Latin America Pharmaceutical Products CMO Market Size, Share, Trends & Growth Forecast Report - Segmented By Application (Active Pharmaceutical Ingredient (API) Manufacturing, Finished Dosage Formulation (FDF) Development and Manufacturing), and Country (The United States, Canada and Rest of North America), Industry Analysis From 2026 to 2034

Latin America Pharmaceutical Products CMO Market Size

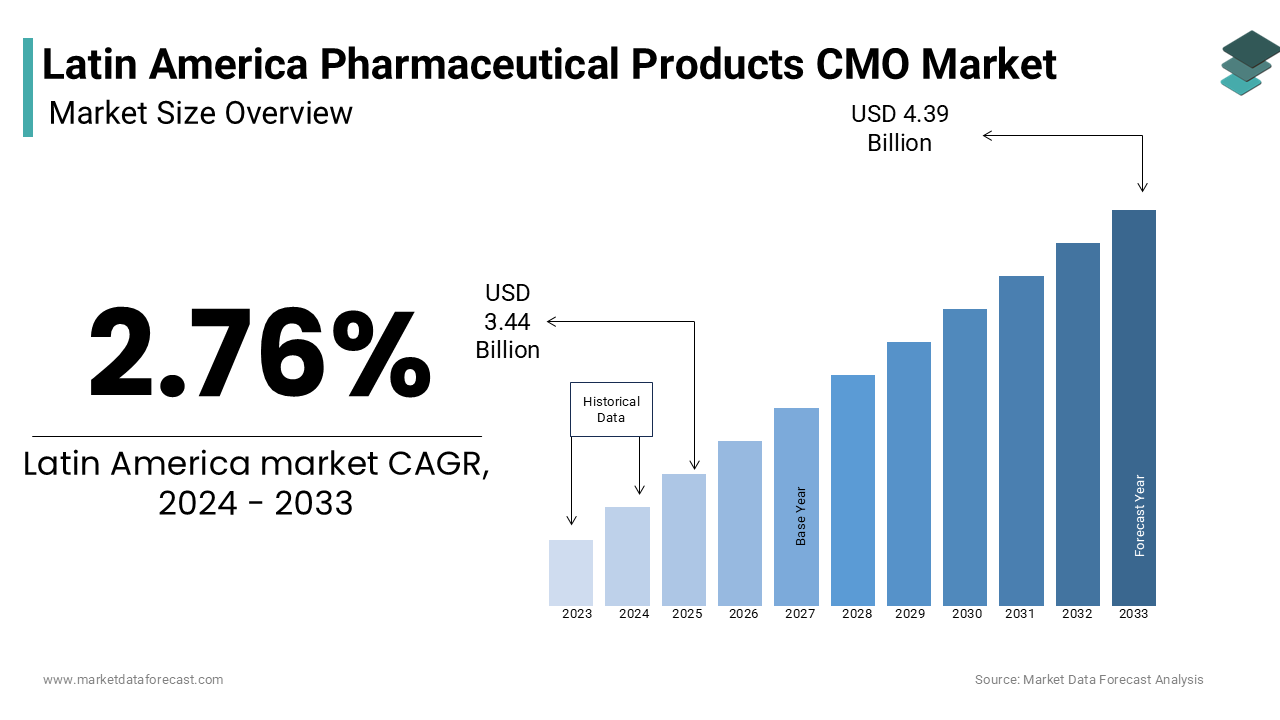

The Latin America pharmaceutical products CMO market size was valued at USD 3.53 billion in 2025 and is anticipated to reach USD 3.63 billion in 2026 from USD 4.51 billion by 2034, growing at a CAGR of 2.76% during the forecast period from 2026 to 2034.

The pharmaceutical products CMO market refers to the network of contract manufacturing organizations engaged in the development, formulation, and production of finished dosage forms, active pharmaceutical ingredients (APIs), and intermediates on behalf of biopharmaceutical firms across the region. These entities operate under strict regulatory compliance frameworks, providing end-to-end services ranging from clinical trial material production to commercial-scale manufacturing. As per the Pan American Health Organization, Latin America imports a notable share of its essential medicines, exposing systemic vulnerabilities in local supply chains. This gap has intensified demand for qualified CMOs capable of delivering high-quality, cost-efficient manufacturing solutions, particularly as governments push for greater self-reliance in medicine production amid recurring global supply disruptions.

MARKET DRIVERS

The rising demand for localized drug manufacturing to reduce dependency on imports is a primary driver of growth in the Latin America pharmaceutical products CMO market. In Brazil, local contract manufacturers produced a substantial number of doses of generics and biosimilars annually. This shift is further reinforced by Mercosur’s harmonization of GMP inspections, enabling regional CMOs to serve multiple markets with a single compliance framework, thereby enhancing scalability and operational efficiency.

The expansion of biosimilars and specialty drug production, which requires advanced manufacturing infrastructure that many originator companies lack in-house, is another critical demand driver. Also, biosimilars account for a significant share of monoclonal antibody prescriptions in Brazil and Mexico, driven by public health cost-containment strategies. This surge has prompted multinational pharmaceutical firms to outsource production to specialized CMOs with bioreactor capacities and regulatory expertise. Also, investment in biomanufacturing CMOs has grown annually, reflecting sustained institutional confidence in outsourced biologic production.

MARKET RESTRAINTS

The scarcity of regulatory harmonization across national agencies, which complicates multi-country manufacturing and distribution, is a major restraint in the Latin America pharmaceutical products CMO market. As per the Pan American Health Organization, while Brazil’s ANVISA, Mexico’s COFEPRIS, and Argentina’s ANMAT have made progress in adopting ICH guidelines, significant discrepancies remain in inspection timelines, dossier requirements, and post-approval changes. This fragmentation increases compliance costs and delays market entry, discouraging investment from global CMOs. Additionally, frequent policy shifts, such as Argentina’s 2022 requirement for local clinical validation of imported generics—further destabilize long-term planning and contract stability.

Limited access to capital for technology upgrades remains a systemic barrier for regional CMOs seeking to meet international quality benchmarks. In contrast, Indian and Chinese CMOs benefit from government subsidies and export incentives that exceed $2 billion annually. Without similar support, Latin American CMOs struggle to attract high-value contracts from global biopharma firms, remaining confined to low-margin generic production and limiting their ability to transition into complex formulations or sterile manufacturing segments.

MARKET OPPORTUNITIES

The development of regional vaccine and mRNA-based therapeutic manufacturing hubs, catalyzed by pandemic-driven health sovereignty initiatives is one significant opportunity. As per the Coalition for Epidemic Preparedness Innovations (CEPI), Brazil and Argentina were designated as regional vaccine production centers under the WHO’s mRNA Technology Transfer Hub program in 2022. These initiatives position regional CMOs as strategic partners in next-generation medicine production, opening access to high-growth therapeutic platforms.

Another emerging opportunity is the integration of digital twins and AI-driven process optimization in pharmaceutical manufacturing, enabling CMOs to enhance efficiency and regulatory compliance. Chile’s regulatory agency, ISP, has begun accepting AI-generated process validation data for certain sterile products, signaling regulatory openness to advanced manufacturing paradigms. Companies are already deploying machine learning models to predict lyophilization cycle outcomes and optimize formulation stability, setting new benchmarks for quality and speed. This technological leap offers regional CMOs a competitive edge in attracting global outsourcing contracts.

MARKET CHALLENGES

A persistent challenge is the shortage of skilled pharmaceutical engineers and regulatory affairs professionals capable of managing complex CMO operations. Like, Latin America has fewer certified pharmaceutical manufacturing scientists compared to that in Western Europe. Also, CMOs in Mexico and Colombia face delays in regulatory submissions due to insufficient in-house expertise. Training programs remain underfunded, with only some universities in the region offering specialized courses in biopharmaceutical process engineering. This human capital gap undermines quality assurance, prolongs approval timelines, and limits the ability of CMOs to adopt advanced manufacturing technologies at scale.

Geopolitical and macroeconomic instability continues to disrupt investment planning and supply chain continuity for pharmaceutical CMOs across Latin America. Like, inflation in Argentina remained significantly high in 2024, while the Argentine peso depreciated notably against the U.S. dollar, drastically increasing the cost of importing critical raw materials and bioreactors. In Venezuela, hyperinflation and capital controls have halted all foreign direct investment in pharmaceutical manufacturing since 2021. These economic volatilities erode profit margins, discourage long-term contracts, and deter multinational CMOs from establishing regional production bases, thereby constraining the sector’s growth potential and technological advancement.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 2.76% |

| Segments Covered | By Services Type and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | Brazil, Mexico, Argentina, Chile, and the Rest of Latin America. |

| Market Leaders Profiled | Catalent Inc., Boehringer Ingelheim Group, Pfizer CentreSource, Thermo Fisher Scientific (Patheon), Acino International AG, Lonza Group AG, Famar SA, Baxter Biopharma Solutions, BASF SE, Bayer AG, F. Hoffmann-La Roche Ltd., Merck & Co., Inc., Novartis AG, Pisa Farmacéutica, Fresenius SE & Co. KGaA, Takeda Pharmaceutical Company Limited, Ferring Pharmaceuticals Inc., Landsteiner Scientific. |

SEGMENTAL ANALYSIS

By Service Type Insights

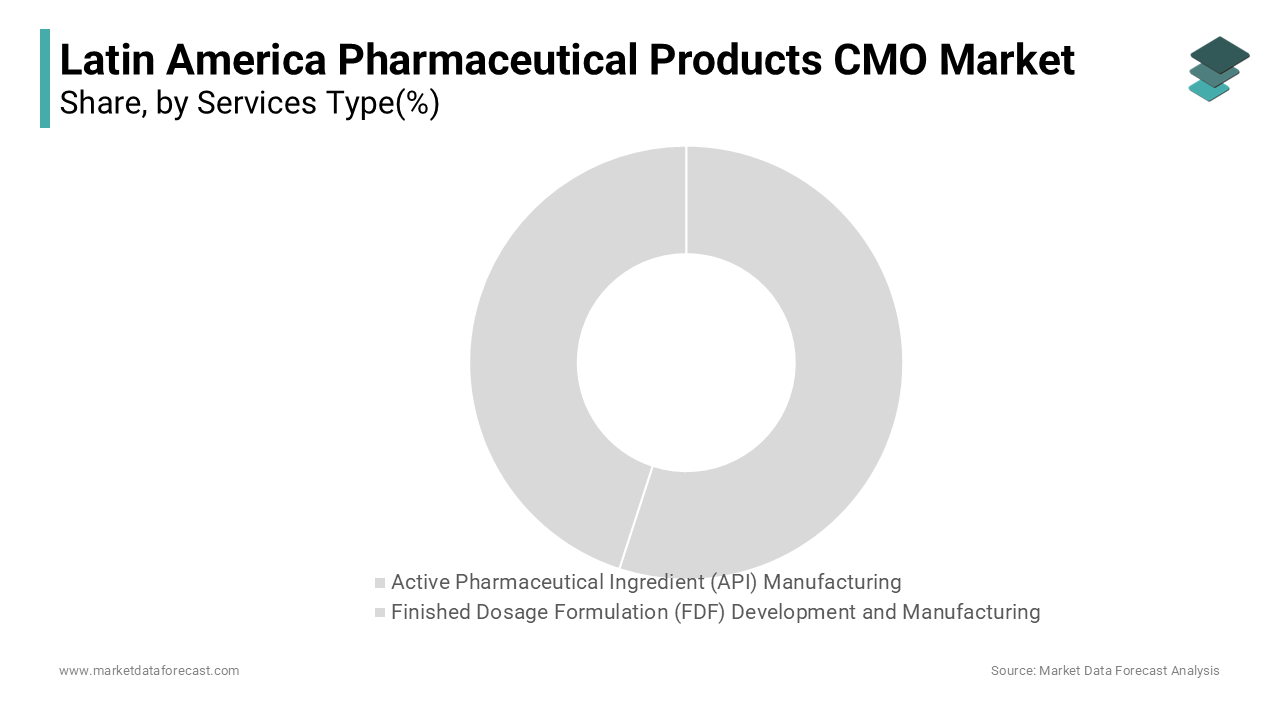

The Finished Dosage Formulation (FDF) Development and Manufacturing segment was the largest part in the Latin America pharmaceutical products CMO market by capturing a 57.3% of total revenue in 2024. This dominance is primarily driven by the region’s strong demand for oral solid dosage forms, particularly generics, which constitute a major portion of prescriptions dispensed in public health systems across Brazil, Mexico, and Argentina. Also, Latin American countries rely heavily on locally manufactured tablets and capsules to meet essential medicine needs. The push for medicine localization is another pivotal factor reinforcing FDF’s leadership. Additionally, FDF facilities require lower capital investment than API plants, enabling faster regulatory approval and scalability. These economic and policy advantages position FDF as the most accessible and strategically vital service segment in the regional CMO landscape.

The Active Pharmaceutical Ingredient (API) Manufacturing segment is the fastest-growing in the Latin America pharmaceutical products CMO market and is projected to expand at a CAGR of 12.3% from 2025 to 2033. This surge is fueled by growing concerns over supply chain vulnerabilities, particularly after disruptions during the pandemic exposed overreliance on Asian API suppliers. Most of APIs used in Latin America were imported from China and India, prompting governments to incentivize domestic production. A further key driver is the expansion of biologic and complex molecule manufacturing. These developments, combined with technology transfer initiatives from the WHO’s mRNA hub program, are accelerating the region’s capacity to produce high-value, complex APIs, positioning this segment for sustained high growth.

REGIONAL ANALYSIS

Brazil Pharmaceutical Products CMO Market Analysis

Brazil held the largest share of the Latin America pharmaceutical products CMO market at 44.6% of regional revenue in 2024. As the region’s most industrialized nation, Brazil serves as the epicenter of pharmaceutical manufacturing, supported by a well-established network of research institutions, regulatory infrastructure, and public health demand. The government’s commitment to health sovereignty has been a major catalyst. Brazil’s Ministry of Health invested significantly in domestic pharmaceutical production between 2020 and 2023. Also, Brazil produces a key portion of its insulin and its oncology drugs domestically. Additionally, ANVISA’s adoption of mutual recognition agreements with the EU and Australia has streamlined inspections, attracting global biopharma firms to partner with Brazilian CMOs. These advancements solidify Brazil’s leadership in both volume and technological capability.

Mexico Pharmaceutical Products CMO Market Analysis

Mexico is also a key market for pharmaceutical CMO services in Latin America. The country’s strategic position is anchored in its proximity to the U.S. market, robust industrial base, and growing emphasis on domestic medicine production. Mexico’s participation in USMCA facilitates technology transfer and regulatory alignment, enhancing its appeal as an outsourcing destination. These factors, combined with a skilled labor force and established supply chains, position Mexico as a key player in high-quality, nearshore pharmaceutical manufacturing.

Argentina Pharmaceutical Products CMO Market Analysis

Argentina commands a significant share of the Latin America pharmaceutical products CMO market, establishing itself as a technologically advanced yet economically constrained player. The country’s position is defined by a long-standing tradition of biopharmaceutical innovation and a growing role in regional API development. The WHO’s mRNA Technology Transfer Hub initiative designated mAbxience enabling technology sharing with other Latin American nations. These capabilities ensure Argentina’s continued relevance in high-value, complex molecule production.

Chile Pharmaceutical Products CMO Market Analysis

Chile holds a notable share of the Latin America pharmaceutical CMO market and is emerging as a niche but high-integrity player focused on quality, regulatory compliance, and digital manufacturing innovation. The country’s position is bolstered by political stability, strong intellectual property protections, and integration into global regulatory networks. The government has prioritized biotechnology development, allocating millions between 2021 and 2024 to modernize pharmaceutical manufacturing infrastructure. These attributes position Chile as a trusted partner for high-quality, low-volume pharmaceutical manufacturing.

COMPETITIVE LANDSCAPE

The competition in the Latin America pharmaceutical products CMO market is evolving into a dual-tier landscape, where multinational CMOs coexist with regionally rooted manufacturers, each leveraging distinct advantages. Global players bring technological sophistication, regulatory credibility, and scalable infrastructure, while local firms offer cost efficiency, policy alignment, and faster response to public health demands. Differentiation increasingly hinges on compliance with international GMP standards, speed of tech transfer, and adaptability to national medicine security programs. Economic volatility and fragmented regulations create entry barriers, yet also open opportunities for agile providers. As governments prioritize supply chain resilience, competitive success is shifting toward those who combine quality, localization, and strategic public-private collaboration, fostering a dynamic and increasingly specialized market environment.

KEY MARKET PLAYERS

Catalent Inc., Boehringer Ingelheim Group, Pfizer CentreSource, Thermo Fisher Scientific (Patheon), Acino International AG, Lonza Group AG, Famar SA, Baxter Biopharma Solutions, BASF SE, Bayer AG, F. Hoffmann-La Roche Ltd., Merck & Co., Inc., Novartis AG, Pisa Farmacéutica, Fresenius SE & Co. KGaA, Takeda Pharmaceutical Company Limited, Ferring Pharmaceuticals Inc., Landsteiner Scientific.

Top Players in the Latin America Pharmaceutical Products CMO Market

Catalent

Catalent has established a significant presence in the Latin America pharmaceutical products CMO market by leveraging its global expertise in advanced drug delivery and biologics manufacturing. The company strengthened its regional footprint in 2023 by expanding its softgel and oral solid dosage capabilities at its São Paulo facility, aligning with rising demand for locally produced generics and consumer health products. Catalent has deepened collaborations with public health agencies in Brazil and Mexico to support the domestic production of essential medicines, including antivirals and chronic disease therapeutics. In 2024, it launched a technology transfer initiative with a Mexican biotech firm to co-develop biosimilar formulations, enhancing regional self-reliance. Its integration of digital process analytics and adherence to FDA- and ANVISA-aligned quality standards has positioned Catalent as a preferred partner for both regional and multinational innovators seeking scalable, compliant manufacturing solutions.

Recipharm

Recipharm has strategically positioned itself in Latin America by focusing on sterile injectables, oncology formulations, and regulatory-compliant manufacturing services. In 2022, the company inaugurated its first regional facility in Montevideo, Uruguay, designed to serve multiple Latin American markets under a single regulatory approval framework, streamlining distribution. The site specializes in lyophilized oncology drugs and antibiotic formulations, addressing critical public health needs. Recipharm has actively engaged with health ministries in Colombia and Chile to support national medicine security initiatives, supplying GMP-grade products for public procurement programs. In 2023, it implemented AI-driven batch optimization systems at its facility, reducing cycle times by 28% and enhancing yield predictability. These advancements, combined with its commitment to sustainable manufacturing and rapid tech transfer, have solidified Recipharm’s reputation as a technologically advanced and reliable CMO partner in the region.

Neos Lab

Neos Lab, a leading Argentine CMO, has emerged as a pivotal player in Latin America by specializing in complex generics, biosimilars, and API-to-FDF integrated services. The company has played a key role in Argentina’s biopharmaceutical sovereignty agenda, producing recombinant insulin and monoclonal antibodies under technology transfer agreements with international partners. In 2023, Neos Lab received approval from ANMAT for the commercial production of a trastuzumab biosimilar, marking a milestone in regional oncology drug manufacturing. It has also expanded its sterile filling capacity to meet growing demand for injectable formulations in Brazil and Central America. Collaborating with the WHO’s mRNA hub program, Neos Lab is exploring mRNA-LNP formulation capabilities, positioning itself at the forefront of next-generation therapeutic manufacturing. Its focus on innovation, regulatory excellence, and public health alignment underscores its growing influence in the regional CMO ecosystem.

Top Strategies Used by Key Market Participants

Key players in the Latin America pharmaceutical products CMO market are deploying strategies centered on regulatory harmonization, technology adoption, public-sector partnerships, facility localization, and end-to-end service integration. Companies are aligning with ICH and WHO standards to ensure cross-border acceptability of manufactured products. Investment in continuous manufacturing, AI-driven process control, and digital batch records enhances efficiency and compliance. Firms are expanding regional facilities to serve multiple countries under centralized quality systems, reducing logistical complexity. Collaborations with national health agencies secure long-term supply contracts and strengthen policy alignment. Additionally, offering integrated API-to-FDF services enables CMOs to provide comprehensive solutions, increasing client retention and reducing dependency on external suppliers, thereby solidifying competitive advantage in a rapidly evolving market landscape.

RECENT MARKET DEVELOPMENTS

- In June 2023, Catalent expanded its oral solid dosage production capacity at its São Paulo facility, introducing high-speed tablet compression and advanced coating technologies to meet rising demand for generic cardiovascular and antidiabetic drugs in Brazil’s public health system.

- In February 2022, Recipharm inaugurated its GMP-certified manufacturing site in Montevideo, Uruguay, establishing a regional hub for sterile injectables and lyophilized oncology drugs, enabling supply to eight Latin American countries under a unified regulatory framework.

- In September 2023, Neos Lab received ANMAT approval for commercial-scale production of a trastuzumab biosimilar, becoming the first Latin American CMO to manufacture a monoclonal antibody therapy for breast cancer, enhancing regional access to high-cost biologics.

- In May 2024, Catalent launched a technology transfer partnership with a Mexican biopharmaceutical company to co-develop biosimilar formulations, strengthening local manufacturing capabilities and supporting Mexico’s national biologics substitution strategy.

- In January 2023, Recipharm implemented an AI-powered batch optimization system at its Montevideo facility, reducing production cycle times by 28% and improving yield consistency, setting a new benchmark for operational efficiency in sterile pharmaceutical manufacturing across Latin America.

MARKET SEGMENTATION

This research report on the Latin America pharmaceutical products CMO market is segmented and sub-segmented based on categories.

By Services Type

- Active Pharmaceutical Ingredient (API) Manufacturing

- Small Molecule

- Large Molecule

- High Potency API (HPAPI)

- Finished Dosage Formulation (FDF) Development and Manufacturing

- Solid Dose Formulation

- Tablets

- Others (Capsules, Powder, etc.)

- Liquid Dose Formulation

- Injectable Dose Formulation

- Solid Dose Formulation

By Country

- Mexico

- Brazil

- Argentina

- Chile

- Rest of Latin America

Frequently Asked Questions

What is driving the growth of the Latin America pharmaceutical products CMO market?

The growth is driven by rising demand for cost-effective drug manufacturing, increasing outsourcing by pharmaceutical companies, expansion of generics, and investments in advanced manufacturing capabilities.

Which pharmaceutical manufacturing services are most in demand in Latin America?

Finished dosage formulation (FDF) development, particularly solid dosage forms such as tablets and capsules, along with injectable formulations, are in high demand.

What challenges are restraining the Latin America pharmaceutical products CMO market?

Challenges include regulatory complexities, supply chain disruptions, lack of advanced infrastructure in some countries, and high competition from global CMOs.

What is the future outlook of the Latin America pharmaceutical products CMO market?

The market is expected to grow steadily, supported by increasing demand for biologics, biosimilars, and personalized medicine, along with strengthening regulatory frameworks.

Which countries are key contributors to the Latin America CMO market?

Brazil, Mexico, and Argentina are leading contributors due to their strong pharmaceutical industry presence, large patient population, and government healthcare initiatives.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com