North America Smartphone Market Size, Share, Trends & Growth Forecast Report By Operating System (Android, iOS, Others (KaiOS, HarmonyOS, etc.)), Price Band (Entry-level (Less than USD 200), Mid-range (USD 200 - 499), Premium (USD 500 - 799), Ultra-premium (Greater than or equal to USD 800)), Technology (5G, 4G/LTE, 3G and Below), Form Factor (Bar, Foldable/Flip, Rugged/Industrial), Distribution Channel (Operator/Carrier Stores, Brand-Owned Retail, Multi-brand Physical Retail, Online Direct-to-Consumer), and Country (United States, Canada, Mexico, Rest of North America) – Industry Analysis, 2026 to 2034

North America Smartphone Market Summary

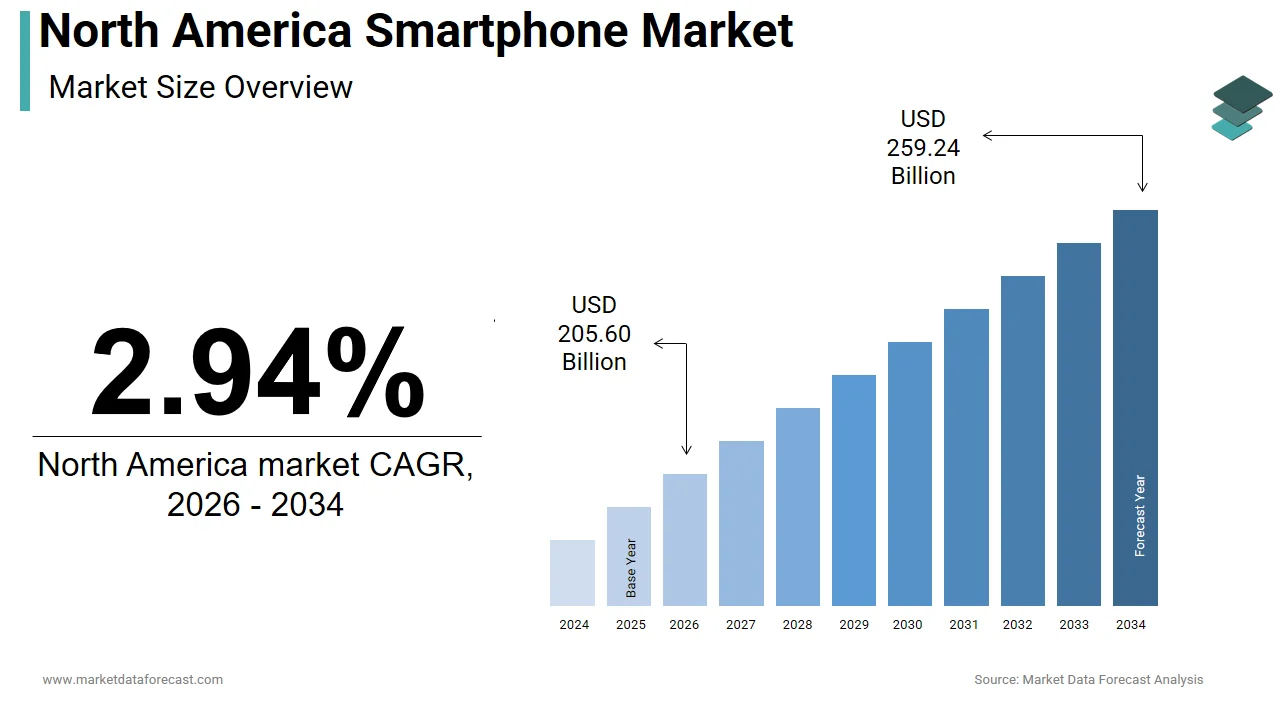

The North America smartphone market was valued at USD 199.73 billion in 2025, is estimated to reach USD 205.60 billion in 2026, and is projected to reach USD 259.24 billion by 2034, growing at a CAGR of 2.94% from 2026 to 2034. The proliferation of 5G networks, deep smartphone integration in daily life, and innovations in mobile health and financial services are key growth drivers.

Key Market Trends & Insights

- United States held the highest share of the North America smartphone market in 2025.

- Canada showed increasing adoption driven by digital inclusion programs.

- Based on operating system, the Android segment led the market with a 56.4% share in 2024.

- Based on price band, the mid-range smartphone segment was the largest in 2025.

- Based on technology, 5G was the dominant segment in 2025.

- Based on form factor, bar phones held the major share in 2025.

- Based on distribution channel, the operator and carrier-owned outlets led in 2025.

Market Size & Forecast

- 2025 Market Size: USD 199.73 Billion

- 2026 Estimated Market Size: USD 205.60 Billion

- 2034 Projected Market Size: USD 259.24 Billion

- CAGR (2026 to 2034): 2.94%

- United States: Largest market in 2025

- Canada: Digitally inclusive and sustainability-focused region

North America Smartphone Market Size

The size of the North America smartphone market was worth USD 199.73 billion in 2025. The regional market is anticipated to grow at a CAGR of 2.94% from 2026 to 2034 and be worth USD 259.24 billion by 2034 from USD 205.60 billion in 2026.

The smartphone is a mobile computing devices that serve as a primary conduit for digital interaction, integrating telephony, internet access, multimedia, and personal productivity into a single handheld platform. These devices have evolved beyond communication tools into essential instruments for financial transactions, health monitoring, remote work, and civic engagement. The integration of advanced sensors, biometric authentication, and artificial intelligence has transformed smartphones into personalized digital assistants, capable of adapting to user habits and environmental contexts. Moreover, the proliferation of 5G networks across urban and suburban regions over 90% of Americans live in areas with 5G coverage, as reported by the Federal Communications Commission, has amplified device utility by enabling ultra-low latency applications such as cloud gaming and real-time telemedicine.

MARKET DRIVERS

Proliferation of 5G Networks and Infrastructure Expansion

The rapid deployment of 5G infrastructure, with the growing consumer expectations for speed, responsiveness, and application capability, is inclined to boost the growth of the North America silica sand market. This leap in connectivity enables seamless streaming of 4K video, real-time cloud gaming, and instantaneous file transfers, compelling users to upgrade from legacy 4G-capable devices. In rural regions, the Rural Digital Opportunity Fund has allocated $20 billion to expand broadband access, with a significant portion supporting 5G small cell deployment, as noted by the U.S. Department of Agriculture. This expansion is prompting carriers to offer trade-in incentives and installment plans to accelerate device turnover. In Canada, Innovation, Science and Economic Development Canada reports that 5G coverage reached 65% of the population by 2023, with telecom providers like Rogers and Telus bundling 5G smartphones with enterprise IoT solutions for smart cities and agriculture.

Integration of Smartphones into Daily Life Through Digital Services and Financial Inclusion

The deep entrenchment of smartphones in essential life functions from banking and healthcare to education and transportation is additionally to fuel the growth of the North America silica sand market. Similarly, telehealth platforms, many of which are smartphone-exclusive, saw over 1.2 billion virtual visits in 2022, as documented by the Centers for Disease Control and Prevention. The U.S. Digital Service reports that 78 federal agencies now offer mobile-optimized portals for tax filing, passport applications, and benefit enrollment. Educational institutions increasingly rely on mobile-first platforms over 60% of college students use smartphones for coursework, according to the National Center for Education Statistics.

MARKET RESTRAINTS

Declining Replacement Cycles Due to Enhanced Device Longevity and Software Support

The lengthening replacement cycle, which is driven by improved hardware durability and extended software support from manufacturers, is likely to restrict the growth of the North America smartphone market. This shift is attributable to advancements in build quality, with flagship models now featuring sapphire-reinforced glass, IP68 water resistance, and aerospace-grade aluminum frames that withstand prolonged use. These updates maintain performance, security, and app compatibility, reducing the urgency to upgrade. Additionally, the marginal gains between successive generations, such as incremental camera improvements or slightly faster processors, fail to justify the high cost of new models for many consumers. The U.S. Consumer Product Safety Commission notes that smartphone failure rates have declined by 38% since 2018 due to better thermal management and battery longevity. In Canada, Environment and Climate Change Canada reports that extended device usage has contributed to a 22% reduction in electronic waste per capita since 2020.

Economic Pressures and Inflation-Driven Consumer Caution

The persistent inflation and macroeconomic uncertainty have significantly impeded the growth of the North America smartphone market. The U.S. Bureau of Labor Statistics recorded an 8.3% year-over-year increase in the consumer price index for communication equipment in 2023, outpacing wage growth, which rose by only 4.6%. As essential expenses such as housing, food, and healthcare consume a larger share of household budgets, consumers are deferring non-essential purchases. A 2023 survey by the Conference Board found that 54% of American consumers planned to keep their current smartphone for at least another year, citing cost as the primary factor. Similarly, in Canada, Statistics Canada reported that household debt reached a record 185% of disposable income in 2023, limiting capacity for high-ticket items. Financing options, while available, often come with interest rates exceeding 15% for subprime borrowers, as noted by the Consumer Financial Protection Bureau.

MARKET OPPORTUNITIES

Expansion of Mobile Health and Telemedicine Applications

The accelerating integration of smartphones into personal healthcare is posing new opportunities for the growth of the North America smartphone market. Apple’s ECG feature on the Apple Watch, which relies on iPhone integration, has been used in over 12 million rhythm checks as of 2023, according to the FDA’s Digital Health Center of Excellence. In Canada, the Ontario Telemedicine Network connects over 1.2 million patients annually via smartphone-enabled consultations, reducing hospital visits by 30%, as documented by the Canadian Institute for Health Information. This shift not only increases device indispensability but also opens avenues for partnerships with insurers, healthcare providers, and pharmaceutical companies, positioning smartphones as central nodes in a decentralized, patient-centric care model.

Growth of Mobile-First Financial Services and Digital Identity Platforms

The emergence of smartphones as primary tools for financial inclusion and digital identity verification is creating substantial growth opportunities for the North America smartphone market. Mobile banking, digital wallets, and peer-to-peer payment apps have become mainstream, with the Federal Reserve reporting that 87% of U.S. adults used a mobile payment app in 2023, up from 65% in 2020. Services like Zelle, Venmo, and Cash App processed over $1.3 trillion in transactions in 2023 alone, according to the American Bankers Association. Beyond payments, smartphones are now used for credit scoring, loan applications, and investment platforms. Robo-advisors like Acorns and Robinhood report that 78% of their users access services exclusively via mobile. In Canada, the federal government’s Verified. The Me platform allows citizens to use smartphones for secure identity verification in banking and healthcare, reducing fraud and streamlining access. The U.S. General Services Administration is piloting a mobile driver’s license program in 12 states, with over 5 million digital licenses issued by 2023, as reported by the Department of Homeland Security.

MARKET CHALLENGES

Escalating Cybersecurity Threats and Data Privacy Concerns

The increasing sophistication of cyber threats targeting smartphones is inhibiting the growth of the North America smartphone market. The Federal Trade Commission received over 450,000 reports of mobile-related fraud in 2023, a 32% increase from the previous year, with smishing (SMS phishing) incidents rising sharply. State-sponsored spyware such as Pegasus has demonstrated the ability to infiltrate iOS and Android devices without user interaction, as confirmed by the cybersecurity division of the U.S. Cybersecurity and Infrastructure Security Agency. In Canada, the Office of the Privacy Commissioner documented a 41% rise in data breaches involving mobile devices between 2021 and 2023, many linked to third-party apps with excessive permissions. Consumers are increasingly aware of these risks. Pew Research Center found that 72% of Americans are concerned about apps collecting their location and usage data without consent. While manufacturers have enhanced encryption and on-device processing, the fragmented app ecosystem and inconsistent update policies leave vulnerabilities. Regulatory responses, such as the proposed American Data Privacy and Protection Act, may impose compliance burdens on developers and OEMs.

Environmental Impact and Regulatory Pressure on E-Waste and Sustainability

The environmental footprint of smartphone production and disposal is attracting regulatory scrutiny and shifting consumer sentiment, which is also limiting the growth of the North America smartphone market. The extraction of rare earth elements, cobalt, and lithium for batteries involves significant ecological degradation and human rights concerns, as documented by the U.S. Geological Survey and the Department of Labor’s Bureau of International Labor Affairs. E-waste is another pressing issue only 15% of discarded smartphones in North America are properly recycled, with the rest ending up in landfills or storage, as reported by Environment and Climate Change Canada. The European Union’s Right to Repair directive is influencing North American policy, with states like California and New York enacting laws requiring manufacturers to provide repair manuals and spare parts. The Federal Trade Commission has also launched an initiative to combat planned obsolescence, citing concerns over non-replaceable batteries and software throttling. Consumers are responding: a 2023 NielsenIQ survey found that 68% of buyers consider repairability and recyclability when purchasing a new device. Companies face mounting pressure to adopt circular economy models, including modular designs, take-back programs, and longer support cycles.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Operating System, Price Band, Technology, Form Factor, Distribution Channel, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | United States, Canada, Mexico, Rest of North America |

| Market Leaders Profiled | Samsung Electronics Co., Ltd, Apple Inc., BBK Electronics Corp., Ltd, Xiaomi Corp., and Motorola Mobility LLC (Lenovo Group Ltd). |

SEGMENTAL ANALYSIS

By Operating System Insights

The android segment held 56.4% of the North America smartphone operating system market share in 2024 with its broad accessibility across price tiers and carrier ecosystems. According to the Cellular Telecommunications and Internet Association, over 70% of postpaid smartphone activations on Verizon, AT&T, and T-Mobile in 2023 were Android-based. Additionally, Android’s open ecosystem supports extensive customization, third-party app stores, and sideloading, appealing to technically inclined users and enterprise IT departments seeking control over device functionality.

The iOS segment is lucratively to grow lucratively with an expected CAGR of 6.3% from 2026 to 2034 with Apple’s tightly integrated hardware-software ecosystem, which fosters exceptional user retention and cross-device loyalty. As of 2023, over 92% of iPhone users in the U.S. upgraded to another iPhone, the highest brand loyalty rate among smartphone manufacturers, according to the U.S. Department of Commerce’s Bureau of Economic Analysis. The seamless integration between iPhone, iPad, Mac, Apple Watch, and AirPods creates a compelling value proposition for consumers invested in the Apple ecosystem. Additionally, iOS benefits from superior software longevity. Apple provides up to seven years of iOS updates, compared to an average of three for Android devices, as confirmed by the National Institute of Standards and Technology. This extended support enhances device resale value and reduces the urgency to switch platforms. In Canada, iOS holds a 42% market share, rising to 55% in urban centers like Toronto and Vancouver, where higher disposable incomes and tech-savvy demographics favor premium devices, as reported by Statistics Canada.

By Price Band Insights

The mid-range smartphone segment was the largest and held 48.3% of the North America smartphone market share in 2024, with a confluence of economic pragmatism and technological parity, where consumers seek high-value devices without the premium price tag. According to the Consumer Technology Association, 62% of smartphone buyers in 2023 prioritized "value for money" over brand prestige, with mid-range phones delivering 80–90% of the functionality of top-tier models at half the cost. In Canada, the trend is amplified by the rising popularity of carrier-agnostic models, with Best Buy Canada reporting a 34% year-over-year increase in mid-range smartphone sales. Additionally, the secondhand market has elevated expectations: refurbished premium phones now compete in this band, pushing OEMs to enhance features.

The entry-level smartphone segment is projected to grow at a CAGR of 7.1% from 2026 to 2034, with the increasing demand from cost-conscious consumers, secondary device users, and underserved populations who rely on smartphones as their sole internet access point. According to the Federal Communications Commission, 14% of U.S. households are "smartphone-dependent," meaning they lack home broadband and rely entirely on mobile data. For these users, affordable devices like the Motorola Moto G series and Samsung Galaxy A14 are essential for education, job searches, and telehealth. Additionally, prepaid and MVNO (Mobile Virtual Network Operator) carriers such as Mint Mobile and Cricket Wireless have expanded service plans tailored to budget devices, often bundling phones with unlimited data for under $30 per month. In Canada, Indigenous and remote communities in the Northwest Territories and Nunavut increasingly adopt low-cost smartphones for connectivity, with Indigenous Services Canada noting a 40% increase in mobile device distribution programs since 2020. The rise of durable, long-battery-life models with 4G/5G support has improved functionality in this segment.

By Technology Insights

The 5G technology segment in the North America smartphone market held a dominant share in 2025 with the near-complete phaseout of 3G networks and aggressive carrier migration toward 5G infrastructure. AT&T, Verizon, and T-Mobile have all decommissioned their 3G networks, compelling users to upgrade to at least 4G-capable devices, with 5G now the default offering. The Federal Communications Commission confirms that 5G coverage extends to over 90% of the U.S. population, with mid-band and mmWave deployments enabling download speeds exceeding 300 Mbps in urban areas.

5G segment is anticipated to register a CAGR of 9.4% from 2026 to 2034 with the transition from standalone 5G (SA) networks, which offer lower latency and higher reliability than initial non-standalone (NSA) deployments. Carriers are now rolling out SA 5G, which supports advanced use cases like autonomous vehicle coordination and remote industrial control, necessitating newer smartphones with updated modems. According to T-Mobile’s 2023 Network Expansion Report, its standalone 5G coverage increased by 65% in one year, reaching 250 million people. Additionally, the proliferation of private 5G networks in sectors such as manufacturing, logistics, and healthcare is creating demand for ruggedized 5G smartphones capable of operating in industrial environments. The Department of Defense has also initiated procurement of 5G-enabled devices for secure battlefield communications, as disclosed in its 2023 Digital Modernization Strategy. In Canada, the federal government’s 5G for Rural Canada program is funding 5G-enabled devices for telehealth and distance learning in remote communities, with over 120,000 units distributed in 2023 alone, as reported by Innovation, Science and Economic Development Canada.

By Form Factor Insights

The bar form factor segment was the largest by holding a prominent share of the North America smartphone market in 2025. The vast majority of smartphones, from budget models to premium flagships, are built in this format by offering a proven balance of screen size, portability, and durability. According to the National Highway Traffic Safety Administration, bar-style phones are less prone to mechanical failure and water ingress compared to foldable devices, with drop survival rates 40% higher in standardized tests. Carriers and retailers favor this form due to ease of inventory management and compatibility with existing accessories like cases, mounts, and charging docks. In Canada, the bar form remains the standard in public safety and transportation sectors, where RCMP, firefighters, and transit operators rely on durable, glove-compatible devices, as noted by Public Safety Canada.

The foldable and flip smartphones segment is more likely to witness a CAGR of 18.7% from 2026 to 2034, with the technological maturation, with improved hinge durability, reduced crease visibility, and enhanced water resistance making foldables more viable for daily use. Samsung’s Galaxy Z Flip and Z Fold series have led adoption, with over 3.2 million units sold in North America in 2023, as reported by Samsung Electronics America. According to a 2023 survey by the Fashion Institute of Technology, 58% of women aged 18–34 preferred flip phones for their aesthetic appeal and discreet usability. In Canada, Telus reported a 120% increase in foldable activations in 2023, attributing it to improved carrier support and trade-in programs. Google’s entry with the Pixel Fold in 2023 has intensified competition, pushing innovation in software optimization for dual-screen interfaces.

By Distribution Channel Insights

The operator and carrier-owned segment was the largest with 52.3% of the North America smartphone market share in 2024, with the controlled subsidy models, installment plans, and network bundling that lower the upfront cost barrier for consumers. Major providers such as Verizon, AT&T, and T-Mobile offer "free" or heavily discounted smartphones when bundled with postpaid service plans, a strategy that drives customer acquisition and retention. According to the Federal Communications Commission, over 68% of new smartphone activations in the U.S. occur through carrier channels, where sales representatives guide device selection based on service compatibility and data needs. Additionally, rural and underserved areas often lack brand-owned retail presence, making carrier outlets the default point of purchase. The integration of eSIM technology has further strengthened carrier control by allowing remote provisioning and reducing reliance on third-party retailers.

The online distribution channel segment is projected to grow with a CAGR of 11.3% from 2026 to 2034, with the shift in consumer behavior toward digital shopping, accelerated by the pandemic and sustained by convenience, price transparency, and expanded delivery networks. E-commerce platforms like Amazon, BestBuy.com, and direct-to-consumer brand websites now offer comprehensive product comparisons, user reviews, and instant financing options, empowering informed decisions. In Canada, Shopify reports that mobile device sales through independent online retailers grew by 41% in 2023, driven by competitive pricing and fast shipping. Additionally, the rise of refurbished and open-box marketplaces like Back Market and Gazelle has expanded access to premium devices at lower costs.

COUNTRY-LEVEL ANALYSIS

United States Smartphone Market Insights

The United States was the top performer of the North America smartphone market with 86.3% of share in 2024 with the world’s most advanced telecommunications infrastructure, a highly competitive carrier landscape, and a culture of rapid technology adoption. The Federal Communications Commission reports that 5G coverage now reaches 92% of the population, enabling widespread adoption of next-generation smartphones. Additionally, the U.S. leads in mobile-first services, from digital banking to telehealth, reinforcing device indispensability. The Consumer Technology Association notes that Americans spend an average of 4.8 hours daily on smartphones, the highest in North America.

Canada Smartphone Market Insights

Canada smartphone market held 12.3% of the share in 2024 with a smaller but highly developed digital ecosystem. The country exhibits high smartphone penetration, with over 89% of the population owning a device, driven by universal carrier coverage and strong integration of mobile services into daily life. In recent years, the government has prioritized digital inclusion, launching initiatives like Connecting Families, which provides low-cost smartphones and data plans to low-income households. Environment and Climate Change Canada also reports rising consumer demand for repairable and sustainable devices, influencing brand strategies.

COMPETITIVE LANDSCAPE

The competition in the North America smartphone market is characterized by a high-stakes interplay between technological leadership, brand loyalty, and ecosystem control. While the market is mature and growth is constrained by long replacement cycles, rivalry remains intense as players vie for mindshare in a space where innovation is incremental and consumer expectations are sky-high. Apple and Samsung dominate through scale, vertical integration, and retail influence, but their competition is less about price and more about defining the future of mobile interaction. Google challenges the status quo by leveraging software intelligence and AI to differentiate its Pixel line, positioning itself as the innovator of the Android experience rather than just another hardware vendor. The battlefield has shifted from raw specifications to holistic user experience privacy, sustainability, seamless connectivity, and personalization are now key differentiators. Carriers amplify this competition by bundling devices with services, financing, and network perks, turning every upgrade into a strategic retention opportunity. Meanwhile, emerging trends like foldables, on-device AI, and digital identity are creating new arenas for differentiation.

KEY MARKET PLAYERS

Noteworthy Companies dominating the North America Smartphone market profiled in the report are

- Samsung Electronics Co., Ltd

- Apple Inc.

- Google LLC

- BBK Electronics Corp., Ltd

- Xiaomi Corp.

- Motorola Mobility LLC

TOP LEADING PLAYERS IN THE MARKET

- Apple stands as a defining force in the North America smartphone market, where the iPhone is not merely a communication device but a cultural and technological benchmark. The company’s vertically integrated ecosystem, seamlessly linking hardware, software, and service,s creates unparalleled user loyalty and enables a premium brand experience. Apple’s influence extends globally through its App Store, privacy-centric design philosophy, and leadership in semiconductor innovation with its custom A- and M-series chips. Its retail presence, both physical and digital, sets industry standards for customer engagement and after-sales support. Apple has redefined the smartphone’s role in personal and societal infrastructure by making it a central node in the digital lives of millions across North America and beyond.

- Samsung Electronics holds a dominant position in the North America smartphone landscape, distinguished by its comprehensive product portfolio that spans entry-level to ultra-premium devices. The company’s strength lies in its end-to-end manufacturing capabilities, from displays and memory chips to finished handsets, allowing rapid innovation and supply chain resilience. Samsung’s Galaxy series, particularly the S and Z lines, drives technological frontiers in foldable design, camera systems, and 5G integration. Its deep partnerships with U.S. carriers and commitment to Android ecosystem leadership enable widespread distribution and influence. Beyond hardware, Samsung invests heavily in software localization, security (Knox), and cross-device synergy, ensuring relevance in both consumer and enterprise markets. Globally, Samsung’s scale and R&D investment make it the most formidable competitor to Apple, shaping industry trends and setting benchmarks in display technology and mobile form factors.

- Google has redefined the Android experience in North America through its Pixel smartphone line, serving as a flagship reference for the world’s most widely used mobile operating system. Unlike other Android OEMs, Google controls both the software and hardware integration, allowing it to showcase the full potential of AI-driven features, computational photography, and real-time language translation. The Pixel series acts as a proving ground for innovations later adopted across the broader Android ecosystem, reinforcing Google’s strategic influence over mobile computing. Its focus on privacy, timely security updates, and seamless integration with Google Workspace, Assistant, and cloud services position the smartphone as an intelligent personal assistant. By prioritizing software-led differentiation over hardware excess, Google shapes the future of mobile interaction, emphasizing context-aware computing, sustainability, and ethical design, with global implications for how users engage with technology.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One major strategy employed by leading players is ecosystem integration, where smartphones are positioned as central hubs within a broader network of devices and services. Companies like Apple and Samsung link phones to wearables, tablets, smart home systems, and cloud platforms, creating seamless user experiences that increase switching costs and brand dependency. This interconnected environment fosters long-term customer retention and drives cross-product sales.

Another approach is vertical innovation, particularly in semiconductor and camera technology. By designing proprietary processors and imaging systems, companies gain performance advantages, differentiate their offerings, and reduce reliance on third-party components. This control over core technologies enables faster optimization, improved energy efficiency, and unique features that are difficult for competitors to replicate.

RECENT MARKET DEVELOPMENTS

- In March 2023, Apple introduced Priority Messages in iMessage, allowing users to texts from contacts by enhancing communication clarity and reinforcing the iPhone’s role as a personalized digital hub.

- In July 2023, Samsung launched its Galaxy AI platform in North America, bringing on-device generative AI features like real-time call translation and photo editing to the Galaxy S23 series, which is elevating its software differentiation.

- In October 2023, Google announced a partnership with T-Mobile to offer exclusive Pixel Pass benefits, including cloud storage, YouTube Premium, and device upgrades by deepening its integration with carrier ecosystems.

- In January 2024, Apple expanded its Self Service Repair program to include iPhone 14 and 15 models, responding to Right to Repair advocacy and improving customer retention through enhanced service accessibility.

- In May 2024, Samsung unveiled a new AI-powered camera assistant on the Galaxy S24 series, capable of automatically optimizing settings based on scene recognition and user behavior, which is setting a new standard for computational photography.

MARKET SEGMENTATION

This North America Smartphone market research report is segmented and sub-segmented into the following categories.

By Operating System

- Android

- iOS

- Others (KaiOS, HarmonyOS, etc.)

By Price Band

- Entry-level (Less than USD 200)

- Mid-range (USD 200 - 499)

- Premium (USD 500 - 799)

- Ultra-premium (Greater than or equal to USD 800)

By Technology

- 5G

- 4G/LTE

- 3G and Below

By Form Factor

- Bar

- Foldable/Flip

- Rugged/Industrial

By Distribution Channel

- Operator/Carrier Stores

- Brand-Owned Retail

- Multi-brand Physical Retail

- Online Direct-to-Consumer

By Country

- United States

- Canada

- Mexico

- Rest of North America

Frequently Asked Questions

1. What is the projected value of the North America Smartphone Market by 2034?

The North America Smartphone Market is forecast to reach USD 259.24 billion by 2026–2034, growing at a CAGR 2.94%.

2. Which brands lead the North America Smartphone Market?

Apple dominates with roughly 55–57% market share, followed by Samsung at around 22–23%, and Google, Motorola, and Xiaomi making up smaller portions of the market.

3. What is the market share between iOS and Android in North America?

iOS (Apple) leads with around 60% market share, about 20 percentage points ahead of Android, reflecting strong Apple brand loyalty and seamless integration within the Apple ecosystem.

4. What are the core drivers of the North America Smartphone Market?

Growth is propelled by high disposable incomes, early tech adoption, robust 5G rollout, digital transformation, demand for premium devices, and a culture of rapid innovation and device upgrades.

5. How is 5G adoption impacting the North America Smartphone Market?

Expanding 5G networks drive strong demand for device upgrades as consumers seek faster data speeds, lower latency, and improved mobile experiences for streaming, gaming, and connectivity.

6. What are the primary challenges in the North America Smartphone Market?

The market faces saturation—over 90% smartphone penetration in the US—leading to slower new user growth, supply chain disruptions, longer replacement cycles, and environmental pressures for sustainable production.

7. What trends are emerging in the North America Smartphone Market?

Rising emphasis on sustainability, premium device growth, AI and AR/VR integration, longer device lifespans, smart home interoperability, and eco-friendly materials are key trends.

8. How is the smartphone replacement cycle evolving in North America?

Consumers are now keeping devices for longer periods, with trade-in and financing programs by carriers and OEMs incentivizing upgrades, especially in the premium device segment.

9. What segments dominate the North America Smartphone Market?

Premium smartphones (USD 800+) are favored for their features and brand prestige, but mid-range devices are also significant, while low-end segments are shrinking due to declining prepaid demand.

10. Who are the leading operating system providers in the North America Smartphone Market?

iOS (Apple) and Android (Google) are the leading mobile operating systems, with iOS maintaining a significant lead due to strong brand loyalty and ecosystem integration.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com