United States Commercial Real Estate Market Size, Share, Trends & Growth Forecast Report Segmented By Business Model (Sales, Rental), Property Type, End-User and Country – Industry Analysis From 2026 to 204

United States Commercial Real Estate Market Report Summary

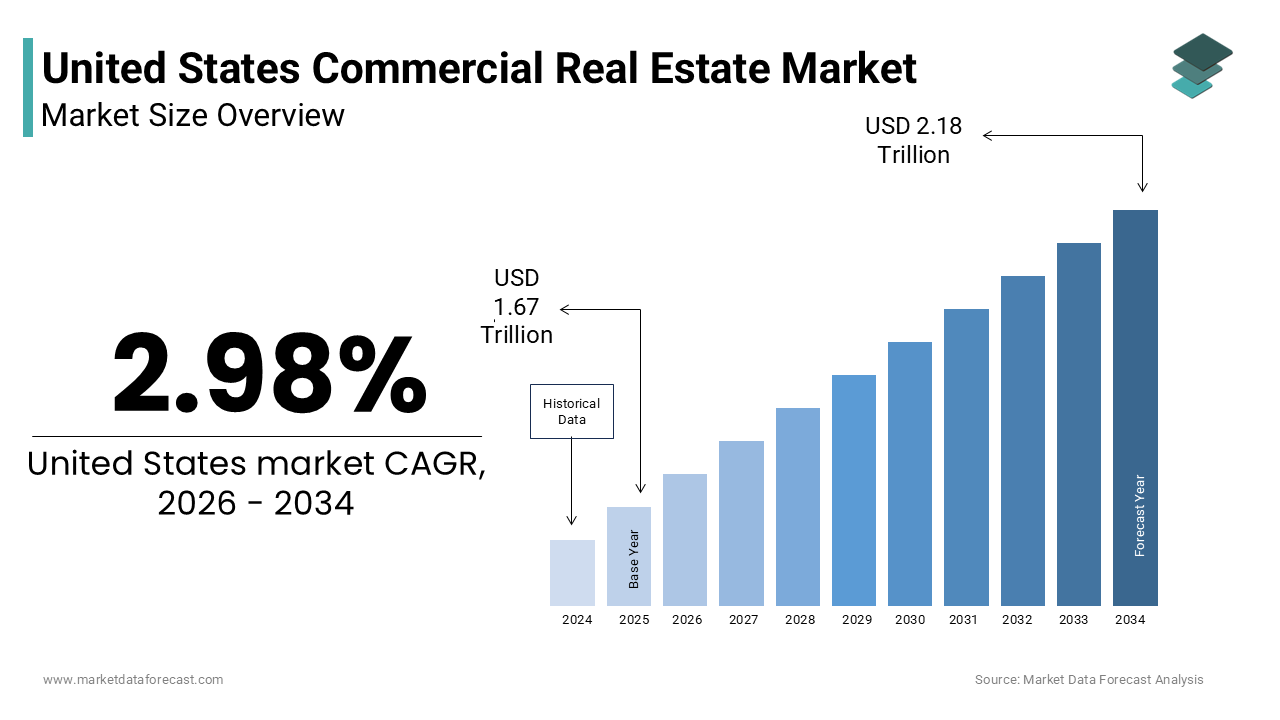

The United States commercial real estate market was valued at USD 1.67 trillion in 2025, is estimated to reach USD 1.72 trillion in 2026, and is projected to reach USD 2.18 trillion by 2034, growing at a CAGR of 2.98% during the forecast period from 2026 to 2034. The growth of the U.S. commercial real estate market is driven by the expansion of e-commerce and logistics infrastructure, increasing urban revitalization initiatives, and rising demand for mixed-use developments. Additionally, the integration of smart building technologies and sustainability practices is reshaping property development and asset management across the country.

Key Market Trends

- Rising demand for logistics and warehousing facilities driven by e-commerce growth

- Increasing focus on mixed-use developments and urban revitalization projects

- Growing adoption of smart building technologies and energy-efficient infrastructure

- Shift toward adaptive reuse of office spaces into residential or alternative assets.

- Expansion of data centers and digital infrastructure supporting cloud and AI growth

Segmental Insights

- Based on the business model, the rental segment was the largest and held a significant share of the United States commercial real estate market in 2025. The segment’s dominance is attributed to operational flexibility, lower upfront costs for businesses, and strong demand from institutional investors such as REITs generating stable rental income.

- Based on property type, the logistics segment accounted for the largest share of the market in 2025. This dominance is driven by the rapid expansion of e-commerce, demand for last-mile delivery facilities, and the increasing need for modern warehousing infrastructure with automation capabilities.

Regional Insights

The United States commercial real estate market is witnessing steady growth across major regions, supported by strong demand for industrial assets, urban redevelopment projects, and technological advancements in building management. Key metropolitan areas continue to attract investments due to high economic activity, infrastructure development, and demand for premium commercial spaces.

Competitive Landscape

The United States commercial real estate market is highly competitive, characterized by the presence of large institutional investors, global real estate service providers, and diversified property developers. Companies are focusing on portfolio diversification, sustainability initiatives, and digital transformation to strengthen their market positions. Prominent players in the United States commercial real estate market include CBRE Group, Inc., Jones Lang LaSalle Incorporated (JLL), Cushman & Wakefield plc, Colliers International Group Inc., Newmark Group, Inc., Marcus & Millichap, Inc., Hines, Tishman Speyer, Brookfield Asset Management, Blackstone Inc., Prologis, Inc., Simon Property Group, Inc., Equinix, Inc., Digital Realty Trust, Inc., and Vornado Realty Trust.

United States Commercial Real Estate Market Size

The United States commercial real estate market size was valued at USD 1.67 trillion in 2025 and is anticipated to reach USD 1.72 trillion in 2026 from USD 2.18 trillion by 2034, growing at a CAGR of 2.98% during the forecast period from 2026 to 2034.

The commercial real estate is property types, including office retail, industrial hospitality, and multifamily residential assets, utilized for business and income generating purposes. Regulatory frameworks at local and state levels govern zoning land use and building codes influencing development feasibility and operational costs. Environmental sustainability has become a central theme with increasing mandates for energy efficiency and carbon reduction in building operations. The integration of smart building technologies enhances operational efficiency and tenant experience. Stakeholders, including developers investors and tenants navigate these factors to optimize asset performance and value.

MARKET DRIVERS

Expansion of E-Commerce and Logistics Infrastructure Demand

The relentless growth of e-commerce serves, particularly within the industrial and logistics sectors, which is propelling the growth of United States commercial real estate market. Consumers increasingly prefer online shopping for convenience and variety leading to a surge in demand for warehousing distribution centers and last mile delivery facilities. According to the U.S. Census Bureau, e-commerce sales have maintained a significant portion of total retail sales necessitating robust supply chain infrastructure. Retailers and third-party logistics providers require modern facilities with high ceilings advanced automation capabilities and strategic locations near urban centers to ensure rapid delivery times. This shift has spurred construction activity in key logistics hubs across the country. The need for inventory redundancy and faster fulfillment speeds has further amplified the demand for industrial space. Companies are expanding their footprints to accommodate larger inventories and streamline operations. The scarcity of prime industrial land in major metropolitan areas has driven up rental rates and property values. The integration of technology in warehouses such as robotics and artificial intelligence requires specialized building designs. This evolution supports sustained demand for modern industrial properties.

Urban Revitalization and Mixed Use Development Trends

The urban revitalization initiatives and the rise of mixed-use developments is another attribute enhancing the growth of the United States commercial real estate market. Cities are increasingly focusing on creating vibrant live work play environments that attract residents businesses and tourists. According to the Urban Land Institute, mixed use projects that combine residential office retail and entertainment spaces are gaining popularity due to their ability to foster community engagement and reduce transportation needs. These developments maximize land use efficiency and create synergies between different property types. Municipalities offer incentives such as tax abatements and zoning adjustments to encourage redevelopment of underutilized areas. The demand for walkable neighborhoods with access to amenities drives leasing activity in these zones. Younger people, particularly millennials and Generation Z prefer urban lifestyles that offer convenience and social interaction. This preference supports demand for retail and hospitality components within mixed use complexes. The adaptability of mixed use properties allows them to withstand economic fluctuations better than single use assets. Investors are drawn to the diversified revenue streams provided by these projects. The focus on placemaking and experiential retail enhances the appeal of commercial spaces. Urban renewal projects also improve infrastructure and public services contributing to overall property value appreciation. This trend aligns with broader sustainability goals by promoting density and reducing urban sprawl. The continued investment in urban cores ensures steady demand for well located commercial assets.

MARKET RESTRAINTS

Rising Interest Rates and Financing Costs

The elevated interest rates and increased financing costs by affecting both acquisition and development activities is restraining the growth of United States commercial real estate market. The Federal Reserve monetary policy decisions aimed at combating inflation have led to higher borrowing costs for investors and developers. According to the Federal Reserve Bank of St. Louis, mortgage rates for commercial properties have risen significantly reducing the affordability of leverage dependent transactions. Higher debt service requirements compress capitalization rates and lower property valuations. Many potential buyers are sidelined as financing becomes less attractive or unavailable. Refinancing existing debt poses challenges for property owners facing maturity walls in a higher rate environment. This situation limits liquidity and slows down transaction volumes. Developers face increased costs for construction loans impacting project feasibility and profitability. Some projects are delayed or cancelled due to unfavorable financing conditions. The cost of capital influences investment decisions leading to a more cautious approach among institutional investors. Lenders have tightened underwriting standards requiring higher equity contributions and stricter financial metrics. This credit contraction restricts market activity and slows growth. The uncertainty surrounding future interest rate movements adds complexity to financial planning.

Remote Work Adoption and Office Space Utilization Decline

The widespread adoption of remote and hybrid work models, particularly in the office sector is also hindering the growth of United states commercial real estate market. Employees and employers have embraced flexible work arrangements reducing the need for traditional office space. Companies are downsizing their real estate footprints to cut costs and align with new operational models. This trend has resulted in increased vacancy rates and downward pressure on rents in many urban markets. Sublease availability has surged as firms seek to offload excess space. The demand for office space has shifted towards high quality amenity rich buildings, while older Class B and C properties face obsolescence. Property owners struggle to attract tenants and maintain revenue stability. The uncertainty regarding long term office demand discourages new construction and renovation investments. Cities reliant on office workers experience reduced foot traffic impacting retail and hospitality sectors. The structural shift in work habits challenges the traditional office lease model. Landlords must innovate by repurposing spaces or enhancing amenities to remain competitive.

MARKET OPPORTUNITIES

Adaptive Reuse and Conversion of Office Properties

The conversion of obsolete office buildings into residential or other uses is ascribed to boost the growth of United States commercial real estate market in coming years. As demand for office space declines, the need for housing in urban areas remains strong creating a viable pathway for asset repurposing. Converting office towers into apartments or condominiums allows owners to capture value from stranded assets. Municipalities support these initiatives through zoning changes and financial incentives to promote urban density and vibrancy. The structural characteristics of older office buildings such as large floor plates and window placements often suit residential conversions. This strategy reduces the environmental impact of demolition and new construction aligning with sustainability goals. Investors see potential in acquiring distressed office properties at discounted prices for conversion. The demand for urban living among younger demographics supports leasing and sales of converted units. Successful conversions require careful planning and significant capital investment but offer long term stability. The trend encourages innovation in design and construction techniques. Adaptive reuse transforms vacant spaces into productive assets contributing to community revitalization. This approach mitigates the risks associated with holding underperforming office properties. The growing interest in sustainable development further enhances the appeal of conversion projects.

Integration of Smart Building Technologies and Sustainability

The integration of smart building technologies and sustainability initiatives is also to enhance the growth of the United States commercial real estate market. Tenants and investors increasingly prioritize energy efficient and technologically advanced properties that reduce operating costs and environmental impact. According to the U.S. Energy Information Administration, commercial buildings consume a significant portion of national energy driving demand for green solutions. Smart systems, such as Internet of Things sensors automated lighting and HVAC controls optimize energy usage and enhance tenant comfort. Properties with LEED or WELL certifications command premium rents and attract high quality tenants. Investors view sustainable assets as lower risk and more resilient to regulatory changes. The implementation of renewable energy sources such as solar panels further reduces carbon footprints. Technology platforms enable predictive maintenance and improved operational efficiency. Landlords who invest in upgrades differentiate their properties in a competitive market. The demand for healthy and productive work environments supports the adoption of wellness focused features. Government incentives and tax credits encourage green building practices. The transition to net zero emissions creates opportunities for innovation and value creation. Smart buildings provide data insights that inform decision making and enhance asset performance. This trend aligns with corporate environmental social and governance goals.

MARKET CHALLENGES

High Construction Costs and Material Supply Chain Disruptions

The high construction costs and supply chain disruptions affecting development timelines and budgets is to act as a major barrier for the growth of United States commercial real estate market. The prices of key materials, such as steel lumber and concrete have remained volatile due to global supply chain constraints and labor shortages. According to the U.S. Bureau of Labor Statistics, the producer price index for construction inputs has shown significant increases raising the cost of new projects. Developers face difficulties in securing materials and skilled labor leading to delays and cost overruns. These uncertainties complicate financial modeling and risk assessment for new developments. Contractors may hesitate to bid on projects or include substantial contingencies in their proposals. The rising cost of construction impacts the feasibility of projects particularly in margin sensitive sectors. Delays in completion affect leasing schedules and cash flow projections. Supply chain bottlenecks persist due to geopolitical tensions and logistical issues. The scarcity of skilled tradespeople exacerbates labor costs and project timelines. Developers must navigate these challenges by adopting flexible procurement strategies and exploring alternative materials. The unpredictability of costs discourages speculative development. Existing properties may also face higher maintenance and renovation expenses.

Regulatory Complexity and Zoning Restrictions

The regulatory complexity and stringent zoning restrictions by hindering development and adaptation efforts is also to restrict the growth of the United States commercial real estate market. Local governments impose varied and often conflicting regulations regarding land use building codes and environmental compliance. According to the National League of Cities navigating the permitting process can be time consuming and costly for developers. Zoning laws may restrict the types of activities allowed in certain areas limiting flexibility for property owners. Changes in regulations can occur unexpectedly affecting project viability and investment returns. Compliance with environmental standards such as energy efficiency mandates requires significant capital investment. The lack of uniformity across jurisdictions creates inefficiencies for national developers and investors. Community opposition and lengthy approval processes further delay projects. Affordable housing requirements and inclusionary zoning policies impact profitability for residential components of mixed use projects. Property owners face challenges in adapting existing buildings to new uses due to restrictive codes. The regulatory burden increases operational costs and reduces agility. Stakeholders must engage in extensive lobbying and community outreach to secure approvals. The uncertainty surrounding regulatory changes adds risk to investment decisions. Streamlining processes and harmonizing regulations could alleviate some of these pressures. However the current landscape remains fragmented and challenging. Navigating this complex web of rules requires specialized expertise and resources.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 2.98% |

| Segments Covered | By Business Model, Property Type, End-User and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Key Market Players | CBRE Group, Inc., Jones Lang LaSalle Incorporated (JLL), Cushman & Wakefield plc, Colliers International Group Inc., Newmark Group, Inc., and Marcus & Millichap, Inc., along with major real estate developers and investors such as Hines, Tishman Speyer, Brookfield Asset Management, and Blackstone Inc., as well as prominent REITs including Prologis, Inc., Simon Property Group, Inc., Equinix, Inc., Digital Realty Trust, Inc., and Vornado Realty Trust. |

SEGMENTAL ANALYSIS

By Business Model Insights

The rental segment holds the leading position in the United States commercial real estate market due to the strong preference among businesses for operational flexibility and capital preservation. Leasing allows companies to occupy prime locations without the substantial upfront capital required for property acquisition which is crucial for maintaining liquidity in uncertain economic conditions. Tenants benefit from the ability to scale space up or down based on business needs without the long-term commitment and transaction costs associated with ownership. This flexibility is particularly valuable for startups and expanding enterprises that require agility in their real estate strategies. Landlords prefer rental models as they provide steady recurring income streams and retain asset appreciation potential. The prevalence of triple net leases shifts maintenance and operational responsibilities to tenants further enhancing the appeal for institutional investors. Regulatory frameworks support leasing through standardized contract laws and tax deductions for lease expenses. The rental model also facilitates easier entry into high cost markets where purchasing power may be limited.

The dominance of the rental segment is further reinforced by the structure of institutional investment and the prevalence of Real Estate Investment Trusts in the United States. REITs are legally required to distribute at least 90% of their taxable income to shareholders which incentivizes a business model focused on generating consistent rental income rather than speculative sales. According to the National Association of Real Estate Investment Trusts equity REITs own and operate income producing real estate representing a substantial portion of the commercial market. These entities acquire properties to lease them out creating a vast inventory of rental space available to tenants. The stability of rental cash flows attracts pension funds insurance companies and other institutional investors who seek predictable returns. This capital influx supports the development and maintenance of high quality rental properties. The professional management provided by REITs ensures efficient operations and tenant retention which enhances the value of the rental portfolio. The transparency and liquidity of publicly traded REITs make them attractive vehicles for investing in commercial real estate thereby sustaining the rental ecosystem. The alignment of investor interests with income generation solidifies the rental model as the cornerstone of the commercial real estate industry.

The sales segment is experiencing rapid growth in the United States commercial real estate market driven by aggressive acquisition strategies employed by private equity firms and institutional investors. Despite higher interest rates there is a significant volume of capital seeking to acquire distressed assets or undervalued properties with strong fundamentals. According to data from Green Street private equity dry powder dedicated to real estate remains at historic highs enabling large scale purchase transactions. Investors are capitalizing on market dislocations to buy properties at discounted prices with the intent of repositioning and holding for long term appreciation. This trend is particularly evident in the industrial and multifamily sectors where demand fundamentals remain robust. The sale of entire portfolios rather than individual assets has increased transaction values and velocity. Corporate occupiers are also engaging in sale leaseback transactions to unlock capital tied up in real estate while retaining operational use. These transactions provide immediate liquidity for sellers and stable yield opportunities for buyers. The strategic shift towards owning core assets in gateway markets drives competition and pricing in the sales segment. As market confidence returns the pace of sales activity is expected to accelerate further. This dynamic creates a vibrant sales market alongside the dominant rental sector.

The growth of the sales segment is further accelerated by the expansion of owner occupied facilities particularly within the industrial and logistics sectors. Companies recognizing the strategic importance of supply chain control are increasingly choosing to purchase warehouses and distribution centers rather than lease them. According to the National Association of Industrial and Office Professionals the rate of owner occupancy in industrial properties has risen as firms seek to secure long term operational stability. Owning real estate protects businesses from rental inflation and provides an asset that can appreciate in value over time. This trend is supported by low vacancy rates in key logistics hubs which make purchasing a more attractive option than competing for limited lease inventory. Manufacturing reshoring initiatives also drive demand for owned facilities as companies establish domestic production capabilities. The tax benefits of depreciation and interest deductions further incentivize ownership. Financial institutions are providing specialized lending products to facilitate these purchases. The desire for customization and control over facility modifications also favors ownership. As e commerce continues to grow the need for dedicated owned infrastructure becomes more critical. This shift towards ownership in the industrial sector contributes significantly to the growth of the sales segment.

By Property Type Insights

The logistics segment holds the leading position in the United States commercial real estate market due to the sustained growth of e commerce and the strategic imperative for supply chain resilience. The shift in consumer behavior towards online shopping has created an insatiable demand for warehousing and distribution facilities. According to the U.S. Census Bureau e commerce sales continue to represent a double digit%age of total retail sales requiring extensive physical infrastructure for storage and fulfillment. Companies are expanding their logistics networks to reduce delivery times and improve customer satisfaction. The need for last mile delivery facilities in urban areas has intensified competition for industrial space. Supply chain disruptions during recent global events have prompted businesses to hold larger inventories and diversify sourcing leading to increased demand for storage capacity. Modern logistics facilities with high ceilings automation capabilities and proximity to transportation hubs are highly sought after. The scarcity of developable land in major metropolitan areas has driven up rental rates and property values. Investors view logistics real estate as a defensive asset class with strong growth prospects. The structural changes in retail and manufacturing ensure that logistics remains the dominant property type. This segment benefits from long term leases and creditworthy tenants providing stable income streams.

The dominance of the logistics segment is further reinforced by the integration of advanced technologies and automation in warehouse operations. Modern distribution centers require specialized buildings designed to accommodate robotics autonomous vehicles and sophisticated inventory management systems. According to the Material Handling Industry the adoption of automation in warehouses is accelerating driving demand for new construction and retrofitting of existing facilities. These technological advancements increase operational efficiency and throughput making modern logistics properties essential for competitive advantage. Properties with adequate power capacity floor load ratings and clear heights are preferred by tenants implementing automated solutions. The investment in technology enhances the value of logistics real estate as it becomes integral to business operations. Developers are focusing on building smart warehouses that support digital connectivity and energy efficiency. The convergence of real estate and technology creates a high barrier to entry for older facilities ensuring demand for new developments. This trend supports higher rental premiums and lower vacancy rates for modern logistics assets. The continuous evolution of supply chain technology sustains the leadership of the logistics segment in the commercial real estate market.

The Others segment specifically data centers is the fastest growing property type in the United States commercial real estate market driven by exponential growth in data consumption and cloud computing adoption. Businesses across all sectors are migrating operations to the cloud increasing the demand for secure and reliable data storage facilities. According to the International Data Corporation global data creation is projected to grow exponentially necessitating massive expansion of data center capacity. The rise of artificial intelligence and machine learning applications further accelerates the need for high performance computing infrastructure. Data centers require specialized real estate with robust power cooling and connectivity capabilities. The concentration of tech companies in specific regions has led to clusters of data center development. Investors are attracted to the long term leases and high barriers to entry in this sector. The critical nature of data infrastructure ensures consistent demand regardless of economic cycles. Government initiatives promoting digital infrastructure also support growth. The transition to 5G networks requires edge data centers closer to users further expanding the market. This technological revolution drives unprecedented growth in the data center segment.

The growth of the Others segment is further accelerated by the expansion of artificial intelligence infrastructure and edge computing networks. AI applications require significant computational power and low latency connections driving demand for specialized data centers equipped with high density power and cooling systems. According to industry analysis from JLL the power requirements for AI driven data centers are substantially higher than traditional facilities creating a niche but rapidly growing market segment. Edge computing brings data processing closer to the source reducing latency for applications such as autonomous vehicles and IoT devices. This decentralization requires a network of smaller data centers located in diverse geographic areas. Real estate developers are adapting existing properties or building new facilities to meet these specific technical requirements. The scarcity of power capacity in key markets has become a critical constraint driving up values for sites with accessible energy resources. Tech giants are investing heavily in securing data center real estate to support their AI ambitions. This strategic focus on next generation technology ensures that the data center segment continues to grow at the fastest rate.

By End-User Insights

The corporates and SMEs segment was the largest by holding 43.5% of the United States commercial real estate market share in 2025. The size and health of the corporate sector directly correlate with demand for commercial real estate. According to the Small Business Administration, small businesses account for nearly half of private sector employment in the United States driving significant demand for flexible office and retail spaces. Large corporations require headquarters regional offices and distribution networks to support their operations. The expansion or contraction of corporate workforces influences leasing activity and space requirements. SMEs often serve as anchor tenants in suburban office parks and neighborhood retail centers contributing to widespread market activity. The diversity of industries within this segment ensures broad based demand across different property types. Corporate decisions regarding remote work expansion and consolidation have immediate impacts on market dynamics. The financial health of corporations determines their ability to commit to long term leases or purchase properties. The sheer volume of businesses operating in the United States sustains the leadership of this end user group.

The Individuals and Households segment is esteemed to witness a fastest CAGR of 8.2% from 2026 to 2034 with the rise of freelancers entrepreneurs and home based businesses. The gig economy and remote work trends have blurred the lines between residential and commercial space usage. According to the Bureau of Labor Statistics, the number of self-employed individuals has increased significantly creating demand for flexible workspaces and mixed use properties. Many individuals are converting residential spaces or utilizing co working environments for business purposes. This shift has spurred growth in the coworking and flexible office sectors which cater to individual professionals. The desire for work life balance and reduced commuting times encourages people to work from home or nearby local hubs. Real estate developers are responding by creating mixed use communities that integrate living and working spaces. The demand for high-speed internet and professional amenities in residential areas has increased. This trend represents a structural change in how individuals engage with commercial real estate. The flexibility and autonomy offered by this model appeal to a growing segment of the workforce.

COMPETITIVE LANDSCAPE

The competition in the United States commercial real estate market is characterized by intense rivalry among large institutional investors regional developers and specialized service providers. Major players compete on the basis of capital access operational expertise and technological innovation. The market is fragmented with numerous local firms catering to specific geographic areas or niche property types. Differentiation is achieved through superior asset management sustainability credentials and tenant service quality. Price competition is evident in acquisition transactions where bidding wars can drive up valuations. The rise of private equity firms has increased competition for core and value add assets. Service providers compete on the breadth of their offerings and integration of digital tools. Brand reputation and track record play crucial roles in securing mandates from large corporate clients. Regulatory compliance and adaptability to changing work patterns are key competitive factors. The shift towards experiential retail and flexible office spaces creates new arenas for competition.

KEY MARKET PLAYERS

A few of the major companies in the United States commercial real estate market include

- CBRE Group, Inc.

- Jones Lang LaSalle Incorporated (JLL)

- Cushman & Wakefield plc

- Colliers International Group Inc.

- Newmark Group, Inc.

- Marcus & Millichap, Inc.

- Hines

- Tishman Speyer

- Brookfield Asset Management

- Blackstone Inc.

- Prologis, Inc.

- Simon Property Group, Inc.

- Equinix, Inc.

- Digital Realty Trust, Inc.

- Vornado Realty Trust

Top Players in the US Commercial Real Estate Market

Prologis Inc

Prologis Inc stands as the global leader in logistics real estate with a dominant presence in the United States market. The company contributes significantly to the global supply chain by owning and operating high quality distribution facilities in key markets worldwide. It strengthens its position through strategic development of modern warehouses equipped with advanced automation capabilities. Recent actions include expanding its portfolio in high growth sunbelt regions and investing in sustainable building technologies. Prologis focuses on creating value for customers through superior location and operational efficiency. The organization leverages its scale to provide comprehensive solutions for e commerce and third-party logistics providers. Its commitment to environmental sustainability aligns with corporate goals of major tenants. This strategic focus on innovation and customer centricity solidifies its leadership role in the industrial sector.

The Blackstone Group

The Blackstone Group is a leading global investment firm with substantial holdings in the United States commercial real estate market. The company contributes to the global market by deploying capital across diverse property types including logistics hospitality and residential sectors. It strengthens its position through active asset management and strategic acquisitions of distressed or undervalued properties. Recent actions involve raising large funds dedicated to real estate opportunities and focusing on thematic trends such as digital infrastructure. Blackstone leverages its extensive network and operational expertise to enhance property values. The firm emphasizes sustainability and energy efficiency in its portfolio companies. Its ability to access capital and execute complex transactions provides a competitive advantage. This approach ensures consistent returns for investors and maintains its status as a major market participant.

CBRE Group Inc

CBRE Group Inc is the largest commercial real estate services and investment firm in the world with a strong footprint in the United States. The company contributes to the global market by providing comprehensive services including leasing sales valuation and property management. It strengthens its position through digital transformation and expansion of advisory services. Recent actions include acquiring specialized firms to enhance capabilities in data analytics and sustainability consulting. CBRE focuses on delivering integrated solutions that help clients navigate complex market conditions. The organization invests in technology platforms that improve transaction efficiency and transparency. Its global reach allows for cross border collaboration and knowledge sharing. This comprehensive service model ensures relevance and resilience in a changing industry landscape.

Top Strategies Used by Key Market Participants

Key players in the United States commercial real estate market employ diversification strategies to mitigate risks associated with specific property types. Companies expand into resilient sectors such as industrial and data centers while reducing exposure to vulnerable office assets. Sustainability initiatives are central to corporate strategies as firms prioritize green building certifications and energy efficiency. Digital transformation is prioritized through investment in propTech solutions that enhance operational efficiency and tenant experience. Strategic partnerships with technology providers enable better data analytics and decision making. Capital recycling involves selling non-core assets to fund acquisitions in high growth markets. Focus on customer centric services helps retain tenants and attract new business. Risk management practices include hedging against interest rate fluctuations and maintaining flexible lease structures.

MARKET SEGMENTATION

This research report on the United States commercial real estate market has been segmented based on the following categories.

By Business Model

- Sales

- Rental

By Property Type

- Offices

- Retail

- Logistics

- Others (industrial, hospitality, etc.)

By End-user

- Individuals / Households

- Corporates & SMEs

- Others

By Country

- United States

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com