Global Plastic Bags Market Size, Share, Trends, and Growth Analysis Report, Segmented By Material, Product, Application, & Region (North America, Europe, Latin America, Asia Pacific, Middle East & Africa), Industry Forecast From 2026 to 2034

Global Plastic Bags Market Summary

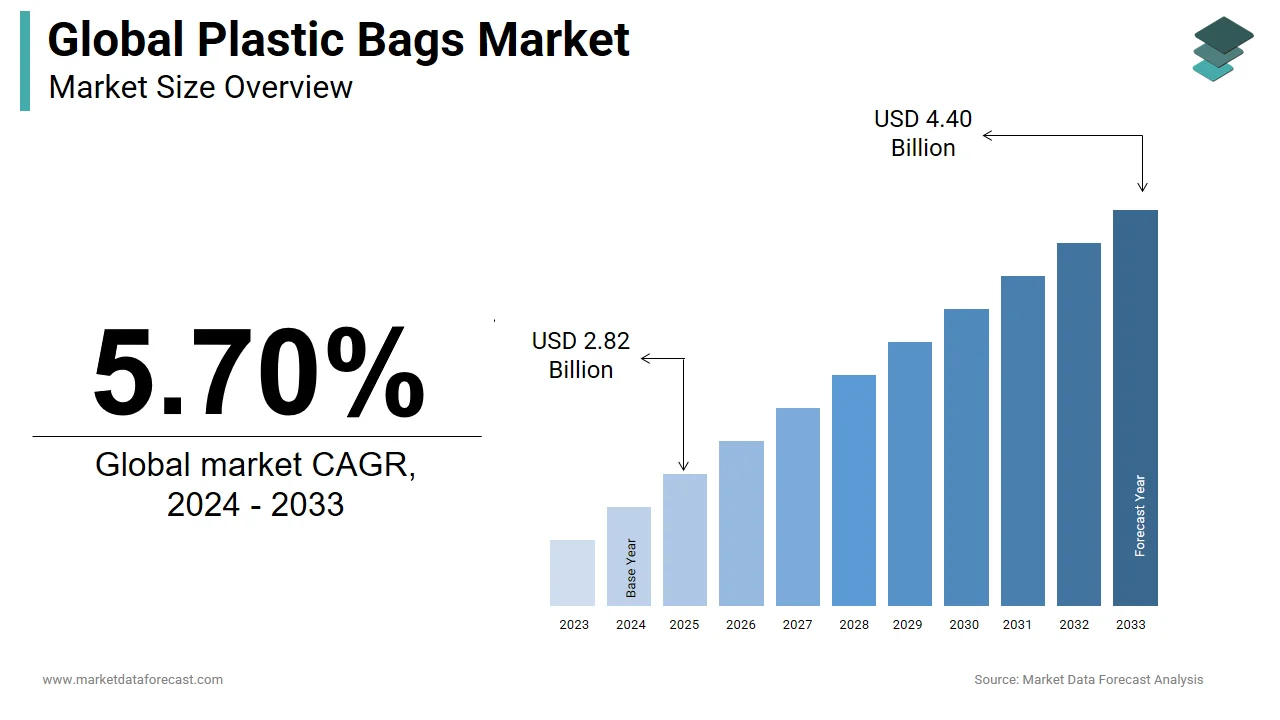

The global plastic bags market reached USD 2.82 billion in 2025 and is projected to grow to USD 2.98 billion in 2026, and is anticipated to reach USD 4.64 billion by 2034, expanding at a CAGR of 5.70% from 2026 to 2034. The growth of the global plastic bags market is attributed to their wide-scale usage in packaging, retail, and waste management, coupled with low production costs, durability, and convenience of handling. However, increasing environmental concerns and regulatory restrictions are also driving innovations toward sustainable and recyclable alternatives.

Key Market Trends

- Rising demand for eco-friendly and biodegradable plastic bags.

- Growth in retail, e-commerce, and food packaging sectors.

- Increasing global focus on plastic waste management and recycling initiatives.

- Innovation in lightweight, durable, and cost-efficient designs.

- Government initiatives encouraging a shift towards sustainable packaging.

Segmental Insights

- Based on material, the non-biodegradable plastic bags segment dominated the market by capturing a significant share in 2024.

- Based on product, the trash bags segment held the leading share of 62.1% of the plastic bags market in 2024.

Regional Insights

- Asia-Pacific was the top performer in the global plastic bags market, accounting for 46.9% of the share in 2024, driven by rising consumption in retail, household, and industrial applications.

- North America is witnessing steady growth due to waste management and retail sector demand.

- Europe is influenced by stricter sustainability regulations, pushing adoption of eco-friendly bags.

- Latin America and the Middle East & Africa are emerging regions with gradual growth due to rising urbanization and retail expansion.

Competitive Landscape

Some of the leading players in the global plastic bags market include Berry Global Inc., Mondi, Amcor plc, Inteplast Group, Smurfit Kappa, Novolex, Bischof+Klein SE & Co. KG, Alfa Poly Plast, Goglio SpA, ARIHANT PACKAGING, ProAmpac, Schur, Starlinger & Co Gesellschaft m.b.H., Packman Packaging Private Limited, Knack Packaging Pvt. Ltd., The Buckeye Bag Company, Kanpur Plastipack Limited, Fujian Yangqiang Plastic Products Co., Ltd., VAVA PACK CO., LTD., and Leadpacks (Xiamen) Environmental Protection Packing Co., Ltd. These companies are focusing on product innovation, recyclable solutions, and strategic collaborations to enhance their global footprint.

Global Plastic Bags Market Size

The global plastic bags market reached USD 2.82 billion in 2025, is expected to grow to USD 2.98 billion in 2026, and is anticipated to touch USD 4.64 billion by 2034, at a CAGR of 5.70% from 2026 to 2034.

Plastic bags are lightweight and single-use carryout bags made from low-density polyethylene (LDPE) and high-density polyethylene (HDPE). It is widely used in retail, grocery, and e-commerce packaging. These bags remain deeply embedded in global consumer logistics due to their durability, moisture resistance, and cost efficiency. According to the United Nations Environment Programme (UNEP), approximately 5 trillion plastic bags are consumed annually worldwide, with an average usage time of less than 20 minutes before disposal. Over 70% of these end up in landfills, oceans, or informal waste streams, where they persist for centuries, as reported by the Global Partnership on Marine Litter.

MARKET DRIVERS

Strong Demand for Plastic Bags in Emerging Economies with Limited Alternatives

The persistent demand in emerging economies with underdeveloped packaging alternatives is boosting the growth of the plastic bags market. In countries across South Asia, Sub-Saharan Africa, and Southeast Asia, plastic bags remain the dominant form of retail packaging due to the absence of affordable, scalable alternatives. In India, significant tons of plastic carry bags are consumed annually, primarily in unorganized retail markets, as per sa tudy. Plastic bags remain a low-cost and hygienic solution for food and dry goods transport since a percentage of grocery transactions occur in small kirana stores that lack access to compostable or reusable substitutes. In Nigeria, where formal waste management covers only a portion of urban areas, plastic bags are extensively used for secondary purposes such as waste lining and water carriage, according to research. Their resilience in humid and tropical conditions further enhances utility in regions prone to monsoon rains and high humidity, where paper or biodegradable options degrade rapidly.

Growth of E-Commerce and Last-Mile Delivery Boosting Plastic Bag Demand

The integration into e-commerce and last-mile delivery logistics is surging the growth rate of the plastic bags market. The global e-commerce sector generated a substantial amount in sales, with a large number of packages shipped annually, as per a study. A significant portion of these shipments relies on polyethylene-based mailing bags, lightweight, puncture-resistant, and moisture-proof, for final delivery. In China, Alibaba’s Cainiao Network processed billions of parcels, a portion of which were packed in plastic shipping pouches, according to research. These bags weigh less than paper alternatives, reducing shipping costs and carbon emissions per unit, as per a study. In Southeast Asia, where e-commerce is growing annually, plastic courier bags dominate last-mile delivery in countries like Indonesia and the Philippines due to their durability in tropical climates.

MARKET RESTRAINTS

Regulatory Bans and Levies on Single-Use Plastic Bags

The strict regulatory bans and levies on single-use plastics is hindering the growth of the plastic bags market. As of mid-2024, reports indicated that around 91 countries and territories had implemented full or partial bans on plastic bags, with more having taxes or other restrictions. In Canada, the federal government classified checkout bags as toxic substances under the Canadian Environmental Protection Act in 2022. Kenya, often cited as having the world’s strictest plastic law, imposes fines or years in prison for manufacturing or using plastic bags, as per research. These legal frameworks have reduced plastic bag usage in regulated markets, which severely constrains market expansion in high-income and environmentally progressive regions.

Low Recycling Potential and Infrastructure Gaps Limiting Market Growth

The low recycling potential is limiting the expansion of the plastic bags market. Only a portion of plastic bags are recycled globally, with the majority either incinerated, landfilled, or discarded into the environment, according to a study. Their thin structure and frequent contamination with food residue make them unsuitable for conventional mechanical recycling processes. In the U.S., plastic bags account for a percentage of recyclable film waste that gets rejected at material recovery facilities (MRFs), as per research. When mixed with paper or fiber streams, they cause jamming in sorting machinery, increasing operational costs. In India, a smaller share of plastic waste is effectively recycled, with carry bags contributing significantly to clogged drainage systems and urban flooding. The lack of dedicated collection infrastructure and economically viable recycling technologies limits circularity.

MARKET OPPORTUNITIES

Development of Advanced Recyclable and Mono-Material Plastic Bags

The development of advanced recyclable and mono-materials is fuelling new opportunities for the growth of the plastic bags market. Polyethylene-based bags designed for full recyclability are emerging as a transitional solution in markets resistant to complete phaseouts. Companies like Dow and SABIC have introduced metallocene-catalyzed LLDPE films that maintain strength at reduced thickness and are compatible with existing recycling streams. In addition, Walmart launched a new private-label produce bag made from a recyclable mono-PE structure, which eliminates polypropylene lamination that previously hindered recycling.

Growth of Chemical Recycling Creating a Circular Economy for Plastic Bags

The chemical recycling technologies, such as pyrolysis and depolymerization, are gaining traction over the growth of the plastic bags market. The global chemical recycling market for plastics is projected to grow in the coming years. In Japan, the government has classified chemical recycling as a key national strategy, supporting projects like Mitsubishi Chemical’s pilot plant that converts tons of plastic waste annually into naphtha feedstock. According to a study, scaling chemical recycling could divert millions of tons of plastic film from landfills. This technological shift enables producers to reintegrate plastic bag waste into the value chain, which transforms a liability into a resource and opens new business models in closed-loop packaging.

MARKET CHALLENGES

Negative Public Perception and Policy Backlash Against Plastic Bags

Emblematic of broader plastic pollution, which is frequently featured in media coverage of marine debris and landfill overflow that hampers the growth of plastic bags market. A portion of respondents associate plastic bags with environmental harm, with a share actively avoiding retailers that provide them. Images of plastic-choked waterways in Southeast Asia and Africa have influenced international policy and corporate sustainability commitments. In response, major brands have pledged to eliminate non-recyclable plastic bags as part of their ESG disclosures. The backlash extends to investor sentiment, funds managing a notable amount in assets support the UN Plastic Treaty negotiations. This reputational burden forces manufacturers and retailers to innovate rapidly or risk exclusion from supply chains, which makes public perception an important operational and strategic challenge.

Volatile Polyethylene Prices and Hydrocarbon Dependency Impacting Margins

The production of polyethylene is directly tied to naphtha and ethane derived from crude oil and natural gas, which is a barrier impacting the plastic bags market growth. In 2022, the price of LDPE resin surged following geopolitical disruptions in energy supply, as per study by a leading petrochemical market intelligence firm. Such volatility affects profit margins for bag manufacturers, particularly small and medium enterprises in developing countries that lack hedging mechanisms. In Turkey, where a percentage of polyethylene is imported, resin price fluctuations led to a rise in plastic bag production costs, according to the study. Apart from these, carbon pricing mechanisms like the EU’s Carbon Border Adjustment Mechanism (CBAM) may impose indirect costs on fossil-based plastics, further squeezing margins. This dependency on hydrocarbon markets introduces financial instability, complicating long-term planning and investment in a sector already under regulatory and environmental burden

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Material, Product, Application, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Market Leaders Profiled | Berry Global Inc., Mondi, Amcor plc, Inteplast Group, Smurfit Kappa, Novolex, Bischof+Klein SE & Co. KG, Alfa Poly Plast, Goglio SpA, ARIHANT PACKAGING, ProAmpac, Schur, Starlinger & Co Gesellschaft m.b.H., Packman Packaging Private Limited, Knack Packaging Pvt. Ltd., The Buckeye Bag Company, Kanpur Plastipack Limited, Fujian Yangqiang Plastic Products Co., Ltd., VAVA PACK CO., LTD., Leadpacks (Xiamen) Environmental Protection Packing Co., Ltd.. |

SEGMENTAL ANALYSIS

By Material Insights

The non-biodegradable plastic bags segment remained prominent in the plastic bags market by capturing a significant share of the global market in 2025. Cost efficiency, established manufacturing infrastructure, and functional superiority in harsh environmental conditions are primarily driving the growth of the non-biodegradable plastic bags segment. These bags, primarily made from high-density polyethylene (HDPE) and low-density polyethylene (LDPE), remain the backbone of retail and industrial packaging due to their durability and low production cost. This cost advantage is amplified by the existence of many extrusion lines globally dedicated to polyethylene film production. In countries like India, Indonesia, and Nigeria, where informal retail dominates, low-cost bags are essential for daily commerce.

The biodegradable plastic bags segment is growing lucratively with an expected CAGR of 10.7% from 2023 to 2030, owing to regulatory mandates and corporate sustainability commitments. In Italy, law requires households to use certified compostable bags for food waste, driving demand for polylactic acid (PLA) and PBAT-based films. These policies are linked to circular economy goals. Municipal composting infrastructure is expanding in North America and Asia, creating structural demand for certified biodegradable films. Many multinational retailers have pledged to phase out non-recyclable plastic bags. Similarly, in 2022, Lidl GB (Great Britain) introduced a switch to compostable produce bags for fruits and vegetables.

By Product Insights

The Trash bags segment held the leading share of 62.1% of the plastic bags market in 2024. Universal household and commercial usage are largely contributing to the dominance of the trash bags segment in the global market. The average household in the U.S. uses many trash bags annually, with larger families consuming more units, according to a study. This high turnover creates consistent demand, independent of economic cycles. The standardization of bin sizes in municipalities has led to the mass production of size-specific bags, enhancing consumer convenience. Brands like Glad, Simplehuman, and Jumbo dominate with scented, leak-proof variants, strengthening habitual consumption. The integration of trash bags into daily sanitation routines ensures sustained demand across income levels and geographies.

The rubble sacks segment is predicted to witness the highest CAGR of 9.4% from 2025 to 2033 due to the construction sector expansion. The global construction waste is projected to increase, with a portion of demolition debris initially contained in heavy-duty plastic rubble sacks, according to research. These sacks, typically made from woven polypropylene with UV stabilization, can hold notable kg and resist tearing during lifting and transport. Green building certifications like LEED and BREEAM require documented waste segregation and recycling, driving the use of durable, reusable rubble sacks on construction sites. Therefore, Rubble sacks are becoming essential tools in sustainable construction logistics as the global green building area is expected to surge in the coming years.

REGIONAL ANALYSIS

Asia-Pacific Plastic Bags Market Insights

Asia-Pacific was the top performer in the plastic bags market in 2024 and accounted for 46.9% of the market share in 2024. Population density and industrial activity are the factors driving the domination of the Asia Pacific in the global market. China and India are the largest producers and consumers, with China manufacturing significant tons of plastic bags annually, as per a study. Enforcement remains uneven by allowing continued production in rural and export-oriented zones despite national restrictions. India’s informal retail sector, comprising millions of small shops, relies heavily on low-cost polyethylene bags, with annual consumption exceeding in tons, according to research. Southeast Asian nations like Vietnam and Indonesia are emerging as manufacturing hubs for export-grade trash and shopping bags, benefiting from low labor costs and flexible regulations. However, rising public burden has prompted cities like Bangkok and Manila to introduce phased bans, which creates a dual market of compliance and informal use.

North America Plastic Bags Market Insights

North America region held 20.5% of the share in 2024. The U.S. accounts for the majority of regional consumption. The U.S. generates billions of plastic shopping bags annually, but only a portion are recycled, according to research. State-level regulations are fragmenting the market—California, New York, and Oregon have implemented full bans, while Texas and Florida resist restrictions. This divergence has led to a rise in "bag neutrality" policies, where retailers charge fees to discourage use. In Canada, the federal ban on single-use plastics, which is eliminating an estimated billion bags annually, as reported by Environment and Climate Change Canada.

Europe Plastic Bags Market Insights

Europe region is likely to grow with strong regulatory frameworks. The EU's Plastic Bags Directive (Directive (EU) 2015/720) has required Member States to reduce lightweight plastic bag consumption since 2015. Countries like Ireland and Denmark achieved significant reductions through taxation measures introduced long before this directive. Germany recycles a portion of its plastic packaging, supported by a dual system (DSD) that incentivizes reusable and compostable formats.

Middle East & Africa Plastic Bags Market Insights

Middle East & Africa is anticipated to achieve potential growth in the plastic bags market, with demand shaped by urbanization and inconsistent enforcement. Kenya implemented one of the world’s strictest plastic bag bans in 2017, reducing usage, according to research. However, illegal production persists, with a portion of bags still circulating in Nairobi markets, as per the study. In contrast, Saudi Arabia and the UAE have no nationwide bans, allowing continued use in retail and construction. In rural Africa, plastic bags are repurposed for water transport, grain storage, and roofing, extending their utility.

Latin America Plastic Bags Market Insights

Latin America is predicted to expand in the plastic bags market, with Brazil and Mexico as primary consumers. Brazil uses billions of plastic bags annually, but only a portion are recycled, according to the study. São Paulo and Rio de Janeiro have introduced levies, reducing consumption in urban centers, as per research. Mexico City banned single-use plastics in 2021, but informal markets continue distribute. However, economic hardship limits access to reusable alternatives, keeping plastic bags prevalent in low-income communities.

COMPETITIVE LANDSCAPE

The plastic bags market is characterized by intense regional fragmentation and divergent regulatory landscapes, creating a complex competitive environment. Multinational producers compete with thousands of regional and local converters, particularly in Asia and Africa, where price sensitivity and informal distribution dominate. While global firms leverage R&D, sustainability certifications, and vertical integration, smaller players thrive on agility and low overhead. Innovation in recyclable materials, digital traceability, and circular partnerships is redefining prominence. However, in markets with weak enforcement, non-compliant production persists, weakening formal sector efforts.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global plastic bags market include

- Berry Global Inc.

- Mondi

- Amcor plc

- Inteplast Group

- Smurfit Kappa

- Novolex

- Bischof+Klein SE & Co. KG

- Alfa Poly Plast

- Goglio SpA

- ARIHANT PACKAGING

- ProAmpac

- Schur

- Starlinger & Co Gesellschaft m.b.H.

- Packman Packaging Private Limited

- Knack Packaging Pvt. Ltd.

- The Buckeye Bag Company

- Kanpur Plastipack Limited

- Fujian Yangqiang Plastic Products Co., Ltd.

- VAVA PACK CO., LTD.

- Leadpacks (Xiamen) Environmental Protection Packing Co., Ltd.

Top Players in the Plastic Bags Market

- Novolex operates extensively across the Asia-Pacific region through strategic partnerships and localized manufacturing units, supplying a wide range of plastic bags for retail, food service, and waste management. The company has strengthened its presence by introducing high-strength, thin-gauge HDPE bags tailored for high-volume retail chains in India and Southeast Asia, where durability and cost efficiency are paramount. Novolex supports take-back programs and promotes compatibility with existing recycling infrastructure by integrating circular economy principles, which strengthens its reputation as a solutions-driven supplier in evolving regulatory environments.

- Berry Global has established a robust footprint in Asia-Pacific through joint ventures and technology transfer agreements with local converters in Thailand, Vietnam, and India. The company supplies engineered plastic films for high-performance trash and industrial sacks, emphasizing durability and resource efficiency. Berry is positioning itself at the intersection of functionality, compliance, and sustainability in the region’s transitioning packaging landscape through collaborations with municipal waste systems in Australia and New Zealand.

- Mondi, though traditionally strong in paper packaging, has expanded its hybrid plastic bag offerings in Asia-Pacific by combining polyethylene with recyclable design principles. The company operates production facilities in China and India, supplying industrial sacks and retail carry bags with enhanced tear resistance and printability. Mondi is shaping a pragmatic transition model that balances environmental goals with real-world usability in diverse Asian markets by leveraging its global R&D network and regional customer insights.

Top Strategies Used by Key Market Participants

Key players in the plastic bags market are prioritizing material innovation to develop mono-structure, recyclable films that comply with evolving waste management regulations. Companies are investing in advanced extrusion and lamination technologies to reduce gauge thickness while maintaining strength, thereby lowering resin consumption and transportation emissions. Strategic collaborations with retailers and municipalities are enabling pilot programs for bag take-back and chemical recycling integration. Firms are also adopting digital watermarking, as seen in the HolyGrail 2.0 initiative, to improve sorting efficiency in material recovery facilities. Manufacturers are diversifying into hybrid formats, combining plastic with reusable or compostable elements, particularly in high-income markets, to navigate regulatory burden.

MARKET SEGMENTATION

This research report on the global plastic bags market has been segmented and sub-segmented into the following categories.

By Material

- Non-biodegradable

- High-density Polyethylene (HDPE)

- Low-density Polyethylene (LDPE)

- Linear Low-density Polyethylene (LLDPE)

- Polypropylene (PP)

- Polystyrene (PS)

- Others

- Biodegradable

- Polylactic Acid (PLA)

- Polyhydroxyalkanoates (PHA)

- Polybutylene Succinate (PBS)

- Starch Blends

- Others

By Product

- T-shirt Bags

- Trash Bags

- Rubble Sacks

- Woven Sacks

- Others

By Application

- Retail & Consumer Applications

- Grocery

- Food & Beverage

- Clothing & Apparel

- Others

- Institutional Services

- Hospitality

- Healthcare

- Others

- Industrial Applications

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

1. What is the Plastic Bags Market?

The Plastic Bags Market represents all production, distribution, and consumption of plastic bags across consumer, industrial, retail, food service, waste management, and e-commerce applications worldwide

2. What sectors drive demand in the Plastic Bags Market?

Retail, food service, healthcare, personal care, e-commerce, household, and industrial sectors are top consumers of plastic bags

3. What are the major types of bags in the Plastic Bags Market?

Key types include T-shirt bags, zipper bags, gusseted bags, slider bags, garbage/waste bags, reusable bags, packaging bags, and specialty food service bags

4. Which materials are most used in the Plastic Bags Market?

Polyethylene (PE) dominates with more than 46% share due to its durability and cost efficiency, though compostable and biodegradable materials are gaining ground

5. How are environmental regulations impacting the Plastic Bags Market?

Plastic bags face strict global regulations, including bans and mandates for recyclable/compostable materials, driving innovation and shifts toward eco-friendly alternatives

6. Which regions lead the Plastic Bags Market?

Asia Pacific and North America account for over 39% of market share in 2035, led by China, India, and the United States due to growth in retail and food packaging

7. Who are leading manufacturers in the Plastic Bags Market?

Major companies include Berry Global, Novolex, Amcor, Mondi, Sonoco, ProAmpac, CeDo, RKW Group, and Bischof & Klein, with many focused on eco-friendly innovation

8. How is sustainability influencing the Plastic Bags Market?

Sustainability trends are driving the adoption of biodegradable and compostable bags, recycling initiatives, and innovations in bag design and materials

9. What recent innovations exist in the Plastic Bags Market?

Developments include enzyme-embedded compostable plastics, recyclable multi-layer films, lightweight and durable designs, and transparent brands for traceable supply chains

10. How do consumers drive change in the Plastic Bags Market?

Growing consumer awareness and preference for eco-friendly packaging are leading manufacturers to invest in green materials and reusable bag options

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com