U.S. E-Learning Market Size, Share, Trends, and Growth Analysis Report, Segmented by Technology, Provider, Application, and Country – Industry Forecast From 2026 to 2034

U.S. E-Learning Market Size

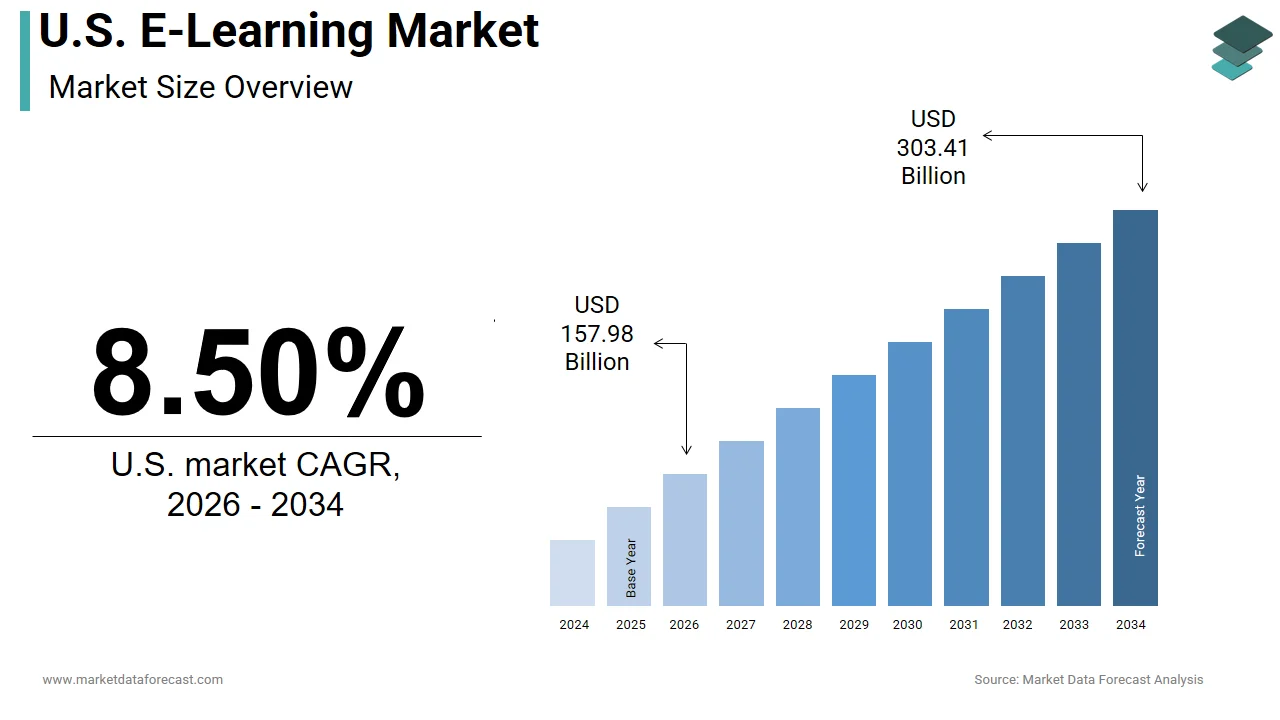

The size of the U.S. e-learning market was worth USD 145.60 billion in 2025. The market is anticipated to grow at a CAGR of 8.50% from 2026 to 2034 and be worth USD 303.41 billion by 2034 from USD 157.98 billion in 2026.

The e-learning is digitally delivered educational content and interactive platforms that facilitate formal and informal learning across academic corporate and individual contexts. It leverages internet based technologies, including learning management systems video conferencing artificial intelligence and mobile applications to enable asynchronous and synchronous instruction. Behavioral shifts are equally significant with the 68% of adults aged 25 to 44 engaged in some form of digital upskilling in the past year driven by labor market volatility, as per the study. This ecosystem operates within a dynamic policy environment where state education departments increasingly recognize digital credentials and the Department of Labor promotes online apprenticeships. The emergence of infrastructure access learner demand and regulatory support defines the current landscape of e learning in the United States.

MARKET DRIVERS

Pervasive Digital Device Ownership and Internet Accessibility

The widespread access to connected devices and high speed internet forms a foundational driver of e-learning adoption is impacting positively on the growth of the United States e-learning market. As per the research, 96% of American adults own a cellphone and 85% possess a smartphone enabling mobile first learning experiences that transcend geographic and temporal barriers. These connectivity thresholds support bandwidth intensive applications such as live virtual classrooms interactive simulations and cloud based assessments without significant latency. This digital infrastructure enables consistent engagement with e learning platforms whether for K 12 homework college coursework or professional certification. Without such foundational access the scalability and equity of digital education would remain constrained particularly for non-traditional learners, who rely on flexible modalities to balance education with work and caregiving responsibilities.

Labor Market Pressures and Rapid Skill Obsolescence

The accelerating technological change and evolving employer expectations compel continuous reskilling creating sustained demand for accessible just in time e-learning solutions, which is also accelerating the growth of the United States e-learning market. As per the World Economic Forum’s Future of Jobs Report 44% of workers’ core skills are expected to be disrupted by 2027 with digital literacy data analysis and AI fluency becoming baseline requirements across industries. The Bureau of Labor Statistics documented that some employed adults participated in job related training in 2023 with those engagements occurring via online platforms due to scheduling flexibility and relevance to immediate role demands. Employers increasingly mandate digital upskilling with the Society for Human Resource Management reporting that many US companies, now require annual compliance or technical training delivered primarily through e-learning systems. This trend is amplified in high turnover sectors, such as retail and healthcare, where onboarding efficiency is critical.

MARKET RESTRAINTS

Digital Equity Gaps in Underserved Communities

The persistent disparities in device quality internet reliability and digital literacy is also hindering the growth of the United States e-learning market. The Federal Communications Commission acknowledged that while broadband availability has improved latency and upload speeds in remote areas often remain inadequate for interactive applications such as live proctoring or collaborative whiteboarding. Compounding this issue the National Skills Coalition found that 36% of adults without a college degree possess limited digital problem-solving abilities hindering navigation of complex learning platforms. Although, the Affordable Connectivity Program subsidized internet costs for millions enrollment gaps persist due to documentation hurdles and awareness deficits.

Credibility and Quality Assurance Deficits

The absence of universal standards for content rigor assessment validity and credential recognition undermines trust in many offerings, particularly in non-accredited or direct to consumers is also impacting negatively on the growth of the United States e-learning market. The Federal Trade Commission documented over 1200 consumer complaints in 2023 regarding misleading job placement claims by unaccredited coding bootcamps and certification mills. Employers remain cautious with the Society for Human Resource Management finding that only 48% of hiring managers consider non degree digital credentials equivalent to traditional qualifications even when skills align. This awareness is exacerbated by inconsistent assessment integrity with the International Journal of Educational Technology reporting that 63% of proctored online exams in 2023 used basic browser lockdown tools easily circumvented by screen sharing or secondary devices. Without robust third party validation mechanisms learners face uncertainty about return on investment while institutions struggle to differentiate high quality programs.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence for Personalized Learning

The strategic deployment of artificial intelligence to tailor educational experiences to enhance engagement efficacy and scalability is creating new opportunities for the growth of the US e-learning market. These systems analyze real time interaction data to adjust content difficulty pacing and modality recommending supplementary resources or alternative explanations based on individual knowledge gaps. Major platforms have operationalized this capability with Coursera launching an AI tutor in early 2024 that answers conceptual questions across 5000 courses using verified academic sources. Similarly, Khan Academy’s Khanmigo assistant provides step by step guidance in math and writing while maintaining pedagogical alignment with classroom standards as validated by Stanford University researchers. The Department of Education’s Office of Educational Technology endorsed such innovations in its 2023 AI Playbook citing evidence that personalized feedback loops reduce cognitive overload and improve long term retention. As AI models become more sophisticated in understanding learner intent and emotional state e learning can evolve from content delivery to cognitive coaching creating differentiated value beyond human instructor scalability.

Expansion of Workforce Development Partnerships with Public Sector

The strategic alliances between e-learning providers and federal state and local government agencies, unlock large scale adoption through funded upskilling initiatives targeting displaced workers and underserved populations. The expansion of workforce development is another attribute elevating the growth of the United States e-learning market. The Department of Veterans Affairs partnered with leading platforms to deliver free digital skills training to 50000 transitioning service members annually under the VET TEC program which reported an 82% job placement rate in 2023. State level efforts are equally impactful with California’s Community Colleges Online Education Initiative allocating 120 million dollars in 2023 to standardize and enhance digital course quality across 116 campuses serving 18 million learners. These public private collaborations de risk learner investment by covering tuition providing stipends and guaranteeing industry recognized credentials. They also generate longitudinal data on skill outcomes enabling continuous curriculum refinement. By embedding e learning into social safety net and economic development infrastructure providers secure stable demand while advancing national competitiveness in critical talent pipelines.

MARKET CHALLENGES

Student Disengagement and Completion Attrition

Low persistence and high dropout rates in self-directed e-learning environments pose a persistent challenge to educational efficacy and return on investment. The Journal of Online Learning and Teaching identified isolation as a key psychological barrier with 68% of surveyed adult learners citing absence of peer interaction as a primary reason for disengagement. While discussion forums and live sessions mitigate this to some extent algorithmic fatigue from excessive screen time further diminishes motivation. Without intentional design for community building intrinsic motivation and cognitive rest e learning risks becoming a passive content repository rather than an active transformational experience particularly for learners without strong self regulation skills.

Data Privacy and Algorithmic Bias Risks

The extensive collection and analysis of learner behavior data necessary for personalization and assessment introduce significant ethical and regulatory challenges around privacy consent and algorithmic fairness. The data privacy and algorithmic bias risks is additionally to decline the growth of the United States e-learning market. The Federal Trade Commission took enforcement action against two edtech companies in 2023 for retaining children’s biometric data from proctoring software beyond stated purposes violating the Children’s Online Privacy Protection Act. More insidiously algorithmic bias can reinforce inequities if training data reflects historical disparities. Similarly, recommendation engines may steer underrepresented learners away from advanced STEM pathways based on flawed correlation models. The Department of Education’s Civil Rights Office has opened investigations into three major platforms for potential discriminatory impacts.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Technology, Provider, Application, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | Adobe Inc., Cisco Systems Inc., Coursera, Inc., Docebo Inc., edX LLC, Oracle Corporation, Pearson Plc, SAP SE, Skillsoft, Udemy, Inc., and Others. |

SEGMENTAL ANALYSIS

By Technology Insights

The learning management systems segment was the largest by holding 34.2% of the US e-learning market share in 2025. The growth of the segment is majorly driven by the institutional mandate for centralized course administration assessment tracking and compliance reporting. As per the Educause Center for Applied Research, 96% of US higher education institutions rely on a single enterprise grade learning management system for credit bearing courses with Canvas Moodle and Blackboard collectively serving over 80% of enrollments. These platforms enable faculty to distribute content grade assignments and monitor participation while providing administrators with audit trails required for accreditation. Additionally, corporate adoption has surged with the Association for Talent Development finding that 77% of Fortune 500 companies use LMS platforms to manage mandatory training records and skill gap analyses. This institutional entrenchment ensures sustained demand as organizations prioritize interoperability data security and integration with student information or HR systems over fragmented point solutions.

The mobile e-Learning segment is esteemed to witness a fastest CAGR of 18.2% from 2026 to 2034 with the shift toward on the go learning among working professionals and Gen Z learners. As per the reports, 97% of Americans aged 18 to 29 own a smartphone and spend an average of 4.8 hours daily on mobile devices creating natural engagement windows for bite sized lessons. Platforms like Duolingo and LinkedIn Learning have optimized content for mobile consumption with Duolingo noting that 82% of its US user sessions occur on smartphones, as per reports. The rise of field based and frontline workforces who lack desktop access is also boosting the growth of the segment.

By Provider Insights

The services segment was accounted in holding 59.3% of the US e-learning market share in 2025 with the increasing complexity of digital learning ecosystems which demand implementation support customization and ongoing management beyond off the shelf content. As per the Educause Review over 70% of universities engaged external service providers in 2023 to redesign curricula for online delivery integrate analytics dashboards and train faculty on pedagogical best practices. These services ensure pedagogical fidelity and technical reliability that generic content cannot guarantee. In the corporate sector, the Association for Talent Development found that 84% of large employers outsource at least one aspect of their e learning operations including platform configuration content localization and learner support. Additionally, the shift toward outcome based contracts where vendors are paid per credential earned or job placement achieved has elevated the value of service expertise over static materials.

The content segment is projected to expand at a CAGR of 15.7% from 2026 to 2034 with the proliferation of microcredentialing in high velocity fields, such as artificial intelligence cybersecurity and renewable energy. The Burning Glass Institute reported that 71% of job postings requiring cloud engineering skills in 2023 specified certifications from AWS Microsoft or Google all of which rely on proprietary e learning content updated quarterly. The rise of user generated and peer reviewed content on platforms like GitHub Education and Coursera, where practitioners publish lab exercises and case studies. The National Science Foundation documented a 240% increase in STEM educators contributing open educational resources between 2020 and 2023 enabling rapid dissemination of emerging knowledge.

By Application Insights

The academic applications segment was accounted in holding 52.6% of the United States e-learning market share in 2025 with the policy mandated digital learning pathways across public education. As per the Education Commission of the States, 42 states now require high school students to complete at least one online course for graduation with Florida and Michigan operating statewide virtual schools serving over 200000 students each. Additionally, accreditation bodies like the Higher Learning Commission now evaluate online program quality as part of institutional reviews ensuring sustained investment. The Brookings Institution noted that 89% of community colleges now offer associate degrees fully online enabling access for rural adult and working learners. This systemic embedding across grade levels and governance structures ensures academic applications remain the bedrock of the US e learning ecosystem.

The government applications segment is projected to register a fastest CAGR of 19.4% from 2026 to 2034 with the expansion of federally funded upskilling initiatives targeting displaced workers and public sector employees. The Department of Veterans Affairs scaled its VET TEC program to train 55000 transitioning service members annually in cybersecurity and software development using approved e learning providers. Additionally, state and local governments are digitizing compliance training with the National Association of Counties documenting that 76% of county agencies migrated mandatory ethics and safety courses online in 2023 to reduce costs and ensure auditability. The 2023 Executive Order on AI further mandated digital literacy training for all federal employees accelerating contracts with e learning vendors.

COMPETITIVE LANDSCAPE

The US e learning market features intense rivalry among technology driven platforms traditional education publishers and university led initiatives all competing for learner attention institutional contracts and employer partnerships. Differentiation is achieved through content quality accreditation pathways technological sophistication and alignment with labor market outcomes. Large players leverage data analytics and AI to refine user experiences while niche providers focus on specialized domains such as healthcare compliance cybersecurity or trades training. Universities act as both collaborators and competitors by launching in house platforms or selectively outsourcing to third parties. Pricing models range from subscription and freemium to outcome based agreements tied to job placement or credential completion. Regulatory developments around data privacy credential recognition and federal financial aid eligibility add complexity to market entry and scaling. Despite fragmentation the trend favors consolidation as companies acquire complementary technologies content libraries or distribution channels to offer integrated end to end solutions. Success in this environment demands agility pedagogical integrity and demonstrable impact on learner advancement.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. e-learning market include

- Adobe Inc.

- Cisco Systems Inc.

- Coursera, Inc.

- Docebo Inc.

- edX LLC

- Oracle Corporation

- Pearson Plc

- SAP SE

- Skillsoft

- Udemy, Inc.

TOP PLAYERS IN THE MARKET

- Coursera operates as a global gateway connecting learners to university backed degrees and industry certifications with a strong foothold in the US e learning ecosystem. The company partners with over 300 institutions and corporations to deliver accredited programs in data science business and technology. It also enhanced its AI powered learning assistant to provide real time feedback and personalized pathways. These moves reinforce its role in bridging academic rigor with labor market relevance while extending its influence across 190 countries through localized content and multilingual support.

- Udemy serves millions of learners through a dynamic marketplace model where expert instructors create and distribute courses on diverse topics from programming to personal development. Its Udemy Business division has become a strategic asset for enterprises seeking scalable upskilling solutions. It also deepened partnerships with workforce development boards to align course catalogs with regional job demands.

- 2U leverages deep institutional partnerships to build and operate high quality online degree programs for nonprofit universities. The company manages technology marketing student support and instructional design enabling universities to extend their reach without building internal digital capacity. Following its acquisition of edX in 2022 2U launched a stackable credential platform allowing learners to progress from short courses to full degrees. This model positions 2U as a critical enabler of accredited online higher education both in the United States and internationally through its university network.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Leading participants in the US e learning market prioritize strategic institutional and corporate partnerships to enhance content credibility and distribution reach. They invest heavily in artificial intelligence to enable adaptive learning personalized recommendations and automated assessment. Companies increasingly bundle short form credentials with degree pathways to meet evolving workforce demands for modular and stackable learning. Geographic expansion is pursued through localized content multilingual interfaces and compliance with regional accreditation standards. Integration with enterprise HR and talent management systems allows seamless embedding of training into daily workflows. Continuous platform innovation including mobile optimization hands on labs and offline access addresses learner expectations for flexibility and practicality.

MARKET SEGMENTATION

This research report on the U.S. e-learning market has been segmented and sub-segmented into the following categories.

By Technology

- Online E-Learning

- Learning Management Systems

- Mobile E-Learning

- Rapid E-Learning

- Virtual Classroom

- Others

By Provider

- Services

- Content

By Application

- Academic

- K-12

- Higher Education

- Vocational Training

- Corporate

- Small and Medium Enterprises

- Large Enterprises

- Government

By Country

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

What is the U.S. e-learning market?

The U.S. e-learning market provides digital courses, training platforms, and educational content for corporate, academic, and individual learners across devices.

How does the U.S. e-learning market function?

The U.S. e-learning market operates through content creators, LMS providers, and platforms delivering interactive courses via web and mobile access.

What drives growth in the U.S. e-learning market?

The U.S. e-learning market expands due to remote work demands, flexible learning needs, tech advancements, and corporate skill development priorities.

Which segments lead the U.S. e-learning market?

The U.S. e-learning market features corporate training, K-12 education, higher education, and professional development as primary growth areas.

What role does corporate training play in the U.S. e-learning market?

Corporate training dominates the U.S. e-learning market by delivering scalable employee upskilling through customized online modules and assessments.

How important are LMS platforms in the U.S. e-learning market?

LMS platforms power the U.S. e-learning market by managing course delivery, tracking progress, and enabling personalized learning experiences.

What types define the U.S. e-learning market?

The U.S. e-learning market includes custom e-learning, gamified learning, microlearning, and responsive courses tailored for diverse audiences.

How does mobile learning fit the U.S. e-learning market?

Mobile learning enhances the U.S. e-learning market with on-demand access to bite-sized content via apps for busy professionals and students.

What trends shape the U.S. e-learning market?

The U.S. e-learning market follows AI personalization, VR simulations, gamification, and micro-credentials for modern skill acquisition.

What challenges face the U.S. e-learning market?

The U.S. e-learning market navigates engagement issues, content quality concerns, digital divides, and competition among platforms.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com