U.S Hair Care Market Size, Share, Trends & Growth Forecast Report - Segmented By Distribution Channel, Price Range, Product, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S Hair Care Market Size

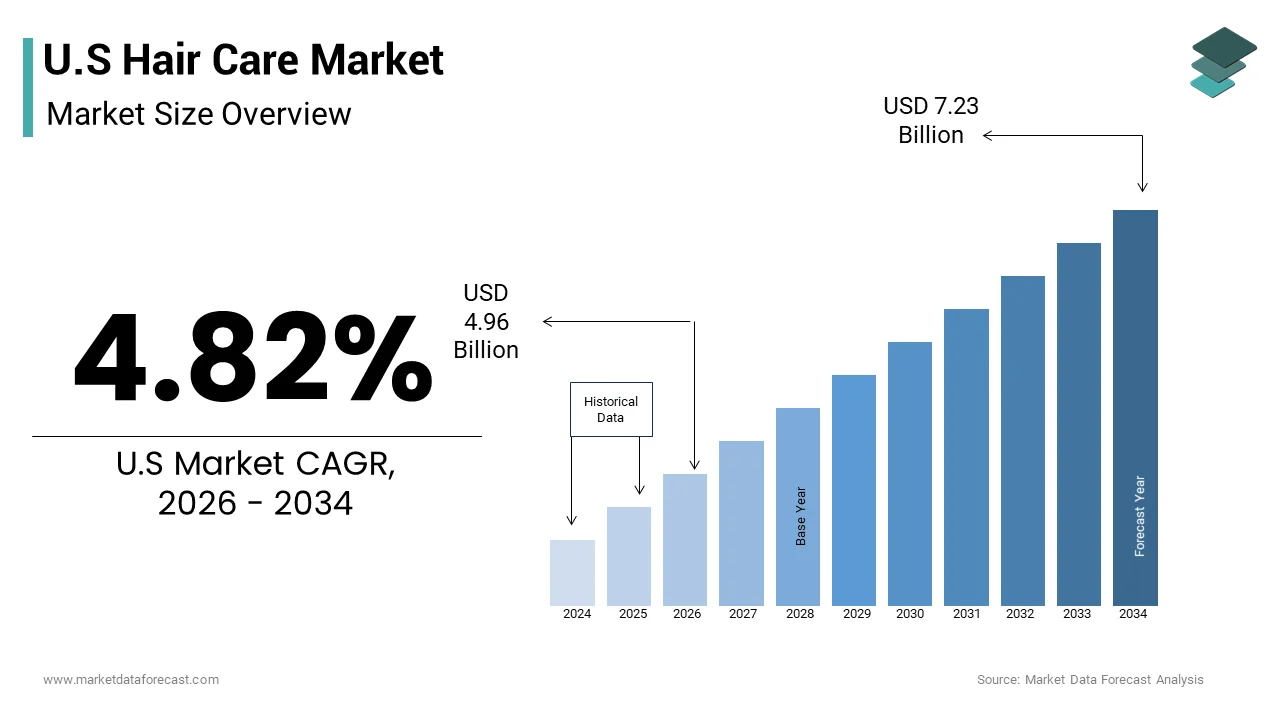

The US hair care market size was valued at USD 4.73 billion in 2025 and is anticipated to reach USD 4.96 billion in 2026 to reach USD 7.23 billion by 2034, growing at a CAGR of 4.82% during the forecast period from 2026 to 2034.

Current Market Overview and Definition

The hair care is the product designed for cleansing conditioning styling and treating the scalp and hair strands. The population exceeds 330 million individuals creating a vast and consistent base for personal care consumption. The high degree of fragmentation, where mass brands coexist with prestige and niche artisanal labels. The average annual expenditure on personal care products and services remains steady reflecting the essential nature of grooming in daily life. Consumer behavior is increasingly influenced by digital media trends and social platforms which dictate emerging styles and product preferences. The industry operates within a regulatory framework overseen by the Food and Drug Administration which ensures safety standards for cosmetic ingredients.

MARKET DRIVERS

Influence of Social Media and Digital Beauty Trends

The pervasive influence of social media and digital beauty trends by accelerating product discovery and shaping consumer preferences is fuelling the growth of the United States hair care market. Platforms, such as Instagram, TikTok, and YouTube, function as powerful marketing engines, where influencers and content creators showcase tutorials reviews and before and after transformations. This exposure creates viral demand for specific products and ingredients often leading to rapid sell outs and brand awareness. The digital recommendations significantly impact purchasing decisions with consumers trusting peer reviews and influencer endorsements over traditional advertising. The visual nature of these platforms allows brands to demonstrate efficacy and texture appealing to sensory driven buyers. Additionally, the rise of user generated content fosters community engagement where users share their hair journeys and solutions creating a feedback loop that drives innovation. Brands leverage these channels to launch targeted campaigns and collaborate with creators who resonate with niche audiences. This digital ecosystem reduces the barrier to entry for new brands and enables direct interaction with consumers.

Growing Demand for Personalized and Inclusive Solutions

The increasing demand for personalized and inclusive hair care solutions by addressing the diverse needs of a multicultural population is another attribute escalating the growth of the United States hair care market. Consumers are seeking products tailored to their specific hair type texture and scalp condition rather than relying on one size fits all formulations. As per the US Census Bureau, the demographic diversity of the United States continues to expand with significant populations identifying with various ethnic backgrounds that require specialized care. This trend is supported by the rise of diagnostic tools and algorithms that recommend customized regimens based on individual characteristics. A majority of consumers prefer brands that offer inclusive shade ranges and formulations for curly coily and textured hair. Manufacturers invest in research and development to create ingredients that cater to these diverse requirements ensuring efficacy and safety. The emphasis on inclusivity extends to marketing campaigns that feature models of various ethnicities and hair types fostering a sense of representation and belonging. This strategic focus on personalization enhances customer loyalty and satisfaction as individuals feel understood and valued by brands.

MARKET RESTRAINTS

Regulatory Scrutiny and Ingredient Safety Concerns

The increasing regulatory scrutiny and concerns regarding ingredient safety by imposing stricter compliance requirements and limiting formulation options is degrading the growth of United States hair care market. Consumers are becoming more aware of potentially harmful chemicals such as sulfates parabens and formaldehyde releasers leading to demands for cleaner and safer products. This regulatory pressure forces manufacturers to reformulate products which can be costly and time consuming. The lack of uniform standards for terms like natural and organic creates confusion and skepticism among buyers who struggle to verify claims. Compliance with varying state laws such as the California Safe Cosmetics Act adds complexity for national brands that must navigate a fragmented legal landscape. The potential for bans on specific ingredients restricts innovation and limits the toolbox available to chemists. Additionally, the cost of third party testing and certification increases operational expenses squeezing profit margins.

Economic Volatility and Price Sensitivity

The economic volatility and rising inflation by influencing consumer spending habits and increasing price sensitivity is additionally hindering the growth of the United States hair care market. During periods of economic uncertainty, households prioritize essential expenditures and may opt for lower cost alternatives or reduce the frequency of premium purchases. This inflationary pressure erodes disposable income leading shoppers to trade down from prestige brands to mass market or private label options. The value oriented segments often outperform premium categories during economic downturns as buyers seek affordability without compromising basic functionality. The rising cost of raw materials such as surfactants and packaging further strains manufacturer margins forcing difficult decisions regarding pricing strategies. Retailers respond by promoting discounts and bundle deals which can devalue brand equity and train consumers to wait for sales. Small and independent brands with limited financial reserves struggle to absorb these costs making them vulnerable to market fluctuations. The unpredictability of economic conditions complicates long term planning and inventory management.

MARKET OPPORTUNITIES

Expansion of Scalp Care and Skinification Trends

The expansion of scalp care by merging skincare principles with hair wellness routines is anticipated to enhance new opportunities for the growth of the United States hair care market. Consumers increasingly recognize the scalp as an extension of facial skin requiring similar attention and specialized treatments such as exfoliants serums and masks. The belief that a healthy scalp is the foundation for strong and vibrant hair. The products claiming scalp benefits are gaining traction with consumers willing to pay a premium for therapeutic effects. Brands can capitalize on this opportunity by developing formulations with active ingredients like salicylic acid niacinamide and hyaluronic acid that address specific scalp concerns. The integration of diagnostic tools and apps allows users to monitor scalp health and receive personalized recommendations enhancing engagement. Educational campaigns that emphasize the importance of scalp hygiene further drive adoption of these specialized products. Additionally, the crossover appeal to skincare enthusiasts expands the potential customer base beyond traditional hair care users.

Adoption of Sustainable and Eco Friendly Practices

The adoption of sustainable and eco-friendly practices by appealing to environmentally conscious consumers is also to elevate the expansion of the United States hair care market. Buyers are increasingly prioritizing brands that demonstrate commitment to reducing environmental impact through responsible sourcing biodegradable packaging and cruelty free certifications. The waste reduction initiatives have heightened awareness about the lifecycle of personal care products prompting demand for circular economy solutions. Manufacturers can innovate by introducing waterless formats such as shampoo bars and concentrated powders that minimize plastic usage and transportation emissions. The significant portion of consumers prefer brands with clear sustainability credentials and are willing to support companies that align with their values. The use of upcycled ingredients and renewable resources further enhances brand appeal and storytelling potential. Partnerships with environmental organizations and transparent reporting on carbon footprints build trust and loyalty among eco aware shoppers. Retailers are also expanding shelves dedicated to green beauty providing visibility for sustainable brands.

MARKET CHALLENGES

Supply Chain Disruptions and Raw Material Scarcity

The supply chain disruptions and scarcity of key raw materials is affecting production stability and cost efficiency, which is likely to decline the growth of United States hair care market. The industry relies on global sourcing for ingredients, such as botanical extracts oils and synthetic compounds, which are vulnerable to geopolitical tensions climate change and logistical hurdles. As per the Bureau of Labor Statistics, producer price indices for chemical and allied products have experienced volatility impacting the cost structure for manufacturers. Dependence on imported materials exposes companies to risks such as port congestion and trade restrictions that delay shipments. The supply chain constraints have led to extended lead times forcing brands to hold higher inventory levels which ties up capital. The rising cost of freight and energy further exacerbates these issues squeezing profit margins for both manufacturers and retailers. Companies struggle to pass these costs onto consumers without risking demand erosion in a competitive market. Additionally, the scarcity of specific natural ingredients due to overharvesting or poor harvests affects the availability of premium products. This instability complicates long term planning and formulation consistency making it difficult for brands to maintain product quality.

Counterfeit Products and Brand Integrity Issues

The proliferation of counterfeit hair care products by undermining brand integrity and posing safety risks to consumers is additionally to be a challenge for the growth of the United States hair care market. Illicit manufacturers produce fake versions of popular brands using substandard or harmful ingredients which are sold through unauthorized online marketplaces and social media platforms. The trade in counterfeit goods affects the personal care sector extensively causing significant revenue losses and reputational damage. Counterfeits often fail to meet safety standards leading to adverse reactions such as allergic responses or hair damage, which consumers may attribute to the authentic brand. The enforcement against online counterfeiters remains challenging due to the anonymity and cross border nature of these operations. The presence of fakes dilutes brand exclusivity and erodes consumer trust, making it difficult for legitimate companies to maintain loyalty. Brands must invest heavily in authentication technologies and legal actions to combat this issue which increases operational costs. Furthermore, the ease of accessing counterfeits online complicates the purchasing decision for buyers who fear receiving fraudulent items.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.82% |

| Segments Covered | By Distributional Channel , Price Range, Product and Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities. |

| Regions Covered | California, Washington, Oregon, New York & Rest of the United States |

| Market Leaders Profiled | Amway Corp., Ceremonia Inc., Combe Inc., Grove Collaborative Inc., Henkel AG and Co. KGaA, John Paul Mitchell Systems, Johnson and Johnson Services, Kao Corp., Knowlton Development Corp., Loreal SA, Max Private Label, Procter and Gamble Co., RainShadow Labs, Revlon Inc., Scotch Porter, SEEN Haircare, Shiseido Co. Ltd., The Estee Lauder Co. Inc., Tropical Products Inc., Unilever PLC |

SEGMENTAL ANALYSIS

By Distribution Channel Insights

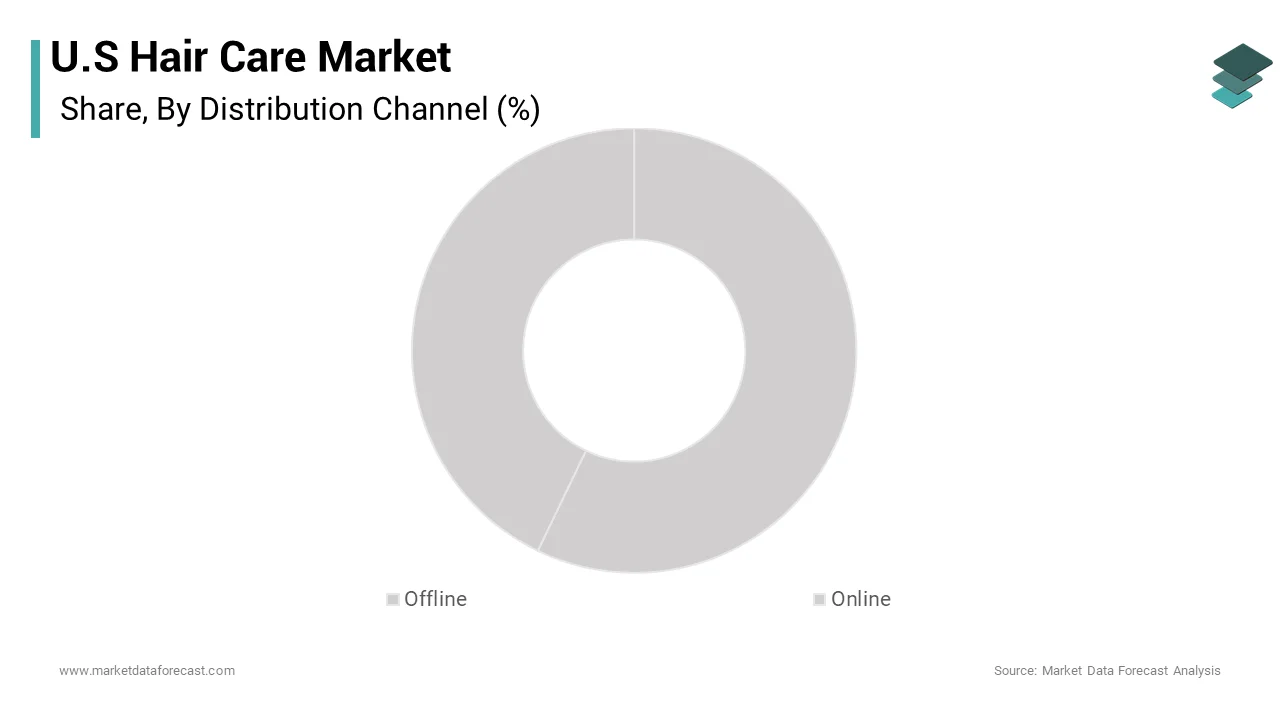

The offline distribution channel segment was accounted in holding a prominent share of the United States hair care market in 2025 with the immediate accessibility of products and the consumer preference for physical evaluation before purchase. Brick and mortar retailers, such as supermarkets, drugstores, and specialty beauty stores that allow shoppers to assess product texture scent and packaging which are critical factors in personal care decisions. As per the National Retail Federation approximately 80% of personal care purchases still occur in physical stores reflecting the entrenched habit of buying essentials during routine grocery trips. The presence of professional salon channels, where stylists recommend and sell high performance products directly to clients ensuring expert guidance and trust. The mass brands rely heavily on shelf visibility and promotional displays in retail environments to drive impulse buys and brand loyalty. The ability to obtain products instantly without shipping delays appeals to consumers with urgent needs such as running out of shampoo or conditioner. Additionally, the tactile experience of testing samples in stores reduces the risk of purchasing unsuitable products for specific hair types. Retailers leverage loyalty programs and in store events to enhance customer engagement and retention. This combination of convenience expert endorsement and sensory evaluation ensures that offline channels remain the primary destination for hair care purchases despite the growth of digital alternatives.

The online distribution channel is projected to register a fastest CAGR of 12.5% during the forecast period with the convenience of home delivery and the expansion of direct to consumer brands. E-commerce platforms offer an extensive selection of niche and specialized products that may not be available in local stores appealing to consumers seeking unique formulations. The online sales of beauty and personal care products have surged as shoppers increasingly prefer the ease of subscribing to regular deliveries for staple items. This trend is fueled by the rise of digital native brands that leverage social media marketing and influencer partnerships to reach targeted audiences effectively. According to Digital Commerce 360 data shows that subscription models for hair care products enhance customer retention and provide predictable revenue streams for manufacturers. The availability of detailed product descriptions user reviews and virtual consultation tools helps buyers make informed decisions about ingredients and suitability. Additionally, the integration of augmented reality apps allows users to visualize hair color changes or styles enhancing confidence in online purchases. The pandemic accelerated the shift toward digital shopping a habit that has persisted post pandemic due to time savings and competitive pricing.

By Price Range Insights

The mass segment was the largest by holding 34.8% of the United States hair care market hare in 2025 due to its affordability widespread availability and appeal to a broad consumer base. Products in this category are priced competitively making them accessible to households across various income levels ensuring consistent high-volume sales. The majority of American families allocate a modest portion of their budget to personal care favoring value oriented options for daily essentials. The presence of major brands in supermarkets drugstores and discount retailers, which serve as primary shopping destinations for most consumers. Promotional activities, such as buy one get one free offers and coupons further incentivize purchases, among price sensitive shoppers. The perception of established mass brands as reliable and effective sustains loyalty despite the emergence of premium alternatives. Additionally, private label offerings from retailers provide even lower cost options that attract budget conscious buyers. The sheer scale of distribution and marketing support for mass brands ensures high visibility and brand recognition.

The premium segment is expected to grow at an anticipated to register a fastest CAGR of 9.8% from 2026 to 2034 with the increasing consumer willingness to invest in high quality ingredients and specialized treatments. Buyers are prioritizing efficacy and luxury experiences seeking products that address specific concerns such as damage repair scalp health and color protection. The significant portion of consumers are trading up to prestige brands perceived, as offering superior performance and safer formulations. The individuals apply skincare standards to their hair routines demanding active ingredients like hyaluronic acid and peptides. The sales of prestige beauty products, including hair care have outpaced mass growth, reflecting the shift toward indulgence and self-care. Social media influencers and dermatologists play a crucial role in educating consumers about the benefits of premium formulations driving demand for scientifically backed solutions. The rise of clean beauty and sustainable packaging also appeals to affluent shoppers who value ethical production practices. Brands in this segment leverage exclusive distribution channels, such as salons and specialty boutiques to create an aura of exclusivity.

By Product Insights

The shampoo segment was accounted in holding 45.8% of the United States hair care market share in 2025 with its fundamental role in daily hygiene and the universal need for cleansing hair and scalp. As an essential consumable product, shampoo is purchased frequently by nearly every household ensuring a stable and high-volume demand baseline. The shampoo is the most widely used hair care product with almost all consumers reporting regular usage. The diversity of formulations available ranging from moisturizing and volumizing to clarifying and anti-dandruff options catering to varied hair types and concerns. Innovations, such as sulfate, free organic, and color safe formulas are attracting health conscious and specialized users. The integration of shampoo into daily routines makes it resistant to economic downturns as consumers prioritize basic grooming needs. Retailers prioritize shelf space for shampoo due to its consistent sales performance and broad appeal.

The hair color segment is expected to grow at a fastest CAGR of 7.5% during the forecast period with the rising popularity of at home coloring and the desire for personal expression. Consumers are increasingly experimenting with hair color to refresh their look cover gray hairs or follow trends, influenced by celebrities and social media. The sales of at home hair color kits have surged particularly among millennials and Gen Z, who view hair dye as a form of self-care and creativity. This growth is fueled by improvements in formulation technology that offer easier application better coverage and reduced damage compared to traditional products. The demand for natural and ammonia free hair colors is rising, as consumers seek safer and gentler alternatives. The influence of digital tutorials and virtual try on apps has lowered the barrier to entry for DIY coloring boosting consumer confidence. Additionally, the aging population contributes to steady demand for gray coverage products which are considered essential maintenance rather than optional cosmetics. Brands are launching innovative formats such as foams mousses and root touch up sprays that enhance convenience and precision.

COMPETITIVE LANDSCAPE

The competition in the United States hair care market is intense and characterized by a mix of multinational conglomerates and agile indie brands vying for consumer attention. Major players compete on brand equity innovation and distribution reach while smaller companies differentiate themselves through niche formulations and ethical practices. The rise of direct to consumer models has disrupted traditional retail channels forcing established brands to enhance their digital presence and customer engagement strategies. Price sensitivity varies across segments with value driven shoppers seeking affordability and enthusiasts willing to pay premiums for specialized treatments. Innovation in ingredients and sustainability provides competitive advantages for early adopters who can offer superior efficacy and environmental credentials. Regulatory compliance and ingredient transparency also influence competitive dynamics as consumers demand safer and cleaner products. Social media plays a pivotal role in shaping trends and driving viral demand for specific items.

KEY MARKET PLAYERS

A few of the dominating market players that are in the U.S hair care market are

- Amway Corp.

- Ceremonia Inc.

- Combe Inc.

- Grove Collaborative Inc.

- Henkel AG and Co. KGaA

- John Paul Mitchell Systems

- Johnson and Johnson Services

- Kao Corp.

- Knowlton Development Corp.

- Loreal SA

- Max Private Label

- Procter and Gamble Co.

- RainShadow Labs

- Revlon Inc.

- Scotch Porter

- SEEN Haircare

- Shiseido Co. Ltd.

- The Estee Lauder Co. Inc.

- Tropical Products Inc.

- Unilever PLC

Top Players In The Market

- The Procter and Gamble Company is a global leader in the hair care industry with a diverse portfolio including Head and Shoulders Pantene and Herbal Essences. The company leverages extensive research and development capabilities to innovate formulations that address specific scalp and hair concerns effectively. Recent actions include expanding its sustainable packaging initiatives and launching concentrated product lines to reduce environmental impact. Procter and Gamble strengthens its market position through strategic digital marketing campaigns that engage consumers on social media platforms. The firm invests in advanced technologies such as artificial intelligence to personalize product recommendations and enhance customer experience. These efforts ensure continued growth and brand loyalty across diverse demographics, while adapting to evolving consumer preferences for clean and effective hair care solutions globally.

- L'Oreal S.A. stands as a dominant force in the global beauty and hair care sector with prestigious brands such as Kerastase Redken and Garnier. The company focuses on scientific innovation and luxury positioning to cater to both professional salon clients and retail consumers. Recent strategies involve acquiring niche brands to diversify its portfolio and expand into emerging markets with high growth potential. L'Oreal invests heavily in digital transformation by enhancing e commerce platforms and virtual try on tools for hair color and styling. The firm strengthens its market position through partnerships with influencers and hairstylists who endorse products to targeted audiences. By committing to sustainability goals including responsible sourcing and eco friendly packaging L'Oreal aligns with modern consumer values. These initiatives enable the company to maintain leadership in the premium segment while driving innovation and inclusivity in the global hair care industry.

- Unilever PLC is a major global player in the hair care market with popular brands such as Dove TRESemme and Suave that appeal to mass market consumers. The company emphasizes affordability and accessibility ensuring its products are available in retail outlets worldwide. Recent actions include reformulating products to remove harmful chemicals and introducing plant based ingredients to meet demand for cleaner beauty options. Unilever strengthens its market position through robust supply chain optimization and cost efficiency measures that support competitive pricing. The firm leverages data analytics to understand consumer trends and tailor marketing strategies for different regions. These efforts enable the company to sustain growth in the mass market segment while adapting to changing regulatory standards and consumer expectations for ethical and effective hair care products globally.

Top Strategies Used By Key Market Participants

Key players in the United States hair care market prioritize product innovation by developing clean and sustainable formulations that align with consumer demand for transparency and safety. Companies focus on digital engagement through social media campaigns and influencer partnerships to build brand awareness and drive sales effectively. Strategic acquisitions of niche brands allow firms to expand their portfolios and reach diverse demographic segments with specialized needs. Manufacturers invest in personalized technology such as AI driven diagnostics to offer customized hair care solutions that enhance customer loyalty. Sustainability initiatives including recyclable packaging and responsible sourcing are central to corporate strategies to mitigate environmental impact. Omnichannel distribution models integrate online and offline experiences to maximize reach and convenience for shoppers.

MARKET SEGMENTATION

This research report on the U.S hair care market is segmented and sub-segmented into the following categories.

By Distribution channel

- Offline

- Online

By Price range

- Mass

- Premium

By Product

- Hair color

- Shampoo

- Conditioner

- Others

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Frequently Asked Questions

What is currently driving growth in the United States hair care market?

Rising consumer focus on personal grooming and premium products is driving market growth.

Why is hair care becoming more important among consumers in the United States?

Consumers are prioritizing appearance, hygiene, and hair health.

How would you explain the hair care market in simple terms?

It involves products used to clean, maintain, and style hair.

Where are hair care products most commonly used in the United States?

They are widely used at home, salons, and professional settings.

What makes hair care products important for daily routines?

They support hair health, cleanliness, and styling needs.

From a consumer perspective, are premium hair care products worth the investment?

Yes, many consumers value quality, effectiveness, and brand reputation.

What challenges are affecting the United States hair care market?

Intense competition and changing consumer preferences are key challenges.

How is consumer awareness influencing hair care product demand?

Increased awareness of ingredients and hair health is shaping buying decisions.

Which product segments contribute the most to hair care demand?

Shampoos, conditioners, and styling products are major contributors.

Is the United States hair care market growing steadily?

Yes, it is expanding with increasing demand for diverse and specialized products.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com