Global Plastic Packaging Market Size, Share, Trends & Growth Forecast Report - Segmented By Type (Rigid Plastic Packaging and Flexible Plastic Packaging), Product, End-User, Region, and Industry Analysis (2026 to 2034)

Global Plastic Packaging Market Size

The global plastic packaging market size was valued at USD 316.65 million in 2025, and the market size is expected to reach USD 539.54 million by 2034 from USD 335.97 million in 2026. The market is growing at a CAGR of 6.10% during the forecast period.

Plastic packaging refers to the containment systems derived from synthetic polymers, such as polyethylene, polypropylene, PET, and multilayer composites, designed to preserve product integrity, extend shelf life, and enable logistical efficiency across industries. Unlike passive enclosures, modern plastic packaging integrates active barriers, intelligent indicators, and resealable architectures calibrated for specific environmental and mechanical stresses.

MARKET DRIVERS

E-commerce Boom Drives Plastic Packaging Demand

The exponential expansion of e-commerce, which demands lightweight, shock-absorbent, and customizable packaging formats to survive multi-leg logistics, drives the plastic packaging market growth. According to study, global parcel volumes rose in 2024, with a portion requiring plastic-based protective solutions. In the United States alone, the National Retail Federation recorded a year-over-year growth in online retail in 2024, directly correlating with rising demand for mailers and reusable solutions alongside e-commerce growth. Amazon’s packaging initiatives, which reduced secondary packaging, and further validated engineered plastic’s capacity to merge durability with dimensional optimization, a non-negotiable for last-mile economics.

Rising Processed Food Consumption Fuels Market Growth

The global shift toward processed and convenience foods, necessitating high-barrier, portion-controlled, and shelf-stable plastic formats, propels the expansion of the plastic packaging market. As per the research, a portion of urban consumers purchase pre-packaged meals weekly, a increase since 2019. In parallel, the U.S. saw single-person households, which rely disproportionately on individually sealed plastic portions, grew to millions in recent years, which represents a share of American households. According to study, vacuum skin packaging and other vacuum/skin techniques extend meat shelf life.

MARKET RESTRAINTS

Global Regulations Restrict Single-Use Plastic Packaging

The intensifying global regulatory burden to curb single-use plastic consumption, particularly in consumer-facing applications, which restricts the growth of plastic packaging market. As per the United Nations Environment Assembly, 127 countries have now enacted legislation restricting lightweight plastic bags, with the European Union’s Single-Use Plastics Directive mandating a 90% collection target for plastic bottles by 2029. In Canada, Environment and Climate Change Canada confirmed a nationwide ban on single-use plastics took full effect in December 2024 by eliminating over 1.3 million tonnes of hard-to-recycle plastic waste over the next 10 years.

Consumer Skepticism Slows Market Expansion

Persistent consumer skepticism and greenwashing accusations, which affects brand trust despite technical advances in recyclability, hinders the expansion of the plastic packaging market. As per the Study by Simon-Kucher & Partners, a share of consumers in G7 nations have strong interest in sustainability and willingness-to-pay patterns. The U.S. Federal Trade Commission The FTC ran a high-profile workshop and review on “recyclable” claims in 2024 and has been active on green-marketing enforcement. According to study, a portion of U.S. shoppers avoid products in non-monolayer plastic, even if functionality is superior.

MARKET OPPORTUNITIES

Chemical Recycling Technologies Create Growth Opportunities

The rapid advancement of chemical recycling technologies, which convert mixed or contaminated plastic waste back into virgin-grade feedstock, which sets up new opportunities for the plastic packaging market growth. According to research, commercial-scale pyrolysis and depolymerization plants processed notable metric tons of post-consumer plastic in 2024, an increase from 2020. Dow Chemical’s partnership with Mura Technology enables hydrothermal recycling of multi-layer films into reusable naphtha.

Smart Packaging Enhances Traceability and Sustainability

The integration of digital watermarking and blockchain traceability into plastic packaging by enabling granular material tracking and automated sorting, which provides fresh opportunities for the growth of the plastic packaging market. A significant number of digitally watermarked plastic packages were piloted, which improves sorting accuracy at recycling facilities. In parallel, according to plastic bank, millions of Kg of plastic was collected in 2024 across countries where it operates.

MARKET CHALLENGES

Inadequate Recycling Infrastructure Limits Market Growth

The global inadequacy of recycling infrastructure, particularly in emerging economies where consumption surges outpace waste management capacity, challenges the growth of the plastic packaging market. As per the World Bank, only a portion of plastic waste in Sub-Saharan Africa is formally collected, with lesser share undergoing mechanical recycling. In India, despite being a major plastic producer, a portion of plastic packaging still ends up in open dumps or waterways due to fragmented collection systems. Even in developed nations, according to research, only a percentage of plastic film, including grocery bags and wrappers, was recycled in 2024.

Multilayer Plastic Complexity Hampers Recycling Efficiency

The technical incompatibility of high-performance multilayer plastic structures with existing recycling streams, rendering them functionally non-recyclable despite consumer perception, hampers the expansion of the plastic packaging market. As per the study, a portion of flexible food packaging contains incompatible polymer blends that jam or contaminate mechanical recycling lines. Also, according to research, separating polyethylene terephthalate from ethylene vinyl alcohol in barrier films requires solvent-based processes not yet scalable beyond lab environments.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.10% |

| Segments Covered | By Type, Product, End-User, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Mondi Group, Berry Plastics Corporation, Sonoco Products Company, Amcor Limited, DS Smith plc, Bemis Company, Inc., NatureWorks LLC, Consolidated Container Company, Reynolds Group Holdings Limited, Alpla Werke Alwin Lehner GmbH & Co. KG., and Others. |

SEGMENTAL ANALYSIS

By Type Insights

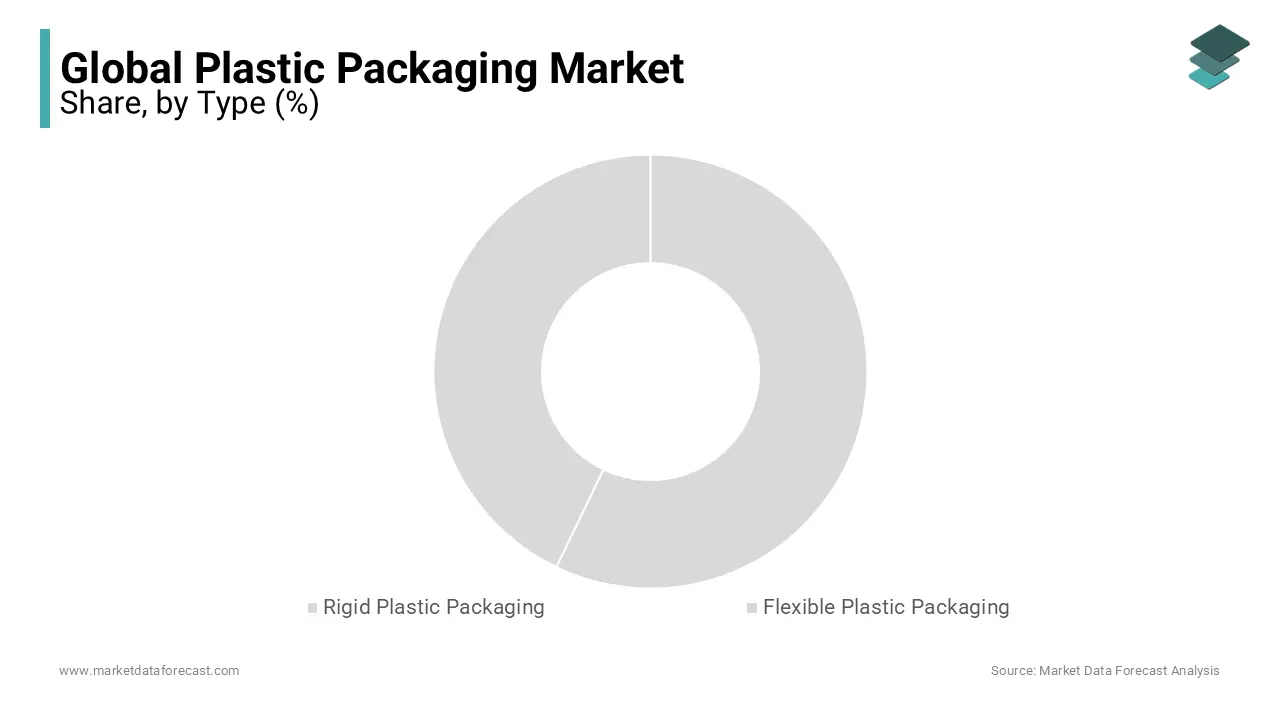

The rigid plastic packaging segment dominated the plastic packaging market by capturing 58.9% of the global market in 2025. The growth of the rigid plastic packaging market is driven by industrial and consumer reliance on dimensional stability and reusability, traits flexible formats cannot replicate at scale. As per study, a portion of dairy products are distributed in HDPE or PET bottles due to their crush resistance and light-blocking properties, which reduce spoilage compared to translucent alternatives. Infrastructure inertia further cements this lead.

The flexible plastic packaging segment is predicted to witness the highest CAGR of 6.9% from 2026 to 2034. The rapid growth of the flexible plastic packaging segment is fueled by e-commerce’s logistical imperatives, lightweight, form-fitting, and damage-resistant formats reduce shipping costs, according to the study. In food retail, stand-up pouches with reclosable zippers grew year-over-year in 2024, as per study, as consumers prioritize portion control and pantry efficiency. Technological breakthroughs also drive adoption. Like, ultra-thin barrier film reduced material use while maintaining low oxygen transmission rates, as per research.

By Product Insights

The bottles segment led the plastic packaging market by accounting for 34.8% share in 2025. The growth of the bottles segment is because of universal compatibility with liquid and semi-liquid products, from water and sauces to shampoos and pharmaceutical syrups. According to research, global bottled water consumption was billions of liters in 2024, with a percentage packaged in PET, a format chosen for its clarity, lightness, and shatter resistance. In pharmaceuticals, the U.S. Pharmacopeia requires child-resistant closures for a portion of oral liquid prescriptions, a specification most efficiently met by injection-molded polypropylene bottles with tamper-evident rings.

The pouches segment is estimated to register the fastest CAGR of 8.3% during the forecast period. In emerging markets, flexible pouches displaced a share of glass and metal containers in edible oil packaging across India and Indonesia, as per research, due to lower breakage and transport costs. Innovations like spouted stand-up pouches for infant nutrition recorded growth, according to study, combining hygiene, dosing precision, and shelf appeal. Pouches are not containers, but are behavioral drivers reshaping consumption rituals.

By End-User Insights

The food and beverage segment held 42.5% of the plastic packaging market share in 2025. The prominence of the food and beverage segment in the global market is attributed to non-negotiable functional requirements, modified atmosphere packaging extended the shelf life of pre-cut produce by several days, according to the study. The European Food Safety Authority provides guidance on the composition of multilayer films for food packaging. Urbanization intensifies dependence. According to study, a portion of urban households in Southeast Asia purchase weekly groceries in pre-packaged formats, up from that in 2019. Even regulatory burden supports plastic’s role, without high-barrier films, food waste in the EU would increase by millions of tonnes annually.

The healthcare segment is anticipated to witness the fastest CAGR of 9.1% from 2026 to 2034. Factors such as the sterile barrier systems for surgical kits grew, driven by outpatient procedure expansion, which contributes to the growth of the healthcare segment. In diagnostics, single-use plastic sample containers accounted for a portion of specimen transport, as per research, due to contamination control imperatives. The U.S. saw an increase in home-administered injectables since 2020, which necessitates pre-sterilized, auto-disable plastic delivery systems. Thus, healthcare’s plastic dependency is non-substitutable, it is a hygiene and safety imperative encoded in global clinical protocols.

REGIONAL ANALYSIS

North America Market Analysis

North America was the top performer in the plastic packaging market by capturing 28.8% of share in 2025 with the material science innovation, a portion of new polymer patents filed globally in 2024 originated from U.S. institutions, according to the study. The U.S. Food and Drug Administration’s stringent extractables and leachables guidelines compel manufacturers to develop ultra-pure resins by setting global benchmarks.

Asia Pacific Market Analysis

Asia Pacific was the second-largest in the plastic packaging market by accounting for 35.8% share in 2025. China produced millions of tonnes of plastic packaging in 2024, according to the study, driven by e-commerce parcel growth exceeding annually. India’s street food formalization initiative promotes hygienic plastic wrapping for millions of vendors, as per research, which triggers mass adoption of low-cost polypropylene films. Japan leads in high-tech recycling, its notable PET bottle recovery rate, as per research, stems from AI-powered reverse vending machines installed in a portion of municipalities. This region’s dominance is a synchronized engine of consumption, innovation, and infrastructural adaptation.

Europe Market Analysis

Europe plastic packaging market is esteemed to grow with significant growth opportunities during the forecast period with its legislative architecture that transforms environmental burden into industrial innovation. The European Union emphasized that plastic packaging placed on the market be reusable or recyclable, which influences of new product launches, according to study. France banned plastic packaging for 80% of fruits and vegetables in 2024, per the Ministry of Ecological Transition by forcing accelerated adoption of compostable biofilms.

Latin America Market Analysis

Latin America grew gradually in the plastic packaging market due to the regulatory asymmetry but explosive retail modernization. Brazil accounts for a portion of regional demand, as per study, with flexible packaging for snacks and ready meals growing. Chile became the first South American nation to mandate recycled content in all beverage bottles, as per research. Urbanization is decisive, a portion of Peruvians now reside in cities, according study, accelerating shift from bulk to portion-controlled plastic packs.

Middle East and Africa Market Analysis

The Middle East and Africa is likely to grow in the global plastic packaging demand owing to infrastructural gaps and demographic urgency. Saudi Arabia’s Vision 2030 spurred funds in packaging infrastructure investments, as per the study, targeting food security through shelf-life extension. South Africa leads in polymer recycling, a portion of plastic packaging was recovered, according to study, despite energy constraints. Nigeria’s informal retail sector, comprising a share of FMCG sales, as per study, relies on low-cost plastic sachets for affordability. This region’s trajectory is rewriting plastic’s role in survival economies.

COMPETITIVE LANDSCAPE

KEY MARKET PLAYERS

Some of the key players dominating the global plastic packaging market are

- Mondi Group

- Berry Plastics Corporation

- Sonoco Products Company

- Amcor Limited

- DS Smith plc

- Bemis Company, Inc.

- NatureWorks LLC

- Consolidated Container Company

- Reynolds Group Holdings Limited

- Alpla Werke Alwin Lehner GmbH & Co. KG

TOP STRATEGIES USED BY KEY MARKET PLAYERS

Leading players prioritize circular material innovation, replacing multilayer composites with mono-material or chemically recyclable structures. They acquire recycling technology startups to vertically integrate post-consumer feedstock control. Strategic partnerships with CPG giants embed packaging engineers early in product development, ensuring recyclability by design. Automation investments optimize material usage through AI-driven right-sizing and defect detection. Geographic expansion targets emerging markets where e-commerce and urbanization drive format adoption. Compliance with Extended Producer Responsibility laws is engineered into product architecture, not retrofitted. Digital watermarking pilots enable sorting accuracy, while blockchain traceability validates recycled content claims, which transforms packaging from waste generator to circular asset.

TOP PLAYERS IN THE MARKET

- Amcor plc operates as a global architect of advanced plastic packaging, engineering solutions across rigid containers, flexible laminates, and specialty healthcare formats. Amcor also partnered with Nestlé and Unilever to co-develop refillable mono-material structures, embedding circularity into product design. Its global network of facilities ensures localized compliance with evolving EPR and recyclability mandates by strengthening its role as a sustainability enabler.

- Sealed Air Corporation leads in protective and food packaging systems, renowned for innovations like Cryovac barrier films and Instapak foam-in-place solutions. The company acquired a German automation firm to integrate AI-driven right-sizing algorithms into its packaging lines, reducing material waste. Sealed Air also collaborated with major retailers to implement in-store recycling kiosks for flexible films. Its focus on performance-driven sustainability, balancing protection, shelf life, and end-of-life responsibility, cements its position at the convergence of logistics and circular design.

- Berry Global Group, Inc. dominates in high-volume rigid and flexible formats, serving food, healthcare, and personal care sectors with precision-engineered solutions. Berry’s acquisition of a specialty barrier coating startup enhanced its ability to replace multilayer structures with mono-material alternatives. Its vertically integrated resin-to-finished-pack model ensures control over purity, cost, and regulatory compliance, a decisive advantage in an era of material scrutiny.

RECENT HAPPENINGS IN THE MARKET

- In January 2024, Amcor launched a recyclable mono-material stand-up pouch for instant noodles in Indonesia, developed in collaboration with a leading food brand, enhancing product shelf life while supporting sustainability goals and strengthening its position in the Asia Pacific flexible packaging market.

- In March 2024, Mondi expanded its technical support team in Vietnam and introduced a fully recyclable polyethylene lidding film for dairy applications, enabling regional clients to replace multi-material laminates and comply with evolving packaging regulations in the Asia Pacific region.

- In August 2024, Sealed Air inaugurated a new innovation center in Shanghai, focused on developing lightweight, high-barrier packaging solutions tailored for the Chinese food and e-commerce sectors, accelerating product customization and reinforcing its technological dominance in the Asia Pacific market.

- In November 2024, Amcor partnered with the Alliance to End Plastic Waste to fund a plastic collection and recycling initiative in rural India, improving waste recovery infrastructure and enhancing brand credibility among environmentally conscious consumers and corporate clients.

- In April 2025, Sealed Air introduced its Cryovac® Darfresh on Demand vacuum packaging system in Japan, reducing plastic usage by 30% while extending shelf life for fresh meat, which is marking a significant advancement in sustainable retail-ready packaging and its foothold in the premium Asia Pacific food packaging segment.

MARKET SEGMENTATION

This research report on the global plastic packaging market has been segmented and sub-segmented based on the product, type, end-user, and region.

By Type

- Rigid Plastic Packaging

- Flexible Plastic Packaging

By Product

- Bags

- Cans

- Bottles

- Pouches

- Others

By End-User

- Food and Beverage

- Healthcare

- Pharmaceutical

- Retail

- Personal and Home Care

- Others

By Region

- North America

- Latin America

- Europe

- Asia Pacific

- Middle East & Africa

Frequently Asked Questions

1. What is the projected size of the global plastic packaging market by 2034?

The global plastic packaging market is expected to reach USD 539.54 million by 2034.

2. What are the current trends in the global plastic packaging market?

Trends include the rise of lightweight packaging, flexible plastics, and the integration of recyclable materials.

3. What factors are driving the growth of the global plastic packaging market?

Growth is driven by rising demand from food, beverage, and healthcare sectors, along with increased e-commerce activity.

4. How is sustainability influencing the global plastic packaging market?

Brands are shifting to recyclable and biodegradable plastic solutions to meet regulatory and consumer sustainability demands.

5. What technological innovations are impacting the global plastic packaging market?

Advancements in smart packaging, bioplastics, and barrier technologies are enhancing performance and shelf life.

6. What are the major challenges facing the global plastic packaging market?

Key challenges include environmental concerns, stringent regulations, and competition from alternative packaging materials.

7. How is consumer behavior affecting the global plastic packaging market?

Eco-conscious consumers are pushing for reduced plastic use, prompting brands to adopt greener packaging solutions.

8. Which industries are the top consumers of plastic packaging globally?

The food & beverage, healthcare, personal care, and industrial sectors are the primary users of plastic packaging.

9. Which regions are leading growth in the global plastic packaging market?

Asia-Pacific leads due to industrial growth and population demand, while North America and Europe follow with innovation-driven adoption.

10. What is the competitive landscape of the global plastic packaging market?

The market is competitive, with companies focusing on material innovation, cost efficiency, and sustainability compliance.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com