Latin America Toy Market Size, Share, Trends & Growth Forecast Report By Product Type (Action Figures, Building Sets, Dolls, Games and Puzzles, Sports and Outdoor Toys, Plush, and Others), Age Group, Sales Channel, and Region (Brazil, Mexico, Argentina, Chile & Rest of Latin America) – Regional Industry 2026 to 2034

Latin America Toy Market Size

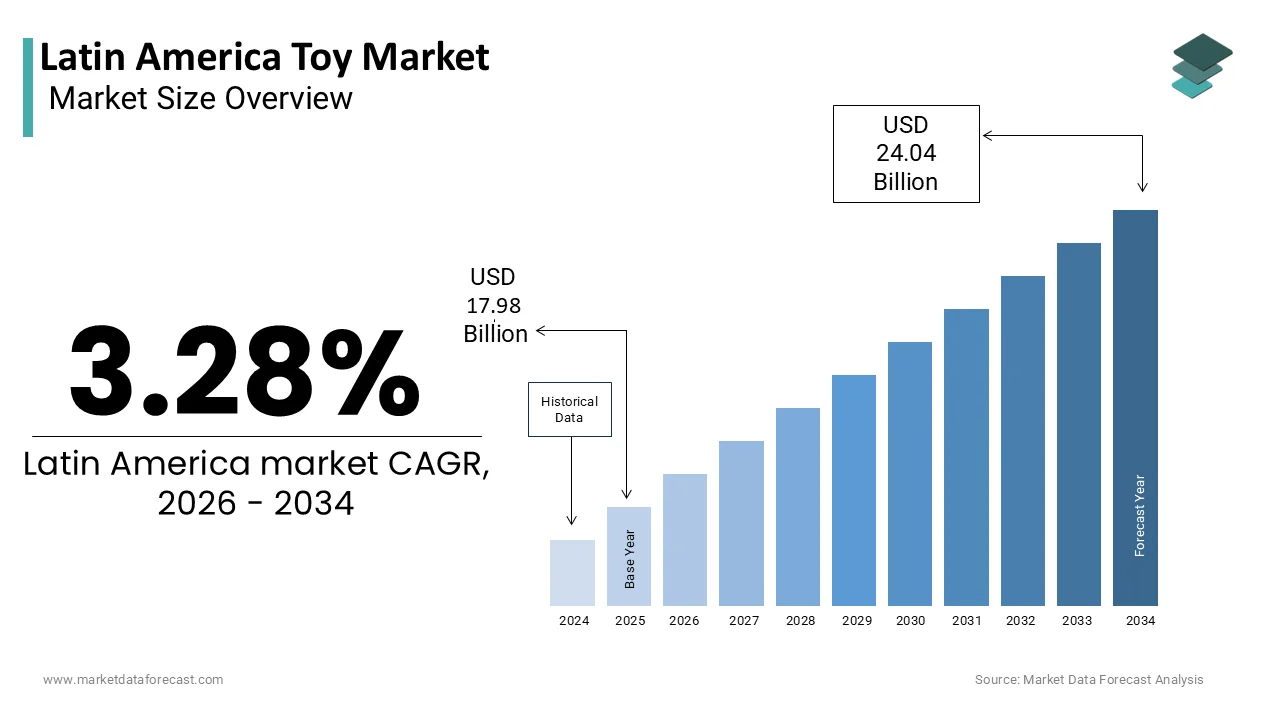

The Latin America toy market size was valued at USD 17.98 billion in 2025 and is expected to reach USD 24.04 billion by 2034 from USD 18.57 billion in 2026. The market is projected to grow at a CAGR of 3.28%.

The toy is a play-based product tailored for children aged 0–14, spanning educational toys, action figures, dolls, puzzles, and electronic games. Rooted in evolving consumer preferences and cultural dynamics, the sector reflects broader socioeconomic shifts across urban and rural populations. As per UNICEF, approximately 142 million children reside in Latin America, constituting nearly 23% of the region’s total population, forming the foundational consumer base for toy demand.

MARKET DRIVERS

Expanding Middle-Class Households with Rising Disposable Incomes

Latin America’s growing middle class is increasing toy consumption, as families allocate greater portions of income toward child-centric expenditures, which is expected to boost the growth of the Latin American toy market. This economic mobility has translated into higher spending on developmental and recreational products for children.

Integration of Educational and STEM-Based Play in Early Learning

The increasing emphasis on early cognitive development that blends entertainment with learning, particularly in science, technology, engineering, and math (STEM, is expected to further boost the growth of the Latin American toy market. As per UNESCO’s Regional Office for Latin America and the Caribbean, over 27,000 public and private preschools across the region have adopted play-based curricula since 2020, incorporating building blocks, coding kits, and interactive puzzles. Private kindergartens in Mexico report a 40% increase in STEM toy purchases between 2021 and 2023, as noted by the National Association of Private Schools (ANMEPP).

MARKET RESTRAINTS

High Import Dependency and Tariff-Induced Price Inflation

The branded and electronic toys sold in Latin America are manufactured abroad in Asia, leading to vulnerability to import costs and trade policies. This factor is attributed to hampering the growth of the Latin American toy market. According to the United Nations Economic Commission for Latin America and the Caribbean (ECLAC), over 65% of toys consumed in the region are imported, with Brazil and Argentina imposing average tariffs of 20% and 35%, respectively, on toy categories. Additionally, supply chain delays at ports like Santos and Callao extend lead times, disrupting seasonal sales cycles.

Prevalence of Informal and Unregulated Toy Sales

The informal sector accounts for a substantial share of toy distribution, particularly during festive periods, and is additionally limiting the growth of the Latin America toy market. According to the International Labour Organization, nearly 48% of toys sold in open-air markets across Central America and the Andean region lack compliance with regional safety regulations such as NOM-251 in Mexico or INMETRO certification in Brazil. In Guatemala, INSP enforcement raids in 2023 seized over 120,000 counterfeit toys containing hazardous materials like lead and phthalates.

MARKET OPPORTUNITIES

E-Commerce Expansion and Digital Engagement with Millennial Parents

The rapid adoption of online shopping among digitally native parents is expected to impact the growth of the Latin American toy market in the coming years. As per the Digital 2023 report by DataReportal, internet penetration in the region reached 79%, with Brazil and Mexico recording over 100 million social media users each, enabling targeted digital campaigns. Platforms like Mercado Libre and Magazine Luiza reported a 67% year-on-year increase in toy sales via mobile apps during the 2023 holiday season. Additionally, YouTube and Instagram influencers specializing in “unboxing” videos have become trusted recommendation sources 82% of mothers in urban Colombia consult online reviews before purchasing toys, according to a Kantar Latinobarómetro survey. Companies are responding with augmented reality (AR) catalogs and subscription toy boxes delivered monthly.

Localization of Product Design and Cultural Representation

Toy manufacturers are increasingly customizing products by fostering emotional resonance and brand loyalty, which is also enhancing the growth of the Latin American toy market. Mattel’s launch of a Frida Kahlo-themed Barbie in Mexico and Hasbro’s introduction of Carnaval-inspired action figures in Brazil exemplify this trend. Educational toy makers are incorporating regional biodiversity jigsaws featuring Amazonian wildlife, or puzzles of Machu Picchu, which are gaining popularity in school supply kits. This cultural alignment not only differentiates products in a competitive landscape but also supports inclusive identity development in children, which is creating a sustainable niche for socially conscious brands.

MARKET CHALLENGES

Regulatory Fragmentation Across National Toy Safety Standards

The absence of harmonized safety regulations across Latin American countries complicates compliance for manufacturers and importers,, restraining the growh of the Latin American toy market. According to the Pan American Standards Commission (COPANT), there are 14 different national standards for toy safety in the region, requiring multiple testing cycles for cross-border distribution. In 2022, Argentina’s INAMEC rejected 22% of imported toy shipments due to non-compliance with local labeling laws, including Spanish-language instructions and age grading. This regulatory divergence increases time-to-market and compliance costs, particularly for small and medium enterprises.

Seasonal Demand Volatility and Economic Sensitivity

Toy sales in Latin America are heavily concentrated in a few high-spending periods, primarily year-end holidays and Children’s Day in Octobe,y creating operational imbalances. This attribute is expected to decline the fastest in the growth of the Latin American toy market. According to the Retail Federation of Latin America (Federación Latinoamericana de Retail), nearly 58% of annual toy sales occur between October and December, forcing manufacturers to ramp up production months in advance. This seasonality increases inventory risks,, unsold stock often leads to deep discounting, eroding margins. Similarly, currency devaluations in Venezuela and Ecuador reduce purchasing power, pushing families to prioritize essentials over discretionary items. This sensitivity to macroeconomic conditions makes long-term forecasting and investment planning exceptionally challenging for stakeholders across the supply chain.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 3.28% |

| Segments Covered | By Product Type, Age Group, Sales Channel, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | Latin Americincludesde Brazil, Argentina, Mexico, and the Rest of Latin Amer.ica |

| Market Leaders Profiled | Hasbro, Inc., Mattel, Inc., Lego Group, MGA Entertainment, Spin Master, Bandai Namco Holdings Inc., Jakks Pacific, Inc., Playmobil (Brandstätter Group), Funko, Inc., Tomy Company, Ltd., Ravensburger AG, Fisher-Price (a subsidiary of Mattel, Inc.), Mega Bloks (a subsidiary of Mattel, Inc.), VTech Holdings Limited, WowWee Group Limited, and others. |

SEGMENTAL ANALYSIS

By Product Type Insights

The games and puzzles segment was the largest and held 24.3% of the Latin America toy market share in ,2024 with the rising emphasis on cognitive development and family-based recreational activities. Board games and puzzles are increasingly integrated into early childhood education frameworks across the region. According to UNESCO’s Regional Office for Education in Latin America, over 18,000 preschools in Brazil, Colombia, and Chile have incorporated logic and memory-based games into daily learning routines to enhance problem-solving and concentration. The popularity of strategy-based games such as Catan and localized versions of Trivial Pursuit has surged, particularly in middle-income urban areas.

The building sets segment is expected to grow with a CAGR of 8.6% during the forecast p,eriod with the increasing integration of STEM (Science, Technology, Engineering, and Mathematics) learning in school curricula and extracurricular programs. Brazil’s Ciência na Escola program has similarly driven demand, with municipal education departments purchasing 1.2 million building sets for STEM labs. Companies like LEGO have responded with region-specific kits featuring Latin American architecture, further boosting appeal.

By Age Group Insights

The up to 5 years age group set was accounted in holding 48.2% of the Latin America toy market share in 2024, with the developmental milestones achieved during early childhood and the corresponding demand for sensory, motor, and language-stimulating toys. Retail data from Chile’s Falabella shows that 61% of toy purchases for this demographic are made by mothers under 35, who prioritize safety, brand reputation, and developmental claims.

The 5 to10-years age group is projected to witness a CAGR of 7.9% during the forecast period with the integration of school-based learning, digital influence, and social play dynamics. Children in this bracket are increasingly exposed to global media franchises Marvel, Pokémon, and Bluey, which directly influence toy purchasing behavior. According to a 2023 survey by Kantar Latinobarómetro, 81% of children aged 6–10 in urban centers request toys linked to TV or streaming content. Additionally, the rise of extracurricular STEM clubs and robotics competitions in schools across Brazil and Mexico has amplified demand for advanced building sets, science kits, and interactive electronics. Retailers report that this age group generates the highest average transaction value, as children exert greater influence on spending decisions.

By Sales Channel Insights

The supermarkets and hypermarkets segment accounted in holding 42.3% of the Latin America toy market share in 2024, with the widespread physical presence, consumer trust, and strategic product placement during high-traffic periods. Chains like Walmart Mexico, Carrefour Brazil, and Jumbo Chile dedicate prominent shelf space to toys, especially during seasonal campaigns such as Children’s Day and year-end holidays. These retailers also benefit from integrated supply chains, enabling consistent stock availability. In rural and semi-urban areas where e-commerce penetration is limited, supermarkets remain the primary access point for branded toys. Their ability to combine affordability, convenience, and reliability ensures continued dominance, particularly for mass-market and entry-level products.

The online stores segment isgrowing lucrativelyg with an anticipated CAGR of 12.3% during the forecast period, with improved digital infrastructure, rising smartphone ownership, and evolving consumer behavior. Data from DataReportal shows that Latin America recorded 455 million internet users in 2023, with 97% accessing the web via mobile devices. Platforms like Mercado Libre, Amazon Mexico, and Magazine Luiza have optimized toy categories with filters for age, educational value, and safety certifications, enhancing user experience. According to a 2023 survey by Ipsos, 54% of parents in urban areas prefer online shopping for toys due to wider selection, competitive pricing, and home delivery.

REGIONAL ANALYSIS

Brazil Toy Market Insights

Brazil was the largest contributortof the Latin American toy market by accounting for 38.3% ofthe market the market share in 2024, with a mature retail ecosystem, a large child population, anda strong cultural emphasis on play and gifting. Educational toys are gaining traction, supported by federal programs promoting early childhood development. However, high import taxes on electronic toys limit affordability, prompting local manufacturers like Grow and Estrela to focus on cost-effective, culturally relevant products.

Mexico Toy Market Insights

Mexico was positioned next to Brazil by capturing 27.4% of the Latin American toy market share in 2024. Mexico’s toy market growth is driven by the growing middle-class families and increasing discretionary spending on children’s products. The nearshoring trends have boosted domestic manufacturing, with companies like Mattel operating regional production facilities in Nuevo León.

Argentina Toy Market Insights

Argentina's's toy market growth is more likely to grow with the highest CAGR during the forecast period, heavily influenced by economic instability, with hyperinflation and currency controls limiting purchasing power. However, the cultural importance of gift-giving during Día del Niño and Christmas sustains baseline activity, with 72% of families still purchasing at least one toy annually, as noted by the University of Buenos Aires’ Consumer Behavior Institute. Local manufacturers like Playmobil Argentina have adapted by producing smaller, lower-priced product lines. Informal markets account for nearly 40% of toy distribution, driven by affordability.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Hasbro, Inc., Mattel, Inc., Lego Group, MGA Entertainment, Spin Master, Bandai Namco Holdings Inc., Jakks Pacific, Inc., Playmobil (Brandstätter Group), Funko, Inc., Tomy Company, Ltd., Ravensburger AG, Fisher-Price (a subsidiary of Mattel, Inc.), Mega Bloks (a subsidiary of Mattel, Inc.), VTech Holdings Limited, and WowWee Group Limited.

The competition in the Latin American toy market is marked by a dynamic interplay between multinational corporations and regional manufacturers, each leveraging distinct advantages. Global players like Mattel and Hasbro dominate through brand equity, innovation, and extensive distribution networks, while local firms such as Estrela and Grow compete through cultural authenticity, pricing agility, and deep retail relationships. The market is highly fragmented across countries, with regulatory, economic, and consumer behavior differences shaping competitive dynamics. Urban centers favor premium and educational toys, whereas rural areas rely on affordable, durable products distributed through informal channels. Digital transformation is intensifying rivalry, as companies race to capture online demand through personalized marketing and seamless logistics. Additionally, safety compliance and sustainability are emerging as key differentiators.

TOP PLAYERS IN THE MARKET

Mattel

Mattel was the top player in the Latin American toy market through its culturally adapted portfolio and strategic retail partnerships. The company has localized iconic brands such as Barbie, Hot Wheels, and Fisher-Price to reflect regional diversity, launching dolls with Afro-Latin features and indigenous-inspired clothing lines in Brazil and Mexico. In 2023, Mattel collaborated with Mexico’s Ministry of Education to distribute literacy-focused toy kits in rural schools, reinforcing its commitment to developmental play. It has strengthened distribution through alliances with major retailers like Soriana and Falabella, while expanding e-commerce visibility via Mercado Libre. The company also invested in a regional innovation hub in São Paulo to accelerate product development tailored to Latin American preferences.

Hasbro

Hasbro hasa dominant role in Latin America by leveraging global franchises and expanding its educational and digital play offerings. The company has localized brands like Transformers, Nerf, and Play-Doh with region-specific marketing campaigns, including Portuguese and Spanish-language content featuring Latin celebrities. In 2023, Hasbro launched a partnership with Argentina’s public television network to air interactive toy-based educational programming for children. It has also enhanced its digital footprint by integrating augmented reality features into board games like Jenga and Monopoly, available through mobile apps in Brazil and Colombia. Additionally, the company participates in sustainability initiatives by aiming for 100% recyclable packaging by 2025, a move that resonates with environmentally conscious urban consumers.

Estrela

Estrela stands as a leading homegrown toy manufacturer in Latin America by primarily serving the Brazilian market with a strong emphasis on cultural relevance and affordability. Known for brands like Bubu, Poupeta, and the licensed Turma da Mônica series, Estrela designs toys that reflect Brazilian childhood experiences and linguistic identity. In 2023, the company launched an AI-powered app that integrates with physical toys to create interactive storytelling experiences, blending digital and tactile play. Estrela also expanded its presence in educational toys by partnering with São Paulo’s municipal education department to supply STEM kits to public schools. The company has modernized its production facilities in São José dos Pinhais to improve efficiency and sustainability.

TOP STRATEGIES USED BY THE KEY MARKET PLAYERS

Key players in the Latin American toy market are deploying multifaceted strategies to capture consumer attention and enhance market penetration. Major approaches include localization of product design to reflect regional cultures, languages, and traditions, strengthening emotional resonance with families. Companies are increasingly investing in educational toys that align with STEM and early cognitive development curricula, responding to parental demand for enriching play. Strategic partnerships with public institutions and schools are being leveraged to distribute learning-focused toys at scale. Digital integration is another priority, with augmented reality, mobile apps, and interactive packaging enhancing engagement. E-commerce optimization and social commerce through Instagram and WhatsApp are expanding reach, particularly among millennial parents. Additionally, sustainability initiatives such as recyclable packaging and eco-friendly materials are improving brand perception. These strategies collectively enable companies to differentiate in a competitive, culturally diverse, and economically variable market.

RECENT HAPPENINGS IN THE MARKET

- In March 2023, Mattel launched a new line of Barbie dolls representing Latin American heritage, including versions with traditional Mexican, Afro-Brazilian, and Andean indigenous attire by enhancing cultural representation and consumer engagement across the region.

- In July 2023, Hasbro opened a regional innovation and distribution center in Panama City, enabling faster logistics across Central America and the Caribbean while supporting localized product development for Spanish-speaking markets.

- In November 2023, Estrela partnered with Brazil’s São Paulo state education department to supply 500,000 STEM-based toy kits to public elementary schools, which is strengthening its presence in the educational segment and building institutional trust.

- In January 2024, LEGO introduced a Latin American architecture series featuring iconic landmarks like Christ the Redeemer and Cartagena’s historic walls, available exclusively through Mercado Libre to boost online visibility and regional appeal.

- In May 2024, Fisher-Price collaborated with Chilean pediatricians and early childhood experts to launch a developmental milestone guide bundled with infant toys.

MARKET SEGMENTATION

This research report on the LatinAmericana toy market is segmented and sub-segmented into the following categories.

By Product Type

- Action Figures

- Building Sets

- Dolls

- Games and Puzzles

- Sports and Outdoor Toys

- Plush

- Others

By Age Group

- Up to 5 Years

- 5 to 10 Years

- Above 10 Years

By Sales Channel

- Supermarkets and Hypermarkets

- Specialty Stores

- Department Stores

- Online Stores

- Others

By Country

- Brazil

- Argentina

- Mexico

- Rest of Latin America

Frequently Asked Questions

1. What is the Latin America Toy Market?

It covers the production, sales, and consumption of toys including action figures, dolls, puzzles, outdoor toys, and educational products.

2. What drives growth in the Latin America Toy Market?

Rising disposable incomes, e-commerce expansion, and demand for branded and educational toys drive market growth.

3. Which countries dominate the Latin America Toy Market?

Brazil and Mexico lead the market, followed by Argentina, Chile, and Colombia.

4. What types of toys are popular in the Latin America Toy Market?

Popular toys include dolls, action figures, building sets, puzzles, plush toys, and electronic toys.

6. Which distribution channels are important in the Latin America Toy Market?

Sales occur through toy stores, supermarkets, specialty shops, and online platforms.

7. Who are the leading players in the Latin America Toy Market?

Key players include Mattel, Hasbro, LEGO Group, Spin Master, Bandai Namco, and MGA Entertainment.

8. What challenges face the Latin America Toy Market?

Challenges include high competition, counterfeit products, and economic fluctuations in the region.

9. Which consumer segments drive the Latin America Toy Market?

Children under 14 are the primary consumers, with parents focusing on safe and educational toys.

10. What is the future outlook for the Latin America Toy Market?

The market is expected to grow steadily with demand for sustainable, digital, and premium toys.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com