Global Family Entertainment Centers Market Size, Share, Trends & Growth Forecast Report – Segmented By Demographics, Facility Size, Revenue Source, Application, Type, & Region - Industry Forecast From 2024 to 2033

Global Family Entertainment Centers Market Size

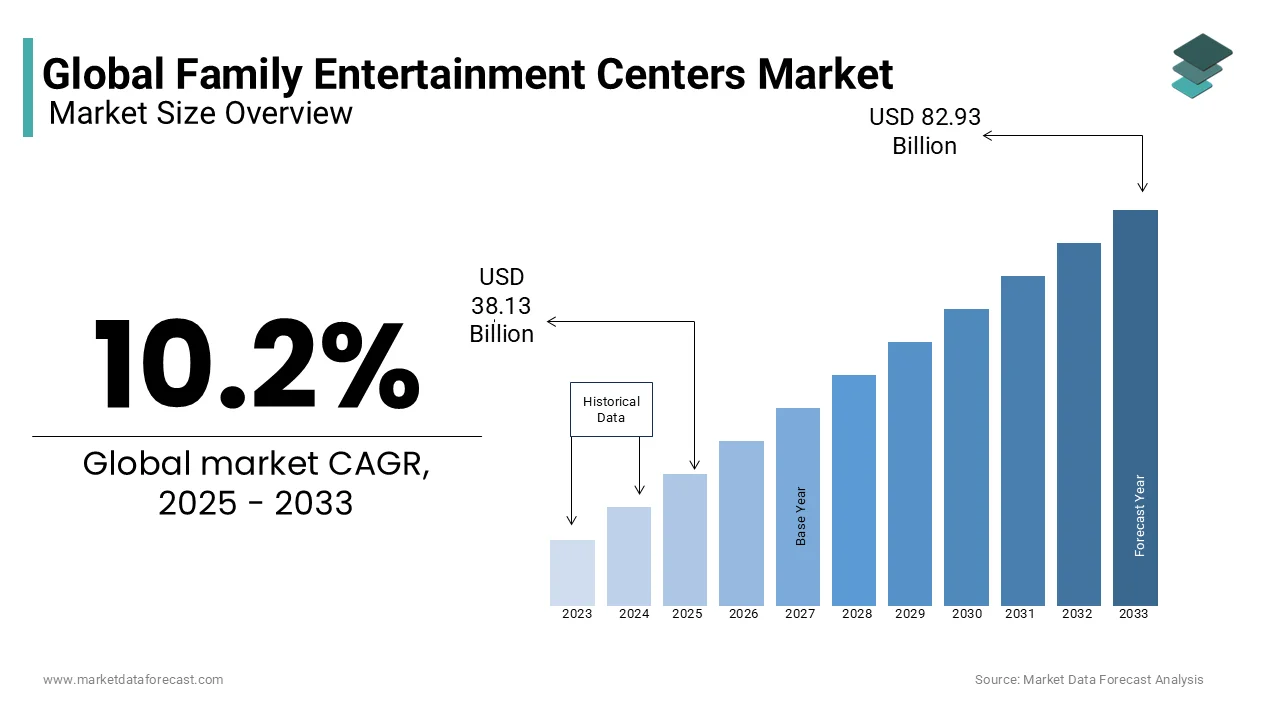

The global family entertainment centers market was worth USD 34.60 billion in 2024. The global market is projected to grow at a CAGR of 10.2% from 2025 to 2033, and the global market size is expected to be worth USD 82.93 billion by 2033 from USD 38.13 billion in 2025.

The Family Entertainment Centers (FECs) are a specialized segment of the leisure industry comprising indoor and outdoor venues designed to deliver multi-generational recreational experiences through a curated mix of attractions such as arcade games, laser tag, mini-golf, trampolines, and edutainment zones. Unlike traditional amusement parks, FECs are typically located in suburban or urban commercial hubs, offering shorter-duration, accessible visits. According to the International Association of Amusement Parks and Attractions, over 380 million visits were recorded at FECs across North America and Europe in 2023, with children aged 4–12 and their caregivers constituting the primary demographic.

MARKET DRIVERS

Rising Demand for Screen-Free, Experiential Family Outings

The growing parental preference for immersive, screen-free recreational environments that encourage physical activity and social interaction among children is driving the growth of the Family Entertainment Centers (FECs) Market. FECs address this need by offering interactive attractions such as obstacle courses, virtual reality arenas, and skill-based games that blend entertainment with motor development. A 2023 study by the Child Mind Institute found that 67% of parents in urban U.S. households expressed concern about excessive screen exposure, with 52% indicating they deliberately scheduled weekly off-screen activities.

Expansion of Suburban Mixed-Use Developments and Retail Synergies

The integration of FECs into mixed-use commercial developments, where they serve as anchor tenants that drive foot traffic to adjacent retail and dining outlets, is leveraging the growth of the Family Entertainment Centers (FECs) Market. These centers benefit from high visibility, ample parking, and synergistic consumer behavior. According to the National Retail Federation reports that families visiting FECs spend an average of $42 on retail and food services during the same trip, which is amplifying their economic value to developers.

MARKET RESTRAINTS

High Capital Intensity and Operational Cost Pressures

The substantial capital investment required for facility development, equipment procurement, and ongoing maintenance is restricting the growth of the Family Entertainment Centers Market. Additionally, operational expenses, including staffing, utilities, and equipment recalibratio,n consume approximately 55% of gross revenue, as reported by the International Council of Shopping Centers. These financial burdens limit scalability for independent operators and deter new entrants, particularly in markets where consumer spending remains volatile.

Vulnerability to Public Health and Safety Regulations

FECs are highly susceptible to disruptions from public health mandates and evolving safety standards in the wake of global health crises is limiting the growth of the Family Entertainment Centers Market. During the 2020–2021 period, over 70% of FECs in the U.S. and EU were forced to close temporarily due to pandemic-related restrictions, as documented by the World Health Organization’s Regional Office for Europe. Moreover, safety incidents involving equipment malfunction or child injuries can trigger regulatory scrutiny. In 2023, Australia’s Product Safety Commission issued 14 recalls of inflatable play structures used in FECs due to entrapment and collapse risks. These regulatory and reputational vulnerabilities necessitate continuous compliance investments, which are constraining operational flexibility and profitability.

MARKET OPPORTUNITIES

Integration of Immersive Technologies and Gamified Learning

The fusion of augmented reality (AR), virtual reality (VR), and educational content to create “edutainment” experiences that appeal to both children and academically focused parents is likely to impact on the growth of the Family Entertainment Centers Market. FECs are increasingly incorporating STEM-based attractions such as robotics challenges, coding games, and science-themed escape rooms. According to the Joan Ganz Cooney Center at Sesame Workshop, 73% of parents consider educational value a factor when selecting recreational activities for children. In Singapore, the government-backed PlayMakers Festival has collaborated with FEC operators to introduce curriculum-aligned play zones that teach physics and problem-solving through interactive exhibits. Similarly, in the U.S., Wonder Works has reported a 41% increase in school group bookings since launching its “Science of Fun” program.

Strategic Partnerships with Franchise Brands and IP Licensing

The leveraging of intellectual property (IP) from globally recognized children’s franchises is an avenue for FECs seeking differentiation and brand loyalty, which is also enhances the growth opportunities for the Family Entertainment Centers Market. Collaborations with entertainment giants such as Disney, Universal, and Mattel enable centers to feature themed zones based on popular characters like Peppa Pig, Paw Patrol, and Minions. As per the Licensing Industry Merchandisers’ Association, licensed children’s entertainment properties generated $129 billion in global retail sales in 2023, reflecting strong consumer affinity.

MARKET CHALLENGES

Workforce Retention and Training Consistency

The difficulty in maintaining a skilled, consistent, and motivated workforce in frontline guest service roles is acting as a barrier to the growth of Fthe amily Entertainment Centers Market. High employee turnover averaging 95% annually in the U.S. leisure sector, as reported by the Bureau of Labor Statistics undermines service quality and operational continuity. Many FECs rely on part-time and seasonal staff, with 62% of employees under the age of 24, according to the National Association of Theatre Owners, resulting in frequent retraining cycles. Inadequate training can lead to safety lapses; a 2022 incident at a Texas-based trampoline park, where improper supervision led to a spinal injury, prompted the Consumer Product Safety Commission to issue new operational guidelines. Establishing standardized certification programs and career progression paths remains a systemic challenge for smaller operators lacking centralized HR infrastructure.

Balancing Digital and Physical Engagement Without Diminishing Tangibility

Integrating digital enhancements such as app-based scoring, contactless payments, and AR overlays without compromising the tactile, physical nature of play that defines their appeal is likely to hinder the growth of the Family Entertainment Centers Market. Over-digitization risks alienating younger children and parents seeking off-screen experiences. Striking the right balance requires nuanced design: for instance, Cava Robata in Dubai introduced AR treasure hunts that require children to physically navigate mazes, blending movement with digital interactivity. This duality demands continuous innovation and consumer insight to preserve the essence of experiential play while embracing modern conveniences.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 10.2% |

| Segments Covered | By Demographics, Facility Size, Revenue Source, Application, Type and Region |

|

Various Analyses Covered | Global, Regional, & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled | Dave & Buster’s, CEC Entertainment, Inc., Cinergy Entertainment, KidZania, Scene 75 Entertainment Centers, The Walt Disney Company, Lucky Strike Entertainment, FunCity, Smaaash Entertainment Pvt. Ltd., LegoLand Discovery Centre, and others. |

SEGMENTAL ANALYSIS

By Demographics Insights

The Families with Children (0–8) segment was the largest and held 54.3% of the Family Entertainment Centers Market share in 2024, with the developmental and safety-centric needs of young children, which FECs are uniquely positioned to meet through age-appropriate attractions. According to the American Academy of Pediatrics, children under eight benefit significantly from structured, sensory-rich environments that promote motor and social development, with 78% of pediatricians recommending supervised group play activities for cognitive growth.

The Teenagers (13–19) segment is expected to register a CAGR of 13.6% during the forecast period, with the increasing socialization needs of adolescents in a post-pandemic context, where peer interaction has regained cultural and psychological significance. As per the Centers for Disease Control and Prevention, 37% of high school students reported persistent feelings of sadness or hopelessness in 2023, prompting parents and educators to encourage supervised social environments. FECs have responded by introducing high-adrenaline attractions such as VR combat zones, escape rooms, and competitive gaming arenas that align with teenage preferences for challenge and autonomy.

By Facility Size Insights

The 20,001 to 40,000 sq. ft. segment was the largest and held 39.2% of the Family Entertainment Centers Market share in 2024. According to the Urban Land Institute, facilities in this category achieve the highest return on investment, with average break-even periods of 2.8 years, compared to 4.5 years for centers exceeding 30 acres. Their footprint allows placement within shopping malls, lifestyle centers, and suburban commercial hubs, maximizing accessibility. Facilities of this scale can function as anchor tenants without requiring standalone land acquisition, reducing development risk.

The 5,001 to 10,000 sq. ft. segment is anticipated to grow with a CAGR of 15.3% during the forecast period, with the rising demand for hyper-local, community-integrated entertainment hubs in densely populated urban areas where large footprints are impractical. In cities like Tokyo, Singapore, and Dubai, land scarcity and high rental costs make compact FECs economically advantageous. As per the World Bank, 56% of the global population lives in urban centers, intensifying competition for space-efficient leisure solutions. These smaller centers specialize in high-turnover, low-dwell-time attractions such as skill games, VR pods, and quick-service dining, catering to time-constrained families and youth groups.

By Application Insights

The physical play activities segment was the largest by capturing 42.3% of the share in 2024, with the foundational role of kinetic engagement in child development and family bonding. Activities such as trampolining, climbing walls, ball pits, and obstacle courses are central to the FEC experience, particularly for children under 12. According to the American Academy of Pediatrics, at least 60 minutes of daily physical activity is essential for healthy childhood development, yet only 24% of children in the U.S. meet this benchmark, as per the CDC’s 2023 Youth Risk Behavior Survey. FECs fill this gap by offering structured, fun-based exercise in a supervised environment.

The AR and VR Gaming Zones segment is likely to register a CAGR of 17.8% in the coming years, with the rising demand for immersive, technologically advanced experiences that appeal to older children, teenagers, and young adults. Virtual reality arcades and augmented reality scavenger hunts offer novel forms of engagement that differentiate FECs from home-based gaming. As per the Entertainment Software Association, 65% of teens prefer playing games in social settings, and VR zones provide a shared, high-impact experience.

By Type Insights

The children's entertainment centers segment dominated the global market revenue with a prominent growth rate. Most schoolchildren visit entertainment centers, which are incorporated with various recreational facilities and games. These engaging activities are expected to develop the children's social skills, ensuring active learning.

Adult entertainment centers are gaining traction due to the growing technological facilities they provide, attracting youth for socialization and entertainment purposes.

REGIONAL ANALYSIS

North America Family Entertainment Centers Market Insights

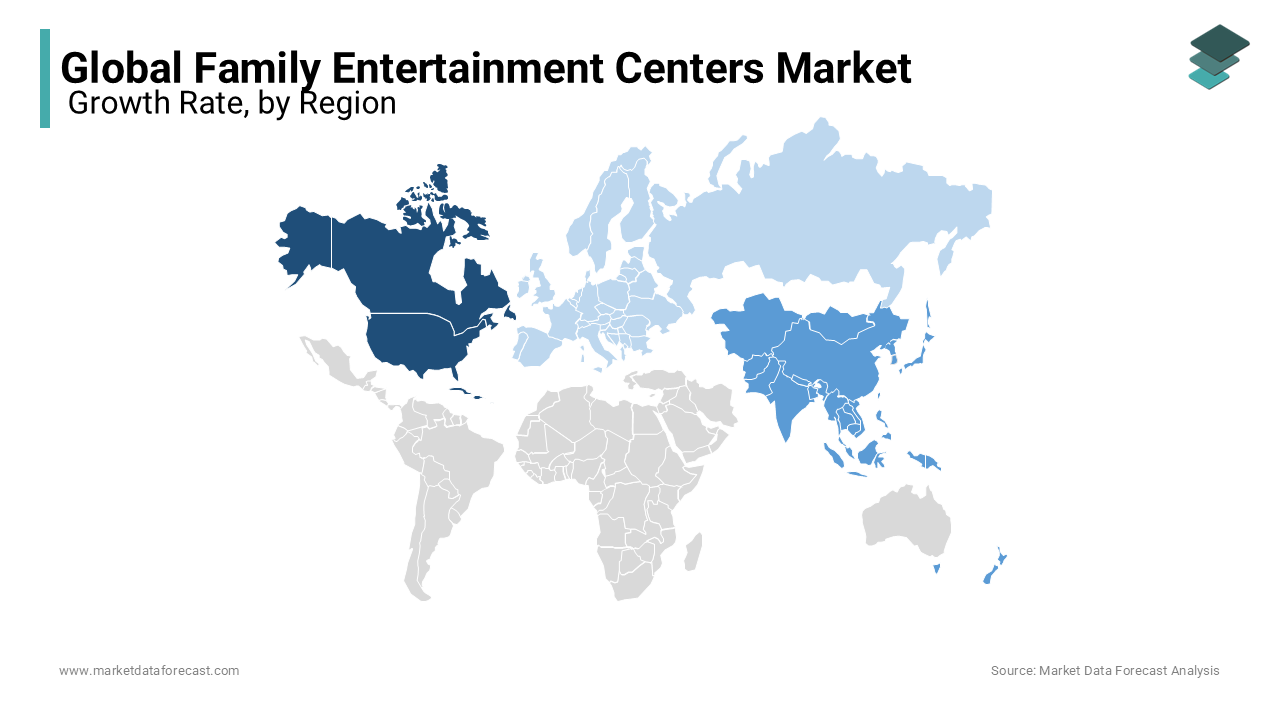

North America was the top performer in the global Family Entertainment Centers Market by holding 41.3% of the share in 2024. According to the U.S. Bureau of Labor Statistics, American households spent $1,020 annually on recreational outings for children in 2023, a 19% increase from 2020. Suburban sprawl and car-centric urban planning have facilitated the development of large-format FECs in commercial corridors.

Europe Family Entertainment Centers Market Insights

Europe was ranked second with 28.3% of the Family Entertainment Centers Market share in 2024. Countries like the UK, Germany, and France have embraced FECs as part of urban regeneration strategies, integrating them into shopping centers and former industrial sites. According to the European Retail Roundtable, over 60% of new lifestyle centers in Western Europe include dedicated FEC zones, enhancing foot traffic and dwell time. In Scandinavia, public-private partnerships have introduced FECs with educational mandates, such as Sweden’s “Lekos” initiative, which combines play with cognitive development tracking.

Asia Pacific Family Entertainment Centers Market Insights

Asia Pacific Family Entertainment Centers Market growth is driven by the rapid urbanization and shifting family dynamics in emerging economies. In China, FECs like Miniso Kids and Happy Monk have proliferated in Tier 1 cities, often integrated into metro-connected malls. Japan’s aging population has paradoxically boosted FEC demand, as grandparents increasingly engage in child-led outings; the Japan Tourism Agency reports that 38% of FEC visitors in Tokyo are accompanied by grandparents. However, land constraints in cities like Mumbai and Manila limit facility size, pushing operators toward compact, high-density models. Digital integration, including facial recognition entry and app-based rewards, is accelerating adoption in tech-savvy markets.

Latin America Family Entertainment Centers Market Insights

Latin America Family Entertainment Centers Market growth is likely to have steady pace in the coming years. Brazil leads the region, with private operators such as Boliche Querido and Hopi Hari expanding FEC offerings in São Paulo and Rio de Janeiro. The Brazilian Institute of Geography and Statistics recorded a 27% increase in family leisure spending between 2020 and 2023, driven by post-pandemic recovery and youth demographics.

Middle East & Africa Family Entertainment Centers Market Insights

Middle East & Africa Family Entertainment Centers Market growth is likely to grow slowly in the coming years. The UAE and Saudi Arabia are investing heavily in entertainment infrastructure as part of economic diversification plans. Under Saudi Vision 2030, over $40 billion has been allocated to leisure and entertainment development, including FECs in NEOM and Riyadh. Dubai’s indoor theme parks, such as IMG Worlds of Adventure, attract over 4 million visitors annually, as reported by Dubai Tourism.

KEY PLAYERS IN THE MARKET

Companies playing a significant role in the global family/indoor entertainment centers market are Dave & Buster's, CEC Entertainment, Inc., Cinergy Entertainment, KidZania, Scene 75 Entertainment Centers, The Walt Disney Company, Lucky Strike Entertainment, FunCity, Smash Entertainment Pvt. Ltd., and LegoLand Discovery Centre.

TOP LEADING PLAYERS IN THE MARKET

Dave & Buster’s

Dave & Buster’s has extended its experiential entertainment model into the Asia Pacific through strategic licensing partnerships and localized adaptations. While direct franchising remains limited, the brand has collaborated with regional operators in Japan and South Korea to introduce compact, urban-format venues integrating its signature “Eat, Drink, Play, Watch” concept. In 2023, the company launched a digital kiosk system tailored for high-traffic Asian malls, enabling self-service game card purchases and table reservations. It also introduced localized menu items such as matcha-infused cocktails and Korean-style sliders to align with regional palates.

KidZania

KidZania has established a significant presence across the Asia Pacific by redefining family entertainment as immersive, role-based learning. With operational centers in Tokyo, Jakarta, and Dubai, the company partners with local institutions to design child-sized cities where children engage in simulated professions from banking to firefighting using regionally relevant career models. In 2022, KidZania Tokyo introduced a sustainability-themed zone in collaboration with Japan’s Ministry of Environment, teaching waste management and energy conservation through interactive play. The company also integrated QR-coded activity passports in 2023, allowing parents to digitally track their child’s developmental progress across visits.

Merlin Entertainments

Merlin Entertainments has its footprint in the Asia Pacific through its LEGOLAND Discovery Centers and SEA LIFE attractions, strategically located within major shopping malls in Singapore, Bangkok, and Shanghai. These compact, indoor venues cater to urban families seeking accessible, weather-independent entertainment. In 2023, Merlin introduced augmented reality scavenger hunts at its Shanghai center, blending physical LEGO builds with digital storytelling to enhance engagement. The company also partnered with local transportation networks to offer bundled tickets, increasing visitation from suburban areas. By leveraging the global appeal of the LEGO brand and implementing data-driven guest analytics, Merlin optimizes staffing, inventory, and promotional timing.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Family Entertainment Centers Market are deploying experiential differentiation, digital integration, strategic real estate placement, brand licensing, and educational alignment to strengthen their competitive positioning. Companies are investing in immersive technologies such as AR, VR, and interactive flooring to enhance engagement. Location strategy focuses on co-anchoring within mixed-use developments and shopping malls to maximize foot traffic. Franchising and IP partnerships with global brands enable rapid scalability and consumer trust. Data analytics and mobile apps are used to personalize experiences and improve retention.

COMPETITION OVERVIEW

The competition in the Family Entertainment Centers Market is intensifying as operators navigate between technological innovation, experiential authenticity, and economic viability. Differentiation increasingly hinges on thematic depth, intergenerational appeal, and seamless digital integration. In the Asia Pacific, competition is further shaped by urban density, cultural preferences for educational play, and rising disposable income. Companies that balance physical engagement with digital enhancement, while maintaining safety and accessibility, are capturing sustained consumer loyalty.

RECENT MARKET DEVELOPMENTS

- In January 2022, Dave & Buster’s launched a localized digital kiosk system in its Tokyo partner venue, enabling self-service game purchases and table bookings by improving operational efficiency and enhancing user experience in high-density urban settings.

- In June 2022, KidZania Tokyo introduced a sustainability-themed educational zone in collaboration with Japan’s Ministry of Environment, which is integrating environmental learning into role-play activities and attracting school group visits.

- In March 2023, Merlin Entertainments implemented augmented reality scavenger hunts at its LEGOLAND Discovery Center in Shanghai by blending physical LEGO models with digital storytelling to increase dwell time and engagement.

- In August 2023, Dave & Buster’s introduced region-specific menu items including matcha cocktails and Korean-style sliders in its Seoul-affiliated venue, which is aligning its culinary offerings with local consumer preferences.

- In November 2023, KidZania rolled out a QR-coded digital activity passport across its Asia Pacific centers by allowing parents to track children’s developmental progress and enhancing the perceived educational value of visits.

MARKET SEGMENTATION

This research report on the global family entertainment centers market has been segmented and sub-segmented based on demographics, facility size, revenue source, application, type and region.

By Demographics

- Families with Children (0-8)

- Families with Children (9-12)

- Teenagers (13-19)

- Young Adults (20-25)

- Adults (Ages 25+)

By Facility Size

- 5,000 sq. ft.

- 5,001 to 10,000 sq. ft.

- 10,001 to 20,000 sq. ft.

- 20,001 to 40,000 sq. ft.

- 1 to 10 acres

- 11 to 30 acres

- over 30 acres

By Revenue Source

- Entry Fees & Ticket Sales

- Food & Beverages

- Merchandising

- Advertisement

- Others

By Application

- Arcade Studios

- AR and VR Gaming Zones

- Physical Play Activities

- Skill/Competition Games

- Others

By Type

- Children’s Entertainment Centers (CECs)

- Children’s Edutainment Centers (CEDCs)

- Adult Entertainment Centers (AECs)

- Location-based VR Entertainment Centers (LBECs)

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What is the current size of the global family entertainment centers (FEC) market?

The global family entertainment centers market is expected to be valued at USD 34.6 billion in 2024.

Which regions contribute the most to the global family entertainment centers market share?

North America, Europe, and Asia-Pacific are among the leading contributors to the global family entertainment centers market share, with a diverse range of offerings catering to varied preferences.

How is the COVID-19 pandemic impacting the global family entertainment centers market?

The COVID-19 pandemic initially led to temporary closures and reduced footfall in family entertainment centers. However, the market is adapting with enhanced safety measures, online booking systems, and a renewed focus on cleanliness.

Who are the key players in the global family entertainment centers market?

Dave & Buster’s, CEC Entertainment, Inc., Cinergy Entertainment, KidZania, Scene 75 Entertainment Centers, The Walt Disney Company, Lucky Strike Entertainment, FunCity, Smaaash Entertainment Pvt. Ltd., and LegoLand Discovery Centre are some of the key players in the global market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com