Global Seed Market Size, Share, Trends & Growth Forecast Report, Segmented By Crop (Field Crops & Fruit & Vegetable Crops), Availability (Commercial Seeds & Saved Seeds), Seed Treatment (Treated & Untreated), Seed Trait (Insecticide Resistant, Herbicide Tolerant, Other Stacked Traits) and Region (North America , Europe, Asia Pacific, Latin America, Middle East And Africa), Industry Analysis From 2026 to 2034

Global Seed Market Report Summary

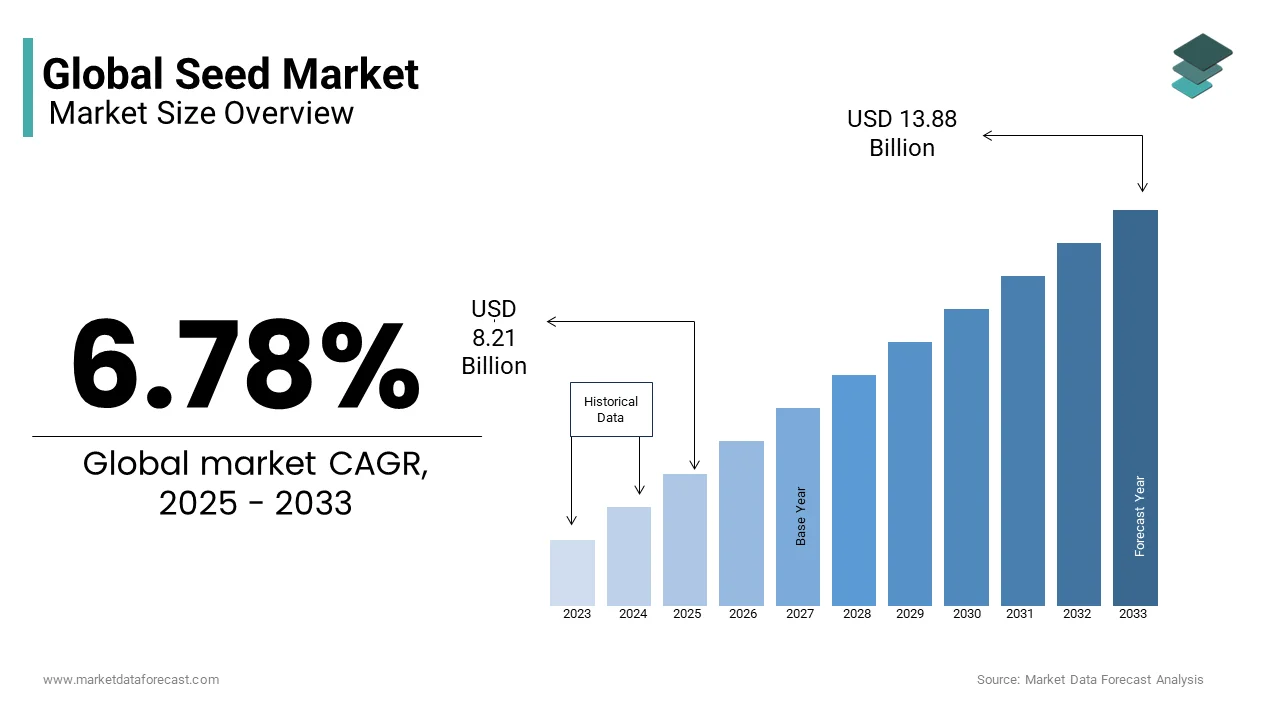

The global seed market was valued at USD 8.21 billion in 2025, is estimated to reach USD 8.77 billion in 2026, and is projected to expand to USD 14.82 billion by 2034, growing at a CAGR of 6.78% during the forecast period from 2026 to 2034. The growth of the global seed market is driven by rising global food demand, increasing adoption of high-yield and resilient crop varieties, and the need to improve agricultural productivity amid climate variability. Advancements in seed breeding technologies, growing penetration of commercial seeds, and increasing focus on crop protection traits such as herbicide tolerance are further fueling market growth. Additionally, government initiatives supporting modern agriculture and seed replacement rates are strengthening long-term market expansion.

Key Market Trends

Growing demand for high-yield and stress-tolerant seed varieties to address climate change and resource constraints. Increasing adoption of commercial seeds over farm-saved seeds due to better yield consistency and disease resistance. Rising use of biotech and trait-enhanced seeds, particularly herbicide-tolerant varieties, to improve weed management efficiency. Expansion of hybrid and genetically improved seeds in large-scale commercial farming. Strong focus on sustainable agriculture, including demand for non-GMO and organic seed systems in developed markets.

Segmental Insights

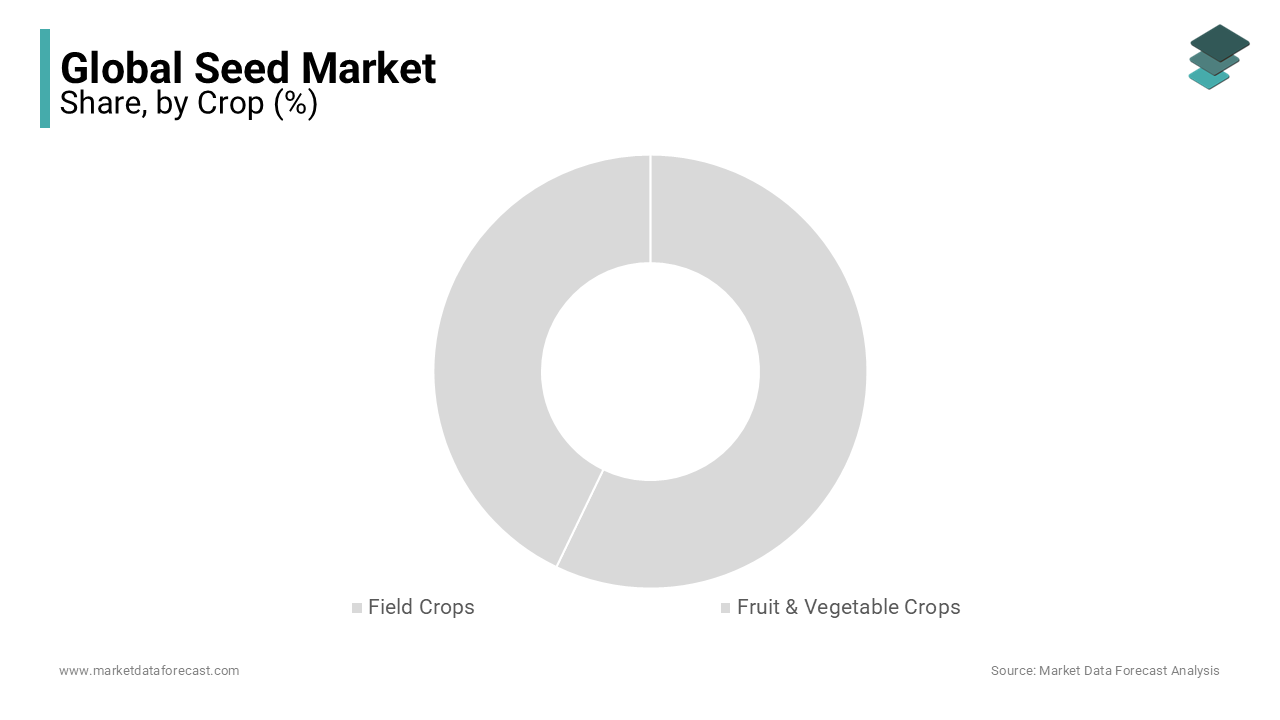

- Based on crop, the field crops segment dominated the global seed market in 2024, accounting for 65.2% of the total market value. The segment’s dominance is attributed to extensive cultivation of crops such as corn, wheat, rice, and soybeans, which form the backbone of global food and feed supply.

- Based on availability, the commercial seeds segment constituted the largest share of the market, representing 54.5% of the total global seed volume consumed in 2024. This dominance reflects increasing farmer preference for certified seeds that offer higher productivity, uniformity, and reliability.

- Based on seed traits, the herbicide-tolerant (HT) segment held a prominent position in 2024, accounting for 41.6% of all biotech seed hectares planted globally. The segment’s growth is driven by the need for efficient weed control, reduced labor costs, and improved crop management practices.

Regional Insights

The global seed market shows strong regional variation.

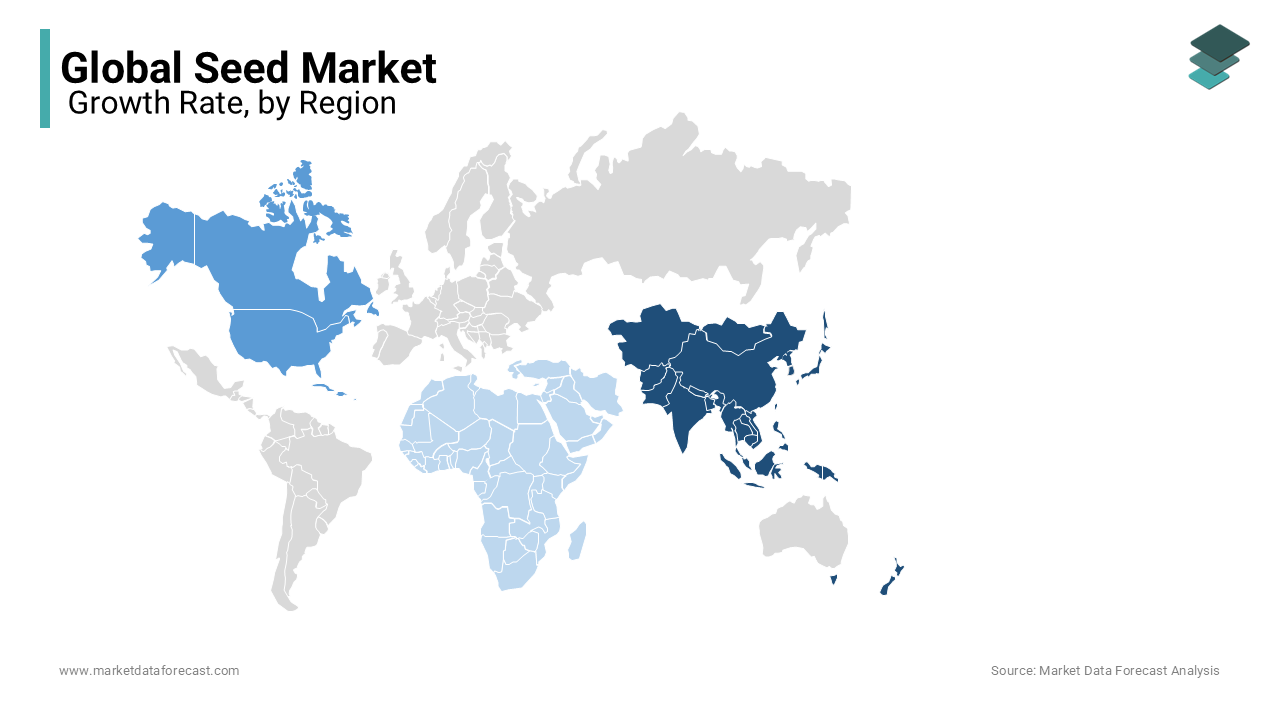

- North America led the market in 2024, accounting for 34.6% of the global share, supported by advanced agricultural practices, high adoption of biotech seeds, and the strong presence of major seed companies.

- Europe holds a significant share, characterized by a strong emphasis on non-GMO and organic seed systems.

- The Asia-Pacific region accounts for a notable share, driven by large agricultural economies such as India, China, and Japan, along with rising demand for improved seed varieties.

- Latin America represents a key market, led by Brazil and Argentina, with high adoption of commercial and biotech seeds.

- The Middle East and Africa collectively account for a smaller share, constrained by lower adoption rates and limited access to advanced seed technologies.

Competitive Landscape

The global seed market is highly competitive and consolidated, dominated by multinational agribusiness companies with strong research and breeding capabilities. Market players are focusing on innovation in seed traits, regional crop adaptation, and sustainable farming solutions to maintain a competitive advantage. Prominent companies operating in the global seed market include Monsanto Company (Bayer AG), Syngenta AG, Corteva Agriscience, BASF SE, Limagrain, KWS SAAT SE, Groupe InVivo, Sakata Seed Corporation, Enza Zaden, Rijk Zwaan, Burrus Seed Farms, Land O’Lakes, Inc. (WinField United), Takii & Co., Ltd., DLF Seeds, Emerald Seed Company, Delta Seeds, Gansu Dunhuang Seed Co., Ltd., and Nunhems (Bayer Crop Science).

Global Seed Market Size

The global seed market size was valued at USD 8.21 billion in 2025, and it is anticipated to reach USD 8.77 billion in 2026, from USD 14.82 billion by 2034, growing at a CAGR of 6.78% from 2026 to 2034.

Seed Market covers agricultural and horticultural seeds intended for food crops, fiber, biofuels, and landscaping. These biological inputs serve as the foundational element of global food systems, with increasing emphasis on genetic integrity, climate adaptability, and yield optimization.

According to the Food and Agriculture Organization (FAO), over 70% of the world’s caloric intake is derived from just nine crop species, underscoring the strategic importance of seed quality in food security. The International Seed Federation points out that professionally bred, quality-assured seeds contribute to a 20–30% increase in crop productivity compared to traditional farm-saved seeds. This biological and agronomic centrality positions the seed sector as a critical lever in sustainable agriculture and climate resilience.

MARKET DRIVERS

Rising Demand for Climate-Resilient and High-Yield Seeds Driving the Global Seed Mar

The escalating global demand for high-yielding and stress-tolerant crop varieties due to shifting climatic patterns and shrinking arable land is a primary driver of the Seed Market. As per the Intergovernmental Panel on Climate Change (IPCC), rising temperatures have already reduced global wheat yields, while drought frequency has increased in key agricultural zones between 2000 and 2020. In response, farmers are increasingly adopting certified seeds engineered or selected for drought, heat, and salinity tolerance. The International Maize and Wheat Improvement Center (CIMMYT) developed drought-resistant maize varieties that have been adopted across multiple African countries, improving yields under water-stressed conditions. This agronomic necessity is accelerating investment in both conventional breeding and advanced genomic selection techniques.

Supportive Seed Certification and IP Regulations Driving Innovation in the Global Seed Market

The expansion of regulatory frameworks supporting seed certification and intellectual property rights, which incentivize private-sector innovation, is another pivotal driver. Countries such as Brazil, Kenya, and the Philippines have strengthened their Plant Variety Protection (PVP) laws in recent years, aligning with UPOV 1991 standards to encourage research-based seed companies to introduce new cultivars. In Sub-Saharan Africa, the African Union’s Seed Trade Harmonization initiative reduced cross-border certification delays, facilitating faster dissemination of improved seeds. This regulatory maturation enables firms like Bayer and Corteva to recoup R&D investments, fostering a pipeline of genetically enhanced seeds.

MARKET RESTRAINTS

High Dependence on Farm-Saved Seeds Restraining Growth of the Global Seed Market

The persistent reliance on farm-saved seeds in developing economies, which limits the adoption of certified, high-performance varieties, is one major restraint in the Seed Market. According to the FAO, smallholder farmers in regions such as South Asia and Sub-Saharan Africa use saved or informal seed sources for up to 80% of their planting needs. In Ethiopia, only a limited share of maize planted came from certified seed, despite evidence from the Ethiopian Institute of Agricultural Research showing a yield advantage. This low adoption stems from limited access to distribution networks, high costs, and a lack of awareness. Additionally, weak rural extension services hinder technology transfer. These systemic barriers constrain market penetration and discourage investment in localized seed development, particularly for underrepresented crops like millets and legumes.

Regulatory Restrictions and Public Resistance to GM Seeds Restraining the Global Seed Market

The growing regulatory and public resistance to genetically modified (GM) seeds in several key markets, particularly in Europe and parts of Africa, is another significant restraint. As per the European Commission’s 2023 report on GMO cultivation, 23 out of 27 EU member states have imposed national bans on GM crop planting, citing environmental and health concerns. This has curtailed the commercialization of advanced seed technologies, even when scientifically validated. The African Centre for Biodiversity reports that misinformation and a lack of transparent risk communication have fueled skepticism. Moreover, the Cartagena Protocol on Biosafety imposes stringent import regulations, increasing compliance costs. These socio-political headwinds slow innovation diffusion and fragment global seed development strategies, particularly for climate-adaptive traits.

MARKET OPPORTUNITIES

Digital Agriculture Platforms Creating New Growth Opportunities in the Global Seed Market

The integration of digital agriculture platforms with seed selection and distribution, enabling precision agronomy at scale, is a transformative opportunity. According to the World Economic Forum, millions of smallholder farmers could benefit from digital advisory tools, many of which include seed recommendation engines based on soil, weather, and historical yield data. In India, the government-backed e-NAM (National Agriculture Market) platform now integrates seed advisories, reaching 18 million farmers across 1,000 mandis. These tools not only enhance decision-making but also create direct digital pathways for seed companies to engage farmers, monitor performance, and collect feedback, transforming traditional supply chains into responsive, data-driven ecosystems.

Role of Crop Biodiversity and Indigenous Varieties in Shaping the Global Seed Market

The resurgence of interest in underutilized and indigenous crop species, driven by nutritional security and biodiversity conservation goals, is another emerging opportunity. As per the United Nations Environment Programme (UNEP), over 7,000 edible plant species exist, yet fewer than 200 contribute significantly tothe global food supply. significantly Initiatives like the Crop Trust’s “10-Year Action Plan for Crop Diversity” aim to revive neglected crops such as finger millet, teff, and Bambara groundnut through modern seed systems. Ethiopia released certified seeds of drought-tolerant tef varieties, leading to an increase in cultivated area. Similarly, India’s National Bureau of Plant Genetic Resources conserved over 360,000 seed accessions by 2023, with 12,000 actively being bred for commercialization. This shift supports climate-resilient agriculture while opening niche markets for specialty and organic seeds.

MARKET CHALLENGES

Market Consolidation and Genetic Resource Concentration: Challenging the Global Seed Market

The concentration of genetic resources in a few multinational corporations, raising concerns about biodiversity and farmer autonomy, is a critical challenge facing the Seed Market. According to the ETC Group’s 2023 "Who Owns Nature?" report, four firms—Bayer, Corteva, ChemChina, and BASF—control over 60% of the global commercial seed market, with even higher shares in key crops like maize and soy. This consolidation reduces genetic diversity in circulation and limits access for public breeding programs. The FAO warns that 75% of crop genetic diversity has been lost over the past century due to the dominance of uniform commercial varieties. In addition, patenting practices restrict seed-saving traditions, particularly in developing nations.

Climate-Induced Disruptions Threatening Seed Production and Supply Chains in the Global Seed Market

The vulnerability of seed production systems to climate-induced disruptions, particularly in major seed-exporting regions, is another pressing challenge. These climatic shocks delay commercial availability and increase prices, disproportionately affecting small-scale farmers. Furthermore, rising temperatures accelerate pest proliferation. These environmental pressures compromise the reliability of seed supply chains and necessitate costly adaptation measures, including relocation of breeding stations and investment in controlled-environment facilities.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.78% |

| Segments Covered | Crop, Availability, Seed Treatment, Seed Trait, Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Monsanto Company (Now part of Bayer AG), Bayer AG, Syngenta AG, Corteva Agriscience (Formerly DowDuPont), BASF SE, Limagrain, KWS SAAT SE, Groupe InVivo, Sakata Seed Corporation, Enza Zaden, Rijk Zwaan, Burrus Seed Farms, Land O'Lakes, Inc. (WinField United), Takii & Co., Ltd., DLF Seeds, Emerald Seed Company, Delta Seeds, Gansu Dunhuang Seed Co., Ltd., Nunhems (Bayer Crop Science) |

SEGMENT ANALYSIS

By Crop Insights

The field crops segment dominated the global seed market by capturing 65.2% the total value in 2024. This dominance is primarily driven by the vast cultivated area dedicated to staple grains and oilseeds, which form the backbone of global food and feed systems. Maize, soybean, wheat, and rice alone occupy over 600 million hectares worldwide, according to the International Institute for Applied Systems Analysis (IIASA). The demand for high-yielding, uniform varieties in large-scale mechanized farming has favored the adoption of commercial hybrid and genetically enhanced seeds. In the United States, over 92% of maize and 95% of soybean acreage was planted with certified seeds in 2023, as documented by the U.S. Department of Agriculture. Additionally, government procurement programs in countries like India and Brazil prioritize certified field crop seeds for national food security initiatives, further entrenching their market leadership.

The fruit and vegetable crops segment is expanding at the fastest CAGR of 9.6% from 2025 to 2033. This rapid growth is fueled by rising consumer demand for diverse, nutrient-dense, and visually appealing produce in both developed and emerging markets. According to the World Health Organization, less than 20% of the global population consumes the recommended daily intake of fruits and vegetables, prompting public health campaigns that incentivize production. The horticultural seed sector has responded with innovations in flavor, shelf life, and disease resistance. Besides, urban agriculture and vertical farming in cities like Singapore and Tokyo rely heavily on high-performance vegetable seeds, accelerating demand for precision-bred cultivars tailored to controlled environments.

By Availability Insights

The commercial seeds segment constituted the largest part of the seed market by accounting for 54.5% of total volume consumed globally in 2024. This position is anchored in the increasing adoption of hybrid and genetically improved varieties that cannot be reliably reproduced through farm-saved seed due to genetic segregation. In industrialized agriculture, particularly in North America and Europe, regulatory frameworks and intellectual property rights mandate the use of certified seeds for many high-value crops. As per the European Seed Association, over 98% of sugar beet and 90% of maize seeds planted in the EU are commercially sourced. Furthermore, public extension services in countries like Brazil and South Africa actively promote certified seeds through subsidy programs. As per the Brazilian Agricultural Research Corporation (Embrapa), farmers using certified soybean seeds achieved an average yield increase of 18% compared to those using saved seeds, reinforcing economic incentives for commercial adoption.

The saved seeds segment is witnessing a resurgence in specific regions and is growing at a CAGR of 6.3% in Sub-Saharan Africa and South Asia between 2025 and 2034. This growth is not due to stagnation in commercial seed access but rather to a strategic revival of community-based seed systems in response to climate variability and biodiversity loss. These initiatives are backed by growing recognition from the FAO that agro-biodiversity enhances long-term food system resilience, particularly for smallholders facing unpredictable weather patterns.

By Seed Trait Insights

The herbicide-tolerant (HT) trait segment held the prominent share of the global seed trait market by representing 41.6% of all biotech seed hectares planted in 2024. This dominance is due to the widespread adoption of HT crops, particularly glyphosate-tolerant soybeans and cotton, in large-scale farming systems across the Americas. In the United States, 94% of soybean acreage was planted with HT varieties in 2023, enabling efficient weed control in no-till and reduced-till systems that conserve soil moisture and reduce erosion, as per the U.S. Department of Agriculture. The economic advantage is clear. This operational efficiency continues to drive farmer preference despite growing concerns about herbicide-resistant weeds.

The stacked traits segment is growing at the fastest CAGR of 8.7% from 2026 to 2034. This acceleration is driven by the need for multi-pest and multi-stress management in intensively farmed regions. Modern stacked varieties, such as Bt + HT cotton and maize, provide dual protection, reducing reliance on chemical pesticides and improving yield consistency. In India, over 95% of cotton acreage was planted with stacked-trait seeds in 2023, up from 78% in 2018, according to the Central Institute for Cotton Research. The African Agricultural Technology Foundation notes that stacked traits are now being developed for drought tolerance combined with pest resistance, particularly in sub-Saharan Africa, where climate and pest pressures converge, making them essential for sustainable intensification.

REGIONAL ANALYSIS

North America Market Analysis

North America led the global seed market by commanding a 34.6% share in 2024. The region’s dominance is underpinned by advanced agricultural infrastructure, high mechanization rates, and robust intellectual property frameworks that encourage private-sector R&D. The United States alone accounts for over 40% of global commercial seed sales, with corn, soybean, and cotton seeds forming the core of its biotech portfolio. Canada complements this with strong public breeding programs, particularly in canola and pulses. Regulatory efficiency through the USDA’s SECURE rule has expedited the approval of genome-edited crops, positioning North America as a pioneer in next-generation seed innovation and export leadership.

Europe Market Analysis

Europe holds a significant market share, with a distinct emphasis on non-GMO and organic seed systems, as reported by Eurostat. The region’s market dynamics are shaped by stringent GMO regulations and a growing consumer preference for sustainable agriculture. France and Germany are leading producers of conventional hybrid seeds for wheat, sunflower, and vegetables. According to the European Seed Association, over 70% of vegetable seeds used in the EU are commercially sourced, with companies like KWS Saat SE and Limagrain driving innovation.

Asia Pacific Market Analysis

Asia Pacific accounts for a notable share of the global seed market, with India, China, and Japan as key contributors. India is the world’s fifth-largest seed market and the largest producer of hybrid cotton seeds, exporting to over 40 countries. China, meanwhile, is investing heavily in seed sovereignty. Japan focuses on high-value vegetable and flower seeds, with Sakata Seed Corporation dominating the global ornamental seed market. Urban farming and protected cultivation are further accelerating demand for precision-bred cultivars.

Latin America Market Analysis

Latin America represents a key share of the global seed market, with Brazil and Argentina as dominant players. Brazil is the world’s second-largest market for genetically modified seeds, cultivating over 65 million hectares of biotech crops in 2023, as reported by CTNBio, the country’s biosafety authority. The adoption of HT soybeans and stacked-trait maize has been instrumental in expanding agricultural productivity. Embrapa’s public-private partnerships have led to the development of tropicalized seed varieties suited to the Cerrado biome, increasing national self-sufficiency. Argentina, despite economic volatility, maintains high adoption rates of GM seeds, with over 99% of soybean and maize acreage planted with certified biotech varieties.

Middle East And Africa Market Analysis

The Middle East and Africa collectively account for a small share of the global seed market, but Sub-Saharan Africa exhibits the fastest growth in seed system development. Kenya, Nigeria, and Ethiopia are emerging as regional hubs for seed production and distribution. According to the Alliance for a Green Revolution in Africa (AGRA), the formal seed market in Africa grew from $1.1 billion in 2015 to $1.8 billion in 2023. Egypt leads in vegetable seed production, exporting to Europe and the Gulf. Despite challenges, the push for food self-reliance is driving unprecedented investment in seed infrastructure and farmer access programs.

COMPETITIVE LANDSCAPE

Competition in the Seed Market is characterized by a blend of technological superiority, regional adaptation, and regulatory navigation. While multinational corporations dominate high-input farming systems, regional and local seed enterprises are gaining ground by addressing niche crops and smallholder needs. The race for innovation is intensifying, with CRISPR-based breeding and climate-resilient traits becoming key differentiators. However, disparities in intellectual property enforcement, biosafety regulations, and farmer access create fragmented market dynamics across geographies. Companies are increasingly competing on trust, transparency, and ecosystem support rather than price alone. Public-private collaborations and open-source breeding initiatives are emerging as counterweights to corporate consolidation, fostering a complex, multi-layered competitive environment where agility, localization, and scientific credibility determine long-term success.

KEY MARKET PLAYERS

are some of the market players dominating the global seed market.

- Monsanto Company (Now part of Bayer AG)

- Bayer AG

- Syngenta AG

- Corteva Agriscience (Formerly DowDuPont)

- BASF SE

- Limagrain

- KWS SAAT SE

- Groupe InVivo

- Sakata Seed Corporation

- Enza Zaden

- Rijk Zwaan

- Burrus Seed Farms

- Land O'Lakes, Inc. (WinField United)

- Takii & Co., Ltd.

- DLF Seeds

- Emerald Seed Company

- Delta Seeds

- Gansu Dunhuang Seed Co., Ltd

- Nunhems (Bayer Crop Science)

Top Players In The Market

- Bayer CropScience has established a significant presence in the Asia Pacific seed sector through strategic investments in rice and vegetable breeding programs tailored to regional agro-climatic conditions. The company operates advanced research centers in India, Thailand, and China, focusing on developing high-yielding, stress-tolerant rice varieties using molecular breeding and gene-editing technologies. It also expanded its vegetable seed portfolio in Japan and South Korea by acquiring local breeding lines to enhance flavor and shelf life. Collaborations with national agricultural institutes in Vietnam and Indonesia have accelerated the release of certified seeds, while digital farming platforms like Xarvio provide seed-specific agronomic recommendations, strengthening farmer engagement and adoption across diverse cropping systems.

- Corteva Agriscience is deeply embedded in the Asia Pacific seed landscape, particularly in India, Australia, and Southeast Asia, where it delivers hybrid maize, rice, and specialty crop seeds. The company has intensified its R&D efforts through its Hyderabad-based research hub, which develops climate-smart varieties for smallholder farmers. It also launched a farmer-centric digital platform, Cropwise, in Indonesia and Thailand, offering seed selection tools based on local soil and weather data. In Australia, Corteva strengthened its canola seed portfolio through partnerships with Grain Producers Australia, enhancing trait integration for pest resistance. These initiatives reflect a broader strategy of localized innovation, capacity building, and extension services to deepen market penetration and build trust among farming communities.

- Sakata Seed Corporation, headquartered in Japan, is a global leader in vegetable and ornamental seed development, with a dominant footprint across the Asia Pacific. The company supplies over 600 vegetable seed varieties to markets in China, India, Thailand, and Vietnam, focusing on high-nutrition, disease-resistant cultivars for tomatoes, cucumbers, and leafy greens. Sakata operates breeding stations in Chiang Mai and Nashik, enabling rapid adaptation to local pests and consumer preferences. The company also launched farmer training programs in the Philippines to improve seedling management and yield outcomes. Its commitment to non-GMO breeding and sustainable production has positioned Sakata as a trusted provider in premium and organic vegetable supply chains.

Top Strategies Used By The Key Market Participants

Key players in the Seed Market are leveraging advanced breeding technologies, regional localization, and digital integration to consolidate their influence. Companies are investing heavily in gene editing, marker-assisted selection, and AI-driven phenotyping to accelerate trait development. Strategic partnerships with public research institutions and national agricultural agencies enable faster varietal release and regulatory approval. Firms are tailoring seed portfolios to regional climatic and cultural preferences, particularly in Asia and Africa, to enhance adoption. Digital platforms that provide real-time agronomic advice are being used to drive seed sales and improve farmer outcomes. Additionally, vertical integration—from breeding to distribution—is improving supply chain efficiency. Sustainability initiatives, including non-GMO innovation and reduced chemical dependency, are increasingly shaping brand positioning and regulatory compliance in environmentally sensitive markets.

RECENT MARKET NEWS

- In January 2022, Bayer CropScience launched its Climate-Resilient Rice Initiative in collaboration with the International Rice Research Institute in the Philippines, introducing five new flood-tolerant and heat-resistant rice varieties to smallholder farmers across Southeast Asia.

- In June 2022, Corteva Agriscience inaugurated a state-of-the-art seed processing facility in Pune, India, designed to enhance the quality and scalability of hybrid maize and vegetable seed production for domestic and export markets.

- In March 2023, Sakata Seed Corporation introduced a digital seed traceability system in Thailand, enabling retailers and farmers to verify the origin and breeding history of vegetable seeds via QR codes, improving transparency and brand trust.

- In September 2023, Bayer expanded its Xarvio Digital Farming Platform to Vietnam, integrating seed-specific agronomic recommendations for rice and sugarcane, helping farmers optimize planting decisions and input use.

- In February 2024, Corteva Agriscience partnered with the Australian Grains Gene Bank to co-develop next-generation canola varieties using gene-editing technologies aimed at improving drought tolerance and oil profile for global markets.

MARKET SEGMENTATION

This research report on the global seed market has been segmented & sub-segmented based on the crop, availability, seed treatment, seed trait, and region.

By Crop

- Field Crops

- Fruit & Vegetable Crops

By Availability

- Commercial Seeds

- Saved Seeds

By Seed Treatment

- Treated

- Untreated

By Seed Trait

- Herbicide-Tolerant

- Insecticide Resistant

- Other Stacked Traits

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

what is the size of global seed market ?

As per our analysis report, the global Seed Market is expected to reach USD 8.21 billion by 2025.

what is the CAGR of global seed market?

The Global seed market is expected to be valued at a CAGR of 6.78% by the end of 2033.

what are key market players in seed market?

Monsanto Company (Now part of Bayer AG), Bayer AG, Syngenta AG, Corteva Agriscience (Formerly DowDuPont), BASF SE, Limagrain, KWS SAAT SE, Groupe InVivo, Sakata Seed Corporation, Enza Zaden, Rijk Zwaan, Burrus Seed Farms, Land O'Lakes, Inc. (WinField United), Takii & Co., Ltd., DLF Seeds, Emerald Seed Company, Delta Seeds, Gansu Dunhuang Seed Co., Ltd., Nunhems (Bayer Crop Science)

What is driving growth in the global seed market?

Rising food demand from a growing population and the need for high-yield, climate-resilient crops are pushing innovation in seed technology.

Which crop segments dominate the seed market?

Corn, soybean, and rice lead due to their large-scale cultivation and widespread use in food, feed, and biofuels.

How do biotech and GM seeds influence the industry?

Genetically modified seeds with traits like pest resistance and drought tolerance are widely adopted in regions like North and South America.

What role do hybrid seeds play globally?

Hybrid seeds offer higher productivity and uniformity, making them popular in both developed and emerging agricultural economies.

How is sustainability shaping seed development?

Companies are breeding seeds that require less water, tolerate poor soils, and thrive in extreme weather due to climate change.

What are the key challenges in the global seed market?

Strict regulations, intellectual property disputes, and limited access in smallholder farming regions slow down innovation adoption.

How are digital tools impacting seed selection and distribution?

Farmers now use farm management software and AI-driven platforms to choose the best seed varieties for their soil and climate.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com