Europe Weight Loss Drugs Market Size, Share, Trends, & Growth Forecast Report By Type (Prescription Drugs, Over-the-Counter Drugs, Herbal and Natural Supplements) , Dosage, Target Audience, Mechanism of Action, and Distribution Channel and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

Europe Weight Loss Drugs Market Report Summary

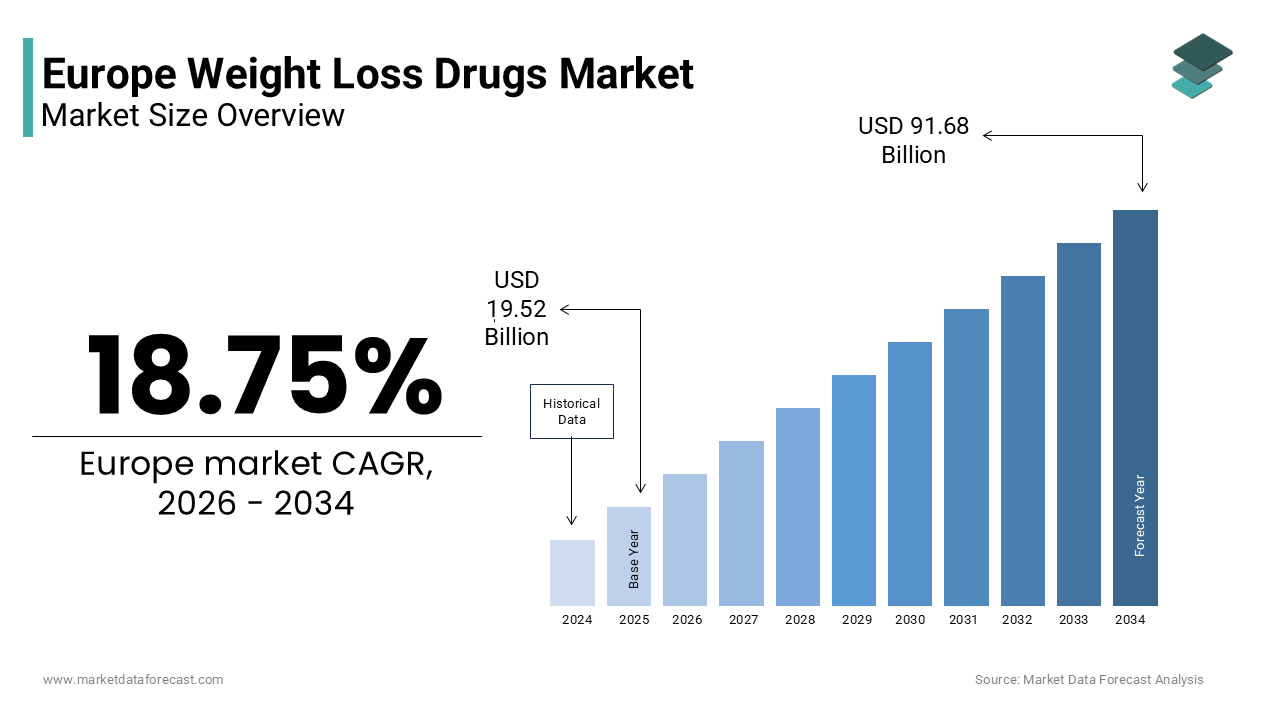

The Europe weight loss drugs market was valued at USD 19.52 billion in 2025, is estimated to reach USD 23.18 billion in 2026, and is projected to reach USD 91.68 billion by 2034, growing at a CAGR of 18.75% during the forecast period from 2026 to 2034. The growth of the European weight loss drugs market is driven by the rising prevalence of obesity and related comorbidities, increasing awareness of medical weight management, and advancements in pharmacological therapies such as GLP-1 receptor agonists. The shift in perception of obesity as a chronic disease rather than a lifestyle issue and the expansion of innovative treatment options are further fueling market growth. Additionally, integration with digital health platforms and personalized treatment approaches is accelerating adoption across Europe.

Key Market Trends

- Rising demand for GLP-1 receptor agonists and advanced hormonal therapies due to superior efficacy

- Increasing awareness of obesity as a chronic medical condition requiring pharmacological intervention

- Growing adoption of digital health platforms and remote monitoring solutions

- Strong focus on personalized medicine and combination therapies

- Expanding interest in herbal and natural supplements as complementary solutions

Segmental Insights

- Based on type, the prescription drugs segment was the largest and held a significant share of the Europe weight loss drugs market in 2025. The segment’s dominance is attributed to high clinical efficacy, strong regulatory approval standards, and increasing physician preference for medically supervised treatments.

- Based on dosage form, the injections segment accounted for a major share of the Europe weight loss drugs market in 2025. This is driven by the effectiveness of injectable GLP-1 therapies, improved patient outcomes, and convenient dosing regimens such as once-weekly injections.

Regional Insights

The European weight loss drugs market is witnessing rapid growth across major economies, supported by rising obesity prevalence, strong healthcare infrastructure, and increasing adoption of advanced therapies.

- Germany was the largest contributor, accounting for a significant share of the European market in 2025, driven by high obesity rates, strong reimbursement frameworks, and advanced healthcare systems. The region overall benefits from growing health awareness, supportive clinical guidelines, and expanding pharmaceutical innovation.

Competitive Landscape

The Europe weight loss drugs market is highly competitive, characterized by the presence of leading pharmaceutical companies focusing on innovation, clinical research, and expanding production capacity. Companies are emphasizing next-generation therapies, digital integration, and strategic partnerships to strengthen their market positions. Prominent players in the Europe weight loss drugs market include Novo Nordisk A/S, Eli Lilly and Company, Pfizer Inc., Amgen Inc., AstraZeneca plc, Sanofi S.A., Novartis AG, Roche Holding AG, Biocon Ltd., and Hanmi Pharmaceutical Co., Ltd.

Europe Weight Loss Drugs Market Size

The Europe weight loss drugs market size was valued at USD 19.52 billion in 2025 and is anticipated to reach USD 23.18 billion in 2026 from USD 91.68 billion by 2034, growing at a CAGR of 18.75% during the forecast period from 2026 to 2034.

The Europe weight loss drugs market is expected to experience robust growth over the next several years as healthcare systems increasingly prioritize the pharmacological treatment of metabolic disorders. These therapeutic agents primarily function through mechanisms such as appetite suppression, inhibition of nutrient absorption, or modulation of hormonal pathways that regulate satiety and glucose metabolism. The clinical landscape has shifted dramatically with the advent of glucagon like peptide 1 receptor agonists, which have demonstrated superior efficacy compared to traditional treatments. Obesity remains a critical public health challenge across the continent, with the World Health Organization stating that more than 59% of adults in the European Region are living with overweight or obesity. As per Eurostat data, the prevalence of self reported obesity in adults aged 18 years and over reached 17% in several member states, indicating a substantial patient pool requiring medical intervention. The regulatory environment in Europe is stringent, with the European Medicines Agency evaluating safety and efficacy profiles before approval. Recent approvals have expanded the therapeutic arsenal, offering patients new options for long term weight management. The integration of these drugs into standard care protocols reflects a growing recognition of obesity as a chronic disease rather than a lifestyle choice. This paradigm shift underscores the importance of accessible and effective pharmacotherapy in combating the rising tide of metabolic disorders across European healthcare systems.

MARKET DRIVERS

Rising Prevalence of Obesity Related Comorbidities Drives Pharmaceutical Demand

The rising incidence of obesity associated health complications is poised to drive sustained demand for weight loss pharmacotherapy across Europe in the coming years, which is one of the major market drivers. Chronic conditions such as type 2 diabetes, cardiovascular diseases, and hypertension are increasingly linked to excessive body weight, prompting healthcare providers to prioritize effective weight management strategies. According to the International Diabetes Federation, approximately 61 million adults in Europe were living with diabetes in 2021, a figure projected to rise significantly in the coming decades. This correlation between adiposity and metabolic dysfunction creates a compelling clinical imperative for interventions that offer dual benefits of weight reduction and glycemic control. Glucagon like peptide 1 receptor agonists have emerged as pivotal tools in this context, demonstrating ability to lower blood sugar levels while facilitating substantial weight loss. The European Society of Cardiology notes that cardiovascular disease remains the leading cause of death in Europe, accounting for nearly 45% of all deaths. Weight reduction through pharmacological means has been shown to mitigate risk factors associated with these fatal conditions. Consequently, physicians are more inclined to prescribe anti-obesity medications as part of comprehensive treatment plans for patients with multiple comorbidities. This clinical validation enhances patient adherence and justifies the higher cost of newer therapies. The burden on healthcare systems from treating obesity related illnesses further incentivizes payers to cover these treatments, recognizing their potential to reduce long term medical expenses associated with chronic disease management.

Increasing Consumer Awareness and Shifting Societal Perceptions Fuel Market Growth

Growing public awareness regarding health and wellness, coupled with evolving societal attitudes toward obesity is expected to continue fuelling the regional market growth across European demographic segments. Individuals are increasingly informed about the medical implications of excess weight and are actively seeking professional assistance rather than relying solely on informal dieting methods. Social media platforms and digital health applications have democratized access to information, enabling consumers to learn about advanced therapeutic options. As per a survey conducted by the European Commission, 70% of Europeans consider health to be very important in their lives, which is reflecting an increased focus on personal well-being. This cultural shift reduces the stigma associated with obesity, encouraging more individuals to consult healthcare professionals for medical weight management solutions. Furthermore, the visibility of successful outcomes from new pharmacological treatments has generated considerable interest among the general population. Patients are more willing to invest in prescribed medications that offer proven results compared to over the counter supplements with limited efficacy. The influence of celebrity endorsements and public figures discussing their weight loss journeys has also normalized the use of prescription drugs for weight management. This normalization fosters a conducive environment for market expansion as patients feel empowered to discuss their weight concerns openly with doctors. The convergence of health consciousness and reduced stigma creates a robust demand base for innovative weight loss therapies across diverse demographic segments in Europe.

MARKET RESTRAINTS

High Treatment Costs and Limited Reimbursement Coverage Restrict Market Access

The prohibitive cost of novel weight loss medications combined with restrictive reimbursement policies continues to act as a significant barrier to market expansion in Europe. Newer anti-obesity drugs, particularly glucagon like peptide 1 receptor agonists, carry substantial price tags that often exceed the budget constraints of both patients and healthcare systems. In many European countries, national health services do not fully cover these treatments, categorizing them as lifestyle drugs rather than essential medicines. According to data from the Organisation for Economic Cooperation and Development, out of pocket expenditure on pharmaceuticals varies widely across Europe, with some nations requiring patients to bear up to 50% of medication costs. This financial burden limits accessibility primarily to affluent individuals, thereby excluding a large segment of the population that could benefit from these therapies. Public healthcare providers face immense pressure to manage budgets amidst rising demand for various medical services, leading to stringent criteria for approving expensive treatments. Only patients with severe obesity and specific comorbidities may qualify for subsidized access, leaving those with moderate overweight conditions without affordable options. The disparity in reimbursement policies across different European nations further complicates market dynamics, creating uneven access levels. Pharmaceutical companies face challenges in negotiating favorable pricing agreements with government bodies, which strive to balance innovation incentives with fiscal responsibility. Until broader reimbursement frameworks are established, the high cost will remain a formidable restraint limiting the widespread adoption of effective weight loss pharmacotherapy.

Stringent Regulatory Hurdles and Safety Concerns Impede Rapid Adoption

Rigorous regulatory requirements and ongoing safety monitoring obligations are further hampering the expansion of the European weight loss drugs market. The European Medicines Agency maintains strict evaluation protocols to ensure the safety and efficacy of new pharmaceutical products, resulting in prolonged approval timelines. Historical precedents involving withdrawn weight loss medications due to adverse cardiovascular effects have heightened regulatory scrutiny, necessitating extensive clinical trials before market authorization. According to the European Medicines Agency, the assessment process for new active substances can take up to 210 days, excluding clock stops for additional data requests. This lengthy procedure delays patient access to innovative therapies and increases development costs for manufacturers. Post marketing surveillance requirements further compel companies to monitor long term safety profiles, adding to operational burdens. Concerns regarding potential side effects such as gastrointestinal disturbances and rare but serious conditions like pancreatitis influence prescribing patterns. Healthcare professionals remain cautious, often reserving these drugs for cases where benefits clearly outweigh risks. Patient apprehension regarding safety also affects adherence rates, with some individuals discontinuing treatment due to mild adverse events. The need for continuous risk management plans and periodic safety updates requires significant resource allocation from pharmaceutical firms. These regulatory complexities create an environment of caution that slows the pace of market penetration. Balancing innovation with patient safety remains a delicate task for regulators, ensuring that only thoroughly vetted treatments reach the European market while maintaining public trust in pharmacological interventions.

MARKET OPPORTUNITIES

Expansion into Combination Therapies and Personalized Medicine Offers Growth Potential

The development of combination therapies and personalized medicine approaches is a lucrative opportunity for the Europe weight loss drugs market over the coming years. Researchers are increasingly exploring synergistic effects of combining different molecular targets to enhance efficacy and minimize side effects. Dual and triple agonists that target multiple hormonal pathways simultaneously have shown promising results in clinical trials, offering greater weight loss percentages compared to single agent therapies. According to clinical studies, combination treatments have achieved weight reduction exceeding 20% in obese patients, surpassing the outcomes of existing monotherapies. This scientific advancement opens new avenues for pharmaceutical companies to differentiate their portfolios and address patients who do not respond adequately to current options. Personalized medicine leverages genetic and biomarker data to tailor treatments to individual patient profiles, improving therapeutic outcomes and adherence. The integration of digital health tools allows for real time monitoring of patient responses, enabling dynamic adjustment of dosage and regimen. This precision approach aligns with the broader trend toward customized healthcare solutions in Europe. Regulatory bodies are showing willingness to expedite reviews for innovative combination products that demonstrate superior clinical benefits. Collaborations between biotechnology firms and academic institutions are accelerating the discovery of novel targets, fostering a vibrant ecosystem for innovation. By focusing on enhanced efficacy and tailored treatments, companies can capture value from patients seeking optimal results, thereby driving market growth through scientific differentiation and improved patient satisfaction.

Integration with Digital Health Platforms and Remote Monitoring Enhances Engagement

The seamless integration of weight loss pharmacotherapy with digital health platforms and remote monitoring technologies is set to create significant opportunities for the European weight loss drugs market. Digital therapeutics and mobile applications provide continuous support, tracking dietary habits, physical activity, and medication adherence, which are crucial for successful weight management. According to a report by the European Digital Health Observatory, the adoption of health apps in Europe has grown by 30% annually, indicating a receptive user base for integrated solutions. Pharmaceutical companies are partnering with technology providers to offer comprehensive care packages that combine drug therapy with behavioral coaching and data analytics. This holistic approach addresses the multifactorial nature of obesity, enhancing the effectiveness of pharmacological interventions. Remote monitoring enables healthcare providers to adjust treatment plans based on real time data, reducing the need for frequent clinic visits and improving convenience for patients. Insurance providers are increasingly recognizing the value of these integrated models in reducing long term healthcare costs, potentially leading to broader coverage decisions. The availability of user friendly interfaces and personalized feedback loops increases patient engagement and motivation, leading to higher adherence rates. Furthermore, data collected through these platforms can inform future research and development efforts, creating a feedback loop for continuous improvement. By leveraging digital ecosystems, stakeholders can deliver superior value propositions that extend beyond mere medication supply, fostering loyalty and driving sustainable market expansion in the European landscape.

MARKET CHALLENGES

Supply Chain Vulnerabilities and Manufacturing Constraints Pose Logistical Challenges

Persistent supply chain disruptions and manufacturing limitations are primarily challenging the growth of the European weight loss drugs market. The surge in demand for popular anti-obesity medications has outpaced production capacity, leading to widespread shortages across multiple countries. According to the European Medicines Agency, several member states reported intermittent shortages of key weight loss ingredients due to raw material scarcity and production bottlenecks. These supply issues undermine patient trust and continuity of care, forcing clinicians to switch prescriptions or delay treatments. The complex global supply chain for pharmaceutical ingredients relies heavily on specific geographic regions, making it vulnerable to geopolitical tensions and logistical interruptions. Manufacturing facilities require significant time and investment to scale up production, limiting the ability to respond rapidly to demand spikes. Quality control standards in Europe are exceptionally high, further constraining the speed at which new production lines can be approved and operationalized. The reliance on single source suppliers for critical components exacerbates the risk of disruptions, highlighting the need for diversification strategies. Healthcare systems struggle to manage inventory levels effectively amidst unpredictable supply flows, leading to inefficiencies and increased administrative burdens. Patients facing inconsistent access may resort to unofficial channels, posing safety risks and undermining regulated market integrity. Addressing these logistical challenges requires coordinated efforts among manufacturers, regulators, and distributors to build resilient supply networks that can withstand future demand fluctuations and ensure reliable access to essential therapies.

Ethical Considerations and Equitable Access Debates Hinder Policy Formulation

Ethical dilemmas surrounding equitable access and the prioritization of weight loss drugs within public healthcare systems create significant challenges for policy makers in Europe. The high cost of these medications raises questions about resource allocation, particularly when other critical healthcare needs remain underfunded. Debates persist regarding whether obesity treatment should be prioritized over other chronic conditions, given the perceived lifestyle components associated with weight gain. According to bioethics experts cited in European health policy forums, there is concern that widespread coverage of expensive weight loss drugs could exacerbate health inequalities if access is determined by socioeconomic status rather than medical need. Critics argue that public funds might be better spent on preventive measures such as nutrition education and community fitness programs rather than costly pharmacological interventions. This ethical tension complicates the formulation of uniform reimbursement policies across different European nations. Some countries face public backlash against covering weight loss drugs, viewing them as cosmetic enhancements rather than medical necessities. The stigma associated with obesity further influences policy decisions, with some policymakers hesitant to allocate substantial resources to treatments for a condition often misunderstood by the general public. Balancing the medical necessity of treating obesity as a chronic disease with fiscal responsibility and social equity remains a complex challenge. These ethical considerations slow down the harmonization of regulations and reimbursement frameworks, creating a fragmented market environment that hinders optimal patient care and market stability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 18.75% |

| Segments Covered | By Type, Dosage, Target Audience, Mechanism of Action, and Distribution Channel and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

| Key Market Players | Novo Nordisk A/S and Eli Lilly and Company as dominant leaders, along with Pfizer Inc., Amgen Inc., AstraZeneca plc, Sanofi S.A., Novartis AG, Roche Holding AG, Biocon Ltd., and Hanmi Pharmaceutical Co., Ltd., |

SEGMENTAL ANALYSIS

By Type Insights

The prescription drugs segment held the dominant position in the Europe weight loss drugs market by accounting for 66.5% of the regional market share in 2025. The superior clinical efficacy of approved pharmacotherapies compared to over the counter alternatives is majorly driving the dominance of prescription drugs segment in the European market. Healthcare professionals increasingly prescribe glucagon like peptide 1 receptor agonists and other advanced molecules due to their proven ability to induce significant weight loss in patients with obesity. According to the European Medicines Agency, the approval of new anti-obesity medications has expanded treatment options, leading to higher prescription rates across member states. The stringent regulatory framework in Europe ensures that only drugs with robust safety and efficacy profiles reach the market, fostering trust among physicians and patients. Clinical guidelines from the European Association for the Study of Obesity recommend pharmacological intervention for individuals with a body mass index above 30 or those with comorbidities, further boosting demand for prescription treatments. The integration of these drugs into national healthcare protocols in countries like Germany and the United Kingdom enhances accessibility for eligible patients. Moreover, the rising prevalence of obesity related complications such as type 2 diabetes necessitates medically supervised treatment plans, which predominantly involve prescription medications. The high cost of these drugs is often partially offset by insurance coverage in specific cases, making them a viable option for many patients. The dominance of this segment is reinforced by continuous research and development efforts by pharmaceutical companies to introduce more effective and safer prescription options.

On the other hand, the herbal and natural supplements segment is projected to register the highest CAGR of 10.6% over the forecast period owing to the increasing consumer preference for holistic and non-invasive weight management solutions. Many individuals in Europe are seeking alternatives to synthetic drugs due to concerns about potential side effects and long term health impacts. According to a survey by the European Federation of Associations of Health Product Manufacturers, sales of natural health products have increased by 15% annually, reflecting a shift toward preventive healthcare. The availability of diverse herbal ingredients such as green tea extract, garcinia cambogia, and glucomannan appeals to consumers looking for mild and natural aids. Social media influencers and wellness advocates frequently promote these supplements, enhancing their visibility and acceptance among younger demographics. The ease of access through online retail platforms and health stores further facilitates market expansion. Additionally, the perception of herbal supplements as safe and compatible with healthy lifestyles drives their adoption among fitness enthusiasts and individuals with moderate weight concerns. Regulatory improvements in labeling and quality standards for natural products in the European Union have also boosted consumer confidence. As awareness of the benefits of plant based remedies grows, the demand for herbal weight loss supplements continues to rise, positioning this segment as a key growth driver in the market.

By Mechanism of Action Insights

The hormonal regulators segment dominated the market by commanding for 51.6% of the regional market share in 2025. The growth of the hormonal regulators segment in the European market is driven by the widespread adoption of glucagon like peptide 1 receptor agonists. These agents mimic natural hormones that regulate appetite and glucose metabolism, offering superior weight loss outcomes compared to traditional mechanisms. According to clinical data published in The Lancet, patients treated with semaglutide achieved an average weight reduction of 15%, significantly higher than results from appetite suppressants or fat blockers. The mechanism of action involves slowing gastric emptying and enhancing satiety signals to the brain, which helps patients maintain calorie deficits with less effort. The European Society of Endocrinology highlights the role of hormonal therapies in managing obesity as a chronic metabolic disease, encouraging their integration into standard care. The success of these drugs in treating both obesity and type 2 diabetes creates a dual therapeutic value, appealing to clinicians and payers. Pharmaceutical companies are investing heavily in developing next generation hormonal regulators with improved profiles, further solidifying this segment's dominance. The strong clinical evidence supporting their efficacy has led to broader guideline recommendations across Europe. As healthcare systems recognize the long term benefits of effective weight management, the demand for hormonal regulators continues to surge. The segment's leadership is also supported by extensive marketing efforts and educational initiatives that highlight the scientific basis of hormonal weight control.

On the other hand, the appetite suppressants segment is expected to grow at a CAGR of 8.4% over the forecast period in the European market owing to their established presence in the market and lower cost compared to newer therapies. These drugs function by influencing neurotransmitters in the brain to reduce hunger sensations, providing a straightforward approach to weight management. According to data from the Organisation for Economic Co operation and Development, older generation appetite suppressants remain widely prescribed in several European countries due to their affordability and familiarity among healthcare providers. Patients with mild to moderate obesity often prefer these medications as a first line treatment before considering more expensive hormonal options. The availability of generic versions of common appetite suppressants further enhances accessibility for budget conscious consumers. Clinical studies indicate that when combined with lifestyle modifications, appetite suppressants can achieve modest but meaningful weight loss, making them a viable option for many individuals. The segment benefits from a well understood safety profile, although monitoring for potential side effects such as increased heart rate remains necessary. Healthcare systems in regions with limited reimbursement for newer drugs continue to rely on appetite suppressants for managing obesity. The steady growth of this segment is also supported by ongoing research into novel compounds with fewer side effects. As demand for accessible weight loss solutions persists, appetite suppressants maintain a significant role in the therapeutic landscape.

By Target Audience Insights

The individuals with obesity or overweight segment held the major share of the European weight loss drugs market in 2025 due to the critical medical need for effective weight management in this population. Obesity is recognized as a chronic disease by major European health organizations, necessitating professional intervention to prevent severe health complications. According to the World Health Organization, more than 59% of adults in the European Region are living with overweight or obesity, creating a vast patient base for weight loss drugs. Healthcare providers prioritize pharmacological treatments for these individuals to reduce the risk of developing type 2 diabetes, cardiovascular diseases, and other metabolic disorders. Clinical guidelines recommend medication for patients with a body mass index above 30 or those with a body mass index above 27 accompanied by comorbidities. The high prevalence of obesity in countries such as the United Kingdom and Germany fuels demand for prescription drugs in this segment. Insurance coverage and reimbursement policies in certain nations support access to these treatments for eligible patients, further boosting market participation. The severity of health risks associated with obesity motivates patients to adhere to prescribed regimens, ensuring consistent demand. Public health campaigns raising awareness about the dangers of obesity also encourage individuals to seek medical help. The dominance of this segment reflects the urgent need to address the obesity epidemic through effective pharmacological means.

The individuals with chronic diseases segment is projected to exhibit the highest CAGR of 11.4% over the forecast period owing to the dual therapeutic benefits of weight loss drugs in managing conditions such as type 2 diabetes and hypertension. Many anti obesity medications, particularly glucagon like peptide 1 receptor agonists, offer significant advantages in glycemic control and cardiovascular risk reduction. According to the International Diabetes Federation, the number of adults with diabetes in Europe is expected to reach 68 million by 2045, highlighting the growing intersection between obesity and chronic disease management. Clinicians increasingly prescribe these drugs to patients with multiple comorbidities to address both weight and metabolic health simultaneously. Clinical trials have demonstrated that weight loss induced by these medications can improve insulin sensitivity and lower blood pressure, reducing the overall burden of chronic diseases. The European Society of Cardiology emphasizes the importance of weight management in preventing cardiovascular events, supporting the use of these drugs in high risk populations. Reimbursement policies in some countries favor treatments that provide comprehensive health benefits, making them accessible to patients with chronic conditions. The growing recognition of obesity as a root cause of many chronic diseases drives the adoption of weight loss pharmacotherapy in this segment. As the prevalence of chronic diseases rises, the demand for integrated treatment solutions continues to expand rapidly.

By Dosage Form Insights

The injections segment led the market with 50.8% of the regional market share in 2025. The dominance of injections segment in the European market is primarily due to the dominance of injectable glucagon like peptide 1 receptor agonists such as semaglutide and liraglutide. These formulations offer superior bioavailability and consistent drug delivery, resulting in more predictable and effective weight loss outcomes compared to oral alternatives. According to clinical data from Novo Nordisk, injectable semaglutide demonstrated significantly greater weight reduction than placebo in large scale trials, reinforcing its position as a preferred treatment option. The once weekly dosing regimen of many injectable drugs enhances patient convenience and adherence, addressing a common challenge in long term weight management. Healthcare providers favor injections for their proven efficacy in patients with severe obesity, where maximum therapeutic impact is required. The European Medicines Agency has approved several injectable agents for chronic weight management, expanding the available options for clinicians. Patient education programs and support services provided by manufacturers help alleviate fears related to self-injection, which is further boosting acceptance. The high cost of injectable drugs is often justified by their superior performance, leading to widespread adoption despite price considerations. The robust supply chains and manufacturing capabilities established by key pharmaceutical players is further propelling the dominance of injections segment in the regional market. As new injectable formulations enter the market, the dominance of this dosage form is expected to strengthen further.

On the other hand, the tablets segment is anticipated to grow at a CAGR of 9.4% over the forecast period in the European market owing to the patient preference for oral administration and the introduction of new oral weight loss medications. Many individuals hesitate to use injectable therapies due to needle phobia or inconvenience, making tablets an attractive alternative. According to a survey by the European Patients Forum, a significant proportion of patients express a strong preference for oral medications due to ease of use and discretion. The recent approval of oral semaglutide and other small molecule drugs has expanded the options available in this format, offering efficacy comparable to some injectables. Pharmaceutical companies are investing in advanced delivery technologies to enhance the absorption and effectiveness of oral weight loss drugs. The lower production costs associated with tablets compared to injectables also make them more affordable for patients and healthcare systems. In regions with limited access to specialized injection training, tablets provide a practical solution for widespread deployment. The convenience of storing and transporting tablets further supports their adoption in remote or resource limited settings. As research into oral formulations advances, the efficacy gap between tablets and injections is narrowing, driving increased interest in this segment. The growth of the tablets segment reflects a broader trend toward patient centric drug delivery methods.

REGIONAL ANALYSIS

Germany Weight Loss Drugs Market Analysis

Germany stood as the largest market for weight loss drugs in Europe with 24.1% of the regional market share in 2025. The dominance of Germany in the European market is driven by a high prevalence of obesity and a robust healthcare system. According to the Robert Koch Institute, nearly 24% of adults in Germany are classified as obese, creating a substantial demand for pharmacological interventions. The country’s advanced medical infrastructure facilitates early diagnosis and treatment of obesity, with many clinics specializing in metabolic disorders. Statutory health insurance schemes in Germany cover a range of prescription medications, improving access for patients with diagnosed obesity. The presence of major pharmaceutical companies and research institutions in Germany fosters innovation and rapid adoption of new therapies. Clinical guidelines from the German Obesity Society recommend comprehensive treatment approaches, including pharmacotherapy, for eligible patients. High health awareness among the German population encourages individuals to seek professional help for weight management. The government’s focus on preventive healthcare further supports the integration of weight loss drugs into standard care protocols. Strong distribution networks and a well developed retail pharmacy sector ensure wide availability of medications. The combination of high disease burden, favorable reimbursement policies, and a commitment to advanced healthcare infrastructure positions Germany as the dominant market for weight loss drugs in Europe.

COMPETITIVE LANDSCAPE

The competition in the Europe weight loss drugs market is characterized by intense rivalry among established pharmaceutical giants and emerging biotechnology firms striving for technological superiority. Major players leverage their extensive research pipelines to introduce innovative therapies that offer enhanced efficacy and convenience. The market dynamics are shaped by continuous clinical advancements particularly in the realm of glucagon like peptide 1 receptor agonists and multi target hormones. Companies compete not only on product performance but also on supply chain reliability and manufacturing scalability to address persistent shortages. Strategic collaborations with digital health platforms have become essential for differentiating offerings through comprehensive care models. Regulatory compliance and successful navigation of reimbursement landscapes serve as critical competitive advantages in this highly regulated environment. Patent expirations and the entry of generic alternatives pose challenges that incumbent firms counter through lifecycle management and brand loyalty initiatives. The focus on personalized medicine and real world evidence generation further intensifies competition as companies seek to demonstrate superior value propositions. Market participants also engage in aggressive marketing campaigns to educate healthcare providers and reduce societal stigma associated with obesity. This competitive landscape drives rapid innovation and improves patient access to effective weight management solutions across the region.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe weight loss drugs market include

- Novo Nordisk A/S

- Eli Lilly and Company

- Pfizer Inc.

- Amgen Inc.

- AstraZeneca plc

- Sanofi S.A.

- Novartis AG

- Roche Holding AG

- Biocon Ltd.

- Hanmi Pharmaceutical Co., Ltd.

Top Players in the Market

Novo Nordisk

Novo Nordisk stands as a pivotal force in the Europe weight loss drugs market through its pioneering development of glucagon like peptide 1 receptor agonists. The company has significantly influenced global therapeutic standards with its flagship products semaglutide and liraglutide which demonstrate high efficacy in chronic weight management. Recent actions include expanding manufacturing capacities across European facilities to address surging demand and mitigate supply constraints. Novo Nordisk actively engages in clinical research to explore additional indications for its existing portfolio thereby broadening its therapeutic scope. The company collaborates with healthcare providers to enhance disease awareness and promote early intervention strategies. Its robust pipeline includes next generation multi agonist candidates that target multiple hormonal pathways simultaneously. These strategic initiatives reinforce its leadership position by ensuring consistent product availability and scientific innovation. Novo Nordisk also invests in digital health solutions to support patient adherence and long term outcomes. By prioritizing sustainable production methods and ethical clinical practices the company strengthens its reputation among regulators and patients alike. This comprehensive approach ensures sustained relevance and competitive advantage in the evolving landscape of obesity treatment across Europe and globally.

Eli Lilly and Company

Eli Lilly and Company plays a critical role in the Europe weight loss drugs market by introducing innovative therapies such as tirzepatide which targets dual hormone receptors. The company has demonstrated strong commitment to addressing obesity as a complex chronic disease through extensive clinical trials and regulatory engagements. Recent actions involve securing approvals for new indications and expanding distribution networks to improve patient access across various European countries. Eli Lilly invests heavily in research and development to create novel molecules with improved safety profiles and enhanced efficacy. The company partners with digital health platforms to integrate medication management with lifestyle coaching services. These collaborations aim to provide holistic care solutions that support sustained weight loss and metabolic health. Eli Lilly also focuses on educating healthcare professionals about the benefits of early pharmacological intervention. By leveraging its global expertise and local market insights the company adapts its strategies to meet diverse regional needs. Its emphasis on patient centric innovation and strategic partnerships solidifies its position as a key contributor to the advancement of weight management therapies in Europe and worldwide.

Boehringer Ingelheim

Boehringer Ingelheim contributes significantly to the Europe weight loss drugs market through its strategic focus on developing novel mechanisms for metabolic disease management. The company has formed key alliances with biotechnology firms to accelerate the discovery of next generation weight loss candidates. Recent actions include initiating late stage clinical trials for oral GLP 1 receptor agonists which offer convenient administration options for patients. Boehringer Ingelheim emphasizes precision medicine approaches to tailor treatments based on individual patient profiles and genetic markers. The company actively participates in policy discussions to shape favorable reimbursement frameworks for obesity treatments in European markets. It also invests in real world evidence studies to demonstrate the long term benefits of its therapeutic candidates. By fostering innovation through open collaboration and rigorous scientific inquiry Boehringer Ingelheim enhances its portfolio diversity. The company’s commitment to addressing unmet medical needs in obesity care drives its strategic investments in research infrastructure. These efforts enable Boehringer Ingelheim to remain competitive and responsive to changing market dynamics while delivering valuable solutions to patients and healthcare systems across Europe and beyond.

Top Strategies Used by the Key Market Participants

Key players in the Europe weight loss drugs market primarily focus on expanding manufacturing capabilities to meet escalating demand for anti obesity medications. Companies invest heavily in research and development to create novel molecules with superior efficacy and safety profiles. Strategic partnerships with digital health providers enable integrated care solutions that enhance patient adherence and outcomes. Pharmaceutical firms actively engage in regulatory dialogues to secure broader reimbursement coverage across European healthcare systems. Clinical trial expansions into diverse patient populations help validate therapeutic benefits for various comorbidities. Marketing efforts emphasize disease awareness and destigmatization of obesity to encourage early treatment seeking behavior. Supply chain diversification strategies mitigate risks associated with raw material shortages and logistical disruptions. Companies also pursue licensing agreements to access innovative technologies and broaden their product portfolios. Educational initiatives targeting healthcare professionals ensure proper prescribing practices and optimal patient management. These multifaceted strategies collectively strengthen market positions and drive sustainable growth in the competitive landscape of weight management therapies throughout Europe.

MARKET SEGMENTATION

This research report on the Europe weight loss drugs market has been segmented and sub-segmented based on the following categories.

By Type

- Prescription Drugs

- Over-the-Counter Drugs

- Herbal and Natural Supplements

By Dosage

- Tablets

- Capsules

- Liquids

- Injections

By Target Audience

- Individuals with Obesity or Overweight

- Individuals with Chronic Diseases

- Fitness and Wellness Enthusiasts

By Mechanism of Action

- Appetite Suppressants

- Fat Blockers

- Stimulants

- Hormonal Regulators

By Distribution Channel

- Pharmacies

- Online Retailers

- Healthcare Professionals

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com