Latin America Retail Market Size, Share, Trends & Growth Forecast Report By Product Type (Food, Beverage, and Grocery, Personal and Household Care, Apparel, Footwear, and Accessories, Furniture and Home Décor, Toys, Hobby, and Household Appliances, Industrial and Automotive, Electronic, Consumer Durables and IT, Pharmaceuticals, Others), By Sector (Organised, Unorganised), By Distribution Channel (Supermarkets and Hypermarkets, Convenience Stores, Speciality Stores, Online, Others), and By Country (Brazil, Mexico, Argentina, Chile, Rest of Latin America) – Industry Analysis, 2026 to 2034

Latin America Retail Market Size

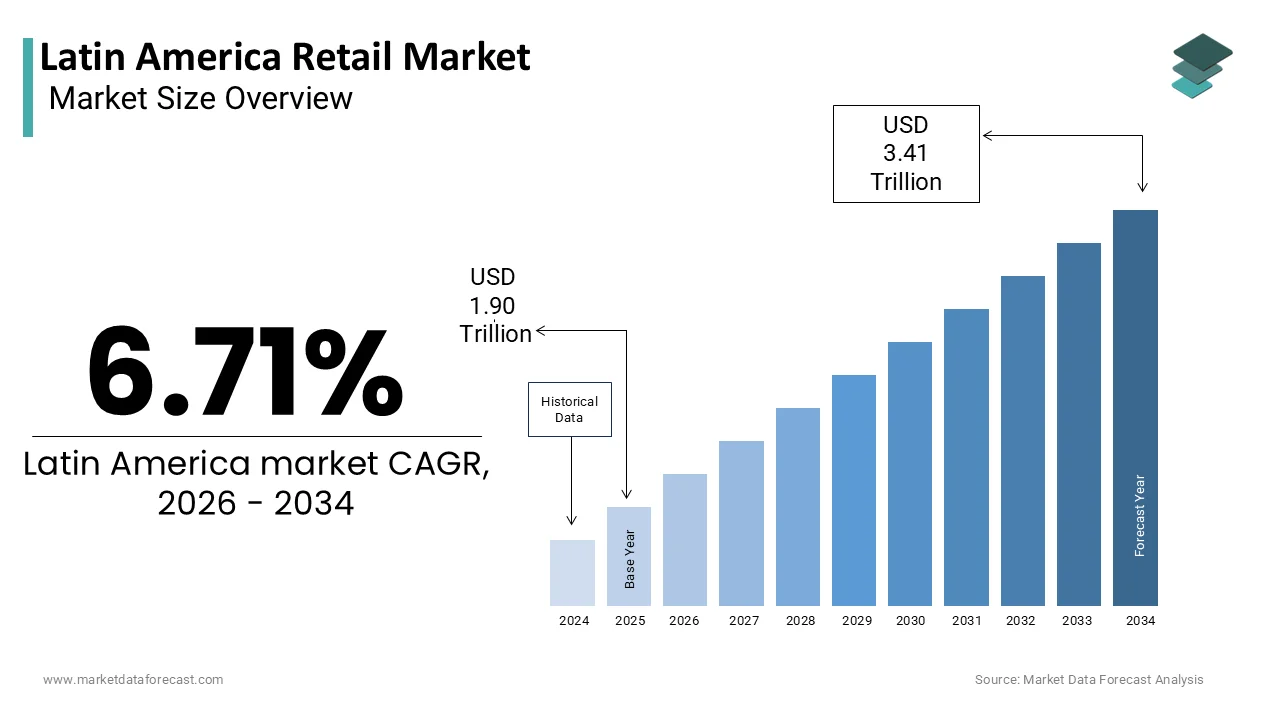

The Latin America retail market was valued at USD 1.90 trillion in 2025, is estimated to reach USD 2.03 trillion in 2026, and is projected to reach USD 3.41 trillion by 2034, growing at a CAGR of 6.71% from 2026 to 2034.

Retail is formal and informal commerce, spanning hypermarkets, convenience stores, e-commerce platforms, and traditional street-level vendors across 20 countries. Characterized by deep cultural diversity and uneven economic development, the sector serves a population exceeding 660 million, with urban centers like São Paulo, Mexico City, and Bogotá acting as primary consumption hubs. According to the Economic Commission for Latin America and the Caribbean (ECLAC), over 58% of the region’s population resides in urban areas, where purchasing behaviors are increasingly influenced by digital access and credit availability.

MARKET DRIVERS

Expansion of Financial Inclusion and Digital Payment Infrastructure

The rapid integration of financial services into everyday commerce is accelerating the growth of the Latin America retail market. Brazil’s Pix instant payment system, launched by the Central Bank in 2020, processed over 20 billion transactions monthly by 2023, as reported by Banco Central do Brasil, facilitating seamless in-store and online purchases. Retailers are leveraging these tools to offer “buy now, pay later” options, increasing basket sizes and customer retention among younger, digitally native consumers.

Rising Middle-Class Consumption and Urban Lifestyle Shifts

The expanding middle class is fueling sustained demand for branded goods, convenience, and experiential retail across major metropolitan areas, which is enhancing the growth of the Latin America retail market. Urban consumers in cities like Santiago and Lima are increasingly prioritizing time efficiency, driving demand for ready-to-eat meals, subscription services, and one-stop shopping centers. These shifts reflect deeper changes in lifestyle expectations, where retail is no longer transactional but integrated into social and leisure routines with the viability of premium and convenience-oriented formats.

MARKET RESTRAINTS

High Levels of Informal Retail Sector Activity

The informal economy, with the growth of formal chains and reduced tax compliance, is limiting the growth of the Latin America retail market. According to the International Labour Organization, approximately 47% of non-agricultural employment in the region is informal, with street vendors, unregistered kiosks, and home-based sellers accounting for a significant share of daily consumer transactions. These operators avoid regulatory costs, operate with minimal overhead, and often undercut formal retailers on price.

Logistical Fragmentation and Supply Chain Inefficiencies

Geographic dispersion, underdeveloped transportation networks, and bureaucratic customs procedures impede efficient retail distribution across Latin America. According to the World Bank’s Logistics Performance Index, only Chile and Uruguay rank above the global average in supply chain efficiency, while countries like Venezuela and Honduras face severe delays. These inefficiencies inflate inventory costs, limit product availability, and delay e-commerce fulfillment. Retailers often maintain excess stock to buffer disruptions, reducing capital flexibility and increasing spoilage rates for perishable goods in supermarket chains.

MARKET OPPORTUNITIES

Accelerated Adoption of Omnichannel Retail Models

Consumers are increasingly blending digital and physical shopping experiences by creating fertile ground for omnichannel strategies, which is enhancing the growth of the Latin American retail market. Retailers are integrating click-and-collect, in-app inventory checks, and geolocated promotions to enhance engagement. Falabella in Chile reported a 40% increase in sales through its mobile app in 2022, while Magazine Luiza in Brazil expanded its delivery network to over 10,000 pickup points.

Growth of Locally Sourced and Sustainable Consumer Goods

A rising consumer preference for authenticity, environmental responsibility, and support for local economies is additionally to elevate the growth of the Latin America retail market. According to Latinobarómetro, 54% of consumers in the region consider sustainability important when making purchases, with higher sentiment in Uruguay and Costa Rica. Certification programs such as Rainforest Alliance and Fair Trade are gaining visibility on packaging.

MARKET CHALLENGES

Currency Volatility and Inflationary Pressures on Pricing Strategy

The persistent macroeconomic instability complicates pricing, inventory planning, and profitability for retailers may inhibit the growth of the Latin America retail market. According to the International Monetary Fund, Argentina experienced an inflation rate of 211% in 2023. In Venezuela, hyperinflation has rendered local currency transactions nearly obsolete, pushing commerce toward dollarization. Retailers must navigate complex hedging strategies, dynamic pricing models, and consumer resistance to frequent price hikes.

Cybersecurity Risks and Data Privacy Compliance in Digital Expansion

The growing exposure to cyber threats and regulatory scrutiny as retailers digitize operations and collect increasing volumes of consumer data is enhancing the growth of the Latin America retail market. In 2023, a major data breach at a Colombian retail chain exposed over 1.2 million customer records, as confirmed by the Superintendency of Industry and Commerce. Regulatory frameworks are evolving; Brazil’s General Data Protection Law (LGPD), enacted in 2020, imposes strict penalties for non-compliance, yet only 30% of retailers are fully compliant, according to the Brazilian Institute of Consumer Defense.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Product Type, Sector, Distribution Channel, and Country. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | Brazil, Mexico, Argentina, Chile, Rest of Latin America |

| Market Leaders Profiled | Amazon.com, Inc., The Home Depot, Inc., The Kroger Co., Walgreens Boots Alliance, Inc., Alibaba Group Holding Limited, Target Corporation, Lowe's Companies, Inc., The Schwarz Group, Koninklijke Ahold Delhaize N.V., Carrefour Group, and Auchan Retail International. |

SEGMENTAL ANALYSIS

By Product Type Insights

The Food, Beverage, and Grocery segment was the largest and held 56.4% of the Latin America retail market share in 2024, with the essential nature of daily sustenance and the region’s dietary reliance on fresh produce, staples, and packaged goods. According to ECLAC, household spending on food constitutes nearly 24% of total consumption in lower-middle-income countries like Guatemala and Bolivia, significantly higher than the global average. Supermarkets and traditional bodegas alike prioritize high-turnover perishables, while rising health consciousness has spurred demand for fortified staples and organic produce.

The Apparel, Footwear, and Accessories segment is projected to grow at a CAGR of 7.8% during the forecast period with the shifting consumer preferences toward self-expression, seasonal trends, and digital fashion engagement. Young consumers, who constitute over 30% of the population under 25, are increasingly influenced by social media and global fashion cycles, which are fueling demand for fast fashion and niche brands. Moreover, localized production in countries like Peru and Uruguay is known for alpaca wool and sustainable denim that adds premium value. Retailers such as C&A and Zara have expanded omnichannel inventories to meet rising expectations for style variety and rapid delivery.

By Distribution Channel Insights

The supermarkets and hypermarkets segment was the largest by accounting for 48.3% of the Latin America retail market share in 2024, with economies of scale, centralized procurement, and consumer trust in product quality and safety. Chains like Walmart Mexico and Carrefour Brazil have expanded private-label offerings, increasing margins while maintaining affordability. The integration of loyalty programs and digital promotions further enhances customer retention.

The convenience and discount stores segment is likely to grow with an expected CAGR of 8.3% during the forecast period, with the rising cost sensitivity, urban density, and the proliferation of small-format retail in densely populated areas. These stores offer essential goods at reduced prices, often through bulk purchasing and limited service models. Furthermore, proximity to residential areas enables frequent, low-volume purchases, aligning with cash-based economies. Retailers are enhancing these formats with digital payment integration and localized assortments, which is making them indispensable in both affluent and low-income urban corridors.

COUNTRY-LEVEL ANALYSIS

Brazil Retail Market Insights

Brazil was the largest and held 38.2% of the Latin America retail market share in 2024. The country recorded BRL 1.8 trillion in retail sales in 2023, driven by robust consumer demand in metropolitan areas like São Paulo and Rio de Janeiro. According to the National Confederation of Commerce (CNC), e-commerce sales grew by 16% year-on-year, while physical stores rebounded post-pandemic with a 9.2% increase in foot traffic. Retailers such as Magazine Luiza and GPA have leveraged digital transformation to integrate online and offline channels. Additionally, the expansion of atacadistas (wholesale-retail hybrids) into underserved regions has broadened market reach.

Mexico Retail Market Insights

Mexico was positioned second by capturing 29.3% of the Latin America retail market share in 2024, owing to the strategic location, trade agreements, and strong manufacturing base support a robust retail ecosystem. Walmart de México y Centroamérica operates over 2,800 stores, which serve 10 million customers weekly, according to its annual sustainability report. The rise of fintech platforms like Clip and Konfío has enabled small retailers to accept digital payments, improving transaction efficiency.

Chile Retail Market Insights

Chile retail market is expected to grow at the highest CAGR during the forecast period, with its stable regulatory environment and high consumer purchasing power, Chile serves as a regional benchmark for retail sophistication. Santiago alone hosts over 70% of the country’s shopping malls, which generate 40% of total retail sales, according to the Chamber of Commerce of Santiago. Retailers like Falabella and Cencosud have pioneered omnichannel integration, with mobile app sales growing by 38% in 2022.

KEY MARKET PLAYERS

Some of the noteworthy companies in the Latin America retail market profiled in this report are Amazon.com, Inc., The Home Depot, Inc., The Kroger Co., Walgreens Boots Alliance, Inc., Alibaba Group Holding Limited, Target Corporation, Lowe's Companies, Inc., The Schwarz Group, Koninklijke Ahold Delhaize N.V., Carrefour Group, and Auchan Retail International.

TOP LEADING PLAYERS IN THE MARKET

Walmart de México y Centroamérica (Walmex)

Walmart de México y Centroamérica operates one of the most extensive retail networks in Latin America, spanning hypermarkets, supermarkets, and e-commerce platforms across Mexico and Central America. The company has intensified its digital transformation by enhancing its online marketplace and expanding last-mile delivery capabilities through partnerships with local logistics providers. In 2023, Walmex launched a new fulfillment center in Toluca, integrating automation to accelerate e-commerce order processing. It has also deepened financial inclusion by introducing prepaid digital wallets for unbanked customers. These initiatives reflect a strategic focus on accessibility, speed, and technological integration to maintain leadership in a competitive, fast-evolving market.

Cencosud

Cencosud, a Chilean multinational retailer, maintains a diversified presence across hypermarkets, home improvement, and shopping malls in Argentina, Brazil, Chile, Colombia, and Peru. The company has prioritized omnichannel integration, significantly upgrading its e-commerce platforms and mobile applications to offer real-time inventory tracking and click-and-collect services. In 2023, Cencosud partnered with Mercado Libre to expand its digital reach, enabling third-party sellers to access its supply chain infrastructure. It also launched a sustainability initiative to eliminate single-use plastics across its Jumbo and Santa Isabel stores by 2025, aligning with consumer demand for eco-conscious retail. In Colombia, it expanded its Easy home improvement chain into secondary cities, capitalizing on rising construction activity.

Falabella

Falabella has established itself as a retail innovator through its integrated ecosystem of stores, financial services, and logistics. The company operates Sodimac (home improvement), Tottus (supermarkets), and Falabella department stores, supported by its proprietary delivery network, Chilexpress. Falabella has also expanded its credit offerings through Banco Falabella, providing installment plans that boost average transaction values. In Peru, it opened a regional fulfillment hub in Lima to reduce delivery times to 24 hours in major cities.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Latin America retail market are deploying strategies including omnichannel integration, supply chain digitization, private label expansion, financial service bundling, and sustainability-driven branding to consolidate their market presence. Retailers are synchronizing online and offline inventories to enable seamless shopping experiences, while automated warehouses and AI-powered demand forecasting improve fulfillment accuracy. Private labels are being expanded to increase margins and build brand loyalty. In-house fintech solutions such as retail credit cards and digital wallets enhance customer stickiness. Additionally, strategic partnerships with e-commerce enablers and last-mile providers are accelerating digital reach in underserved urban and peri-urban areas.

COMPETITIVE LANDSCAPE

Competition in the Latin America retail market is intensifying as multinational chains, regional operators, and digital-native platforms vie for consumer loyalty amid economic volatility and shifting purchasing behaviors. While traditional giants like Walmart and Cencosud dominate through scale and logistics, agile e-commerce players such as Mercado Libre are redefining convenience and speed. The rise of discount retailers and informal vendors adds pressure on pricing, which is compelling formal chains to innovate in cost efficiency. Differentiation increasingly hinges on digital experience, delivery reliability, and value-added services like in-house financing. Regulatory disparities, currency fluctuations, and logistical fragmentation further complicate national scalability. Success now depends on adaptive business models that blend physical presence with digital fluency, localized assortment strategies, and resilience to macroeconomic shocks across diverse national markets.

RECENT MARKET DEVELOPMENTS

- In January 2023, Walmart de México launched a fully automated fulfillment center in Toluca, enhancing e-commerce order processing speed and expanding same-day delivery capabilities across central Mexico.

- In May 2023, Cencosud initiated a strategic partnership with Mercado Libre to integrate its supply chain and logistics network, enabling faster delivery and broader digital marketplace access in Argentina and Chile.

- In September 2023, Falabella introduced an AI-powered product recommendation engine on its e-commerce platform, increasing online conversion rates by 22% and improving customer personalization in Peru and Colombia.

- In March 2024, Grupo Éxito expanded its home delivery fleet in Colombia by 300 electric vehicles, reducing last-mile emissions and improving delivery efficiency in Bogotá and Medellín.

- In July 2023, Soriana opened 15 new Hiper and Súper stores in northern Mexico, focusing on underserved municipalities and reinforcing its regional presence through localized product assortments.

MARKET SEGMENTATION

This Latin America retail market research report is segmented and sub-segmented into the following categories.

By Product Type

- Food, Beverage, and Grocery

- Personal and Household Care

- Apparel, Footwear, and Accessories

- Furniture and Home Décor

- Toys, Hobby, and Household Appliances

- Industrial and Automotive

- Electronic, Consumer Durables and IT

- Pharmaceuticals

- Others

By Sector

- Organised

- Unorganised

By Distribution Channel

- Supermarkets and Hypermarkets

- Convenience Stores

- Speciality Stores

- Online

- Others

By Country

- Brazil

- Mexico

- Argentina

- Chile

- Rest of Latin America

Frequently Asked Questions

1. What is the Latin America Retail Market?

The Latin America Retail Market consists of physical stores, digital platforms, and hybrid channels for consumer goods, apparel, grocery, electronics, and luxury products, serving urban and rural populations across the region

2. What are the main segments in the Latin America Retail Market?

Key segments include grocery, apparel, consumer electronics, travel retail, e-commerce, and hybrid models blending online and offline experiences

3. Which countries lead the Latin America Retail Market?

Brazil and Mexico dominate the market, with Colombia, Argentina, and Chile also showing strong retail growth and shopper base expansion

4. What drives growth in the Latin America Retail Market?

Growth factors include rising middle-class incomes, rapid digital adoption, expanding smartphone use, investments in omnichannel retail, and consumer demand for convenience and experience

5. How is e-commerce changing the Latin America Retail Market?

E-commerce is a rapidly growing segment, with Brazil and Mexico accounting for major shares and online retail revenues projected to surpass $150 billion in incremental sales across the region over the next two years

6. What is smart retail and how is it affecting Latin America?

Smart retail involves technology-driven innovations such as contactless payment, AI, advanced CRM solutions, and digital inventory management, with the smart retail market set to grow over 30% CAGR from 2025 to 2033

7. How do omnichannel strategies benefit the Latin America Retail Market?

Omnichannel approaches bridge online and offline retail, improve customer engagement, personalize shopping, and help retailers compete with global entrants

8. What trends are influencing grocery retail in Latin America?

Trends include value-centered shopping, expansion of convenience stores, private-label product growth, premium and economy brand shifts, and increased e-commerce grocery penetration

9. What is the role of travel retail in the Latin America Retail Market?

Travel retail, especially airport and border duty-free, is robust in Mexico and Colombia, benefiting from rising tourism, international connectivity, and digital transformation in duty-free shopping

10. How are retailers in Latin America using technology?

Retailers are embracing AI, augmented reality, mobile apps, personalization, and data-driven analytics to improve inventory management and enhance customer experiences

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com