang, Safran SA, Volocopter, Lilium Aviation GmbH, Carter Aviation, AIRSPACEX, Aurora Flight Sciences, and Others. |

SEGMENTAL ANALYSIS

By Vehicle Type Insights

The Air Taxi segment captured the majority share of 38.5% of the Europe urban air mobility market in 2024. The supremacy of the air taxi segment is driven by its alignment with Europe’s premium urban mobility needs and high visibility in public-private trials. An additional driver is the integration of air taxis into multimodal transit ecosystems in megacities facing severe congestion. Average car speeds in major European central cities are low and continue to experience a general decline as a result of increased congestion and urban planning measures that prioritize other transport modes. A further growth factor is regulatory prioritization. Regulatory bodies in Europe and globally are making significant progress on the legal framework for advanced air mobility, with some regions having fully adopted operational rules, but the first type certification for a piloted electric vertical take-off and landing aircraft is an anticipated future development. Plans for initial air taxi services in various European urban areas are advancing, and the foundational regulations are in place to allow local authorities to establish operational routes connecting key locations, such as airports and city centers. These institutional endorsements accelerate infrastructure readiness and public perception by cementing air taxis as the flagship application of urban air mobility.

The Air Ambulance segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 31.4% from 2026 to 2034 due to Europe’s aging population and geographic healthcare disparities. The European population includes a substantial and increasing segment of older individuals. Acute medical events like cardiovascular incidents and strokes necessitate rapid intervention within a short timeframe for optimal results. Access to continuous emergency care for these conditions varies, with many rural areas lacking 24-hour specialized units. Geographic isolation in remote areas contributes to slower medical responses with conventional transport. Unmanned aerial vehicles are being assessed for their potential to deliver vital equipment and medications to areas with limited access. Early studies indicate that incorporating autonomous flight technology may significantly cut down the time from an emergency notification to the arrival of medical aid. Additionally, new EU medical device regulations now classify autonomous medical drones as Class III devices by enabling faster certification for life-saving payloads. These clinical and regulatory tailwinds position air ambulance as the highest growth vehicle segment.

By Range Insights

The Intracity range segment led the Europe urban air mobility market and held a 64.4% share in 2024. The leading position of the intracity range segment is attributed to technological feasibility and infrastructure pragmatism. This reflects the initial focus on short-distance urban applications such as airport shuttles, downtown commuting, and hospital transfers. Most certified eVTOLs have a practical range of 80 to 120 kilometers, perfectly suited for journeys within metropolitan boundaries like Munich to its airport or Amsterdam to Schiphol. According to research, a portion of daily urban trips in the EU are under 25 kilometers, making intracity operations the most efficient use of current battery capabilities. A different factor is regulatory streamlining. European drone regulation is evolving to create distinct, simpler low-altitude pathways for urban flights, streamlining drone traffic management within cities. Leading European cities are actively establishing digitally managed drone corridors with real-time monitoring, accelerating approvals for urban flights compared to complex inter-city routes.

The Intercity segment is expected to exhibit a noteworthy CAGR of 28.7% during the forecast period, owing to Europe’s corridor-based transport policy and emerging battery swap ecosystems. A transportation network has incorporated aerial mobility lanes along major corridors, establishing connections between several prominent cities. Funding has been directed towards the development of intercity landing and takeoff facilities, specifically designed with systems for efficient energy replenishment. Regulations have been established that require all intercity aerial routes to utilize sustainable energy sources, either through alternative fuels or grid-charged batteries. A cooperative assessment of an intercity shuttle service indicated a potential for high passenger capacity utilization and significantly reduced end-to-end travel times compared to existing ground transport during periods of heavy use. These developments transform intercity routes from speculative to commercially viable.

By End User Insights

The ridesharing companies segment dominated the Europe urban air mobility market by accounting for a 32.3% share in 2024. The dominance of the ridesharing companies segment is supported by its capital resources, digital platform integration, and first-mover advantage in consumer-facing aerial mobility. Companies like Uber Elevate (now transitioned to partners) and Bolt Air have leveraged existing user bases to pilot pre-booking and dynamic pricing models for air taxi services. An additional driver is the strategic alignment with Europe’s Mobility as a Service vision. A growing number of urban areas within a specific region are implementing new requirements for mobility platforms, mandating the integration of both traditional ground-based services and emerging aerial transportation options. A further growth factor is venture funding concentration. Investment in aerial transportation initiatives linked to established ridesharing services has shown significant growth, with funding for these ventures notably exceeding that of other consumer-focused transport categories. This financial muscle enables extensive simulation testing, vertiport reservations, and customer acquisition campaigns that position ridesharing firms as the public face of urban air mobility.

The hospitals and medical agencies segment is predicted to witness the highest CAGR of 33.2% from 2025 to 2033. The rapid expansion of the hospitals and medical agencies segment is fuelled by urgent clinical needs and public health policy alignment. The European Union’s Beating Cancer Plan mandates that all member states reduce diagnostic and treatment delays, with aerial logistics emerging as a key enabler. Variations in medical equipment utilization rates across certain geographic areas suggest that logistical barriers can impact the efficiency of diagnostic services. The integration of unmanned aerial systems into clinical workflows offers a potential method for addressing transportation challenges and optimizing resource allocation. Automated transit solutions have demonstrated the ability to significantly reduce the time required for moving biological samples between facilities compared to traditional ground methods. The maintenance of precise environmental conditions during flight ensures that the integrity of sensitive medical materials is preserved during rapid transit. Collaborative regional initiatives are increasingly focusing on the development of dedicated aerial corridors to facilitate the movement of healthcare supplies across administrative boundaries. These institutional commitments ensure sustained demand beyond pilot phases.

COUNTRY-LEVEL ANALYSIS

Germany Urban Air Mobility Market Analysis

Germany was the top performer in the Europe urban air mobility market by capturing a 22.1% share in 2024. The supremacy of the German market is propelled by its advanced aerospace industry, federal support for innovation, and dense urban corridors. The nation facilitates a major validation center for regional unmanned airspace frameworks, specifically focusing on urban integration. A growing number of metropolitan areas have formally incorporated aerial mobility into their long-term urban transportation strategies. National innovation programs provide dedicated financial support to advance sustainable propulsion technologies within the aviation sector. Local engineering initiatives have conducted extensive flight testing to gather comprehensive data on operational safety and acoustic impact. The technical databases generated through these domestic flight trials serve as a foundational resource for shaping international aviation regulations. This combination of regulatory leadership, industrial capability, and municipal readiness solidifies Germany’s top position.

France Urban Air Mobility Market Analysis

France was the second-largest player in the Europe urban air mobility market by holding a share of 17.6% in 2024. The expansion of the French market is driven by its centralized aviation policy and strong public investment in aerial innovation. Initial operational deployment of a national unmanned aircraft system traffic management service has occurred in key metropolitan areas, including Paris, Lyon, and Toulouse. The number of authorized test flights for aerial mobility solutions within the region has been substantial, reportedly representing a significant volume of such activity across the continent. A substantial financial commitment has been directed towards the development of infrastructure to support future urban air mobility operations, specifically involving key transport hubs. Additionally, Groupe ADP and RATP are co-developing seamless air rail interchanges, with a pilot at La Défense enabling passengers to book combined eVTOL and metro tickets via a single app. These top-down initiatives create a cohesive ecosystem unmatched in scale and coordination.

United Kingdom Urban Air Mobility Market Analysis

The United Kingdom grew steadily in the Europe urban air mobility market because of its agile regulatory sandbox and strength in medical and offshore logistics applications. Efforts have been made to expedite the progression of numerous urban air mobility projects. An aerial delivery network focused on medical logistics has been established and now serves a significant number of medical facilities across distinct regions. Trials involving the use of aerial transport for critical medical supplies demonstrated a substantial reduction in transit duration within specific health districts. Financial resources have been committed to consortia engaged in the development of zero-emission intercity air shuttles connecting several major metropolitan areas. Despite Brexit, the UK maintains close alignment with EASA standards, ensuring cross-border operational compatibility. This focus on life-critical and regional connectivity applications sustains the UK’s leadership.

Italy Urban Air Mobility Market Analysis

Italy is also a major player in the European market, with growth supported by tourism logistics and historic city preservation. Italian airspace authorities have granted special urban air mobility corridors over Venice, Florence, and Rome, where ground vehicle access is restricted to protect cultural heritage. Demonstration flights of advanced aerial mobility vehicles have been conducted for both tourist transport and emergency response purposes in protected heritage areas. A significant investment plan has been allocated for the construction of landing infrastructure in island regions, which frequently experience disruptions to conventional sea transport during adverse weather. The use of unmanned aerial vehicles for the transport of medical supplies between mainland locations and island clinics has substantially increased. This niche focuses on heritage-sensitive and geographically fragmented environments creates a unique Italian model.

Sweden Urban Air Mobility Market Analysis

Sweden is predicted to expand in the Europe urban air mobility market from 2026 to 2034 due to its integration of urban air mobility with climate neutrality goals and welfare services. Regulatory requirements have been established for new aerial mobility projects to demonstrate significantly reduced lifecycle emissions compared to ground transportation methods. Battery-electric vertical take-off and landing (eVTOL) aircraft are currently meeting these environmental standards. Drones utilized for air ambulance services are in operation across several northern regions, providing critical stroke and cardiac care to sparsely populated communities. Partnerships have been formed to supply vertiport operations entirely with renewable power sources, incorporating real-time carbon monitoring for individual flights. Furthermore, Sweden’s Innovation Agency Vinnova funds cross-municipality data pools that optimize drone routing for both public health and postal services. This systems approach positions Sweden as a model for equitable and sustainable urban air mobility.

COMPETITIVE LANDSCAPE

Competition in the Europe urban air mobility market is characterized by a delicate balance between technological ambition and regulatory realism. Unlike markets driven primarily by venture capital or consumer hype, Europe’s competitive landscape is shaped by stringent safety standards, environmental mandates, and public sector engagement. Incumbent aerospace leaders compete alongside agile startups, each leveraging distinct advantages established firms bring certification experience and industrial scale, while newcomers offer innovative architectures and digital native operations. The European Union’s unified regulatory framework under EASA creates a level playing field but also raises the barrier to entry, favoring players with deep compliance capabilities. Simultaneously, municipal governments act as gatekeepers, selecting partners based on noise performance, sustainability credentials, and integration with existing mobility networks. This ecosystem fosters collaboration over pure rivalry, with competitors often co-developing infrastructure or sharing U-space data. Success ultimately hinges not on speed to market alone but on the ability to embed aerial mobility into Europe’s broader vision of safe, sustainable, and socially inclusive urban futures.

KEY MARKET PLAYERS

The leading companies operating in the Europe urban air mobility market include:

- Textron Inc.

- Uber Technologies Inc.

- Airbus SE

- Ehang

- Safran SA

- Volocopter

- Lilium Aviation GmbH

- Carter Aviation

- AIRSPACEX

- Aurora Flight Sciences

TOP PLAYERS IN THE MARKET

- Volocopter, headquartered in Germany, is a pioneer in electric vertical takeoff and landing aircraft development and a cornerstone of Europe’s urban air mobility ecosystem. The company has conducted test flights across different countries and holds the world’s first design organization approval for eVTOLs from the European Union Aviation Safety Agency. It also partnered with Fraport to build Germany’s first commercial vertiport at Frankfurt Airport. These milestones demonstrate Volocopter’s commitment to regulatory compliance, public demonstration, and infrastructure readiness, positioning it as a global standard setter for safe and scalable urban air transport.

- Lilium, based in Munich, distinguishes itself through its jet-powered eVTOL architecture, enabling higher speeds and longer ranges suited for intercity mobility. The company’s Lilium Jet features electric ducted fans and targets routes up to 250 kilometers, aligning with Europe’s corridor-based transport vision. It also signed agreements with Ferrovie dello Stato Italiane and Iberia to integrate aerial shuttles into national rail and airline networks. Lilium is addressing mobility gaps in southern and central Europe and complementing existing ground infrastructure by strategically concentrating on regional connectivity over dense urban cores.

- Airbus Urban Mobility, a division of Airbus Group, leverages its aerospace heritage to advance scalable and certifiable urban air solutions. Its CityAirbus NextGen prototype, designed for intracity operations, emphasizes low noise and high safety through distributed electric propulsion and redundant systems. It also joined the European Urban Air Mobility Initiative to co-develop common vertiport standards across many metropolitan areas. Airbus’s global supply chain, certification expertise, and government relationships enable it to bridge innovation with industrialization, ensuring urban air mobility solutions meet both European regulatory rigor and worldwide operational demands.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe urban air mobility market pursue five core strategies to establish sustainable leadership. First, they prioritize regulatory certification by working closely with the European Union Aviation Safety Agency to achieve type and operational approvals ahead of competitors. Second, they form strategic alliances with airports, public transport authorities, and energy providers to co-develop integrated vertiport ecosystems and power infrastructure. Third, they focus on noise reduction through aerodynamic design and operational curfews to gain social acceptance in densely populated cities. Fourth, they target public service applications such as medical transport and emergency response to demonstrate social value and accelerate policy support. Fifth, they adopt modular and scalable aircraft architectures that allow incremental upgrades in range, payload, and autonomy as battery and AI technologies mature.

EUROPE URBAN AIR MOBILITY MARKET NEWS

- In July 2024, Volocopter launched commercial air taxi operations during the Paris Olympics, transporting spectators between venues using EASA-certified VoloCity aircraft and strengthening its Europe urban air mobility market presence

- In February 2025, Lilium received type certification from the European Union Aviation Safety Agency for its seven-seat Lilium Jet, enabling intercity passenger services and strengthening its Europe urban air mobility market presence

- In October 2024, Airbus Urban Mobility partnered with Fraport and Deutsche Bahn to develop a multimodal vertiport at Frankfurt Airport, integrating aerial shuttles with high-speed rail and strengthening its Europe urban air mobility market presence

- In May 2024, Volocopter and Swissport inaugurated Europe’s first commercial vertiport at Paris Le Bourget Airport, featuring battery swap and passenger screening systems, and strengthening its Europe urban air mobility market presence

- In March 2025, Lilium signed a strategic agreement with Ferrovie dello Stato Italiane to deploy air shuttle services connecting Rome, Milan, and Naples by 2027, and strengthening its Europe urban air mobility market presence

MARKET SEGMENTATION

This research report on the Europe urban air mobility market has been segmented and sub-segmented into the following categories.

By Vehicle Type

- Air Taxis

- Air Metros

- Air Ambulance

- Last-Mile Delivery

- Others

By Range

- Intercity

- Intracity

By Operation

- Piloted

- Autonomous

- Hybrid

By End User

- Ridesharing Companies

- Scheduled Operators

- E-Commerce Companies

- Hospitals and Medical Agencies

- Private Operators

By Country

- United Kingdom

- France

- Spain

- German

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is the Europe urban air mobility market?

The Europe urban air mobility market features eVTOL aircraft for efficient city transport. It integrates vertiports and digital airspace for seamless aerial commuting.

Why is the Europe urban air mobility market emerging?

The Europe urban air mobility market emerges from traffic congestion and green transport demands. eVTOL solutions offer rapid alternatives to ground travel.

What segments define the Europe urban air mobility market?

Segments in the Europe urban air mobility market include passenger air taxis and cargo drones. Infrastructure like vertiports supports operational scalability.

Who leads the Europe urban air mobility market?

Leaders in the Europe urban air mobility market pioneer certified eVTOL designs. They collaborate on regulatory frameworks for commercial viability.

What drives innovation in the Europe urban air mobility market?

Innovation in the Europe urban air mobility market advances battery tech and autonomy. These enable quieter, efficient flights over urban landscapes.

How do regulations shape the Europe urban air mobility market?

Regulations in the Europe urban air mobility market ensure safe airspace integration via EASA standards. They guide certification and operational approvals.

What trends influence the Europe urban air mobility market?

Trends in the Europe urban air mobility market emphasize autonomous fleets and vertiport networks. Sustainability drives electric propulsion adoption.

What challenges face the Europe urban air mobility market?

Challenges in the Europe urban air mobility market involve airspace congestion and public acceptance. Solutions focus on advanced traffic management systems.

How does technology advance the Europe urban air mobility market?

Technology advances the Europe urban air mobility market with AI navigation and quiet electric propulsion. It ensures safe, scalable urban operations.

What role does infrastructure play in the Europe urban air mobility market?

Infrastructure like vertiports defines the Europe urban air mobility market by enabling takeoff and landing. Urban integration optimizes connectivity.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com