U.S. IoT Market Size, Share, Trends & Growth Forecast Report By Component, By End-Use Industry, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. IoT Market Size

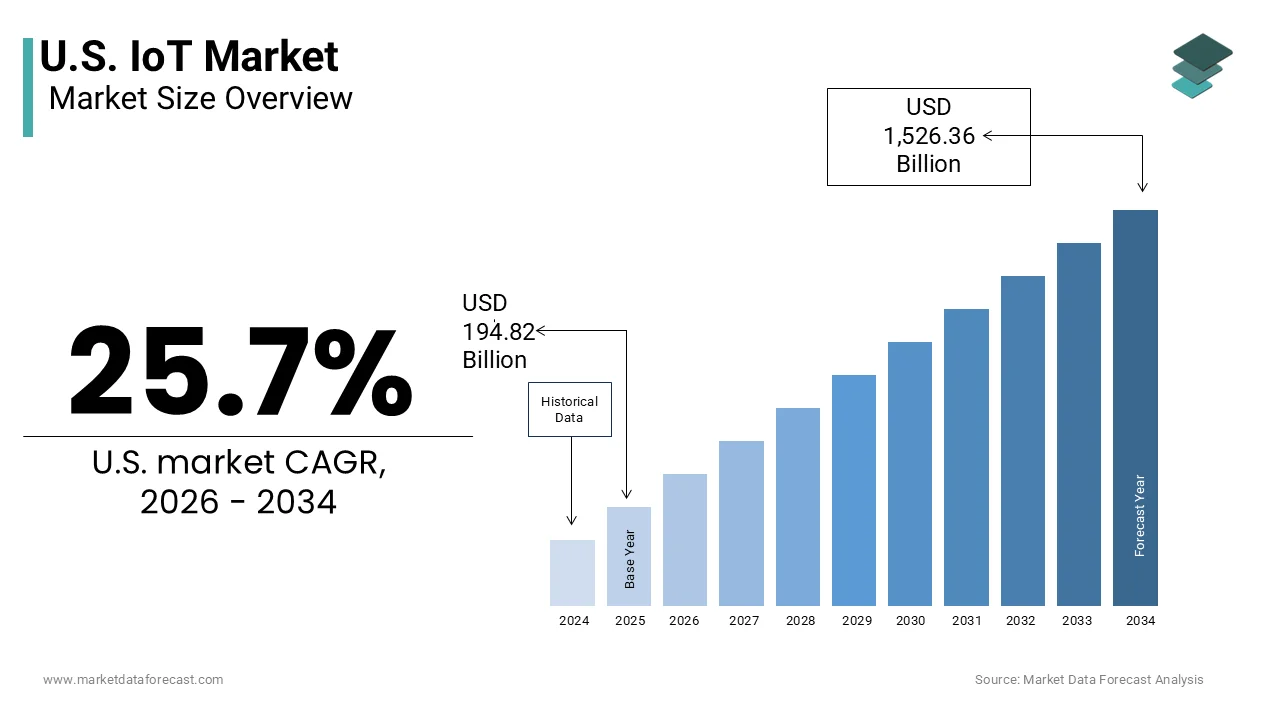

The United States Internet of Things Market was valued at USD 194.82 billion in 2025, is estimated to reach USD 244.89 billion in 2026, and is projected to reach USD 1,526.36 billion by 2034, growing at a CAGR of 25.7% from 2026 to 2034.

The Internet of Things is a digital infrastructure, industrial modernization, and consumer technology adoption, wherein physical devices embedded with sensors, software, and network connectivity generate and exchange data to enable intelligent decision-making across sectors. In recent years, the proliferation of 5G networks, edge computing capabilities, and cloud-based analytics platforms has significantly accelerated IoT deployment, particularly in manufacturing, healthcare, logistics, and smart infrastructure. Furthermore, the National Institute of Standards and Technology has actively developed cybersecurity frameworks tailored to IoT applications, reflecting the growing institutional recognition of this technology’s strategic importance. The integration of artificial intelligence with IoT systems has also matured, enabling predictive maintenance, remote monitoring, and real-time operational optimization. Urban centers such as New York, Los Angeles, and Chicago have implemented smart city initiatives that rely heavily on IoT for traffic management, waste collection, and energy efficiency.

MARKET DRIVERS

Accelerated Industrial Automation Drives Enterprise IoT Adoption

The imperative for operational efficiency and resilience in the US manufacturing and industrial sectors has led to widespread adoption of IoT-enabled automation systems, which is fuelling the growth of the United States Internet of Things market. Industrial facilities now deploy connected sensors, actuators, and control systems to monitor equipment health, optimize energy consumption, and reduce unplanned downtime. The Department of Energy notes that industrial facilities utilizing IoT-based predictive maintenance report up to 30% reduction in maintenance costs and 25% extension in asset lifespan. Moreover, the reshoring of supply chains spurred by geopolitical volatility has intensified demand for smart factory solutions that enhance visibility and control across production lines. Companies, such as General Electric and Honeywell, have embedded IoT platforms into their industrial real-time systems, enabling real-time data analytics at the edge. The National Association of Manufacturers confirms that over 65% of large US manufacturers have implemented IoT solutions in at least one production facility. This trend is further reinforced by federal incentives under the CHIPS and Science Act, which allocate funding for advanced manufacturing technologies, including IoT infrastructure. Consequently, industrial automation remains a cornerstone driver of IoT expansion in the United States.

Consumer Demand for Smart Home Ecosystems Fuels Residential IoT Growth

The proliferation of voice-enabled assistants, connected thermostats, and intelligent security systems has transformed the American household into a hub of IoT activity, driven by consumer expectations for convenience, energy savings, and safety. The growing consumer demand for smart home ecosystems is also escalating the growth of the United States Internet of Things market. According to the Consumer Technology Association, more than 55 million US households owned at least one smart home device in 2023, representing a compound annual growth rate of 12% since 2020. Energy efficiency incentives have played a pivotal role, with the Environmental Protection Agency reporting that ENERGY STAR-certified smart thermostats saved American consumers over one point two billion dollars in energy costs in 2022 alone. Major retailers, including Best Buy and Amazon, have expanded their smart home product portfolios, responding to heightened consumer interest, particularly among millennials and Gen Z demographics, who prioritize integrated digital living experiences. The Federal Trade Commission has also observed a surge in consumer data sharing willingness when tangible benefits, such as personalized climate control or e-emotion surveillance, are offered. Furthermore, insurance providers like Sta Farm and Allstat now offer premium discounts for homes equipped with IoT-enabled detectors and fire alarms, further incentivizing adoption.

MARKET RESTRAINTS

Persistent Cybersecurity Vulnerabilities Undermine Trust in IoT Deployments

The rising cybersecurity threats due to fragmented device standards, inconsistent update protocols, and limited built-in security features are restricting the growInternetited States internet of Things market in the United States. According to the study, over 45% of surveyed US organizations experienced an IoT-related security incident in 2023, with nearly 30% reporting data breaches originating from unsecured connected devices. Many consumer and industrial IoT products lack secure boot mechanisms, regular firmware updates, or encrypted communication channels, rendering them susceptible to botnet recruitment and lateral network infiltration. The Government Accountability Office has repeatedly found that manufacturers often prioritize time to market over security rigor, resulting in devices that remain vulnerable throughout their operational lifecycle. In healthcare settings, where IoT devices monitor vital signs and administer treatments, the stakes are especially high, as the Food and Drug Administration documented more than six hundred medical device cybersecurity vulnerabilities in 2022 alone. Moreover, the absence of mandatory federal regulations governing IoT device security allows substandard products to enter the market unchecked. Although the National Institute of Standards and Technology has published voluntary guidelines, adoption remains inconsistent across sectors. This persistent insecurity not only deters enterprise investment but also erodes consumer confidence, thereby constraining the scalability and reliability of IoT ecosystems across the United States.

Interoperability Deficits Impede Seamless IoT Integration Across Verticals

The absence of universal communication protocols and data standardization frameworks is additionally hindering the growth of the UnitedThings Internet of Things market. According to the research, over 60 distinct IoT communication standards are currently in use, ranging from Zigbee and Z-Wave to LoRaWAN and NB IoT, creating significant integration barriers for enterprises seeking unified solutions. In industrial environments, this lack of interoperability forces companies to maintain parallel systems or invest heavily in middleware translating between incompatible protocols. The Department of Commerce has noted that small and medium-sized manufacturers often abandon IoT adoption due to the complexity and cost of reconciling disparate vendor ecosystems. Even in smart city projects, municipal agencies struggle to aggregate data from traffic sensors, environmental monitors, and utility meters because each system operates on proprietary architectures. Although initiatives like the Connectivity Standards Alliance’s Matter protocol aim to unify smart home devices, adoption remains nascent, with less than 20% of new IoT products certified under the standard as of early 2024. The National Science Foundation emphasizes that without coordinated industry and government action to enforce baseline interoperability requirements, the full potential of IoT-driven data synergy will remain unrealized.

MARKET OPPORTUNITIES

Federal and State Smart Infrastructure Investments Unlock Municipal IoT Potential

The targeted public sector funding for intelligent infrastructure, across American cities and utilities, is ascribed to boost the growth of the United States Internet of Things market. According to the White House Office of Science and Technology Policy, the Bipartisan Infrastructure Law allocates over 65 billion dollars specifically for digital infrastructure, including smart grid modernization, intelligent transportation systems, and water quality monitoring networks. These investments enable municipalities to deploy IoT sensors at scale for real-time management of traffic flow, energy distribution, and environmental hazards. Similarly, the Environmental Protection Agency’s Clean Water State Revolving Fund now prioritizes IoT-enabled leak detection and pressure monitoring in aging water systems, which lose an estimated 6 billion gallons of treated water daily. Government-backed initiatives not only stimulate hardware and software demand but also establish regulatory sandboxes for testing next-generation IoT applications, thereby catalyzing private sector co-investment and accelerating nationwide digital transformation.

Healthcare System Digitization Creates High-Value IoT Use Cases

The ongoing digitization of the US healthcare delivery model for specialized IoT applications that enhance patient outcomes, reduce costs, and alleviate expected train is expected to fuel the growth of the United States Internet of Things market in the coming years. According to the Centers for Medicare and Medicaid Services, national health expenditures reached four point three trillion dollars in 2023, with administrative inefficiencies and chronic disease management accounting for a significant share of waste. Remote patient monitoring devices now enable continuous tracking of glucose levels, cardiac rhythms, and respiratory function, reducing hospital readmissions by as much as 38%, as documented by the Agency for Healthcare Research and Quality. Furthermore, the Food and Drug Administration has cleared more than a hundred IoT-based medical devices since 2020, including ingestible sensors and wearable ECG patches, reflecting regulatory support for innovation. Hospitals are also integrating asset tracking systems to locate infusion pumps, wheelchairs, and staff in real time, improving operational throughput.

MARKET CHALLENGES

Legacy Infrastructure Incompatibility Hinders Industrial IoT Scalability

The US industrial base operates on decades-old machinery and control systems that lack native connectivity or modern data interfaces, thereby obstructing seamless IoT integration, which is expected to limit the growth of the United States internet of things market. Retrofitting these legacy assets with IoT sensors and gateways often proves cost-prohibitive or technically unfeasible due to proprietary protocols, mechanical obsolescence, and spatial constraints. In sectors such as oil and gas and chemical processing, where safety certifications restrict hardware modifications, the challenge intensifies, with operators forced to maintain parallel manual and digital workflows. The Occupational Safety and Health Administration has documented cases where attempts to overlay IoT monitoring on outdated pressure relief systems led to calibration errors and false alarms. Moreover, the absence of standardized retrofit kits forces companies to develop custom engineering solutions, delaying deployment timelines by 6 to 18 months on average. This technological inertia disproportionately affects small and medium manufacturers who lack the capital and expertise to navigate complex integration pathways.

Workforce Skill Gaps Limit IoT Implementation and Maintenance Capacity

The rapid evolution of IoT technologies has outpaced the development of a sufficiently skilled technical workforce capable of designing, deploying, and sustaining complex connected systems, which, whichex connected systems is also impeding the growth of the United States internet of things market. According to the survey, there were unfilled cybersecurity and network engineering positions in 2023, with IoT-specific competencies, such as edge computing, protocol configuration, and sensor data validation, in particular short supply. In manufacturing settings, this deficit manifests as prolonged deployment cycles and suboptimal system utilization, as plant engineers struggle to interpret data streams or troubleshoot connectivity issues. The National Association of Manufacturers confirms that over 50% of small manufacturers cite lack of in-house expertise as a primary barrier to IoT adoption. The Department of Commerce has acknowledged this gap in its recent National Strategy for Advanced Manufacturing, calling for expanded public-private partnerships to build IoT workforce pipelines.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Component, End-Use Industry, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | Amazon Web Services Inc., Microsoft Corporation, IBM Corporation, Cisco Systems Inc., Intel Corporation, Oracle Corporation, SAP SE, General Electric Company, AT&T Inc., Siemens AG, PTC Inc., Honeywell International Inc. |

SEGMENTAL ANALYSIS

By Component Insights

The platform segment was the largest by holding 42.3% of the US IoT market share in 2025. Enterprises increasingly rely on cloud-based IoT platforms to manage millions of connected endpoints while ensuring elastic compute and storage capacity. These platforms reduce infrastructure overhead and allow rapid deployment of analytics workflows without on-premises hardware investment. The National Institute of Standards and Technology reports that cloud native IoT architectures lower the total cost of ownership by up to 35% over five years compared to legacy on-site systems. Additionally, built-in security features like device attestation and encrypted data pipelines address critical compliance requirements under frameworks such as NIST SP 800 213. The scalability of these platforms has proven vital in sectors like logistics, where real-time fleet telemetry from tens of thousands of vehicles must be processed simultaneously. This combination of cost efficiency, regulatory alignment, and operational agility solidifies the platform segment’s leadership in the US IoT component landscape.

The services segment is projected to expand at a CAGR of 21.3% from 2026 to 2034. As cyber threats targeting connected devices proliferate, organizations are outsourcing security operations to specialized service providers. According to the Cybersecurity and Infrastructure Security Agency, 63% of US enterprises engaged third-party IoT security services in 2023, up from 39% in 2020. These services include continuous vulnerability scanning, device behavior monitoring,g and incident response orchestration tailored to IoT environments. The Government Accountability Office notes that managed security services reduce breach response time by an average of 72 hours compared to in-house teams lacking IoT-specific tooling. Healthcare providers rely on these services to comply with HIPAA requirements for connected medical devices , with over 80% of hospital systems contracting external IoT security vendors, as per data from the American Hospital Association.

By End-use Industry Insights

The manufacturing industry accounted in holding 28.4% of the US IoT market share in 2025. US manufacturers are aggressively implementing Industry 4.0 frameworks that rely fundamentally on IoT connectivity to synchronize machine workflows and analytics. According to the National Association of Manufacturers, 82% of large US manufacturing facilities operated at least one smart factory line in 2023, up from 54% in 2020. These deployments integrate thousands of sensors on CNC machines, robotic arms, and conveyors, feeding real-time data to centralized dashboards. Companies like Caterpillar and John Deere embed IoT modules directly into heavy machinery, enabling remote diagnostics and usage-based service contracts. Federal initiatives under the CHI Real-Time Act further accelerate adoption by subsidizing digital transformation in critical manufacturing subsectors. This convergence of economic pressure, technological maturity,y and policy support cements manufacturing’s position as the dominant IoT end-use industry in the United States.

The sustainable energy sector segment is projected to grow at a CAGR of 24.7% throughout the forecast period. The integration of solar wind and battery storage into the US power grid necessitates real-time monitoring and control capabilities that only IoT can provide. According to the Department of Energy, over 110 gigawatts of distributed solar capacity were installed across US homes and businesses by the end of 2023, requiring dynamic grid balancing. Utilities deploy IoT sensors on inverters, transformers, and feeders to detect voltage fluctuations and reroute power flows instantaneously. The North American Electric Reliability Corporation confirms that grid operators using IoT-based distributed energy resource management systems reduced curtailment events in 2023, enhancing renewable utilization. Programs like California’s Self Generation Incentive Program mandate IoT telemetry for all subsidized storage systems, ensuring grid compliance. As the Inflation Reduction Act channels billions into clean energy infrastructure, I oT becomes the nervous system of the modern grid, driving unprecedented adoption in this sector.

COMPETITIVE LANDSCAPE

The US IoT market features intense competition characterized by a blend of technology giants, specialized startups, and industrial incumbents vying for dominance across verticals. Major cloud providers such as Microsoft, Amazon, and Google compete on platform scalability and AI integration, while networking firms like Cisco and Qualcomm emphasize secure connectivity and edge infrastructure. Simultaneously, hundreds of niche players offer specific solutions in healthcare, agriculture,e and logistics, creating a highly fragmented yet innovative ecosystem. Competitive differentiation hinges on interoperability, security compliance, and cost of ownership rather than price alone. Strategic alliances, w, ith syw th integtors,telecooperatorsars and regulatory bodies further shape market dynamics. The absence of universal standards allows for rapid innovation but also complicates enterprise adoption.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. IoT Market include

- Amazon Web Services Inc.

- Microsoft Corporation

- IBM Corporation

- Cisco Systems Inc.

- Intel Corporation

- Oracle Corporation

- SAP SE

- General Electric Company

- AT&T Inc.

- Siemens AG

- PTC Inc.

- Honeywell International Inc.

TOP LEADING PLAYERS IN THE MARKET

- Microsoft plays a pivotal role in the US IoT market through its Azure IoT suite,e which offers end-to-end cloud-based services for device connectivity,y data ingestion, and AI-driven analytics. The company has significantly expanded its edge computing capabilities, enabling real-time processing in remote industrial and retail environments. In recent years, Microsoft has deepened in,tegrations wit,h operAI-drivenechnology vendors and launched industry specific accelerators for the manufacturin,g,, healthcare, and energy sectors. Its partnership with semiconductor firms to optimize low-power RTOS for low-power devices further strengthens its hardware and software ecosystem. Microsoft industry-specific contributions to global IoT standard,ization efforts through alliances like the Industrial Internet Consortium, ensuring interoperability and security across international deployments.

- Amazon Web Services dominates the IoT infrastructure landscape with AWS IoT Core, a scalable managed cloud service that securely connects billions of devices worldwide. The company continuously enhances its edge offerings through AWS IoT Greengras,s allowing local compute and machine learning inference without constant cloud dependency. Recently,y AWS introduced sustainability-focused IoT tools enabling enterprises to monitor carbon emissions and energy usage across supply chains. It has also expanded its device qualification program to accelerate time to market for hardware partners. Glocross-borderupports cross border IoT deployments with localized data residency and compliance frameworks, making it a preferred choice for multinational corporations seeking consistent IoT operations across regions, including North America, Europe, pe and Asia.

- Cisco Systems leverages its networking heritage to deliver secure and scalable IoT infrastructure for industrial and enterprise environments across the United States. Its IoT Operations Platform provides centralized management for diverse device types while integrating with existing IT and OT systems. Cisco has recently intensified its focus on cybersecurity by embedding zero-trust principles into its IoT gateways and edge routers. The company launched new cellular and Wi-Fi 6-enabled industrial routers tailored for smart city and transportation use cases. Globally, Cisco collaborates with telecom operators and municipal governments to deploy large-scale IoT networks, particularly in smart utilities and public safety. Its acquisition of IoT analytics firms and investment in developer ecosystems underscore its commitment to building a comprehensive and secure IoT value chain.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the US IoT market primarily employ strategic partnerships to develop industry-specific solutions and accelerate time to market. They invest heavily in research and development to enhance edge AI capabilities and cybersecurity protocols. Acquisitions of niche IoT software and hardware firms enable the rapid expansion of their technology portfolios. Companies also focus on platform interoperability by adopting open standards and joining consortia like the Connectivity Standards Alliance. Additionally, they offer managed services and consulting to lower adoption barriers for small and medium enterprises. Cloud providers integrate IoT offerings with broader enterprise software suites to drive cross-selling.

MARKET SEGMENTATION

This research report on the US IoT market is segmented and sub-segmented into the following categories

By Component

- Platform

- Services

By End-Use Industry

- Manufacturing

- Sustainable Energy

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com