Latin America Automated Material Handling Market Size, Share, Growth, Trends, And Forecast Research Report, Segmented By Product, Equipment, End-User, And Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC), Industry Analysis From (2025 to 2033)

Latin America Automated Material Handling Market Size

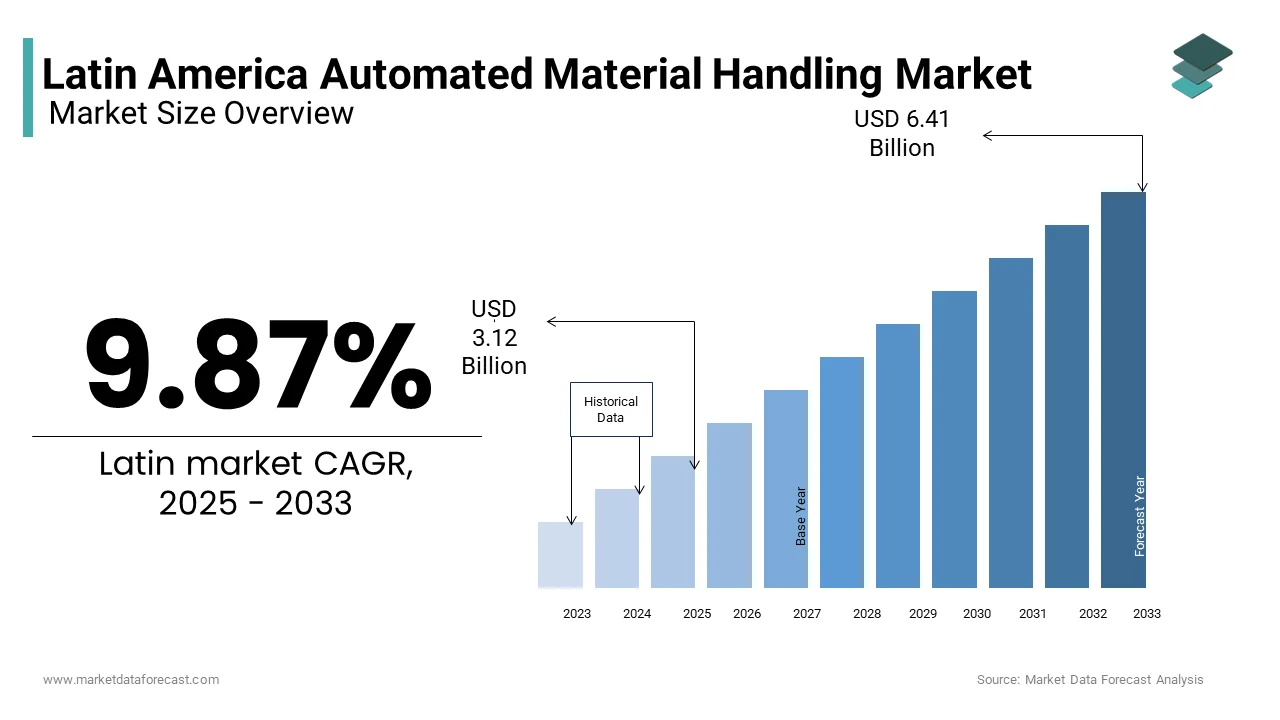

The Latin America automated material handling market size was valued at USD 2.84 billion in 2024 and is anticipated to reach USD 3.12 billion in 2025 to USD 6.41 billion by 2033, growing at a CAGR of 9.87% during the forecast period from 2025 to 2033.

The automated material handling is a range of technologically advanced systems, including automated guided vehicles (AGVs), conveyor networks, robotic palletizers, and automated storage and retrieval systems (AS/RS). According to the International Federation of Robotics, Brazil alone installed 2,850 industrial robots in 2022, reflecting a growing appetite for automation in production and warehousing.

MARKET DRIVERS

Expansion of E-Commerce and Last-Mile Fulfillment Infrastructure

The rapid growth of online retail is compelling logistics operators to modernize warehousing and distribution networks is majorly driving the growth of the Latin America automated material handling market. This surge has intensified pressure on fulfillment centers to process orders faster and with fewer errors. Mercado Libre, the region’s largest e-commerce platform, has invested over $2 billion since 2020 in automated fulfillment centers across the region, including its robotic warehouse in São Paulo that uses Kiva-style robots to reduce picking time by 60%. In Mexico, logistics operators report a 40% increase in demand for automated sortation systems between 2021 and 2023, as per the Mexican Association of Logistics.

Industrial Modernization and Government-Led Smart Manufacturing Initiatives

The national industrial strategies aimed at enhancing productivity and global competitiveness are accelerating automation in manufacturing and warehousing, which is bolstering the growth of the Latin American automated material handling market. According to the Brazilian Confederation of Industry (CNI), 34% of large manufacturers have integrated robotics into their assembly and logistics workflows, a 12% increase from 2020. These policy-driven efforts are fostering a culture of technological adoption, particularly in automotive, pharmaceutical, and food processing sectors that require high-throughput, error-free material movement.

MARKET RESTRAINTS

High Upfront Capital Costs and Limited Access to Financing

The acquisition and integration of automated material handling systems require substantial initial investment is restraining the growth of the Latin America automated material handling market. In Colombia, only 18% of logistics firms have secured financing for automation projects, as reported by the National Association of Industrialists (ANDI). Leasing models remain underdeveloped, and local banks are hesitant to finance unproven technologies. This financial constraint is particularly acute in countries like Bolivia and Paraguay, where institutional lending for industrial tech is minimal.

Shortage of Skilled Workforce for System Integration and Maintenance

The lack of technical expertise required for installation, programming, and ongoing maintenance is hindering the growth of the Latin American automated material handling market. According to the OECD Skills Outlook 2023, only 22% of vocational training programs in Latin America include robotics or industrial automation curricula. In Peru, the Ministry of Education estimates a shortfall of 15,000 automation technicians by 2025. This gap forces companies to rely on foreign engineers for system commissioning, increasing costs and downtime.

MARKET OPPORTUNITIES

Growth of Free Trade Zones and Export-Oriented Logistics Hubs

The special economic zones and export-processing corridors are emerging as hotspots due to their focus on efficiency, customs compliance, and international standards, which are expected to create new opportunities for the Latin American automated material handling market. According to the United Nations Conference on Trade and Development, Latin America hosts over 200 free trade zones, with major clusters in Panama, the Dominican Republic, and northern Mexico. These zones serve as gateways for global supply chains, handling high-value electronics, pharmaceuticals, and automotive parts that require precise inventory tracking and rapid throughput. In Mexico’s Apodaca FTZ, logistics operators have deployed automated conveyors and RFID-based sorting systems to achieve 99.8% order accuracy, as reported by the National Free Zone Association. Similarly, in Costa Rica’s free zones, companies like Intel and HP have integrated robotic palletizing and AGVs to streamline export logistics.

Rising Adoption of Modular and Scalable Automation Solutions

The emergence of flexible, plug-and-play automation systems is enabling smaller warehouses and mid-tier manufacturers to adopt material handling technologies without large-scale infrastructure overhauls. This attribute is also to enhance the growth of the Latin America automated material handling market. Companies like Geek+ and KUKA have introduced compact robotic fleets that can be deployed in under 72 hours, reducing implementation complexity. In Argentina, logistics firm Grupo Logístico QA implemented a mobile robot system in its Buenos Aires warehouse, achieving a 50% reduction in picking errors and a 30% increase in throughput. These systems are particularly suited to e-commerce fulfillment centers with fluctuating demand cycles. Additionally, cloud-based warehouse execution systems (WES) allow remote monitoring and scaling by making automation accessible to firms without in-house IT infrastructure, thereby broadening the market beyond multinational corporations.

MARKET CHALLENGES

Integration Complexity with Legacy Systems and IT Infrastructure

Many industrial and logistics facilities operate on outdated warehouse management systems (WMS) and enterprise resource planning (ERP) platforms, by complicates the integration of modern automation technologies, which is to impede the growth of the Latin America automated material handling market. In Chile, a 2023 survey by the Logistics Chamber of Commerce found that 45% of companies delayed automation projects due to compatibility issues with existing software. Retrofitting legacy facilities with sensors, network connectivity, and data synchronization tools often requires costly custom engineering. Moreover, inconsistent internet reliability in rural and peri-urban areas disrupts cloud-based automation coordination.

Regulatory Fragmentation and Lack of Standardization Across Countries

The absence of harmonized technical and safety regulations for automation equipment across Latin American nations impedes cross-border deployment and discourages multinational suppliers from standardizing offerings, and additionally inhibits the growth of the Latin American automated material handling market. According to the Pan American Standards Commission (COPANT), only 12 of 20 Latin American countries have adopted IEC 61508 or ISO 13849 safety standards for industrial automation, creating compliance uncertainty. In countries like Ecuador and Honduras, import certification for robotic systems can take over 10 months, compared to 3–4 months in Mexico or Brazil, as reported by the Latin American Robotics Association. This fragmentation increases lead times and costs for equipment suppliers and end-users alike.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 9.87% |

| Segments Covered | By Product, Equipment, End-User Country |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | Brazil, Mexico, Argentina, Chile, Colombia, Peru |

| Market Leaders Profiled | Daifuku Co. Ltd, KUKA AG, SSI Schafer, Interroll Group, Kardex Group, KION Group, Columbus McKinnon Group, BEUMER Group GmbH & Co. KG. |

SEGMENTAL ANALYSIS

By Product Insights

The Hardware segment accounted in holding a dominant share of the Latin America automated material handling market in 2024, with the foundational need for physical systems such as conveyors, robotic arms, automated storage units, and mobile robots to enable operational transformation. According to the Brazilian Automation and Robotics Society (SBR), over 78% of automation investments in manufacturing and logistics are allocated to equipment procurement rather than software or services. Additionally, free trade zones in Central America are prioritizing hardware deployment to meet North American supply chain efficiency standards.

The Software segment is projected to grow at a CAGR of 10.3% in the coming years, with the increasing recognition that automation efficacy depends on intelligent control systems, real-time data analytics, and integration with enterprise platforms. Companies like Mercado Libre have deployed proprietary AI-driven orchestration software to coordinate thousands of robots across their fulfillment centers. Furthermore, modular software platforms now allow mid-sized operators to scale automation incrementally.

By Equipment Insights

The Automated Conveyor segment held 34.3% of the Latin America automated material handling market share in 2024, with the widespread use of conveyor systems in manufacturing assembly lines, food processing plants, and parcel sorting facilities where continuous, high-volume movement is essential. In Mexico’s automotive sector, which produces over 3.5 million vehicles annually, as reported by the Mexican Automotive Industry Association (AMIA), conveyors form the backbone of just-in-time production workflows. The technology’s maturity, reliability, and compatibility with legacy infrastructure make it a preferred choice for initial automation upgrades. Moreover, integration with barcode scanners and RFID systems enhances traceability in regulated industries such as pharmaceuticals and perishable goods.

The Mobile Robots segment is projected to grow with a CAGR of 14.6% during the forecast period, with the flexibility, scalability, and rapid deployment capabilities of autonomous mobile robots (AMRs) in dynamic environments such as e-commerce fulfillment centers and distribution hubs. According to ECLAC, same-day delivery expectations have increased by 52% across major Latin American cities since 2020, compelling logistics operators to adopt goods-to-person robotics.

By End-User Vertical Insights

The Retail/Warehousing/Distribution Centers/Logistic Centers vertical segment was the largest and held 41.3% of the share in 202,4 with the explosive growth of e-commerce and the need for high-speed, error-free order fulfillment. According to Mercado Libre, the region’s largest online marketplace, parcel volumes surged by 38% in 2023, necessitating automated sortation, conveyors, and robotic picking systems. Similarly, in Chile, Falabella’s distribution hub in Maipú uses automated conveyors and RFID tracking to achieve 99.5% inventory accuracy. The pressure to reduce delivery times to under 24 hours in urban centers has made automation a strategic imperative.

The Airport vertical is projected to expand at a CAGR of 11.8% during the forecastperiodd with the increasing air cargo volumes and the need for secure, efficient baggage and freight handling. According to the International Air Transport Association (IATA), Latin America’s air cargo traffic grew by 9.3% in 2023, reaching 5.7 million metric tons. Major hubs like São Paulo-Guarulhos and Mexico City International Airport are modernizing baggage handling systems with automated conveyors and RFID tagging to reduce misrouted luggage, which declined by 22% post-automation at Bogotá’s El Dorado Airport, as reported by Aerocivil Colombia. Additionally, e-commerce-driven express freight is increasing demand for automated cargo sorting and palletization. Panama’s Tocumen International Airport has invested $120 million in an automated cargo terminal to serve as a regional logistics gateway.

COUNTRY-LEVEL ANALYSIS

Brazil was the top performer in the Latin American automated material handling market by capturing 39.3% of share in 2024. The country’s "Indústria 4.0" initiative has incentivized over 1,200 factories to integrate robotics and smart logistics systems since 2019. According to the National Service for Industrial Training (SENAI), Brazil installed 2,850 industrial robots in 2022, the highest in Latin America. Major e-commerce players like Magazine Luiza and logistics operators such as Jadlog have deployed mobile robots and automated sortation systems to meet rising delivery demands. Additionally, ports in Santos and Rio de Janeiro are upgrading cargo handling with automated cranes and conveyors.

Mexico was positioned second by holding 28.3% of share in 202,4, with its strategic proximity to the U.S., robust manufacturing base, and integration into USMCA trade agreements have made it a focal point for automated logistics and production systems. The automotive sector alone accounts for over 40% of industrial robot installations, according to the National Institute of Statistics and Geography (INEGI). Companies like BMW, Ford, and Tesla suppliers in Nuevo León and Jalisco rely on automated conveyors and robotic palletizers for precision assembly. In logistics, free trade zones along the U.S. border are deploying automated warehouses to expedite cross-border shipments. Amazon operates a fully automated fulfillment center in Apodaca, utilizing Kiva-style robots. Argentina's automated material handling market growth is likely to be driven by the advancing automation in select high-value sectors such as pharmaceuticals, food processing, and logistics. In Buenos Aires, Grupo Logístico QA implemented a mobile robot fleet in its primary distribution center, improving order accuracy and reducing labor costs. The Ministry of Productive Innovation supports automation through tax incentives under its "Productive Innovation 2030" program.

KEY MARKET PLAYERS

Daifuku Co., Ltd, KUKA AG, SSI Schafer, Interroll Group, Kardex Group, KION Group, Columbus McKinnon Group, and BEUMER Group GmbH & Co. KG are the market players that are dominating the Latin America automated material handling market.

Top Players in the Market

KUKA AG

KUKA has established a strong foothold in Latin America through its industrial robotics and automated guided vehicle (AGV) solutions in the automotive and manufacturing sectors. The company has expanded its regional presence by partnering with local system integrators in Brazil and Mexico to deliver turnkey automation projects. In 2023, KUKA launched a regional training center in Querétaro, Mexico, to upskill engineers in robotic integration and maintenance, addressing the region’s technical talent gap. Its flexible production cells and mobile robotics are increasingly deployed in tier-one supplier plants serving North American markets.

Daifuku Co., Ltd.

Daifuku has extended its global material handling expertise into Latin America, focusing on high-throughput automated storage and retrieval systems (AS/RS) and conveyor networks for logistics and airport applications. The company has executed major installations in Chile’s retail distribution centers and Colombia’s international airports, where its automated baggage handling systems have improved sorting accuracy and reduced processing time. In 2022, Daifuku partnered with a leading e-commerce fulfillment operator in Brazil to deploy a shuttle-based storage system capable of handling 10,000 orders per day. Its solutions are tailored to Latin American infrastructure constraints, incorporating robust controls for variable power and environmental conditions. Daifuku also provides remote monitoring services from its regional support hub in Panama by ensuring rapid response.

SSI Schäfer

SSI Schäfer has strengthened its presence in Latin America by delivering integrated warehouse automation solutions for retail, pharmaceutical, and third-party logistics providers. The company’s modular shuttle systems, pallet racking, and warehouse management software are deployed in major distribution centers across Argentina, Chile, and Peru. In 2023, SSI Schäfer completed an automated fulfillment center for a leading pharmacy chain in Santiago, incorporating goods-to-person stations and AI-driven inventory control. The company has also localized service operations by establishing technical support teams in Bogotá and São Paulo, reducing deployment timelines and improving after-sales responsiveness. Its partnership with regional integrators enables faster project execution and compliance with local safety standards.

Top Strategies Used by Key Market Participants

Key players in the Latin America automated material handling market are leveraging strategies such as localized service networks, strategic partnerships with system integrators, modular and scalable system designs, digital twin modeling for deployment planning, and direct engagement with government industrial modernization programs. Companies are investing in regional training centers to build technical capacity and ensure post-installation support. Collaborations with e-commerce platforms and logistics operators enable tailored automation solutions for high-velocity fulfillment. Firms are also offering hybrid financing models, including leasing and pay-per-use options, to lower entry barriers. Integration of AI-driven warehouse execution software enhances real-time decision-making.

COMPETITION OVERVIEW

Competition in the Latin American automated material handling market is intensifying as global technology leaders, regional integrators, and emerging local engineering firms compete for dominance across fragmented national markets. While multinational corporations like KUKA and Daifuku bring advanced engineering and global track records, regional players are gaining traction through cost-effective, adaptable solutions and faster deployment cycles. The absence of dominant homegrown automation champions has created opportunities for strategic alliances between foreign vendors and local partners. Differentiation increasingly hinges on after-sales support, integration speed, and system resilience in challenging environments. Regulatory variation, infrastructure disparities, and capital constraints further shape competitive dynamics.

RECENT HAPPENINGS IN THE MARKET

- In June 2023, KUKA inaugurated a robotics training and innovation center in Querétaro, Mexico, to enhance local engineering capabilities and support the deployment of automated guided vehicles in automotive manufacturing facilities.

- In February 2024, Daifuku implemented an automated baggage handling system at El Dorado International Airport in Bogotá, which is improving sorting efficiency and reducing luggage misrouting by 25% in the first quarter of operation.

- In September 2023, SSI Schäfer completed the installation of a fully automated shuttle-based warehouse for a major pharmaceutical distributor in Santiago, Chile by enabling 99.8% inventory accuracy and 40% faster order fulfillment.

- In January 2024, Swisslog partnered with a Brazilian e-commerce logistics provider to deploy over 200 autonomous mobile robots in a new fulfillment center near São Paulo, which is scaling same-day delivery capacity by 60%.

- In May 2023, Honeywell Intelligrated launched a regional support hub in Panama City by offering remote monitoring and predictive maintenance services for automated conveyor systems across Central and South America.

MARKET SEGMENTATION

This research report on the Latin America automated handling market is segmented and sub-segmented into the following categories.

By Product Type

- Hardware

- Software

- Services

By Equipment Type

- Mobile Robots

- Automated Guided Vehicle (AGV)

- Automated Forklift

- Automated Tow/Tractor/Tug

- Unit Load

- Assembly Line

- Special Purpose

- Automated Guided Vehicle (AGV)

- Autonomous Mobile Robots (AMR)

- Laser Guided Vehicle

- Automated Storage and Retrieval System (ASRS)

- Fixed Aisle (Stacker Crane + Shuttle System)

- Carousel (Horizontal Carousel + Vertical Carousel)

- Vertical Lift Module

- Automated Conveyor

- Belt

- Roller

- Pallet

- Overhead

- Palletizer

- Conventional (High Level + Low Level)

- Robotic

- Sortation System

By End-user Vertical

- Airport

- Automotive

- Food and Beverage

- Retail/Warehousing/ Distribution Centers/Logistic Centers

- General Manufacturing

- Pharmaceuticals

- Post and Parcel

- Other End Users

By Country

- Brazil

- Argentina

- Mexico

- Colombia

- Peru

- Chile

- Rest of Latin America

Frequently Asked Questions

What is automated material handling?

It involves using technology like conveyors, AGVs, and robotics to move goods in warehouses and factories.

Why is this market growing in Latin America?

E-commerce, manufacturing growth, and supply chain modernization are driving demand.

Which countries lead in adoption?

Brazil and Mexico are front-runners due to larger industrial bases and foreign investment.

What industries use these systems most?

Retail, e-commerce, automotive, and food & beverage sectors rely heavily on automation.

Are small businesses adopting automation too?

Yes, as modular and scalable systems become more affordable.

What are the main challenges?

High initial costs and limited technical expertise can slow adoption.

How important is robotics in this market?

Robotics is becoming key, especially for order picking and palletizing.

Are local companies building these systems?

Some regional firms offer integration and maintenance services.

How is technology changing the market?

AI, IoT, and real-time data are making systems smarter and more adaptive.

What’s the future of automation in Latin America?

Growth will continue as more companies seek resilience and speed.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com