Global Sexual Wellness Market Size, Share, Trends & Growth Forecast Report By Product (Contraceptives, Condoms, Sex Toys, Lubricants, Sexual Enhancement Supplements and Others), Distribution Channel (Hospital Pharmacy, Retail Pharmacy and Online Pharmacy) and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2025 To 2033.

Global Sexual Wellness Market Summary

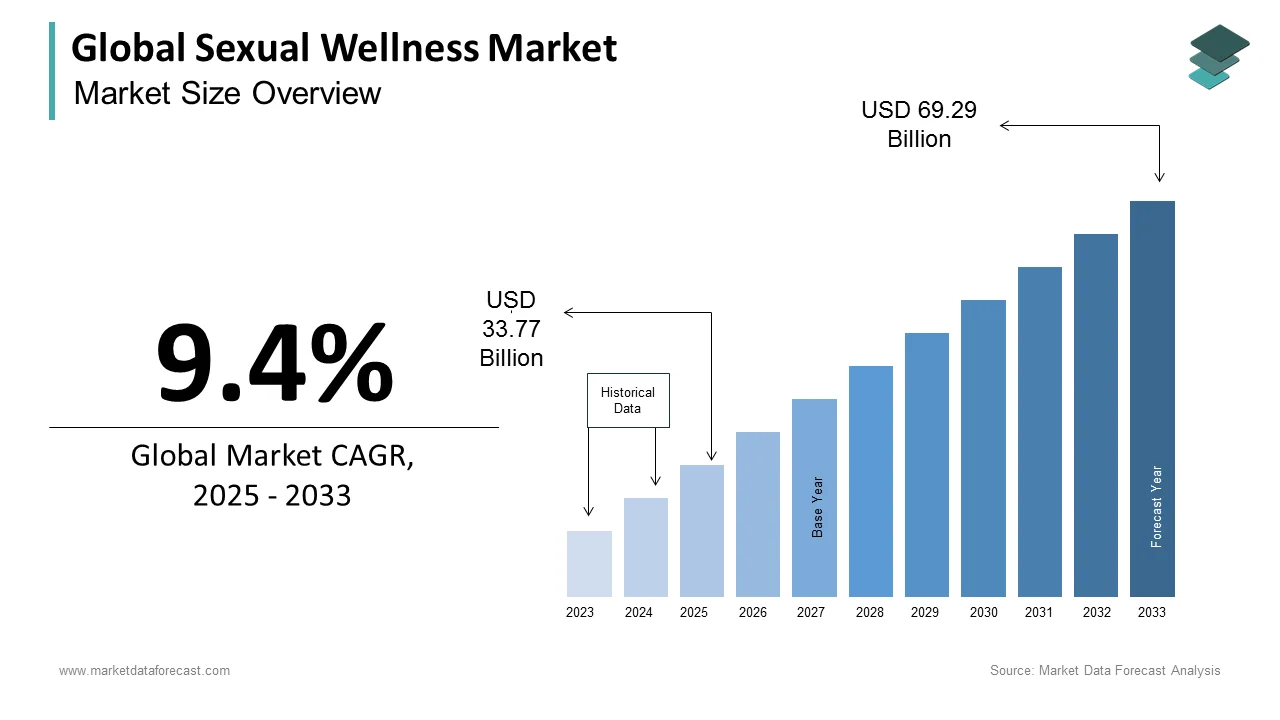

The global sexual wellness market size was estimated at USD 30.87 billion in 2024 and is projected to reach USD 69.29 billion by 2033, growing at a CAGR of 9.4% from 2025 to 2033. Increasing awareness of sexual health, technological advancements in intimate products, and rising investments in women’s sexual wellness are key growth factors.

Key Market Trends & Insights

- Asia Pacific led the global sexual wellness market in 2024.

- North America is expected to showcase strong growth throughout the forecast period.

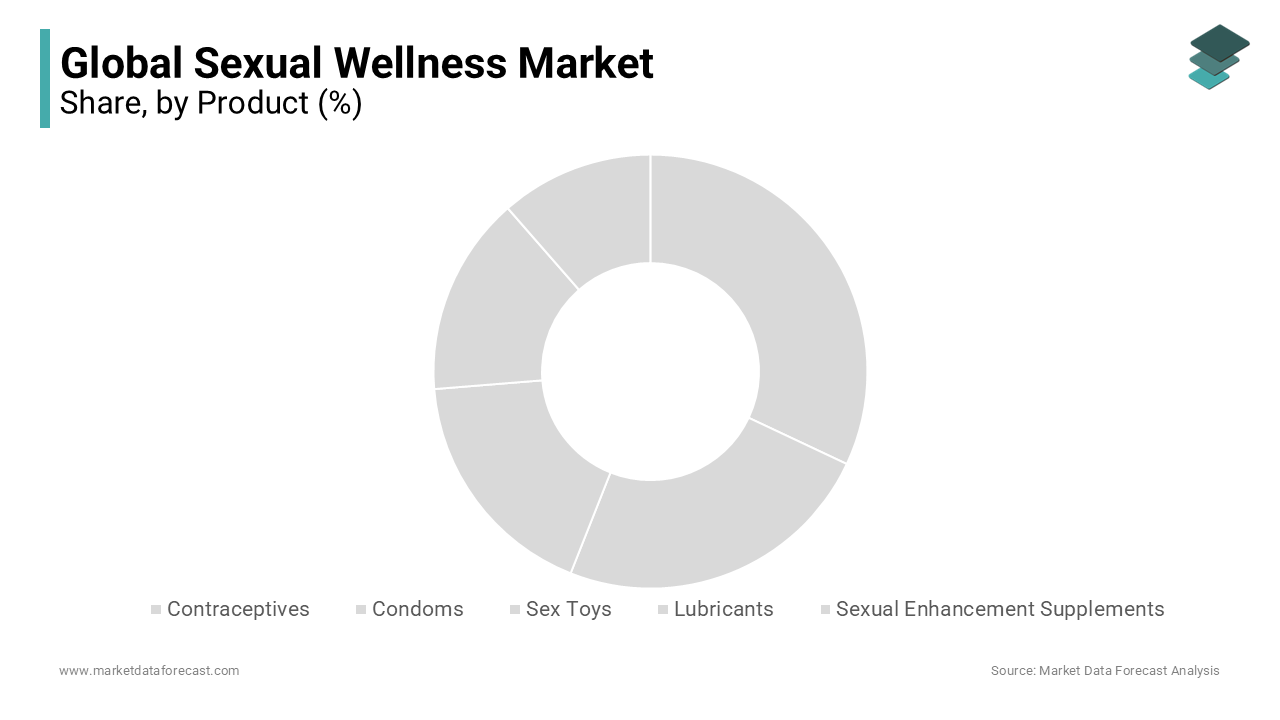

- Based on product, the lubricants was the leading segment in 2024.

- Based on distribution channel, the retail pharmacy segment held the dominant market share in 2024.

- Based on fastest-growing segments, sexual enhancement supplements and online pharmacy are projected to record the highest growth during 2025–2033.

Market Size & Forecast

- 2024 Market Size: USD 30.87 Billion

- 2033 Projected Market Size: USD 69.29 Billion

- CAGR (2025–2033): 9.4%

- Asia Pacific: Largest market in 2024

- North America: Strong growth region

Global Sexual Wellness Market Size

The size of the global sexual wellness market was worth USD 30.87 billion in 2024. The global market is anticipated to grow at a CAGR of 9.4% from 2025 to 2033 and be worth USD 69.29 billion by 2033 from USD 33.77 billion in 2025.

Sexual Wellness is a broad spectrum of products, services, and educational initiatives designed to enhance sexual health, improve intimacy, and support reproductive well-being across all genders and age groups. It extends beyond conventional sexual health care to include sexual pleasure, mental wellness related to sexuality, and the prevention and management of sexual dysfunction. This market integrates physical, emotional, and psychological dimensions of sexual health, offering solutions such as lubricants, intimate hygiene products, sexual wellness devices, telehealth consultations, and hormone therapies. As awareness grows around holistic well-being, sexual wellness has emerged as a critical component of overall health.

According to the World Health Organization, sexual health is a state of physical, emotional, mental, and social well-being with sexuality, not merely the absence of disease. The integration of digital health platforms has further expanded access, with apps offering personalized sexual health tracking and education. In 2023, the Global Burden of Disease Study highlighted that over 40% of women and nearly 30% of men globally experience some form of sexual dysfunction during their lifetime, underscoring the growing need for comprehensive sexual wellness solutions. Cultural shifts, increasing openness in discussing intimate health, and rising investments in women’s health innovation are reshaping the landscape, particularly in emerging economies where traditional taboos are gradually diminishing.

MARKET DRIVERS

Growing Awareness of Sexual Health and Its Impact on Demand

The escalating public awareness regarding sexual health and its intrinsic link to overall well-being is a pivotal driver of the Sexual Wellness Market. In recent years, global health institutions and advocacy groups have intensified efforts to normalize conversations around sexual wellness, leading to increased consumer engagement. This educational shift has translated into higher demand for preventive and enhancement-oriented products. Moreover, digital media and influencer-led campaigns have played a transformative role. This visibility reduces stigma and encourages informed decision-making. In the Asia-Pacific region, countries such as India and Indonesia have witnessed a surge in online searches for sexual wellness terms. The proliferation of tele-gynecology and discreet e-commerce options further supports this demand, enabling users to access products and consultations without social discomfort. As awareness becomes institutionalized through education and media, consumer behavior is shifting from reactive to preventive care, fueling sustained market expansion.

Technological Innovation in Sexual Wellness Products

Technological advancement stands as a cornerstone in the evolution of the Sexual Wellness Market, significantly amplifying consumer interest and product efficacy. The integration of artificial intelligence, biometrics, and app-connected devices has redefined how individuals monitor and enhance their sexual health. For example, wearable devices that track physiological responses during intimacy, such as heart rate variability and pelvic floor activity, are gaining traction. Moreover, AI-powered chatbots offering personalized sexual health advice have seen adoption. These tools provide tailored insights on menstrual cycles, fertility, and sexual well-being, bridging gaps in clinical access. In the realm of male sexual wellness, at-home testing kits for testosterone and erectile function have surged in popularity. Furthermore, 3D-printed anatomically accurate intimacy devices are being developed to cater to diverse body types and preferences, enhancing user satisfaction. The U.S. Food and Drug Administration has also cleared several digital therapeutics for sexual dysfunction, including apps for treating hypoactive sexual desire disorder, signaling regulatory validation of tech-driven solutions. These innovations not only improve functionality but also ensure privacy and convenience, critical factors for consumer adoption. As technology continues to merge with intimate health, the market is poised for exponential growth driven by personalized, data-driven experiences.

MARKET RESTRAINTS

Persistent Cultural Stigma and Its Market Suppression

Deep-rooted cultural stigma surrounding sexuality remains a formidable restraint on the Sexual Wellness Market, particularly in conservative regions. In many societies, discussions about sexual health are deemed inappropriate, leading to underreporting of issues and reluctance to seek solutions. The cultural silence directly impacts consumer behavior. Even in more progressive nations, implicit biases persist. In rural areas of China and India, traditional beliefs often equate sexual wellness products with promiscuity, discouraging uptake. Moreover, media censorship in countries like Malaysia and Saudi Arabia restricts advertising for sexual wellness brands, limiting public awareness. This stigma also deters investment. Until societal norms evolve to embrace sexual health as a legitimate aspect of well-being, market growth will remain constrained in key regions, impeding equitable access and innovation.

Regulatory Hurdles in Product Classification and Approval

Inconsistent and often ambiguous regulatory frameworks governing product classification and approval is a significant restraint within the Sexual Wellness Market. Many sexual wellness products, particularly those positioned at the intersection of medical devices and consumer goods, face classification challenges that delay market entry and increase compliance costs. In the European Union, for instance, the Medical Device Regulation (MDR) reclassified certain intimate devices as Class IIa medical devices, requiring rigorous clinical evaluations. In the United States, the FDA does not recognize “sexual wellness” as a distinct category, forcing companies to navigate multiple regulatory pathways, either as cosmetics, drugs, or medical devices, depending on claims made. This complexity discourages small and mid-sized enterprises. Additionally, import restrictions in countries like Indonesia and Turkey further limit availability. Without harmonized global standards, manufacturers face fragmented compliance landscapes, increasing time-to-market, and reducing consumer trust in product safety and efficacy.

MARKET OPPORTUNITIES

Expansion of Digital Health Platforms in Sexual Wellness

The rapid expansion of digital health platforms that deliver personalized, accessible, and discreet care is one of the most transformative opportunities in the Sexual Wellness Market. Telehealth services specializing in sexual health have gained significant momentum, particularly following the normalization of virtual consultations during the pandemic. These platforms offer everything from prescription treatments for low libido to counseling for sexual trauma, integrating medical expertise with user-friendly interfaces. In low-resource settings, mobile health apps are proving instrumental. AI-driven symptom checkers and chat-based consultations are reducing barriers to entry, especially for marginalized populations. Furthermore, digital platforms enable data aggregation for trend analysis, allowing providers to anticipate demand and tailor interventions. The integration of blockchain for secure health records also enhances privacy, a critical concern for users. With global smartphone penetration increasing in urban areas, the scalability of digital sexual wellness solutions is unparalleled. As connectivity improves and digital literacy rises, these platforms are poised to become primary access points for sexual health care, particularly in regions with limited clinical infrastructure.

Rising Investment in Women’s Sexual Health Innovation

The increasing focus on women’s sexual health, long neglected in medical research and product development, is a burgeoning opportunity within the Sexual Wellness Market. Historically, female sexual dysfunction has been underdiagnosed and undertreated, but recent shifts in funding and research priorities are catalyzing innovation. This has led to the approval of non-hormonal therapies such as bremelanotide and vaginal laser treatments. Venture capital is also flowing into femtech startups. Companies like Peanut and Elvie are expanding their offerings beyond fertility and pregnancy into sexual wellness, leveraging community-based models to drive engagement. In India, startups such as Sirona and Nua have disrupted the market with culturally sensitive products. Moreover, corporate wellness programs are beginning to include sexual health screenings. This institutional recognition validates the sector’s importance and encourages broader adoption. As gender equity gains prominence in healthcare, the focus on women’s sexual wellness is not only correcting historical imbalances but also unlocking a vast, underserved market segment with high growth potential.

MARKET CHALLENGES

Lack of Standardized Education and Professional Training

The absence of standardized education and professional training for healthcare providers in sexual health is a critical challenge facing the Sexual Wellness Market. Despite its significance, sexual wellness remains a peripheral subject in most medical and nursing curricula. The deficiency translates into inadequate patient care. In low- and middle-income countries, the situation is more acute. The lack of expertise undermines consumer trust in clinical recommendations and pushes individuals toward unregulated online sources. Moreover, the absence of certified sexual wellness practitioners limits service scalability. The scarcity forces reliance on generalists who may lack specialized skills. Even within allied professions like physiotherapy and mental health, training in pelvic floor dysfunction and sexual trauma remains inconsistent. Without a globally recognized certification framework, the quality of care varies significantly, hindering market credibility. Addressing this challenge requires systemic reform in medical education and the establishment of accredited training pathways to ensure competent, compassionate care.

Product Counterfeiting and Consumer Safety Concerns

The proliferation of counterfeit sexual wellness products represents a growing challenge that undermines consumer trust and poses serious health risks. With the rise of e-commerce and cross-border online marketplaces, substandard and falsified products ranging from lubricants to intimacy devices are increasingly entering the market. As per the World Health Organization, 1 in 10 medical products in low- and middle-income countries is substandard or falsified, and intimate health items are among the most commonly affected categories. Similarly, the UK’s Medicines and Healthcare products Regulatory Agency reported an increase in counterfeit sexual health product seizures between 2021 and 2023. These products often lack proper labeling, sterility, or safety testing, leading to adverse reactions. Consumer awareness remains low. The issue is exacerbated by the discreet nature of these purchases, which discourages users from reporting adverse effects. Brands face reputational damage, and legitimate manufacturers incur higher compliance costs to differentiate their offerings. Without stronger international enforcement and supply chain transparency, the prevalence of counterfeit goods will continue to erode consumer confidence and impede market integrity.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Product, Distribution Channel, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Market Leaders Profiled | Church & Dwight Co., Inc., Reckitt Benckiser Group plc, Doc Johnson Enterprises, Karex Berhad, TENGA Co., Ltd., Hot Octopuss, Caya, California Exotic Novelties LLC, Bijoux Indiscrets, and Adam & Eve Stores. |

SEGMENTAL ANALYSIS

By Product Insights

The Lubricants segment was the largest product within the Sexual Wellness Market and accounted for 26.3% of the global share in 2024. This dominance is primarily driven by their universal applicability across genders, age groups, and sexual orientations, coupled with increasing recognition of their role in enhancing comfort and preventing tissue damage during intimacy. A key factor underpinning this segment’s leadership is the rising prevalence of vaginal dryness and genitourinary symptoms, particularly among aging populations. Additionally, medical endorsements have elevated their status from lifestyle products to therapeutic aids. A further driving force is the expansion of product innovation, with brands introducing pH-balanced, organic, and condom-compatible formulations. Furthermore, growing awareness among men about anal health and comfort during same-sex intimacy has broadened the user base. This cross-demographic utility, combined with clinical validation and evolving social norms, solidifies lubricants as the cornerstone of the sexual wellness ecosystem.

The Sexual Enhancement Supplements segment is the fastest-growing segment in the market and is projected to expand at a CAGR of 12.4% from 2025 to 2033. This surge is largely attributed to increasing consumer preference for natural and non-invasive solutions to sexual dysfunction. One major driver is the growing incidence of low libido and erectile difficulties linked to sedentary lifestyles and chronic stress. Moreover, consumers are turning to herbal supplements containing ingredients like maca root, horny goat weed, and L-arginine. An additional critical factor is the destigmatization of male sexual health issues. Further, digital marketing and influencer endorsements have accelerated adoption, particularly among younger demographics. Regulatory flexibility, where these products are classified as dietary supplements rather than drugs, also enables faster market entry and lower pricing, further boosting accessibility and appeal.

By Distribution Channel Insights

The Retail Pharmacy segment prevailed in the distribution landscape by capturing 42.6% of the global Sexual Wellness Market in 2024. This dominance is because of the enduring consumer preference for in-person consultations and immediate product access, particularly for sensitive health-related purchases. A primary driver of retail pharmacy leadership is the trust consumers place in pharmacists as accessible healthcare advisors. This advisory role is especially critical in regions with limited access to physicians, such as rural areas in Europe and Australia. Besides, major pharmacy chains have expanded their private-label sexual wellness offerings, enhancing margins and consumer loyalty. The physical presence of pharmacies also provides a sense of legitimacy and discretion shelving of products in dedicated, semi-private sections reduces embarrassment. This blend of professional guidance, immediacy, and cultural acceptability ensures that retail pharmacies remain the dominant conduit for sexual wellness products despite digital competition.

The Online Pharmacy segment is the fastest-growing distribution channel and is projected to grow at a CAGR of 16.8% in the coming years. This rapid expansion is fueled by the increasing demand for privacy, convenience, and discreet delivery in sexual health purchases. One of the most influential drivers is the normalization of telehealth-integrated e-pharmacies, where consumers can consult licensed providers and receive prescriptions for sexual wellness products within hours. An additional critical factor is the rise of subscription-based models that ensure continuous access to products like lubricants and supplements. Furthermore, younger demographics, particularly Millennials and Gen Z, are more inclined to shop online for intimate products. Cross-border e-commerce is also expanding access in regions with restrictive retail environments, and users in the Middle East and Southeast Asia increasingly rely on international platforms to bypass local taboos. With advancements in secure payment systems and AI-driven personalization, online pharmacies are not only growing in volume but also transforming into comprehensive sexual health ecosystems.

REGIONAL ANALYSIS

North America Sexual Wellness Market Analysis

North America stood as the most advanced and mature market for sexual wellness. The region’s position is anchored in robust healthcare infrastructure, progressive social attitudes, and strong regulatory support for sexual health innovation. The U.S., in particular, drives regional growth through high consumer spending on preventive and enhancement-oriented products. Additionally, the FDA’s clearance of digital therapeutics for sexual dysfunction, such as the app Sprout for HSDD, reflects a regulatory environment conducive to innovation. The U.S. also leads in venture capital investment in femtech and sexual wellness startups. Canada complements this momentum with universal healthcare coverage that includes sexual health counseling and STI screening, contributing to an increase in lubricant and supplement sales between 2020 and 2023. Cultural openness further amplifies demand. This combination of medical accessibility, technological adoption, and social acceptance positions North America as the global epicenter of sexual wellness innovation and consumption.

Europe Sexual Wellness Market Analysis

Europe is another key player in the market, with Western European nations leading in product diversification and policy integration. Countries like Germany, France, and the UK have institutionalized sexual wellness into public health frameworks, ensuring widespread access to contraceptives and counseling services. The UK’s National Health Service distributed millions of free condoms in 2023, reflecting a proactive approach to sexual health prevention. Germany, known for its advanced medical device sector, has become a hub for innovation in intimate diagnostics and pelvic floor therapy. The region also benefits from high consumer literacy. However, disparities exist in Eastern Europe due to conservative norms and limited sex education. Online sales of sexual wellness products in Europe grew between 2021 and 2023, driven by privacy-conscious consumers in countries like Sweden and the Netherlands. With strong regulatory oversight and rising digital engagement, Europe remains a pivotal market for sustainable growth.

Asia-Pacific Sexual Wellness Market Analysis

Asia-Pacific (APAC) exhibits the most dynamic transformation due to shifting cultural paradigms and digital penetration. While traditional taboos persist in countries like India and Indonesia, urbanization and youth-driven demand are dismantling long-standing stigmas. India’s sexual wellness market is growing annually, fueled by startups like Sirona and Amour. Japan, despite its conservative public discourse, has one of the highest per capita consumptions of intimate hygiene products. China’s market is expanding through e-commerce giants like Alibaba and JD.com, where searches for “sexual wellness” increased by 200% between 2020 and 2023, according to QuestMobile. Government initiatives are also emerging. Also, digital platforms are bypassing traditional retail barriers. As younger generations embrace body positivity and self-care, APAC is evolving from a repressed market into a high-potential frontier for global brands.

Latin America Sexual Wellness Market Analysis

Latin America accounts for a modest share of the global market, with Brazil and Mexico emerging as key growth engines amid rising health awareness and economic liberalization. Brazil leads the region with a burgeoning middle class that increasingly prioritizes preventive health and personal well-being. The country’s Ministry of Health distributed a substantial quantity of condoms in 2023 as part of its HIV prevention strategy, indicating institutional commitment to sexual health. Mexico has witnessed an increase in online sales of sexual wellness products since 2021, driven by platforms like Claro Shop and Mercado Libre. Cultural shifts are also evident. Argentina became the first Latin American country to offer free, nationwide access to emergency contraception in 2022. A. However, challenges remain, including inconsistent sex education and gender-based disparities in healthcare access. Despite this, the region’s youthful population represents a vast untapped market. Social media influencers in Colombia and Chile are normalizing discussions around pleasure and consent, accelerating product adoption. With increasing urbanization and digital connectivity, Latin America is poised for accelerated growth, particularly in supplements and intimate devices.

Middle East and Africa Sexual Wellness Market Analysis

Middle East and Africa (MEA) collectively hold a small share of the global market with significant variation between subregions. Gulf Cooperation Council (GCC) countries like the UAE and Saudi Arabia are witnessing gradual liberalization, enabling discreet access to sexual wellness products through e-commerce and private clinics. The UAE’s sexual wellness market grew in 2023, supported by expatriate demand and medical tourism. In contrast, Sub-Saharan Africa faces systemic challenges, including limited healthcare infrastructure and high STI prevalence. South Africa remains the most developed market. Cultural conservatism remains a barrier, but mobile health initiatives are making inroads. With rising female economic participation and digital adoption, MEA is gradually transitioning from a neglected region to one with long-term strategic importance for global market players.

COMPETITIVE LANDSCAPE

The competition in the Sexual Wellness Market is intensifying as both established corporations and agile startups vie for consumer attention in a rapidly evolving landscape. Incumbents like Reckitt, Church & Dwight, and Kenvue leverage brand equity, global distribution, and regulatory expertise to maintain dominance, particularly in mature markets. However, they face growing pressure from digitally native brands that prioritize inclusivity, transparency, and innovation. These challenger brands often emerge from the femtech and wellness sectors, offering personalized solutions such as hormone-tracking supplements and body-positive intimacy devices. The competitive dynamic is further shaped by shifting consumer expectations. Privacy, sustainability, and clinical credibility are now essential differentiators. In the Asia Pacific, local players are gaining traction by addressing cultural nuances and affordability, challenging multinational pricing models. Mergers, acquisitions, and strategic alliances are common, as larger firms integrate niche innovations to stay relevant. Meanwhile, e-commerce platforms and social media enable smaller brands to scale rapidly without traditional retail dependencies. Regulatory disparities across regions create both barriers and opportunities, influencing market entry strategies. The absence of a unified global standard for product classification allows for creative positioning but also invites scrutiny. As sexual wellness becomes integrated into broader health and wellness ecosystems, competition is no longer solely about products but about trust, education, and user experience. This multifaceted rivalry is driving unprecedented innovation and market expansion.

KEY MARKET PLAYERS

Some of the most promising companies playing a leading role in the global sexual wellness market profiled in this report are

- Church & Dwight Co., Inc.

- Reckitt Benckiser Group plc

- Doc Johnson Enterprises

- Karex Berhad

- TENGA Co., Ltd.

- Hot Octopuss

- Caya

- California Exotic Novelties LLC

- Bijoux Indiscrets

- Adam & Eve Stores

- Others

TOP LEADING PLAYERS IN THE MARKET

- Reckitt has established a strong footprint in the Asia Pacific sexual wellness market through its Durex brand, a globally recognized name in condoms and lubricants. The company has prioritized consumer education and stigma reduction by launching digital campaigns across India, China, and Southeast Asia that promote safe sex and sexual well-being. In recent years, Reckitt has localized its product offerings, introducing thinner, flavored, and textured condoms tailored to regional preferences. It has also partnered with telehealth platforms in India to integrate Durex products into sexual health consultation packages. By leveraging e-commerce channels and collaborating with pharmacies and online retailers, Reckitt has enhanced product accessibility. The company continues to invest in sustainability, launching recyclable packaging for Durex in Australia and New Zealand. Its emphasis on brand trust, innovation, and public health engagement has solidified its role as a market influencer in the region.

- Church & Dwight Co., Inc. drives significant momentum in the Asia Pacific market through its Trojan brand, a leader in male sexual wellness products. The company has expanded its presence in urban centers across Japan, South Korea, and Southeast Asia by introducing premium condoms and personal lubricants designed for enhanced comfort and sensitivity. Trojan has collaborated with local health organizations to support sexual wellness awareness campaigns, particularly targeting young adults. In 2023, the company intensified its digital outreach through social media influencers and discreet online subscription models in countries like Thailand and Malaysia. It has also strengthened distribution partnerships with major e-commerce platforms such as Lazada and Shopee. By emphasizing product quality, discretion, and modern branding, Church & Dwight has successfully positioned Trojan as a lifestyle-oriented, trustworthy choice. Its focus on consumer-centric innovation and digital engagement continues to amplify its relevance in a culturally diverse and rapidly evolving market.

- Kenvue plays a pivotal role in the Asia Pacific sexual wellness landscape through its LifeStyles and Schmid & Partner brands, offering a wide range of condoms, lubricants, and intimate care products. The company has deepened its regional engagement by launching culturally sensitive marketing initiatives in India and Indonesia, focusing on education and inclusivity. Kenvue has introduced vegan, non-latex, and dermatologically tested products to meet rising demand for hypoallergenic options. In 2023, it expanded its digital footprint by integrating with health apps and teleconsultation services in Australia and Singapore. The company also supports public health programs, distributing millions of condoms in partnership with NGOs across Southeast Asia. By combining medical credibility with consumer-focused innovation, Kenvue has strengthened its reputation as a responsible market participant. Its ongoing investment in sustainable packaging and localized product development underscores its commitment to long-term growth and trust-building in the region.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Sexual Wellness Market deploy a range of strategic initiatives to consolidate their presence and drive growth. Product innovation remains a core focus, with companies developing advanced formulations, eco-friendly materials, and smart devices to differentiate offerings. Strategic partnerships with telehealth platforms enable seamless integration of products into digital sexual health services, enhancing accessibility and consumer trust. Geographic expansion, particularly into emerging markets in the Asia Pacific and Latin America, allows brands to tap into rising awareness and disposable incomes. E-commerce optimization is another critical strategy, with companies investing in direct-to-consumer models, discreet packaging, and AI-driven personalization. Additionally, brands are intensifying consumer education campaigns to reduce stigma and promote sexual well-being, often leveraging social media and influencer collaborations. Acquisitions and collaborations with femtech startups enable rapid entry into niche segments such as hormonal wellness and pelvic health. Sustainability initiatives, including recyclable packaging and ethical sourcing, are increasingly used to appeal to environmentally conscious consumers. Collectively, these strategies reflect a shift from transactional sales to holistic, trust-based engagement, positioning companies as long-term advocates of sexual wellness.

GLOBAL SEXUAL WELLNESS MARKET NEWS

- In January 2023, Reckitt launched a digital sexual wellness campaign in India under the Durex brand, partnering with telehealth platform Pristyn Care to offer bundled condom and consultation packages, enhancing accessibility and reducing stigma among young adults.

- In June 2023, Church & Dwight expanded its Trojan product line in Southeast Asia by introducing a new range of ultra-thin, vegan condoms available exclusively through Shopee and Lazada, strengthening its e-commerce presence and appealing to environmentally conscious consumers.

- In September 2023, Kenvue collaborated with Australia’s Family Planning Alliance to distribute 500,000 free condoms across urban and rural clinics, reinforcing its commitment to public health and increasing brand visibility in the Oceania region.

- In February 2024, LifeStyles Healthcare launched a new AI-powered intimacy app in Singapore that provides personalized sexual wellness tips and product recommendations, integrating digital health with consumer engagement to enhance user loyalty.

- In May 2024, Himalaya Wellness introduced a plant-based sexual wellness supplement for women in India, backed by clinical studies and promoted through influencer-led campaigns, marking a significant entry into the female sexual health segment by a traditional Ayurvedic brand.

MARKET SEGMENTATION

This research report on the global sexual wellness market has been segmented and sub-segmented based on product, distribution channel, and region.

By Product

- Contraceptives

- Condoms

- Sex Toys

- Lubricants

- Sexual Enhancement Supplements

- Others

By Distribution Channel

- Hospital Pharmacy

- Retail Pharmacy

- Online Pharmacy

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What is the Sexual Wellness Market?

The Sexual Wellness Market includes products and services designed to enhance sexual health and satisfaction, such as sex toys, lubricants, contraceptives, intimate hygiene products, and sexual health supplements

2. What are the major product categories in the Sexual Wellness Market?

Key categories include sex toys (vibrators, dildos, etc.), condoms, lubricants (water-based, silicone-based), female contraceptives, sexual wellness supplements, and intimate hygiene products

3. Which regions dominate the Sexual Wellness Market?

North America and Asia Pacific (especially India and China) are among the lead markets, driven by rising awareness, urbanization, and e-commerce growth

4. How is digital retail impacting the Sexual Wellness Market?

E-commerce accounts for over 60% of sales in many regions, offering discreet shopping, wide product variety, and convenience, fueling rapid market expansion

5. What trends are driving growth in the Sexual Wellness Market?

Growth drivers are increasing openness toward sexual health, destigmatization, smart sex toys using AI and VR, rising STI rates, and improving sex education

6. Who are the top players in the Sexual Wellness Market?

Leading companies include LifeStyles Healthcare, Reckitt Benckiser, Lovehoney Group, Church & Dwight, Okamoto Industries, Karex Berhad, and various regional brands

7. What role do innovations like AI and VR play in sexual wellness?

AI and VR technologies enable interactive and personalized experiences, enhancing product appeal and user engagement

8. How is sexual health education affecting the Sexual Wellness Market?

Better education reduces stigma, informs product choice, and motivates use, expanding market size

9. What challenges face the Sexual Wellness Market?

Challenges include regulatory complexity, cultural taboos, counterfeit products, and ensuring product safety and quality

10. How is the sexual wellness market segmented by gender?

Products and marketing increasingly target both men and women, with tailored solutions addressing unique needs of each group

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com