Global Telehealth Market Size, Share, Trends & Growth Forecast Report By Component (Services, Software and Hardware), Delivery Mode (Web-based, Cloud-Based and On-premises), End Users (Providers, Patients, Payers and Others) and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2025 To 2033.

Global Telehealth Market Size

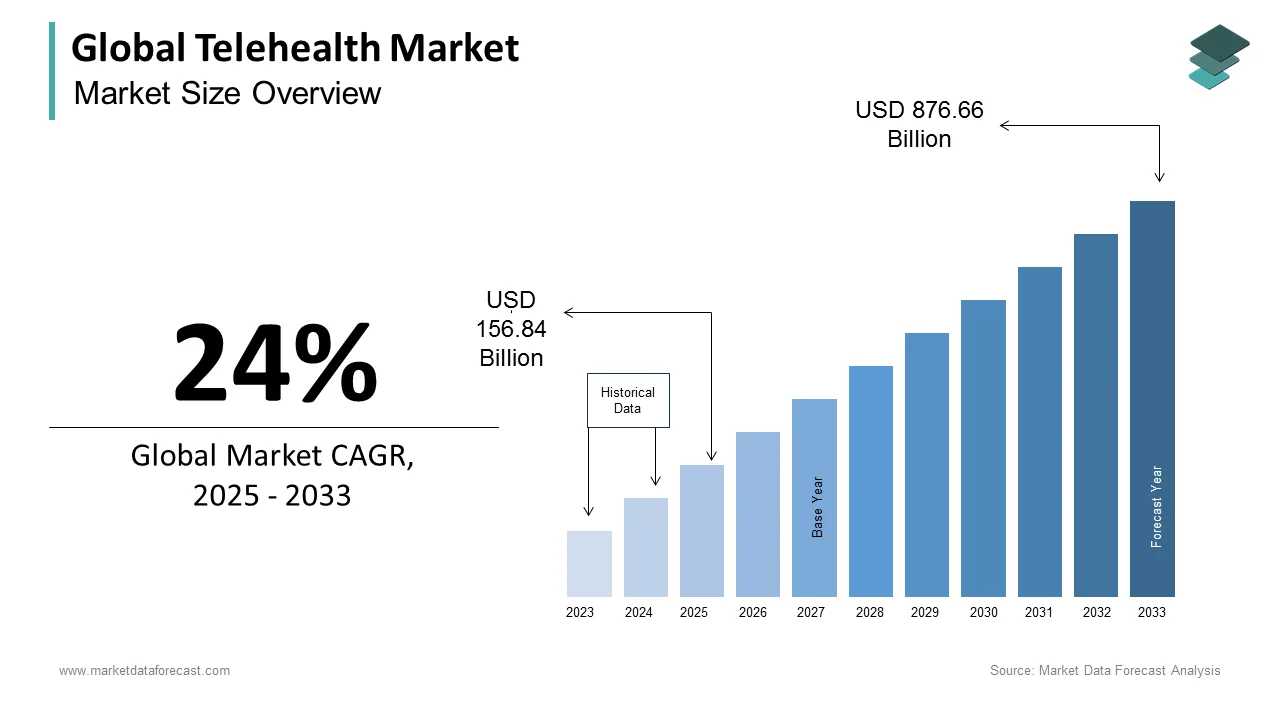

The size of the global telehealth market was worth USD 126.48 billion in 2024. The global market is anticipated to grow at a CAGR of 24% from 2025 to 2033 and be worth USD 876.66 billion by 2033 from USD 156.84 billion in 2025.

Telehealth is the delivery of clinical, diagnostic, and wellness services through digital communication platforms, including real-time video consultations, remote patient monitoring (RPM), and asynchronous messaging systems. It extends beyond virtual visits to include mobile health applications, store-and-forward imaging, and AI-driven triage tools that facilitate care continuity across geographies. As healthcare systems confront physician shortages and rising chronic disease burdens, telehealth has evolved from a convenience to a structural component of care delivery. According to the World Health Organization, 83% of member states had implemented national telehealth policies by 2023, reflecting institutional recognition of its public health value. The U.S. Health Resources and Services Administration reports that over 88 million Americans live in areas designated as medically underserved.

MARKET DRIVERS

Rising Chronic Disease Burden Driving Telehealth Adoption

The escalating prevalence of chronic diseases requiring continuous monitoring and frequent clinical touchpoints is leveraging the growth of the Telehealth Market. The World Health Organization states that non-communicable diseases such as diabetes, hypertension, and heart failure account for 74% of global deaths annually, with affected individuals often requiring multidisciplinary care coordination. Telehealth platforms enable real-time transmission of vital signs such as glucose levels, blood pressure, and ECG data by allowing clinicians to intervene proactively. As per the American Heart Association, remote monitoring of heart failure patients reduced 30-day hospital readmissions by 24% in a 2023 multi-center trial. The International Diabetes Federation reports that 537 million adults live with diabetes, a condition where regular virtual consultations improve medication adherence and glycemic control. Additionally, the Centers for Disease Control and Prevention notes that 60% of U.S. adults have at least one chronic condition, which is creating sustained demand for accessible, longitudinal care models that telehealth uniquely supports.

Growing Integration of Telehealth in Corporate Wellness Programs

The integration of telehealth into employer-sponsored and corporate wellness programs, transforming it into a standard employee benefit is also escalating the growth of the Telehealth Market. The Society for Human Resource Management states that 71% of large U.S. employers offered telehealth services as part of their health plans in 2023, up from 38% in 2019. Companies such as Amazon and Walmart have deployed in-house virtual clinics to reduce absenteeism and lower healthcare expenditures. According to the Kaiser Family Foundation, employers saved an average of $120 per telehealth visit compared to in-person primary care, primarily due to reduced overhead and travel costs. In Europe, Germany’s Techniker Krankenkasse and France’s CNP Santé have partnered with digital health providers to offer virtual consultations to insured employees.

MARKET RESTRAINTS

Digital Divide and Limited Accessibility Among Vulnerable Populations

The persistent digital divide among elderly, low-income, and rural populations who lack reliable internet access or digital literacy is limiting the growth of the telehealth market. According to the U.S. Federal Communications Commission, 14.5 million Americans still lack access to broadband speeds deemed adequate for video consultations. The National Institute on Aging reports that only 42% of adults over 75 in the United States use telehealth, citing difficulties with device navigation and audiovisual connectivity. In low- and middle-income countries, the World Bank notes that 3.7 billion people remain offline, limiting telehealth’s reach despite mobile penetration.

Inconsistent Reimbursement Policies Limiting Telehealth Scalability

The inconsistency in reimbursement policies across public and private payers, which creates financial uncertainty for providers and limits service scalability is also inhibiting the growth of the telehealth market. While the U.S. Centers for Medicare & Medicaid Services expanded telehealth coverage during the pandemic, long-term payment parity remains unresolved. The Commonwealth Fund reports that as of 2023, only 23 states had enacted permanent telehealth reimbursement parity laws for private insurers. In Europe, the European Commission notes that cross-border teleconsultations are rarely reimbursed under national health systems, discouraging pan-European service models.

MARKET OPPORTUNITIES

AI and Wearable Integration Enabling Predictive Telehealth Ecosystems

The adoption of the telehealth with artificial intelligence and wearable biometrics to create proactive, predictive care ecosystems is major factor to enhance new growth opportunities for the telehealth market. The U.S. Food and Drug Administration has cleared over 200 AI-powered diagnostic algorithms for use in virtual care settings, including tools for detecting atrial fibrillation and diabetic retinopathy from patient-generated data. According to the Consumer Technology Association, global shipments of health-tracking wearables surpassed 200 million units in 2023, with devices like smartwatches and glucose monitors feeding real-time data into telehealth platforms. The Mayo Clinic’s 2023 pilot program demonstrated that AI triage tools reduced emergency department overutilization by 18% by redirecting low-acuity cases to virtual care. Furthermore, the National Institutes of Health’s All of Us Research Program is integrating wearable data with EHRs to personalize virtual care pathways.

Rising Adoption of Telehealth in Mental and Behavioral Health

The expansion of telehealth into mental health and behavioral wellness, a domain where virtual delivery offers unique advantages in privacy, accessibility, and stigma reduction is also to leverage the growth of the telehealth market. The World Health Organization reports that 1 in 8 people globally live with a mental health disorder, yet two-thirds go untreated due to provider shortages and social barriers. Teletherapy platforms like BetterHelp and Talkspace have demonstrated clinical efficacy; a 2023 study in JAMA Psychiatry found that video-based cognitive behavioral therapy achieved remission rates comparable to in-person sessions for mild-to-moderate depression. In the U.S., the Substance Abuse and Mental Health Services Administration notes that telehealth accounted for 37% of all mental health visits in 2023. Employers and insurers are increasingly covering virtual mental health services, with UnitedHealthcare reporting a 45% increase in teletherapy utilization between 2022 and 2023.

MARKET CHALLENGES

Clinical Quality Variability and Regulatory Gaps in Telehealth Platforms

The variability in clinical quality and regulatory oversight for direct-to-consumer platforms operating across jurisdictions is to pose new challenge for the growth of the telehealth market. The U.S. Federal Trade Commission received over 12,000 consumer complaints in 2023 related to telehealth services, including concerns about misdiagnosis, inadequate follow-up, and lack of provider credentials verification. The Journal of the American Medical Association published a 2023 investigation revealing that 30% of online dermatology consultations failed to recommend biopsy for visible melanomas in test cases. Regulatory bodies struggle to keep pace with rapid platform proliferation; as per the World Health Organization, only 40 of 194 countries have specific licensing frameworks for cross-border telehealth providers.

Clinician Burnout and Workflow Strain in Virtual Care Delivery

The clinician burnout associated with the blurring of professional boundaries in virtual care environments is additionally to limit the growth of the telehealth market. A 2023 survey by the American Medical Association found that 58% of physicians providing telehealth reported increased fatigue due to extended screen time, after-hours messaging, and lack of physical separation between work and home. The Agency for Healthcare Research and Quality notes that EHR documentation time increased by 15% for telehealth visits due to heightened need for detailed digital notes. Additionally, the absence of non-verbal cues can increase diagnostic uncertainty, requiring longer consultations to compensate.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Component, Delivery, End Users, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Market Leaders Profiled | American Well, GlobalMed, Teladoc Health, Inc., Dictum Health Inc., InTouch Technologies, Inc., Doctor on Demand, Inc., MDLIVE Inc., Encounter Telehealth, HelloMD, SnapMD, Inc, and Others.. |

SEGMENTAL ANALYSIS

By Component Insights

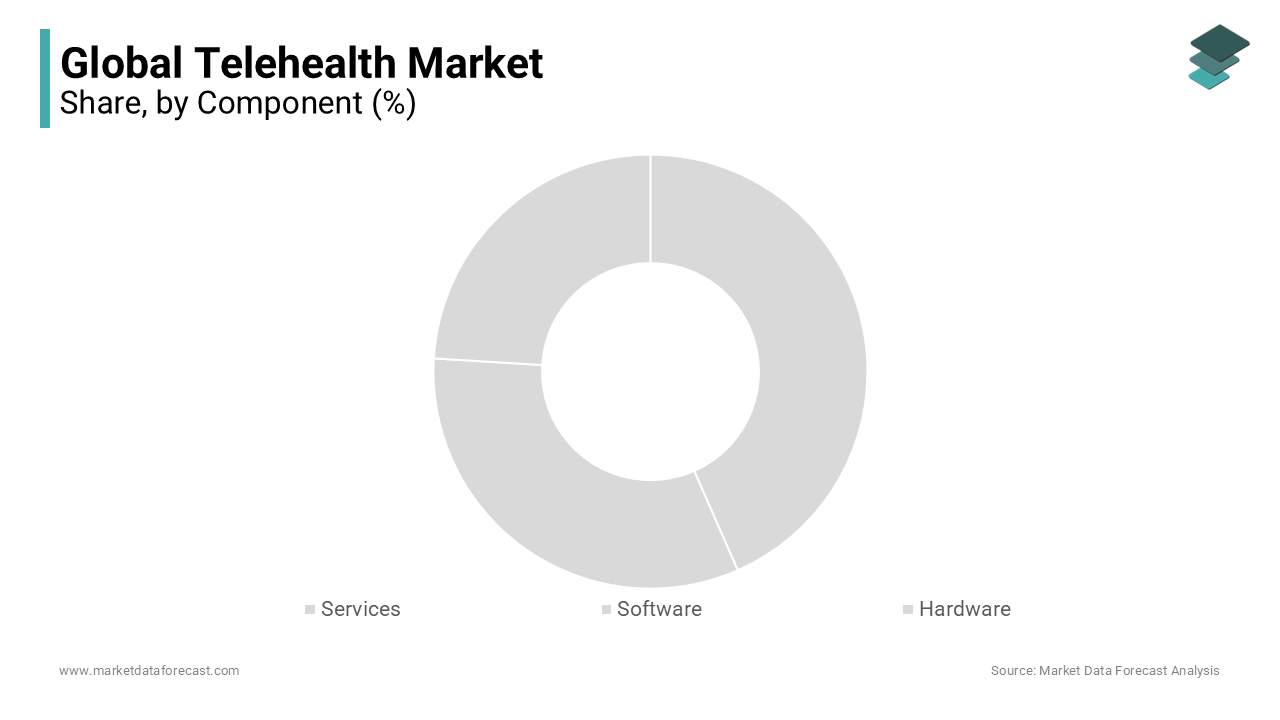

The services segment dominated the global telehealth market by accounting for 48.3% of the telehealth market share in 2024 with the increasing demand for remote patient monitoring, virtual consultations, and chronic disease management support. According to the Centers for Disease Control and Prevention (CDC), six in ten adults in the U.S. live with at least one chronic disease, driving demand for continuous care delivery via telehealth services. Additionally, the integration of telehealth into mainstream care models has expanded service offerings. For instance, the American Medical Association notes that over 80% of healthcare organizations now offer some form of telehealth services, reinforcing the sector’s dominance.

The telehealth software segment is projected to register a CAGR of 22.3% during the forecast period due to the digital transformation of healthcare systems and the urgent need for interoperable platforms. Also, the widespread adoption of Electronic Health Records (EHRs) integrated with telehealth capabilities is to leverage the growth of the segment. According to a 2023 report by the Office of the National Coordinator for Health IT (ONC), over 96% of non-federal acute care hospitals in the U.S. use certified EHR systems, many of which now include built-in telehealth modules.

By Delivery Mode Insights

The cloud-based delivery segment was the largest by occupying 55.3% of the telehealth market in 2024 with the scalability, cost-efficiency, and ease of integration with existing healthcare IT systems. Unlike on-premises solutions, cloud platforms eliminate the need for heavy capital investment in servers and IT staff. Security and compliance advancements have further boosted confidence in cloud platforms. Amazon Web Services (AWS) and Microsoft Azure, which host major telehealth platforms, are now fully HIPAA-compliant and offer end-to-end encryption. The U.S. Department of Health and Human Services confirms that no major HIPAA breaches have been attributed to compliant cloud infrastructure in the past three years, dispelling earlier concerns.

The web-based telehealth delivery mode segment is ascribed to witness a CAGR of 20.8% in coming years. WebRTC (Web Real-Time Communication) technology now enables high-quality video consultations without plugins. Google’s 2023 analysis shows that WebRTC supports over 2 billion devices globally, enabling seamless telehealth access on laptops, tablets, and smart TVs. Additionally, web-based platforms reduce IT overhead for providers. A 2022 KLAS Research study found that health systems using web-based telehealth reduced deployment time by 50% compared to native apps.

By End Users Insights

The healthcare segment held 52.3% of the global telehealth market share in 2024 with the integration of telehealth into clinical workflows and the operational necessity for scalable care delivery. Hospitals and clinics are investing heavily in telehealth infrastructure to expand reach and reduce overhead. According to the American Hospital Association, 93% of U.S. hospitals now use telehealth in some capacity, with large health systems like Kaiser Permanente conducting over 50% of their outpatient visits virtually in 2023.

The payers insurance companies and managed care organizations segment is swiftly emerging with an anticipated CAGR of 23.1% from 2025 to 2033 with the shift from fee-for-service to value-based care models, where payers are incentivized to reduce costs and improve outcomes.

REGIONAL ANALYSIS

North America Telehealth Market Analysis

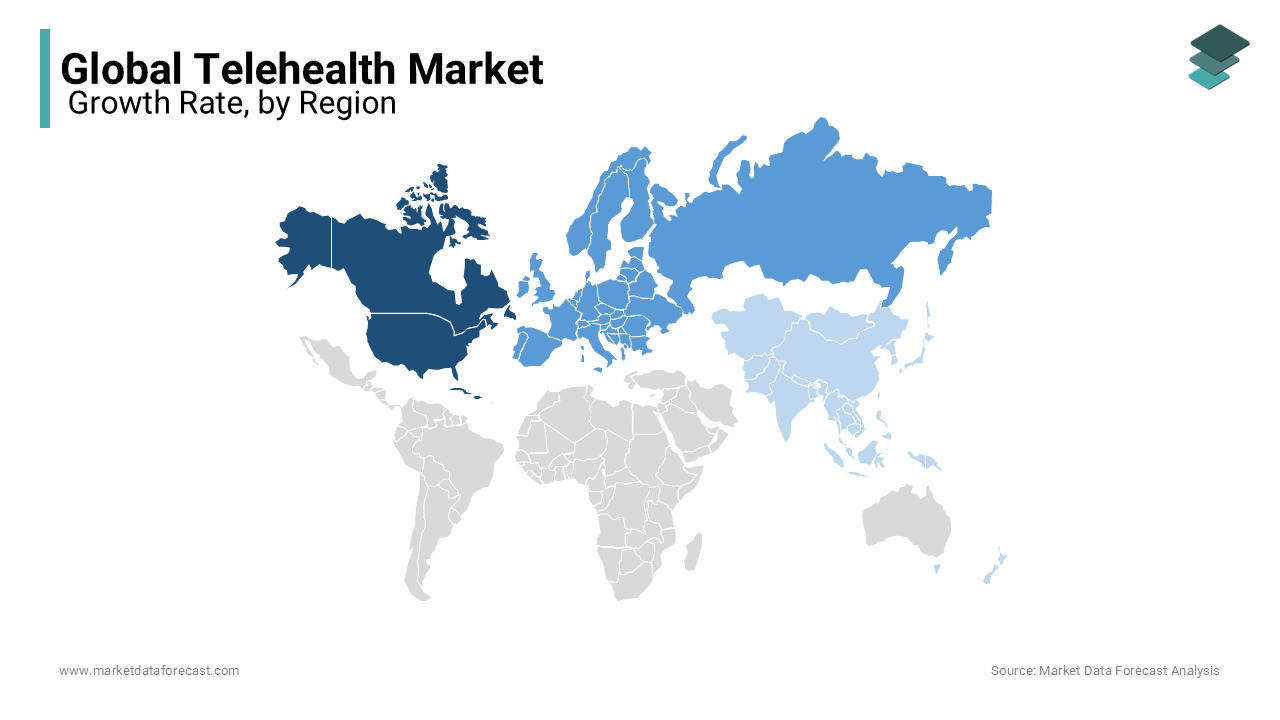

North America was the top performer of the global telehealth market with 45.3% of the share in 2024 with the anchored in advanced digital infrastructure, strong regulatory support, and high healthcare spending. The U.S., in particular, has seen explosive telehealth adoption, with telehealth visits reaching 1.9 billion in 2022, as reported by the CDC. Regulatory momentum continues: the 2023 Consolidated Appropriations Act extended Medicare telehealth flexibilities through 2024.

Europe Telehealth Market Analysis

Europe was ranked second in the telehealth market with 23.3% of share in 2024 with EU digital health initiatives and national e-health strategies. The European Commission’s Digital Health Platform supports cross-border telehealth services, with 24 member states now implementing e-prescriptions and virtual consultations. The UK’s National Health Service (NHS) has also scaled virtual care NHS Digital reports that over 25 million video consultations were delivered in 2022, a 300% increase from 2020. Data privacy under GDPR has encouraged secure platform development, while countries like Sweden and Denmark boast near-universal broadband access, enabling equitable telehealth reach.

Asia Pacific Telehealth Market Analysis

The Asia Pacific region telehealth market growth is fueled by massive unmet healthcare demand and mobile-first populations. India’s National Digital Health Mission (NDHM) has linked over 500 million health records digitally, enabling teleconsultations across 300,000 Ayushman Bharat centers, as per the Ministry of Health and Family Welfare. In rural areas of Indonesia and the Philippines, telehealth startups like Halodoc and KonsultaMD are bridging care gaps.

Latin America Telehealth Market Analysis

Latin America telehealth market is expected to have steady opportunities with Brazil and Mexico leading regional adoption. The region’s growth is propelled by public-private partnerships and rising smartphone use. Brazil’s Ministry of Health launched the Telessaúde Brasil Redes program, supporting over 30,000 monthly teleconsultations across 2,000 municipalities, according to the Pan American Health Organization (PAHO). Mexico’s telehealth market grew by 38% in 2022, driven by startups like Kaila and Teladoc’s regional expansion.

Middle East & Africa Telehealth Market Analysis

The Middle East and Africa telehealth market growth is likely to grow eventually with promientn opportunities in the next coming years. According to the Dubai Health Authority, over 2 million teleconsultations were conducted in 2022, supported by AI-powered platforms like Doctor for Every Citizen. Saudi Arabia’s Vision 2030 includes a $4.7 billion investment in digital health, with the Ministry of Health conducting over 10 million virtual visits in 2023. In Africa, telehealth is emerging as a lifeline Nigeria’s Helium Health and Kenya’s mPharma are digitizing clinics across 15 countries. The World Health Organization estimates that Africa has only 2.3 health workers per 1,000 people, making telehealth essential for coverage.

COMPETITIVE LANDSCAPE

The telehealth market is marked by intense competition driven by rapid technological innovation, evolving regulatory landscapes, and increasing demand for accessible care. Established players like Teladoc and Amwell compete with regional giants such as Ping An Good Doctor and emerging local startups offering niche solutions. Differentiation arises through AI integration, platform usability, and strategic alliances with payers and providers. The shift toward value-based care and post-pandemic normalization of virtual visits has intensified the race for clinical efficacy and scalability. Companies are investing heavily in interoperability, cybersecurity, and mobile-first designs to capture diverse demographics. While North America remains saturated, Asia Pacific and Africa present high-growth battlegrounds where first-mover advantages and localization determine success. This dynamic environment fosters continuous innovation by making the telehealth space one of the most competitive in digital health.

KEY MARKET PLAYERS

- American Well

- GlobalMed

- Teladoc Health, Inc.

- Dictum Health Inc.

- InTouch Technologies, Inc.

- Doctor on Demand, Inc.

- MDLIVE Inc.

- Encounter Telehealth

- HelloMD

- SnapMD, Inc.

TOP LEADING PLAYERS IN THE MARKET

- Teladoc Health has established a significant footprint in the Asia Pacific telehealth landscape by forging strategic partnerships and localized service offerings. In 2023, the company expanded into Japan through a collaboration with Sony Group Corporation to launch a joint venture, Teladoc Health Japan, aimed at delivering virtual care to Japanese employers and health plans. The platform offers 24/7 access to medical consultations, mental health support, and chronic care management tailored to regional needs. Teladoc has also integrated AI-driven triage tools to enhance user experience.

- Ping An Good Doctor is a leading digital health platform in China, plays a pivotal role in shaping telehealth adoption across Asia Pacific. Leveraging artificial intelligence and big data, the company provides end-to-end services including online consultations, prescription delivery, and (health management). In 2023, it deepened its integration with Ping An Insurance to offer bundled health plans, enhancing patient retention. The platform reported over 1.4 billion annual consultations, primarily in China, serving as a model for scalable telehealth in densely populated regions. It has also expanded into Southeast Asia by supporting digital transformation for clinics in Indonesia and Vietnam.

- Amwell has intensified its presence in the Asia Pacific market by focusing on enterprise-level collaborations and technology licensing. In 2022, the company partnered with Australia’s Medinet to power virtual care for over 1,000 clinics, enabling secure, real-time video consultations across rural and metropolitan areas. Amwell’s platform supports interoperability with local EHR systems, ensuring smooth clinical workflows. In 2023, it launched a white-label telehealth solution for Japanese healthcare providers, aligning with the country’s digital health reforms. The company also collaborated with Singapore-based NTUC Health to pilot remote monitoring for elderly patients. By offering scalable, compliant, and clinician-friendly platforms, Amwell is positioning itself as a B2B enabler rather than a direct-to-consumer provider.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the telehealth market are deploying strategic partnerships, technology integration, geographic expansion, M&A activity, and platform interoperability to strengthen their positions. Collaborations with insurers, hospitals, and tech firms enable seamless care delivery and broader user access. Integration of AI and EHR systems enhances diagnostic accuracy and workflow efficiency. Companies are expanding into emerging markets, particularly in the Asia Pacific and Latin America, to tap underserved populations.

GLOBAL TELEHEALTH MARKET NEWS

- In January 2023, Teladoc Health launched a joint venture with Sony Group in Japan named Teladoc Health Japan, aiming to deliver integrated virtual care services to employers and health plans across the country.

- In September 2023, Amwell partnered with Medinet in Australia to power virtual care for over 1,000 primary care clinics, enhancing access to telehealth in both urban and rural regions.

- In July 2022, Ping An Good Doctor expanded its AI-powered consultation services into Indonesia and Vietnam, supporting digital transformation for thousands of clinics in Southeast Asia.

- In March 2023, Philips integrated its telehealth platform with India’s National Digital Health Mission, enabling secure exchange of health records and virtual consultations across Ayushman Bharat centers.

MARKET SEGMENTATION

This research report on the global telehealth market has been segmented and sub-segmented based on component, delivery, end-users, and region.

By Component

- Services

- Remote Monitoring

- Real-Time Interactors

- Store And Forward Consulting

- Software

- Integrated

- Standalone

- Hardware

- Monitors

- Medical Peripheral Devices

- Blood Pressure Monitors

- Blood Glucose Meters

- Weight Scales

- Pulse Oximeters

- Peak Flow Meters

- ECG Monitors

- Others

By Delivery

- Web-based

- Cloud-Based

- On-premise

By End Users

- Providers

- Patients

- Payers

- Other End Users

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

1. What is the Telehealth Market?

The Telehealth Market comprises digital health services that deliver medical care remotely using technologies like video consultations, mobile health apps, and remote patient monitoring to enhance healthcare accessibility and efficiency

2. Which regions dominate the Telehealth Market?

North America leads with about 46.58% market share in 2024, followed by Europe and fast-growing Asia Pacific markets

3. What are the main growth drivers for the Telehealth Market?

Drivers include rising demand for accessible healthcare, chronic disease management needs, smartphone and internet penetration, government support, and cost efficiency

4. What are the key telehealth service types?

Services include virtual consultations, remote patient monitoring, tele-radiology, tele-ICU, mental health teletherapy, and mobile health applications

5. Who are the leading companies in the Telehealth Market?

Key players include Teladoc Health, Amwell, Doctor on Demand, Cerner Corporation, Siemens Healthineers, Medtronic, and Philips

6. How did COVID-19 impact the Telehealth Market?

COVID-19 significantly accelerated telehealth adoption globally by enabling remote care, reducing infection spread, and supporting healthcare system resilience

7. How is AI integrated into the Telehealth Market?

AI powers predictive diagnostics, virtual assistants, personalized care plans, clinical decision support, and enhanced remote patient monitoring

8. What role does telehealth play in rural healthcare?

Telehealth improves access in underserved rural areas by connecting patients to specialists and reducing geographic barriers

9. What challenges does the Telehealth Market face?

Challenges include data privacy concerns, technology adoption barriers, regulatory variations, reimbursement complexities, and digital literacy gaps

10. How is telehealth enhancing mental health care?

Teletherapy and digital mental health apps provide accessible, confidential support, addressing increasing demand for behavioral health services

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com