Global Recreational Boats Market Size, Share, Trends & Growth Forecast Report, Segmented By Power (Engine-Powered, Man-Powered, Sail Powered), Product Type (Inboard Boats, Outboard Boats, Inflatable, Sail Boats, Personal Watercrafts), Activity Type (Watersports, Cruising, Fishing) And By Region (North America, Europe, Asia Pacific, Latin America, and Middle East and Africa), Industry Analysis From (2025 to 2033)

Global Recreational Boats Market Size

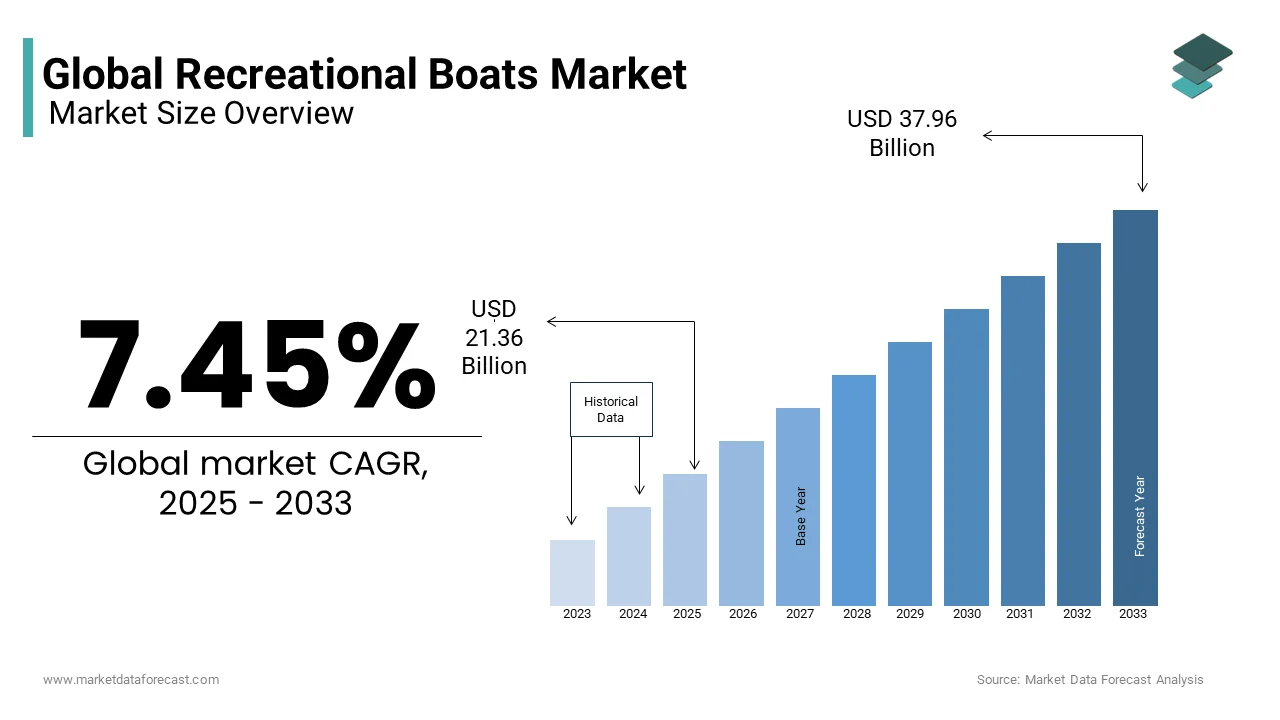

The global recreational boats market was valued at USD 19.88 billion in 2024 and is anticipated to reach a valuation of USD 21.36 billion in 2025, from USD 37.96 billion by 2033, growing at a CAGR of 7.45% during the forecast period from 2025 to 2033.

The recreational boats are designed for leisure, sports, and personal enjoyment rather than commercial or industrial use. These include motorboats, sailboats, yachts, personal watercraft, pontoons, and fishing boats, among others. As per data from the National Marine Manufacturers Association (NMMA), the U.S. recreational boating industry alone accounted for over 890,000 boat registrations in 2023, reflecting sustained demand despite macroeconomic fluctuations. In Europe, countries such as Germany and France have seen rising participation in sailing and lake-based recreational activities, contributing to a steady growth trajectory. A notable trend is the increasing adoption of electric and hybrid-powered recreational vessels, aligning with global sustainability goals.

MARKET DRIVERS

Rise in Disposable Income and Lifestyle Changes

The rise in disposable income across both developed and emerging economies is amplifying the growth of the recreational boats market. As per the World Bank, global GDP per capita increased by approximately 2.3% annually between 2018 and 2023, enabling a larger portion of the population to allocate funds toward discretionary spending. This trend is particularly evident in North America and Western Europe, where consumers are increasingly investing in leisure activities that offer escapism and outdoor engagement. In the United States, the Census Bureau reported that personal income rose by 6.3% in 2022 compared to the previous year, directly influencing the surge in recreational vehicle and equipment purchases. Moreover, lifestyle changes post-pandemic have shifted consumer behavior toward health-conscious and socially distanced forms of recreation. A study by McKinsey & Company noted that 60% of high-net-worth individuals surveyed expressed increased interest in private leisure experiences, including boating.

Expansion of Water-Based Tourism and Infrastructure Development

The expansion of water-based tourism and the development of supporting infrastructure such as marinas, boat ramps, and coastal resorts will additionally fuel the growth of the recreational boats market. According to the World Travel & Tourism Council, the global tourism sector contributed over $9.1 trillion to the global economy in 2022, with water-based tourism accounting for an estimated 15% of this value. This growth has been underpinned by strategic investments in maritime infrastructure, particularly in the Asia-Pacific and the Mediterranean regions. Additionally, governments in countries like Australia and Canada are offering tax incentives and subsidies for small businesses entering the charter boating industry, further stimulating market growth.

MARKET RESTRAINTS

High Initial and Maintenance Costs

The high initial purchase cost and ongoing maintenance expenses associated with owning a boat are slightly degrading the growth of the recreational boats market. According to Statista, the average price of a new recreational boat in the United States was approximately $65,000 in 2023, with luxury yachts often exceeding $1 million. This includes expenses such as winterization, engine maintenance, hull cleaning, and trailer storage. Furthermore, supply chain disruptions and inflationary pressures since 2021 have exacerbated these costs. These financial barriers deter first-time buyers and reduce repeat purchases, particularly in regions with lower average incomes.

Regulatory and Environmental Compliance Pressures

Increasingly stringent environmental regulations and compliance requirements are another major restraint on the recreational boats market. Governments worldwide are implementing tighter emissions standards and pollution control measures to protect aquatic ecosystems. For instance, the European Union’s Recreational Craft Directive mandates that all new boats meet strict noise, exhaust, and chemical resistance standards, significantly raising production costs for manufacturers.

According to the International Council on Clean Transportation, the implementation of Tier 4 emission standards in the U.S. has led to a 20–25% increase in the cost of marine engines compliant with these norms. Additionally, states like California have introduced low-emission zones in certain waterways, restricting access for older or non-compliant vessels. These policies, while environmentally beneficial, create additional hurdles for manufacturers and consumers alike. Environmental advocacy groups are also exerting pressure on policymakers to limit fossil fuel-powered boating activities. A 2023 report by the Natural Resources Defense Council estimated that recreational boating contributes approximately 1.5 million tons of carbon dioxide annually in the U.S. alone. As a result, some jurisdictions are considering bans or restrictions on gasoline-powered boats in ecologically sensitive areas.

MARKET OPPORTUNITIES

Growth in Electric and Hybrid Boat Technology

The advancement and adoption of electric and hybrid propulsion systems represent a transformative opportunity for the recreational boats market. According to BloombergNEF, the global market for electric marine propulsion systems is expected to grow at a compound annual rate of 14% through 2030, with recreational applications accounting for nearly 40% of this demand. Companies such as Torqeedo, Vision Marine Technologies, and Candela are leading the charge in developing high-efficiency electric motors tailored for leisure boats. In 2023, Candola's fully electric hydrofoil yacht achieved a breakthrough with a 50% reduction in energy consumption compared to conventional electric boats. Moreover, government incentives are accelerating this transition. Norway, for example, has mandated that all new boats registered in its fjords must be zero-emission by 2026.

Digital Integration and Smart Boating Solutions

The integration of digital technologies into recreational boats is unlocking new opportunities for market expansion. Modern consumers are increasingly seeking smart features such as GPS navigation, remote diagnostics, autopilot systems, and mobile connectivity. Boat manufacturers are partnering with tech firms to embed AI-driven safety systems, real-time weather monitoring, and IoT-enabled control panels. Garmin’s 2023 product lineup, for instance, included a fully integrated touchscreen navigation system compatible with voice commands and smartphone apps, enhancing user experience and safety. Additionally, subscription-based software platforms are gaining traction in the industry. Companies like Navico offer cloud-connected dashboards that provide analytics on fuel efficiency, route optimization, and maintenance alerts.

MARKET CHALLENGES

Supply Chain Disruptions and Raw Material Shortages

The volatility in global supply chains and raw material availability is a challenging factor for the growth of the recreational boats market. The marine industry relies heavily on components such as fiberglass, aluminum, marine-grade wood, and electronic systems, many of which have faced shortages in recent years. In addition, the price of core materials has fluctuated dramatically. The Aluminum Association reported that aluminum prices in the U.S. rose by 24% in 2022 compared to the previous year, driven by energy crises and trade restrictions. Fiberglass resin, another input, saw a 30% price hike during the same period, as per data from the American Composites Manufacturers Association. Geopolitical tensions have further exacerbated logistical bottlenecks. The conflict in Ukraine disrupted the supply of neon gas used in semiconductor manufacturing, while port congestion in China delayed shipments of boat components.

Seasonal Demand and Weather-Dependent Usage

The inherently seasonal nature of demand and the dependency on favorable weather conditions also limit the growth of the recreational boats market. Unlike essential transportation sectors, recreational boating is largely tied to summer months and mild climates, resulting in uneven revenue streams for manufacturers and dealers. This seasonality affects inventory management and financing strategies across the supply chain. Boat dealerships often face cash flow issues during off-peak months, as noted in a 2023 report by Deloitte, which found that 40% of surveyed dealers experienced reduced liquidity from October to February. In regions prone to hurricanes or monsoons, such as Florida and Southeast Asia, boat owners may avoid using their vessels for extended periods due to safety concerns. The Insurance Information Institute indicated that storm-related claims for recreational boats in the U.S. rose by 18% in 2022 compared to the previous decade’s average.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 7.45% |

| Segments Covered | By Power, Product Type, Activity Type, and Region. |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Caterpillar Incorporated, Azimut-Benetti, Ferretti, Carlisle Paddles, Avon Inflatables, Brunswick Corporation, Rodriguez, Bombardier Recreational Products Incorporated, Bavarian, Sealine Attwood, Zodiac Marine & Pool, Platinum Equity, Baja Marine, Suzuki Motor Corporation, Princess, Group Beneteau, Sunseeker, Azimut-Benetti, Yamaha Motor Company Limited, Kawasaki Heavy Industries Limited, KCS International Incorporated, Honda Motor Company Limited, Poly Marquis Yach, Tognum AG, Hydra-Sports Boat, Godfrey Marine, Crusader Marine Engines, General Motors Company, Pleasurecraft Engine Group, Interphase Technologies, Fountain Powerboat Industries Incorporated, and Others. |

SEGMENT ANALYSIS

By Power Insights

The engine-powered segment dominated the recreational boats market share in 2024. According to Grand View Research, this segment was valued at approximately USD 18 billion and is projected to maintain its dominance throughout the forecast period due to strong consumer preference for motorized convenience and performance. Another major driver is the integration of advanced marine propulsion systems. Companies like Yamaha Marine and Mercury Marine have introduced fuel-efficient, low-emission engines that comply with environmental regulations while improving user experience. For instance, Mercury’s Verado line of four-stroke outboards has seen a 22% year-over-year sales increase since 2021, as per company reports.

The sail-powered boats segment is swiftly growing with an expected CAGR of 7.5% between 2023 and 2030, according to Global Market Insights. While currently holding a smaller market share compared to engine-powered boats, their appeal is rising steadily, especially in Europe and North America. Additionally, the expansion of sailing clubs and training institutions is boosting participation. The Royal Yachting Association recorded a 15% rise in sailing course enrollments in the UK between 2021 and 2023. Governments and tourism bodies in countries like Greece and Croatia are also promoting sailing holidays through marina development and tax incentives.

By Product Insights

The outboard boats segment accounted in holding 38.3% of the recreational boats market share in 2024, with the growing popularity of small to mid-sized boats powered by detachable outboard motors. These motors allow for easy repair and replacement, making them ideal for budget-conscious consumers. Technological advancements in outboard motor efficiency have further enhanced demand. For example, Mercury Marine introduced the 600HP V12 outboard engine in 2022, which offers improved fuel economy and reduced emissions.

The personal watercrafts (PWCs) segment is projected to grow with a CAGR of 8.1% in the coming years. The surge in adventure tourism and youth engagement in watersports is also fueling the growth of the recreational boats market. A 2023 survey conducted by Statista revealed that 68% of PWC users in North America were under the age of 45, indicating strong traction among younger demographics who seek excitement and mobility. Additionally, rental services in coastal destinations have expanded significantly, allowing tourists to access PWCs without ownership burdens. Manufacturers are capitalizing on this trend by introducing technologically advanced models with GPS, Bluetooth connectivity, and enhanced safety features. Sea-Doo, a division of BRP Inc., reported a 24% increase in global PWC sales in 2023, attributing much of this success to its GTX Limited model series.

By Activity Insights

The fishing segment held 42.3% of the recreational boats market share in 2024, with the strong regulatory support and conservation programs encouraging responsible angling practices. Moreover, the availability of affordable, purpose-built fishing boats has made ownership more accessible. Brands such as Lund, Ranger Tugs, and Boston Whaler have expanded their entry-level fishing boat lines, catering to middle-income consumers. As per NMMA, fishing boat sales in the U.S. grew by 7.3% in 2023, outpacing other recreational categories.

The watersports boats segment is likely to register a CAGR of 9.2% during the forecast perio,d with the increasing participation in water-based adventure activities, particularly among millennials and Gen Z. According to a 2023 Nielsen Sports report, watersports engagement in the U.S. rose by 18% over the past five years, with wakeboarding and wakesurfing leading the way. This shift has led to a surge in demand for customized boats equipped with ballast tanks, wave-generating systems, and onboard audio systems. Major manufacturers like MasterCraft Boat Holdings and Malibu Boats have capitalized on this trend by launching innovative models tailored to the needs of watersport enthusiasts. For instance, MasterCraft’s X26 model saw a 32% sales increase in 2023 due to its superior wave-creation capabilities.

REGIONAL ANALYSIS

North America

North America was the top performer of the global recreational boats market by accounting for 42.3% of the share in 2024. The U.S. is the epicenter of this dominance, contributing over 85% of regional demand, driven by high disposable income, extensive coastline, and a deeply ingrained boating culture. The National Marine Manufacturers Association (NMMA) reported 307,000 new powerboat sales in the U.S. in 2022, a 12% increase from 2020, reflecting sustained consumer interest. Canada complements this with steady growth, particularly in freshwater lakes and coastal provinces. Favorable government policies, such as tax incentives for marina development in Florida and Michigan, further stimulate infrastructure. Additionally, the rise in remote work post-pandemic has increased leisure time spent on water activities. Online boat rental platforms like GetMyBoat have seen a 35% YoY user growth (2021–2023), indicating shifting consumption patterns.

Europe

Europe was positioned second with 28.3% of the global recreational boats market share in 20,24, with strong maritime traditions and developed coastal infrastructure. Italy leads in manufacturing, producing 35% of Europe’s recreational boats, while Germany and France are top consumers due to high affluence and lake-rich geographies. The EU’s Blue Growth strategy has injected €70 million into sustainable marina development since 2020, boosting accessibility.

Asia-PacifThe ic

Asia-Pacific recreational boats market is likely to have a significant CAGR during the forecast period, with growth concentrated in developed economies and emerging luxury markets. Australia and Japan are established players, with Australia reporting 1.1 million registered recreational vessels (Australian Bureau of Statistics, 2022) and Japan maintaining steady demand for compact, fuel-efficient boats suited to its island geography. China’s market is nascent but accelerating—recreational boat sales grew at a CAGR of 9.3% from 2018 to 2022 (China Marine Equipment Research Institute), supported by government initiatives like the “National Fitness Plan” promoting water sports. Thailand and Malaysia are emerging as yachting tourism hubs, with Phuket and Langkawi investing in marina infrastructure; Thailand’s marina capacity expanded by 30% between 2020 and 2023 (Tourism Authority of Thailand).

Latin America

Latin American recreational boats market is expected to grow steadily in the coming years. Mexico’s coastal tourism, especially in the Riviera Maya and Baja California, fuels demand for charter fleets and personal watercraft; the country added 1,200 new marina berths between 2020 and 2023 (Mexican Ministry of Tourism). Argentina shows potential in freshwater boating on Lake Nahuel Huapi, though economic volatility limits consistent growth.

Middle East and Africa

The Middle East and Africa recreational boats market is also expected to have sustained growth opportunities during the forecast period. The UAE, particularly Dubai and Abu Dhabi, is the epicenter, hosting over 12,000 registered recreational vessels (Dubai Maritime City Authority, 2023) and attracting ultra-high-net-worth individuals with tax-free ownership and luxury marinas like Dubai Marina—the world’s largest, with 1,400 berths.

KEY MARKET PLAYERS

Caterpillar Incorporated, Azimut-Benetti, Ferretti, Carlisle Paddles, Avon Inflatables, Brunswick Corporation, Rodriguez, Bombardier Recreational Products Incorporated, Bavarian, Sealine Attwood, Zodiac Marine & Pool, Platinum Equity, Baja Marin, Suzuki Motor Corporation, Princess, Group Beneteau, Sunseeker, Azimut-Benetti, Yamaha Motor Company Limited, Kawasaki Heavy Industries Limited, KCS International Incorporated, Honda Motor Company Limited, Poly Marquis Yach, Tognum AG, Hydra-Sports Boat, Godfrey Marine, Crusader Marine Engines, General Motors Company, Pleasurecraft Engine Group, Interphase Technologies, Fountain Powerboat Industries Incorporated. These are the market players that are dominating the global recreational boats market.

Top Players In The Market

Brunswick Corporation

Brunswick Corporation is a global leader in the recreational boating industry, with a strong presence across boat manufacturing, marine engines, and parts distribution. The company owns several premium boat brands such as Sea Ray, Boston Whaler, and Mercury Marine, which collectively contribute significantly to the global market. Brunswick has played a pivotal role in shaping consumer preferences and setting industry standards. Its commitment to sustainability and advanced marine technology has reinforced its leadership position.

Yamaha Motor Co., Ltd.

Yamaha Marine, a division of Yamaha Motor Co., Ltd., is a major player in the outboard engine segment and also produces personal watercrafts that are widely used for recreational purposes. The company is recognized for its reliable, high-performance engines and Jet Boats that cater to both leisure and sport activities. Yamaha’s focus on integrating cutting-edge technology into marine products has enhanced user experience and strengthened its global footprint. It's a continuous investment in research and development that ensures consistent product evolution and customer satisfaction.

Malibu Boats, Inc.

Malibu Boats specializes in high-performance towed watersports boats, particularly wakeboarding and wakesurfing vessels. It holds a significant share in the premium segment due to its innovative hull designs and onboard systems tailored for professional and recreational use. Malibu's dedication to enhancing the watersports experience through engineering excellence and customization options has made it a preferred choice among enthusiasts. The company consistently introduces new models that set trends in the performance boating sector, which is contributing to market growth and competitive differentiation.

Top Strategies Used By Key Market Participants

One of the primary strategies adopted by leading companies in the recreational boats market is product innovation and technological advancement. Manufacturers are focusing on developing fuel-efficient engines, electric propulsion systems, and smart navigation features to meet evolving consumer demands and regulatory requirements. These innovations not only enhance performance but also align with sustainability goals, attracting environmentally conscious buyers.

Another key strategy is strategic acquisitions and partnerships. Companies are acquiring complementary brands or forming alliances to expand their product portfolios, enter new markets, and strengthen their supply chains. These moves allow firms to consolidate their market presence, access new customer bases, and benefit from shared R&D capabilities.

The brand diversification and customization play a crucial role in maintaining competitiveness. By offering a wide range of models across different price points and functionalities, companies can cater to varied consumer preferences. Additionally, personalized design options and after-sales services help build brand loyalty and improve customer retention.

COMPETITION OVERVIEW

The competition in the recreational boats market is characterized by a mix of established global players and regional manufacturers striving for market expansion and technological leadership. While large corporations dominate through brand recognition, scale of operations, and extensive distribution networks, mid-sized and local firms compete by offering niche products and cost-effective solutions. Innovation remains a central battleground, with companies investing heavily in R&D to introduce advanced features such as hybrid propulsion, digital integration, and enhanced safety mechanisms. Mergers and acquisitions are frequently employed to gain strategic advantages and broaden geographic reach. Moreover, sustainability initiatives and eco-friendly product development are increasingly influencing competitive positioning.

RECENT HAPPENINGS IN THE MARKET

- In February 2024, Brunswick Corporation launched a new line of fully electric pontoon boats under its Mercury Marine brand, which is aiming to capitalize on the growing demand for sustainable marine solutions and reinforce its leadership in green boating technology.

- In June 2023, Yamaha Motor Co., Ltd. entered into a strategic partnership with a European-based battery technology firm to develop next-generation lithium-ion power systems for recreational boats by enhancing performance and extending operational range.

- In September 2024, Malibu Boats introduced an AI-driven onboard control system across its latest model series, allowing users to customize ride settings, monitor performance metrics, and receive predictive maintenance alerts via mobile connectivity.

- In March 2023, Brunswick Corporation acquired a U.S.-based digital marine electronics startup specializing in smart navigation and vessel monitoring systems, which i strengthening its portfolio of connected boating technologies.

- In November 2024, Yamaha Motor Co., Ltd. expanded its production facility in Thailand to increase output capacity for outboard engines by supporting rising demand in the Asia-Pacific region and reinforcing its supply chain resilience.

MARKET SEGMENTATION

This research report on the global recreational boats market is segmented and sub-segmented into the following categories.

By Power

- Engine-Powered

- Man-Powered

- Sail Propelled

By Product Type

- Inboard Boats

- Outboard Boats

- Inflatable

- Sail Boats

- Personal Watercrafts

By Activity Type

- Watersports

- Cruising

- Fishing

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

What are recreational boats?

Recreational boats are vessels used for leisure activities like fishing, cruising, water sports, and sailing rather than for commercial or military purposes.

What drives growth in the global recreational boats market?

The market grows due to rising disposable incomes, increased interest in outdoor activities, and innovations in boat design and technology.

Which regions have the largest share in the recreational boats market?

North America and Europe hold the largest share, driven by strong boating cultures and high purchasing power.

What types of recreational boats are most popular?

Popular boats include motorboats, sailboats, yachts, pontoon boats, and personal watercraft.

How is technology shaping the recreational boats market?

Advancements like electric propulsion, smart navigation systems, and connected features are making boating safer and more enjoyable.

What are major challenges in the recreational boats market?

Key challenges include environmental concerns, high ownership costs, and strict regulatory standards.

Who are the primary buyers of recreational boats?

Enthusiasts, families, rental companies, and luxury consumers are key buyers in this market.

How do environmental regulations impact the market?

Stringent emissions and safety regulations drive manufacturers to adopt cleaner and safer technologies.

What role does boat rental and sharing play in market growth?

Boat rental platforms and sharing apps make boating more accessible and boost market participation.

What trends are shaping the future of recreational boating?

Trends include eco-friendly boats, digital connectivity, automation, and personalized customer experiences.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com