Global Food Service Market Size, Share, Trends, & Growth Forecast Report - Segmented By Type (Full-Service Restaurants, Quick Service Restaurants, Institutes, Others), Service Type (Commercial, Institutional), And Region (North America, Europe, Asia Pacific, Latin America, Middle East And Africa And Rest Of The Region) – Industry Analysis (2026 To 2034)

Global Food Service Market Summary

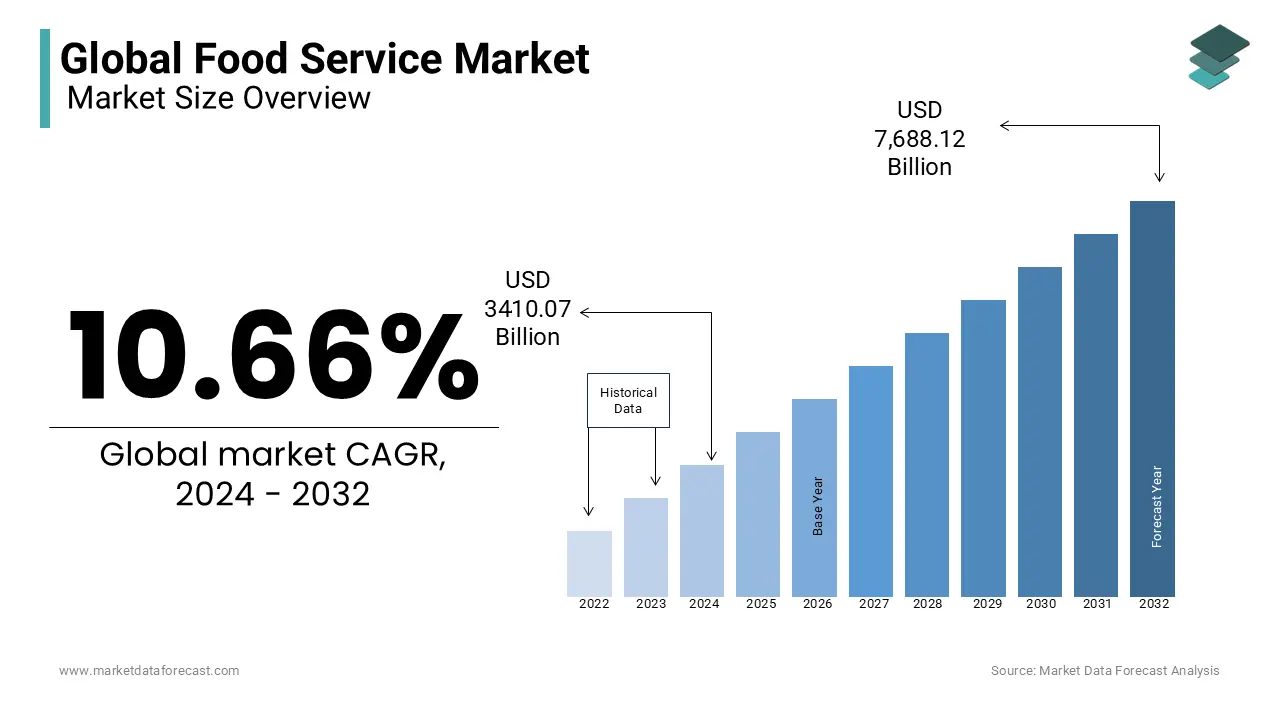

The global food service market size was calculated to be USD 3,773.58 billion in 2025 and is anticipated to be worth USD 9,390.08 billion by 2034 from USD 4,175.84 billion in 2026, growing at a CAGR of 10.66% during the forecast period. Growth is driven by rapid urbanization, rising disposable incomes, evolving consumer lifestyles, and the increasing adoption of digital ordering and delivery platforms.

Key Market Trends & Insights

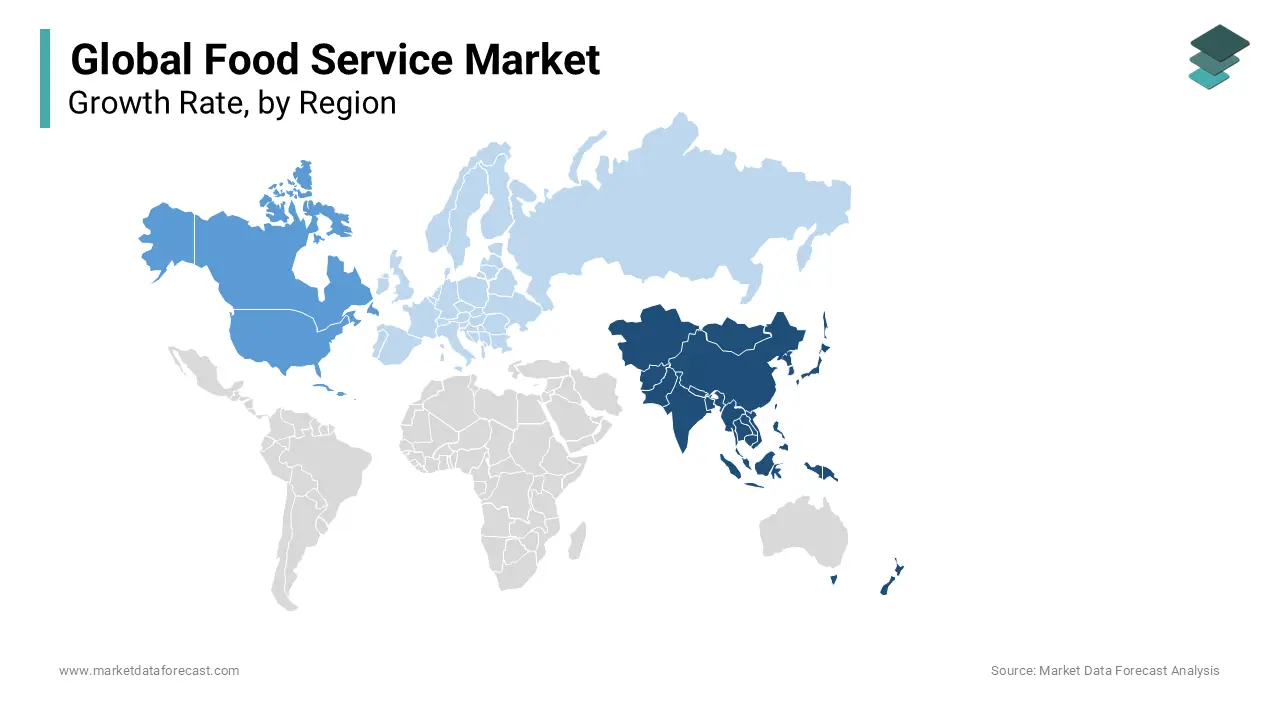

- Asia Pacific: Largest market in 2025, driven by massive population, rapid urbanization, and cultural diversity in dining preferences; China and India lead growth with increasing Western-style dining adoption.

- North America: Strong growth region, with U.S. fast-casual brands leveraging health-conscious trends and Canada excelling in institutional catering.

- Europe: Focus on premiumization, sustainability, and strong institutional presence; plant-based menus gaining traction.

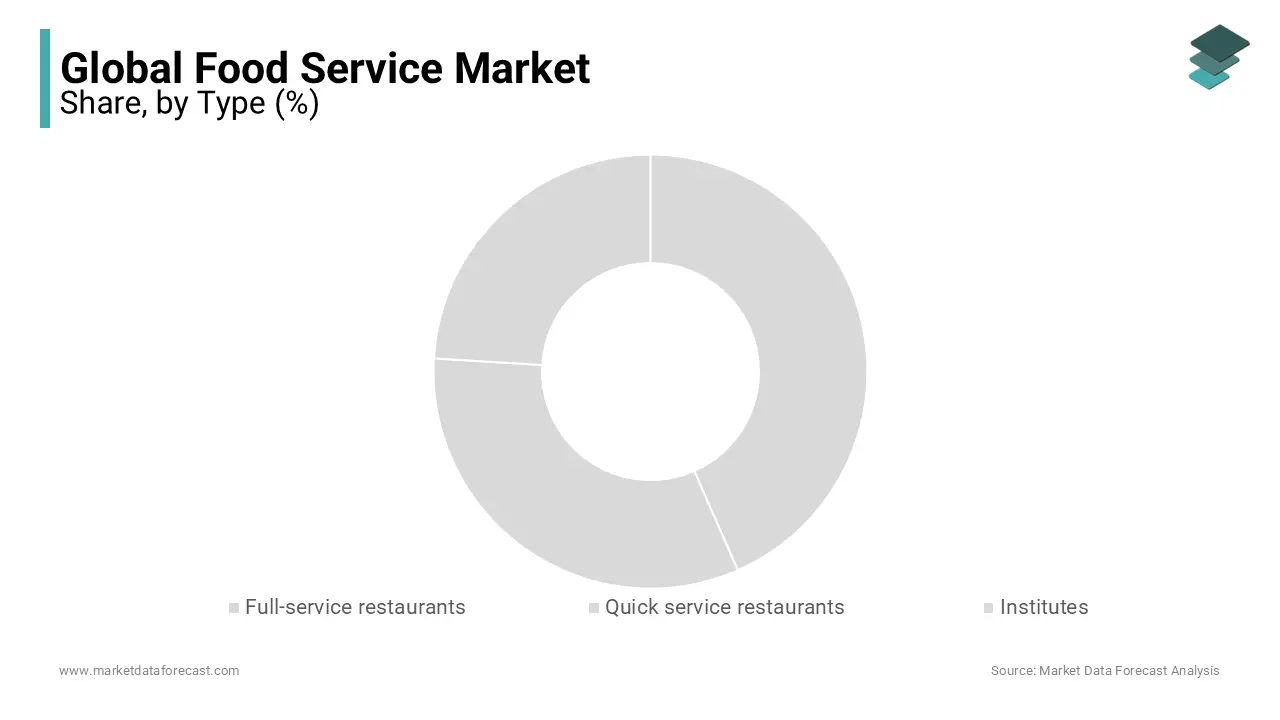

- By Type: Quick Service Restaurants (QSRs) dominated with 43.5% share in 2025, supported by convenience, digital integration, and global franchise scalability.

- Fastest-growing Type: Institutions segment, projected CAGR of 7.8%, driven by infrastructure growth and workplace nutrition programs.

- By Service Type: Commercial segment led with 65.2% share in 2025 due to high dining-out frequency and rapid innovation.

Market Size & Forecast

- 2026 Market Size: USD 4,175.84 Billion

- 2034 Projected Market Size: USD 9,390.08 Billion

- CAGR (2026–2034): 10.66%

- Asia Pacific: Largest market in 2025

- North America: Strong growth region

Global Food Service Market Size

The global food service market size was calculated to be USD 3,773.58 billion in 2025 and is anticipated to be worth USD 9,390.08 billion by 2034 from USD 4,175.84 billion in 2026, growing at a CAGR of 10.66% during the forecast period.

Food Service refers to the establishments and services that prepare and deliver meals and beverages to consumers outside the home environment. This includes full-service and quick-service restaurants, cafés, catering services, food trucks, institutional food providers, and digital food delivery platforms. As urbanization accelerates and lifestyles evolve, the demand for convenient, diverse, and experiential dining options has reshaped the industry’s structure. In the Asia-Pacific region, the food service sector is undergoing rapid transformation driven by shifting consumer behaviors, technological integration, and demographic changes.

The expansion of digital infrastructure has also enabled seamless access to online food platforms, with over 1.3 billion internet users across Asia-Pacific as per the International Telecommunication Union, amplifying the reach and efficiency of food service delivery models. These structural shifts underscore the market’s evolution beyond traditional dining into a dynamic ecosystem integrating technology, convenience, and cultural preferences.

MARKET DRIVERS

Rising Urbanization and Changing Workforce Dynamics

Urbanization across the Asia-Pacific region is fundamentally altering eating habits and increasing dependency on external food sources. As more individuals migrate to metropolitan centers for employment, the time available for meal preparation diminishes, elevating demand for ready-to-eat meals and delivery services. In China alone, over 60% of the population lived in urban areas as of 2023, as per the National Bureau of Statistics of China, with similar trends visible in India and Southeast Asian nations. This shift correlates with a rise in dual-income households, where both partners are employed, reducing domestic cooking time. Furthermore, the expansion of business districts and commercial hubs has led to a proliferation of corporate cafeterias and nearby eateries. These socio-economic transformations are not transient but represent structural changes that continue to fuel demand across both physical and digital food service channels.

Expansion of Digital Food Delivery Platforms and Mobile Penetration

The proliferation of smartphones and high-speed internet has catalyzed the growth of digital food delivery ecosystems, significantly expanding the operational footprint of food service providers. These platforms have not only enhanced consumer convenience but also allowed small and mid-sized restaurants to scale operations without significant physical expansion. Moreover, real-time logistics optimization has reduced delivery times. The financial inclusion driven by digital wallets further supports transaction efficiency. This digital infrastructure has transformed the food service market from a location-dependent industry into a data-driven, on-demand economy, enabling hyperlocal delivery models and personalized customer engagement, thereby amplifying overall market reach and consumption frequency.

MARKET RESTRAINTS

Stringent Food Safety and Regulatory Compliance Requirements

The food service industry in Asia-Pacific faces escalating regulatory scrutiny aimed at ensuring public health and food integrity, which imposes operational and financial burdens on providers. Governments across the region have intensified enforcement of hygiene standards, labeling requirements, and traceability protocols, particularly in response to recurring foodborne illness outbreaks. Compliance with these regulations demands continuous staff training, equipment upgrades, and documentation, disproportionately affecting small and independent operators. Additionally, cross-border supply chain regulations complicate ingredient sourcing. These regulatory complexities increase operational costs and reduce profit margins, particularly for smaller players lacking compliance expertise, thereby constraining market entry and scalability.

Volatility in Food Supply Chains and Ingredient Sourcing

The Asia-Pacific food service sector is highly vulnerable to disruptions in agricultural production and logistics networks, which directly impact ingredient availability and cost stability. Climate change has intensified weather-related shocks, affecting crop yields and livestock production. Additionally, geopolitical tensions and trade restrictions have disrupted supply flows. Labor shortages in farming and transportation sectors further exacerbate delays. These supply chain instabilities force food service operators to frequently revise menus or absorb cost increases, undermining pricing strategies and customer retention.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence and Automation in Kitchen Operations

The adoption of artificial intelligence (AI) and automation technologies presents a transformative opportunity for the Asia-Pacific food service market to enhance efficiency, consistency, and scalability. AI-powered systems are increasingly deployed for demand forecasting, inventory management, and personalized marketing, reducing waste and improving customer engagement. AI-driven analytics also enable dynamic pricing and menu optimization. Additionally, voice-enabled ordering kiosks and AI chatbots are being integrated into quick-service restaurants across China. These innovations not only lower operational costs but also allow human staff to focus on customer experience, thereby elevating service quality. With government support for Industry 4.0 initiatives in countries like Malaysia and Vietnam, the scalability of AI integration is poised to redefine kitchen economics across the region.

Growing Demand for Health-Conscious and Functional Food Offerings

A rising awareness of nutrition and wellness is driving consumer preference for healthier, functional, and transparently sourced food options within the food service sector. As lifestyle diseases such as diabetes and hypertension increase, diners are actively seeking meals with reduced sugar, salt, and fat content, as well as fortified ingredients. In addition, food service providers are reformulating menus to include plant-based proteins, whole grains, and organic ingredients. Fast-casual chains have introduced low-sugar smoothies and allergen-free meals, experiencing year-on-year growth in sales. Additionally, menu labeling laws in cities like Hong Kong and Taipei require calorie disclosure, pushing operators to innovate. This trend enables differentiation and premium pricing, offering food service brands a strategic avenue for growth amid increasing health consciousness.

MARKET CHALLENGES

Escalating Labor Costs and Workforce Shortages

The food service industry across Asia-Pacific is grappling with a persistent shortage of skilled labor and rising wage pressures, undermining operational sustainability. As minimum wage policies tighten and competition for service workers intensifies, restaurants face mounting financial strain. Training and retention have become critical challenges. The situation is further complicated by the physically demanding nature of the job and limited career progression, deterring long-term engagement. These labor dynamics compel operators to invest in automation or reduce operating hours, ultimately constraining growth and service availability.

Environmental Sustainability and Waste Management Pressures

Food service operators in Asia-Pacific are under increasing pressure to adopt sustainable practices due to environmental regulations, consumer expectations, and resource scarcity. The sector generates significant waste, particularly single-use plastics and food scraps, contributing to pollution and landfill overload. Governments are responding with stringent policies. Additionally, consumer sentiment is shifting. However, transitioning to sustainable models involves high upfront costs. Moreover, lack of infrastructure for composting and recycling limits effective waste diversion. These challenges force operators to balance environmental responsibility with economic viability, complicating long-term planning and investment strategies.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 10.66% |

| Segments Covered | By Type, Service Type, And Region. |

| Various Analyses Covered | Global, Regional and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Aramark Corporation, Compass Group North America, Doctor’s Associates Inc., Domino’s, Restaurant Brands International, Seven & I Holdings Co. Ltd, Sodexo, Starbucks Corporation, Yum! Brands Inc. |

SEGMENTAL ANALYSIS

By Type Insights

The Quick Service Restaurants (QSRs) segment dominated the global food service market, capturing an estimated 43.5% share in 2025. The widespread appeal of QSRs is due to their alignment with fast-paced urban lifestyles, where speed, affordability, and consistency are paramount. This dominance is primarily driven by two interrelated factors: evolving consumer behavior and the scalability of standardized operations. The first driver is the growing preference for convenience-oriented dining, particularly among younger demographics and working professionals. This behavioral shift is mirrored across Asia-Pacific. The predictability of menu offerings and minimal waiting times make QSRs a default choice for time-constrained consumers. Additionally, the integration of digital kiosks and mobile ordering has reduced service latency. This seamless operational model fosters repeat patronage and brand loyalty, reinforcing market growth. A further driver is the global expansion and franchise efficiency of major QSR chains. The franchise model allows rapid market penetration with lower capital risk, enabling localized adaptation while maintaining global brand standards. This scalability, combined with aggressive marketing and value-menu strategies, ensures sustained consumer engagement and revenue resilience, solidifying QSRs as the most dominant segment.

By Service Type Insights

The Commercial segment held the largest share of the food service market at 65.2% of total revenue in 2025. This preeminence is anchored in the vast network of profit-driven dining establishments that cater to discretionary consumer spending, including restaurants, cafes, bars, and delivery-only kitchens. One fundamental driver is the rising disposable income and consumption upgrade trend in middle-income populations. This financial flexibility has translated into higher dining-out frequency. The commercial segment benefits from its ability to innovate rapidly, introducing limited-time offers, themed experiences, and celebrity collaborations that stimulate impulse purchases and social media engagement. A further pivotal factor is the digital transformation of commercial food service. This agility allows commercial operators to test new concepts, target niche markets, and scale rapidly, reinforcing their dominance in the broader food service ecosystem.

The Institutional service type is experiencing the fastest growth and is projected to expand at a CAGR of 7.4% in the coming years. This surge is driven by structural reforms in public welfare and the professionalization of outsourced food management. A primary catalyst is the strengthening of government-led nutrition programs, especially in low- and middle-income countries. Additionally, aging demographics in developed nations are expanding demand for elderly care nutrition services. The institutional frameworks provide long-term revenue visibility, attracting major players like Compass Group and Sodexo to invest heavily in specialized kitchen infrastructure and dietitian staffing, thereby accelerating market growth.

REGIONAL ANALYSIS

Asia Pacific

Asia Pacific (APAC) stood as the undisputed leader in the global food service market by commanding a 40.5% share in 2025. The region’s dominance is rooted in its massive population base, rapid urbanization, and cultural affinity for diverse culinary experiences. China and India alone account for a large number of people, with urban residents increasingly adopting Western-style dining habits. India’s market is expanding annually, fueled by rising youth consumption and digital penetration. The region also leads in innovation. Government support for food safety modernization and foreign investment in restaurant chains further strengthens the ecosystem, positioning APAC as both the largest and most dynamic market.

North America

North America holds a significant market share, with the United States serving as the cornerstone of commercial food service activity. Fast-casual brands like Chipotle and Sweetgreen have capitalized on health-conscious trends. Canada contributes significantly through institutional catering, particularly in healthcare and education. The region’s robust logistics infrastructure and high credit card penetration enable seamless operations. Additionally, labor automation in drive-thrus and kitchens is advancing faster here than in other regions.

Europe

Europe accounts for a notable share of the global food service market, with Western European nations leading in premiumization and sustainability. The United Kingdom’s food service sector generated major revenue in 2023, despite post-pandemic challenges, according to UKHospitality. France emphasizes culinary heritage, with Michelin-starred establishments and bistros contributing to a strong full-service restaurant culture. Germany’s institutional segment is highly developed. Additionally, plant-based menus have gained traction.

Latin America

Latin America holds a notable share of the global market, with Brazil and Mexico driving regional growth. Brazil’s food service revenue increased in recent years, according to the Brazilian Association of Franchising, supported by a vibrant street food culture and expanding mall-based dining. Mexico’s QSR sector grew in 2023, with international chains like Domino’s and Starbucks accelerating store rollouts. The region faces challenges in supply chain consistency, but digital adoption is rising. Additionally, government initiatives in Chile and Peru to formalize street vendors have improved hygiene standards and expanded tax compliance, creating a more structured market environment.

Middle East and Africa

Middle East and Africa (MEA) collectively represent small share of the global food service market, with the Gulf Cooperation Council (GCC) countries leading in commercial development. Saudi Arabia’s Vision 2030 initiative has spurred investments in hospitality. In South Africa with urban consumers dining out at least once a week. However, economic volatility in nations like Nigeria and Egypt limits purchasing power, though mobile money platforms like M-Pesa in Kenya are improving transaction accessibility, enabling informal vendors to scale operations.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Key players in the global food service market are Aramark Corporation, Compass Group North America, Doctor’s Associates Inc., Domino’s, Restaurant Brands International, Seven & I Holdings Co. Ltd, Sodexo, Starbucks Corporation and Yum! Brands Inc. are some of the major players in the global food service market.

Competition in the food service market is intensifying as global chains, regional players, and digital-native brands vie for consumer attention across diverse geographies. The landscape is marked by strategic differentiation, where legacy operators leverage scale and brand equity while agile startups exploit niche segments such as health-focused meals, plant-based cuisine, and hyperlocal delivery. In Asia-Pacific, competition is particularly fierce due to fragmented consumer preferences, rapid urbanization, and high digital adoption. International giants like McDonald’s and Starbucks face strong challenges from homegrown brands such as Jollibee and Ajinomoto Foods, which enjoy cultural affinity and pricing advantages. The rise of third-party delivery platforms has lowered entry barriers, enabling virtual brands to operate without physical storefronts, increasing market saturation. Institutional catering is dominated by specialized providers like Compass Group and Sodexo, who compete on operational efficiency and compliance expertise. Price wars, menu innovation, and loyalty programs are common tactics. At the same time, sustainability and transparency are becoming competitive differentiators, with consumers favoring brands that demonstrate ethical sourcing and environmental responsibility. The integration of AI and automation is reshaping service delivery, giving technologically advanced players an edge in speed and cost management. As consumer expectations evolve toward personalization and convenience, continuous innovation and adaptive business models are essential for maintaining relevance in this dynamic, high-turnover industry.

TOP PLAYERS IN THE MARKET

Jollibee Foods Corporation

Headquartered in the Philippines, Jollibee has emerged as a dominant force in the Asia-Pacific food service landscape by leveraging its deep cultural understanding and localization strategy. The company operates over 6,000 stores globally, with more than 80% located across Southeast Asia. Jollibee emphasizes menu innovation tailored to regional palates, such as its famous sweet-style spaghetti and chickenjoy, which resonate strongly with local consumers. In 2023, the company expanded into India and Nepal, opening cloud kitchens and delivery-dedicated outlets to tap into urban demand. It also invested in digital infrastructure, launching AI-driven loyalty programs and integrating with regional delivery platforms like Grab and Zomato. Jollibee strengthened its supply chain by establishing centralized production hubs in Vietnam and Indonesia to ensure consistency and reduce costs. Its acquisition of Tim Ho Wan in 2022 allowed entry into the premium dim sum segment, broadening its portfolio. By focusing on affordability, speed, and emotional branding, Jollibee continues to outmaneuver global giants in home markets while expanding its transnational footprint.

Compass Group PLC

Compass Group, a UK-based contract foodservice provider, maintains a substantial presence across Asia-Pacific through large-scale institutional catering operations. The company serves millions of meals daily in corporate offices, hospitals, schools, and government facilities across Australia, Japan, India, and Singapore. Compass has prioritized sustainability and digital transformation, launching its "Net Zero by 2030" initiative, which includes reducing food waste by 50% and sourcing 100% sustainable proteins in key markets. In 2023, it partnered with Singapore’s Ministry of Health to manage food services in 15 public hospitals, enhancing its institutional credibility. The company introduced AI-powered menu planning tools in Australia to optimize nutrition and reduce waste, improving client retention. Compass also invested in local sourcing, contracting with smallholder farmers in Thailand and Vietnam to ensure fresh supply and support community development. Its recent collaboration with Nanyang Technological University in Singapore to pilot robot-assisted meal delivery in campus cafeterias highlights its focus on innovation. With a strong emphasis on operational efficiency and ESG compliance, Compass continues to secure long-term contracts across the region’s public and private sectors.

Yum China Holdings, Inc.

Yum China, operator of KFC, Pizza Hut, and Taco Bell in mainland China, plays a pivotal role in shaping the country’s commercial food service sector. The company manages over 13,000 restaurants, making it one of the largest restaurant operators in Asia. KFC alone accounts for more than 9,000 outlets, strategically located in tier-1 to tier-3 cities, ensuring wide accessibility. In 2023, Yum China accelerated digital adoption by integrating its loyalty app with Alipay and WeChat Pay, reaching over 400 million registered users. It launched over 700 new stores, with a focus on lower-tier cities and delivery-only formats. The company also invested in automation, deploying robotic fryers and AI-driven inventory systems in Shanghai and Guangzhou. Yum China introduced localized menus, including congee and mooncakes, to align with consumer preferences. Sustainability efforts include eliminating single-use plastics in 80% of outlets and launching electric delivery fleets in Beijing and Hangzhou. These initiatives reinforce its market leadership and responsiveness to evolving urban consumer demands.

TOP STRATEGIES USED BY THE KEY MARKET PLAYERS

Key players in the food service market deploy a range of strategic initiatives to maintain competitive advantage and expand their footprint. Franchising remains a dominant model, enabling rapid geographic expansion with reduced capital risk, particularly in emerging markets. Companies increasingly adopt digital transformation, integrating mobile apps, AI-driven analytics, and contactless payment systems to enhance customer experience and operational efficiency. Strategic mergers and acquisitions allow firms to diversify offerings and enter new segments, such as health-focused or premium dining. Localization of menus and marketing campaigns ensures cultural relevance and strengthens brand loyalty. Investment in cloud kitchens and dark stores optimizes delivery economics in urban centers. Sustainability initiatives, including waste reduction, eco-friendly packaging, and ethical sourcing, are now core to brand positioning. Workforce upskilling and automation help mitigate labor shortages and improve service consistency. Additionally, public-private partnerships in institutional catering secure long-term revenue streams. These strategies collectively enable market leaders to adapt to dynamic consumer behaviors, regulatory environments, and technological advancements across regions.

RECENT HAPPENINGS IN THE MARKET

- In January 2023, Jollibee Foods Corporation launched a dedicated cloud kitchen network in partnership with Swiggy in India, enabling faster delivery and reduced operational costs to penetrate urban markets efficiently.

- In May 2023, Compass Group PLC partnered with Singapore’s Ministry of Health to manage food services across 15 public hospitals, enhancing its institutional footprint and demonstrating compliance with stringent healthcare nutrition standards.

- In September 2023, Yum China introduced AI-powered inventory management systems in 2,000 KFC outlets across Guangdong and Zhejiang provinces, reducing food waste by 18% and improving supply chain responsiveness.

- In February 2025, McDonald’s Australia rolled out fully automated drive-thru ordering using voice recognition technology developed by Artificial Solutions, increasing order accuracy and service speed during peak hours.

- In June 2025, Domino’s Pizza Group opened a new AI-driven pizza production center in Tokyo, integrating robotic assembly lines and predictive demand analytics to optimize freshness and delivery timelines in high-density urban areas.

MARKET SEGMENTATION

This research report on the global food service market has been segmented and sub-segmented based on type, service type, and region.

By Type

- Full-service restaurants

- Quick service restaurants

- Institutes

- Others

By Service Type

- Commercial

- Institutional

By Region

- Asia Pacific

- Middle East and Africa

- Latin America

- Europe

- North America

Frequently Asked Questions

1. What is the food service market?

The food service market includes businesses that prepare, serve, and sell food and beverages for consumption outside the home.

2. Which factors are driving the food service market growth?

Urbanization, changing lifestyles, tourism growth, and increasing demand for convenient dining.

3. What are the main types of food service outlets?

Quick-service restaurants, full-service restaurants, cafes, catering services, and food trucks.

4. Which regions dominate the global food service market?

North America, Europe, and Asia-Pacific lead in market share.

5. Who are the major players in the food service industry?

McDonald’s, Yum! Brands, Starbucks, Subway, and Compass Group are key players.

6. What consumer trends are shaping the food service market?

Health-conscious menus, plant-based options, and digital ordering platforms.

7. How is technology impacting the food service industry?

Mobile apps, AI-driven recommendations, online ordering, and contactless payments are transforming operations.

8. What role does delivery play in the food service market?

Delivery services are expanding rapidly through third-party apps and in-house systems.

9. What challenges does the food service market face?

Labor shortages, rising food costs, and regulatory compliance issues.

10. How is the demand for plant-based food impacting the industry?

Restaurants are adding more vegan and vegetarian dishes to meet consumer demand.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com