U.S Craft Beer Market Size, Share, Growth, Trends & Analysis Research Report, Segmented By Product, Age Group, Distributional Channel, And By Country (California, Washington, Oregon, New York & Rest of the United States), Industry Analysis From 2026 to 2034

U.S Craft Beer Market Size

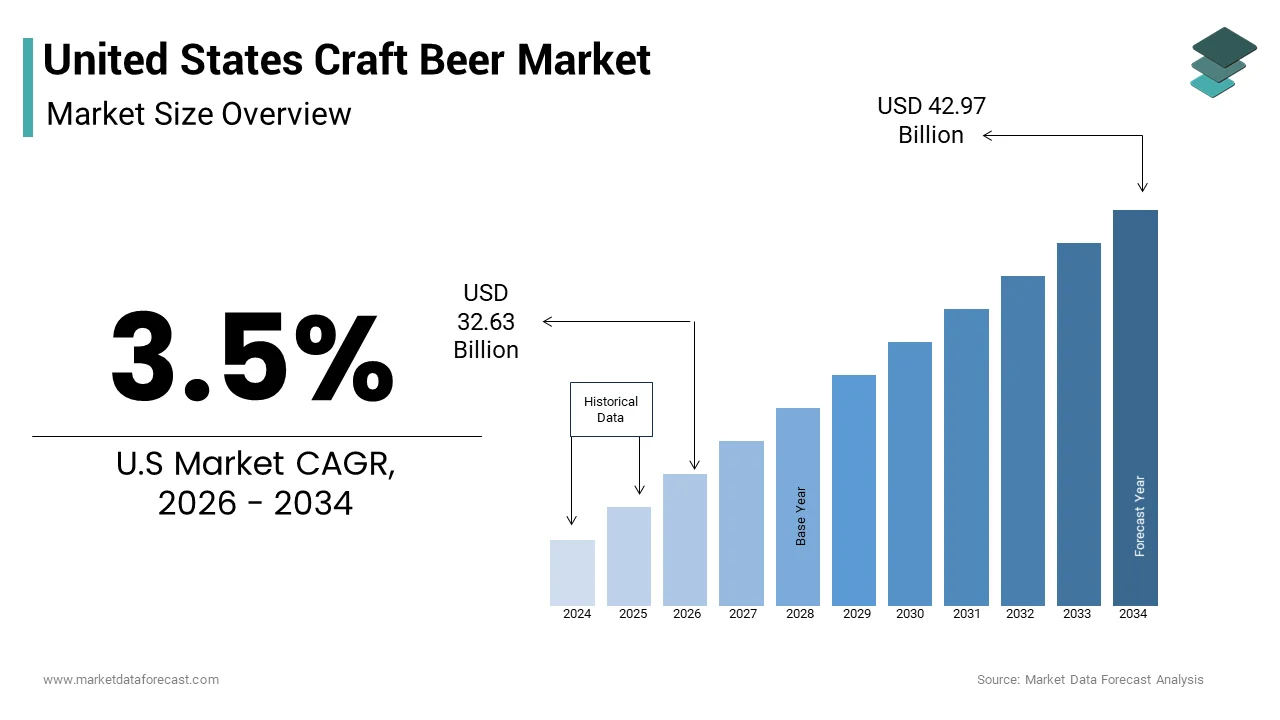

The U.S craft beer market size was valued at USD 31.53 billion in 2025 and is anticipated to reach USD 32.63 billion in 2026 to reach USD 42.97 billion by 2034, growing at a CAGR of 3.50% during the forecast period from 2026 to 2034.

Introduction and Market Definition

The craft beer is the broader alcoholic beverage industry characterized by small independent breweries that emphasize traditional brewing methods and innovative flavor profiles. As per the Brewers Association, an American craft brewer is defined as small annual production of 6 million barrels of beer or less independent less than 25% of the craft brewery is owned or controlled by an alcoholic beverage industry member. Consumer behavior has shifted markedly toward experiential consumption where patrons value the story behind the brand and the community connection provided by taprooms. This shift reflects a broader trend in retail where provenance and transparency dictate purchasing decisions. Regulatory frameworks vary significantly by state influencing distribution capabilities and direct to consumer sales models. The definition continues to adapt as consolidation pressures mount and consumer preferences diversify beyond traditional ale and lager styles into sour wild and hybrid categories.

MARKET DRIVERS

Consumer Preference for Premiumization and Flavor Diversity

The relentless pursuit of premium quality and diverse flavor experiences is propelling the growth of United States craft beer market. Modern consumers increasingly view beer as a culinary component rather than a commodity leading to heightened demand for complex taste profiles. Tudy, According to premium and super premium beer segments have consistently outpaced value oriented brands in terms of dollar sales growth reflecting this shift in consumer priority. The average price per case for craft beer remains significantly higher than domestic macro lagers indicating willingness to pay for perceived quality. This demand drives breweries to experiment with adjuncts like fruit coffee and spices creating limited edition releases that foster urgency and exclusivity. The rise of social media platforms amplifies this trend as enthusiasts share tasting notes and ratings thereby influencing peer purchasing decisions. Furthermore, the profile of craft beer drinkers skews younger with millennials and Generation Z consumers, showing greater openness to trying new styles compared to older generations. This generational shift ensures a steady influx of new customers who prioritize artisanal production methods over mass market consistency.

Strong Emphasis on Localism and Community Engagement

The profound connection between craft breweries and their local communities for the expansion and customer loyalty is fuelling the growth of United States craft beer market. Consumers increasingly prefer to support local businesses as a means of sustaining regional economies and reducing environmental footprints associated with long distance transportation. As per a study by the Brewers Association locally produced craft beer generates substantial economic impact by creating jobs and sourcing ingredients from nearby farms. Taprooms have become social hubs where residents gather fostering a sense of belonging and identity tied to the brand. This direct to consumer model allows breweries to retain higher margins while gathering immediate feedback on new products. Data from the National Beer Wholesalers Association suggests that on premise sales at brewery taprooms contribute disproportionately to overall revenue for small producers. The locavore movement extends beyond food to beverages with patrons actively seeking out beers brewed within their county or state. This preference insulates local breweries from national competition to some extent as brand loyalty is rooted in geographic proximity rather than just taste. Additionally, many breweries engage in charitable activities and sponsor local events further embedding themselves in the social fabric.

MARKET RESTRAINTS

Intensifying Market Saturation and Consolidation Pressures

The sheer volume of new entrants into the craft brewing space has led to severe market saturation posing a significant restraint on growth for existing players. With over 9000 breweries operating in the United States the shelf space in retail outlets and tap handles in bars have become fiercely contested resources. Small breweries struggle to achieve economies of scale making it difficult to compete on price with larger regional or national brands that have acquired craft labels. The oversupply of similar styles has led to consumer fatigue and diminished differentiation among brands. Distributors often prioritize established brands with higher turnover rates leaving smaller producers with limited access to broader markets. Furthermore, the cost of customer acquisition has risen as marketing channels become crowded with competing messages. Financial strain is evident as profit margins compress due to rising input costs and the need for continuous promotional spending to maintain visibility.

Regulatory Complexity and Rising Input Costs

Navigating the intricate web of federal state and local regulations for craft breweries operating across multiple jurisdictions is degrading the growth of united States craft beer market. The three tier distribution system mandated in many states requires breweries to sell to distributors, who then sell to retailers adding layers of cost and complexity to the supply chain. According to the research, compliance with labeling advertising and reporting requirements demands significant administrative resources that small businesses often lack. Variations in excise tax rates between states further complicate pricing strategies and market entry decisions. Additionally, the volatility in the cost of key raw materials such as barley hops and aluminum cans exerts pressure on profitability. Energy costs for brewing and refrigeration also contribute to operational expenses which have risen in recent years. These financial pressures are exacerbated by labor shortages in the hospitality and manufacturing sectors forcing breweries to increase wages to attract and retain skilled workers. The cumulative effect of these regulatory and cost burdens reduces the capital available for innovation and expansion. Smaller breweries without substantial cash reserves find it challenging to absorb these shocks leading to stagnation or exit from the market.

MARKET OPPORTUNITIES

Expansion into Non Traditional Beer Categories

The emergence of adjacent beverage categories, such as hard seltzers, hard kombucha, and malt based ready to drink cocktails, offers a significant opportunity for craft breweries to diversify their portfolios. The expansion into non-traditional beer categories is creating new opportunities for the growth of United States craft beer market. Consumers seeking lower calorie and lower alcohol options are driving demand for these alternatives, which align well with the craft ethos of quality and innovation. Craft breweries possess the technical expertise and brand equity to enter these spaces effectively leveraging their existing distribution networks and customer loyalty. This diversification mitigates the risk associated with declining beer consumption trends among certain age groups. Furthermore, these products often command higher price points and enjoy favorable placement in retail environments due to their health conscious positioning. Breweries that successfully integrate these offerings into their core lineup can enhance revenue stability and reduce dependence on traditional beer sales. The flexibility of small batch production allows for rapid experimentation with flavors and formats enabling quick response to emerging trends. This strategic pivot allows craft brewers to remain relevant in a changing beverage, while maintaining their independent status. The cross pollination of brewing techniques with other fermentation processes opens new avenues for product development and brand storytelling.

Direct to Consumer Sales and E Commerce Growth

The acceleration of direct to consumer sales channels, including e-commerce and subscription services to bypass traditional distribution barriers is to set up the growth of United States craft beer market. The regulatory landscape has gradually evolved to permit shipping of alcohol directly to consumers in numerous states enabling breweries to reach customers beyond their immediate geographic vicinity. Subscription models allow breweries to create recurring revenue streams and foster deeper relationships with customers through curated selections and exclusive releases. Direct sales also eliminate the margin share taken by distributors and retailers improving overall profitability for the brewery. The convenience factor appeals to busy consumers who prefer home delivery over visiting multiple retail locations. Breweries can leverage digital marketing tools to target specific demographics and personalize communications increasing conversion rates. The integration of virtual tasting events and online community building further strengthens brand loyalty in the digital realm. This channel resilience was particularly evident during periods of restricted on premise dining proving its viability as a long-term strategy.

MARKET CHALLENGES

Supply Chain Volatility and Raw Material Scarcity

The instability of global supply chains to the consistent production and profitability is to inhibit the growth of United States craft beer market. Dependence on imported hops particularly from regions like Germany and New Zealand exposes breweries to geopolitical risks and currency fluctuations. According to the study, climate related events such as droughts and floods have impacted crop yields leading to scarcity and price spikes for certain aromatic hop varieties. Aluminum can shortages have also plagued the industry forcing breweries to revert to less efficient packaging formats or face production delays. Small breweries lack the bargaining power to secure favorable contracts with suppliers making them vulnerable to sudden price hikes. This volatility disrupts production schedules and forces frequent reformulation of recipes, which can alienate loyal customers expecting consistent flavor profiles. The carbon footprint associated with long distance sourcing also conflicts with the sustainability goals many craft breweries espouse. Mitigating these risks requires significant investment in local sourcing initiatives which may not always be feasible due to limited domestic availability of specific ingredients. The unpredictability of input costs makes financial planning difficult and erodes profit margins. Breweries must maintain higher safety stocks tying up capital that could otherwise be used for growth initiatives.

Labor Shortages and Skilled Workforce Gaps

The acute shortage of skilled labor in both brewing operations and hospitality services is additionally to impede the growth of United States craft beer market. Finding qualified brewers cellar operators and taproom staff has become increasingly difficult as competition for talent intensifies across the hospitality sector. Craft brewing requires specialized technical knowledge regarding fermentation chemistry and quality control which takes time to develop. The turnover rate in taproom positions remains high leading to increased training costs and inconsistent customer experiences. Wage inflation driven by labor scarcity further strains operating budgets particularly for small independent breweries with limited financial reserves. The lack of standardized training programs in some regions exacerbates the skill gap making recruitment a prolonged and costly process. Additionally, the physical demands of brewing work combined with irregular hours can deter potential candidates from entering the field. This labor constraint limits the ability of breweries to expand production capacity or extend operating hours. It also hinders innovation as experienced staff are stretched thin managing daily operations rather than developing new products. Breweries must invest in employee retention strategies such as competitive benefits and career development opportunities to mitigate these effects. However, these measures increase overhead costs potentially reducing competitiveness. The long-term sustainability of the sector depends on addressing these workforce challenges through industry wide collaboration and education initiatives.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.50% |

| Segments Covered | By Product, Age Group, Distributional Channel, and Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities. |

| Regions Covered | US, Canada, and the Rest of North America |

| Market Leaders Profiled | Bell’s Brewery, D.G. Yuengling & Son, Inc., Dogfish Head Craft Brewery, Duvel Moortgat, Minhas Craft Brewery, New Belgium Brewing Company, Oskar Blues Brewery, Sierra Nevada Brewing Co., Stone Brewing, The Boston Beer Company, The Gambrinus Company. |

SEGMENTAL ANALYSIS

By Product Insights

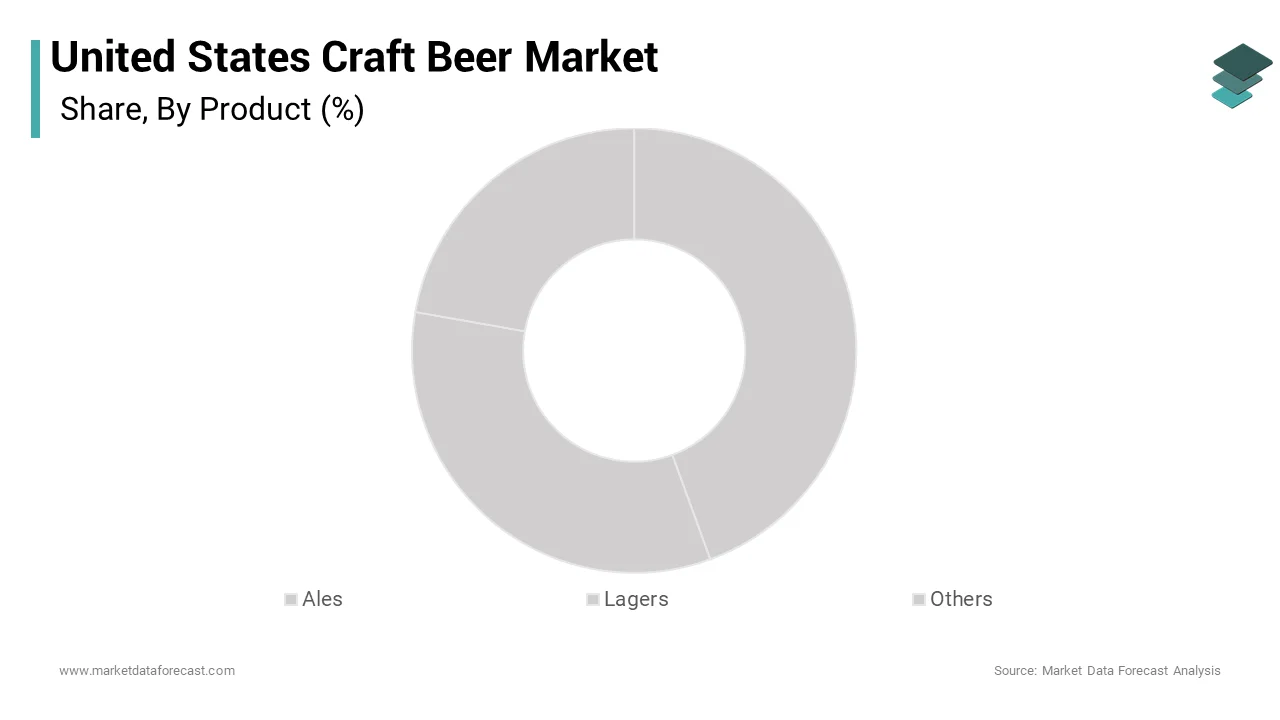

The ales segment was the largest by holding a 24.3% of the United States craft beer market due to their extensive flavor profiles and the widespread consumer preference for hop forward characteristics. The versatility of ale yeast allows brewers to create a vast array of styles ranging from India Pale Ales to stouts and porters, which aligns with the modern consumer demand for sensory exploration. Consumers associate ales with higher quality and artisanal craftsmanship which justifies premium pricing strategies. The ability of ales to incorporate diverse adjuncts such as citrus fruits spices and coffee further enhances their appeal to adventurous drinkers. The cultural narrative surrounding craft beer heavily features ales reinforcing their status as the definitive craft beverage. Retailers prioritize ale selections due to higher turnover rates and consumer demand ensuring prominent shelf placement. Breweries invest heavily in hop sourcing and brewing techniques to differentiate their ale offerings driving sustained dominance in the market.

The others segment is expected to witness a fastest CAGR of 11.2% during the forecast period with the intense innovation and a consumer desire for novel taste experiences. This category appeals to drinkers who have exhausted traditional ale and lager options and seek more adventurous flavors. The fermentation processes used in these beers, such as barrel aging and mixed culture fermentation create complex tart and funky profiles that distinguish them from mainstream offerings. Social media platforms play a crucial role in popularizing these styles as visually distinct packaging and vibrant colors attract attention online. Influencers and beer enthusiasts frequently highlight rare sour releases creating a sense of urgency and exclusivity. Breweries are investing in specialized equipment and expertise to produce these challenging styles, thereby raising the barrier to entry and enhancing perceived value. The health-conscious perception of some sour beers due to their probiotic content also attracts a niche demographic. Additionally, the collaboration between breweries and wineries or distilleries for barrel sourced ingredients fosters cross category interest. This segment benefits from high margin potential as consumers are willing to pay premium prices for limited production runs.

By Age Group Insights

The 21 to 35 years old age group segment was accounted by holding 42.8% of the United states craft beer market with the strong preference of millennials and Generation Z consumers for authentic and transparent brands. These demographics prioritize experiences over possessions and view craft beer as a symbol of individuality and cultural sophistication. This group is highly influenced by social media trends and peer recommendations making them early adopters of new styles and brands. They value the story behind the beer including the sourcing of ingredients and the brewing process which aligns with their ethical consumption habits. The willingness of this demographic to pay premium prices for high quality products supports the profitability of craft breweries. Furthermore, the social aspect of drinking craft beer in taprooms or at festivals appeals to their desire for community and connection. This age group is also more likely to travel to visit breweries contributing to the growth of beer tourism. Their openness to experimentation drives demand for diverse and innovative beer styles keeping the market vibrant. The digital nativity of this segment facilitates effective marketing through online channels enabling breweries to reach them directly. Their influence extends beyond personal consumption as they shape trends and preferences for older demographics.

The 40 to 54 years old age group segment is likely to witness a fastest CAGR of 12.3% from 2026 to 2034 with the increasing disposable income and a shift toward premiumization. Consumers in this demographic are often established in their careers and have greater financial flexibility to spend on high quality beverages. This age group shows a marked increase in spending on premium alcohol categories including craft beer as they seek to enhance their leisure experiences. They are less price sensitive than younger consumers and prioritize quality and complexity in their beer choices. This segment is also influenced by health consciousness leading them to choose craft beers with natural ingredients and lower additive content over mass produced alternatives. The trend of trading up from standard lagers to craft ales and lagers reflects their desire for sophistication and refinement. Breweries are responding by offering sophisticated packaging and marketing messages that appeal to this mature audience. The growth of this segment is further supported by the expansion of craft beer availability in upscale restaurants and hotels where this demographic frequently dines. Their loyalty to brands that consistently deliver quality ensures stable revenue streams for breweries. Additionally, this group is increasingly participating in beer tourism and attending festivals contributing to market expansion.

By Distribution Channel Insights

The off trade channel segment held a dominant share of the United States craft beer market in 2025 due to the unparalleled convenience and widespread availability it offers. Consumers prefer the ability to purchase craft beer for home consumption, where they can enjoy it in a comfortable and cost effective manner. The expansion of craft beer sections in major retail chains has made a wider variety of brands accessible to mainstream consumers beyond dedicated beer enthusiasts. Private label initiatives by retailers have also introduced affordable craft style options that attract budget conscious shoppers. The ability to buy in bulk for parties and gatherings further drives volume sales in this channel. Promotional activities such as discounts and bundle offers incentivize purchases and encourage trial of new brands. The convenience of one stop shopping allows consumers to pair beer with food and other beverages enhancing the overall shopping experience. Additionally, the rise of curbside pickup and delivery services from retail stores has enhanced the accessibility of off trade channels particularly during periods of restricted mobility.

The on trade channel segment is register a fastest CAGR of 12.4% from 2026 to 2034 with the rising demand for experiential consumption and the expansion of taproom facilities. Consumers increasingly value the social and sensory experience of drinking beer in a vibrant atmosphere where they can interact with brewers and other enthusiasts. The number of brewery taprooms has increased significantly providing dedicated spaces for consumers to enjoy fresh and exclusive beers. These venues offer tasting flights and guided tours that educate patrons and enhance their appreciation of the product. The social nature of on trade establishments makes them ideal for gatherings and celebrations driving frequent visits. Breweries leverage these spaces to launch new products and gather immediate feedback fostering a sense of community and loyalty. The premium pricing potential in on trade settings allows breweries to achieve higher margins compared to retail sales. Additionally, the collaboration with local restaurants for beer pairing menus expands the culinary appeal of craft beer. The ambiance and service quality of taprooms create memorable experiences that encourage repeat business.

COMPETITIVE LANDSCAPE

The competition in the United States craft beer market is characterized by intense rivalry among thousands of independent breweries and large multinational corporations that have acquired craft brands. This fragmented landscape requires participants to differentiate themselves through unique flavor profiles branding and community engagement. Small breweries compete on authenticity and local connection while larger entities leverage economies of scale and extensive distribution networks. Innovation is for survival as consumers constantly seek new and exciting taste experiences. Price competition is less prevalent than quality and experience driven differentiation. Breweries invest significantly in marketing and social media to build brand loyalty and attract younger demographics. The rise of alternative beverages such as hard seltzers adds another layer of competition for consumer spending. Regulatory variations across states further complicate competitive dynamics by influencing distribution and sales capabilities. Success depends on agility operational efficiency and the ability to adapt to shifting consumer preferences.

KEY MARKET PLAYERS

A few of the market players that are dominating the U.S craft beer market are

- Bell’s Brewery

- D.G. Yuengling & Son, Inc.

- Dogfish Head Craft Brewery

- Duvel Moortgat

- Minhas Craft Brewery

- New Belgium Brewing Company

- Oskar Blues Brewery

- Sierra Nevada Brewing Co.

- Stone Brewing

- The Boston Beer Company

- The Gambrinus Company

Top Players In The Market

- The Boston Beer Company remains a pivotal force in the United States craft beer landscape through its diverse portfolio of innovative brands. It contributes significantly to the global market by exporting its flagship Samuel Adams brand and pioneering hard seltzer categories with Truly. The company strengthens its position by continuously expanding production capabilities and investing in marketing campaigns that highlight quality and tradition. Recent actions include launching new flavor variations for its hard seltzer line to capture evolving consumer preferences. The organization also focuses on sustainability initiatives such as water conservation and renewable energy usage in breweries. These efforts enhance brand reputation and appeal to environmentally conscious drinkers.

- Sierra Nevada Brewing Co is renowned for its commitment to environmental stewardship and high quality brewing standards which influence global craft beer practices. The company plays a crucial role in the international market by setting benchmarks for sustainable brewing operations and community engagement. It strengthens its market position through consistent innovation in hop forward ales and limited edition releases that attract dedicated enthusiasts. Recent actions involve expanding its taproom experiences and enhancing direct to consumer sales channels. The brewery invests heavily in local sourcing of ingredients to support regional agriculture and reduce carbon footprints. This strategy resonates with consumers who value transparency and locality. Additionally, the company collaborates with other independent breweries to foster industry solidarity and knowledge sharing.

- D.G. Yuengling & Son Inc holds a historic position in the United States beer market as the oldest operating brewery in the nation. Its contribution to the global market lies in demonstrating the longevity and resilience of family-owned brewing enterprises. The company strengthens its position by modernizing its production facilities while preserving traditional brewing methods that define its brand identity. Recent actions include expanding distribution into new western states thereby increasing its national footprint. The brewery focuses on appealing to younger demographics through updated packaging and digital marketing efforts. It also emphasizes its heritage in advertising campaigns to differentiate itself from newer craft competitors. Strategic partnerships with local distributors ensure efficient product delivery and visibility in retail outlets. These measures help the company adapt to changing dynamics, while honoring its longstanding legacy in the American brewing industry.

Top Strategies Used By Key Market Participants

Key players in the United States craft beer market employ diversification strategies to mitigate risks associated with fluctuating beer demand. They expand into adjacent categories such as hard seltzers and ready to drink cocktails to capture broader consumer interest. Companies focus heavily on direct to consumer sales through e commerce platforms and subscription models to bypass traditional distribution barriers and improve margins. Sustainability initiatives are central to their branding as they appeal to environmentally conscious consumers by reducing waste and carbon emissions. Innovation in flavor profiles and limited-edition releases drives excitement and encourages trial among adventurous drinkers. Collaborations with other brands or local businesses create unique products that generate buzz and social media engagement. Taproom expansions serve as experiential hubs that foster community loyalty and provide high margin sales opportunities. Digital marketing efforts target specific demographics with personalized content to enhance brand connection and drive online purchases.

MARKET SEGMENTATION

This research report on the U.S craft beer market is segmented and sub-segmented into the following categories.

By Product Type

- Ales

- Lagers

- Others

By Age Group

- 21–35 Years Old

- 40–54 Years Old

- 55 Years and Above

By Distributional Channel

- On-Trade

- Off-Trade

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Frequently Asked Questions

What is currently driving growth in the United States craft beer market?

Rising consumer preference for unique flavors and premium beverages is driving growth.

Why is craft beer gaining popularity in the United States?

Consumers are seeking diverse tastes and locally produced beverages.

How would you explain craft beer in simple terms?

It is beer produced by small, independent breweries with a focus on quality and flavor.

Where is craft beer most commonly consumed across the United States?

It is widely consumed in urban areas, bars, restaurants, and at home.

What makes craft beer important in the beverage industry?

It offers product diversity and supports local brewing businesses.

From a consumer perspective, is craft beer worth the higher price?

Yes, many consumers value its quality, taste, and variety.

What challenges are affecting the United States craft beer market?

High competition and rising production costs are key challenges.

How is changing consumer preference influencing this market?

Consumers are shifting toward premium and innovative beverage options.

Which segments contribute the most to craft beer demand?

Ales, lagers, and specialty brews are major contributors.

Is the United States craft beer market growing steadily?

Yes, it is expanding with increasing interest in artisanal products.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com