Global Organic Beverage Market Size, Share, Trends,& Growth Forecast Report Segmented By Product (Non-Dairy, Fruit, Coffee & Tea, Beer & Wine), Distribution Channel (Offline, Online), And Region (North America, Europe, APAC, Latin America, Middle East And Africa) – Industry Analysis From 2026 To 2034

Global Organic Beverage Market Size

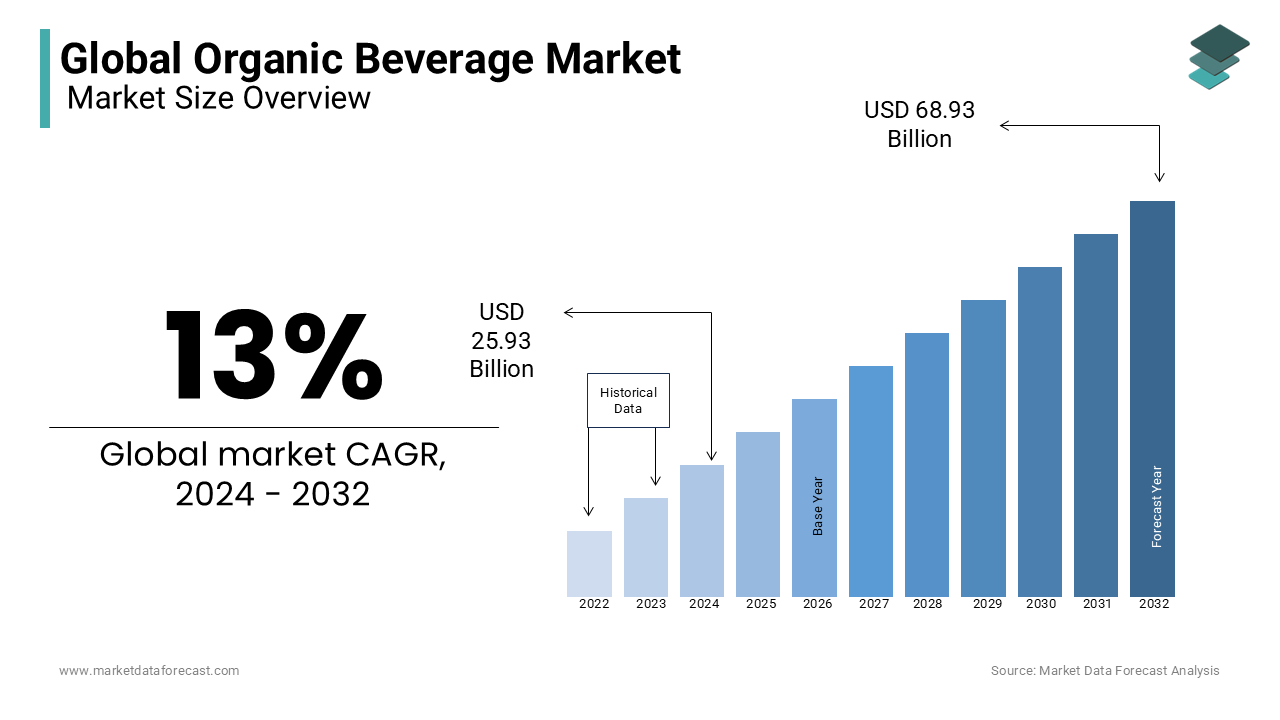

The global organic beverage market size was calculated to be USD 29.30 billion in 2025 and is anticipated to be worth USD 88.02 billion by 2034, from USD 33.11 billion in 2026, growing at a CAGR of 13% during the forecast period. The demand for sugar-free caffeine-free beverages will increase demand for products in the coming years.

Organic Beverage refers to non-alcoholic and alcoholic drinks produced from ingredients cultivated without synthetic pesticides, fertilizers, genetically modified organisms (GMOs), or artificial additives, and certified under recognized organic standards such as USDA Organic, EU Organic, or JAS. These beverages encompass a broad spectrum, including organic fruit juices, plant-based milks, teas, functional waters, kombucha, and craft beers. As consumer awareness intensifies regarding dietary impact on long-term health and environmental sustainability, demand for transparently sourced, chemical-free beverages has surged.

MARKET DRIVERS

Growing Prevalence of Lifestyle-Related Chronic Diseases is a pivotal driver of demand for organic beverages, as consumers seek dietary interventions to mitigate health risks. The World Health Organization attributes 77% of global deaths from non-communicable diseases to conditions such as type 2 diabetes, cardiovascular disorders, and obesity—many of which are influenced by diet. Individuals consuming diets high in ultra-processed foods faced a greater risk of developing metabolic syndrome compared to those prioritizing whole, minimally processed alternatives. Organic beverages, particularly unsweetened plant-based milks and cold-pressed juices, are perceived as healthier substitutes to sugar-laden conventional drinks. The American Heart Association notes that the average American consumes 17 teaspoons of added sugar daily, far exceeding the recommended limit. In response, health-conscious consumers are shifting toward organic kombucha and herbal infusions, which contain natural probiotics and polyphenols, positioning these beverages as functional components of preventive healthcare regimens.

Heightened Environmental Consciousness Among Younger Demographics is significantly shaping purchasing behavior in the organic beverage sector. As per the United Nations Environment Programme, agriculture accounts for 70% of global freshwater use and 30% of greenhouse gas emissions, with conventional farming practices contributing heavily to soil degradation and biodiversity loss. A notable share of Millennials and Gen Z consumers in North America and Western Europe consider environmental sustainability a primary factor when selecting food and drink products. Organic farming, which prohibits synthetic agrochemicals and emphasizes crop rotation and soil health, aligns with these values. Brands like Recess and Health-Ade have capitalized on this sentiment by using regeneratively farmed ingredients and climate-neutral packaging.

MARKET RESTRAINTS

Limited Availability of Certified Organic Raw Materials constrains the scalability and consistency of organic beverage production. Many key ingredients, such as organic citrus, apples, oats, and tea leaves, face supply shortages due to the three-year transition period required for land conversion to organic status and the lower yields typically associated with chemical-free cultivation. According to the U.S. Department of Agriculture, only 1% of total U.S. cropland is certified organic. This dependency exposes manufacturers to geopolitical disruptions, fluctuating tariffs, and logistical delays. Furthermore, inconsistent certification standards across countries complicate global sourcing, forcing brands to invest heavily in supply chain auditing to maintain compliance and consumer trust.

High Susceptibility to Contamination and Shorter Shelf Life presents a significant operational restraint for organic beverage manufacturers. Without synthetic preservatives such as potassium sorbate or sodium benzoate, organic drinks are more vulnerable to microbial spoilage, particularly in ready-to-drink formats like kombucha and fresh juices. The absence of ultrapasteurization in some “raw” organic products further amplifies risk. This necessitates complex cold-chain logistics and limits distribution reach, particularly in regions with underdeveloped refrigerated transport infrastructure, such as parts of Southeast Asia and Sub-Saharan Africa, impeding market expansion.

MARKET OPPORTUNITIES

Expansion of Functional and Adaptogenic Organic Beverages offers a transformative opportunity for innovation and premiumization. Consumers are increasingly seeking beverages that deliver cognitive, immune, and emotional benefits beyond hydration. Brands like Rebbl and Sun Goddess have introduced USDA-certified organic elixirs combining adaptogens with plant-based milks, targeting stress reduction and mental clarity. Hence, manufacturers are investing in evidence-based formulations to capture high-value segments in urban, health-focused markets.

Rise of Direct-to-Consumer (DTC) and Subscription-Based Models is enabling organic beverage brands to bypass traditional retail bottlenecks and cultivate deeper consumer relationships. DTC beverage sales in the U.S. grew, with organic brands leading the trend. Companies such as Harmless Harvest and Suja Life offer monthly kombucha and cold-pressed juice subscriptions, leveraging data analytics to personalize offerings and reduce waste. These models also allow brands to maintain control over branding, pricing, and education, particularly around sourcing and sustainability. By integrating e-commerce with content marketing and community engagement, organic beverage companies are building loyal followings and insulating themselves from retailer margin pressures and shelf-space limitations.

MARKET CHALLENGES

Ensuring Ingredient Authenticity and Preventing Fraud remains a critical challenge in the organic beverage industry. The premium pricing of organic products creates incentives for adulteration, such as blending organic juice with conventionally grown concentrates or mislabeling origin. The absence of universally standardized testing protocols complicates verification. Isotopic analysis and DNA barcoding are emerging tools, but their high cost limits widespread adoption. Brands must invest in blockchain traceability and third-party audits to uphold integrity, but smaller producers often lack the resources, risking reputational damage across the sector.

Navigating Divergent Global Organic Certification Standards poses a persistent challenge for multinational beverage companies. While the USDA, EU Organic, and Japan’s JAS systems share core principles, they differ in allowable substances, labeling thresholds, and inspection protocols. According to the International Federation of Organic Agriculture Movements, over 90 countries have distinct organic regulations, complicating export strategies. For instance, the EU prohibits the use of certain natural flavorings permitted under USDA standards, forcing reformulation for market entry. Harmonization efforts, such as the U.S.-EU Organic Equivalency Arrangement, cover only select commodities and exclude many beverage ingredients. This regulatory fragmentation increases compliance costs and delays product launches, particularly for emerging brands aiming to scale internationally without diluting their organic integrity.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 13% |

| Segments Covered | By Product, Distribution Channel, And Region |

| Various Analyses Covered | Global, Regional and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Boncafe International, Empresa, Uncle Matt's Organic Inc., Parker's organic juices, Bison organic beer, Heavenly Body Servant, Belvoir Fruit Farms Ltd, Coca-Cola Corporation, Whitewave Foods Company, PepsiCo, Inc |

SEGMENTAL ANALYSIS

By Product Insights

The fruit segment dominated the organic beverage market by capturing 31.7% of global revenue in 2023, as reported by Statista. This position is anchored in widespread consumer preference for naturally sweet, nutrient-dense drinks without added sugars or artificial flavors. Organic fruit juices, particularly cold-pressed varieties, are perceived as healthier alternatives to soda and energy drinks. According to the U.S. Centers for Disease Control and Prevention, only 10% of American adults meet the daily recommended intake of fruits and vegetables, prompting many to turn to organic juices as a dietary supplement. The USDA’s Pesticide Data Program found that conventionally grown apples, oranges, and grapes consistently rank among the top five produce items with pesticide residues, further driving demand for organic versions. Brands like Evolution Fresh and Pressed Juicery have capitalized on this trend by emphasizing transparent sourcing and high vitamin C content, reinforcing the segment’s appeal across health-conscious demographics.

The non-dairy segment is the fastest-growing and is projected to expand at a CAGR of 14.7% from 2025 to 2030, according to Grand View Research. This surge is fueled by rising lactose intolerance, veganism, and concerns over the environmental impact of dairy farming. As per the National Institute of Diabetes and Digestive and Kidney Diseases, approximately 68% of the global population exhibits some degree of lactose malabsorption, making plant-based milks a functional necessity. The Global Dairy Platform reports that producing one liter of conventional cow’s milk generates nearly three times the greenhouse gas emissions of oat or almond milk. Innovations in texture and taste, such as enzyme-treated oat milk for creaminess, have enhanced consumer acceptance. Oatly and Califia Farms have led this shift, introducing organic-certified oat, almond, and cashew beverages fortified with calcium and B12. Additionally, the integration of non-dairy organic drinks into coffee culture, with barista-grade formulations, has broadened their usage beyond dietary substitution into mainstream lifestyle consumption.

By Distribution Channel Insights

The offline distribution segment remained the dominant channel by accounting for 62.8% of the organic beverage market in 2025. This dominance is sustained by consumer reliance on physical retail environments, particularly natural food stores, supermarkets, and specialty grocers, for product discovery and immediate consumption. Retailers such as Whole Foods Market, Wegmans, and Eroski in Spain dedicate significant shelf space to organic beverages, often with in-store signage highlighting certifications and sourcing ethics. According to the Food Marketing Institute, 71% of U.S. shoppers inspect product labels in-store before purchasing organic items, valuing tactile engagement and instant availability. In emerging markets like India and Brazil, kirana stores and local cooperatives serve as primary access points, especially in areas with limited internet connectivity. Additionally, promotional activities such as sampling booths and loyalty programs in physical stores have proven effective in driving trial and repeat purchases, reinforcing offline retail’s entrenched role in consumer decision-making.

The online distribution segment is the fastest-growing channel by registering a CAGR of 15.3% from 2026 to 2034. The acceleration is driven by digital adoption, subscription models, and targeted e-commerce strategies that cater to urban, time-constrained consumers. Online sales of organic groceries in the U.S. surged, with beverages being one of the top-performing categories. Platforms like Thrive Market and Amazon Fresh have introduced curated organic beverage boxes, personalized recommendations, and auto-replenishment features, enhancing convenience and retention. A notable share of premium organic buyers prefer online channels for discovering niche or regional brands not available in local stores. In Southeast Asia, platforms such as Lazada and Flipkart have partnered with organic startups to offer first-time buyer discounts and carbon-neutral delivery options. Thus, the digital expansion of organic beverage commerce is poised for sustained momentum.

REGIONAL ANALYSIS

North America Organic Beverage Market Insights

North America led the global organic beverage market by securing a 37.7% share in 2025. The region’s preeminence is underpinned by high consumer awareness, robust certification infrastructure, and strong retail integration of organic products. The USDA’s National Organic Program enforces strict production and labeling standards, fostering consumer trust. California and New York are epicenters of innovation, hosting brands like Suja Life and Harmless Harvest that pioneer cold-pressed and functional organic drinks. Additionally, corporate wellness programs and school nutrition policies increasingly mandate organic beverage options, further institutionalizing demand. With over 55% of U.S. households purchasing organic products at least occasionally, North America remains the benchmark for market maturity and consumer engagement.

Europe Organic Beverage Market Insights

Europe holds a market share, with Germany, France, and the UK driving adoption. The European Union’s organic policy framework mandates clear labeling and prohibits GMOs, synthetic additives, and irradiation, reinforcing consumer confidence. Organic beverage sales in Germany grew annually between 2020 and 2023, fueled by demand for organic apple juice and kombucha. Retail chains like Tesco and Carrefour have committed to expanding their organic private-label beverage lines. Additionally, the Nordic countries lead in sustainability integration, aligning product offerings with regional environmental values.

Asia Pacific Organic Beverage Market Insights

Asia Pacific is another key player in the market, propelled by rising urban affluence and growing exposure to Western wellness trends. Japan and South Korea are at the forefront. Japanese consumers favor organic green tea and barley-based drinks. In India, the FSSAI’s organic certification scheme (Jaivik Bharat) has enabled domestic brands like Organic India and Srikumar to scale. Urbanization and rising disposable income are expanding access, while e-commerce platforms like Flipkart and Tmall Global facilitate cross-border availability. Despite low per capita consumption, the sheer population base and increasing health consciousness position Asia Pacific as a high-potential growth frontier.

Latin America Organic Beverage Market Insights

Latin America accounts for a notable share of the market, with Brazil and Mexico emerging as key contributors. Brazil’s organic sector has gained momentum, with the Ministry of Agriculture certifying over 12,000 organic producers in 2023, including major citrus and sugarcane farms that supply juice manufacturers. Chile has become a major exporter of organic grape juice concentrate to North American and European brands, leveraging its pesticide-free vineyards. However, domestic retail penetration remains limited outside major cities. To bridge this gap, brands like BioFrut and NaturAlma have launched direct-to-consumer delivery models. With organic farmland in the region growing at 8% annually, as per the Research Institute of Organic Agriculture (FiBL), Latin America is evolving into a strategic sourcing and consumption hub.

Middle East and Africa Organic Beverage Market Insights

Middle East and Africa collectively hold a notable share of the global market, with Israel, the UAE, and South Africa leading regional development. Israel’s Ministry of Agriculture supports organic farming through subsidies and export incentives, resulting in an annual increase in certified organic acreage between 2020 and 2023. Israeli brands like Tivall produce organic fruit nectars and plant-based drinks for both domestic and European markets. In the UAE, Dubai’s Sustainable City and Abu Dhabi’s Khalifa Fund promote organic agri-tech startups, including date-based beverage producers. Rooibos, native to the Western Cape, is naturally caffeine-free and rich in antioxidants, qualifying it for organic and functional beverage positioning. With rising health awareness and government backing, the region is gradually building a credible organic beverage ecosystem.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Major Key Players in the Global Organic Beverage Market are Boncafe International, Empresa, Uncle Matt's Organic Inc., Parker's organic juices, Bison organic beer, Heavenly Body Servant, Belvoir Fruit Farms Ltd, Coca-Cola Corporation, Whitewave Foods Company, PepsiCo, Inc.

The competition in the Organic Beverage Market is intensifying as multinational corporations, regional specialty brands, and agile startups vie for consumer attention in a rapidly evolving landscape. Established players leverage scale, distribution, and R&D to introduce certified organic variants of mainstream products, while niche brands differentiate through authenticity, innovation, and hyper-local sourcing. Price sensitivity, varying regulatory environments, and consumer skepticism about greenwashing create barriers to trust. Differentiation is achieved through functional benefits, sustainable packaging, and transparent supply chains. The rise of e-commerce and direct-to-consumer models has lowered entry barriers, increasing fragmentation. As health consciousness and environmental responsibility become central to purchasing decisions, companies must balance scientific credibility, ethical sourcing, and sensory appeal to maintain relevance in a dynamic and increasingly scrutinized market.

TOP PLAYERS IN THE MARKET

Nestlé

Nestlé has significantly expanded its footprint in the Asia Pacific organic beverage sector by leveraging its global R&D infrastructure and localized brand adaptation. The company launched organic variants of its flagship Milo and Nescafé lines in Australia and New Zealand, using certified organic cocoa and coffee sourced from Papua New Guinea and Vietnam. The company also invested in regenerative agriculture initiatives across Southeast Asia, working with smallholder farmers in Thailand to transition rice and coconut farms to organic practices. By aligning with regional sustainability goals and integrating organic offerings into its mainstream distribution network, Nestlé has enhanced accessibility and credibility in a market increasingly sensitive to environmental and health claims.

Danone

Danone has established a strong presence in the Asia Pacific organic beverage landscape through its premium plant-based and dairy-alternative portfolios. The company introduced organic-certified Silk and Alpro products in Singapore and South Korea, featuring oat and almond milks fortified with essential nutrients. The company also strengthened its cold-chain logistics in India to support the distribution of fresh, unpasteurized organic drinks in metropolitan areas. Through its “One Planet. One Health” framework, Danone emphasizes carbon-neutral production and recyclable packaging, resonating with environmentally aware consumers. By focusing on innovation in texture, taste, and sustainability, Danone has positioned itself as a leader in premium organic beverages across diverse cultural and dietary preferences in the region.

Coca-Cola Company

Coca-Cola Company has strategically diversified into the organic beverage space in Asia Pacific through acquisitions and reformulations of niche brands. Its ownership of AdeZ, an organic plant-based drink line, has been extended to markets such as Indonesia, Malaysia, and Taiwan, featuring soy, almond, and oat formulations with no artificial additives. The company also invested in blockchain traceability systems to verify the organic origin of ingredients across its supply chain in Vietnam and Sri Lanka. By utilizing its unparalleled distribution network and brand visibility, Coca-Cola has brought organic beverages into mainstream retail and convenience channels, increasing consumer access. This integration of organic offerings into a mass-market infrastructure enables scalability while maintaining compliance with regional organic certification standards.

TOP STRATEGIES USED BY KEY MARKET PLAYERS

Key players in the Organic Beverage Market are deploying vertical integration, strategic acquisitions, product innovation, sustainability-driven branding, and digital engagement to consolidate their positions. Companies are securing direct supply chains by partnering with organic farms to ensure ingredient authenticity and reduce dependency on third-party suppliers. Expansion into functional beverages—infused with adaptogens, probiotics, or plant proteins—allows premium pricing and differentiation. Major firms are reformulating existing products to meet organic certification standards while leveraging their distribution dominance. E-commerce optimization, subscription models, and blockchain-based traceability enhance consumer trust and loyalty. Additionally, investment in regenerative agriculture and carbon-neutral packaging aligns with global ESG expectations, strengthening brand equity in environmentally conscious markets across North America, Europe, and Asia Pacific.

RECENT HAPPENINGS IN THE MARKET

- In January 2023, Nestlé launched an organic version of its Wunda oat milk in Australia, sourced from certified organic farms in New South Wales, to meet rising demand for plant-based alternatives in the Organic Beverage Market.

- In March 2023, Danone introduced an organic matcha oat beverage in Japan, developed in collaboration with Shizuoka tea growers, to expand its premium plant-based portfolio in the Organic Beverage Market.

- In June 2023, Coca-Cola Company expanded its AdeZ organic plant-based drink line to Malaysia and Indonesia, utilizing local distribution networks to enhance regional availability in the Organic Beverage Market.

- In September 2023, PepsiCo partnered with an organic coconut water supplier in the Philippines to launch a new line of cold-pressed organic hydration drinks in Southeast Asia in the Organic Beverage Market.

- In February 2025, Fraser & Neave launched an organic-certified lychee juice in Singapore, using fruit from pesticide-free orchards in Thailand, to capture health-focused urban consumers in the Organic Beverage Market.

MARKET SEGMENTATION

This research report on the global organic beverage market has been segmented and sub-segmented based on product, distribution channel, & region.

By Product

- Non-dairy drinks (soy, rice, and oats)

- Fruit drinks

- Coffee and tea

- Beer and wine

By Distribution channel

- Offline

- Online

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What factors are driving the Global Organic Beverage Market growth?

Health awareness, clean-label preferences, and increasing consumption of organic juices, teas, and functional drinks fuel market growth.

2. Which regions dominate the Global Organic Beverage Market?

North America and Europe lead the Global Organic Beverage Market, while Asia Pacific shows the fastest growth with rising urbanization.

3. What are the key product segments in the Global Organic Beverage Market?

The market includes organic juices, teas, coffees, dairy alternatives, functional beverages, and flavored waters.

4. What role do functional beverages play in the Global Organic Beverage Market?

Functional organic beverages with added vitamins, probiotics, and plant extracts are gaining strong popularity worldwide.

5. Who are the leading players in the Global Organic Beverage Market?

Key players include The Hain Celestial Group, PepsiCo, Danone, Nestlé, and Organic Valley.

6. What challenges affect the Global Organic Beverage Market?

Challenges include higher production costs, limited raw material availability, and shorter shelf life of organic beverages.

7. What are the major trends in the Global Organic Beverage Market?

Trends include plant-based beverages, sugar-free organic drinks, sustainable packaging, and premium wellness-focused products.

8. What opportunities exist in the Global Organic Beverage Market?

Opportunities lie in functional wellness beverages, dairy alternatives, and expanding into Asia-Pacific and Middle Eastern markets.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com