Middle East Media and Entertainment Market Size, Share, Trends & Growth Forecast Report By Type (Digital Music, Video Games, Video-on-Demand, E-Publishing, Advertising, Internet Access Services), By Platform (Online/Digital, Traditional/Linear, Hybrid (Omnichannel)), By Revenue Model (Subscription-Based, Advertising-Supported, Pay-Per-View/Transactional, Freemium/In-App Purchase), By End-User Age Group, By Device, and By Country (KSA, UAE, Israel, Rest of GCC countries, Rest of Middle East) – Industry Analysis, 2026 to 2034

Middle East Media and Entertainment Market Size

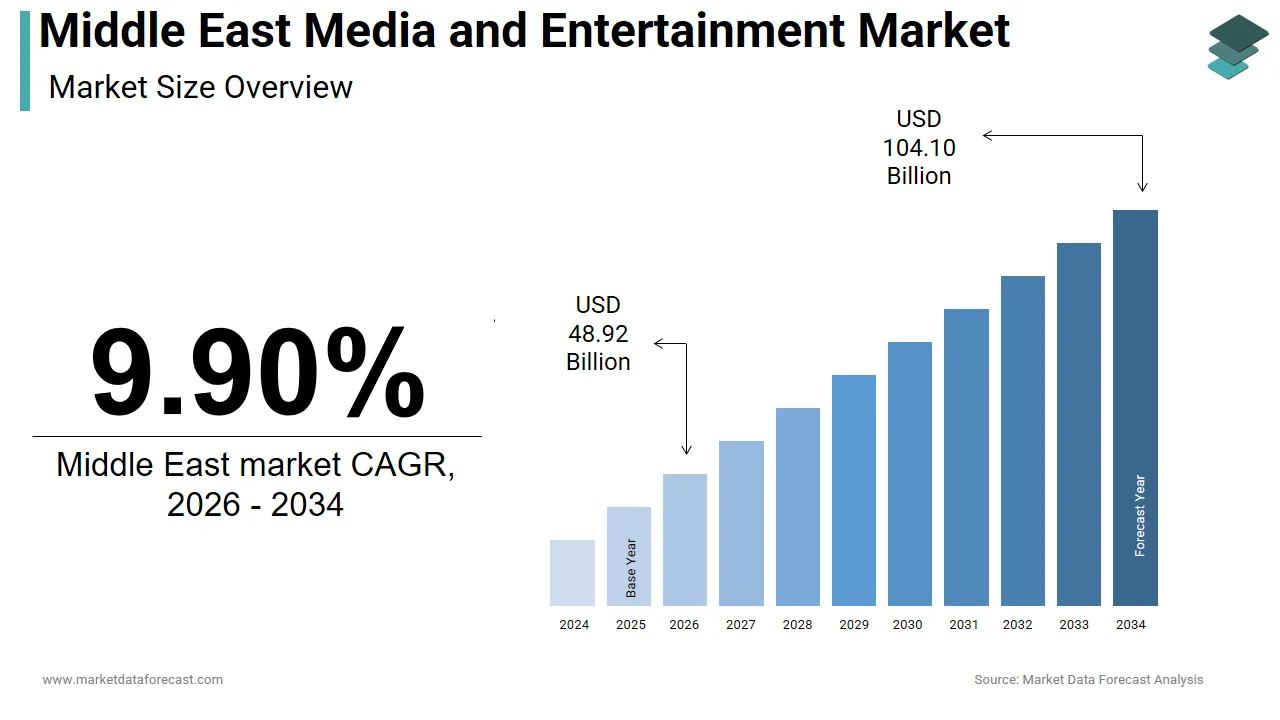

The Middle East media and entertainment market was valued at USD 44.51 billion in 2025, is estimated to reach USD 48.92 billion in 2026, and is projected to reach USD 104.10 billion by 2034, growing at a CAGR of 9.90% from 2026 to 2034.

The media and entertainment is a rapidly transforming ecosystem shaped by digital disruption, cultural renaissance, and state-led diversification agendas. Internet penetration has reached 85%, as reported by the International Telecommunication Union, enabling widespread access to on-demand content.

MARKET DRIVERS

Youth-Centric Demographics Fueling Digital Content Consumption

The growing young population is a primary driver for the growth of the Middle East media and entertainment market. According to the World Bank, 65% of the population in Arab states is under 30, with youth in Saudi Arabia and Egypt representing over 60% of internet users. This cohort exhibits a strong preference for video-on-demand, social media content, and gaming, driving rapid adoption of platforms such as Shahid, Starzplay, and YouTube. In 2023, Arab youth spent an average of 3.7 hours per day on digital entertainment, as per a regional study by YouGov, with short-form video content on TikTok and Instagram Reels witnessing a 62% year-on-year increase in engagement. The rise of Arab influencers and homegrown digital creators has further amplified demand for localized, culturally resonant content. Additionally, the expansion of 5G networks available in 90% of urban areas in the UAE and Saudi Arabia, according to Ericsson, enables high-quality streaming, reducing latency and enhancing user experience, thereby sustaining long-term growth in digital media consumption.

Government-Led Investment in Cultural and Entertainment Infrastructure

The national economic transformation programs in the Gulf are channeling unprecedented capital into media production, film, and large-scale entertainment events, which is enhancing the growth of the Middle East media and entertainment market. The government has established dedicated zones such as the King Abdulaziz Center for World Culture and NEOM’s entertainment giga-projects to institutionalize the sector. These investments are not only stimulating domestic consumption but also positioning the region as a content-exporting entity, which is fostering a self-sustaining ecosystem of production, distribution, and audience engagement.

MARKET RESTRAINTS

Fragmented Regulatory Frameworks and Content Censorship Policies

The lack of harmonized regulatory policies across countries, coupled with stringent content censorship regimes, is hampering the growth of the Middle East media and entertainment market. For instance, a 2023 report by the Gulf Research Center revealed that over 40% of Arabic-dubbed or subtitled international series on major platforms had undergone edits to comply with local norms in Saudi Arabia, Egypt, and Kuwait. These alterations often dilute narrative integrity and discourage global producers from licensing content.

Underdeveloped Intellectual Property Protection Mechanisms

The weak enforcement of intellectual property (IP) rights is hindering sustainable content creation and foreign investment in the region’s media and entertainment sector, which is ascribed in limiting the growth of the Middle East media and entertainment market. Piracy of films, music, and digital content is widespread, with a 2023 study by the Arab States Broadcasting Union indicating that over 60% of online video consumption in the Middle East occurs through unauthorized platforms. In Egypt and Iraq, unlicensed streaming sites attract more traffic than legitimate services, depriving creators and distributors of revenue. The absence of robust legal frameworks deters international studios from releasing content simultaneously in the region. Hollywood films often face delays of several weeks to months.

MARKET OPPORTUNITIES

Expansion of Arabic-Language Streaming Platforms with Localized Content

The rise of homegrown over-the-top (OTT) platforms offering original Arabic content is creating new opportunities for the growth of the Middle East media and entertainment market. Shahid, operated by MBC Group, surpassed 40 million monthly active users in 2023, as reported by the company, becoming the region’s leading Arabic streaming service. Similarly, Starzplay has invested over $200 million in Arabic content production since 2020, according to its annual media report, which is targeting underserved genres like crime thrillers and romantic dramas. The success of Ramadan programming, where viewership peaks with family-oriented series, further validates the demand for culturally attuned narratives.

Growth of Esports and Interactive Digital Entertainment

The rise in esports and interactive digital entertainment, with high mobile penetration and youth engagemen,t is expected to fuel the growth of the Middle East media and entertainment market. Dubai has established the Dubai Future District as a hub for gaming startups and metaverse development. Additionally, mobile gaming dominates, representing 78% of total game downloads, as noted by App Annie.

MARKET CHALLENGES

Cultural Resistance to Certain Forms of Entertainment in Conservative Markets

Cultural conservatism in parts of the Middle East continues to constrain the rollout of certain entertainment formats, limiting the growth of the Middle East media and entertainment market. In countries like Kuwait, Oman, and rural areas of Saudi Arabia, public performances involving mixed-gender audiences or Western artistic expressions face resistance from religious and social institutions. In 2023, several concerts in Jordan and Lebanon were canceled due to public backlash over perceived moral violations, as documented by Al Jazeera Media Network. Moreover, content involving LGBTQ+ themes, political satire, or religious critique is routinely banned. This cultural friction limits creative freedom and forces producers to self-censor, reducing the diversity and global competitiveness of regional content. Sustained public education and generational shifts are required to normalize entertainment as a legitimate cultural and economic domain.

Digital Divide Between Urban and Rural Access to Entertainment Platforms

The disparity in digital infrastructure between urban centers and rural or conflict-affected regions is another factor challenging the growth of Middle East media and entertainment market. While cities like Dubai, Riyadh, and Tel Aviv enjoy 5G coverage and high-speed broadband, vast areas in Yemen, Sudan, and eastern Libya suffer from unreliable internet and electricity shortages. In Iraq, the average internet speed is 8.4 Mbps, less than half the global average, as reported by Ookla, hindering video streaming quality. This divide excludes millions from the digital entertainment economy, skewing market growth toward affluent urban consumers. Governments and private players face the dual challenge of expanding infrastructure while ensuring affordability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Platform, Revenue Model, End-User Age Group, Device, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | KSA, UAE, Israel, the Rest of GCC, the Rest of the Middle East |

| Market Leaders Profiled | Middle East Broadcasting Center FZ-LLC (MBC Group), Orbit Showtime Network FZ-LLC, beIN MEDIA GROUP LLC, Abu Dhabi Media Company PJSC, Arab Media Group LLC, and Others. |

SEGMENTAL ANALYSIS

By Type Insights

The advertising segment accounted in holding 41.2% of the Middle East media and entertainment market share in 2024, with the region’s rapid digital transformation and the shift of marketing budgets from traditional to digital platforms. The surge in social media engagement across the Arab world is propelling the growth of the segment. According to the Arab Social Media Report published by the Mohammed Bin Rashid School of Government, the number of social media users in the Middle East reached 190 million in 2023, with an average daily usage of 3.5 hours among the highest globally. Platforms such as Instagram, TikTok, and Snapchat are increasingly used for influencer marketing during Ramadan and national holidays, when brand spending peaks.

The video games segment is expected to grow with an expected CAGR of 12.7% during the forecast period, driven by rising youth engagement, mobile accessibility, and state-backed esports initiatives. The average gamer in Saudi Arabia and the UAE spends 6.8 hours per week on mobile games, according to YouGov, reflecting deep behavioral integration. The government's investment in competitive gaming and digital entertainment infrastructure. As per the International Game Developers Association, the number of gaming studios in the GCC doubled between 2021 and 2023.

COUNTRY-LEVEL ANALYSIS

Saudi Arabia Media and Entertainment Market Insights

Saudi Arabia was the top performer in the Middle East media and entertainment market by capturing 33.2% of the market share in 2024. In 2023, the General Entertainment Authority hosted more than 4,000 events nationwide, attracting over 25 million attendees. The launch of the Saudi Audiovisual Licensing Center has streamlined content production, which is leading to a 70% increase in local film and series output. With 67% of the population under 30 and rising disposable income, domestic demand for music, gaming, and streaming is accelerating, transforming Saudi Arabia into the region’s most influential content market.

United Arab Emirates Media and Entertainment Market Insights

The United Arab Emirates was ranked second with 26.3% of the Middle East media and entertainment market share in 2024. Dubai and Abu Dhabi have established themselves as regional hubs for broadcasting, digital content creation, and international media events. The country leads in digital adoption, with 98% of households having internet access and 85% using streaming platforms. Dubai’s designation as a “Smart City” has accelerated investment in AI-driven content personalization and immersive technologies.

Israel Media and Entertainment Market Insights

Israel media and entertainment market growth is likely to be driven by the advanced digital infrastructure, high-tech content production, and strong presence in gaming and cybersecurity entertainment applications. While smaller in scale, Israel’s influence extends through its dominance in augmented reality (AR), virtual reality (VR), and interactive media development. Platforms like Playtika and Moon Active are among the top-grossing mobile game developers worldwide. Additionally, Israeli public broadcasters have pioneered AI-driven news production and real-time subtitling technologies.

Egypt Media and Entertainment Market Insights

The Egyptian media and entertainment market is anticipated to have lucrative growth opportunities in the coming years. Cairo remains the epicenter of Arabic music, television drama, and cinema, producing over 60% of the region’s Arabic TV series, according to the Egyptian Radio and Television Union. The country’s population of 110 million provides a vast domestic audience, with local content consistently outperforming foreign programming in viewership. In 2023, Egyptian YouTube channels generated over 15 billion views, as reported by Google MENA, driven by comedy, music, and religious content. Despite economic challenges, digital platforms like WatchIt and Anghami are expanding paid subscriptions, with over 8 million active users. The government has launched the “Digital Egypt” initiative to modernize broadcasting infrastructure, signaling a gradual shift toward monetized, high-quality digital content delivery.

COMPETITION OVERVIEW

Competition in the Middle East media and entertainment market is intensifying as legacy broadcasters, state-backed entities, and digital-native platforms vie for audience share in a rapidly evolving landscape. Traditional dominance by pan-Arab satellite channels is being challenged by agile streaming services offering on-demand, ad-free experiences. The entry of global giants like Netflix and Amazon Prime has raised production standards, compelling regional players to innovate in content quality and delivery. At the same time, government-backed initiatives in Saudi Arabia and the UAE are fueling a cultural renaissance, increasing the number of local producers and distributors. Piracy, regulatory fragmentation, and cultural sensitivities remain barriers, but rising investment in Arabic originals, gaming, and live events is creating new battlegrounds.

KEY MARKET PLAYERS

Some of the noteworthy companies in the Middle East media and entertainment market profiled in this report are

- Middle East Broadcasting Center FZ-LLC (MBC Group)

- Orbit Showtime Network FZ-LLC

- beIN MEDIA GROUP LLC

- Abu Dhabi Media Company PJSC

- Arab Media Group LLC

TOP LEADING PLAYERS IN THE MARKET

- MBC Group is a pioneering force in shaping modern Arab media consumption by operating a portfolio of free-to-air and digital platforms that reach over 130 million viewers across the Middle East and North Africa. The company’s flagship streaming service, Shahid, has emerged as the region’s most prominent Arabic-language OTT platform, producing original series such as The Platform and Doubt, which have garnered international acclaim. In recent years, MBC has intensified its digital transformation by launching Shahid VIP with enhanced personalization and 4K streaming capabilities. The company also partnered with Netflix in 2023 to co-produce Arabic content, expanding its creative footprint beyond the region. MBC has further strengthened its position by integrating AI-driven analytics to optimize content scheduling and audience engagement.

- Rotana Media Group is a major player in Arabic music and entertainment, with a legacy spanning over three decades in film, television, and music production. The company manages one of the largest Arabic music catalogs, representing over 5,000 artists, including regional icons like Amr Diab and Elissa. Rotana has expanded its digital presence through its Rotana+ streaming platform, offering a vast library of music videos, films, and live concerts tailored to Arab audiences. In 2023, the company launched a blockchain-based royalty distribution system to ensure transparent compensation for artists, marking a technological leap in the regional music industry. It also invested in high-definition remastering of its classic film archive, preserving cultural heritage while making it accessible to younger, digitally native audiences.

- BeIN Media Group has established itself as a dominant player in premium sports and entertainment broadcasting, operating across 43 countries with a strong foothold in the Middle East and North Africa. Through its BeIN SPORTS network, the company holds exclusive rights to major global events, including FIFA World Cup, UEFA Champions League, and La Liga, making it a gatekeeper of live sports content in the region. In 2023, BeIN launched a dedicated 4K HDR channel for premium sports viewing, enhancing broadcast quality for subscribers. The company also expanded its BeIN SERIES and BeIN MOVIES offerings, investing in Arabic subtitling and dubbing to improve accessibility. To combat piracy, BeIN intensified its digital rights management initiatives, collaborating with regional regulators and internet service providers. Its strategic presence in satellite, IPTV, and OTT platforms ensures multi-channel reach, positioning BeIN as a leader in both content acquisition and distribution innovation.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Middle East media and entertainment market are prioritizing original content production, digital platform integration, and strategic rights acquisition to enhance their competitive standing. Companies are investing heavily in Arabic-language storytelling by focusing on high-budget series and localized adaptations to capture domestic audiences. Expansion into streaming and OTT services is being accelerated through AI-driven personalization, multi-device compatibility, and subscription bundling with telecom providers. Strategic partnerships with global platforms enable co-production and international distribution. Anti-piracy enforcement and blockchain-based royalty systems are being adopted to protect intellectual property. Additionally, integration with live events, esports, and social media influencers is enhancing audience engagement, while government-backed cultural initiatives are leveraged to secure funding and regulatory support for large-scale content development.

RECENT MARKET DEVELOPMENTS

- In January 2023, MBC Group launched a strategic collaboration with Netflix to co-produce original Arabic series by enhancing content quality and expanding international distribution for regional storytelling.

- In May 2023, Rotana Media Group introduced a blockchain-based royalty system to ensure transparent and timely payments to over 5,000 affiliated artists, which is setting a new standard for music rights management in the Arab world.

- In September 2023, BeIN Media Group secured exclusive broadcasting rights for the 2023 AFC Asian Cup with its dominance in live sports coverage across the Middle East and North Africa.

- In February 2024, MBC Group upgraded Shahid with AI-powered recommendation engines and 4K streaming, significantly improving user experience and viewer retention rates.

- In June 2024, Rotana launched a high-definition remastering initiative for 200 classic Arabic films, preserving cultural heritage while making it accessible to new generations through its Rotana+ platform.

MARKET SEGMENTATION

This Middle East media and entertainment market research report is segmented and sub-segmented into the following categories.

By Type

- Digital Music

- Music Downloads

- Music Streaming

- Video Games

- Video-on-Demand

- Subscription VoD (SVoD)

- Transaction VoD (TVoD)

- Electronic Sell-Through/Downloads

- E-Publishing

- Advertising

- Digital Advertising

- Newspaper

- Magazine

- Television

- Radio

- Outdoor Advertising

- Internet Access Services

By Platform

- Online/Digital

- Traditional/Linear

- Hybrid (Omnichannel)

By Revenue Model

- Subscription-Based

- Advertising-Supported

- Pay-Per-View/Transactional

- Freemium/In-App Purchase

By End-User Age Group

- Generation Z (≤24)

- Millennials (25-40)

- Generation X (41-56)

- Baby Boomers (57+)

By Device

- Smartphones

- Smart TVs and Connected TV Devices

- PCs and Laptops

- Tablets

- Gaming Consoles

- VR/AR Headsets

By Country

- KSA

- UAE

- Israel

- The rest of the GCC countries

- Rest of the Middle East

Frequently Asked Questions

1. What is the Middle East Media and Entertainment Market?

The Middle East Media and Entertainment Market includes digital and traditional media, streaming, gaming, VOD, advertising, music, e-publishing, and live events targeting the MENA region's diverse audiences

2. What drives growth in the Middle East Media and Entertainment Market?

Key drivers are rising internet and smartphone penetration, a large and young population, booming gaming and streaming demand, government investment, and rapid rollout of 5G and fiber networks

3. Which countries are leading the Middle East Media and Entertainment Market?

Saudi Arabia (33.2% market share in 2025) and the UAE are the largest contributors, driven by economic reforms and progressive digital media policies

4. What are the major segments in the Middle East Media and Entertainment Market?

Segments include digital music, video games, video-on-demand (SVoD, TVoD), e-publishing, advertising (especially digital), TV/radio broadcasting, and cinema

5. How is the Middle East gaming and esports sector performing?

Gaming and esports are some of the fastest-growing sectors, supported by investment in tournaments, mobile gaming, VR/AR, and youth engagement

6. How important is local content in the Middle East Media and Entertainment Market?

Localized, culturally relevant, and Arabic-language content is critical, with increasing investment in regional production and original programming for VOD and TV

7. Which companies are key players in the Middle East Media and Entertainment Market?

Major companies include MBC Group, beIN Media Group, Intigral, OSN, Zawya (Refinitiv), Orbit Showtime Network, and Abu Dhabi Media

8. What trends are shaping consumer behavior in the Middle East Media and Entertainment Market?

Trends include mobile-first media consumption, Gen Z’s preference for interactive and short video, increased SVOD adoption, and social media’s influence on entertainment choices

9. How fast is digital advertising growing in the Middle East?

Digital advertising is among the fastest-growing segments, with adoption of programmatic tech and audience targeting driving double-digit growth by 2033.

10. How does government regulation impact the Middle East Media and Entertainment Market?

Strict content regulation and censorship affect programming; however, reforms and incentives for original production are creating new opportunities

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com