North America Residential Heat Pump Market Size, Share, Trends & Growth Forecast Report By Product Type, Application, and By Country (United States, Canada) – Industry Analysis and Forecast, 2026 to 2034

North America Residential Heat Pump Market Summary

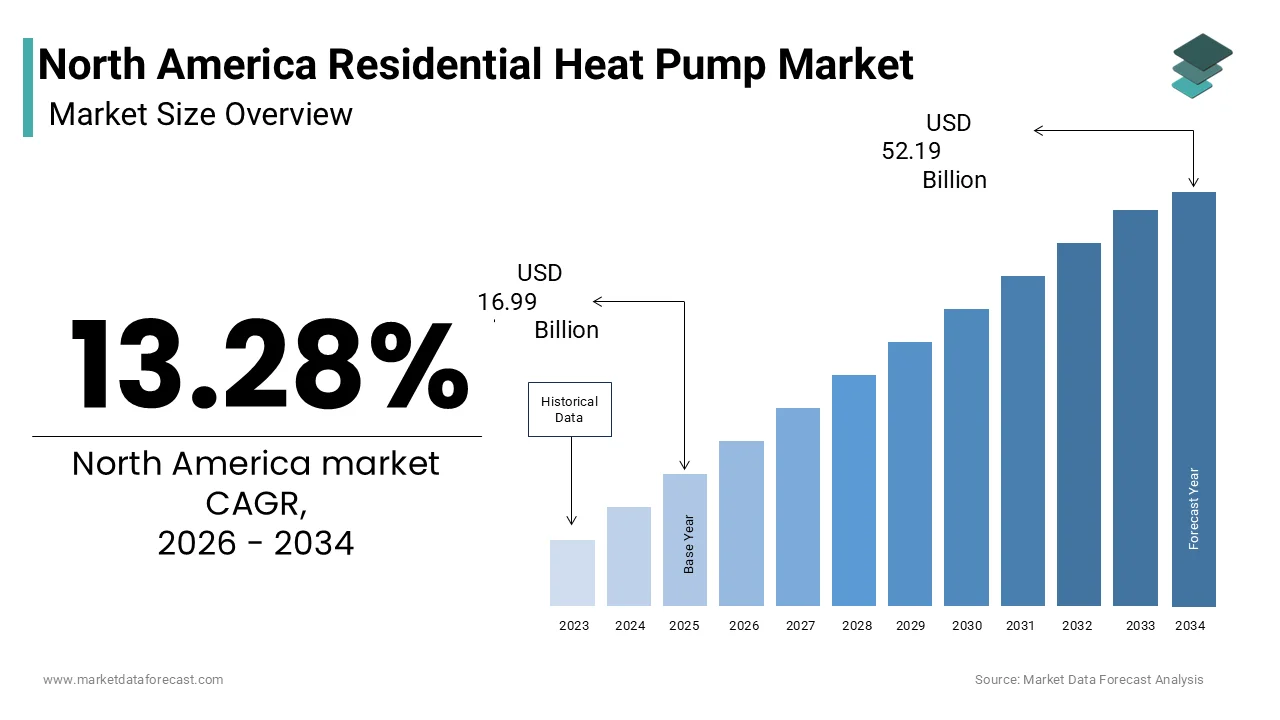

North America’s residential heat pump market, valued at USD 16.99 billion in 2025, is projected to reach USD 52.19 billion by 2034, expanding at a CAGR of 13.28%, driven by electrification incentives, cold-climate technology advances, and rising demand for energy-efficient home heating and cooling.

Key Market Highlights

- 2025 Market Size: USD 16.99 billion

- 2026 Market Size: USD 19.25 billion

- 2034 Forecast: USD 52.19 billion

- CAGR (2026–2034): 13.28%

- Base Year: 2025

- Forecast Period: 2026–2034

Quick Growth Drivers

- Strong government incentives and rebates (IRA in the U.S., Greener Homes Grant in Canada)

- Accelerating residential electrification to meet decarbonization targets

- Rising consumer awareness of energy efficiency and long-term cost savings

- Dual heating–cooling functionality replacing separate HVAC systems

- Advancements in cold-climate heat pump performance

Principal Restraints

- High upfront installation and retrofit costs, especially for geothermal systems

- Limited access to financing among lower-income households

- Persistent performance concerns in extremely cold regions

- Inconsistent pricing and quality due to fragmented contractor networks

High-Value Opportunities

- Expansion of cold-climate air-source and advanced ground-source heat pumps

- Integration with smart home and demand-response ecosystems

- Utility-led electrification and peak-load management programs

- Retrofits of aging single-family and multi-family housing stock

Key Market Challenges

- Shortage of skilled installers and certified technicians

- Training gaps for advanced refrigerants and smart control systems

- Grid capacity and winter peak-load constraints

- Rural and remote infrastructure limitations

Fastest-Growing Segments

- Ground Source Heat Pumps: 8.2% CAGR — superior efficiency and long-term savings

- Multi-Family Residential Applications: 9.8% CAGR — driven by building codes and carbon regulations

- Cold-Climate Air Source Heat Pumps: high double-digit growth in northern states and Canada

Regional Leadership & Dynamics

- United States (89.3%) — IRA incentives, diverse climates, large retrofit potential

- Canada (11.3%) — net-zero targets, strong provincial rebates, cold-climate adoption

- Strong growth in Northeast U.S., Pacific Northwest, Quebec, and British Columbia

What Wins Commercially

- Proven cold-climate performance and reliability

- Access to rebates, financing, and utility incentive alignment

- Strong installer training and certification programs

- Smart thermostat and grid-responsive compatibility

- Scalable retrofit-friendly system designs

Top Strategic Ask for Executives

Scale cold-climate and smart-integrated heat pump portfolios while investing in installer training and grid-aligned deployment to capture mass-market electrification demand.

Leading Players

Some of the companies that are playing a dominating role in the North America residential heat pump market include:

- Carrier Global Corporation

- Trane Technologies

- Daikin Industries, Ltd.

- Johnson Controls International plc

- Lennox International Inc.

- Rheem Manufacturing Company

- Bosch Thermotechnology Corp.

- Mitsubishi Electric US, Inc.

- LG Electronics Inc.

- Samsung Electronics Co., Ltd.

North America Residential Heat Pump Market Size

The north america residential heat pump market was valued at USD 16.99 billion in 2025 and grew to USD 19.25 billion in 2026. The market is projected to reach USD 52.19 billion by 2034, expanding at a CAGR of 13.28% from 2026 to 2034.

Heat pumps, which transfer heat rather than generate it, have emerged as a sustainable alternative to traditional heating systems such as gas furnaces and electric resistance heaters. In 2023, approximately 20% of U.S. homes utilized heat pumps for space heating, according to the U.S. Energy Information Administration (EIA), with higher adoption rates observed in regions like the Southeast and Pacific Northwest. The technology's dual functionality provides both heating and cooling that makes it particularly appealing in climates with moderate temperature variations. Despite this momentum, market penetration remains uneven due to factors including upfront costs, installation complexity, and regional climate suitability.

MARKET DRIVERS

Government Incentives and Rebates

Government support plays a pivotal role in boosting the growth of the North American residential heat pumps market. The Inflation Reduction Act (IRA) in the United States allocates up to $8,000 in tax credits for qualifying heat pump installations under the Home Energy Efficiency and Electrification Rebates program, significantly lowering the financial burden on homeowners. As per the U.S. Department of Energy, these incentives are projected to increase residential heat pump adoption by nearly 30% through 2030. Similarly, in Canada, the Canada Greener Homes Grant offers rebates of up to CAD 5,000 for energy-efficient home retrofits, including heat pump installations. Natural Resources Canada reported that over 70% of applicants in 2022 chose heat pump retrofits, indicating strong consumer responsiveness to financial incentives. For instance, Canada’s commitment to achieving net-zero emissions by 2050 necessitates widespread electrification of residential heating, with heat pumps being central to that strategy. Additionally, several states and provinces have introduced complementary local incentives, further amplifying the impact. British Columbia’s CleanBC plan, for example, provides point-of-sale rebates worth up to CAD 5,600 for qualifying heat pump systems.

Rising Consumer Awareness of Energy Efficiency

Growing environmental consciousness and rising electricity costs are prompting homeowners to seek more energy-efficient alternatives for residential heating and cooling, which is substantially contributing to the growth of the North American residential heat pump market. According to the American Council for an Energy-Efficient Economy (ACEEE), high-efficiency heat pumps can reduce energy consumption by up to 50% compared to conventional electric resistance heating systems. This efficiency advantage becomes even more pronounced when paired with renewable energy sources such as rooftop solar installations, which are increasingly common among eco-conscious consumers. A 2023 survey conducted by the Consumer Reports National Research Center revealed that 64% of respondents were more likely to consider energy-efficient appliances when renovating or purchasing new HVAC systems. Furthermore, the average annual energy savings from a ductless mini-split heat pumpranges between $180 and $400, depending on regional electricity rates, as indicated by the Northeast Energy Efficiency Partnerships (NEEP). In colder climates, advancements in cold-climate heat pump technology have alleviated previous concerns about performance during winter months, broadening their appeal. Manufacturers like Mitsubishi Electric and Daikin have introduced models capable of operating efficiently at temperatures as low as -13°F by enhancing reliability and consumer confidence.

MARKET RESTRAINTS

High Upfront Installation Costs

The initial investment required for residential areas installation is hindering the growth of the North American residential heat pump market. These figures often surpass the upfront costs of traditional HVAC systems, deterring price-sensitive consumers despite potential energy savings over time. The complexity of certain installations, particularly for geothermal systems, necessitates specialized labor and site preparation, further inflating expenses. In rural and suburban areas, where existing infrastructure is limited, retrofitting older homes with ductwork or ground loops can add substantial costs. Data from the U.S. Census Bureau indicates that nearly 28% of American households earn less than $50,000 annually, making such investments financially burdensome without substantial rebates or financing options. Even with available incentives, many consumers lack access to affordable credit or are unaware of available programs. Moreover, the fragmented nature of the HVAC contractor network in North America contributes to inconsistent pricing and service quality, creating additional hesitation among homeowners.

Climate Limitations and Performance Concerns

Although modern heat pump technology has advanced considerably, climatic constraints continue to limit its effectiveness and acceptance in certain regions of North America. The climate limitations and performance concerns are attributedton limiting the growth of the North American residential heat pump market. Traditional air-source heat pumps experience diminished efficiency in extremely cold climates, where outdoor temperatures frequently drop below freezing. According to the National Renewable Energy Laboratory (NREL), standard heat pumps may lose up to 40% of their heating capacity at temperatures near 0°F unless equipped with cold-climate enhancements. While newer cold-climate models have addressed some of these limitations, they often come at a premium cost, reducing their accessibility. In Canada, regions such as the Prairie provinces and Northern Ontario still show relatively low adoption rates, partly due to skepticism regarding year-round performance. Additionally, misconceptions about heat pump performance persist, fueled by outdated information and inadequate installer training. Many contractors remain unfamiliar with optimal sizing and placement techniques for cold climates, leading to subpar installations and unsatisfactory user experiences.

MARKET OPPORTUNITIES

Expansion of Cold-Climate Heat Pump Technologies

The development and commercialization of advanced cold-climate heat pump technologies for expanding reach into previously underserved geographic regions is creating new opportunities for the growth ofthe North American residential heat pump market. Innovations such as variable refrigerant flow (VRF) systems, enhanced compressors, and improved defrost cycles enable effective operation in sub-zero temperatures, addressing a major limitation of earlier models. Manufacturers like Carrier and Lennox have introduced next-generation units capable of delivering consistent heating performance at temperatures as low as -22°F, according to product testing data published by the Air-Conditioning, Heating, and Refrigeration Institute (AHRI). These technological improvements are gaining traction in markets like the U.S. Upper Midwest and Canadian Prairies, where cold winters historically discouraged heat pump adoption. The U.S. Department of Energy’s Cold Climate Heat Pump Working Group has identified over 1.2 million households in these regions as viable candidates for conversion, representing a substantial growth potential. Additionally, partnerships between manufacturers and utilities are driving pilot programs to demonstrate real-world performance and build consumer trust. For instance, Xcel Energy launched a cold-climate heat pump demonstration project in Minnesota, resulting in a 35% increase in customer inquiries within the first year. As production scales and costs decrease, these high-performance systems are expected to penetrate mainstream markets, unlocking new demand segments and supporting broader decarbonization objectives.

Integration with Smart Home Ecosystems

The emergence of residential heat pump systems with smart home technologies offers a compelling avenue for differentiation and value-added service delivery is additionally leverages opportunities for the growth of the North American residential heat pump market. Smart thermostats, remote monitoring platforms, and AI-driven energy management tools are increasingly being integrated with heat pump installations to optimize performance and enhance user experience. According to a 2023 report by Statista, over 60% of North American households now own at least one connected home device, signaling strong consumer readiness for interoperable HVAC solutions. Companies like Ecobee and Google Nest have developed thermostats specifically designed to work with heat pumps, enabling features such as adaptive recovery, occupancy sensing, and grid-responsive controls. Furthermore, utility companies are leveraging smart heat pump systems to support demand response initiatives, offering dynamic pricing and load-shifting incentives that benefit both consumers and grid operators. In Quebec, Hydro-Québec’s residential smart thermostat program has resulted in peak load reductions of 12 MW during winter months, primarily through optimized heat pump usage. As smart home ecosystems mature and consumer expectations evolve, the integration of heat pumps with intelligent controls is poised to become a standard expectation, opening new revenue streams and competitive advantages for manufacturers and installers alike.

MARKET CHALLENGES

Skilled Labor Shortage and Installer Training Gaps

The shortage of qualified technicians and inadequate installer training, particularly for complex systems, such as geothermal and ductless mini-split systems,s is acting as a barrier for the growth of the North American residential heat pump market. This deficiency leads to inconsistent service quality, improper system sizing, and inefficient installations that undermine consumer satisfaction and system performance. The problem is exacerbated by the rapid pace of technological advancement, with newer models featuring advanced controls and refrigerants that require specialized knowledge. Geographic disparities also exist, with rural and remote areas experiencing disproportionately low access to certified professionals. In Canada, the Canadian Institute for Climate Choices reported that over 30% of provinces lack sufficient numbers of licensed heat pump installers to meet projected demand growth. Without targeted workforce development initiatives, including apprenticeship programs and continuing education courses, the industry risks compromising system reliability and consumer confidence. Addressing this challenge will require coordinated efforts between manufacturers, trade associations, and government agencies to invest in training infrastructure and certification pathways.

Grid Stability and Electrical Infrastructure Limitations

As residential heat pump adoption accelerates, concerns regarding electrical grid stability and infrastructure adequacy are emerging as a significant challenge for the growth ofthe North American residential heat pump market. Heat pumps, especially during peak heating periods, place considerable strain on local distribution networks, potentially leading to voltage fluctuations, transformer overloads, and increased outage risks. The Electric Power Research Institute (EPRI) estimates that widespread electrification of residential heating could increase peak winter electricity demand by up to 25% in certain regions, straining aging grid assets. In areas with limited generation capacity or outdated transmission systems, this surge in load may necessitate costly infrastructure upgrades. For instance, in parts of New England and Atlantic Canada, utilities have begun implementing time-of-use pricing and load management programs to mitigate peak demand impacts. However, these measures may inadvertently discourage heat pump adoption if perceived as inconvenient or costly by consumers. Rural communities face additional hurdles, where sparse population density and weak grid connections make electrification economically unfeasible without substantial public investment. The International Energy Agency (IEA) has noted that coordinated planning between utilities, regulators, and policymakers is essential to ensure that grid modernization keeps pace with electrification goals. Without proactive infrastructure investment and demand-side management strategies, the scalability of the residential heat pump market may be constrained, particularly in regions most vulnerable to grid instability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, Application, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | United States |

| Market Leaders Profiled | Carrier Global Corporation, Trane Technologies, Daikin Industries, Ltd., Johnson Controls International plc, Lennox International Inc., Rheem Manufacturing Company, Bosch Thermotechnology Corp., Mitsubishi Electric US, Inc., LG Electronics Inc., Samsung Electronics Co., Ltd., Goodman (Daikin brand), Nordyne LLC (subsidiary of Carrier), Hitachi Appliances, Inc., Fujitsu General Limited, Panasonic Corporation, Viessmann Group, NIBE Industrier AB, Bryant (Carrier brand), Heil (ICM Controls / Carrier ecosystem), American Standard (Trane affiliate) |

SEGMENTAL ANALYSIS

By Product Type Insights

The air source heat pumps segment was the largest by capturing a dominant share of the North America residential heat pump market in 2025, with its cost-effectiveness, simpler installation requirements, and technological advancements that have expanded operational capabilities in colder climates. Their significantly lower upfront cost compared to alternative technologies is expected to propel the growth of the North American residential heat pump market. In contrast, ground source systems can cost between $15,000 to $30,000, creating a substantial price barrier. The National Renewable Energy Laboratory reports that air source heat pumps offer payback periods of 4-7 years in most climates, compared to 8-12 years for ground source alternatives. Recent innovations in cold-climate air source heat pump technology have dramatically expanded their geographical viability and appeal. Modern variable-speed compressors and enhanced defrost cycles enable these systems to maintain efficiency at temperatures as low as -13°F, addressing previous limitations in northern regions. The Cold Climate Heat Pump Working Group documented that cold-climate air source heat pumps can achieve coefficient of performance (COP) ratings above 2.0 even at 5°F, representing a 40% improvement over conventional models. Manufacturers like Mitsubishi Electric and Daikin have reported 150% growth in cold-climate model sales between 2019 and 2023, with these units now comprising over 30% of their residential heat pump portfolios. The Northeast Energy Efficiency Partnerships noted that states like Maine and Vermont have seen air source heat pump adoption rates increase from 8% to 22% of new heating installations, directly attributable to these technological improvements.

The ground source heat pumps segment is likely to witness the fastest CAGR of 8.2% throughout the forecast period, owing to increasing recognition of their superior energy efficiency, long-term cost savings, and enhanced environmental benefits. Ground source heat pumps demonstrate exceptional energy efficiency that significantly outperforms air source alternatives, driving their accelerated adoption despite higher initial costs. The U.S. Environmental Protection Agency estimates that ground source systems reduce energy consumption by 25-50% compared to conventional heating and cooling systems, translating to average annual savings of $1,500 to $2,500 per household. Long-term operational savings become particularly compelling when considering system lifespans exceeding 25 years for ground loops and 20 years for heat pump units. Expanding government incentives and innovative financing mechanisms are driving the rapid growth of ground source heat pump adoption across North America. Additionally, state-level programs like New York's Clean Heat Program offer supplementary rebates of up to $20,000 for qualifying ground source installations, effectively reducing net costs to levels competitive with air source alternatives. Financing innovations such as property-assessed clean energy (PACE) programs and energy-efficient mortgages have made these systems accessible to mainstream consumers.

By Application Insights

The single-family residential applications segment accounted for a prominent share of the North America residential heat pump market in 2025, with the inherent compatibility of heat pump systems with standalone residential properties, where individual homeowners have complete control over HVAC decisions and can optimize system design for specific building characteristics. The high rate of homeownership in North America directly contributes to the dominance of single-family applications in the residential heat pump market. Homeowners possess the autonomy to make independent decisions regarding HVAC system upgrades and replacements, unlike multi-family tenants who must rely on landlord preferences and building management policies. This decision-making flexibility enables direct consumer engagement with heat pump technology, resulting in higher adoption rates. These properties typically provide adequate outdoor space for air-source unit placement and sufficient indoor area for ductwork modifications or ductless system configurations. Additionally, single-family homes generally have simpler thermal envelopes that are easier to optimize for heat pump operation, with fewer shared walls and reduced thermal bridging issues. Homeowners also havea greater ability to implement complementary energy efficiency measures, such as insulation upgrades and window replacements, which enhance heat pump effectiveness and justify higher initial investments.

The multi-family residential applications segment is anticipated to grow atthea fastest CAGR of 9.8% throughout the forecast period, with the increasing regulatory pressure, rising tenant demand for energy-efficient housing, and evolving building management strategies that recognize the long-term benefits of heat pump technology. Stringent building codes and energy efficiency regulations are compelling multi-family property owners to adopt heat pump technology at accelerating rates. Cities like New York, Seattle, and Vancouver have implemented aggressive carbon reduction targets that require existing buildings to achieve significant emissions reductions by 2030. The New York City Local Law 97 mandates that buildings over 25,000 square feet reduce emissions by 40% by 2030, prompting widespread HVAC system upgrades, including heat pump installations. The Urban Land Institute reports that 65% of large multi-family properties in major metropolitan areas are planning heat pump retrofits to comply with these regulations. California's Title 24 building code requires all new multi-family constructions to incorporate high-efficiency heating systems, with heat pumps meeting these standards in 89% of cases. Similar regulatory frameworks across Canadian provinces, including British Columbia's Step Code and Ontario's Building Code updates, mandate minimum efficiency standards that favor heat pump technology. The compelling economic advantages of heat pump systems in multi-family applications are driving rapid adoption among property managers and investors seeking to optimize operational performance. Heat pumps can reduce heating and cooling costs by 30-50% compared to traditional electric resistance heating and central air conditioning systems, according to the U.S. Department of Energy's Better Buildings Initiative. For large multi-family properties, these savings translate to substantial annual reductions in utility expenses, with some complexes reporting $50,000 to $150,000 in annual savings following heat pump installations. Tenant satisfaction improvements further enhance property values and occupancy rates, with surveys conducted by the National Apartment Association showing that 78% of renters prefer properties with energy-efficient HVAC systems. The reduced maintenance requirements and longer equipment lifespans of heat pump systems provide additional operational benefits, with typical maintenance costs 25% lower than conventional systems according to the Building Owners and Managers Association. Property managers also benefit from simplified tenant billing and reduced service calls, as heat pump systems demonstrate superior reliability and consistent performance across varying weather conditions.

COUNTRY LEVEL ANALYSIS

United States Residential Heat Pump Market Analysis

The United States was the largest contributor in the North American residential heat pump market by occupying 89.3% of the share in 2025, owing to the vast residential housing stock, diverse climatic conditions that create varied demand patterns, and robust policy frameworks supporting energy efficiency initiatives. The sheer scale of the American residential sector, combined with increasing electrification trends and climate-conscious consumer preferences, establishes the United States as the primary growth engine for residential heat pump adoption across the continent. The American market's maturity and sophistication are evident in its comprehensive distribution networks, advanced technological capabilities, and extensive consumer awareness programs. Federal and state-level incentives have created favorable conditions for market expansion, while regional climate variations have driven demand for diverse heat pump technologies ranging from traditional air-source units to advanced cold-climate models. The market's growth trajectory is supported by strong manufacturing capabilities, innovative product development, and evolving building codes that increasingly favor electric heating solutions. The Inflation Reduction Act's comprehensive electrification incentives, combined with state-level rebate programs and utility-sponsored initiatives, have created unprecedented demand stimulation. The fragmented nature of the American housing market, with diverse property types and ownership structures, creates multiple pathways for market penetration and sustained growth opportunities.

Canada Residential Heat Pump Market Analysis

Canada's residential heat pump market held 11.3% of the share in 2025, with the commitment to reducing greenhouse gas emissions, coupled with substantial government investment in clean energy initiatives and building electrification programs. The Canadian market's growth is particularly notable given the country's challenging climate conditions, which historically limited heat pump adoption but now drive demand for advanced cold-climate technologies. Provincial governments across Canada have implemented aggressive climate targets and supportive policy frameworks that encourage residential heat pump deployment as part of broader decarbonization strategies. Provinces like British Columbia, Quebec, and Nova Scotia have emerged as early adopters, driven by strong provincial incentives and progressive building standards. Canadian consumers show high levels of environmental consciousness and willingness to invest in energy-efficient technologies, which is creating favorable conditions for market expansion. Canada's residential heat pump market experiences robust growth driven by comprehensive federal and provincial policy support, technological advancements suitable for cold climates, and increasing consumer awareness of environmental benefits. Natural Resources Canada reports that residential heat pump installations increased by 25% in 2023, with strength in Atlantic provinces and British Columbia, where adoption rates exceed 20% of new heating installations.

COMPETITIVE LANDSCAPE

The North American residential heat pump market exhibits intense competition characterized by the presence of established global manufacturers, regional specialists, and emerging technology innovators. Market leaders such as Carrier, Daikin, and Trane Technologies compete aggressively for market share through product differentiation, pricing strategies, and comprehensive customer support programs. The competitive landscape is further complicated by the entry of new players offering disruptive technologies and business models that challenge traditional market approaches. Companies compete based on factors including energy efficiency ratings, reliability, warranty offerings, installation support, and smart technology integration capabilities. Price competition remains significant, particularly in the mid-tier market segments where consumers are highly price-sensitive but still demand quality performance. Brand reputation and dealer relationships play crucial roles in customer decision-making processes, leading manufacturers to invest heavily in relationship building and professional installer training programs. The market also experiences competition from alternative heating technologies, es including gas furnaces and electric resistance heating systems, requiring heat pump manufacturers to continuously demonstrate superior value propositions. Innovation cycles are accelerating as companies race to develop next-generation technologies that address climate change concerns while meeting evolving consumer expectations for convenience and connectivity.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global north america residential heat pump market include

- Carrier Global Corporation

- Trane Technologies

- Daikin Industries, Ltd.

- Johnson Controls International plc

- Lennox International Inc.

- Rheem Manufacturing Company

- Bosch Thermotechnology Corp.

- Mitsubishi Electric US, Inc.

- LG Electronics Inc.

- Samsung Electronics Co., Ltd.

- Goodman (Daikin brand)

- Nordyne LLC (subsidiary of Carrier)

- Hitachi Appliances, Inc.

- Fujitsu General Limited

- Panasonic Corporation

- Viessmann Group

- NIBE Industrier AB

- Bryant (Carrier brand)

- Heil (ICM Controls / Carrier ecosystem)

- American Standard (Trane affiliate)

TOP LEADING PLAYERS IN THE MARKET

- Carrier Global Corporation stands as a dominant force in the North American residential heat pump market through its comprehensive portfolio of advanced heating and cooling solutions. The company's extensive research and development capabilities have enabled the creation of innovative products,s including variable refrigerant flow systems and cold-climate heat pumps specifically designed for challenging North American weather conditions. Carrier's strong distribution network spans across the United States and Canada, supported by a vast network of certified dealers and installation professionals. The company's commitment to sustainability and energy efficiency has positioned its residential heat pump offerings as premium solutions for environmentally conscious consumers. Through strategic acquisitions and partnerships, Carrier has expanded its technological capabilities while maintaining strong brand recognition and customer loyalty. Their focus on smart home integration and connected technologies has enabled seamless incorporation of heat pump systems with modern residential automation platforms, enhancing user experience and system performance optimization.

- Daikin Industries has established itself as a leading innovator in the North American residential heat pump market through its advanced inverter technology and superior system efficiency. The Japanese multinational has successfully adapted its global expertise to meet specific North American climate requirements and consumer preferences, particularly in developing cold-climate heat pump solutions that perform effectively in harsh winter conditions. Daikin's comprehensive product range includes ductless mini-split systems, multi-split configurations, and whole-house solutions that cater to diverse residential applications. The company's commitment to quality manufacturing and rigorous testing standards has earned strong consumer trust and professional installer confidence throughout the region. Strategic investments in local manufacturing facilities and technical support infrastructure have strengthened Daikin's market position while ensuring reliable product availability and service excellence. Their emphasis on environmental responsibility through the use of eco-friendly refrigerants and energy-efficient designs aligns with growing consumer demand for sustainable heating and cooling solutions.

- Trane Technologies has emerged as a significant player in the North American residential heat pump market through its dual-brand strategy encompassing both Trane and American Standard product lines. The company's extensive engineering expertise and decades of HVAC industry experience have enabled the development of highly efficient residential heat pump systems that deliver exceptional performance across various climate conditions. Trane's strong relationships with residential builders, contractors, and distributors provide extensive market reach and customer access throughout North America. The company's focus on innovation has resulted in breakthrough technologies,s including advanced climate control algorithms and smart system integration capabilities that enhance user comfort and energy savings. Their commitment to dealer support through comprehensive training programs, marketing assistance, and technical resources has strengthened professional installer loyalty and market penetration. Trane Technologies' emphasis on system compatibility and holistic home comfort solutions has differentiateitsir residential heat pump offerings while supporting long-term customer satisfaction and brand advocacy.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

- Leading players in the North American residential heat pump market continuously invest in research and development to create advanced technologies that address specific regional challenges and consumer needs. This strategy involves developing cold-climate heat pump models capable of efficient operation in extreme temperatures, integrating smart home connectivity features, and utilizing environmentally friendly refrigerants. Companies focus on enhancing system efficiency through variable-speed compressors, advanced defrost cycles, and improved heat exchanger designs. Innovation efforts also include developing user-friendly control interfaces, mobile applications for remote system monitoring, and compatibility with renewable energy sources such as solar panels. These technological advancements enable manufacturers to differentiate their products, command premium pricing, and capture market share from competitors while meeting evolving consumer expectations for performance and convenience.

- Key market participants actively pursue strategic partnerships with contractors, distributors, utilities, and government agencies to strengthen their market presence and expand customer reach. These collaborations include training programs for installation professionals, co-marketing initiatives with utility companies, and partnerships with home builders for new construction projects. Companies establish comprehensive dealer networks that provide local support, installation services, and after-sales maintenance to ensure customer satisfaction. Strategic alliances with technology companies enable integration of heat pump systems with smart home platforms and energy management solutions. Partnerships with financial institutions facilitate consumer financing options that make heat pump installations more accessible to broader market segments. These collaborative approaches help manufacturers overcome market barriers, reduce customer acquisition costs, and build long-term relationships with key industry stakeholders.

- Major players implement geographic expansion strategies to penetrate new regional markets and increase their overall market share across North America. This approach involves establishing local manufacturing facilities, regional distribution centers, and customer service operations to ensure product availability and responsive support. Companies adapt their product offerings to meet specific regional climate requirements, building codes, and consumer preferences through localized design modifications and feature enhancements. Market expansion efforts include developing relationships with local contractors and distributors, participating in regional trade shows and industry events, and implementing culturally appropriate marketing campaigns. Manufacturers also focus on regulatory compliance and certification processes specific to different states and provinces to ensure legal market access. These localization strategies enable companies to compete effectively against regional players while building strong brand recognition and customer loyalty in diverse geographic markets.

MARKET SEGMENTATION

This research report on the north america residential heat pump market is segmented and sub-segmented into the following categories.

By Product Type

- Air Source Heat Pumps

- Ground Source Heat Pumps

By Application

- Single-Family Residential

- Multi-Family Residential

By Country

- United States

- Canada

Frequently Asked Questions

1. What are the main types of heat pumps in the North America Residential Heat Pump Market?

Key types include air source, water source, and geothermal heat pumps, with air source dominating due to lower installation costs and versatility in residential settings across North America. Water source models grow fastest in suitable climates, offering higher efficiency.

2. Who are the leading companies in the North America Residential Heat Pump Market?

Major players include Daikin Industries, Carrier Corporation, Mitsubishi Electric, Emerson Electric, and Nortek Global HVAC, focusing on innovative, low-GWP refrigerant models compliant with 2025 regulations like the AIM Act. They compete through efficiency and smart integrations.

3. What drives growth in the North America Residential Heat Pump Market?

Growth stems from energy efficiency demands, rising utility costs, environmental concerns, and policies like US tax credits and Canada's rebate programs, promoting heat pumps over traditional furnaces in residential new builds and retrofits.

4. What challenges exist in the North America Residential Heat Pump Market?

Challenges include high upfront costs, performance in extreme cold climates, and limited awareness, though innovations in cold-climate models and incentives mitigate these for residential adoption in North America.

5. How do government incentives impact the North America Residential Heat Pump Market?

Incentives like the US Inflation Reduction Act and Home Efficiency Rebate in Canada reduce costs, accelerating residential installations and contributing to market expansion in North America.

6. What is the role of air source heat pumps in the North America Residential Heat Pump Market?

Air source heat pumps lead the North America Residential Heat Pump Market for their dual heating-cooling functionality, affordability, and suitability for most US and Canadian homes, especially with smart features.

7. Are geothermal heat pumps growing in the North America Residential Heat Pump Market?

Yes, geothermal options gain traction in the North America Residential Heat Pump Market for superior efficiency and longevity, though higher costs limit them to premium residential segments in suitable ground conditions.

8. What future trends shape the North America Residential Heat Pump Market?

Trends include low-GWP refrigerants, smart home integration, and hybrid systems, enhancing the North America Residential Heat Pump Market's appeal for energy-conscious homeowners amid decarbonization efforts.

9. How does the US contribute to the North America Residential Heat Pump Market?

The US dominates the North America Residential Heat Pump Market with urbanization, rebates, and electrification programs driving residential demand, especially in milder climates.

10. What efficiency standards apply to the North America Residential Heat Pump Market?

New standards require 14.3 SEER2 and 7.5 HSPF2 for split-system units in the North America Residential Heat Pump Market, ensuring higher performance in residential applications post-2023.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com