Middle East Smartphone Market Size, Share, Trends & Growth Forecast Report By Operating System (Android, iOS, Windows, Others (Linux)), Distribution Channel (OEMs Stores, Retailer, E-Commerce), and Country (KSA, UAE, Israel, Rest of GCC Countries, Rest of Middle East) – Industry Analysis, 2026 to 2034

Middle East Smartphone Market Size

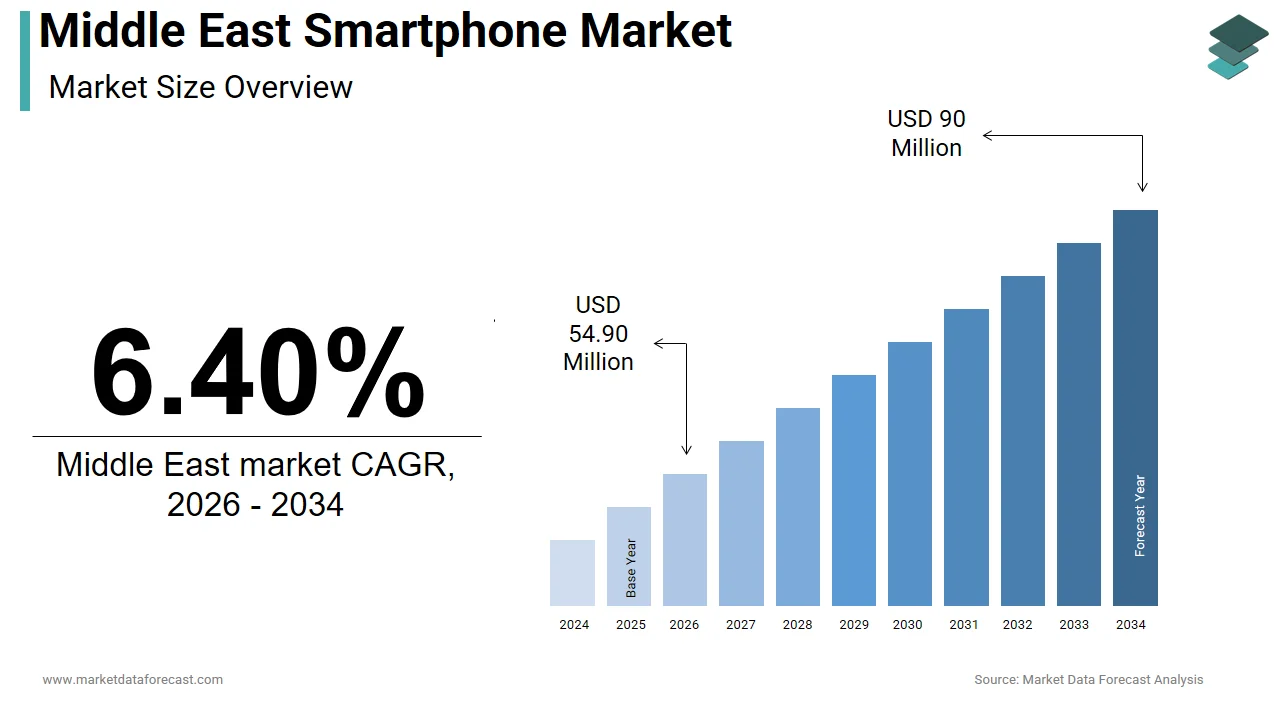

The Middle East smartphone market was valued at USD 51.6 million in 2025, is estimated to reach USD 54.90 million in 2026, and is projected to reach USD 90 million by 2034, growing at a CAGR of 6.40% from 2026 to 2034.

The Smartphone market encompasses the sale, distribution, and technological adoption of mobile devices across GCC and non-GCC nations, deeply influenced by digital transformation policies, youth demographics, and economic diversification agendas. As of 2023, smartphone penetration in the region reached 82% of the population, according to the International Telecommunication Union (ITU), driven by widespread 4G infrastructure and government-led smart city initiatives. In Saudi Arabia, Vision 2030 has accelerated digital inclusion, with most citizens accessing government services via mobile apps, as reported by the Ministry of Communications and Information Technology. The UAE leads in 5G readiness, with 94% population coverage as of 2023, as per the Telecommunications and Digital Government Regulatory Authority (TDRA). These developments underscore the smartphone’s role not merely as a communication tool but as a gateway to financial, educational, and administrative ecosystems across the region.

MARKET DRIVERS

Rapid Digital Government Transformation

Governments across the Middle East are mandating digital service delivery, compelling citizens to adopt smartphones for daily interactions. In the UAE, over 200 government services are exclusively accessible through the UAE Pass digital identity app, with 4.3 million active users recorded in 2023, as per the Smart Dubai Office. Similarly, Saudi Arabia’s Absher platform, used by over 18 million individuals, requires smartphone access for employment, travel, and healthcare services, according to the Ministry of Interior. In Bahrain, the BeAware Bahrain app became essential during public health monitoring, accelerating smartphone adoption among older demographics. These state-driven digital mandates have transformed smartphones into essential utilities.

Youth-Driven Demand for Mobile-First Lifestyles

The Middle East hosts one of the world’s youngest populations, with 60% of its citizens under the age of 30, according to the United Nations Economic and Social Commission for Western Asia (ESCWA). This demographic is inherently mobile-native, relying on smartphones for social engagement, content creation, and digital commerce. TikTok, Instagram, and Snapchat rank among the most-used apps. The rise of mobile gaming, live streaming, and influencer culture further entrenches smartphone dependency, making device ownership a social necessity rather than a luxury, particularly among university students and young professionals.

MARKET RESTRAINTS

High Import Tariffs and Regulatory Barriers in Non-GCC Countries

Several Middle Eastern nations impose steep import duties on smartphones, limiting affordability and market expansion. In Iraq, import tariffs on mobile devices are high, inflating retail prices compared to Gulf markets. Lebanon’s financial crisis has exacerbated import restrictions, with customs delays averaging 45 days for electronics shipments, according to the Beirut Chamber of Commerce. These structural impediments suppress device turnover and hinder the penetration of newer models, particularly in low-income regions where second-hand or outdated devices dominate, constraining the overall growth trajectory of the regional market.

Persistent Digital Literacy Gaps Among Older Populations

Despite high connectivity, a significant portion of adults over 50 in the Middle East lacks the skills to fully utilize smartphones beyond basic calling. In Jordan, only a limited share of individuals aged 50–64 use smartphones for internet-based services, according to the Department of Statistics. Also, a notable share of elderly respondents in rural Saudi Arabia avoid mobile banking due to fear of fraud or technical complexity. In Iran, digital literacy rates among women over 60 are low, limiting the reach of mobile health and e-commerce platforms. These gaps reduce effective smartphone utilization and slow the adoption of value-added services, undermining the potential for inclusive digital transformation across the region.

MARKET OPPORTUNITIES

Expansion of Mobile Financial Services and Digital Wallets

The rise of fintech platforms is creating a powerful incentive for smartphone adoption, particularly in underbanked populations. In the UAE, digital wallet transactions reached AED 147 billion in 2023, a 39% increase from the previous year, according to the Central Bank of the UAE. Saudi Arabia’s STC Pay now serves over 12 million users, enabling peer-to-peer transfers, bill payments, and microloans via smartphone. In Egypt, Vodafone Cash has a large base of active users, driving demand for affordable smartphones capable of running financial apps. This financial inclusion trend is transforming smartphones into essential economic tools, especially in rural and semi-urban areas.

Growth of Localized Arabic Content and App Ecosystems

The proliferation of Arabic-language digital content is enhancing smartphone relevance across the region. Arabic content online grew between 2020 and 2023, with platforms like MBC Shahid and Tamatem Games attracting millions of mobile users. Tamatem, a Jordan-based mobile gaming company, reported a year-on-year increase in downloads in 2023, catering specifically to Arabic-speaking audiences. Educational apps such as Noon Academy and Darsak have gained traction, with millions of students using smartphones for remote learning in K-12 and higher education. This cultural localization increases engagement and retention, making smartphones indispensable for knowledge access and entertainment in native linguistic contexts.

MARKET CHALLENGES

Shortage of Skilled Local Workforce in Mobile Technology Development

The Middle East faces a deficit in homegrown software developers and mobile engineers, limiting innovation and increasing dependency on foreign tech Also, only a small share of STEM graduates in the region specialize in software or telecommunications, with most pursuing careers in oil and gas or public administration. In Saudi Arabia, despite Vision 2030’s emphasis on digital transformation, most of mobile app development is outsourced to Indian and Eastern European firms. The UAE’s Dubai Future Foundation acknowledges a shortage of 12,000 qualified digital talent by 2025, hindering the development of region-specific applications and security frameworks essential for sustainable smartphone ecosystem growth.

Environmental and E-Waste Management Pressures

The rapid turnover of smartphones is generating significant electronic waste, with limited regional recycling infrastructure. According to the United Nations Institute for Training and Research (UNITAR), the Middle East produces over 2.1 million tonnes of e-waste annually, yet only 14% is formally recycled. In Egypt, discarded smartphones contribute to 38% of urban e-waste, often ending up in informal landfills or being dismantled under hazardous conditions, as per the Egyptian Environmental Affairs Agency. The UAE generates 24 kg of e-waste per capita annually, the highest in the region, according to the Emirates Wildlife Society. Without robust take-back programs and regulatory enforcement, the environmental cost of smartphone proliferation threatens long-term sustainability, particularly as device replacement cycles shorten to under 2.5 years in affluent markets.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Operating System, Distribution Channel, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | KSA, UAE, Israel, the Rest of GCC, the Rest of Middle East |

| Market Leaders Profiled | Samsung Electronics Co. Ltd, Huawei Technologies Co. Ltd, Apple Inc., Xiaomi Corporation, BBK Electronics Corporation, Lenovo Group Limited, HTC Corporation, HMD Global Oy, Sony Corporation, ZTE Corporation, Google LLC, and Others. |

SEGMENTAL ANALYSIS

By Operating System Insights

The android segment dominated the Middle East smartphone market by capturing a substantial share of operating system usage in 2025. This lead position is primarily driven by its integration into a broad spectrum of devices across price tiers, making it accessible to diverse income groups. In Egypt, Android powers most smartphones, largely due to the affordability of entry-level models from brands like Tecno, Infinix, and Samsung’s Galaxy A series, according to the National Telecom Regulatory Authority. The open-source nature of Android enables local customization, with Arabic language support, regional app stores, and compatibility with dual-SIM functionality critical in markets where users maintain multiple carriers for cost efficiency. Google’s ecosystem integration, including YouTube, Google Maps, and Gmail, further entrenches user dependency, particularly among younger demographics who rely on these platforms for education, navigation, and entertainment.

The iOS segment is the fastest-growing operating system in the region and is achieving a CAGR of 7.6% between 2026 and 2034. This growth is fueled by rising disposable incomes and the increasing perception of iPhones as status symbols in affluent urban centers. In the UAE, iPhone penetration is high among high-income households in 2023, driven by strong brand loyalty and seamless integration with other Apple devices. Saudi Arabia witnessed a year-on-year increase in iPhone 15 sales, attributed to expanded carrier financing plans and trade-in programs. Additionally, the expansion of Apple’s official retail presence has enhanced consumer trust and after-sales service accessibility, reinforcing its premium appeal.

By Distribution Channel Insights

The retailers segment constituted the prominent distribution channel in the Middle East smartphone market by commanding 56.3% of total sales in 2024. This dominance is due to the extensive network of independent and chain electronics stores that offer immediate device access, hands-on experience, and instant activation services. In Saudi Arabia, retail outlets such as eXtra and Jazeel dominate smartphone sales, particularly in secondary cities where e-commerce logistics remain underdeveloped. Besides, retail kiosks in malls like Riyadh Park and City Centre Beirut serve as critical touchpoints for brand visibility and last-minute decision-making, reinforcing their centrality in consumer purchasing journeys.

The e-commerce is the fastest-growing distribution channel and is registering a CAGR of 16.3% from 2025 to 203. This surge is propelled by enhanced digital trust, same-day delivery, and exclusive online promotions. In the UAE, online smartphone sales surged notably. Platforms like Noon, Amazon.ae, and Sharaf DG’s e-store have introduced live chat support, installment payments via Tabby and Tamara, and virtual unboxing experiences to replicate in-store confidence. With improved last-mile logistics and secure payment gateways, e-commerce is redefining accessibility, especially for tech-savvy youth and remote populations.

COUNTRY-LEVEL ANALYSIS

Saudi Arabia Smartphone Market Insights

Saudi Arabia led the MEA smartphone market with a 29.5% share in 2024. It is driven by Vision 2030’s digital transformation agenda and a young, tech-enthusiastic population. As per the Ministry of Communications and Information Technology, smartphone subscriptions increased notably in 2023, surpassing the country’s population due to multiple SIM ownership. The government’s Smart Cities program has accelerated 5G adoption. E-government services like Absher and Tawakkalna have institutionalized smartphone dependency, while rising female workforce participation has increased device ownership among women. Retail expansion by brands like Samsung and Apple, coupled with aggressive carrier financing, has made high-end models more accessible, positioning Saudi Arabia as the region’s most dynamic smartphone market.

The United Arab Emirates Smartphone Market Insights

The United Arab Emirates holds a significant market share and is distinguished by its high smartphone penetration and early adoption of advanced technologies. According to the Telecommunications and Digital Government Regulatory Authority (TDRA), mobile subscription density stands at 138%, with nearly every resident owning at least one device. Dubai and Abu Dhabi serve as regional launch hubs for flagship models, with brands like Xiaomi and OnePlus hosting global unveilings in the emirates. With one of the world’s highest per capita incomes, the UAE remains a premium market for cutting-edge mobile technology.

Egypt Smartphone Market Insights

Egypt commands a notable share of the MEA smartphone market, anchored by its massive population and growing digital economy. As per the National Telecom Regulatory Authority, Egypt had over 72 million smartphone users in 2023, representing 70% of the population. The affordability of Chinese brands like Tecno and Realme has driven mass adoption, particularly among youth and low-income groups. Mobile internet usage surged, fueled by social media and mobile banking. Government initiatives like Digital Egypt have expanded connectivity in rural areas, while fintech apps such as Vodafone Cash incentivize smartphone ownership as a financial tool, making Egypt a critical volume-driven market.

Israel Smartphone Market Insights

Israel holds a notable share of the regional market and is characterized by high innovation, advanced R&D, and strong cybersecurity integration in mobile technology. According to the Israel Central Bureau of Statistics, smartphone penetration exceeds 85%, with 3.8 million active devices in 2023. The country’s tech-savvy population demands high-performance devices, favoring brands with robust encryption and enterprise capabilities. Israeli startups are pioneering mobile AI, biometric authentication, and secure communications apps, influencing global smartphone features. While device sales volume is modest, Israel’s influence on mobile software and security standards gives it disproportionate strategic importance in the regional tech landscape.

Kuwait Smartphone Market Insights

Kuwait is marked by high per capita spending and a preference for premium devices. The country’s dense urbanization and advanced telecom infrastructure support rapid adoption of new technologies, including 5G. Retail chains like Mobile Zone and eStore offer interest-free installment plans, facilitating high-end purchases. Additionally, Kuwait’s youthful population drives demand for gaming, photography, and social media-centric devices, reinforcing its position as a trend-sensitive, high-value market.

COMPETITIVE LANDSCAPE

Competition in the Middle East smartphone market is intense, shaped by a convergence of global brands and evolving consumer expectations. While Samsung leads with broad portfolio coverage, Apple is gaining ground through ecosystem integration and premium retail experiences. Chinese brands like Xiaomi, Oppo, and Realme challenge with value-driven innovation, capturing youth and price-sensitive segments. Differentiation arises from after-sales service, localized software features, and 5G readiness. Carrier partnerships and financing models are critical levers for market access, especially in high-cost economies. The rise of e-commerce and digital engagement further intensifies rivalry, compelling brands to blend technological performance with cultural relevance to sustain loyalty in a dynamic, rapidly digitizing region.

KEY MARKET PLAYERS

Some of the noteworthy companies in the Middle East Smartphone market profiled in this report are

- Samsung Electronics Co. Ltd

- Huawei Technologies Co. Ltd

- Apple Inc.

- Xiaomi Corporation

- BBK Electronics Corporation

- Lenovo Group Limited

- HTC Corporation

- HMD Global Oy

- Sony Corporation

- ZTE Corporation

- Google LLC

TOP LEADING PLAYERS IN THE MARKET

- Samsung Electronics maintains a dominant presence in the Middle East smartphone market through its extensive product range, localized marketing, and robust distribution network. The company has strengthened its position by launching region-specific models such as the Galaxy M series, tailored for extended battery life critical in areas with inconsistent power supply. In 2023, Samsung opened the Samsung Experience Store in Dubai Mall, integrating immersive AR demonstrations and instant repair services to enhance customer engagement. It also partnered with STC and Etisalat to offer bundled 5G plans with new Galaxy devices, accelerating adoption of its latest flagships. By sponsoring major regional events like Dubai Shopping Festival and investing in Arabic-language AI for its Bixby assistant, Samsung reinforces cultural relevance and technological leadership in the Middle East smartphone market.

- Apple Inc. has significantly expanded its influence in the Middle East by establishing its first official retail presence with the launch of Apple Dubai Mall in May 2023. This flagship store serves as a hub for product demonstrations, developer workshops, and Today at Apple sessions, fostering deeper consumer engagement. Apple has localized its ecosystem by enhancing Arabic Siri capabilities and introducing region-specific payment integrations with Mada in Saudi Arabia and BENEFIT in Bahrain. In 2024, the company collaborated with du and Ooredoo to offer exclusive trade-in and installment plans, making iPhones more accessible. Additionally, Apple’s App Store now features a curated selection of Arabic apps and content, strengthening its ecosystem appeal among bilingual users and reinforcing its premium positioning in the Middle East smartphone market.

- Xiaomi Corporation has gained substantial traction in the Middle East by offering high-specification devices at competitive price points, particularly appealing to younger, budget-conscious consumers. The company intensified its regional commitment in 2023 by launching a dedicated Middle East R&D center in Dubai Internet City focused on optimizing MIUI for Arabic users and improving thermal performance in high-temperature environments. Xiaomi also expanded its offline footprint through partnerships with retailers like Jazeel and Emax, ensuring wide availability across Saudi Arabia and Egypt. In early 2024, it introduced a regional warranty expansion, offering two-year coverage in select markets, a move that significantly boosted consumer confidence. Through aggressive digital marketing and sponsorship of tech expos like Gitex, Xiaomi continues to solidify its value-driven brand identity in the Middle East smartphone market.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Middle East smartphone market are deploying localized product development, strategic retail expansion, and carrier partnerships to strengthen market penetration. Companies are optimizing software for Arabic language support, dual-SIM functionality, and heat-resistant hardware to meet regional demands. Premium brands are enhancing customer experience through flagship stores and in-store tech support, while mid-tier manufacturers focus on e-commerce and installment financing. Collaborations with telecom providers for 5G bundling and trade-in programs are driving upgrades. Additionally, investment in after-sales service networks and extended warranties is improving brand trust, particularly in markets with high device turnover and growing consumer expectations for reliability and support.

RECENT MARKET DEVELOPMENTS

- In May 2023, Apple opened its first official retail store at Dubai Mall, offering immersive product experiences and localized services, reinforcing its premium brand presence in the Middle East smartphone market.

- In September 2023, Samsung launched a regional 5G accelerator program in Riyadh, collaborating with Saudi developers to optimize apps for its devices, enhancing ecosystem integration in the Middle East smartphone market.

- In January 2024, Xiaomi introduced a two-year warranty for smartphones in Egypt and Jordan, significantly improving consumer confidence and after-sales trust in the Middle East smartphone market.

- In November 2023, Oppo partnered with Etisalat UAE to offer exclusive bundled 5G data plans with its Find X6 series, boosting high-end device adoption in the Middle East smartphone market.

- In July 2023, Tecno Mobile launched a new thermal management system in its Phantom V series, specifically engineered for Middle East climates, improving device performance and reliability in the Middle East smartphone market.

MARKET SEGMENTATION

This Middle East Smartphone market research report is segmented and sub-segmented into the following categories.

By Operating System

- Android

- iOS

- Windows

- Others (Linux)

By Distribution Channel

- OEMs Stores

- Retailer

- E-Commerce

By Country

- KSA

- UAE

- Israel

- Rest of GCC countries

- Rest of Middle East

Frequently Asked Questions

1. Who are the key brands in the Middle East Smartphone Market?

Samsung leads with a 34% market share, followed by Xiaomi, TRANSSION, HONOR, and Apple. HONOR showed a 95% growth in Q2 2025 driven by AI-rich devices and retail expansion

2. What drives growth in the Middle East Smartphone Market?

Growth drivers include higher consumer demand for premium and mid-range AI-enabled devices, aggressive retail promotions, rising digital engagement, and expanding 5G adoption

3. How has 5G adoption influenced the Middle East Smartphone Market?

5G adoption is growing but not a primary upgrade driver yet. AI-capable models accounted for 53% of Q1 2025 shipments, indicating a shift towards smarter, experience-led devices

4. How did Ramadan and regional holidays affect smartphone sales in early 2025?

Lower spending during Ramadan shifted budgets to lifestyle segments such as travel and automotive, limiting discretionary spending on smartphones

5. What is the impact of regional economic factors on smartphone sales?

Falling oil prices and increased tariffs have strained consumer spending, especially in oil-dependent economies like Saudi Arabia and Iraq, leading to cautious consumption

6. What role do retail promotions play in the Middle East Smartphone Market?

Retail promotions during events like the Hala Festival in Kuwait and Eid al-Fitr in UAE significantly boosted sales and consumer interest

7. What impact do mobile network operators have on the smartphone market?

Operators such as e& (formerly Etisalat) in UAE have strategic partnerships with brands like Samsung to deepen ecosystem integration and drive sales.

8. How important is AI in the smartphone purchase decision in the Middle East?

AI-powered features like real-time translation, personalized content, and smart assistants are key selling points influencing consumer preferences.

9. What are the major challenges facing the Middle East Smartphone Market?

Challenges include rising retail costs, economic uncertainty, complex trade dynamics, and potential supply chain disruptions affecting availability and pricing

10. How do consumer preferences vary across Middle East countries?

While Saudi Arabia and Iraq show more budget-conscious behavior recently, Kuwait and Qatar consumers focus more on premium products and luxury brands

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com