Global Hostels Market Size, Share, Trends & Growth Forecast Report By Deployment (Hybrid, On-Premise, and Cloud), Solution (Channel Manager, Production Reports, Daily Activity Report, Room Management, Canteen Management, Invoice Management and Hostel Member Management), Enterprise (Small and Medium Enterprises and Large Enterprises) and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) - Industry Analysis From (2025 to 2033).

Global Hostels Market Size

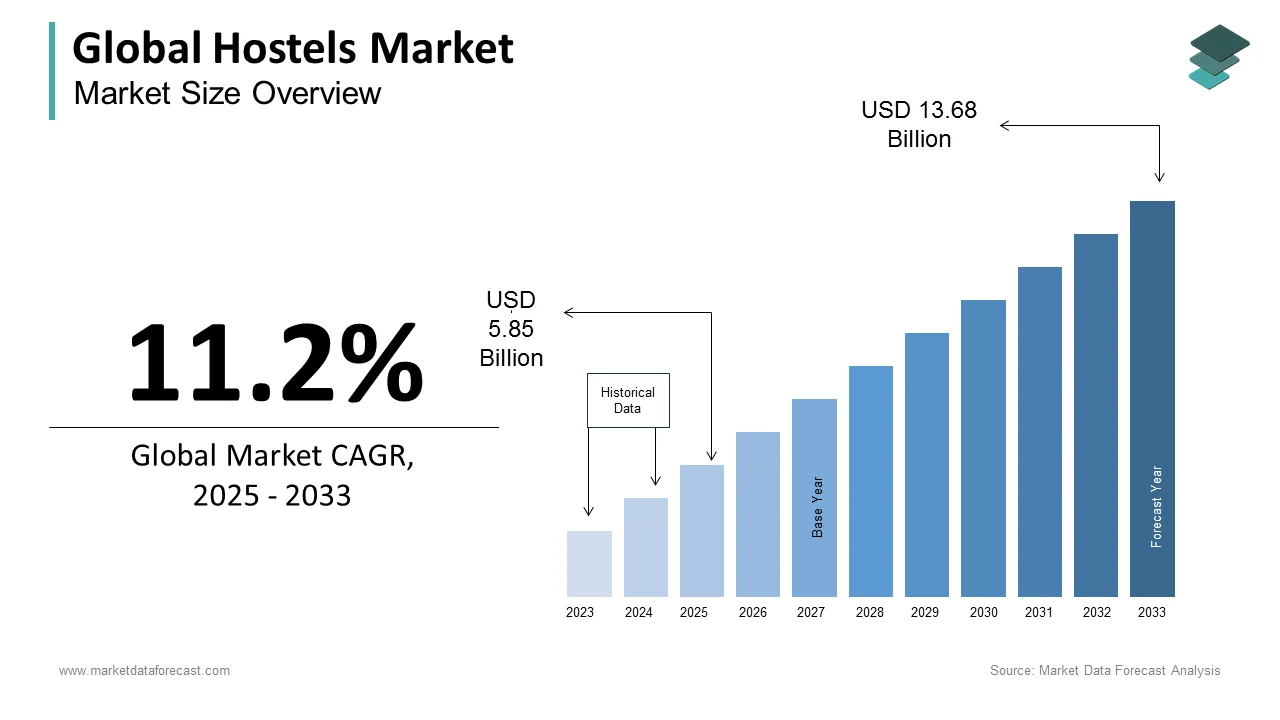

The size of the global hostels market was worth USD 5.26 billion in 2024. The global market is anticipated to grow at a CAGR of 11.2% from 2025 to 2033 and be worth USD 13.68 billion by 2033 from USD 5.85 billion in 2025.

Hostels refers to a accommodation that provides budget-friendly, shared-living lodging primarily targeting young travelers, backpackers, students, and independent explorers seeking social interaction and experiential travel. Unlike traditional hotels, hostels emphasize communal spaces, dormitory-style rooms, and low-cost private options, often integrating cultural activities, local tours, and co-living environments. Youth travelers constitute a significant portion of global tourism, with hostels heavily catering to this demographic. Hostels are increasingly evolving into lifestyle hubs, particularly in urban and heritage destinations, offering not just beds but curated experiences such as city walks, language exchanges, and sustainability workshops. Also, young travelers increasingly value experiential and culturally immersive travel.

MARKET DRIVERS

Rising Popularity of Solo and Experiential Travel Among Millennials and Gen Z

The growing preference for independent, experience-driven travel among younger demographics is a pivotal force expanding the global hostel sector. Solo and experience-driven travel among Millennials and Gen Z is rising, fueling hostel demand. Hostels, with their communal lounges, group events, and shared kitchens, directly cater to this behavioral shift. Hostels are popular among European travelers due to affordability and social opportunities. Hostel bookings among international travelers in Japan are growing, especially in culturally rich urban destinations. This cultural pivot toward meaningful, socially rich travel experiences positions hostels as essential nodes in the modern travel ecosystem.

Expansion of Digital Nomadism and Remote Work Trends

The normalization of remote work has catalyzed a new wave of long-term, location-independent travelers who seek affordable, flexible accommodations with reliable connectivity, conditions that hostels are increasingly designed to meet. The digital nomad population is rising globally, and hostels are adapting to cater to remote workers. Hostels in cities like Chiang Mai, Lisbon, and Medellín have adapted by offering co-living spaces, high-speed Wi-Fi, coworking areas, and monthly stay discounts. Hostels are increasingly used by remote workers for long-term stays due to affordability and social interactionBali has become a major hub for digital nomads, and hostels and co-living spaces are adapting to this demand.

MARKET RESTRAINTS

Regulatory Restrictions and Zoning Laws in Urban Centers

Many major cities impose strict zoning regulations and licensing requirements that limit the operation and expansion of hostels, particularly in residential or heritage zones. Like, major European cities enforce regulations limiting hostel and short-term rental operations to manage tourism and housing pressures. In Barcelona, the city council suspended new hostel licenses in 2022, citing concerns over neighborhood disruption and rising rents. Similarly, stringent safety and building codes increase operational costs for hostels in urban areas. In Asia, Tokyo’s Hotel Business Law requires hostels to meet hotel-grade structural and staffing standards, discouraging small operators. These regulatory barriers restrict supply growth and increase operational costs, hindering market scalability despite strong demand, particularly in high-traffic urban destinations.

Persistent Stigma Around Safety and Privacy in Shared Accommodations

Despite modernization, a significant portion of potential guests, particularly older travelers and families, continue to associate hostels with compromised privacy, noise, and security risks. Like, older travelers often perceive hostels as less private or secure, limiting adoption among this demographic. In India, hostel penetration is lower among certain age groups or regions due to perceived safety and privacy concerns. This perception persists even as many hostels implement keycard access, CCTV surveillance, and gender-separated dorms. Additionally, the absence of standardized quality certifications across regions makes it difficult for travelers to assess reliability. In Latin America, Safety and security concerns in hostels exist, especially where standards vary, ranging from theft to unauthorized access, further undermining trust and limiting broader market penetration.

MARKET OPPORTUNITIES

Integration of Hostels into Sustainable and Community-Based Tourism Models

Hostels are increasingly aligning with global sustainability goals by adopting eco-friendly practices and supporting local economies, creating a compelling value proposition for environmentally conscious travelers. There is a growing consumer preference for sustainable and certified accommodations. Hostels such as Hostelling International properties in Canada and Germany have achieved GSTC certification by implementing solar energy, zero-waste kitchens, and carbon-offset programs. In Costa Rica, Eco- and community-focused hostels can contribute meaningfully to local economies. Furthermore, many hostels now promote volunteer tourism, where guests contribute to conservation or education projects in exchange for reduced stays. This fusion of affordability, sustainability, and community engagement positions hostels as leaders in the ethical travel movement, opening new revenue streams and loyalty-building opportunities.

Adoption of Smart Technology and Digital Booking Ecosystems

The integration of smart technology is transforming hostel operations, enhancing guest experience while improving efficiency and security. Like, online and app-based booking systems are the dominant reservation channel for hostels worldwide. In South Korea, smart technology adoption in hostels improves operational efficiency and guest experience. Additionally, contactless payment systems and mobile key access have become standard in premium hostels, aligning with post-pandemic hygiene expectations. In Australia, many travelers, especially younger demographics, favor hostels offering integrated digital services for booking, tours, and communication. By leveraging data analytics, operators can personalize offerings and optimize occupancy, turning traditionally low-margin operations into scalable, tech-driven hospitality ventures.

MARKET CHALLENGES

Seasonal Fluctuations and Geographic Concentration of Demand

The hostel market is highly susceptible to seasonal variations, with occupancy rates often peaking during summer months and dropping sharply in off-seasons, creating financial instability for operators. In Europe, hostel demand is highly seasonal, with peak occupancy in summer months and reduced utilization in off-season periods. In New Zealand, tourist-dependent destinations experience significant seasonal occupancy variations. This volatility complicates staffing, maintenance planning, and cash flow management. Moreover, demand is heavily concentrated in tourist hotspots, leaving rural or emerging destinations underserved. In Thailand, Hostel supply tends to cluster in major tourist hubs, leading to geographic concentration of demand. Operators face challenges in sustaining year-round profitability without diversifying offerings or expanding into alternative travel segments such as educational or wellness stays.

Intensifying Competition from Alternative Accommodations

Hostels face mounting pressure from alternative lodging options such as budget hotels, capsule hotels, Airbnb’s “budget-plus” listings, and co-living spaces, which offer privacy at competitive prices. Alternative budget accommodations are increasingly competing with hostels by offering private, low-cost options. In Japan, the rise of capsule hotels with soundproof pods and smart amenities has drawn younger travelers seeking solitude without sacrificing affordability. Similarly, in India, Hostels face competition from budget hotels and co-living spaces that replicate social and communal features. This blurring of category boundaries forces traditional hostels to differentiate through enhanced experiences, loyalty programs, or niche positioning, requiring significant investment in branding and service innovation to maintain relevance in an increasingly crowded and hybridized accommodation landscape.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 11.2% |

| Segments Covered | By Implementation, By Solution, By Company Size, By Region |

|

Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | eZee Frontdesk, Hostelworld, Safestay plc, RoomMaster, Rezlynx PMS, Frontdesk Anywhere, MSI CloudPM, Maestro PMS, Hotelogix PMS, OPERA Property Management System (PMS), A&O Hotels and Hostels, Cloudbeds, WOKSEN, Canada Hostels, Newquay Backpackers, London Backpackers, Green Tortoise Hostel, and Hostelling International, and Others. |

SEGMENT ANALYSIS

By Deployment Insights

The Cloud deployment model dominated the Hostels Market by capturing 52.5% of the technology infrastructure segment in 2024. This lead position is due to the growing reliance on scalable, remotely accessible property management systems (PMS) that enable real-time operations across geographically dispersed hostel chains. The increasing need for seamless integration with global distribution systems (GDS), online travel agencies (OTAs), and dynamic pricing engines is a primary driver of cloud dominance. Also, online travel agencies and global distribution systems drive the majority of hostel reservations. In Australia, cloud PMS adoption improves inventory management and reduces overbooking risks. Additionally, cloud systems allow operators to manage multiple locations from a single dashboard, a critical advantage for expanding networks. With minimal upfront hardware investment and automatic software updates, cloud solutions offer cost-effective scalability, particularly for small and mid-sized hostel operators seeking digital transformation without heavy IT overhead.

The Hybrid deployment model is the fastest-growing segment in the Hostels Market and is projected to expand at a CAGR of 16.8% from 2025 to 2033. This growth is driven by hostel operators seeking a balanced approach that combines the security of on-premise data control with the flexibility of cloud connectivity. The rising concern over data privacy and system reliability in regions with unstable internet infrastructure is a key factor fueling this trend. Like, a limited number of rural areas have consistent high-speed internet, making full cloud dependency risky for critical operations like check-ins and payments. Hybrid systems allow hostels to run core functions, such as guest registration and room locking, on local servers while syncing data to the cloud during stable connections. In Nepal, Hybrid PMS is increasingly used in remote or connectivity-challenged areas. Furthermore, hybrid models support compliance with data localization laws in countries like India and Russia, where guest information must be stored domestically. This duality of resilience and connectivity makes hybrid deployment increasingly attractive for hostels operating in remote or regulated environments.

By Solution Insights

The Room Management segment held the largest share of the Hostels Market by solution, with 31.6% of total software functionality adoption in 2024. This dominance is rooted in the operational centrality of room allocation, occupancy tracking, and bed assignment in hostel environments, where shared dormitories and mixed private accommodations require precise coordination. The complexity of hostel inventory, which often includes gender-specific dorms, age-restricted floors, and mixed-bed configurations that standard hotel systems cannot accommodate, is the primary driver behind Room Management’s position. Like, hostels with dedicated room management modules experienced an improvement in occupancy optimization and a reduction in manual errors during peak seasons. In Japan, automated room assignment tools reduced check-in times per guest, significantly enhancing guest satisfaction. Additionally, integration with mobile apps allows guests to select bed locations, view dormmate profiles, and receive digital keys, improving transparency and personalization. With rising guest expectations for seamless digital experiences, advanced room management systems have become indispensable for operational efficiency and competitive differentiation.

The Hostel Member Management segment is the fastest-growing solution and is projected to grow at a CAGR of 18.2% in the coming years. This acceleration is driven by the resurgence of membership-based hostel networks and the strategic push toward customer retention and loyalty programs. The revival of nonprofit hostel associations is a major growth factor. Like, Membership-based hostel networks are growing and support loyalty. These memberships offer benefits such as discounted rates, priority bookings, and access to exclusive events, creating a recurring revenue stream and fostering long-term engagement. In Canada, membership programs increase average guest stay. Additionally, digital membership platforms now integrate with social media, travel tracking, and carbon footprint calculators, appealing to environmentally conscious travelers. Hostels in Germany and New Zealand have begun partnering with universities and student organizations to expand membership bases, further amplifying reach. As operators shift from transactional to relational models, Hostel Member Management systems are becoming central to branding, retention, and community building.

By Enterprise Insights

The Small and Medium Enterprises (SMEs) segment represents the prominent enterprise in the Hostels Market by commanding a substantial share of total hostel units globally in 2024. This dominance reflects the decentralized, independent nature of the hostel industry, where locally owned, boutique-style hostels outnumber large chains. The primary driver of SME prevalence is the low entry barrier for establishing small-scale hostels, particularly in urban and heritage districts where unused buildings can be converted into lodging. The hostel industry in developing regions is largely decentralized and family-operated. In Portugal, new hostel openings are predominantly SMEs, capitalizing on post-pandemic tourism recovery and digital booking platforms. These operators leverage local knowledge, cultural authenticity, and personalized service to differentiate themselves from standardized chains. Additionally, platforms like Hostelworld and Airbnb allow SMEs to achieve global visibility without significant marketing budgets, enabling sustainable growth through niche positioning and community integration.

The Large Enterprises segment is the fastest-growing enterprise in the Hostels Market and is projected to expand at a CAGR of 14.6% during the forecast period. This growth is fueled by increasing consolidation, brand franchising, and institutional investment in scalable hostel networks. A key driver is the professionalization of the hostel sector, with large operators introducing standardized operations, loyalty programs, and tech-integrated experiences that appeal to a broader demographic. Like, large, professional hostel chains are growing their presence globally. In Australia, large hostel chains expand via acquisitions and investments. Additionally, large enterprises are investing in sustainability certifications and digital infrastructure, enhancing credibility and attracting partnerships with airlines, tour operators, and universities. Their ability to negotiate bulk rates for supplies, secure prime real estate, and implement centralized marketing gives them a competitive edge, enabling rapid expansion in high-demand urban corridors and tourist hubs.

REGIONAL ANALYSIS

Europe Hostels Market Insights

Europe led the global hostel market with a share of 44.5% in 2024. The region’s preeminence is anchored in its dense network of historic cities, well-developed rail infrastructure, and deeply entrenched backpacking culture that spans generations. Countries like Germany, the United Kingdom, and Spain host some of the world’s most visited youth accommodations, with Hostelling International and other networks being major contributors. Also, youth hostels account for a significant portion of budget accommodations. The Erasmus+ program, which facilitated exchanges for over 15 million students since 2014, has further institutionalized hostel use among young Europeans. Additionally, cities have embraced hostel tourism as part of their urban hospitality strategy, reinforcing Europe’s status as the epicenter of hostel innovation and volume.

Asia Pacific Hostels Market Insights

Asia Pacific is a key growth region. The region’s hostel sector is characterized by rapid urbanization, rising disposable incomes among youth, and a surge in regional and inbound tourism from long-haul markets. Japan has seen rapid growth in certified hostels. Thailand is a major destination for long-stay youth travellers. India has seen a wave of startup-led hostel chains like Zostel and Backpackers Panda, targeting domestic millennials exploring road trips and hill stations. With improving internet access and digital payment adoption, the region is witnessing a shift from informal guesthouses to branded, tech-enabled hostel experiences, positioning it as the fastest-evolving market globally.

North America Hostels Market Insights

North America holds a notable share of the global hostel market, as reported by the American Youth Hostels (AYH) and Hostelling International USA in their 2023 joint market assessment. The region’s hostel landscape is marked by a growing emphasis on experiential and adventure travel, particularly in national parks and university towns. In the United States, High park visitation supports hostel and budget lodging demand near natural attractions. In Canada, Bookings by international youth travelers are increasing. While hostel density remains lower than in Europe or Asia, urban centers are seeing a resurgence of socially oriented hostels integrating coworking spaces and cultural events, appealing to digital nomads and solo travelers seeking community in high-cost cities.

Latin America Hostels Market Insights

Latin America is a growing hostel market. The region has emerged as a premier destination for experiential and adventure backpacking, drawing travelers along routes from Mexico to Patagonia. Countries like Colombia, Peru, and Guatemala have developed robust hostel networks in cultural hubs such as Medellín, Cusco, and Antigua, where low costs and rich heritage attract long-term stays. Also, youth tourism in the region grew, with hostels serving as primary bases for trekking, volunteering, and language learning. Brazil attracts substantial backpacker traffic. Despite challenges in infrastructure and safety perception, the region’s authenticity and affordability continue to drive organic growth in independent and community-focused hostel models.

Middle East and Africa Hostels Market Insights

Middle East and Africa are emerging markets. The region’s hostel sector is nascent but growing, with concentrated development in tourist-friendly nations such as South Africa, Morocco, and Jordan. In South Africa, Hostel development is accelerating in key urban and tourist regions. Morocco’s hostel sector is growing alongside tourism. In Egypt, Innovative hostel concepts are emerging, though scale and uptake are less well-documented. While cultural norms and regulatory frameworks limit expansion in some countries, initiatives signal growing recognition of hostels as viable components of sustainable and youth-oriented tourism strategies.

KEY MARKET PLAYERS

Companies playing a noteworthy role in the global hostels market include eZee Frontdesk, Hostelworld, Safestay PLC, RoomMaster, Rezlynx PMS, Frontdesk Anywhere, MSI CloudPM, Maestro PMS, Hotelogix PMS, OPERA Property Management System (PMS), A&O Hotels and Hostels, Cloudbeds, WOKSEN, Canada Hostels, Newquay Backpackers, London Backpackers, Green Tortoise Hostel, and Hostelling International.

TOP LEADING PLAYERS IN THE MARKET

Hostelling International

Hostelling International (HI) has played a foundational role in shaping the hostel ecosystem across the Asia Pacific region by promoting safe, sustainable, and socially enriching travel experiences. Through its network of nonprofit hostels in countries such as Japan, Australia, India, and New Zealand, HI emphasizes cultural exchange, environmental responsibility, and community engagement. The organization also partnered with local universities in Thailand and Malaysia to offer student travel discounts and volunteer programs, strengthening youth connectivity. By maintaining rigorous quality standards and digital integration through its global booking platform, HI has reinforced trust and consistency, positioning itself as a benchmark for ethical and accessible accommodation in the region.

Zostel (Zostel Hospitality Pvt. Ltd.)

Zostel has redefined the hostel experience in India and neighboring markets by blending affordability with curated social experiences tailored to young domestic travelers. Originating as a backpacker-focused chain, Zostel has expanded to over 50 properties across India, Nepal, and Sri Lanka, strategically located near hill stations, beaches, and pilgrimage routes. It also launched a mobile app with AI-driven recommendations for local experiences, integrating hostel stays with adventure tourism. By focusing on Instagram-friendly design, hygiene transparency, and community events like bonfires and music nights, Zostel has cultivated a loyal millennial and Gen Z following. Its localized branding and digital-first approach have made it a dominant player in South Asia’s evolving budget travel landscape.

Base Backpackers (Base Urban Adventures)

Base Backpackers has established a strong footprint in Australia and New Zealand by operating urban, design-led hostels that cater to international backpackers, working holiday makers, and digital nomads. With properties in Sydney, Melbourne, Queenstown, and Auckland, the brand combines modern amenities, such as coworking spaces, rooftop bars, and fitness zones, with affordable dormitory and private lodging. The company also invested in proprietary property management software to streamline operations across its multi-city portfolio. By aligning with Australia’s Working Holiday Visa program and sponsoring music and adventure festivals, Base has embedded itself in the youth travel culture. Its focus on lifestyle branding and operational scalability has positioned it as a leading commercial hostel operator in the trans-Tasman corridor.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Hostels Market are deploying multifaceted strategies to enhance competitiveness and expand reach. Brand differentiation through experiential offerings—such as guided tours, social events, and cultural workshops—is being used to transition from mere lodging to lifestyle ecosystems. Digital transformation is a priority, with investments in mobile apps, cloud-based property management systems, and dynamic pricing tools to improve operational efficiency and customer engagement. Strategic geographic expansion into emerging tourist corridors and secondary cities is enabling access to underserved markets. Partnerships with travel platforms, airlines, and visa facilitation services are increasing visibility and conversion. Additionally, sustainability initiatives, including eco-certifications and community-based tourism models, are being leveraged to appeal to environmentally conscious travelers and comply with evolving regulatory expectations in key destinations.

COMPETITION OVERVIEW

The competitive landscape of the Hostels Market is defined by a blend of nonprofit networks, regional chains, and independent operators vying for dominance through differentiation in experience, technology, and location. Established organizations like Hostelling International maintain influence through global standards and sustainability credentials, while agile startups such as Zostel and Base Backpackers leverage digital branding and localized experiences to capture youth markets. Competition is intensifying as operators diversify beyond dormitories into private rooms, co-living spaces, and hybrid work-stay models to appeal to broader demographics. The rise of experiential travel has shifted focus from cost alone to community, safety, and authenticity, compelling hostels to invest in curated programming and digital engagement. Geographic expansion, technological integration, and strategic partnerships are now critical for scalability, particularly in high-growth regions like the Asia Pacific and Latin America, where demand for affordable, social lodging continues to surge.

RECENT MARKET DEVELOPMENTS

- In March 2022, Hostelling International launched the Green Hostels Initiative across its Asia Pacific properties, implementing solar energy systems, water recycling units, and plastic-free operations to align with global sustainability standards and attract eco-conscious travelers.

- In July 2022, Zostel introduced Zostel Holidays, a travel experience arm offering curated group trips across the Himalayas and Andaman Islands, integrating accommodation with adventure tourism to increase customer retention and average spending.

- In January 2023, Base Backpackers launched its Work & Wander membership program in Australia, providing digital nomads with flexible monthly stays, high-speed internet, and event access to capture the growing remote work travel segment.

- In September 2023, Zostel opened a flagship property in Pokhara, Nepal, featuring a rooftop café, cultural exchange lounge, and guided trekking coordination, expanding its footprint into key South Asian tourist hubs.

- In February 2024, Hostelling International partnered with the University of Malaya to offer exclusive hostel rates and cultural immersion programs for international students, strengthening youth engagement in Southeast Asia.

MARKET SEGMENTATION

This research report on the global hostels market has been segmented and sub-segmented.

By Deployment

- Hybrid

- On-Premise

- Cloud

By Solution

- Channel Manager

- Production Reports

- Daily Activity Report

- Room Management

- Canteen Management

- Invoice Management

- Hostel Member Management

By Enterprise

- Small and Medium Enterprises

- Large Enterprises

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

1. What is the Hostels Market growth rate during the projection period?

The Global Hostels Market is expected to grow with a CAGR of 11.20% between 2025-2033.

2. What can be the total Hostels Market value?

The Global Hostels Market size is expected to reach a revised size of US$ 13.68 billion by 2033.

3. Name any three Hostels Market key players?

Hostelworld, Safestay plc, and RoomMaster are the three Hostels Market key players.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com