Global ePharmacy Market Size, Share, Trends & Growth Forecast Report By Drug Type (Prescription Drugs & Over the Counter Drugs), Product Type and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa) – Industry Analysis, 2025 to 2033

Global ePharmacy Market Summary

The global ePharmacy Market was valued at USD 82.34 billion in 2024 and is projected to reach USD 298.74 billion by 2033, growing at a strong CAGR of 15.2% during the forecast period.

Key Market Trends

- Rising adoption of digital healthcare platforms and online medicine delivery

- Growth in OTC drug sales via ePharmacy platforms

- Increasing demand for vitamins, supplements, and wellness products through online channels

- Partnerships and acquisitions among retail giants and ePharmacy platforms to strengthen digital healthcare ecosystems

Segmental Insights

- Based on drug type, the Over-the-Counter (OTC) medications segment dominated the market with a 58.4% share in 2024, driven by increasing consumer reliance on ePharmacies for quick access to pain relievers, cold medicines, and basic healthcare products.

- Based on product type, the vitamins segment accounted for 28.3% of the global share in 2024, supported by rising consumer awareness about preventive healthcare and the convenience of online vitamin subscription models.

Regional Insights

- North America led the global ePharmacy market with a 42.3% share in 2024, driven by strong adoption in the U.S. and Canada, robust logistics networks, and widespread insurance integration.

- Europe recorded a substantial share, supported by regulatory support for online medicine distribution and the presence of well-established retail pharmacy chains moving into digital.

- Asia-Pacific is the fastest-growing region, expected to expand at a double-digit CAGR during 2024–2033, fueled by digital adoption in India, China, and Southeast Asia.

- Latin America is experiencing steady growth, particularly in Brazil and Mexico, where regulatory frameworks for ePharmacies are evolving.

- Middle East & Africa is witnessing moderate growth, with expansion driven by increasing investments in healthcare digitalization and online pharmacy platforms.

Competitive Landscape

The global ePharmacy market is moderately consolidated, with leading players focusing on digital infrastructure, strategic alliances, and enhanced supply chain capabilities to strengthen their market positions. Notable companies include CVS Health, Walmart Stores, Inc., Walgreen Co., The Kroger Co., Rite Aid Corp, Lloyds Pharmacy Ltd., Planter, Canada Drugs, Medicate, Express Scripts Holding Company, Secure Medical Inc., Sani Care A.B., Doctors Rowlands Pharmacy, Giant Eagle, Inc., and Optus Rx, Inc.

Global ePharmacy Market Size

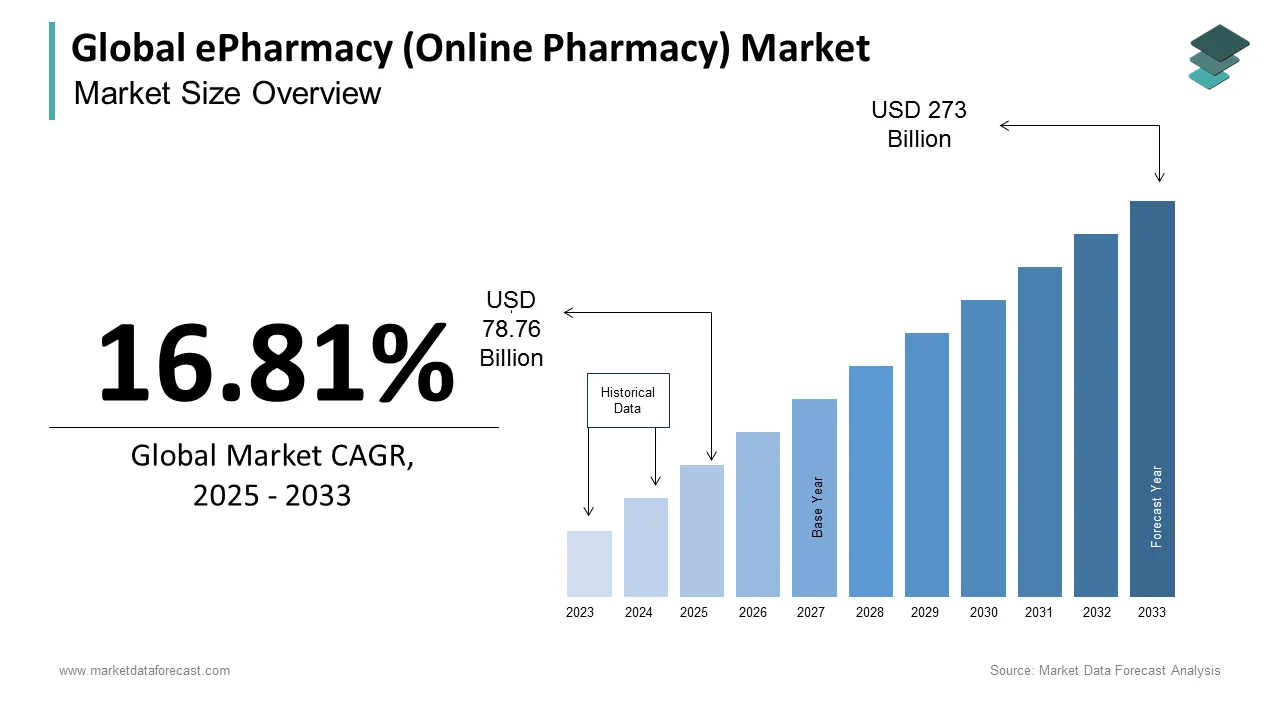

The global ePharmacy market (also known as the online pharmacy market) was valued at USD 67.43 billion in 2024. The global market is anticipated to grow at a CAGR of 16.81% from 2025 to 2033, reaching a value of USD 273 billion by 2033, up from USD 78.76 billion in 2025.

ePharmacy or Online Pharmacy is a digital ecosystem enabling the online procurement, dispensing, and delivery of pharmaceuticals, over-the-counter medications, and wellness products through regulated and licensed platforms. This model has evolved beyond mere transactional convenience to become a node in the broader digital health infrastructure, interfacing with telemedicine, electronic health records, and insurance verification systems. The proliferation of smartphones and high-speed internet has catalyzed this transformation in densely populated urban centers, where time efficiency and access barriers are acute. Regulatory frameworks are also adapting; countries like India and Singapore have introduced national digital health missions that formally recognize e-prescriptions and licensed online pharmacies. The integration of artificial intelligence for personalized health recommendations and automated refill reminders further distinguishes modern ePharmacy platforms.

MARKET DRIVERS

Rising Burden of Chronic Diseases and Long-Term Medication Dependency

The escalating prevalence of chronic diseases is propelling the expansion of the ePharmacy market. Conditions such as diabetes, hypertension, cardiovascular disorders, and respiratory ailments require continuous medication regimens, making patient adherence and supply chain reliability crucial. According to the World Health Organization, non-communicable diseases account for 74% of all deaths globally, with a significant proportion necessitating daily pharmaceutical intake. The convenience of automated prescription renewals, home delivery, and digital tracking significantly reduces treatment discontinuation. Furthermore, ePharmacies enable better inventory management for chronic care products, minimizing stockouts. In aging societies like Japan, where 29% of the population is over 65, the demand for remote medication access is intensifying.

Integration with Telemedicine and Digital Health Ecosystems

The integration of ePharmacy platforms with telemedicine services has redefined patient engagement by creating a seamless continuum from diagnosis to treatment delivery, which is propelling the growth of the ePharmacy market. As virtual consultations become mainstream, the ability to instantly transmit e-prescriptions to licensed online pharmacies eliminates delays in medication access. According to the American Medical Association, over 60% of U.S. healthcare providers now offer telehealth services, many of which are directly linked to pharmacy networks for immediate fulfillment. This integration is particularly transformative in rural and underserved areas where physical healthcare infrastructure is limited. Platforms like Tata 1mg and Apollo 24|7 have reported that over 60% of their e-prescription orders originate from teleconsultations, illustrating the symbiotic relationship between virtual care and online pharmacies. Additionally, AI-driven health apps now offer medication reminders, side-effect tracking, and dosage adjustments, further enhancing treatment outcomes.

MARKET RESTRAINTS

Regulatory Fragmentation and Legal Ambiguity Across Jurisdictions

The lack of harmonized regulatory frameworks governing online pharmaceutical sales is hampering the growth of the ePharmacy market. While some countries have established clear licensing and operational guidelines, others maintain restrictive or ambiguous policies that hinder cross-border scalability and investor confidence. According to the World Health Organization, over 60% of low- and middle-income countries lack comprehensive regulations for ePharmacies by creating legal gray zones that expose consumers to counterfeit or substandard medications. The U.S. Food and Drug Administration permits interstate pharmacy operations only if individual state boards of pharmacy grant approval, resulting in a complex compliance landscape. This fragmentation discourages platform standardization and increases operational costs. Furthermore, the absence of universal digital prescription standards complicates interoperability between healthcare providers and ePharmacies.

Persistent Concerns Over Medication Authenticity and Cybersecurity Risks

The authenticity of medications purchased online in regions with high incidences of counterfeit drugs is also restricting the growth of the ePharmacy market. The World Health Organization estimates that 1 in 10 medical products in low- and middle-income countries is either falsified or substandard, and online channels are increasingly exploited for illicit distribution. A 2023 investigation by Interpol’s Operation Pangea revealed the takedown of over 120,000 websites selling counterfeit medicines, many masquerading as legitimate ePharmacies. These operations often lack proper storage conditions, leading to compromised drug efficacy and patient harm. In India, the Central Drugs Standard Control Organization identified over 8,000 unlicensed online drug sellers in 2022, prompting nationwide enforcement drives.

MARKET OPPORTUNITIES

Expansion of Government-Backed Digital Health Infrastructure

The rollout of national digital health initiatives for ePharmacies to integrate into formal healthcare systems and achieve scalable legitimacy is ascribed to bolster the growth of the ePharmacy market. Governments worldwide are investing in unified health data networks that enable secure e-prescriptions, patient identity verification, and interoperable pharmacy linkages. As per the World Bank, over 120 countries now have active digital health strategies, with India’s Ayushman Bharat Digital Mission creating a unique health ID for over 500 million citizens, facilitating seamless medication access through verified ePharmacy partners. Similarly, Singapore’s National Electronic Health Record system allows authorized pharmacies to retrieve prescriptions electronically, reducing administrative friction. In Estonia, a pioneer in e-governance, 99% of health data is digitized, and e-prescriptions account for over 90% of all prescriptions issued, demonstrating the potential of state-led digitization.

Adoption of AI and Predictive Analytics for Personalized Medication Management

The integration of artificial intelligence into ePharmacy platforms in personalized healthcare by transforming these services from transactional outlets into proactive health management tools is solely to enhance the growth of the ePharmacy market. AI algorithms can analyze patient histories, prescription patterns, and lifestyle data to anticipate medication needs, detect potential drug interactions, and recommend preventive supplements. According to the MIT Technology Review, healthcare AI applications are projected to reduce medication errors by up to 50% through real-time clinical decision support. Companies like Medly and Capsule in the U.S. employ machine learning to optimize delivery routes and predict refill timings, enhancing service reliability. The UK’s National Health Service piloted an AI-powered pharmacy assistant in 2023 that reduced missed doses by 27% among elderly patients. Additionally, natural language processing enables platforms to interpret unstructured doctors notes and convert them into digital prescriptions.

MARKET CHALLENGES

Last-Mile Delivery Limitations in Rural and Remote Areas

The last-mile delivery in geographically dispersed or underdeveloped regions also inhibits the growth of the ePharmacy market. In many parts of Africa, Southeast Asia, and Latin America, poor road infrastructure, extreme weather, and fragmented address systems impede reliable medication delivery. According to the World Bank, over 1.4 billion people globally live in areas with inadequate transport networks, limiting the reach of even well-funded ePharmacy ventures. In rural India, where 66% of the population resides, the lack of standardized delivery pin codes and cold-chain facilities for temperature-sensitive drugs like insulin hampers service consistency.

Intensifying Competition from Unregulated and Informal Market Players

The unregulated vendors and informal digital sellers who operate outside legal frameworks by offering lower prices also to hinder the growth of the ePharmacy market. These entities, often hosted on social media platforms or unlicensed e-commerce sites, bypass licensing requirements, tax obligations, and quality control standards. According to the Alliance for Safe Online Pharmacies, over 95% of websites selling prescription drugs operate illegally, with minimal verification of medical legitimacy. In Indonesia, the Ministry of Health identified more than 10,000 Facebook and WhatsApp-based drug sellers in 2023, many offering prescription medications without valid prescriptions. These informal channels exploit regulatory gaps and consumer price sensitivity, particularly in markets where out-of-pocket healthcare spending is high. Legitimate ePharmacies, burdened by compliance costs, struggle to compete on pricing, forcing them to differentiate through trust and service quality. However, brand-building requires time and investment, creating a disadvantage against agile, low-cost operators.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Drug Type, Product Type, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Market Leaders Profiled | CVS Health, Walmart Stores, Inc., Walgreens Co., The Kroger Co., Rite Aid Corp, Lloyds Pharmacy Ltd., Planter, Canada Drugs, Medicate, Express Scripts Holding Company, Secure Medical Inc., Sani care A.B., Doctors Rowlands Pharmacy, Giant Eagle, Inc., and Optus Rx, Inc. |

SEGMENTAL ANALYSIS

By Drug Type Insights

The Over-the-counter (OTC) medications segment was the largest by capturing 58.4% of the ePharmacy market share in 2024, with the inherent convenience and autonomy OTC products offer that consumers can self-diagnose and purchase treatments for common ailments without requiring a prescription. Categories such as pain relievers, antihistamines, digestive aids, and cold remedies are frequently bought online due to their non-restricted nature and recurring usage patterns. Additionally, ePharmacies enhance accessibility through subscription models and bulk purchasing options. A 2023 McKinsey survey found that 34% of OTC buyers prefer online platforms for their ability to stock up on essentials like ibuprofen and allergy medication, avoiding frequent store visits.

The prescription drugs segment is anticipated to grow with a CAGR of 21.7% from 2025 to 2033, owing to the integration of ePharmacies with telemedicine platforms, enabling seamless e-prescribing, insurance verification, and home delivery of regulated medications. The rising prevalence of chronic diseases that necessitate long-term medication use is driving the growth of the ePharmacy market. In the U.S., the Centers for Disease Control and Prevention reports that 60% of adults have at least one chronic disease, creating sustained demand for reliable medication access. ePharmacies like Capsule and Medly offer automated refill reminders, dose tracking, and same-day delivery, significantly improving treatment adherence.

By Product Type Insights

The vitamins segment accounted in holding 28.3% of the ePharmacy market share in 2024, with the widespread consumer focus on preventive healthcare, immunity enhancement, and nutritional supplementation, particularly in the aftermath of the global pandemic. Unlike condition-specific treatments, vitamins appeal to a broad demographic ranging from children to the elderly by making them a staple in household wellness routines. The Council for Responsible Nutrition states that 77% of U.S. adults regularly consume dietary supplements, with multivitamins being the most commonly used category. The shift toward personalized nutrition and digital health tracking is also to leverage the growth of the ePharmacy market. Companies like Care/of and Ritual use AI-driven quizzes and health data integration to recommend customized regimens, creating strong customer loyalty. The U.S. Department of Health and Human Services notes that over 40% of supplement users now prefer auto-replenishment through online platforms, ensuring recurring revenue. Social media also amplifies adoption; a Morning Consult survey reveals that 58% of millennials and Gen Z consumers have purchased vitamins based on influencer endorsements on Instagram and TikTok.

The weight loss segment is likely to grow with an expected CAGR of 18.3% from 2025 to 2033, owing to the escalating global obesity epidemic and the increasing normalization of medicalized weight management solutions. According to the World Health Organization, global obesity has nearly tripled since 1975, with over 650 million adults classified as obese in 2023. In response, consumers are turning to clinically backed weight loss products, including GLP-1 receptor agonists, fat burners, appetite suppressants, and metabolism boosters, many of which are now available through regulated ePharmacy platforms.

The rapidly growing awareness of fitness culture, digital health apps, and social media influence is additionally to fuel the growth of the segment. According to the International Health, Racquet & Sportsclub Association, over 60 million Americans used fitness tracking apps in 2023, many of which integrate with ePharmacies to recommend supplements based on activity and dietary data. Platforms like Noom and Found combine behavioral coaching with medication access, creating a holistic weight management ecosystem.

REGIONAL ANALYSIS

North America Market Analysis

North America ePharmacy market accounted in holding 42.3% of the share in 2024, with the advanced digital infrastructure, high healthcare costs, and strong consumer adoption of telehealth services. The United States growth is innovation with a mature regulatory framework that supports e-prescriptions and online dispensing. The integration of ePharmacies with employer-sponsored health plans and insurance networks has further accelerated adoption. The American Telemedicine Association reports that 87% of large U.S. employers now offer telehealth benefits, many of which include direct links to ePharmacy services. Platforms like Amazon Pharmacy and Walmart Health have leveraged their logistics and retail ecosystems to offer same-day delivery and competitive pricing. Regulatory clarity from the FDA on digital prescriptions and remote consultations has also reduced legal uncertainties.

Europe Market Analysis

Europe was positioned second by holding 24.3% of the global ePharmacy market share in 2024 with a balanced blend of regulatory rigor and digital innovation, with countries like Germany, the UK, and the Netherlands leading in e-prescription adoption. Germany alone contributes over 30% of Europe’s ePharmacy sales, driven by the nationwide rollout of the eRezept (digital prescription) system. The European Union’s Digital Health Certificate initiative has enabled cross-border prescription validation, facilitating seamless medication access for travelers and expatriates. The European Commission states that 27 EU countries have implemented digital health service infrastructures, supporting interoperability. Consumer trust in licensed online pharmacies remains high, with the European Association of Euro-Pharmacies reporting that over 60% of Europeans prefer purchasing from regulated ePharmacies.

Asia-Pacific Market Analysis

The Asia-Pacific ePharmacy market is likely to grow with a significant CAGR in the coming years. India and China are the primary growth engines, driven by massive populations, rising smartphone penetration, and government-backed digital health initiatives. In China, the National Medical Products Administration reports that over 1,000 online pharmacies were licensed by 2023, up from just 200 in 2019.

Latin America Market Analysis

The Latin America ePharmacy market is expected to grow with prominent growth opportunities in the coming years. Brazil and Mexico lead regional growth, with Brazil accounting for over 50% of the market. The Brazilian Internet Steering Committee (CGI.br) reports that internet penetration reached 81% in 2023, with over 170 million users, enabling digital health adoption. The rise of telemedicine is a major growth driver. The Brazilian Medical Association states that over 60 million teleconsultations were conducted in 2022, many resulting in e-prescriptions. Regulatory progress is accelerating ANVISA has extended temporary online prescription regulations.

COMPETITIVE LANDSCAPE

The competition in the ePharmacy market is intensifying as traditional pharmacy chains, tech giants, and agile startups converge on digital health. The landscape is no longer defined solely by product availability or pricing but by the depth of integration, user experience, and trust in service delivery. Incumbents like CVS and Walgreens are leveraging their physical networks to offer hybrid models, combining online ordering with in-store pickup and clinical services. Meanwhile, pure-play digital platforms such as 1mg and Medly are innovating with AI-driven adherence tools, subscription models, and hyper-local delivery to capture niche segments. The entry of global technology leaders like Amazon has disrupted the market by applying e-commerce efficiency to pharmaceutical distribution, raising consumer expectations for speed and convenience. Regulatory compliance remains a key differentiator, as licensed platforms distinguish themselves from unregulated sellers flooding social media and third-party marketplaces. Brand credibility, data security, and medical accuracy are becoming decisive factors in consumer choice.

KEY MARKET PLAYERS

Some of the notable companies playing a crucial role in the global ePharmacy market profiled in this report are

- CVS Health

- Walmart Stores, Inc.

- Walgreen Co.

- The Kroger Co.

- Rite Aid Corp

- Lloyds Pharmacy Ltd.

- Planter

- Canada Drugs

- Medicate

- Express Scripts Holding Company

- Secure Medical Inc.

- Sani care A.B.

- Doctors Rowlands Pharmacy

- Giant Eagle, Inc.

- Optus Rx, Inc.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One major strategy employed by leading ePharmacy players is vertical integration of healthcare services. Companies are combining telemedicine, diagnostics, pharmacy, and insurance under a single digital umbrella to offer end-to-end health solutions. This approach enhances user retention, streamlines care delivery, and differentiates brands in a crowded market.

Another strategy is strategic partnerships with insurers, hospitals, and technology firms. E-pharmacies ensure seamless reimbursement, prescription routing, and clinical integration with increasing adoption among physicians and patients alike.

Another approach is investment in logistics and fulfillment infrastructure. Companies are building temperature-controlled warehousing, last-mile delivery fleets, and AI-driven inventory systems to ensure speed, reliability, and product integrity for chronic and specialty medications. This operational excellence strengthens consumer confidence and competitive advantage.

TOP LEADING PLAYERS IN THE MARKET

- Amazon Pharmacy has redefined the global ePharmacy landscape by leveraging its unparalleled logistics network, vast customer base, and digital ecosystem integration. As a subsidiary of the e-commerce giant, it offers seamless prescription fulfillment with options for home delivery, same-day dispatch, and integration with Amazon Prime benefits. The platform emphasizes convenience, pricing transparency, and insurance compatibility, making medication access effortless for millions. Its entry into the regulated pharmacy space signaled a major shift in market dynamics, compelling traditional players to accelerate digital transformation. By linking with Amazon Clinic for telehealth consultations, it has created a vertically integrated health service model. Amazon Pharmacy’s influence extends beyond retail, setting new benchmarks for speed, scalability, and user experience in the digital pharmacy domain.

- CVS Health has strategically evolved from a brick-and-mortar pharmacy chain into a comprehensive digital health provider through its CVS Pharmacy online platform. It combines physical store presence with robust ePharmacy services, including prescription refills, home delivery, and integration with its Aetna insurance network. The company has prioritized patient-centric innovation by incorporating medication adherence tools, personalized health alerts, and chronic care management programs. Its digital transformation includes mobile app enhancements, telemedicine access, and data-driven health insights.

- 1mg, now part of the Tata Group, has emerged as a transformative force in the Asia-Pacific ePharmacy market in India, where it addresses gaps in healthcare accessibility. The platform offers a wide range of services, including medicine delivery, lab testing, teleconsultations, and health content in multiple regional languages. 1mg has played a pivotal role in normalizing online medicine purchases in a market traditionally reliant on physical pharmacies. Its focus on authenticity, affordability, and education has built strong consumer trust.

GLOBAL ePHARMACY MARKET NEWS

- In February 2023, Amazon Pharmacy expanded its service to include controlled substances in select U.S. states by enhancing its prescription portfolio and regulatory compliance framework.

- In July 2023, CVS Health integrated its ePharmacy platform with Aetna’s digital health portal by enabling members to manage prescriptions, insurance claims, and telehealth visits in one interface.

- In October 2023, Tata 1mg launched a blockchain-based medicine authenticity verification system to combat counterfeit drugs and increase consumer trust in online purchases.

- In January 2024, Walgreens deepened its partnership with Microsoft to enhance its digital pharmacy platform using cloud computing and AI-driven patient engagement tools.

- In May 2024, Medly Pharmacy introduced a voice-activated prescription refill feature through smart speakers, which is improving accessibility for elderly and visually impaired users.

MARKET SEGMENTATION

This research report on the global ePharmacy market has been segmented and sub-segmented based on the drug type, product type, and region.

By Drug Type

- Prescription Drugs

- Over-the-Counter Drugs

By Product Type

- Skin Care

- Dental

- Cold And Flu

- Vitamins

- Weight Loss

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What is the ePharmacy Market?

The ePharmacy Market covers the distribution and sale of prescription and OTC medications via digital platforms, offering remote ordering, home delivery, teleconsultation integration, and digital prescription management

2. Which regions dominate the ePharmacy Market?

North America leads in market share (over 40% in 2025), propelled by robust digital infrastructure and healthcare adoption, followed by Europe and quickly expanding Asia Pacific markets

3. What factors are driving growth in the ePharmacy Market?

Key drivers include strong internet and smartphone penetration, demand for convenient healthcare access, aging populations, chronic disease prevalence, digital health ecosystem adoption, and post-pandemic care models

4. How is telemedicine influencing the ePharmacy Market?

Telemedicine enables direct e-prescriptions, seamless integration with online pharmacies, remote diagnosis, and rapid home delivery of required medication

5. What are the main product segments in the ePharmacy Market?

Prescription drugs, OTC medications, wellness supplements, personal care products, and subscription-based refill services are prominent categories

6. What challenges does the ePharmacy Market face?

Regulatory compliance, prescription verification, risk of counterfeit drugs, cold chain logistics, last-mile delivery, and data security present significant hurdles

7. Who are the leading ePharmacy Market companies globally?

Major players include CVS Health, Walgreens Boots Alliance, Amazon Pharmacy, Netmeds, PharmEasy, 1mg, DocMorris, Apoteket AB, and specialty digital pharmacy platforms

8. How are AI and digital health tools used in the ePharmacy Market?

AI supports prescription validation, dose optimization, refill reminders, medication tracking, automated drug authentication, and personalized recommendations

9. How does ePharmacy improve chronic disease management?

ePharmacies offer easier access to medication, refill reminders, automated renewals, and integrated digital consultations for patients with diabetes, hypertension, and other chronic illnesses

10. What is the future of prescription validation in the ePharmacy Market?

Trends include adoption of ePrescriptions, AI-powered verification, blockchain for drug traceability, and robust security protocols to prevent fraud

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com