North America Marine Diesel Engine Market Size, Share, Trends, & Growth Forecast Report Segmented By Technology, Application, Power, Country (The United States, Canada, Mexico), Industry Analysis From 2025 to 2033

North America Marine Diesel Engine Market Size

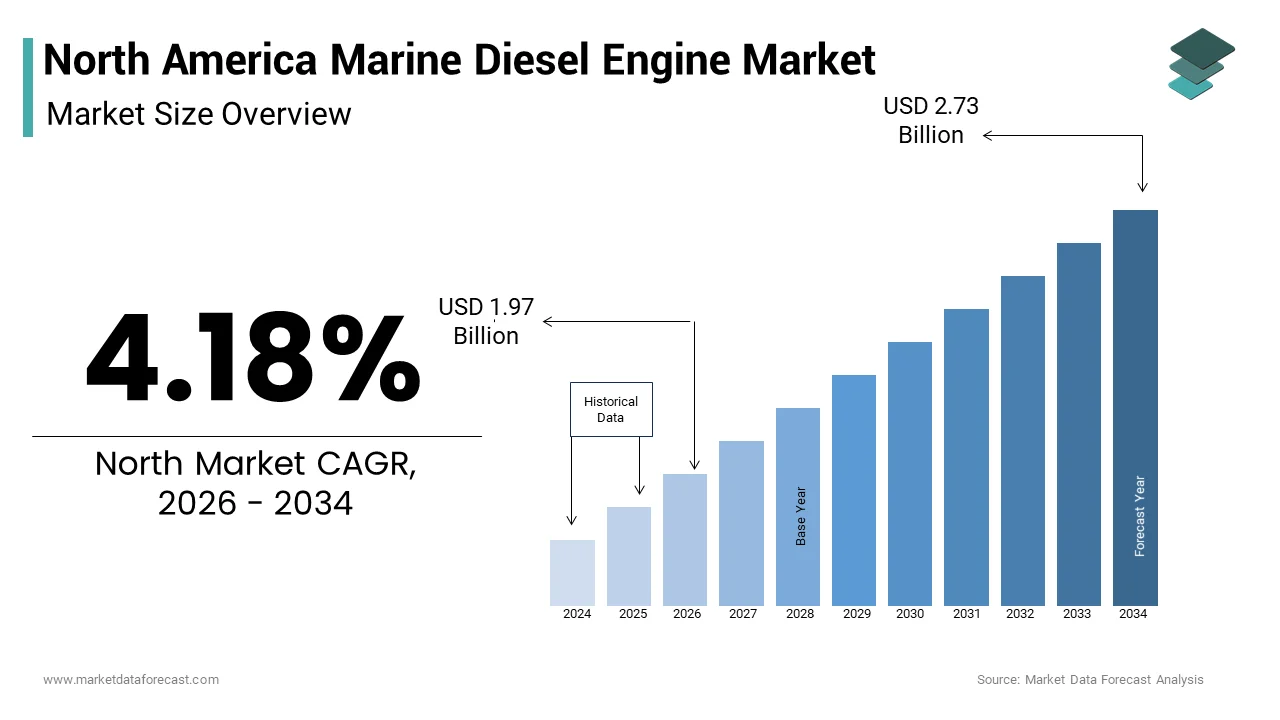

The North America marine diesel engine market was valued at USD 1.82 billion in 2024 and is anticipated to reach USD 1.89 billion in 2025 to USD 2.67 billion by 2033, growing at a CAGR of 4.18% during the forecast period from 2025 to 2033.

Marine diesel engines are diesel-powered propulsion and auxiliary engines used across commercial, recreational, and defense maritime vessels. These engines are critical for operations in cargo ships, fishing boats, offshore support vessels, yachts, and naval fleets. The market is primarily driven by the demand for fuel-efficient, durable, and high-torque engines suitable for long-haul and rough-water navigation. In recent years, technological advancements have led to the integration of emission-compliant and fuel-optimized engines, aligning with regulatory frameworks such as the U.S. Environmental Protection Agency (EPA) Tier 4 standards and the International Maritime Organization (IMO) sulfur cap regulations.

The United States dominates the regional market. Canada and Mexico follow with a growing emphasis on modernizing inland waterway transport and fishing fleets. The U.S. commercial fishing industry alone operates more than 10,000 vessels, the majority of which rely on diesel propulsion systems, according to the National Oceanic and Atmospheric Administration (NOAA).

MARKET DRIVERS

Expansion of Offshore Oil & Gas Exploration Activities

The sustained expansion of offshore oil and gas exploration activities, particularly in the Gulf of Mexico, is one of the primary drivers of the North American marine diesel engine market. As per the U.S. Energy Information Administration (EIA), the Gulf of Mexico accounted for approximately 15% of total U.S. crude oil production and 5% of dry natural gas production. This has led to increased deployment of offshore support vessels (OSVs), anchor handling tug supply (AHTS) vessels, and platform supply vessels (PSVs), all of which rely heavily on marine diesel engines for propulsion and operational support.

These vessels typically use high-horsepower diesel engines from manufacturers such as Caterpillar, Cummins, and Wärtsilä, known for their reliability and compliance with EPA Tier 4 emission standards. Moreover, the Biden administration’s offshore leasing plans, including the Central and Western Gulf of Mexico lease sales in 2024, are expected to further stimulate demand for marine diesel engines.

Growth in Recreational Boating and Yacht Manufacturing

The surge in recreational boating and luxury yacht manufacturing in North America has significantly contributed to the demand for marine diesel engines. Diesel engines are preferred in the mid-to-high-end recreational segment due to their superior fuel efficiency, longer engine life, and enhanced torque output compared to gasoline engines. Additionally, companies such as Viking Yacht, Hatteras Yachts, and Beneteau North America are increasingly integrating advanced diesel engines that meet Tier 4 Final emission standards, further boosting market demand. The expansion of marina infrastructure and the rise in marine tourism also support the ongoing growth of this segment.

MARKET RESTRAINTS

Stringent Emission Regulations and Compliance Costs

The imposition of increasingly stringent emission regulations by both federal and international bodies is one of the major restraints affecting the North American marine diesel engine market. The U.S. Environmental Protection Agency (EPA) has enforced Tier 4 Final emission standards for marine diesel engines above 600 kW, requiring a significant reduction in nitrogen oxides (NOx) and particulate matter (PM). Compliance with these standards necessitates the integration of advanced after-treatment systems such as selective catalytic reduction (SCR) and diesel particulate filters (DPF), which substantially increase the cost and complexity of engine manufacturing.

This has placed financial pressure on smaller manufacturers and operators, particularly in the fishing and inland shipping sectors, where budget constraints are more pronounced. Furthermore, the International Maritime Organization’s (IMO) 2023 update to the NOx Technical Code and the upcoming Carbon Intensity Indicator (CII) regulations for commercial vessels are expected to further tighten emission norms. These regulatory pressures are compelling engine manufacturers to invest heavily in research and development, which may slow the adoption of new engines in cost-sensitive segments of the market.

Decline in Traditional Commercial Fishing Vessel Operations

The decline in traditional commercial fishing vessel operations, particularly in the northeastern U.S. and Atlantic Canada, has had a measurable impact on the demand for marine diesel engines. This decline is attributed to a combination of factors, including stricter catch limits imposed by regional fisheries management councils, rising fuel costs, and aging fleets. Additionally, the shift toward aquaculture and offshore fish farming, which requires different propulsion systems and smaller vessels, has not yet fully offset the decline in traditional fishing operations. As a result, engine manufacturers are facing a shrinking base of traditional customers, which is acting as a restraint on market growth.

MARKET OPPORTUNITY

Electrification and Hybridization of Marine Vessels

The electrification and hybridization of marine vessels is a significant opportunity for growth in the North American marine diesel engine market. While pure electric propulsion is still limited to smaller and short-range vessels, hybrid systems that combine diesel engines with battery storage are gaining traction across multiple maritime segments. Hybrid diesel-electric systems allow for reduced fuel consumption and emissions by enabling engines to operate at optimal efficiency levels. These systems retain diesel engines as the primary power source while integrating electric motors for peak shaving and low-load operations.

Furthermore, the U.S. Department of Transportation’s Maritime Administration (MARAD) has allocated over $250 million in funding for green maritime technology projects under the 2023 Bipartisan Infrastructure Law. This includes grants for the development of dual-fuel and hybrid propulsion systems, which are expected to drive demand for next-generation diesel engines capable of integration with electric systems. Major engine manufacturers such as Cummins and Rolls-Royce are already developing modular diesel-electric hybrid platforms tailored for North American applications.

Modernization of Naval and Coast Guard Fleets

The modernization of naval and coast guard fleets presents a robust growth opportunity for the North American marine diesel engine market. These platforms often incorporate diesel-electric propulsion systems or auxiliary diesel generators for enhanced efficiency and stealth capabilities. For example, the new Constellation-class frigates being built by Fincantieri Marinette Marine use a combined diesel-electric and gas (CODLAG) propulsion system, which includes advanced diesel engines from MTU Friedrichshafen.

Additionally, the U.S. Coast Guard’s Polar Security Cutter (PSC) program aims to replace aging icebreakers with six new vessels, each powered by diesel-electric propulsion. These fleet modernization initiatives are expected to sustain engine demand over the next decade, offering substantial growth potential for manufacturers with specialized defense-grade propulsion solutions.

MARKET CHALLENGES

Supply Chain Disruptions and Component Shortages

Supply chain disruptions and component shortages have emerged as a significant challenge for the North American marine diesel engine market. The global semiconductor shortage, which began in 2021 and persisted through 2023, affected the production of electronic engine control modules and onboard diagnostics systems, essential for Tier 4-compliant engines. Moreover, geopolitical tensions and trade restrictions have impacted the availability of critical raw materials such as rare earth metals used in electric components and catalytic converters. Delays in component delivery have resulted in extended lead times for engine manufacturers, with some lead times increasing from 12 weeks to over 24 weeks in 2023. Additionally, port congestion and shipping delays have further complicated logistics. The Port of Los Angeles, one of the busiest ports in the U.S., reported an average container dwell time that was higher in 2023, compared to 2019. These disruptions have led to increased costs and production bottlenecks, challenging manufacturers’ ability to meet growing demand in key sectors such as offshore logistics and naval modernization.

Rising Fuel Prices and Operating Costs

Rising fuel prices and associated operating costs pose a major challenge to the North American marine diesel engine market. This has placed financial pressure on vessel operators, especially in cost-sensitive segments such as commercial fishing, inland shipping, and recreational boating. However, the upfront cost of such modifications often deters smaller operators, slowing adoption rates. Additionally, these trends indicate a growing sensitivity to fuel prices, which could potentially dampen future demand for marine diesel engines unless more fuel-efficient or alternative propulsion technologies become more accessible and affordable.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 4.18% |

| Segments Covered | By Type, Application, Source, Mode of Application, and Region. |

| Various Analyses Covered | Global, Regional, & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | The USA, Canada, Mexico, and the rest of North America |

| Market Leaders Profiled | AB Volvo, Anglo Belgian, Caterpillar, Cummins, Daihatsu Diesel, Deere & Company, DEUTZ, Hyundai, IHI Corporation, Kawasaki Heavy Industries, MAN Energy Solutions, Rolls-Royce, Scania, Siemens, STX Heavy Industries, Wartsila, Yanmar, and Yuchai International. |

SEGMENTAL ANALYSIS

By Technology Insights

Medium Speed Marine Diesel Engines

The medium speed marine diesel engine segment led the North America marine diesel engine market by accounting for 47.4% of total engine installations in 2024. These engines typically operate between 300 and 1,500 revolutions per minute (RPM) and are widely used in offshore support vessels, ferries, cargo ships, and naval patrol boats due to their optimal balance between fuel efficiency, power output, and reliability. Among the key drivers of this segment is the widespread adoption of medium-speed engines in offshore logistics and supply chain operations. These vessels predominantly use medium-speed engines from manufacturers such as Caterpillar Marine, Cummins, and Rolls-Royce Power Systems. Additionally, the modernization of ferry fleets across the U.S. and Canada is contributing to the dominance of this segment.

High Speed Marine Diesel Engines

The high-speed marine diesel engine segment is projected to grow at the fastest CAGR of 6.2% between 2025 and 2033. The surge in recreational boating activity across North America is a major driver of this segment. High-speed diesel engines are increasingly preferred in boats over 25 feet due to their improved fuel economy and durability compared to gasoline engines. These speed engines, which operate above 1,500 RPM, are primarily used in recreational boats, patrol vessels, and fast ferries, where compact size, lightweight design, and rapid acceleration are essential. Another key growth factor is the U.S. Coast Guard’s initiative to modernize its fast response cutter (FRC) fleet, which relies on high-speed diesel engines for rapid deployment and agility.

By Application Insights

Offshore Application

The offshore application segment accounted for the largest share of the North America marine diesel engine market of 35.5% of total engine installations in 2024. Continued expansion of offshore oil and gas operations is a primary driver of this segment. According to the U.S. Energy Information Administration (EIA), the Gulf of Mexico accounted for 17% of total U.S. crude oil production and 5% of dry natural gas production in 2023. This segment includes engines used in offshore support vessels (OSVs), anchor handling tug supply (AHTS) vessels, and platform supply vessels (PSVs), which are essential for oil and gas exploration and production activities in the Gulf of Mexico and offshore Canada. Additionally, the increasing deployment of subsea production systems and floating production storage and offloading (FPSO) units has led to a growing requirement for advanced propulsion and auxiliary engines.

Cruise & Ferry Application

The cruise & ferry application segment is projected to grow at the fastest CAGR of 6.8% between 2025 and 2033. The resurgence of the cruise and ferry industry post-pandemic and the ongoing fleet modernization efforts across North America are primarily driving the growth of this segment. With major cruise operators such as Carnival Corporation and Royal Caribbean investing in newbuilds and retrofits, there has been a corresponding increase in demand for marine diesel engines, particularly those compatible with dual-fuel or hybrid configurations. Additionally, the U.S. Department of Transportation’s Maritime Administration (MARAD) has allocated over $250 million in green maritime grants under the 2023 Bipartisan Infrastructure Law, supporting the adoption of cleaner propulsion technologies. These initiatives are expected to further accelerate the growth of the cruise & ferry engine segment in the coming years.

By Power Insights

1,000–5,000 HP Range

The 1,000–5,000 horsepower (HP) power segment spearheaded the North America marine diesel engine market by capturing 42.6% of total engine installations in 2024. One of the key drivers of this segment is the booming recreational boating industry in the U.S. This power range is widely used in recreational boats, fishing vessels, inland cargo barges, and smaller offshore support vessels, making it the most versatile and widely adopted engine category. Another major factor contributing to the dominance of this segment is the continued reliance on diesel engines in the commercial fishing industry.

10,001–20,000 HP Range

The 10,001–20,000 HP engine segment is projected to grow at the fastest CAGR of 6.5% between 2025 and 2033. This power range is primarily used in large ferries, coast guard vessels, and mid-sized cargo ships, where higher propulsion power and fuel efficiency are critical. A primary driver of this segment is the modernization of the U.S. Coast Guard and Navy fleets. The U.S. Department of Homeland Security has been expanding its fleet of fast response cutters (FRCs) and national security cutters (NSCs), many of which utilize diesel engines in the 10,000–20,000 HP range. Additionally, the U.S. Navy’s Constellation-class frigate program, managed by Fincantieri Marinette Marine, is also contributing to growth. These frigates use a combined diesel-electric and gas (CODLAG) propulsion system, with diesel engines in the 10,000–20,000 HP range serving as the primary power source.

COUNTRY ANALYSIS

United States

The United States secured the dominant position in the North American marine diesel engine market by accounting for 76.4% of total engine installations in 2024. This lead position is driven by the country’s vast maritime infrastructure, including a large commercial fishing fleet, a robust offshore oil and gas sector, and a growing recreational boating industry. One of the key drivers of the U.S. market is the offshore energy sector, particularly in the Gulf of Mexico. According to the U.S. Energy Information Administration (EIA), the Gulf of Mexico contributed 17% of total U.S. crude oil production and 5% of dry natural gas production in 2023. In addition, this trend, combined with the modernization of naval and coast guard fleets, continues to reinforce the U.S. as the largest market for marine diesel engines in North America.

Canada

Canada holds a significant share of the North American marine diesel engine market. The market is primarily driven by the country’s strong inland shipping industry, commercial fishing sector, and government-led initiatives to modernize its maritime fleet. A major contributor to Canada’s market position is its inland waterway transportation network, particularly the Great Lakes–St. Lawrence Seaway system. Additionally, the fishing industry remains a key user of marine diesel engines. With the government investing in sustainable fisheries and maritime infrastructure, the Canadian marine diesel engine market is expected to maintain steady growth.

Rest of North America

The Rest of North America, primarily consisting of Mexico and Central American territories, holds a smaller but steadily growing share of the regional marine diesel engine market. The market is driven by expanding inland waterway transport, coastal shipping, and offshore fishing activities. Mexico is the primary contributor to this segment, with its inland waterway network and Gulf of Mexico fishing industry playing a significant role. The Mexican Navy (SEMAR) has also been modernizing its fleet, acquiring new patrol and rescue vessels equipped with medium-speed diesel engines from Caterpillar Marine and MAN Energy Solutions. Additionally, the coastal fishing industry remains a key user of marine diesel engines. The expansion of mariculture and offshore fish farming is also contributing to increased demand for smaller diesel engines used in support boats.

KEY MARKET PLAYERS

The major players in the Europe marine diesel engine market include AB Volvo, Anglo Belgian, Caterpillar, Cummins, Daihatsu Diesel, Deere & Company, DEUTZ, Hyundai, IHI Corporation, Kawasaki Heavy Industries, MAN Energy Solutions, Rolls-Royce, Scania, Siemens, STX Heavy Industries, Wartsila, Yanmar, and Yuchai International.

Top Players In The Market

Caterpillar Inc.

Caterpillar is a dominant force in the North American marine diesel engine market, known for its durable and high-performance engine solutions tailored for commercial, defense, and recreational applications. The company offers a broad range of engines from small auxiliary units to large propulsion systems. Caterpillar’s strong distribution network and long-standing relationships with shipbuilders and government agencies support its leadership position. The company is also recognized for integrating advanced fuel-efficient technologies and meeting evolving emission standards, reinforcing its global reputation in the marine propulsion sector.

Cummins Inc.

Cummins plays a pivotal role in the North American marine diesel engine landscape by offering a comprehensive portfolio of diesel engines designed for both inland and offshore applications. The company is known for its innovation in Tier 4 Final compliant engines, which cater to environmental regulations without compromising performance. Cummins collaborates with major boat and ship manufacturers, and its engines are widely used in commercial fishing, ferry services, and naval vessels. Its focus on after-sales service and digital integration further enhances its competitive edge.

Wärtsilä Corporation

Wärtsilä, though headquartered in Finland, has a significant presence in North America and contributes extensively to the marine diesel engine market. The company is recognized for its medium-speed diesel engines used in a variety of marine applications, including LNG carriers, ferries, and offshore support vessels. Wärtsilä emphasizes sustainable marine solutions, hybrid technologies, and smart propulsion systems. Its strategic partnerships with regional shipyards and service centers allow it to maintain a strong foothold in the North American market while supporting global maritime decarbonization goals.

Top Strategies Used By Key Market Participants

Product Innovation and Technological Advancement

Leading companies are prioritizing the development of fuel-efficient, low-emission marine diesel engines to align with tightening environmental regulations. They are investing in research and development to integrate advanced after-treatment systems, hybrid capabilities, and digital engine controls that enhance performance and reduce environmental impact.

Strategic Partnerships and Collaborations

To expand their market reach and strengthen supply chain capabilities, key players are forming strategic alliances with shipbuilders, logistics providers, and government agencies. These collaborations help in customizing engine solutions for specific applications and ensuring seamless integration with vessel systems.

After-Sales Service and Customer Support Expansion

Recognizing the importance of long-term customer engagement, companies are enhancing their service networks and offering digital diagnostics, remote monitoring, and predictive maintenance solutions. This not only improves operational efficiency for end-users but also reinforces brand loyalty and repeat business.

COMPETITION OVERVIEW

The competition in the North American marine diesel engine market is characterized by a blend of established global players and regional manufacturers striving to maintain relevance in a mature yet evolving industry. The market is moderately consolidated, with leading companies leveraging technological expertise, regulatory compliance, and strong after-sales networks to secure long-term contracts and customer loyalty. Innovation remains a key battleground, as manufacturers focus on developing engines that meet stringent emission norms without compromising on performance or fuel efficiency. Strategic acquisitions and partnerships are frequently used to expand product portfolios and regional presence. The defense and offshore energy sectors continue to be critical growth areas, where reliability and durability are paramount, giving an edge to companies with proven track records. Meanwhile, the recreational and inland shipping segments are witnessing increased customization and digital integration, pushing manufacturers to differentiate through smart engine technologies and enhanced service offerings. As environmental regulations tighten, the ability to offer sustainable and future-ready propulsion solutions is becoming a decisive factor in maintaining a competitive advantage.

RECENT HAPPENINGS IN THE MARKET

- In January 2023, Caterpillar Inc. launched a new line of TiFinal-compliant marine diesel engines specifically designed for offshore support vessels operating in the Gulf of Mexico. The launch was aimed at meeting the growing demand for cleaner and more efficient propulsion systems in the energy logistics sector.

- In June 2023, Cummins Inc. announced a collaboration with a leading U.S. shipbuilder to integrate its latest high-speed diesel engines into a new class of fast ferries being developed for the Northeast coastal routes. This partnership is intended to enhance fuel efficiency and reduce emissions in public maritime transport.

- In November 2023, Wärtsilä Corporation expanded its service center network in Canada to provide faster maintenance and technical support for marine diesel engines used in inland shipping and fishing fleets. This expansion is part of the company’s strategy to strengthen its regional presence and improve customer service response times.

- In February 2024, Rolls-Royce Power Systems introduced a modular diesel-electric hybrid propulsion system tailored for U.S. Coast Guard and naval patrol vessels. The new system aims to improve fuel economy and reduce operational costs while meeting environmental compliance standards.

- In May 2024, MTU Friedrichshafen, a subsidiary of Rolls-Royce, partnered with a major U.S. defense contractor to supply marine diesel engines for the U.S. Navy’s next-generation frigate program. This collaboration underscores the company’s commitment to supporting the modernization of the U.S. naval fleet with high-performance propulsion solutions.

MARKET SEGMENTATION

This research report on the North American marine diesel engine market is segmented and sub-segmented into the following categories.

By Technology

- Low Speed

- Medium Speed

- High Speed

By Application

- Merchant

- Container Vessels

- Tankers

- Bulk Carriers

- Gas Carriers

- RO-RO

- Others

- Offshore

- Drilling RIGS & Ships

- Anchor Handling Vessels

- Offshore Support Vessels

- Floating Production Units

- Platform Supply Vessels

- Cruise & Ferry

- Cruise Vessels

- Passenger Vessels

- Passenger/Cargo Vessels

- Others

- Navy

- Others

By Power

- 1,000 HP

- 1,000 - 5,000 HP

- 5,001 - 10,000 HP

- 10,001 - 20,000 HP

- > 20,000 HP

By Country

- The United States

- Canada

- Mexico

- Rest of North America

Frequently Asked Questions

What is a marine diesel engine?

A marine diesel engine is a type of internal combustion engine designed to power boats, ships, and other watercraft using diesel fuel. It’s known for its durability, fuel efficiency, and ability to deliver strong performance in demanding sea conditions.

Why are diesel engines preferred in North American marine applications?

Diesel engines offer higher torque, better fuel economy, and longer service life compared to gasoline engines, making them ideal for commercial fishing, cargo transport, and large recreational vessels. Safety is also a factor—diesel is less flammable than gasoline.

Which sectors drive the demand for marine diesel engines in North America?

Commercial shipping, fishing fleets, offshore support vessels, and government coast guard operations are the primary users. The recreational segment, especially large yachts and charter boats, also contributes significantly to market demand.

How is environmental regulation shaping the market?

Strict emissions standards from the U.S. Environmental Protection Agency (EPA) and Canadian authorities are pushing manufacturers to produce cleaner, Tier 4-compliant engines. This has led to upgrades in fuel injection systems, exhaust after-treatment, and engine efficiency.

Are there regional differences in demand across North America?

Yes—coastal states like Alaska, California, Florida, and regions around the Great Lakes see higher usage due to active fishing and maritime industries. Canada’s remote northern communities also rely on diesel-powered vessels for essential transport and supply.

What role do engine rebuilds and aftermarket services play?

Many operators extend the life of marine diesel engines through regular maintenance, overhauls, and part replacements, reducing the need for new purchases. The aftermarket for filters, turbochargers, and control systems remains strong and profitable.

How are technological advancements affecting marine diesel engines?

Modern engines now feature electronic control units (ECUs), remote diagnostics, and integration with onboard navigation and monitoring systems. These upgrades improve fuel management, performance tracking, and early fault detection.

Are alternative fuels impacting the diesel engine market?

Yes—there’s growing interest in dual-fuel engines that can run on diesel and LNG or biodiesel blends, especially in eco-sensitive areas. However, full electrification remains limited to smaller vessels due to range and power constraints.

Who are the key players in this market?

Major manufacturers include Caterpillar, Cummins, MAN Energy Solutions, Volvo Penta, and Yanmar, all offering engines tailored to North American marine standards. Local distributors and service centers play a vital role in sales and support.

What’s the future outlook for marine diesel engines in North America?

While long-term pressure from decarbonization goals exists, diesel engines will remain essential for medium- and heavy-duty marine applications over the next decade. Evolution, not replacement, is the trend—engines are getting cleaner, smarter, and more efficient.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com