Global Injection Molding Market Size, Share, Trends & Growth Forecast Report By Type (Plastic, Rubber and Metal), Machine Type, End-Use Industry, Clamping Force, and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa), Industry Analysis (2026 to 2034)

Global Injection Molding Market Size

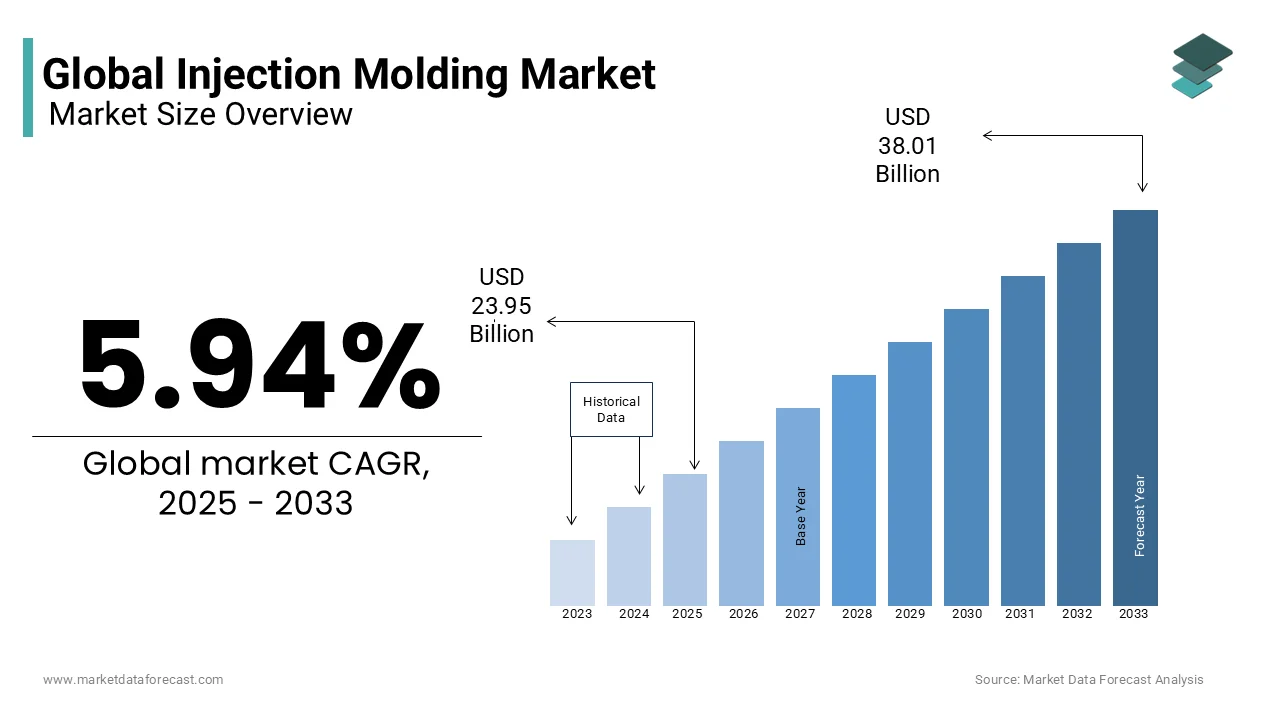

The global injection molding market size was valued at USD 23.95 billion in 2025. The global market is expected to be worth USD 25.37 billion in 2026 and USD 40.25 billion by 2034, growing at a CAGR of 5.94% from 2026 to 2034.

Injection Molding refers to the industrial process of manufacturing high-precision thermoplastic and thermoset components by injecting molten material into custom molds under high pressure, enabling mass production of complex geometries with tight tolerances. This technique is foundational in fabricating parts for automotive systems, medical devices, consumer electronics, and packaging. Injection molding is the single dominant plastic processing method. As per the U.S. Bureau of Labor Statistics, the plastics manufacturing sector employs around 605,750 workers for the year 2023. The process’s scalability, repeatability, and compatibility with engineering-grade polymers continue to solidify its role in high-volume manufacturing ecosystems.

MARKET DRIVERS

Proliferation of Lightweight Components in the Automotive Industry

The automotive sector’s shift toward lightweighting to enhance fuel efficiency and meet emissions standards has significantly amplified demand for injection-molded plastic components. Injection molding enables the production of structural components such as instrument panels, bumpers, and door modules with high dimensional accuracy and reduced assembly complexity. In electric vehicles (EVs), this demand intensifies. This consolidation reduces labor, welding, and material waste, making injection molding indispensable in next-generation automotive design.

Expansion of Medical Device Manufacturing with High-Precision Requirements

The medical technology sector increasingly relies on injection molding to produce sterile, biocompatible, and intricately designed disposable devices. Companies like B. Braun and Medtronic operate ISO 13485-certified molding lines that run 24/7 to meet global demand. Additionally, the World Health Organization estimates that 16 billion injections are administered annually worldwide, nearly all using plastic syringes produced via injection molding. The convergence of aging populations, rising surgical volumes, and infection control protocols ensures sustained growth in this high-value application segment.

MARKET RESTRAINTS

Environmental Regulations Restricting Single-Use Plastics

Stringent global policies targeting plastic waste are constraining the use of conventionally molded disposable products, particularly in packaging and consumer goods. In addition, California’s SB 54 legislation mandates that all plastic packaging be recyclable or compostable by 2032, compelling manufacturers to reengineer products and molds for alternative materials. As per the United Nations Environment Programme, only 9% of all plastic ever produced has been recycled, prompting governments to impose extended producer responsibility (EPR) schemes that increase operational costs for molders. These regulatory pressures are forcing injection molding firms to invest in redesign, material substitution, and closed-loop recycling systems, increasing complexity and capital burden.

Supply Chain Disruptions for Engineering Polymers

The injection molding industry is highly dependent on a stable supply of resins such as polycarbonate, ABS, and polypropylene, which are vulnerable to geopolitical and logistical disruptions. The 2021–2022 global shipping crisis led to resin price spikes rapidly, severely impacting small and medium-sized molders. These disruptions undermine production planning and erode profit margins, particularly for firms without long-term resin procurement agreements.

MARKET OPPORTUNITIES

Adoption of Industry 4.0 and Smart Molding Technologies

The integration of digitalization, real-time monitoring, and predictive maintenance in injection molding is unlocking new efficiency frontiers. Also, smart molding systems equipped with IoT sensors can reduce cycle times and scrap rates through adaptive process control. Companies like Sumitomo (SHI) Demag and Engel have introduced AI-driven molding platforms that autonomously adjust pressure, temperature, and cooling parameters based on real-time cavity feedback. Thus, injection molders adopting digital twins and cloud-based process analytics are positioning themselves for leadership in precision and sustainability.

Growth in Bioplastics and Sustainable Material Processing

The rising adoption of bio-based and biodegradable polymers is creating a transformative opportunity for injection molders to align with circular economy goals. According to the European Bioplastics Association, global production capacity of bioplastics reached 2.4 million metric tons in 2023, with polylactic acid (PLA) and polyhydroxyalkanoates (PHA) increasingly used in food packaging and medical applications. Injection molding parameters for these materials differ significantly from conventional resins, requiring specialized screw designs, temperature profiles, and drying systems. Many major brands have public commitments to increase recycled/renewable content by 2026. This shift is fostering innovation in mold design, material handling, and end-of-life compatibility.

MARKET CHALLENGES

High Capital Intensity and Technological Obsolescence

Establishing a competitive injection molding operation requires substantial investment in machinery, tooling, and skilled labor, creating barriers to entry and operational rigidity. Also, the average cost of a high-tonnage electric molding machine exceeds $500,000, with custom molds often costing between $50,000 and $200,000 depending on complexity. Small molders face particular challenges. In emerging markets, outdated hydraulic presses consume more energy than modern all-electric models. This capital burden limits agility, discourages innovation, and forces firms to operate at high capacity utilization just to maintain profitability, increasing vulnerability to demand fluctuations.

Workforce Skill Gaps in Advanced Molding Techniques

The transition to precision, automated, and digitally integrated molding systems is outpacing the availability of trained technicians and process engineers. The U.S. manufacturing sector faces substantial skilled-worker shortfalls and plastics processing is highlighted as impacted. Complex tasks such as mold flow analysis, cavity pressure sensing, and robotic integration require expertise that traditional apprenticeships are not adequately providing. Skills gaps in Industry 4.0 competencies among new plastics entrants are reported in Germany. This deficit leads to suboptimal machine utilization, higher defect rates, and delayed adoption of advanced technologies, undermining global competitiveness and innovation velocity in the sector.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.94% |

| Segments Covered | By Type, Machine, Clamping Force, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East & Africa |

| Market Leaders Profiled | Sumitomo Heavy Industries (Japan), Arburg (Germany), Nessei Plastic (Japan), Chen Hsong (China), Milacron (United States of America), The Japan Steel Works (Japan), Husky (Canada), Engel (Austria) and Haitian International (China) |

SEGMENTAL ANALYSIS

By Type Insights

The plastic segment dominated the injection molding market by capturing substantial share of total production volume in 2025. This dominance is because of the versatility, low density, and cost-efficiency of thermoplastics in high-volume manufacturing. Global plastics production is in the hundreds of millions of tonnes and injection molding is a major processing route. Engineering resins such as polycarbonate, ABS, and nylon are extensively used in automotive interiors, consumer electronics, and medical devices due to their durability and design flexibility. Modern vehicles use a substantial and growing share of plastic components. Additionally, the proliferation of single-use medical devices, over 16 billion syringes produced annually, as per the World Health Organization, relies almost entirely on plastic injection molding, reinforcing its entrenched position across critical industries.

The metal injection molding (MIM) segment is experiencing the most rapid expansion and is projected to grow at a CAGR of 12.6% from 2026 to 2034. This surge is driven by the rising demand for miniaturized, high-strength components in aerospace, medical implants, and precision electronics. MIM enables the production of complex metal parts, such as surgical instrument components and firearm triggers, with net-shape accuracy and minimal post-processing. MIM and powder-based metal processes are used for many small, complex implant parts. Surgical robotics is a multibillion market and MIM is used for small precision metal components. Furthermore, MIM is increasingly used for aerospace small components due to their dimensional consistency and material efficiency. These performance advantages are accelerating adoption beyond traditional machining.

By Machine Insights

The hydraulic injection molding machines segment remained the largest machine by holding an estimated 52.2% share of the global installed base in 2025. Their dominance is rooted in high clamping force capabilities, durability, and suitability for large-part molding in heavy industries. Hydraulic systems can generate forces exceeding 6,000 tons, making them ideal for producing automotive bumpers, industrial containers, and construction components. Additionally, the U.S. Department of Energy reports that hydraulic presses are preferred in rubber molding and thermoset processing, where consistent pressure maintenance over long cycles is critical. Despite higher energy consumption, more than electric models, their robustness and repairability ensure continued deployment, particularly in emerging markets with less access to precision maintenance infrastructure.

The all-electric injection molding machines segment is growing at the fastest pace, with a projected CAGR of 9.8% through 2034. This acceleration is fueled by their superior energy efficiency, precision, and compatibility with cleanroom environments. All-electric machines are substantially more energy-efficient than hydraulic units. Their servo-driven systems enable micron-level repeatability, essential for medical device manufacturing, where tolerances below ±0.01 mm are required. Companies like Sumitomo (SHI) Demag and Nissei have reported a year-on-year increase in orders for electric models, reflecting a structural shift toward sustainable, high-accuracy production systems.

By Clamping Force Insights

The 201–500 ton force segment commanded the injection molding market by representing a 45.1% of machine installations globally in 2025. This dominance is attributed to its optimal balance between processing capability and operational flexibility for mid-sized components. Machines in this range are widely used to produce automotive dashboards, electronic housings, and medium-capacity containers, which constitute the bulk of industrial molding output. India’s market shows strong demand for mid-range machines for automotive and consumer goods. This segment’s adaptability across industries and compatibility with both hydraulic and electric platforms solidify its central role in global manufacturing.

The above 500-ton force segment is expanding at the fastest rate and is projected to grow at a CAGR of 8.7% from 2026 to 2034. This growth is driven by the increasing production of large, structural components in the automotive and construction industries. High-tonnage machines are essential for molding car bumpers, instrument panels, and exterior cladding in a single shot, reducing assembly time and part count. Additionally, the construction sector’s adoption of molded composite panels for modular housing is further accelerating demand for large-format molding systems.

REGIONAL ANALYSIS

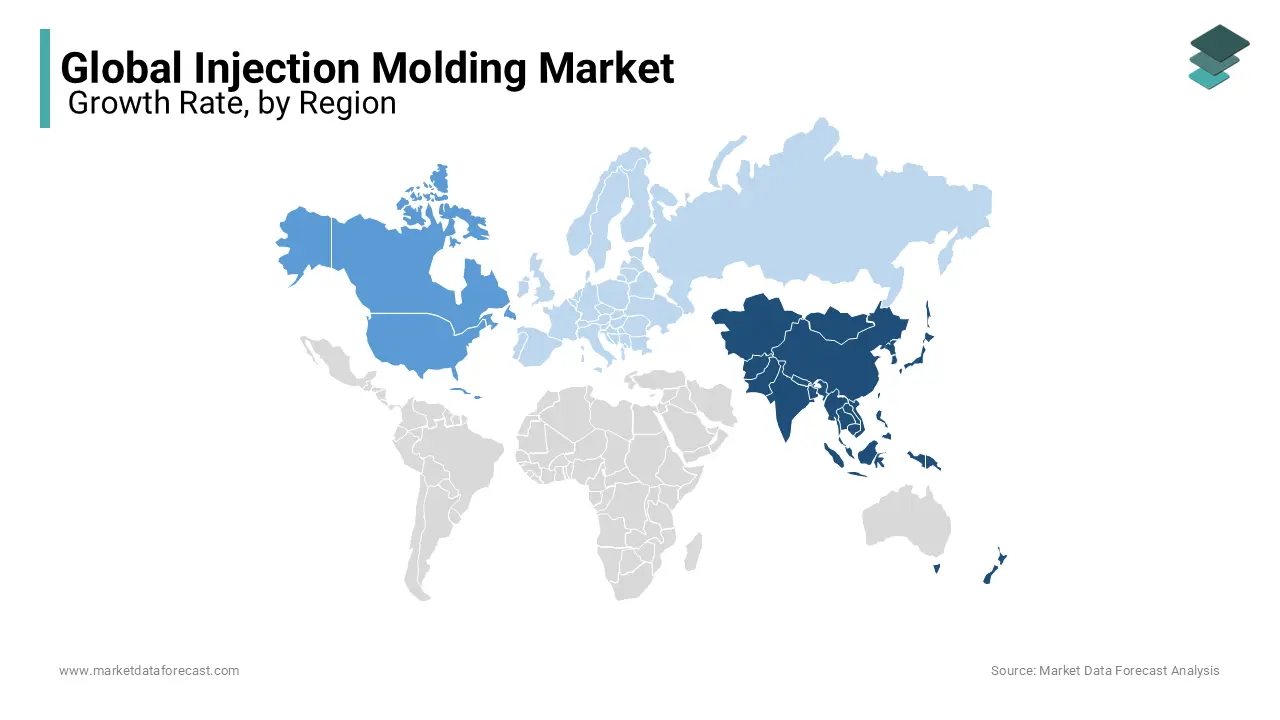

Asia Pacific Injection Molding Market Insights

Asia Pacific held the most significant position in the global injection molding market by accounting for 49.5% of total production value in 2026. The region’s lead position is anchored in its vast manufacturing ecosystem, particularly in electronics, automotive, and consumer goods. Japan and South Korea lead in high-precision molding for semiconductors and medical devices. India’s Make in India has boosted plastics and molding equipment imports. With ASEAN’s electronics exports surpassing $300 billion in 2023, as per the ASEAN Secretariat, the region remains the epicenter of injection molding activity.

Europe Injection Molding Market Insights

Europe holds a significant share of the global injection molding market, with a strong emphasis on high-value, precision manufacturing. Germany stands as the technological leader, hosting over 30% of Europe’s injection molding machinery manufacturers, including global players like Arburg and KraussMaffei. The German Engineering Federation confirms that German-made molding machines accounted for €1.8 billion in exports in 2023, primarily to North America and Asia. The EU’s Green Deal has accelerated the shift toward energy-efficient all-electric systems. Additionally, the European Medical Devices Regulation (MDR) has increased demand for ISO 13485-certified molding facilities, particularly in Ireland and the Netherlands. The region’s focus on automation, sustainability, and regulatory compliance ensures its continued influence in advanced molding applications.

North America Injection Molding Market Insights

North America accounts for a notable share of the global injection molding market, with the United States representing over 90% of regional output. The market is characterized by high automation levels and integration with Industry 4.0 technologies. Automotive and medical sectors dominate demand. Nearshoring trends have boosted domestic production; Mexico’s injection molding capacity grew from 2021 to 2023, driven by U.S. manufacturers relocating supply chains. The Inflation Reduction Act’s incentives for EV manufacturing are further stimulating demand for large-format molding systems in battery and structural components.

Latin America Injection Molding Market Insights

Latin America contributes modest share to the global injection molding market, according to the Inter-American Development Bank, with Brazil and Mexico leading industrial activity. Brazil hosts the largest domestic market. The country’s automotive production, drives demand for interior and exterior components. Mexico’s proximity to the U.S. has made it a hub for export-oriented molding. However, energy instability and limited access to advanced resins constrain growth. Despite challenges, public-private initiatives like Brazil’s “Plastics 4.0” program are promoting digitalization and sustainability, laying the foundation for future expansion.

Middle East Injection Molding Market Insights

The Middle East holds a small share of the global injection molding market, with Saudi Arabia and the UAE driving industrial transformation. The region’s growth is fueled by economic diversification initiatives such as Saudi Vision 2030. The Saudi Plastics Council confirms that domestic plastics processing capacity has doubled since 2018, with new industrial zones in Jubail and Ras Al-Khair hosting integrated molding facilities. The UAE’s Dubai Industrial Strategy 2030 aims to increase manufacturing’s contribution to GDP to 25%, prioritizing high-tech molding for aerospace and healthcare. The Emirates Authority for Standardization and Metrology has introduced strict quality benchmarks, encouraging adoption of precision molding systems. With petrochemical feedstocks locally available and government-backed industrial parks expanding, the Middle East is emerging as a strategic molding hub in the global supply chain.

COMPETITIVE LANDSCAPE

The injection molding market features a highly fragmented yet technologically stratified competitive landscape, where global OEMs coexist with regional specialists. Competition is increasingly defined by innovation in energy efficiency, process accuracy, and digital integration rather than price alone. German and Japanese manufacturers lead in high-end all-electric and precision systems, while Chinese firms dominate the mid-tier hydraulic segment with cost-competitive models. The rise of Industry 4.0 has intensified the race to embed IoT, AI-driven process control, and predictive maintenance into machine platforms. Regional service networks, application expertise, and compliance with environmental regulations are becoming critical differentiators. Emerging players are leveraging partnerships and localized production to challenge established brands, creating a dynamic environment where technological agility and customer support determine long-term market positioning.

KEY MARKET PLAYERS

Companies playing a significant role in the global injection molding market include

-

Sumitomo Heavy Industries (Japan)

-

Arburg (Germany)

-

Nissei Plastic Industrial (Japan)

-

Chen Hsong (China)

-

Milacron (United States of America)

-

The Japan Steel Works (Japan)

-

Husky (Canada)

-

Engel (Austria)

-

Haitian International (China)

TOP PLAYERS IN THE MARKET

- Mitsubishi has established a dominant engineering presence in the Asia Pacific injection molding sector through its high-precision, energy-efficient molding machines tailored for automotive and electronics manufacturing. The company’s ALL-ELECTRIC and hybrid models are widely adopted in Japan, South Korea, and Thailand for their repeatability and low maintenance requirements. It expanded its technical support network in Vietnam and Indonesia to serve fast-growing electronics exporters. Collaborations with local partners in India have enabled customized molding solutions for medical device manufacturers complying with international regulatory standards. Its focus on reducing energy consumption by up to 40% compared to hydraulic systems aligns with regional sustainability mandates, reinforcing its reputation as a technology-forward supplier in precision molding applications.

- Nissei has carved a niche in the Asia Pacific market by specializing in ultra-precision injection molding systems for optical components, medical devices, and semiconductor packaging. The company’s machines are instrumental in producing lenses for smartphone cameras and endoscopic equipment, where micron-level accuracy is critical. The company strengthened its foothold in China by establishing a training center in Suzhou to support local operators in mastering scientific molding techniques. It also partnered with Japanese medical device firms to develop cleanroom-compliant molding lines for disposable diagnostics. With over 50 years of process expertise, Nissei continues to lead in niche, high-value applications that demand exceptional stability and precision, setting it apart in a competitive landscape.

- Sumitomo (SHI) Demag has solidified its influence across Asia Pacific through a combination of advanced all-electric technology and localized service infrastructure. Its machines are widely deployed in automotive and consumer electronics manufacturing hubs in China, India, and Thailand, where energy efficiency and process consistency are paramount. It also launched the IntElect Series in Japan, achieving a 25% reduction in energy use while maintaining high cavity pressure accuracy. Collaborations with local universities in South Korea and Malaysia have accelerated workforce training in smart molding practices. By emphasizing digitalization, sustainability, and regional responsiveness, Sumitomo (SHI) Demag has positioned itself as a forward-thinking partner for manufacturers navigating technological transformation in high-volume production environments.

TOP STRATEGIES USED BY KEY MARKET PLAYERS

Key players in the injection molding market are prioritizing technological differentiation, regional localization, and digital integration to strengthen their competitive edge. Companies are investing heavily in all-electric and hybrid machine development to meet energy efficiency mandates and precision requirements in medical and electronics sectors. Strategic expansions into high-growth regions like Southeast Asia are being executed through local manufacturing, service centers, and training facilities. Partnerships with automation providers and software developers are enabling end-to-end smart factory solutions. Firms are also focusing on sustainability by optimizing machine energy consumption and supporting circular economy initiatives through recyclable material processing. Additionally, customer-centric innovation, including modular machine designs and remote diagnostics, is enhancing operational flexibility and after-sales engagement across diverse industrial applications.

RECENT HAPPENINGS IN THE MARKET

- In February 2022, Mitsubishi Heavy Industries Plastic Technology launched the NeoElectric Series of all-electric injection molding machines with integrated IoT sensors, enhancing process monitoring and energy efficiency for electronics manufacturers in Southeast Asia.

- In July 2022, Nissei Plastic Industrial opened a technical training center in Suzhou, China, to support local medical device producers in adopting precision molding techniques and complying with international quality standards.

- In November 2022, Sumitomo (SHI) Demag inaugurated a smart molding demonstration center in Singapore, showcasing automated, data-driven production cells tailored for high-mix manufacturing in the Asia Pacific region.

- In March 2023, Arburg established a new service hub in Pune, India, to expand its support network for automotive and consumer goods manufacturers adopting high-precision electric molding systems.

- In September 2023, Engel launched the ENGEL e-motion 1050, a large-tonnage all-electric press, targeting EV component producers in Germany and China, reinforcing its position in sustainable, high-performance molding solutions.

MARKET SEGMENTATION

This research report on the global injection molding market has been segmented and sub-segmented based on type, machine, clamping force, and region.

By Type

- Plastics

- Rubber

- Metal

- Ceramic

- Others

By Machine

- Hydraulic

- All-electric

- Hybrid

By Clamping Force

- 0-200 Ton Force

- 201-500 Ton Force

- Above 500 Ton Force

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

1. What is the injection molding market?

It involves the manufacturing of products by injecting molten material into molds, widely used for plastics, metals, and other materials.

2. What is driving the growth of the injection molding market?

High demand from packaging, automotive, medical devices, consumer goods, and electronics industries.

3. Which material dominates the injection molding market?

Plastics hold the largest share due to their cost-effectiveness and wide application scope.

4. What are the main applications of injection molding?

Packaging, automotive components, electronics, household goods, medical equipment, and construction products.

5. Which region leads the global injection molding market?

Asia-Pacific dominates, driven by large-scale manufacturing and high plastic consumption.

6. What technological trends are influencing the injection molding market?

Automation, 3D printing integration, micro-molding, and the use of recycled & bio-based materials.

7. What challenges does the injection molding industry face?

High tooling costs, environmental concerns over plastic waste, and fluctuations in raw material prices.

8. Who are the major players in the injection molding market?

Key players include ENGEL, Arburg, Sumitomo Heavy Industries, Husky Injection Molding Systems, and Haitian International.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com