Global Flooring Market Size, Share, Trends, & Growth Forecast Report Segmented By Product (Ceramic Tiles, Porcelain Tiles, Carpet, Vinyl, Wood & Laminate), Application, and Region (Latin America, North America, Asia Pacific, Europe, Middle East and Africa), Industry Analysis from 2025 to 2033

Global Flooring Market Summary

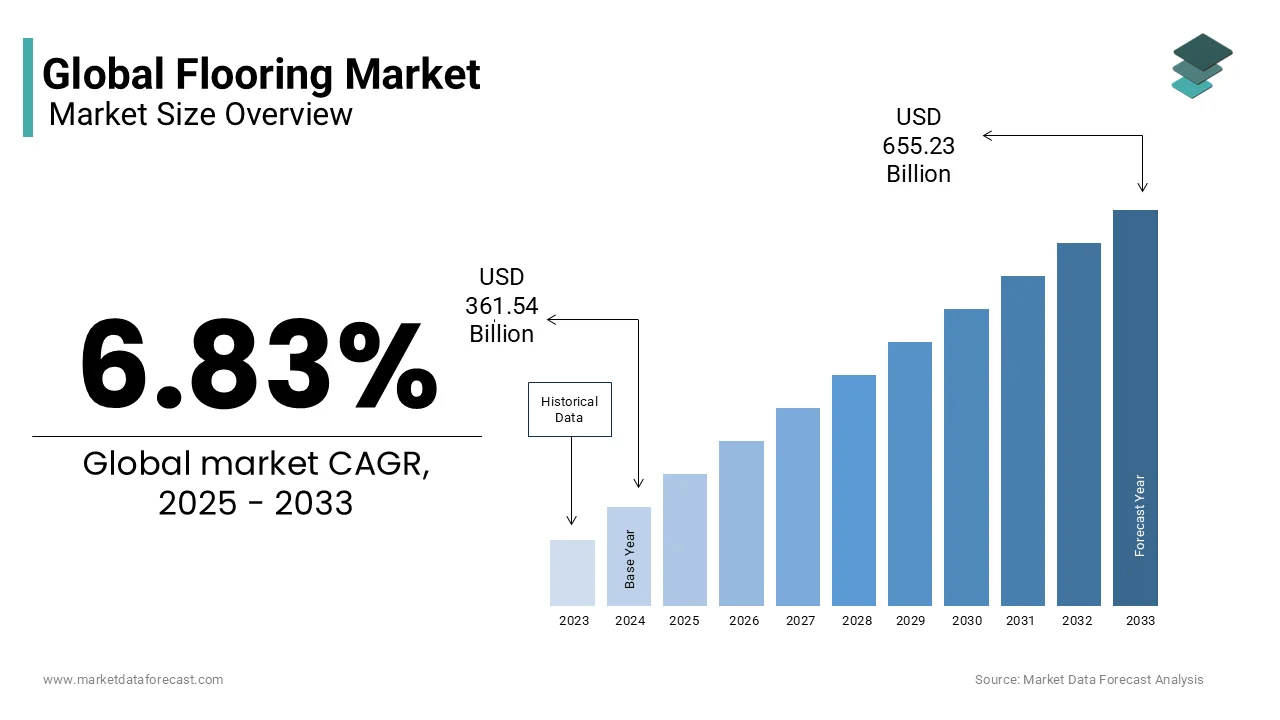

The global flooring market size was valued at USD 361.54 billion in 2024, projected to reach USD 386.23 billion in 2025 and USD 655.23 billion by 2033, expanding at a CAGR of 6.83% from 2025 to 2033. Growth is driven by increasing urbanization, rising demand for modern interior designs, and a surge in construction and renovation activities across residential and commercial sectors. Advancements in sustainable flooring materials and versatile vinyl solutions are further propelling market expansion.

Key Market Trends

- Rising adoption of vinyl flooring due to cost-effectiveness and design versatility

- Growing demand for eco-friendly and sustainable flooring solutions

- Expanding residential construction and renovation projects worldwide

- Technological innovations in flooring manufacturing and installation techniques

Segmental Insights

- Based on product, the vinyl flooring segment dominated the market in 2024 with a 28.3% share, driven by its durability, affordability, and wide usage across both residential and commercial spaces.

- Based on application, the residential segment accounted for the largest share at 58.3% in 2024, supported by strong housing demand and increasing renovation projects worldwide.

Regional Insights

- Asia-Pacific led the global flooring market with a 42.3% share in 2024, fueled by rapid urbanization, infrastructure investments, and high residential construction activity.

- North America is projected to grow steadily, supported by strong renovation demand and the adoption of advanced flooring technologies.

- Europe emphasizes sustainable and eco-friendly flooring solutions, backed by stringent regulations and green construction trends.

- Latin America is emerging as a growing market, supported by rising investments in real estate and infrastructure projects.

- Middle East & Africa are gradually adopting modern flooring solutions, driven by urban development and commercial construction growth.

Competitive Landscape

Leading companies in the global flooring market include Mohawk Industries, Inc., Tarkett S.A., AFI Licensing, Burke Flooring Products, Inc., Firbo Flooring, Shaw Industries, Inc., Interface, Inc., Gerflor, Mannington Mills, Inc., Polyflor, RAK Ceramics, Crossville Inc., Atlas Concorde S.P.A., Porcelanosa Group, and Kajaria Ceramics Limited. These players are focusing on sustainable product innovation, manufacturing capacity expansion, and strategic partnerships to strengthen their market presence.

Global Flooring Market Size

The global flooring market size was valued at USD 361.54 billion in 2024 and is expected to reach USD 655.23 billion by 2033 from USD 386.23 billion in 2025. The market is projected to grow at a CAGR of 6.83%.

The flooring is a broad spectrum of materials and systems designed to cover the structural base of residential, commercial, and industrial buildings by serving both functional and aesthetic purposes. It includes products such as hardwood, laminate, vinyl, tile, and carpet, each tailored to specific performance requirements including durability, moisture resistance, and thermal insulation. As urbanization accelerates and building standards evolve, flooring solutions are increasingly evaluated not only for appearance but also for lifecycle performance and environmental impact. According to the U.S. Census Bureau, over 1.4 million housing units were authorized in the United States in 2023, signaling sustained demand for interior finishes.

MARKET DRIVERS

The surge in residential renovation activities in developed economies where aging housing stock necessitates modernization is driving the growth of flooring market. Homeowners are increasingly investing in interior upgrades to enhance comfort, property value, and energy efficiency. In the United States, the Joint Center for Housing Studies at Harvard University reported that homeowners spent approximately $443 billion on home improvements in 2023, with flooring replacements ranking among the top three renovation categories. This trend is amplified by the growing preference for durable, low-maintenance materials such as luxury vinyl tile (LVT) and engineered wood, which offer cost-effective alternatives to solid hardwood. Moreover, the rise of do-it-yourself (DIY) culture, supported by online tutorials and accessible installation methods, has lowered entry barriers for consumers, further stimulating demand.

The expansion of the commercial construction sector in healthcare, education, and retail infrastructure, where flooring performance directly impacts safety, hygiene, and user experience is additionally to enhance the growth of flooring market. Hospitals and clinics, for instance, require antimicrobial, slip-resistant, and seamless flooring solutions to meet stringent sanitation standards. As per the World Health Organization, global healthcare infrastructure investment exceeded $11 trillion between 2020 and 2023, with a substantial portion allocated to facility upgrades and new constructions. Similarly, the International Council of Shopping Centers noted that over 4,200 shopping malls underwent renovations in 2023, many incorporating resilient flooring like commercial-grade vinyl and rubber to endure high foot traffic. Educational institutions are also prioritizing acoustic and impact-absorbing flooring to improve learning environments.

MARKET RESTRAINTS

The volatility of raw material pfloorings for petroleum-based inputs such as PVC and polyurethane, which are essential for manufacturing vinyl and resilient flooring is hampering the growth of flooring market. Geopolitical disruptions and fluctuating crude oil markets directly influence production costs, limiting profit margins and pricing stability. Additionally, wood-based products face supply constraints due to logging regulations and climate-related forest degradation. The Food and Agriculture Organization of the United Nations stated that global timber supply declined by 5.4% in 2023 compared to the previous year, driven by intensified wildfire seasons and export restrictions in key producing nations.

The growing regulatory scrutiny on volatile organic compound (VOC) emissions and environmental sustainability in flooring production is additionally to hinder the growth of flooring market. Governments worldwide are enforcing stricter indoor air quality standards, compelling manufacturers to reformulate adhesives, coatings, and binders. The European Environment Agency reported that in 2023, 18 EU member states strengthened regulations on formaldehyde emissions from wood-based panels, aligning with the revised Construction Products Regulation. Compliance requires costly investments in low-emission technologies and third-party certifications such as FloorScore and Cradle to Cradle. Additionally, the U.S. Environmental Protection Agency has expanded its Toxic Substances Control Act to include enhanced reporting for phthalates used in vinyl flooring. These regulatory shifts increase operational complexity, especially for small and mid-sized producers lacking the capital for rapid adaptation, thereby constraining market entry and innovation velocity.

MARKET OPPORTUNITIES

The integration of smart flooring technologies, which embed sensors and conductive materials into floor systems to enable motion detection, fall alerts, and energy harvesting is creating new opportunities for the growth of flooring market. These innovations are gaining traction in assisted living facilities and high-end residential buildings. According to the World Health Organization, by 2030, one in six people globally will be over the age of 60, creating a robust demand for age-friendly infrastructure. Companies like Forbo and Tarkett have already introduced pilot projects using conductive linoleum that can monitor resident movement patterns. Additionally, research conducted at the Massachusetts Institute of Technology demonstrated that piezoelectric flooring elements can generate up to 2 watts per square meter under regular foot traffic, offering potential for localized energy recovery in transit hubs and retail spaces.

The rise of circular economy models in flooring, where manufacturers adopt take-back programs, recyclable materials, and modular designs to reduce waste and extend product lifecycles is also to elevate the growth of flooring market. In response, companies such as Interface have achieved 89% recycled content in their carpet tiles and operate a global ReEntry program that reclaimed over 500 metric tons of used flooring in 2023. Similarly, Armstrong Flooring introduced BioBased LVT, which incorporates rapidly renewable materials like limestone and corn-based plasticizers.

MARKET CHALLENGES

The skilled labor shortage in installation and finishing trades, which delays project timelines and increases labor costs is impeding the growth of flooring market. Precision in subfloor preparation, acclimatization, and seamless joining is important, especially for engineered and resilient flooring systems. Similarly, the Federation of Master Builders in the UK reported that 72% of contractors experienced delays due to lack of qualified floor layers in 2023. This scarcity is exacerbated by an aging workforce and limited vocational training pipelines.

The inconsistency in global quality standards and certification frameworks, which complicates international trade and consumer trust is also to restrict the growth of flooring market. While regions like the European Union enforce harmonized standards under CE marking, other markets lack uniform testing protocols for wear resistance, fire safety, and dimensional stability. As per the International Organization for Standardization, over 40% of flooring products seized at EU borders in 2023 failed to meet declared performance claims, indicating widespread mislabeling and substandard imports. Additionally, the absence of universally recognized eco-labels enables greenwashing, undermining genuine sustainability efforts. The Global Construction Review documented that in 2023, 15 major flooring brands were penalized across Asia and North America for misleading environmental claims.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 6.83% |

| Segments Covered | By Product, Application, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Mohawk Industries, Inc., Tarkett, S.A., AFI Licensing, Burke Flooring Products, Inc., Firbo Flooring, Shaw Industries, Inc., Interface, Inc., Gerflor, Mannington Mills, Inc., Polyflor, RAK Ceramics, Crossville Inc., Atlas Concorde S.P.A., Porcelanosa Group, and Kajaria Ceramics Limited., and others |

SEGMENTAL ANALYSIS

By Product Insights

The vinyl flooring segment was accounted in holding 28.3% of the flooring market share in 2024, with confluence of performance, affordability, and design flexibility, particularly in urban and high-moisture environments. A primary driver is its exceptional suitability for multifamily housing and renovation projects, where water resistance and low maintenance are paramount. According to the U.S. Department of Housing and Urban Development, over 52% of new rental apartment constructions in 2023 specified waterproof flooring in kitchens and bathrooms, favoring luxury vinyl tile (LVT) due to its resilience and aesthetic mimicry of natural materials. Additionally, the National Association of Home Builders notes that vinyl flooring adoption in bathroom remodels increased by 18% between 2021 and 2023, outpacing ceramic and laminate alternatives.

The engineered wood segment is likely to grow with an expected CAGR of 8.7% during the forecast period with the shifting consumer preferences toward sustainable, high-end finishes that combine the visual appeal of solid hardwood with enhanced durability and installation versatility. A key driver is the rising demand in premium residential construction, where engineered wood is increasingly specified for its compatibility with underfloor heating systems and resistance to humidity-induced warping. The tightening environmental regulations on deforestation and solid timber harvesting is another factor levelling up the growth of segment. Unlike solid hardwood, which requires large-diameter logs and longer growth cycles, engineered wood optimizes resource use by utilizing fast-growing plantation species and recycled wood fibers.

By Application Insights

The residential application segment was accounted in holding 58.3% of the global flooring market share in 2024 with the scale and continuity of housing activity, especially in urbanizing regions where population growth and household formation drive new construction and renovation. A major contributing factor is the global rise in single-family home ownership and the expansion of the middle class in emerging economies. According to the World Bank, urban populations in Asia and Africa grew by 112 million people in 2023 alone by creating unprecedented demand for housing infrastructure. In India, the Ministry of Housing and Urban Affairs, over 14 million affordable homes were sanctioned under the Pradhan Mantri Awas Yojana by the end of 2023, nearly all of which required full interior flooring packages.

The commercial application segment is the fastest-growing sector in the flooring market, anticipated to grow at a CAGR of 7.9% from 2023 to 2030, outpacing residential and industrial applications. This acceleration is driven by the rapid expansion of service-oriented infrastructure, including healthcare, education, and hospitality, where flooring performance directly influences safety, hygiene, and brand experience. A key catalyst is the global push to modernize healthcare facilities, particularly in aging societies. According to the World Health Organization, 1.2 million new hospital beds were added worldwide between 2021 and 2023, necessitating antimicrobial, slip-resistant, and seamless flooring solutions.

REGIONAL ANALYSIS

Asia Pacific Flooring Market Insights

Asia Pacific was the largest contributor in the flooring market by capturing 42.3% of the share in 2024 with unparalleled pace of urbanization and infrastructure development. China and India serve as the twin engines of this dominance, with massive investments in residential and commercial construction. The Chinese Ministry of Housing and Urban-Rural Development reported that over 1.8 billion square meters of new urban housing was completed in 2023, requiring full flooring installations. Simultaneously, India’s National Building Code revisions in 2023 mandated improved indoor finishes in all new constructions, boosting demand for ceramic and vitrified tiles. Additionally, the region hosts the majority of global flooring manufacturing capacity, with Vietnam and Indonesia emerging as export hubs for engineered wood and vinyl.

North America Flooring Market Insights

North America was positioned second by capturing 23.2% of the global flooring market share in 2024. The U.S. dominates the regional share, with a highly developed distribution network and consumer preference for premium products like hardwood and LVT. According to the U.S. Census Bureau, new residential construction starts reached 1.46 million units in 2023, while the Joint Center for Housing Studies estimated that homeowners spent $443 billion on improvements, a record high. The Environmental Protection Agency’s updated indoor air quality guidelines have also accelerated the shift toward low-VOC and formaldehyde-free products.

Europe Flooring Market Insights

Europe flooring market growth is likely to grow with the strong preference for sustainable, high-performance flooring and a regulatory framework that shapes global standards. The European Union’s Construction Products Regulation (CPR) mandates CE marking and lifecycle assessments, influencing product design far beyond its borders. According to Eurostat, construction output in the EU grew by 3.4% in 2023, with Germany, France, and Poland leading in residential and public infrastructure projects. The region is a pioneer in circular economy practices, with companies like Tarkett and Forbo implementing take-back schemes and bio-based materials.

Latin America Flooring Market Insights

Latin America flooring market growth with Brazil and Mexico emerging as key growth poles amid economic recovery and urban expansion. The Brazilian Institute of Geography and Statistics recorded a 5.2% increase in construction activity in 2023, driven by federal housing programs and private investment in shopping centers and hospitals. Ceramic tiles dominate due to climate suitability and cultural preference, with Argentina and Chile importing over $480 million worth of tiles in 2023, as reported by the United Nations Comtrade database. However, affordability remains a constraint, limiting penetration of premium products. The Inter-American Development Bank noted that 62% of new housing in the region falls under the low-income category, where cost-effective options like sheet vinyl and basic ceramics prevail.

Middle East & Africa Flooring Market Insights

Middle East & Africa flooring market growth is likely to grow with growth concentrated in the Gulf Cooperation Council (GCC) countries and select African economies undergoing infrastructural transformation. The UAE and Saudi Arabia are leading large-scale giga-projects such as NEOM and Expo City Dubai, which require high-specification flooring for hospitality, retail, and mixed-use towers. According to the Gulf Construction Index, capital expenditure on non-oil construction in the GCC reached $280 billion in 2023, with flooring packages accounting for 4–6% of total project costs. In Africa, Nigeria and Kenya are witnessing growth in private real estate development, though informal housing remains dominant.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Mohawk Industries, Inc., Tarkett, S.A., AFI Licensing, Burke Flooring Products, Inc., Firbo Flooring, Shaw Industries, Inc., Interface, Inc., Gerflor, Mannington Mills, Inc., Polyflor, RAK Ceramics, Crossville Inc., Atlas Concorde S.P.A., Porcelanosa Group, and Kajaria Ceramics Limited are the key players in the flooring market.

The competition in the flooring market is intensifying as global manufacturers contend with regional players, evolving consumer preferences, and regulatory pressures. The landscape is characterized by a blend of technological differentiation, sustainability claims, and supply chain resilience as key battlegrounds. Multinational companies leverage brand equity and R&D capabilities to introduce advanced products such as smart and carbon-negative flooring, while regional firms compete on cost and localized customization. Pflooring sensitivity in emerging markets and performance expectations in developed regions create a fragmented yet dynamic environment. Companies are increasingly focusing on total lifecycle value rather than upfront cost, promoting durability, ease of installation, and end-of-life recyclability. This competitive shift is driving innovation but also raising barriers for smaller players lacking the capital for compliance and scalability.

TOP PLAYERS IN THE MARKET

Mohawk Industries

Mohawk Industries is a dominant force in the global flooring landscape, with a significant footprint across the Asia Pacific region. The company has strategically expanded its manufacturing and distribution networks in India, China, and Southeast Asia to meet rising demand for resilient and engineered flooring. Mohawk has localized product development to align with regional preferences, introducing moisture-resistant vinyl and ceramic-look tiles tailored for tropical climates. In 2023, it launched a new R&D center in Shanghai focused on sustainable materials, reinforcing its innovation agenda. The company has also invested in digital showrooms and B2B e-commerce platforms to enhance engagement with contractors and designers. Its acquisition of local distribution partners in Vietnam and Thailand has strengthened supply chain agility, enabling faster delivery and customized solutions for large-scale residential and commercial projects.

Tarkett

Tarkett maintains a strong presence in the Asia Pacific flooring market through its emphasis on sustainable innovation and commercial sector specialization. The company has established manufacturing facilities in India and China, producing vinyl, linoleum, and sports flooring that comply with both EU environmental standards and local building codes. In 2023, it introduced its first carbon-negative vinyl flooring in Australia, leveraging bio-based raw materials and closed-loop recycling. The company also partnered with Singapore’s Building and Construction Authority to promote circular economy practices in public construction. These initiatives underscore Tarkett’s commitment to sustainability while expanding its influence across institutional and green-certified developments in the region.

LG Hausys

LG Hausys (now LG Chem’s Flooring Division) has emerged as a key player in the Asia Pacific flooring market, particularly in the luxury vinyl and sheet flooring segments. Leveraging LG’s brand recognition and technological expertise, the company has introduced advanced SPC and WPC flooring lines with enhanced scratch and water resistance, targeting premium residential and retail spaces in South Korea, Japan, and Southeast Asia. In 2023, LG Hausys opened a new automated production line in Changshu, China, to increase output and reduce lead times. The company has also intensified its digital marketing efforts, collaborating with interior design influencers and launching AR-based visualization tools for consumers. Its flooring products are increasingly specified in smart home developments, aligning with LG’s broader ecosystem of connected home solutions, thereby strengthening its competitive differentiation in high-growth urban markets.

TOP STRATEGIES USED BY THE KEY MARKET PLAYERS

Key players in the flooring market are deploying a mix of vertical integration, sustainability innovation, digital transformation, strategic acquisitions, and regional expansion to consolidate their positions. Companies are investing in backward integration to secure raw material supply and stabilize costs amid pflooring volatility. There is a pronounced shift toward bio-based and recyclable materials to meet tightening environmental regulations and ESG mandates. Digital tools such as augmented reality apps, online configurators, and AI-driven inventory management are being adopted to enhance customer engagement and streamline distribution. Firms are also pursuing mergers and acquisitions to access new technologies and geographic markets. Additionally, partnerships with architects, contractors, and green building councils are being leveraged to influence specification decisions at the design stage by ensuring long-term market penetration and brand loyalty across residential and commercial sectors.

RECENT HAPPENINGS IN THE MARKET

- In April 2024, Mohawk Industries launched a new carbon-neutral vinyl flooring line at its manufacturing plant in Chennai, India, incorporating 100% renewable energy and recycled content with its sustainability in the Asia Pacific region.

- In January 2024, Tarkett partnered with the Singapore Green Building Council to certify 15 of its commercial flooring products under the Green Mark scheme by enhancing its credibility in institutional and public sector projects.

- In September 2023, LG Hausys inaugurated an AI-powered design studio in Seoul, enabling real-time visualization of flooring options in virtual home environments, bridging the gap between digital and physical retail experiences.

- In June 2023, Armstrong Flooring introduced a modular carpet tile system with biophilic patterns in collaboration with global architects at the Milan Design Week, which is targeting premium office spaces in Asia and Europe.

- In February 2024, Forbo expanded its production capacity in Suzhou, China, by 40% to meet rising demand for Marmoleum linoleum in healthcare and education facilities across Southeast Asia.

MARKET SEGMENTATION

This research report on the global flooring market has been segmented and sub-segmented based on product, application, and region.

By Product

- Ceramic Tiles

- Porcelain Tiles

- Carpet

- Vinyl

- Wood & Laminate

By Application

- Residential

- Commercial

- Industrial

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What is the flooring market?

The flooring market refers to the industry that manufactures and sells materials such as tiles, vinyl, carpet, wood, laminate, and other coverings used to finish and protect floors in residential, commercial, and industrial spaces.

2. What are the main types of flooring materials?

The key flooring materials include hardwood, laminate, vinyl, ceramic tiles, natural stone, carpets, and engineered wood.

3. Which sector is the largest end-user of flooring products?

The residential sector holds the largest share due to high demand for home renovation, remodeling, and new housing projects.

4. What factors are driving the growth of the flooring market?

Urbanization, rising disposable incomes, demand for sustainable materials, and growth in the construction industry are major growth drivers.

5. What are the latest trends in the flooring industry?

Popular trends include eco-friendly flooring solutions, luxury vinyl tiles (LVT), digitally printed tiles, and antimicrobial or waterproof flooring.

6. Which region dominates the global flooring market?

Asia-Pacific leads the market, driven by rapid urban development, infrastructure investments, and an expanding middle-class population.

7. What is the fastest-growing region in the flooring market?

North America is witnessing strong growth due to increasing renovation activities, technological advancements, and rising adoption of premium flooring products.

8. What challenges does the flooring market face?

Price volatility of raw materials, environmental concerns, and high installation costs pose significant challenges for market players.

9. Who are the leading companies in the flooring market?

Major players include Mohawk Industries, Tarkett, Shaw Industries, Mannington Mills, Interface, and Gerflor, among others.

10. What is the market outlook for flooring in the next decade?

The flooring market is expected to grow steadily, driven by increased construction, remodeling projects, and innovations in sustainable and smart flooring materials.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com