U.S. Cigarette Market Size, Share, Trends & Growth Forecast Report By Type (Light, Medium, and Others), Distribution Channel, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Cigarette Market Report Summary

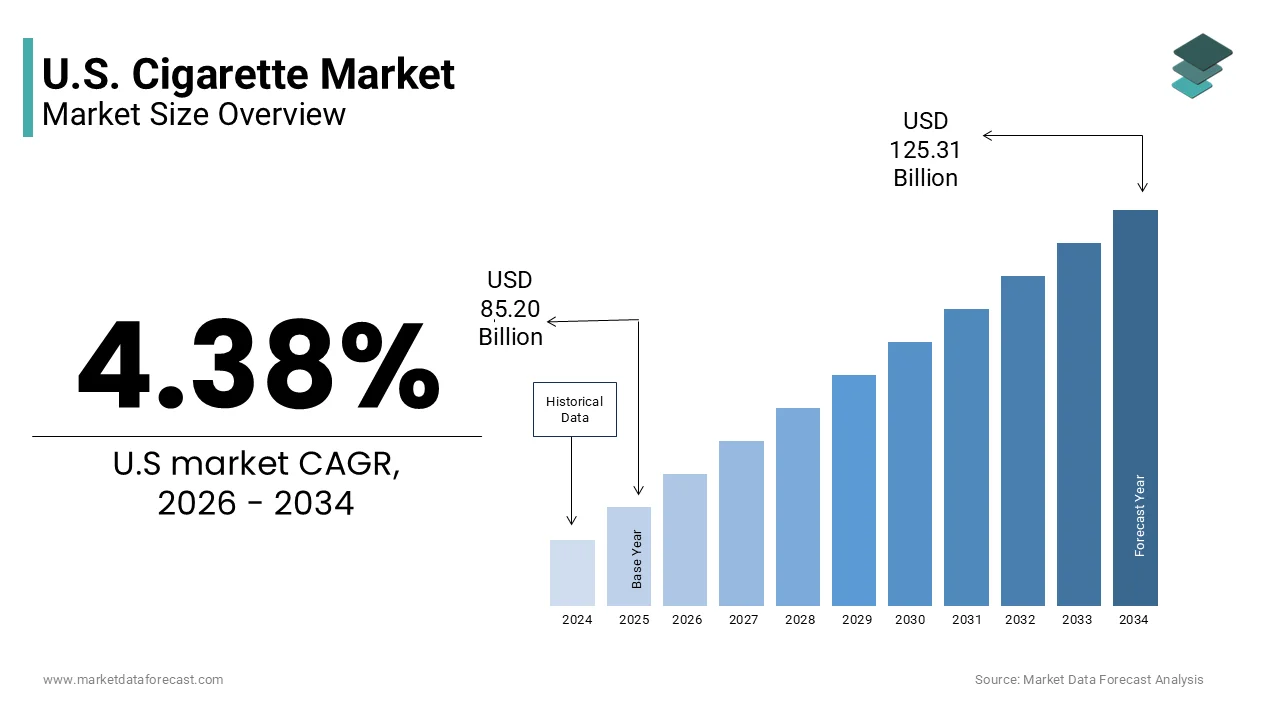

The U.S. cigarette market was valued at USD 85.20 billion in 2025, is estimated to reach USD 88.93 billion in 2026, and is projected to reach USD 125.31 billion by 2034, growing at a CAGR of 4.38% during the forecast period. Market growth is influenced by stable demand among existing consumers, pricing strategies, and product segmentation. Despite regulatory pressures and rising health awareness, the market continues to generate steady revenue through premiumization and brand loyalty. The presence of established distribution networks and consistent retail availability is further supporting market stability.

Key Market Trends

- Stable demand among existing consumers is sustaining market growth.

- Increasing product premiumization is boosting revenue generation.

- Strong retail distribution through convenience stores is supporting accessibility.

- Regulatory frameworks and health awareness are shaping consumption patterns.

- Brand loyalty and product differentiation are influencing purchasing behavior.

Segmental Insights

- Based on type, the full flavor or regular cigarette segment held a dominant share of the U.S. cigarette market in 2025, driven by long standing consumer preference and established product positioning.

- Based on distribution channel, the convenience stores segment accounted for 40.1% of the U.S. cigarette market share in 2025, supported by widespread availability and ease of purchase.

Competitive Landscape

The U.S. cigarette market is highly concentrated, with major players focusing on brand strength, pricing strategies, and distribution efficiency to maintain their market position. Companies are also adapting to regulatory changes and evolving consumer behavior. Key players in the U.S. cigarette market include Altria Group, Inc., Reynolds American Inc., Imperial Brands Plc, Vector Group Ltd., and Japan Tobacco International.

U.S. Cigarette Market Size

The U.S. cigarette market was valued at USD 85.20 billion in 2025, is estimated to reach USD 88.93 billion in 2026, and is projected to reach USD 125.31 billion by 2034, growing at a CAGR of 4.38% from 2026 to 2034.

The cigarette is entrenched consumer habits and significant regulatory scrutiny. As per the Centers for Disease Control and Prevention, approximately 11.5% of US adults were current cigarette smokers in 2023, which translates to roughly 28 million individuals. The controlled legal framework that mandates warning labels, restricts advertising channels, and imposes substantial excise taxes. The federal taxes generate billions in revenue annually by reflecting the dual role of cigarettes, as both a consumer good and a fiscal instrument. Consumer loyalty remains high among long term users, although the demographic profile is shifting toward older age groups and lower income brackets. The definition of this market now increasingly intersects with alternative nicotine delivery systems, yet traditional cigarettes retain distinct regulatory and consumption patterns that differentiate them from emerging products.

MARKET DRIVERS

Persistent Nicotine Addiction Sustains Core Consumer Base

The powerful physiological and psychological dependence on nicotine inherent in combustible tobacco products is boosting the growth of the United States cigarette market. Nicotine acts as a potent stimulant that affects the central nervous system, creating a cycle of craving and relief that makes cessation extremely difficult for regular users. The nicotine addiction is comparable in strength to dependencies on heroin or cocaine, which explains the high relapse rates among those attempting to quit. This retention rate provides manufacturers with a predictable revenue stream from loyal customers who prioritize their habit over cost considerations. Furthermore, the ritualistic aspects of smoking, such as taking breaks or socializing, reinforce behavioral patterns that are resistant to change. Consequently, even as overall participation rates decline, the intensity of consumption among remaining smokers often remains stable or increases, thereby offsetting volume losses with maintained or higher per unit profitability.

Price Inelasticity Among Dedicated Smokers Supports Revenue Stability

The price inelasticity of demand among dedicated smokers, which allows manufacturers to pass on tax increases and production costs without proportional drops in sales volume is additionally bolstering the growth of United States cigarette market. Economic studies consistently show that while higher prices deter initiation among youth and occasional users, they have a limited impact on heavy, addicted adult smokers. This financial resilience enables tobacco companies to maintain robust profit margins even in a shrinking volume environment. The premium brand segments often outperform value brands during periods of economic uncertainty, suggesting that brand loyalty and perceived quality outweigh price sensitivity for core consumers. The manufacturers to focus on premiumization strategies by introducing specialized blends or packaging that justify higher price points.

MARKET RESTRAINTS

Stringent Regulatory Frameworks Limit Product Accessibility and Appeal

The increasing stringent regulatory environment imposed by federal and state authorities, which aims to reduce smoking initiation and encourage cessation is hindering the growth of United States cigarette market. The Family Smoking Prevention and Tobacco Control Act grants the Food and Drug Administration broad authority to regulate the manufacture, marketing, and distribution of tobacco products. The recent initiatives, include mandatory graphic warning labels and restrictions on flavored tobacco products, which significantly diminish the appeal of cigarettes to potential new users. These regulations increase compliance costs for manufacturers and limit their ability to innovate or advertise freely. Additionally, local ordinances frequently ban smoking in public places, including parks, beaches, and outdoor dining areas, further restricting the contexts in which cigarettes can be consumed. According to the American Lung Association, more than 20 states and hundreds of localities have enacted comprehensive smoke free laws that cover nearly all indoor workplaces and public spaces. This social and legal marginalization reduces the convenience and social acceptability of smoking, thereby discouraging casual use and making it harder for smokers to maintain their habit without inconvenience.

Intensifying Public Health Campaigns Shift Social Norms Against Smoking

The relentless and effective nature of public health campaigns that have successfully shifted social norms against smoking is also degrading the growth of United States cigarette market. Decades of coordinated efforts by government agencies, non profit organizations, and healthcare providers have framed smoking as a dangerous and socially undesirable behavior. The Tips From Former Smokers campaign has reached millions of Americans that severe health consequences of tobacco use and motivating quitting attempts. The cultural shift is particularly pronounced among younger demographics, who view smoking with increasing stigma rather than rebellion or sophistication. The generational change ensures a shrinking pipeline of new customers, which threatens the long term viability of the market. Furthermore, healthcare providers routinely screen for tobacco use and offer cessation support, integrating anti-smoking messaging into standard medical care. The physician advice to quit is one of the most effective triggers for smoking cessation attempts.

MARKET OPPORTUNITIES

Expansion into Reduced Risk Products Offers Diversification Pathways

The strategic expansion into reduced risk products, such as e cigarettes and heated tobacco devices, which allow companies to retain nicotine consumers, while adapting to health conscious trends is setting up new opportunities for the growth of United States cigarette market. Major tobacco corporations are increasingly pivoting their portfolios to include these alternatives, positioning them as less harmful substitutes for combustible cigarettes. The investments in vaping technology and smoke free products have become central to their long term growth strategy, aiming to transition existing smokers to these newer formats. The Food and Drug Administration has authorized the marketing of several electronic nicotine delivery systems as appropriate for the protection of public health, providing a regulatory pathway for legitimate market entry. While youth vaping remains a concern, adult adoption of e cigarettes for cessation purposes is growing, with millions of former smokers citing vaping as their primary method for quitting combustibles.

Premiumization and Niche Branding Enhance Profit Margins

The pursuit of premiumization and niche branding strategies that cater to specific consumer segments willing to pay higher prices for perceived quality or exclusivity is additionally to leverage the growth opportunities for the growth of the United States cigarette market. As overall volumes decline, manufacturers can maintain profitability by focusing on high margin specialty products, such as organic tobacco, small batch blends, or luxury packaging. The approach allows companies to differentiate their offerings in a saturated market and build stronger emotional connections with loyal customers. Brands that emphasize craftsmanship, heritage, or unique flavor profiles can command price premiums that offset lower sales volumes. Additionally, targeting specific demographic niches, such as affluent urban professionals or rural traditionalists, enables tailored marketing efforts that resonate deeply with these groups. The spending on premium tobacco products has remained stable even as overall consumption drops, indicating a willingness among certain consumers to trade up.

MARKET CHALLENGES

Litigation Risks and Legal Liabilities Threaten Financial Stability

The persistent threat of litigation and substantial legal liabilities arising from health related claims and regulatory violations is one of the major challenges for the growth of United States cigarette market. Tobacco companies face ongoing lawsuits from individuals, state governments, and class action groups seeking compensation for smoking related illnesses and healthcare costs. As per the Campaign for Tobacco Free Kids, settlements from the Master Settlement Agreement and subsequent legal actions have cost the industry hundreds of billions of dollars by creating a significant financial burden that impacts profitability and shareholder value. These legal challenges not only result in direct monetary penalties but also require extensive resources for defense and compliance management. The risk of new litigation remains high as scientific understanding of tobacco related harms evolves and new evidence emerges regarding the addictiveness and toxicity of cigarette ingredients. The legal environment creates uncertainty for investors and complicates long term planning, as companies must set aside substantial reserves for potential future claims. The constant specter of litigation also damages corporate reputation by making it difficult to attract talent and engage in positive community relations, thereby isolating the industry further from mainstream business practices.

Supply Chain Volatility and Agricultural Constraints Impact Production

The volatility in the supply chain and agricultural constraints affecting the production of high quality tobacco leaf is also to hinder the growth of the United States cigarette market. Climate change, pest infestations, and fluctuating labor costs pose significant risks to tobacco farming, which is concentrated in specific regions such as Kentucky, North Carolina, and Virginia. As per the United States Department of Agriculture, extreme weather events like droughts and floods have increasingly disrupted crop yields, leading to inconsistencies in supply and quality. These disruptions force manufacturers to source tobacco from international markets, which introduces additional complexities related to tariffs, transportation logistics, and geopolitical instability. The reliance on imported leaf exposes companies to currency fluctuations and trade policy changes that can abruptly increase input costs. The rising production costs coupled with stagnant or declining sales volumes squeeze profit margins, requiring efficient operational management to maintain competitiveness. Furthermore, environmental regulations regarding pesticide use and water conservation impose additional constraints on farmers, potentially reducing available acreage for tobacco cultivation. This agricultural precarity undermines the stability of raw material supplies, making it challenging for manufacturers to guarantee consistent product quality and availability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.38% |

| Segments Covered | By Type, Distribution Channel, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | Altria Group, Inc., Reynolds American Inc., Imperial Brands Plc, Vector Group Ltd., and Japan Tobacco International |

SEGMENTAL ANALYSIS

By Type Insights

The full flavor or regular cigarette segment was the largest by holding a dominant share of the United States market in 2025 due to entrenched consumer preference for traditional taste profiles and higher nicotine delivery. Despite the proliferation of light and ultra light variants, a significant portion of smokers remains loyal to robust blends that provide immediate sensory satisfaction. The physiological expectation of heavy smokers, who associate stronger taste with effective nicotine intake. Data from the Federal Trade Commission indicates that while labeled tar and nicotine yields have decreased over decades, actual consumption behavior among regular smokers involves compensatory smoking, such as deeper inhalation, to maintain desired blood nicotine levels. This behavioral pattern reinforces the demand for full strength products. Furthermore, marketing restrictions have limited the ability of manufacturers to promote lighter alternatives as healthier options, causing many consumers to revert to familiar brands. The psychological comfort associated with legacy brands also plays a crucial role, as long term users resist changing their established routines.

The premium and specialty cigarette segment is likely to register a fastest CAGR of 12.2% from 2026 to 2034 with a strategic shift toward high margin niche products rather than volume expansion. While overall cigarette consumption declines, this segment experiences growth due to affluent consumers seeking differentiated experiences through organic tobacco, unique blends, and luxury packaging. The premium tobacco segment has demonstrated resilience with a compound annual growth rate that outpaces the broader market, attributed to trading up behaviors among remaining smokers. This growth is fueled by the perception of quality and exclusivity, where consumers are willing to pay significantly higher prices for products marketed as artisanal or natural. Manufacturers are leveraging this trend by introducing limited edition flavors and sustainable sourcing claims that appeal to environmentally conscious buyers. Additionally, the rise of boutique tobacco shops and specialized retail channels facilitates the discovery of these niche products by creating a dedicated customer base that values craftsmanship.

By Distribution Channel Insights

The convenience stores segment was the largest by holding 40.1% of the United States cigarette market share in 2025 owing to their unparalleled accessibility, extended operating hours, and strategic location near residential and commercial hubs. These outlets cater to the impulse buying behavior of smokers who prioritize immediate availability over price comparisons. The integration of cigarette sales into daily routines, such as purchasing fuel or snacks, which creates frequent touchpoints for consumers. The National Association of Convenience Stores reports that tobacco products remain a key traffic driver, with millions of transactions occurring monthly at these locations. Furthermore, convenience stores often lack the stringent checkout barriers found in larger retailers, allowing for quicker purchases that align with the urgent nature of nicotine cravings. Regulatory environments in many states also favor smaller retailers by limiting the density of large tobacco outlets, thereby preserving the market share of convenience chains. The ability of these stores to maintain localized inventory and offer personalized service further strengthens customer loyalty.

The online and direct to consumer segment is likely to witness a fastest CAGR of 8.3% from 2026 to 2034 with the digital adoption, home delivery convenience, and competitive pricing structures. Although, regulatory hurdles exist, the shift toward e commerce has enabled manufacturers and third party retailers to reach consumers directly, bypassing traditional retail markups. The adoption of age verification technologies has streamlined compliance by allowing legitimate online retailers to expand their customer base without violating federal laws. Additionally, subscription models and bulk purchase discounts available online provide economic incentives that attract cost conscious consumers facing high state taxes. The COVID 19 pandemic accelerated this trend by normalizing contactless shopping habits, which have persisted post pandemic. Manufacturers are investing in robust digital platforms to capture this demand, offering detailed product information and loyalty rewards that enhance user engagement.

COMPETITIVE LANDSCAPE

The competition in the United States cigarette market is characterized by an oligopolistic structure dominated by a few multinational corporations that control the majority of production and distribution. These entities engage in intense rivalry through brand differentiation pricing strategies and innovation in alternative nicotine products. The market exhibits high barriers to entry due to strict regulatory requirements substantial capital needs and established brand loyalty among consumers. Competitors focus on capturing value rather than volume by promoting premium brands and specialized blends that command higher margins. Legal battles over intellectual property and regulatory compliance further intensify the competitive landscape as firms seek to protect their interests. The shift toward smoke free alternatives has created a new arena for competition where technological superiority and scientific validation play crucial roles. Companies invest heavily in research and development to create proprietary devices and formulations that distinguish their offerings. Retail relationships remain critical as shelf space becomes increasingly contested among traditional and emerging products. Price wars are rare due to the inelastic nature of demand but promotional activities and loyalty incentives are common tactics used to attract and retain customers.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. cigarette market include

- Altria Group, Inc.

- Reynolds American Inc.

- Imperial Brands Plc

- Vector Group Ltd.

- Japan Tobacco International

Top Players in the Market

- Altria Group Inc stands as a dominant force in the United States tobacco industry with its flagship brand Marlboro leading consumer preference. The company focuses on maximizing value through premium pricing strategies and operational efficiency within its combustible cigarette portfolio. Altria has actively diversified its holdings by investing heavily in smoke free alternatives including e vaping devices and heated tobacco products. Recent initiatives involve expanding its oral tobacco segment with modern nicotine pouches that appeal to younger adult consumers seeking discreet options. The corporation continues to leverage its extensive distribution network to maintain shelf presence across convenience stores and retail outlets nationwide. Its strategic partnerships and internal innovation labs drive continuous product development aimed at retaining loyal smokers while attracting new users to reduced risk categories. This dual approach solidifies its leadership position without relying solely on declining combustible volumes.

- British American Tobacco plc operates as a major global player with significant influence in the United States market through its subsidiary Reynolds American Inc. The company manages iconic brands such as Camel Newport and Kool which retain strong cultural relevance among diverse demographic groups. British American Tobacco prioritizes transformation by shifting resources toward next generation products including vaporizers and modern oral nicotine solutions. Recent actions, include launching innovative device platforms that offer enhanced user experience and customization features to compete effectively in the evolving landscape. The firm emphasizes sustainability and responsible business practices to improve corporate reputation and engage with stakeholders concerned about environmental impact. Its commitment to reducing harm through science based product development positions it as a forward thinking leader. The company leverages global research capabilities to introduce novel formulations that meet changing consumer preferences while maintaining robust profitability from its established combustible portfolio.

- Japan Tobacco International maintains a notable presence in the United States market primarily through its acquisition of Reynolds American Inc assets and specific brand portfolios. The company focuses on niche segments and premium offerings that differentiate its products from mass market competitors. Japan Tobacco International invests in high quality tobacco sourcing and advanced blending techniques to deliver superior taste experiences for discerning smokers. Recent efforts involve expanding its presence in the fine cut tobacco and cigar categories which show resilience against broader market declines. The corporation utilizes sophisticated data analytics to understand consumer behavior and tailor marketing campaigns that resonate with target audiences. The company also explores strategic collaborations with technology firms to develop smart smoking devices that integrate digital connectivity. These initiatives reflect its commitment to innovation and adaptation in a rapidly changing regulatory environment. Japan Tobacco International continues to strengthen its brand equity through consistent quality and targeted promotional activities that enhance customer loyalty and drive sustainable growth.

Top Strategies Used by Key Market Participants

Key players in the United States cigarette market employ premiumization strategies to offset volume declines by increasing prices and introducing high end products. Companies focus on diversifying portfolios into reduced risk categories such as e cigarettes and nicotine pouches to capture health conscious consumers. Aggressive lobbying and legal defense mechanisms are utilized to navigate stringent regulatory frameworks and mitigate litigation risks. Manufacturers invest heavily in supply chain optimization to reduce costs and improve efficiency amid rising raw material expenses. Digital marketing and direct to consumer channels are expanded to reach younger demographics and bypass traditional retail restrictions. Strategic acquisitions and partnerships enable firms to access new technologies and broaden their product offerings quickly. Brand loyalty programs and personalized customer experiences are developed to retain existing users and enhance engagement levels. Sustainability initiatives are implemented to improve corporate image and comply with environmental standards.

MARKET SEGMENTATION

This research report on the U.S. cigarette market is segmented and sub-segmented into the following categories.

By Type

- Light

- Medium

- Others

By Distribution Channel

- Tobacco Shops

- Supermarkets and Hypermarkets

- Convenience Stores

- Online Stores

- Others

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com