Global Sports Medicine Market Size, Share, Trends & Growth Forecast Report - Segmented By Product (Reconstruction and Repair Products, Support & Recovery Products, Accessories), Application (Head Injuries, Shoulder Injuries, Elbow and Wrist Injuries, Back and Spine Injuries, Hip and Groin Injuries, Knee Injuries and Foot and Ankle Injuries) and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) - Industry Analysis From 2024 to 2033

Global Sports Medicine Market Size

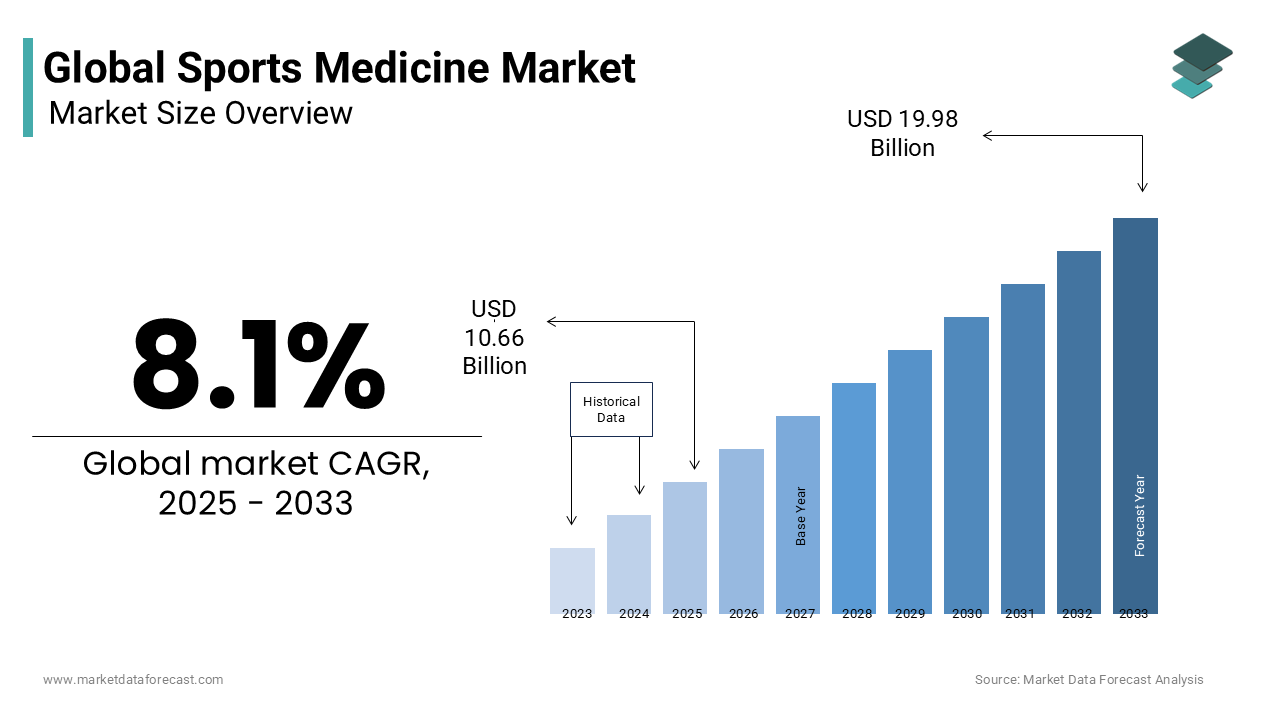

The global sports medicine market is estimated to grow from USD 9.86 billion in 2024 to USD 19.88 billion in 2033, representing a CAGR of 8.1%.

The Sports Medicine is used for the prevention, diagnosis, treatment, and rehabilitation of injuries related to athletic activity and physical exercise. It integrates medical disciplines such as orthopedics, physiotherapy, and biomechanics with advanced technologies to optimize performance and accelerate recovery. According to the American College of Sports Medicine, over 55 million Americans participated in sports medicine-related consultations or therapies in 2023, reflecting a growing reliance on specialized care. According to the World Health Organization, physical inactivity contributes to more than 3.2 million deaths annually with the preventive role of sports medicine in global health initiatives.

MARKET DRIVERS

Rising Incidence of Sports-Related Injuries Among Youth and Recreational Athletes

The escalating frequency of musculoskeletal injuries among young and recreational athletes, fueled by intensified training regimens and early sports specialization is accelerating the growth of the Sports Medicine Market. The increasing participation of adolescents in competitive sports, over 8 million U.S. high school students engaged in organized athletics as per the National Federation of State High School Associations that amplifies exposure to overuse and acute trauma. This demographic shift has spurred demand for diagnostic imaging, arthroscopic procedures, and regenerative therapies. Furthermore, the growing awareness among parents and coaches about long-term consequences of untreated injuries has elevated the prioritization of sports medicine consultations, which is driving clinical adoption and service expansion across outpatient centers and sports clinics.

Expansion of Minimally Invasive Surgical Techniques and Regenerative Therapies

The rapid integration of minimally invasive surgical (MIS) techniques and regenerative medicine into sports injury management is fuelling the growth of the Sports Medicine Market. Arthroscopy, a cornerstone of modern sports orthopedics, now accounts for over 4 million procedures globally each year, as reported by the International Arthroscopy Association. These techniques reduce recovery time, minimize complications, and enable faster return-to-play, making them highly desirable among athletes. Concurrently, regenerative therapies such as platelet-rich plasma (PRP) injections and stem cell treatments are gaining traction; the Global Regenerative Medicine Foundation notes that more than 300,000 PRP procedures were administered for musculoskeletal conditions in 2023, a 15% year-on-year increase. Technological advancements in biologics and tissue engineering are enhancing treatment efficacy, particularly for tendon and cartilage injuries.

MARKET RESTRAINTS

Limited Reimbursement Coverage for Advanced Sports Medicine Procedures

The inconsistent insurance reimbursement for innovative sports medicine treatments with the regenerative therapies and certain arthroscopic interventions is limiting the growth of the Sports Medicine Market. In the United States, Medicare and many private insurers do not routinely cover PRP or stem cell injections, deeming them experimental despite growing clinical evidence. As per the American Academy of Orthopaedic Surgeons, over 60% of patients seeking PRP therapy pay out-of-pocket, with average costs ranging from $500 to $2,000 per injection, creating financial barriers. This lack of coverage discourages widespread adoption, especially among non-professional athletes and middle-income populations.

Shortage of Specialized Sports Medicine Professionals in Developing Regions

The global disparity in the availability of trained sports medicine physicians, physiotherapists, and rehabilitation specialists, particularly in low- and middle-income countries is also to restrict the growth of the Sports Medicine Market. As per the World Federation of Sports Medicine, fewer than 30% of African nations have formal sports medicine training programs, resulting in a severe workforce deficit. India, with over 1.4 billion people, has fewer than 500 certified sports medicine physicians, translating to one specialist per 2.8 million individuals, according to the Indian Association of Sports Medicine. This scarcity limits the capacity for timely injury diagnosis and evidence-based treatment, leading to prolonged recovery and increased risk of chronic disability. Even in developed nations, rural areas face significant shortages; the U.S. Health Resources and Services Administration identifies over 7,000 primary care health professional shortage areas, many lacking access to sports rehabilitation services.

MARKET OPPORTUNITIES

Integration of Wearable Technology and Biomechanical Analytics in Injury Prevention

The integration of the wearable technology and biomechanical data analytics to enhance injury prevention and performance monitoring is likely to showcase new opportunities for the growth of the Sports Medicine Market. Devices such as smart insoles, motion-sensing garments, and GPS-enabled trackers are increasingly deployed across amateur and professional sports. According to the Consumer Technology Association, global shipments of sports and fitness wearables surpassed 150 million units in 2023, reflecting widespread adoption. These tools provide real-time feedback on movement patterns, muscle activation, and joint loading, enabling early detection of biomechanical imbalances that predispose athletes to injury. The NFL, for instance, equips all players with Zebra Technologies’ motion sensors to monitor workload and reduce overuse injuries. When integrated with AI-driven analytics platforms, wearable data can personalize training loads and recovery protocols.

Growth of Sports Tourism and Elite Training Centers Driving Demand for On-Site Medical Support

The proliferation of international sports tourism and high-performance training hubs is significantly fuelling the growth of the Sports Medicine Market. As per the Global Sports Tourism Market Report published by the United Nations World Tourism Organization, over 300 million travelers participated in sports-related trips in 2023, generating more than $800 billion in economic activity. These travelers—ranging from amateur triathletes to youth soccer teams—often require immediate access to sports injury care, physiotherapy, and emergency orthopedic services. Countries like Qatar, the United Arab Emirates, and Switzerland have invested heavily in elite sports complexes equipped with on-site medical clinics, leveraging public-private partnerships to deliver integrated care. The Aspetar Orthopaedic and Sports Medicine Hospital in Qatar, for example, treats over 120,000 athletes annually from more than 140 nations, as noted by the FIFA Medical Committee.

MARKET CHALLENGES

Regulatory Heterogeneity in Approval and Use of Biologic Therapies

The fragmented regulatory landscape governing biologic treatments such as PRP, stem cells, and amniotic tissue products is to elevate the growth of the Sports Medicine Market. In the United States, the Food and Drug Administration regulates these therapies under stringent biologics licensing requirements, whereas in countries like Mexico, Thailand, and India, oversight is less rigorous, leading to unstandardized clinical practices. As per the International Society of Orthopaedic Surgery and Traumatology, over 40% of clinics offering regenerative treatments in emerging markets operate without validated protocols or outcome tracking. This regulatory divergence undermines treatment credibility, increases the risk of adverse events, and complicates cross-border medical tourism. Moreover, inconsistent labeling and manufacturing standards hinder multicenter clinical trials and global data harmonization, delaying evidence-based consensus.

High Cost of Advanced Diagnostic and Therapeutic Equipment

The substantial capital investment required for advanced sports medicine infrastructure poses a persistent challenge, particularly for outpatient clinics and rehabilitation centers in resource-constrained settings. These expenses limit adoption, especially in rural or underserved urban areas. Maintenance, software updates, and technician training further escalate operational burdens. In low-income countries, fewer than 10% of sports medicine facilities possess on-site MRI access, according to the World Health Organization. This technological inequity results in delayed diagnoses, reliance on referral networks, and suboptimal treatment planning.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2024 to 2033 |

| Segments Covered | By Product, Application, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leader Profiled | Smith & Nephew PLC, Arthrex, Inc., össur hf, Stryker Corporation, Conmed Corporation, Zimmer Biomet Holdings, Inc., Breg, Inc., Mueller Sports Medicine, Inc., Tornier, Inc., Skins International Trading AG, Wright Medical Technology, Inc. |

SEGMENTAL ANALYSIS

By Product Insights

The reconstruction and repair products segment was the largest with prominent share of the sports medicine market in 2024. The rising volume of ligament and tendon injuries requiring surgical intervention is majorly propelling the growth of the segment. Anterior cruciate ligament (ACL) reconstructions alone exceed 200,000 procedures annually in the United States, a figure that has increased by 2.3% year-on-year over the past five years, according to the American Academy of Orthopaedic Surgeons. The growing use of biocompatible implants, such as interference screws, suture anchors, and soft tissue grafts, underpins this segment’s expansion. Furthermore, technological advancements in arthroscopic-compatible fixation devices have enhanced surgical precision and graft stability. As per the International Society of Arthroscopy, Knee Surgery and Orthopaedic Sports Medicine, over 90% of ACL reconstructions now utilize bioabsorbable fixation systems, which reduce long-term complications and eliminate the need for hardware removal.

The support and recovery products segment is projected to register CAGR of 8.7% from 2025 to 2033 with the escalating consumer preference for non-invasive, at-home rehabilitation solutions. Compression garments, braces, and neuromuscular electrical stimulation (NMES) devices are witnessing unprecedented adoption across amateur and professional athletic communities. According to the National Athletic Trainers’ Association, over 68% of collegiate sports programs in the U.S. now integrate wearable recovery technology into post-exercise protocols. Additionally, the global rise in home-based physical therapy, accelerated by telehealth integration, has amplified demand for portable recovery tools. A 2023 survey by the Consumer Healthcare Products Association revealed that sales of knee and ankle braces surpassed $2.1 billion worldwide, reflecting a 12% year-over-year increase. Coupled with growing awareness of injury prevention and accelerated recovery, this segment benefits from shifting healthcare models that prioritize outpatient and self-managed care.

By Application Insights

The knee injuries segment was accounted in holding 34.3% of the sports medicine market share in 2024 with the biomechanical vulnerability of the knee joint during dynamic sports activities. The anterior cruciate ligament (ACL) is among the most frequently injured structures, with an estimated 250,000 ACL tears occurring annually in the U.S., according to the American Orthopaedic Society for Sports Medicine. High-risk sports such as soccer, basketball, and skiing impose repetitive rotational and deceleration forces on the knee, increasing injury likelihood. Female athletes face a particularly elevated risk, with studies from the NCAA Injury Surveillance Program indicating they are 2 to 8 times more likely than males to suffer ACL ruptures in the same sports. This disparity has prompted increased investment in gender-specific prevention programs and surgical techniques.

The shoulder injuries segment is likely to grow with expected CAGR of 9.1% from 2025 to 2033 owing to the rising incidence of rotator cuff tears and labral injuries, particularly among overhead athletes such as swimmers, baseball pitchers, and tennis players. The American Shoulder and Elbow Surgeons estimate that over 2 million Americans experience rotator cuff injuries annually, with surgical repair cases increasing by 6% annually over the past decade. A key driver is the growing participation in racket and throwing sports; the United States Tennis Association reports over 23 million active tennis players in the U.S., many of whom engage in year-round training. Additionally, advancements in arthroscopic shoulder stabilization techniques and the development of suture anchor systems have improved clinical outcomes and reduced recovery times. As per the Journal of Shoulder and Elbow Surgery, over 85% of shoulder stabilization procedures are now performed arthroscopically, up from 60% in 2015.

REGIONAL ANALYSIS

North America was the top performer in the global sports medicine market by capturing 41.3% of the share in 2024 with its advanced healthcare infrastructure, high per capita healthcare expenditure, and deeply embedded sports culture. The U.S. alone reports over 60 million individuals participating in organized sports, as documented by the Sports & Fitness Industry Association. A robust pipeline of FDA-approved medical devices, coupled with widespread insurance coverage for orthopedic procedures, facilitates rapid clinical adoption. The presence of leading sports medicine manufacturers such as Arthrex, Stryker, and Smith & Nephew further strengthens the ecosystem. Additionally, collegiate and professional sports leagues maintain stringent medical protocols, driving demand for injury diagnostics and rehabilitation technologies.

Europe was positioned second in the sports medicine market with 28.3% of share in 2024 with the balanced integration of public healthcare systems and private sports medicine clinics, particularly in countries like Germany, the UK, and Switzerland. The German Society of Orthopaedics and Trauma Surgery notes that over 150,000 arthroscopic knee procedures are performed annually in Germany alone. Additionally, the European Union’s Medical Device Regulation (EU MDR) has enhanced product safety and traceability, fostering trust in advanced implants and biologics. Public investment in sports science, exemplified by institutions like the Aspetar-affiliated centers in collaboration with FIFA, has elevated clinical standards.

Asia Pacific is emerging swiftly with significant CAGR in the forecast period owing to the rapid urbanization, rising disposable incomes, and increasing awareness of sports-related healthcare. Countries like Japan, South Korea, and Australia exhibit advanced clinical capabilities, while India and China are witnessing exponential growth in sports participation. The Japan Sports Agency reports that over 70% of Japanese citizens engage in regular physical activity, with government initiatives promoting sports for health. In China, the State General Administration of Sports estimates that more than 400 million people now participate in fitness programs, creating a vast patient pool. However, disparities persist; India has only 150 certified sports medicine centers for a population exceeding 1.4 billion, as noted by the Indian Orthopaedic Association.

Latin America sports medicine market is likely to have prominent opportunities with its strong football culture and growing private healthcare sector. Over 70 million Brazilians participate in football annually, according to the Brazilian Football Confederation, which is generating consistent demand for injury care. Private clinics in São Paulo and Rio de Janeiro offer world-class arthroscopic services, often catering to medical tourists. However, public healthcare access remains limited; the World Bank reports that only 25% of Brazilians have private health insurance, restricting affordability of advanced treatments. Argentina and Mexico are also developing specialized sports medicine units, supported by national sports institutes.

Middle East & Africa Sports Medicine Market growth is likely to have steady pace in the future period . The Gulf Cooperation Council (GCC) nations, particularly the UAE and Qatar, are driving regional growth through strategic investments in sports infrastructure and elite medical facilities. Aspetar in Qatar, recognized as a FIFA Medical Centre of Excellence, treats over 100,000 patients annually from across the Middle East and Africa, as stated by the hospital’s annual report. The UAE’s Vision 2030 includes sports development as a public health pillar, with over $2 billion allocated to sports medicine and wellness initiatives. However, sub-Saharan Africa faces significant challenges, including a shortage of trained professionals and limited diagnostic equipment.

KEY MARKET PLAYERS

Noteworthy companies leading the global sports medicine market profiled in this report are Smith & Nephew PLC, Arthrex, Inc., össur hf, Stryker Corporation, Conmed Corporation, Zimmer Biomet Holdings, Inc., Breg, Inc., Mueller Sports Medicine, Inc., Tornier, Inc., Skins International Trading AG, Wright Medical Technology, Inc., DePuy Mitek, Inc., 3M Company Ace Brand, OttoBock Healthcare GmbH and DJO Global, Inc.

Key market participants invest hugely in Research and Development to create innovative and effective solutions for sports injuries. For instance, Nova Scotia's performance-based company, Athletigen Technology, Inc., has worked with various athletes to use information gathered in DNA to improve performance and reduce the incidence of sports-related injuries. The initiatives mentioned above by various companies are to drive market growth during the forecast period.

The competition in the Sports Medicine Market is intense and innovation-driven, characterized by a convergence of orthopedic device manufacturers, biotechnology firms, and digital health providers. Established players differentiate through technological superiority, clinical evidence, and surgeon education, while emerging companies focus on niche applications such as wearable recovery systems and regenerative therapies. Rivalry is particularly pronounced in minimally invasive devices and biologics, where product performance and recovery outcomes dictate market preference. Strategic collaborations with sports organizations and healthcare institutions enhance brand visibility and trust

Top Players in the Sports Medicine Market

Arthrex, Inc.

Arthrex has established itself as a pioneer in minimally invasive orthopedic solutions, with a strong footprint across the Asia Pacific region. The company operates dedicated training centers in Japan, Australia, and India, where surgeons are educated on advanced arthroscopic techniques, reinforcing clinical adoption of its devices. In recent years, Arthrex has intensified its collaboration with sports medicine societies in South Korea and Singapore to standardize best practices. It launched the BioComposite SwiveLock® anchor in the region, enhancing soft tissue fixation outcomes. The company also expanded its manufacturing facility in Malaysia to support regional supply chains, reducing delivery timelines.

Stryker Corporation

Stryker has significantly amplified its presence in the Asia Pacific sports medicine market through strategic expansions and technology integration. The company introduced its Mako robotic-arm assisted platform in select hospitals in Australia and Japan, enabling precision in ligament reconstruction and joint preservation procedures. Stryker also partnered with the Australian Institute of Sport to develop data-driven rehabilitation protocols using wearable sensors. In 2023, it opened a regional innovation hub in Singapore focused on adapting global technologies to local clinical needs. Additionally, Stryker acquired OrthoSensor, integrating real-time intraoperative data analytics into arthroscopic workflows. These initiatives enhance procedural accuracy and outcomes, positioning Stryker as a leader in smart surgical ecosystems.

Smith & Nephew plc

Smith & Nephew has deepened its engagement in the Asia Pacific market by advancing its biologics and repair solutions portfolio tailored to sports injury recovery. The company launched its INDIBA ACTIV Pro system across Southeast Asia, a radiofrequency-based therapy device proven to accelerate soft tissue healing, gaining traction in professional sports clinics. It also expanded its 3D-printed suture anchor line, specifically designed for rotator cuff and ACL repairs, in collaboration with surgeons in Japan and South Korea. Smith & Nephew actively supports the Asia Pacific Knee Society through educational grants and clinical workshops. In 2024, it initiated a tele-rehabilitation pilot in India, integrating its recovery devices with mobile health platforms.

Top Strategies Used by Key Market Participants

Key players in the Sports Medicine Market predominantly adopt strategies such as product innovation, strategic partnerships, geographic expansion, acquisitions, and clinical education programs. Companies invest heavily in R&D to develop bioabsorbable implants, smart braces, and AI-integrated surgical tools. Collaborations with sports federations and medical societies enhance credibility and adoption. Geographic penetration into emerging markets like India and Southeast Asia is achieved through localized manufacturing and distribution alliances. Acquisitions of niche technology firms enable integration of digital health and real-time monitoring capabilities. Additionally, establishing training centers and surgeon outreach programs ensures clinical familiarity with proprietary devices, which is fostering long-term brand loyalty and procedural standardization across diverse healthcare settings.

RECENT MARKET HAPPENINGS

- In January 2023, Arthrex launched its FiberTape® Suture Anchor System in Japan, enhancing soft tissue fixation capabilities for shoulder and knee repairs, which supported by clinical training programs for orthopedic surgeons across the country.

- In June 2023, Stryker partnered with the Australian Institute of Sport to integrate its Mako robotic technology into athlete rehabilitation protocols by improving precision in post-injury joint restoration and strengthening clinical adoption.

- In September 2023, Smith & Nephew introduced the INDIBA ACTIV Pro therapy device in Thailand and Malaysia, which is expanding its non-invasive recovery solutions portfolio for professional sports clinics and rehabilitation centers.

- In February 2024, Zimmer Biomet collaborated with a Singapore-based AI startup to develop an algorithm-driven platform for predicting ACL injury risk using biomechanical data from wearable sensors.

- In May 2024, Conmed Corporation expanded its arthroscopy manufacturing facility in Pune, India, to meet rising regional demand for surgical instruments and reduce supply chain dependencies in the Asia Pacific market.

MARKET SEGMENTATION

This research report on the global sports medicine market has segmented & sub-segmented the market based on the product, application, and region.

By Product

- Reconstruction and Repair

- Implants

- Prosthetics

- Arthroscopy Devices

- Fracture and Ligament Repair Products

- Orthobiologics

- Support and Recovery

- Braces and Support

- Thermal Therapy Products

- Topical Pain Relief Products

- Compression Clothing

- Monitoring Devices

- Other Body Support and Recovery Products

- Accessories

By Application

- Head Injuries

- Shoulder Injuries

- Elbow and Wrist Injuries

- Back and Spine Injuries

- Hip and Groin Injuries

- Knee Injuries

- Foot and Ankle Injuries

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

Does this report include the impact of COVID-19 on the sports medicine market?

Yes, we have studied and included the COVID-19 impact on the global sports medicine market in this report.

Which segment by product type led the sports medicine market in 2024?

By Product Type, the Reconstruction and repair segment led the sports medicine market in 2024.

Which are the major players operating in the sports medicine market?

Smith & Nephew PLC, Arthrex, Inc., össur hf, Stryker Corporation, Conmed Corporation, Zimmer Biomet Holdings, Inc., Breg, Inc., Mueller Sports Medicine, Inc., Tornier, Inc., Skins International Trading AG, Wright Medical Technology, Inc., DePuy Mitek, Inc., 3M Company Ace Brand, OttoBock Healthcare GmbH and DJO Global, Inc. are some of the prominent companies in the global sports medicine market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com