United States Copper Market Size, Share, Trends & Growth Forecast Report Segmented By Application (Electrical and electronics, Construction, Transportation, Telecommunication, Others), Type, Product Type and Country – Industry Analysis From 2026 to 2034

United States Copper Market Report Summary

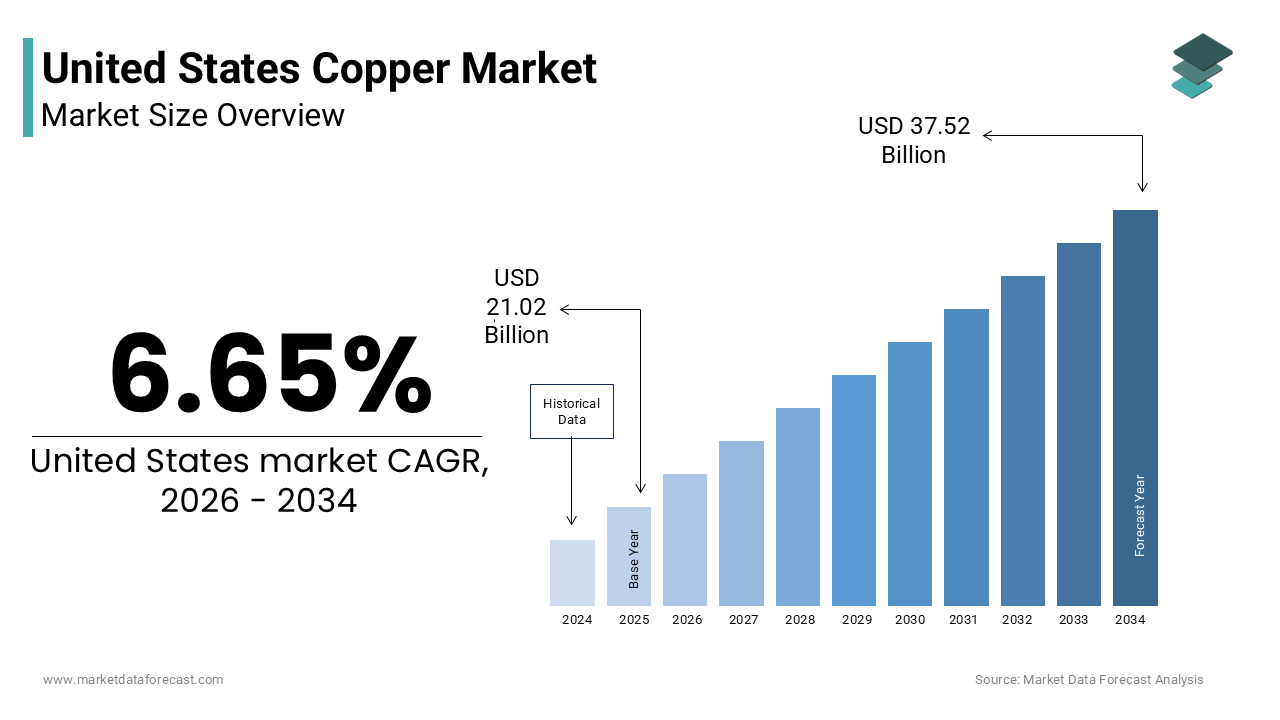

The United States copper market was valued at USD 21.02 billion in 2025, is estimated to reach USD 22.42 billion in 2026, and is projected to reach USD 37.52 billion by 2034, growing at a CAGR of 6.65% during the forecast period from 2026 to 2034. The growth of the U.S. copper market is driven by the increasing demand from electrification, renewable energy expansion, and the rising adoption of electric vehicles. Copper remains a critical material due to its high electrical conductivity, durability, and essential role in infrastructure and advanced technologies. Additionally, the integration of circular economy practices through recycling and the modernization of electrical grids is further supporting market growth.

Key Market Trends

- Rising demand for copper in electric vehicles and charging infrastructure

- Increasing adoption of renewable energy systems such as solar and wind power

- Growing focus on recycling and circular economy practices to enhance supply security

- Expansion of smart grid infrastructure and energy-efficient systems

- Increasing investment in domestic supply chains and critical mineral security

Segmental Insights

- Based on application, the electrical and electronics segment was the largest and held a significant share of the United States copper market in 2025. The segment’s dominance is attributed to extensive use of copper in wiring, power transmission systems, and electronic components across residential, commercial, and industrial sectors.

- Based on type, the primary copper segment accounted for the largest share of the United States copper market in 2025. This is driven by the high demand for consistent quality and purity in large-scale industrial applications such as construction, power infrastructure, and manufacturing.

- Based on product type, the wire segment was the largest, occupying a prominent share of the United States copper market in 2025. The dominance of this segment stems from the critical role of copper wiring in electrical systems, infrastructure development, and the growing adoption of smart technologies.

Regional Insights

The United States copper market is witnessing strong growth driven by industrial demand, infrastructure modernization, and energy transition initiatives. The country continues to rely on both domestic production and imports to meet rising consumption, highlighting the importance of secure supply chains and strategic sourcing.

Competitive Landscape

The United States copper market is characterized by the presence of large mining corporations, global metal producers, and downstream processing companies competing on production efficiency, sustainability, and technological innovation. Companies are focusing on expanding mining capacity, investing in recycling technologies, and strengthening supply chain resilience to maintain competitiveness. Prominent players in the United States copper market include Freeport-McMoRan Inc., Southern Copper Corporation, Rio Tinto, BHP Group, Glencore plc, Teck Resources Limited, KGHM Polska Miedź S.A., Antofagasta plc, Aurubis AG, Southwire Company, LLC, Encore Wire Corporation, Prysmian Group, and Nexans S.A.

United States Copper Market Size

The United States copper market size was valued at USD 21.02 billion in 2025 and is anticipated to reach USD 22.42 billion in 2026 from USD 37.52 billion by 2034, growing at a CAGR of 6.65% during the forecast period from 2026 to 2034.

The copper is component of the national industrial infrastructure, underpinning sectors ranging from construction and electronics to renewable energy and transportation. Copper is valued for its superior electrical conductivity, thermal efficiency, and durability, making it indispensable in modern technological applications. As per the United States Geological Survey, domestic mine production of copper was estimated at 1.1 million metric tons in 2024, reflecting the nation’s significant yet insufficient supply relative to its consumption needs. The United States remains a net importer of copper, relying on sources from Chile, Peru, and Canada to meet the gap between domestic extraction and industrial demand. This dependency highlights the strategic importance of secure supply chains for national economic stability. The market is characterized by a complex interplay of mining operations, recycling facilities, and manufacturing hubs that process raw material into wire rods, tubes, and sheets. According to the International Copper Study Group, global refined copper usage continues to rise, driven by electrification trends that heavily influence American demand patterns . The transition toward green energy technologies has intensified the focus on copper availability, as these systems require substantially more metal than traditional fossil fuel based counterparts. Regulatory frameworks governing environmental protection and labor standards further shape operational dynamics within the industry. The integration of circular economy principles through scrap recycling also plays a vital role, with secondary production accounting for a substantial portion of total supply.

MARKET DRIVERS

Accelerated Adoption of Electric Vehicles and Charging Infrastructure

The accelerated adoption of electric vehicles and the concurrent expansion of charging infrastructure, significantly boosting demand for high conductivity materials is escalating the growth of United States copper market. Electric vehicles require approximately 3 to 4 times more copper than internal combustion engine vehicles due to the extensive wiring harnesses, battery components, and electric motors involved. As per the International Energy Agency, the sale of electric cars in the United States reached 1.4 million units in 2024, representing a substantial year over year increase that directly correlates with higher copper consumption. Furthermore, the establishment of a nationwide charging network necessitates significant amounts of copper for cabling, transformers, and connection points. The Bipartisan Infrastructure Law allocates billions of dollars toward building 500,000 public charging stations, each requiring extensive electrical infrastructure heavily reliant on copper conductors. This government backed initiative ensures sustained demand regardless of short-term fluctuations in consumer vehicle purchases. Automakers are increasingly securing long term supply agreements with mining companies to guarantee access to this critical raw material, highlighting its strategic importance. The shift toward electrification is not limited to passenger cars but extends to commercial fleets and public transit systems, further amplifying the volume of copper required.

Expansion of Renewable Energy Generation Capacity

The expansion of renewable energy generation capacity in wind and solar power due to the metal’s essential role in energy transmission and storage is additionally propelling the growth of United states copper market. Renewable energy systems are far more copper intensive than traditional fossil fuel power plants, with offshore wind farms using up to 15,000 kilograms of copper per megawatt of installed capacity. As per the Department of Energy, the United States aims to achieve 100% carbon pollution free electricity by 2035, a goal that requires massive investments in new generation facilities and grid upgrades. Solar photovoltaic systems also utilize significant amounts of copper in their wiring, inverters, and mounting structures, contributing to overall demand growth. The need to connect remote renewable energy sites to urban centers necessitates the construction of high voltage transmission lines, which are predominantly made of copper or aluminum reinforced with steel. However, copper is preferred for its superior efficiency and smaller footprint in constrained environments. According to the Copper Development Association, renewable energy projects consumed over 200,000 metric tons of copper in the United States in 2024, a figure projected to double by 2030 as installation rates accelerate. State level mandates for renewable portfolio standards further compel utilities to invest in green energy infrastructure, ensuring a steady pipeline of copper intensive projects. The decentralization of energy production through rooftop solar installations also adds to residential and commercial copper demand.

MARKET RESTRAINTS

Stringent Environmental Regulations and Permitting Delays

The stringent environmental regulations and prolonged permitting by delaying new mining projects and increasing operational costs is restricting the growth of the United States copper market. Developing a new copper mine in the United States can take between 10 and 15 years due to rigorous environmental impact assessments, public consultations, and legal challenges. As per the National Mining Association, the average time to obtain all necessary permits for a new mine has increased substantially, creating uncertainty for investors and developers . These delays hinder the ability of domestic producers to respond quickly to rising demand, forcing greater reliance on imports and potentially exacerbating supply shortages. Compliance with the Clean Water Act, the Endangered Species Act, and other federal laws requires significant financial investment in mitigation measures and monitoring systems. Small and mid sized mining companies often struggle to bear these costs, leading to industry consolidation and reduced competition. Additionally, state level regulations may impose further restrictions on water usage and waste management, complicating operational planning. The recent rejection of several high profile mining projects due to environmental concerns underscores the difficulty of expanding domestic production capacity. According to the Government Accountability Office, regulatory inefficiencies contribute to higher capital expenditures and reduced competitiveness for US mining firms compared to international peers . This restrictive environment limits the growth potential of the domestic copper supply chain and increases vulnerability to global market volatility.

Volatility in Global Copper Prices and Supply Chain Disruptions

The volatility in global copper prices and supply chain disruptions by creating financial uncertainty and operational challenges for manufacturers and consumers is declining the growth of United States copper market. Copper prices are subject to fluctuation based on global economic conditions, geopolitical tensions, and speculative trading activities by making long term planning difficult for industries that rely on stable input costs. Sudden price spikes can erode profit margins for manufacturers of electrical equipment and construction materials, leading to project delays or cancellations. Supply chain disruptions, such as port congestion, labor strikes, or logistical bottlenecks, further exacerbate these issues by delaying the delivery of imported copper and semi finished products. The dependence on foreign sources for a significant portion of US copper needs exposes the market to international risks, including trade disputes and export restrictions from producing countries. According to the Bureau of Labor Statistics, producer price indices for copper and brass mill products showed heightened volatility, reflecting the instability in raw material costs . This unpredictability discourages investment in copper intensive technologies and encourages the search for alternative materials where possible. Manufacturers may also hesitate to enter into long term contracts, preferring spot purchases that offer flexibility but lack price security.

MARKET OPPORTUNITIES

Advancements in Recycling and Circular Economy Practices

The advancements in recycling and circular economy practices by enhancing supply security and reducing environmental impact is creating new opportunities for the growth of United States copper market. Copper is fully recyclable without loss of quality by making it an ideal candidate for sustainable resource management. Investments in advanced sorting and processing technologies enable more efficient recovery of copper from electronic waste, end of life vehicles, and construction debris. This reduces reliance on virgin ore mining and lowers the carbon footprint associated with copper production. Government incentives for recycling initiatives and extended producer responsibility laws encourage manufacturers to design products that are easier to dismantle and recycle. The development of urban mining concepts, where valuable metals are extracted from discarded electronics, offers a lucrative avenue for growth. According to the Environmental Protection Agency, only a fraction of electronic waste is currently recycled, indicating substantial untapped potential for copper recovery. Companies that innovate in recycling technologies can capture value from waste streams while contributing to sustainability goals. The integration of blockchain technology for tracking material origins also enhances transparency and trust in recycled copper markets. As corporate sustainability commitments intensify, demand for responsibly sourced and recycled copper is expected to rise.

Integration of Smart Grid Technologies and Infrastructure Upgrades

The integration of smart grid technologies and ongoing infrastructure upgrades by driving demand for high performance electrical components is also escalating the growth of the United States copper market. Modernizing the aging electrical grid requires extensive replacement of outdated wires and transformers with more efficient copper based systems capable of handling bidirectional energy flows and variable loads. Smart meters, sensors, and automated control systems all rely on copper connections for reliable data transmission and power distribution. The resilience of copper against corrosion and its superior conductivity make it the preferred material for these critical applications. Federal funding from infrastructure bills supports these upgrades by ensuring a steady flow of capital into the sector. Additionally, the proliferation of distributed energy resources such as home battery systems and solar panels necessitates robust local grid connections, further boosting copper demand. According to the American Society of Civil Engineers, upgrading the nation’s energy infrastructure is a top priority, with copper playing a central role in achieving reliability and efficiency goals . Collaborations between technology providers and utilities to develop standardized smart grid components create new market avenues for copper fabricators.

MARKET CHALLENGES

Shortage of Skilled Labor in Mining and Processing Sectors

The shortage of skilled labor in the mining and processing sectors by constraining production capacity and increasing operational costs, which is one of the challenges for the growth of United States copper market. The industry faces an aging workforce with many experienced workers nearing retirement, while fewer young professionals are entering the field due to perceived risks and remote working conditions. As per the Society for Mining, Metallurgy and Exploration, the mining industry struggles to attract talent in engineering, geology, and equipment operation, leading to productivity gaps . This labor scarcity results in delayed projects, increased overtime expenses, and potential safety risks if inexperienced workers are deployed. Training new employees requires significant time and resources, further straining company budgets. The competition for skilled technicians from other sectors such as technology and renewable energy exacerbates the problem, as these industries often offer more attractive compensation packages and working environments. Automation and digitalization offer partial solutions but require specialized skills that are also in short supply. The inability to fully staff operations limits the ability of mines to ramp up production in response to rising demand. Addressing this challenge requires coordinated efforts between industry stakeholders, educational institutions, and policymakers to promote career pathways and improve working conditions.

Geopolitical Tensions and Trade Policy Uncertainties

The geopolitical tensions and trade policy uncertainties by disrupting supply chains is also to decline the growth of United States copper market. The United States relies heavily on copper imports from countries that may be subject to political instability or trade disputes by creating vulnerabilities in supply security. As per the Congressional Research Service, trade policies such as tariffs and export controls can alter flow patterns and increase costs for domestic consumers. Tensions with major producing nations or transit countries can lead to sudden supply interruptions, forcing buyers to seek alternative sources at higher prices. The strategic competition for critical minerals has led to increased scrutiny of foreign investments in US mining projects, potentially slowing down development. Additionally, fluctuations in currency exchange rates influenced by geopolitical events affect the competitiveness of imported copper versus domestically produced metal. According to the World Bank, geopolitical risks remain a key factor influencing commodity markets, with copper being particularly sensitive to international relations. Uncertainty regarding future trade agreements makes long term planning difficult for manufacturers and traders. Companies must navigate a complex web of regulations and diplomatic relations to secure reliable supplies, adding layers of complexity to procurement strategies. The potential for retaliatory measures from trading partners further complicates the landscape.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.65% |

| Segments Covered | By Application, Type, Product Type and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Key Market Players | Freeport-McMoRan Inc., Southern Copper Corporation, Rio Tinto, BHP Group, Glencore plc, Teck Resources Limited, KGHM Polska Miedź S.A., Antofagasta plc, along with downstream and processing companies such as Aurubis AG, Southwire Company, LLC, Encore Wire Corporation, Prysmian Group, and Nexans S.A.. |

SEGMENTAL ANALYSIS

By Application Insights

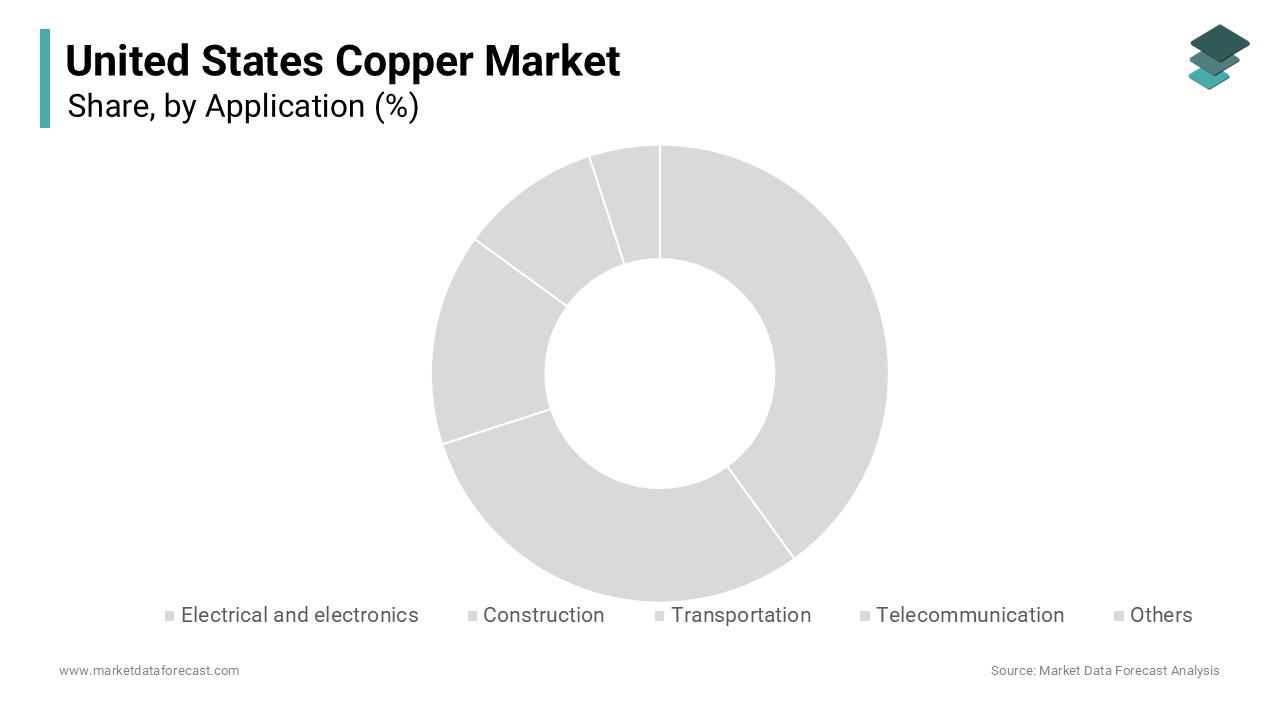

The electrical and electronics segment was the largest by holding 45.3% of the United States copper market share in 2025 due to the indispensable role of copper in power transmission and distribution infrastructure. Copper’s superior electrical conductivity makes it the preferred material for wiring, transformers, and switchgear in both residential and commercial settings. The ongoing modernization of the aging electrical grid requires extensive replacement of aluminum and older copper lines with high efficiency copper conductors to reduce energy loss and improve reliability. Furthermore, the expansion of renewable energy sources necessitates robust transmission networks to connect remote generation sites to urban centers, driving sustained demand for copper wiring. The reliability and durability of copper ensure minimal maintenance costs over the lifespan of electrical installations, making it a cost effective choice for long term infrastructure projects.

The transportation segment is likely to witness a fastest CAGR of 21.2% from 2026 to 2034 with the rapid electrification of vehicle fleets and the associated battery production requirements. Electric vehicles utilize significantly more copper than internal combustion engine vehicles in their batteries, motors, and charging infrastructure. As per the International Energy Agency, electric vehicle sales in the United States are projected to grow at a compound annual growth rate of 25% through 2030, directly correlating with a surge in copper demand. Each electric vehicle contains approximately 83 kilograms of copper, compared to just 23 kilograms in a conventional car, creating a substantial increase in per unit material usage. The expansion of domestic battery manufacturing facilities, supported by federal incentives under the Inflation Reduction Act, further accelerates this trend. Additionally, the development of heavy duty electric trucks and buses for public transit introduces even larger copper loads per vehicle. Automakers are securing long term copper supply contracts to mitigate risks, signaling a structural shift in demand dynamics. This transition away from fossil fuels establishes transportation as a high growth sector, outpacing traditional applications as the industry scales up production to meet regulatory mandates and consumer preferences for sustainable mobility solutions.

By Type Insights

The primary copper segment was accounted in holding 34.2% of the United States copper market share in 2025 with the large scale industrial applications require high purity materials that are most consistently supplied through mining and refining operations. Primary copper, derived directly from ore, offers the consistent quality and traceability necessary for infrastructure projects, such as power grids and construction. As per the United States Geological Survey, primary production accounted for approximately 65% of total copper supply in the United States in 2024, reflecting its foundational role in meeting base demand. Industries, such as aerospace and defense mandate strict material specifications that are easier to guarantee with primary sources rather than recycled scrap, which may contain variable impurities. The stability of primary supply chains allows manufacturers to plan long term projects with confidence in material availability. Major mining operations in states like Arizona and Utah provide a steady stream of cathode copper that is processed into various forms for downstream use. The ability to produce specialized alloys with precise compositions also favors primary copper, as it provides a clean baseline for adding other elements.

The secondary copper segment is lucratively to witness a fastest CAGR of 11.7% during the forecast period. Recycling copper requires up to 85% less energy than producing primary copper from ore, making it an attractive option for companies aiming to reduce their carbon footprint. As per the Environmental Protection Agency, recycling rates for copper in the United States have increased by 15% over the past five years, reflecting growing corporate and consumer commitment to environmental responsibility. Regulatory frameworks, such as extended producer responsibility laws encourage manufacturers to design products for easier disassembly and recycling, increasing the availability of high quality scrap. The construction industry, in particular, is embracing recycled copper for wiring and plumbing due to its comparable performance and lower environmental impact. Corporate sustainability reports increasingly highlight the use of recycled content as a key performance indicator, driving demand for certified secondary copper. This shift is supported by advancements in sorting technologies that improve the purity of recycled material, making it suitable for more demanding applications.

By Product Type Insights

The wire constitutes segment was the largest by the leading product type in the United States copper market due to its critical role in electrical wiring and connectivity across residential, commercial, and industrial sectors. Copper wire is the standard for electrical installations because of its high conductivity, flexibility, and resistance to corrosion. As per the National Electrical Code, copper is the mandated material for most indoor wiring applications due to its safety and performance characteristics, ensuring consistent demand from the construction industry . The expansion of smart home technologies and the Internet of Things has increased the complexity of wiring systems, requiring more extensive networks of copper cables for data and power transmission. Residential construction booms and commercial real estate developments drive substantial volumes of wire consumption, as every new building requires extensive electrical infrastructure. The reliability of copper wire ensures minimal signal loss and energy inefficiency by making it indispensable for high performance applications. Furthermore, the retrofitting of older buildings with updated electrical systems to meet modern safety standards contributes to steady replacement demand. The ubiquity of electrical devices and the need for reliable power delivery ensure that wire remains the primary form factor for copper consumption, maintaining its leading position in the market.

The copper foil segment is likely to grow at an anticipated CAGR of 13.4% from 2026 to 2034 with the surge in lithium ion battery production for electric vehicles and energy storage systems. Copper foil serves as the anode current collector in lithium-ion batteries, where a component that influences battery performance and efficiency. As per the Department of Energy, domestic battery manufacturing capacity is expected to triple by 2030, creating an exponential demand for high quality copper foil. The thinness and purity requirements for battery foil necessitate specialized production processes, distinguishing it from standard copper products. Automakers and battery manufacturers are securing long term supply agreements with foil producers to ensure adequate material availability for their expanding production lines. The shift toward larger format batteries for electric trucks and grid storage further amplifies this demand. Government incentives for domestic battery production under the Inflation Reduction Act accelerate the establishment of new factories, each requiring significant amounts of copper foil.

COMPETITIVE LANDSCAPE

The competition in the United States copper market is characterized by a mix of large integrated mining companies and specialized recyclers vying for dominance in a capital intensive industry. Major players leverage economies of scale and advanced technologies to maintain cost leadership and operational efficiency. The market is influenced by global price fluctuations and supply chain dynamics requiring participants to adopt flexible strategies. Domestic producers compete with imports from Chile Peru and other major exporting nations creating pressure on pricing and margins. Regulatory compliance regarding environmental protection and labor standards adds complexity to operations influencing competitive advantages. Companies differentiate themselves through sustainability initiatives and community engagement efforts to secure social licenses. Innovation in extraction and processing technologies provides a edge in reducing costs and improving yields. The rise of secondary copper production introduces additional competition as recyclers offer environmentally friendly alternatives. Strategic alliances and vertical integration help firms secure supply chains and stabilize revenues.

KEY MARKET PLAYERS

A few of the major companies in the United States copper market include

- Freeport-McMoRan Inc.

- Southern Copper Corporation

- Rio Tinto

- BHP Group

- Glencore plc

- Teck Resources Limited

- KGHM Polska Miedź S.A.

- Antofagasta plc

- Aurubis AG

- Southwire Company, LLC

- Encore Wire Corporation

- Prysmian Group

Top Players in the US Copper Market

Freeport McMoRan Inc

Freeport McMoRan Inc stands as a leading international mining company with significant operations in the United States copper sector. The company operates major mines in Arizona and New Mexico contributing substantially to domestic production volumes. Freeport McMoRan plays a critical role in the global market by supplying high quality copper cathodes and concentrates to international buyers. Recent actions include investing in advanced leaching technologies to improve recovery rates and extend mine life at existing sites. The company focuses on sustainable mining practices and community engagement to maintain its social license to operate. Its strategic investments in exploration and development projects ensure long term resource availability. These initiatives enhance its ability to meet growing global demand for copper while maintaining financial stability and operational excellence in a volatile commodity market environment.

Rio Tinto Group

Rio Tinto Group is a global mining and metals corporation with substantial copper assets in the United States particularly through its Kennecott Utah Copper operation. The company contributes significantly to the global supply chain by producing refined copper gold and silver. Rio Tinto emphasizes innovation and automation in its mining processes to enhance safety and productivity. Recent strategies involve expanding its portfolio of critical minerals and investing in low carbon technologies to support the energy transition. The company actively engages in partnerships with technology firms to develop electric haulage systems and renewable energy solutions for its operations. Its commitment to sustainability and responsible sourcing appeals to environmentally conscious investors and customers. These efforts ensure that Rio Tinto remains a key player in the United States copper market while driving progress in the global mining industry.

Southern Copper Corporation

Southern Copper Corporation is one of the largest integrated copper producers in the world with significant mining and processing facilities in the Americas. Although primarily focused on Latin America the company influences the United States market through its extensive export activities and strategic partnerships. Southern Copper contributes to global supply stability by maintaining large reserves and consistent production levels. Recent actions include investing in expansion projects to increase output and improve infrastructure efficiency. The company focuses on cost management and operational excellence to remain competitive in fluctuating market conditions. Southern Copper also prioritizes environmental compliance and community development initiatives to mitigate risks and enhance its reputation.

Top Strategies Used by Key Market Participants

Key players in the United States copper market primarily focus on operational efficiency and technological innovation to reduce costs and enhance productivity. Companies invest heavily in automation and digital tools to optimize mining processes and improve safety standards. Another major strategy involves expanding recycling capabilities to secure secondary copper sources and meet sustainability goals. Strategic partnerships with technology providers enable the adoption of electric vehicles and renewable energy solutions in operations. Diversification into other critical minerals helps companies mitigate risks associated with copper price volatility. Environmental stewardship and community engagement are central to maintaining social licenses to operate. These approaches help participants navigate regulatory challenges and capitalize on growing demand for sustainable materials in the evolving industrial landscape.

MARKET SEGMENTATION

This research report on the United States copper market has been segmented based on the following categories.

By Application

- Electrical and electronics

- Construction

- Transportation

- Telecommunication

- Others

By Type

- Primary

- Secondary

By Product type

- Wire

- Tube

- Flat rolled products

- Rods and bars

- Foil

By Country

- United States

Frequently Asked Questions

What is the current size of the United States copper market?

The U.S. copper market is valued in billions, driven by demand across multiple industrial sectors.

What is the expected growth rate of the U.S. copper market?

The market is projected to grow steadily due to increasing industrial and infrastructure activities.

What are the key drivers of the U.S. copper market?

Growth is driven by renewable energy adoption, electric vehicles, and construction expansion.

Which industries consume the most copper in the United States?

Construction, electrical & electronics, automotive, and energy sectors are major consumers.

How does the construction sector impact copper demand?

Copper is widely used in wiring, plumbing, and roofing, making construction a key demand driver.

What role does copper play in renewable energy?

Copper is essential in solar panels, wind turbines, and energy storage systems.

Why is copper important for electric vehicles (EVs)?

EVs require significantly more copper than traditional vehicles for batteries and wiring.

What are the major challenges in the U.S. copper market?

Challenges include price volatility, environmental regulations, and supply chain disruptions.

How does copper price volatility affect the market?

Fluctuating prices impact production costs, investment decisions, and profitability.

What is the future outlook of the U.S. copper market?

The market is expected to grow due to electrification, EV adoption, and renewable energy expansion.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com