Global Over the Counter (OTC) Drugs Market Size, Share, Trends & Growth Forecast Report Segmented By Product Type (Analgesics, Cough, Cold, and Flu Products, Vitamins and Minerals, Dermatological Products, Gastrointestinal Products, Ophthalmic Products, Sleep Aid Products, Weight Loss/Diet Products and Others), Formulation Type (Tablets, Liquids, Ointments and Sprays), Distribution Channel (Pharmacies, Supermarkets/Hypermarkets, Convenience stores and Others (Online Drug Stores) and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2025 to 2033

Global Over-the-Counter (OTC) Drugs Market Summary

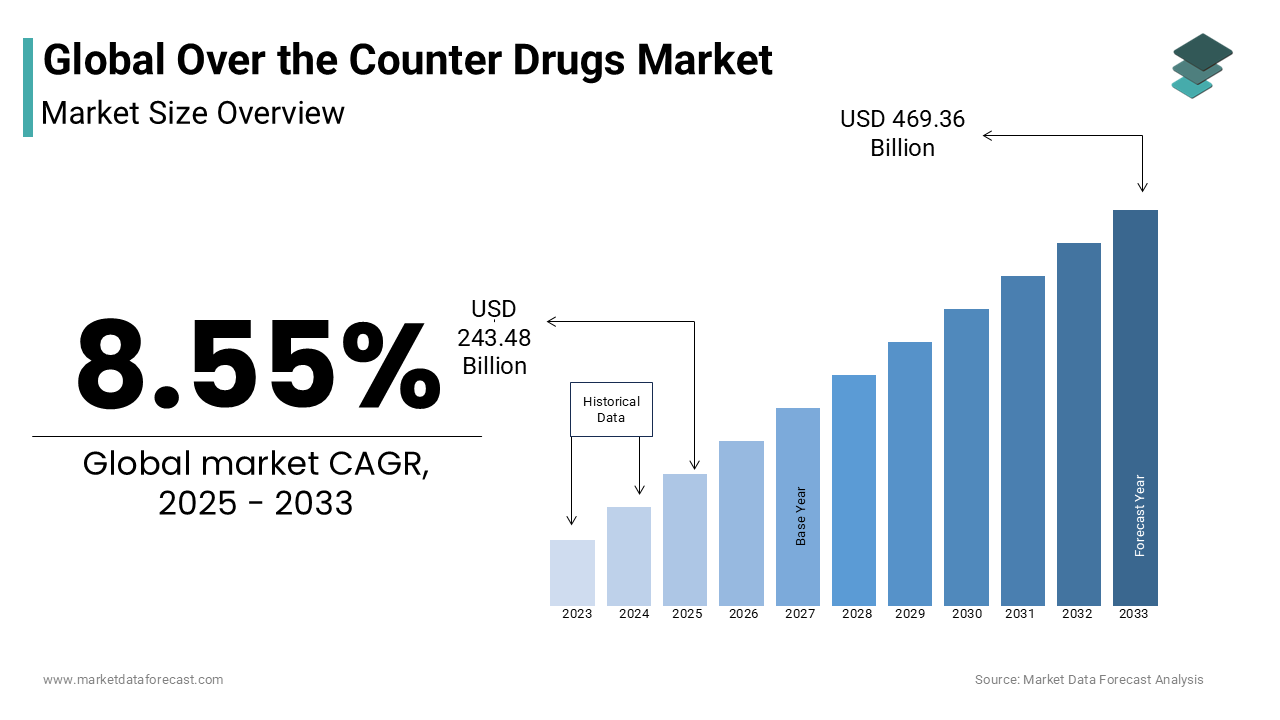

The global over-the-counter (OTC) drugs market size was valued at USD 224.3 billion in 2024, projected to reach USD 243.48 billion in 2025 and further expand to USD 469.36 billion by 2033, at a CAGR of 8.55% from 2025 to 2033. The growth of the market is fueled by increasing self-medication practices, greater access to healthcare products, a growing elderly population, and cost-effectiveness compared to prescription drugs.

Key Market Trends

- Increasing adoption of self-medication practices, particularly for common illnesses like cold, flu, and allergies.

- Rising demand for vitamins, minerals, and dietary supplements as preventive healthcare gains momentum.

- Strong growth of online and e-commerce pharmacies, making OTC drugs more accessible globally.

- Expansion of geriatric population driving sustained demand for gastrointestinal and pain management products.

Segmental Insights

- Based on product, the vitamins & minerals segment dominated with a 28.5% share in 2023, reflecting strong consumer demand for preventive health supplements.

- Based on formulation, the tablets segment held the leading position due to convenience, dosage accuracy, and widespread availability.

- Based on distribution channel, the pharmacies segment accounted for the largest share, supported by pharmacist recommendations and in-store promotions.

Regional Insights

- North America and Europe are the leading markets, benefiting from strong regulatory frameworks and high consumer awareness.

- Asia-Pacific is expected to witness the fastest growth, driven by rising healthcare access, expanding retail chains, and increasing disposable incomes.

- Latin America and Middle East & Africa are experiencing steady adoption, supported by improving healthcare infrastructure and growing awareness of self-care products.

Competitive Landscape

The OTC drugs market is competitive, with global pharmaceutical leaders driving growth through product innovation, strategic partnerships, and regional expansion. Key companies include GlaxoSmithKline (GSK), Johnson & Johnson, Novartis, Bayer, Pfizer, Sanofi, Boehringer Ingelheim, Takeda, and PGT Healthcare.

Global Over-the-Counter Drugs Market Size

The global over-the-counter (OTC) drugs market was valued at USD 224.3 billion in 2024. The global market is predicted to be valued at USD 469.36 billion by 2033 from USD 243.48 billion in 2025, growing at a CAGR of 8.55% between 2025 to 2033.

The Over-the-Counter (OTC) Drugs are pharmaceutical products accessible to consumers without a physician’s prescription, those are designed to manage a wide spectrum of self-diagnosable and self-limiting conditions such as pain, allergies, gastrointestinal disturbances, and respiratory ailments. These medications operate within a regulatory framework that balances public safety with consumer autonomy, allowing individuals to address minor health concerns promptly while reducing strain on formal healthcare systems. The cultural acceptance of self-medication is a critical underpinning of the OTC sector; in Germany, for example, approximately 70% of adults engage in self-treatment for minor illnesses, relying on pharmacist guidance rather than physician consultation, as reported by the German Federal Institute for Drugs and Medical Devices. Similarly, in Japan, the Ministry of Health, Labour and Welfare permits the sale of over 1,800 OTC drug categories, reflecting a highly developed consumer healthcare culture. In India, the Pharmacy Council of India notes that over 55% of urban dwellers prefer purchasing OTC analgesics and antacids directly from pharmacies for immediate symptom relief. The rise of digital health platforms has further empowered consumers, enabling online symptom checkers and virtual consultations that support informed self-care decisions.

Over-the-Counter Drugs Market Trends

Rising Consumer Preference for Natural and Herbal OTC Products

A significant trend in the global over-the-counter (OTC) drugs market is the increasing consumer demand for natural and herbal remedies. Many individuals seek safer, more holistic treatments with fewer side effects. According to a 2024 survey, 62% of consumers reported a preference for plant-based or natural ingredients in their medications. This shift is driving pharmaceutical companies to invest in developing and marketing herbal OTC products for common ailments like digestive issues, colds, and sleep disorders. The global market for herbal medicines is expected to grow at a compound annual growth rate (CAGR) of 7.22% from 2025 to 2033 and be valued at USD 215.4 bn by 2024. This trend highlights consumer interest in wellness and prevention, leading to more OTC products labeled “natural” or “organic.”

Growth in Online Retail for OTC Drugs

The rise of e-commerce has significantly impacted the OTC drugs market. Online platforms provide consumers with the convenience of purchasing OTC products from home, often at competitive prices. Companies like Amazon, Walgreens, and CVS have capitalized on this trend by offering a wide selection of OTC products online. The COVID-19 pandemic accelerated this growth, as many people turned to online shopping for their healthcare needs. E-commerce also allows brands to reach rural or underserved populations, expanding their customer base.

Self-medication and Consumer Awareness

The increasing awareness of health conditions and a desire for self-care have driven the OTC market's expansion. Consumers are more inclined to manage minor ailments themselves to avoid healthcare costs and visits to medical facilities. According to a 2022 report, around 70% of consumers in the U.S. preferred using OTC drugs for managing mild conditions like pain, cold, or allergies. This trend is especially pronounced in developing countries, where healthcare access may be limited. The World Health Organization (WHO) estimates that 60% of global healthcare spending is out-of-pocket, prompting consumers to turn to more affordable OTC solutions. Companies are responding by expanding product lines and focusing on consumer education about self-medication.

MARKET DRIVERS

Rising Burden of Non-Communicable Diseases and Chronic Symptom Management

The escalating prevalence of non-communicable diseases (NCDs) and associated chronic symptoms that necessitate ongoing self-management is propelling the growth of the OTC drugs market. Conditions such as hypertension, diabetes, and arthritis often present with secondary symptoms like pain, inflammation, and gastrointestinal discomfort, which patients routinely address with OTC analgesics, antacids, and anti-inflammatory agents. This epidemiological shift has led to a sustained demand for accessible, immediate relief solutions outside clinical settings. For instance, the American College of Rheumatology reports that 58% of arthritis patients in the U.S. use OTC nonsteroidal anti-inflammatory drugs (NSAIDs) like ibuprofen on a weekly basis to manage joint pain, often in conjunction with prescribed therapies. Similarly, the International Diabetes Federation notes that diabetic neuropathy affects over 50% of long-term diabetes patients, prompting frequent use of OTC pain relievers. In the UK, Public Health England found that 43% of adults with chronic back pain rely on self-medication as their first-line response, citing convenience and reduced waiting times.

Expansion of Retail Pharmacy and E-Commerce Accessibility

The proliferation of retail pharmacy networks and the rapid ascent of e-commerce platforms are fuelling the growth of the OTC drugs market. Urbanization and the formalization of pharmacy chains have created dense distribution networks, particularly in emerging economies where traditional healthcare access remains limited. In China, the National Medical Products Administration recorded over 600,000 registered retail pharmacies in 2023, a 25% increase from 2018, enabling widespread availability of OTC products in both urban and peri-urban areas. Similarly, in Brazil, the Brazilian Institute of Geography and Statistics reported that 89% of households reside within five kilometers of a licensed pharmacy, facilitating immediate access to medications for common ailments. Parallel to physical expansion, digital commerce has revolutionized procurement; in India, the Federation of Indian Chambers of Commerce and Industry noted that online OTC sales grew by 68% in 2023, driven by platforms like PharmEasy and Netmeds offering home delivery and telepharmacy consultations.

MARKET RESTRAINTS

Misuse and Overuse of OTC Medications Leading to Public Health Risks

The widespread misuse and overuse of non-prescription medications, which pose serious public health consequences and undermine consumer trust is also restricting the growth of the OTC drugs market. Acetaminophen is a common analgesic and antipyretic, which is the leading cause of acute liver failure in the United States, responsible for approximately 56,000 emergency department visits annually, as documented by the Centers for Disease Control and Prevention. Similarly, excessive use of NSAIDs such as ibuprofen is linked to gastrointestinal bleeding and renal impairment, with the American Gastroenterological Association reporting that 15% of peptic ulcer cases are attributable to unsupervised NSAID consumption. In low- and middle-income countries, the problem is exacerbated by poor labeling, lack of pharmacist oversight, and polypharmacy practices; a 2023 study by the Indian Council of Medical Research found that 42% of urban consumers combined multiple OTC painkillers without understanding contraindications. These adverse outcomes not only endanger individual health but also prompt regulatory tightening, such as prescription-only reclassification of certain drugs, thereby constraining market expansion and reinforcing caution in consumer behavior.

Regulatory Fragmentation and Varying Classification Standards Across Jurisdictions

The substantial operational and strategic challenges due to the absence of harmonized global regulations governing drug classification, labeling, and sales protocols is hampering the growth of the OTC drugs market. A medication available over the counter in one country may require a prescription in another, creating confusion for consumers and logistical complexity for manufacturers. For example, pseudoephedrine, a decongestant sold without restriction in India, is kept behind pharmacy counters in the United States due to its potential use in illicit methamphetamine production, as regulated by the U.S. Drug Enforcement Administration. Similarly, low-dose oral contraceptives remain prescription-only in most of Asia and Africa, while available OTC in countries like Portugal and Austria, according to the World Health Organization’s Global Report on Access to Contraception. This regulatory asymmetry impedes multinational product launches and increases compliance costs for pharmaceutical firms. Moreover, inconsistent labeling standards—such as variations in dosage instructions, contraindications, and language—limit consumer comprehension, particularly in multilingual regions. The Pan American Health Organization found that only 54% of OTC labels in Latin America met minimum readability criteria, increasing the risk of medication errors.

MARKET OPPORTUNITIES

Integration of Digital Health Tools and AI-Driven Symptom Checkers

The integration of artificial intelligence and digital health technologies to guide safe and effective self-medication. AI-powered symptom checkers, mobile health apps, and virtual pharmacy assistants are increasingly being deployed to support consumer decision-making, reducing the risk of inappropriate drug selection. In the United Kingdom, the National Health Service’s NHS App includes a symptom assessment tool that directs users to appropriate OTC treatments for conditions like colds, allergies, and mild pain, as reported by NHS Digital. According to the European Health Innovation Alliance, 62% of consumers using digital symptom checkers demonstrated improved adherence to correct dosing and duration compared to those relying on self-assessment alone. Furthermore, smart packaging with QR codes linked to augmented reality instructions or dosage reminders enhances compliance and safety. Companies like Bayer and Reckitt have embedded digital guidance into OTC product ecosystems by offering real-time access to pharmacists via chatbots. These tools not only mitigate misuse but also build brand loyalty by positioning OTC brands as responsible health partners.

Expansion of OTC Switch Programs and Rx-to-CTC Transitions

The formal reclassification of prescription drugs to over-the-counter status commonly known as "OTC switch" or "Rx-to-OTC" transition is creating new opportunities for the growth of the OTC drugs market. Regulatory bodies are increasingly approving such switches after extensive post-marketing surveillance confirms long-term safety in unsupervised settings. In the United States, the FDA has facilitated over 100 OTC switches since the 1970s, including medications like omeprazole for acid reflux, loratadine for allergies, and, more recently, naloxone for opioid overdose reversal, as documented by the FDA’s Division of Drug Information. The approval of OTC naloxone in 2023 marked a pivotal public health milestone, expanding access to life-saving intervention. In Japan, the Ministry of Health, Labour and Welfare has accelerated its OTC switch program, converting 42 prescription drugs to non-prescription status between 2020 and 2023, including low-dose statins and antihistamines, according to the Pharmaceuticals and Medical Devices Agency. These transitions not only broaden consumer access but also alleviate pressure on primary care systems.

MARKET CHALLENGES

Counterfeit and Substandard OTC Products in Unregulated Markets

The proliferation of counterfeit and substandard medications in some regions with less regulatory enforcement and informal distribution networks is to pose challenging factor for the growth of the OTC drugs market. These illicit products often contain incorrect dosages, inactive ingredients, or harmful contaminants, posing severe health risks to consumers. According to the World Health Organization, 1 in 10 medical products in low- and middle-income countries is substandard or falsified, with OTC analgesics, antipyretics, and cough syrups among the most commonly affected categories. In Nigeria, the National Agency for Food and Drug Administration and Control seized over 1.2 million counterfeit drug units in 2023, many of which were falsely labeled OTC brands. Similarly, in Southeast Asia, the ASEAN Pharmaceutical Alliance reported that 18% of OTC medications sampled in border markets failed quality tests for potency and sterility. The rise of unregulated e-commerce platforms has exacerbated the issue; Interpol’s Operation Pangea 2023 uncovered 1.4 million fake OTC pills sold online across 80 countries, including adulterated versions of paracetamol and ibuprofen. These incidents erode consumer confidence, damage brand equity, and complicate legitimate market growth.

Consumer Misinformation and Influence of Social Media on Self-Medication Behavior

The spread of health misinformation through social media and digital platforms, which significantly influences consumer self-medication choices, that often leading to inappropriate or dangerous practices is hampering the growth of the OTC drugs market. Platforms like TikTok, Instagram, and YouTube host viral content promoting unverified remedies, off-label drug use, and anecdotal treatment regimens, bypassing traditional medical gatekeeping. A 2023 study by the Lancet Digital Health found that 68% of trending videos related to cold and flu treatment on TikTok recommended OTC medications in ways inconsistent with labeling or clinical guidelines, including excessive dosing and unsafe combinations. This digital-driven behavior undermines public health messaging and complicates regulatory oversight. Pharmacists and health authorities are increasingly required to counter misinformation through digital literacy campaigns and real-time monitoring

SEGMENTAL ANALYSIS

By Product Insights

The analgesics segment was accounted in holding 28.1% of the global over-the-counter (OTC) drugs market share in 2024 owing to the universal prevalence of pain-related conditions and the reliance on immediate, accessible relief solutions across all age groups and geographies.

Driving Factor 1: High Prevalence of Musculoskeletal and Chronic Pain Conditions

A primary force behind the dominance of analgesics is the widespread incidence of musculoskeletal disorders and chronic pain, which affect millions globally and necessitate frequent self-treatment. According to the World Health Organization, musculoskeletal conditions are the second leading cause of disability worldwide, impacting over 1.7 billion people. The aging population further amplifies demand; in Japan, where 29% of the population is aged 65 or older, the Ministry of Health, Labour and Welfare recorded that OTC analgesics were the most frequently purchased drug category in 2023. The episodic yet recurrent nature of headaches, menstrual pain, and post-exertional soreness also ensures sustained consumer demand.

The vitamins and minerals segment is growing lucratively with an expected CAGR of 9.7% from 2025 to 2033. The global emphasis on immune health, intensified by the post-pandemic health consciousness, has significantly increased demand for vitamin supplements, particularly vitamin C, vitamin D, and zinc. According to the National Institutes of Health, vitamin D deficiency affects nearly 42% of the U.S. population, prompting widespread supplementation to support immune function and bone health. A 2023 survey by the Council for Responsible Nutrition found that 86% of American supplement users cited immune support as their primary reason for consumption. In the UK, Public Health England reinforced national guidelines recommending vitamin D supplementation during autumn and winter, driving pharmacy sales. This preventive mindset extends beyond illness avoidance to general vitality, with consumers integrating vitamins into daily routines akin to brushing teeth or exercising, thereby institutionalizing their use.

By Formulation Insights

The tablet formulation dominated the OTC drugs market by capturing 46.3% of share in 2024. Tablets are favored for their compactness, ease of storage, and straightforward administration, making them ideal for daily use and travel. According to the U.S. Pharmacopeia, over 70% of OTC medication users prefer solid dosage forms due to their perceived reliability and mess-free consumption. In urban environments where time efficiency is paramount, tablets offer a quick solution without the need for measuring or refrigeration. In India, the Indian Pharmaceutical Association reported that 82% of OTC buyers in metropolitan areas select tablets over liquids for pain and cold relief, citing convenience and longer shelf life. Similarly, in Brazil, the Brazilian Society of Pharmacists noted that tablet sales outpace liquids by a 3:1 ratio in self-medication scenarios.

The spray formulation segment is likely to grow with an expected CAGR of 12.3% from 2025 to 2033. Spray formulations offer immediate localized action, making them ideal for conditions requiring fast intervention, such as nasal congestion, sore throat, and motion sickness. Nasal sprays like oxymetazoline provide congestion relief within minutes, bypassing the gastrointestinal tract and achieving faster systemic absorption. According to the American Academy of Allergy, Asthma & Immunology, 68% of allergy sufferers prefer nasal sprays over oral antihistamines due to quicker symptom control.

By Distribution Channel Insights

The pharmacies segment held 58.2% of the OTC drugs market share in 2024. Pharmacies remain the preferred destination for OTC purchases due to the availability of trained pharmacists who provide personalized recommendations and safety counseling. According to the International Pharmaceutical Federation, 64% of consumers consult pharmacists before buying OTC medications, particularly for complex conditions like allergies, gastrointestinal issues, or drug interactions. In Canada, the Canadian Pharmacists Association reported that 78% of patients trust pharmacists as their first point of contact for minor ailments. In the UK, the Royal Pharmaceutical Society emphasized that community pharmacists conduct over 4 million medicine use reviews annually, reinforcing their advisory role. This professional oversight mitigates misuse and enhances consumer confidence, especially for first-time users or elderly patients managing multiple medications.

The "Others" segment is growing lucratively with an expected CAGR of 15.6% from 2025 to 2033.

The rise of e-pharmacies has revolutionized OTC access by offering convenience, price transparency, and doorstep delivery. In India, the Federation of Indian Chambers of Commerce and Industry reported that online OTC sales surged by 72% in 2023, led by platforms like 1mg, PharmEasy, and Netmeds. These platforms integrate AI-driven symptom checkers, teleconsultations, and subscription models for recurring purchases, enhancing user experience. In China, Alibaba Health and JD Health recorded over 300 million OTC transactions in 2023, as per the China E-Commerce Research Center. The pandemic accelerated this shift, with the U.S. National Center for Health Statistics noting that 41% of Americans purchased OTC drugs online in 2023, up from 18% in 2019.

REGIONAL ANALYSIS

North America Over-the-Counter Drugs Market Insights

North America was the top performer of the OTC drugs market by capturing 39.3% of share in 2024. The United States is leading with fragmented healthcare system that incentivizes individuals to manage minor ailments independently. According to the National Center for Health Statistics, 81% of American adults use OTC medications as their first response to common conditions like headaches, colds, and allergies. The presence of major pharmaceutical players such as Pfizer, Johnson & Johnson, and Bayer ensures continuous innovation and brand trust. Additionally, the FDA’s OTC Monograph system streamlines product approval, fostering market dynamism. Retail pharmacy chains like CVS and Walgreens, combined with the rapid expansion of e-pharmacies, ensure widespread accessibility.

Europe Over-the-Counter Drugs Market Insights

Europe OTC drugs market held 31.2% of share in 2024 owing to the diverse regulatory frameworks, high public trust in pharmacists, and a growing emphasis on self-care to alleviate pressure on public health systems. Germany led the market growth with self-medication accounting for nearly 30% of total pharmaceutical expenditure, according to the German Federal Ministry of Health. The UK’s National Health Service actively promotes pharmacy-based care for minor illnesses, reducing GP consultations. In France, the government supports OTC access through the "Parcours de Soins" initiative, which incentivizes non-prescription treatment for common conditions. Countries like Sweden and the Netherlands exhibit high OTC penetration due to advanced digital health integration and consumer education.

Asia-Pacific Over-the-Counter Drugs Market Insights

Asia-Pacific OTC drugs market is likely to grow with significant CAGR in the next coming years with rising disposable incomes, urbanization, and increasing health awareness, particularly in middle-class populations. Japan stands out as a mature market, where OTC sales are highly regulated and culturally accepted, with the Ministry of Health, Labour and Welfare overseeing over 1,800 approved non-prescription drugs. China’s market is expanding rapidly, driven by e-commerce giants like Alibaba Health and JD Pharmacy, which have made OTC products accessible to hundreds of millions. In India, rising chronic disease prevalence and pharmacy modernization are boosting demand, with the Indian Pharmaceutical Alliance projecting a doubling of OTC sales by 2030. However, challenges remain in rural areas, where counterfeit products and low health literacy persist.

Latin America Over-the-Counter Drugs Market Insights

Latin America OTC drugs market is likely to grow steadily in the next coming years. Brazil and Mexico are the largest markets, with Brazil’s OTC sector growing at 8% annually due to expanding pharmacy networks and rising middle-class affluence, according to the Brazilian Health Regulatory Agency. In Mexico, over 60% of minor health issues are treated with self-medication, supported by a dense network of independent pharmacies. However, regulatory inconsistencies and widespread sale of unlicensed products in informal markets pose challenges. Countries like Chile and Colombia are advancing formal OTC frameworks, with pharmacist-led counseling gaining traction. Digital health platforms are beginning to penetrate urban centers, offering teleconsultations and home delivery.

Middle East and Africa Over-the-Counter Drugs Market Insights

The Middle East and Africa OTC drugs market growth is likely to grow with steady apace throughout the forecast period. The UAE and Saudi Arabia lead the region, with Dubai and Riyadh establishing modern pharmacy chains and e-health initiatives under national health transformation programs. In Saudi Arabia, Vision 2030 includes plans to expand community pharmacy services and promote self-care to reduce hospital overload, as per the Saudi Ministry of Health. South Africa remains the African leader, with regulated OTC sales through chains like Clicks and Dis-Chem, serving a relatively affluent urban population. However, in Sub-Saharan Africa, access is limited by poor infrastructure, low regulatory enforcement, and high counterfeit prevalence, as reported by the African Medicines Regulatory Harmonization Initiative.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

GlaxoSmithKline, Johnson and Johnson, Novartis, Bayer, Pfizer, GSK, Boehringer Ingelheim, Sanofi, Takeda, and PGT Healthcare are the top companies contributing to the over-the-counter (OTC) drugs market. GlaxoSmithKline, Johnson and Johnson, Novartis, and Sanofi possess the maximum market share. The extension of OTC services for drugs dealing with chronic diseases like diabetes and hypertension is a new trend.

The competitive landscape of the over-the-counter drugs market is defined by a dynamic interplay of brand equity, innovation, and evolving consumer expectations. Unlike prescription pharmaceuticals, where efficacy and regulatory approval dominate, OTC competition hinges on accessibility, trust, and perceived value in everyday health management. Established multinational corporations face increasing pressure from private-label brands, regional manufacturers, and digitally native startups that offer lower prices or niche formulations tailored to specific health trends. The battleground has shifted from mere product availability to holistic consumer experience—encompassing packaging design, ease of use, digital support, and ethical positioning. Differentiation is achieved not only through formulation but also through branding that resonates emotionally, such as positioning a product as part of a wellness ritual or a family care essential. Regulatory scrutiny remains a constant challenge, requiring companies to balance aggressive marketing with compliance and safety. At the same time, the rise of e-commerce and telepharmacy has disrupted traditional retail hierarchies, enabling smaller players to gain visibility and forcing incumbents to adapt their distribution and engagement models.

Top Players in the Over-the-Counter Drugs Market

Johnson & Johnson (United States)

Johnson & Johnson has long been a cornerstone of the global OTC drugs market, leveraging its legacy in healthcare innovation to build a diverse portfolio of trusted consumer health brands. Through products like Tylenol, Benadryl, and Listerine, the company has shaped public perception of safe, effective self-care solutions across pain relief, allergy, and oral care categories. Its contribution extends beyond product development to setting industry benchmarks in labeling clarity, dosage safety, and public education campaigns. The company’s emphasis on research-driven formulations and responsible marketing has reinforced consumer confidence by making its brands synonymous with reliability in household medicine cabinets worldwide.

GlaxoSmithKline (United Kingdom)

GlaxoSmithKline has played a pivotal role in advancing the accessibility and efficacy of non-prescription therapies, particularly in respiratory and immune health. With flagship brands such as Advil, Sensodyne, and Panadol, GSK has positioned itself as a leader in science-backed self-medication, consistently investing in clinical validation and formulation refinement. The company has been instrumental in advocating for regulatory frameworks that support the safe transition of prescription drugs to OTC status, expanding consumer access to proven treatments. Its global outreach includes partnerships with public health entities to promote responsible self-care and combat antimicrobial misuse. GSK’s integration of sustainability into product development and supply chain operations has further strengthened its reputation as a forward-thinking, ethically driven player in the consumer health space.

Reckitt Benckiser (United Kingdom)

Reckitt Benckiser has distinguished itself through its strategic focus on hygiene-integrated health solutions and consumer behavior insights. With iconic brands like Dettol, Mucinex, and Gaviscon, the company has redefined OTC care by linking symptom relief with preventive wellness and home protection. Its innovation strategy emphasizes user experience, from easy-to-use packaging to fast-acting delivery systems, enhancing adherence and satisfaction. Reckitt has been a pioneer in digital engagement, utilizing data analytics to tailor product offerings and educational content to regional health needs. Its global influence is further amplified through public health initiatives that promote hand hygiene, respiratory care, and safe self-medication practices.

Top Strategies Used by Key Market Participants

One of the most impactful strategies employed by leading OTC drug manufacturers is brand extension through product line diversification, where established brands are adapted into new formulations, delivery mechanisms, or complementary categories. This approach leverages existing consumer trust to enter adjacent markets such as transitioning a pain relief brand into sleep aids or digestive health thereby increasing shelf presence and cross-category loyalty. Companies use flavor variants, dosage forms, and targeted messaging to appeal to specific demographics, including children, seniors, or active adults.

Another key strategy is the enhancement of consumer trust through transparency and scientific validation. Leading players invest heavily in clinical studies, third-party endorsements, and clear communication of active ingredients, dosing guidelines, and safety profiles. This includes plain-language labeling, digital QR codes linking to detailed product information, and collaboration with healthcare professionals to endorse responsible use, reinforcing credibility in an environment of rising health consciousness.

RECENT MARKET DEVELOPMENTS

- In March 2024, Johnson & Johnson launched a global digital health initiative integrating Tylenol with a mobile app that provides dosage tracking, symptom logging, and pharmacist chat support, enhancing user engagement and safety.

- In August 2023, GlaxoSmithKline partnered with a leading European telehealth platform to offer virtual consultations for users of its respiratory OTC products by enabling real-time guidance on proper usage and treatment duration.

- In November 2024, Reckitt Benckiser introduced a sustainable packaging line for Mucinex and Gaviscon, utilizing recyclable materials and reduced plastic content, which is aligning with growing consumer demand for environmentally responsible healthcare products.

- In January 2024, Bayer expanded its OTC portfolio by acquiring a digital wellness startup specializing in AI-driven vitamin and supplement recommendations by strengthening its position in the preventive health segment.

- In June 2023, Pfizer Consumer Healthcare introduced a multilingual telepharmacy service in Southeast Asia to support OTC product education and safe self-medication practices, which is increasing accessibility in underserved urban and rural communities.

GLOBAL OVER-THE-COUNTER (OTC) DRUGS MARKET REPORT SCOPE

| Metric | Value |

|---|---|

| Base Year | 2024 |

| Market Size Available | 2024 to 2033 |

| Forecast Period | 2025 to 2033 |

| Quantitative Units | Market Size in USD Billion and CAGR from 2025 to 2033 |

| Various Analyses Included | Global, Regional & Country-Level Analysis; Segment-Level Analysis; DROC; PESTLE; Porter's Five Forces; Competitive Landscape; Investment Opportunities |

| Segments Covered | By Product Type, Formulation Type, Distribution Channels, and Region |

| Regions Analyzed | North America, Europe, APAC, Latin America, Middle East & Africa |

| Countries Covered | U.S, Canada, Mexico, UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Brazil, Argentina, Chile, KSA, UAE, Israel, rest of GCC countries, South Africa, Ethiopia, Kenya, Egypt, Sudan and Other Countries |

| Key Market Players | Johnson and Johnson, Novartis, Bayer, Pfizer, Boehringer Ingelheim, Sanofi, Takeda, and PGT Healthcare |

| Report Format | PDF, Excel, PPT, BI |

| Customization | Report customization as per your requirements with respect to countries, region and segmentation. |

MARKET SEGMENTATION

This research report on the global over-the-counter (OTC) drugs market is segmented and sub-segmented based on the product type, formulation type, distribution channels, and region.

By Product Type

- Analgesics

- Cough, Cold, and Flu Products

- Vitamins and Minerals

- Dermatological Products

- Gastrointestinal Products

- Ophthalmic Products

- Sleep Aid Products

- Weight Loss/Diet Products

- Others

By Formulation Type

- Tablets

- Liquids

- Ointments

- Sprays

By Distribution Channels

- Pharmacies

- Supermarkets/Hypermarkets

- Convenience stores

- Others (Online Drug Stores)

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

What is the current size of the Over the Counter (OTC) Drugs Market?

The global over-the-counter drugs market was valued at USD 206.7 billion in 2023.

Which regions dominate the global OTC drugs market?

North America and Europe lead due to established healthcare systems and regulatory support. Asia-Pacific is showing the fastest growth, fueled by population size, urbanization, and e-commerce expansion.

What are the main drivers of the OTC drugs market?

Key drivers include rising healthcare costs, greater emphasis on preventive health, growing elderly population, and regulatory support for Rx-to-OTC switches in multiple countries.

What are the key segments within the OTC drugs market?

The market is segmented into therapeutic categories such as analgesics, cold and flu remedies, digestive health, dermatology, and nutritional supplements, distributed through pharmacies, supermarkets, and online retailers.

Who are the key players in the OTC drugs market?

Major players include Johnson & Johnson, GSK Consumer Healthcare, Bayer AG, Pfizer, Sanofi, Reckitt Benckiser, and Takeda, along with regional pharmaceutical brands expanding their OTC portfolios.

What is the expected growth rate of the OTC drugs market through 2033?

The market is projected to grow at a CAGR of 8.55% by 2033, supported by increasing consumer confidence in self-medication and digital health literacy.

How is digital transformation influencing the OTC market?

Digital platforms are driving online pharmacy growth, targeted health product marketing, and direct-to-consumer sales, creating new opportunities for brands and retailers alike.

What challenges does the OTC drugs market face?

Challenges include risk of product misuse, tightening regulations, price competition, and difficulty in differentiating brands in crowded categories.

How are Rx-to-OTC switches affecting market growth?

The switch of certain prescription drugs to OTC status has expanded product availability, increased consumer trust, and opened new revenue streams for pharmaceutical manufacturers.

What trends will shape the future of the OTC drugs market?

Key trends include personalized OTC product recommendations, clean label and natural ingredients, sustainable packaging, and integration with telepharmacy and self-care apps.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com