U.S Jewelry Market Size, Share, Trends & Growth Forecast Report By Product, Material, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S Jewelry Market Size

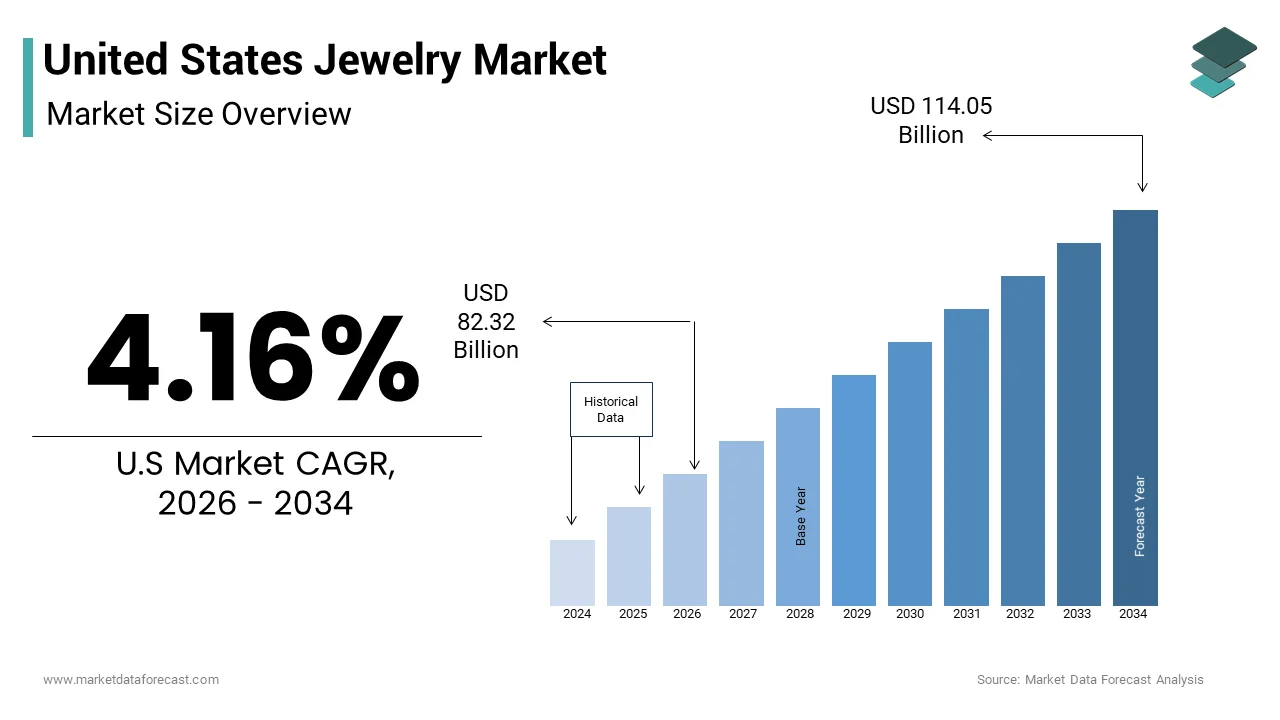

The U.S jewelry market size was valued at USD 79.03 billion in 2025 and is anticipated to reach USD 82.32 billion in 2026 to reach USD 114.05 billion by 2034, growing at a CAGR of 4.16% during the forecast period from 2026 to 2034.

Current Market Overview and Definition

Jewelry refers to decorative items worn for personal adornment. These objects are typically attached to the body or clothing and include common forms like rings, necklaces, bracelets, earrings, and brooches. This market is deeply intertwined with cultural traditions emotional expression and economic indicators serving as both a store of value and a symbol of status. As per the Bureau of Labor Statistics, average consumer expenditure on jewelry and watches is approximately $485 annually per household, reflecting its status as a notable discretionary expense. The market definition extends beyond mere ornamentation to include investment grade diamonds precious metals and ethically sourced gemstones that appeal to conscientious consumers. According to the US Census Bureau, retail sales data indicates consistent demand for luxury goods despite broader economic fluctuations, highlighting the resilience of the jewelry and luxury category. The industry is characterized by a blend of established heritage brands and emerging direct to consumer entities that leverage digital platforms for engagement. Consumer behavior is increasingly influenced by transparency in sourcing and sustainability practices which redefine brand loyalty. Data from the Federal Reserve shows that household wealth levels correlate strongly with jewelry purchases suggesting that asset accumulation drives high end sales. The market also responds to demographic shifts such as delayed marriages and self gifting trends which alter traditional purchase occasions. Understanding this ecosystem requires analyzing the interplay between raw material availability craftsmanship innovation and evolving consumer values that prioritize authenticity and ethical production methods in modern adornment.

MARKET DRIVERS

Rising Disposable Income Fuels Luxury Consumption

The increase in disposable income among American households is one of the major reasons for the growth of the United States jewelry market. This enables greater expenditure on non essential luxury items. Economic stability is improving, leading consumers to invest more in high-value pieces. They often purchase these to signify personal achievement or commemorate significant life events. As per the Bureau of Economic Analysis, while disposable personal income has grown, personal saving rates have trended downward to below 4 percent as consumers prioritize spending over saving. This financial capacity supports the purchase of diamond engagement rings gold chains and premium watches which often require substantial upfront investment. According to the Federal Reserve Bank of St Louis the growth in household net worth has directly correlated with increased retail sales in luxury categories including jewelry. Higher income brackets tend to prioritize quality and brand heritage leading to sustained demand for established luxury houses. Furthermore, the aspiration to maintain social status through visible symbols of wealth drives continuous consumption among affluent demographics. The ability to afford custom designs and rare gemstones enhances the appeal of exclusive collections that cater to niche preferences. This economic empowerment also facilitates the trend of self purchasing where individuals buy jewelry for themselves rather than receiving it as gifts. Thus, the correlation between income growth and jewelry sales remains robust ensuring steady market expansion driven by consumer confidence and financial security.

Cultural Significance of Gift Giving Sustains Demand

The entrenched cultural tradition of gift-giving during holidays, anniversaries, and milestones is the main force behind the expansion of the United States jewelry market. This creates predictable spikes in demand. Jewelry remains a preferred gift choice due to its perceived permanence emotional value and universal appeal across diverse demographics. As per the National Retail Federation holiday spending surveys indicate that jewelry consistently ranks among the top desired gifts with billions of dollars spent annually during the fourth quarter. Occasions such as Valentine’s Day Mother’s Day and Christmas drive significant sales volumes as consumers seek meaningful tokens of affection. According to Jewelers of America (JA) 2024 State of the Industry reports and De Beers Diamond Insight reports, approximately 65% to 70% of jewelry purchases are intended as gifts for occasions such as engagements, weddings, anniversaries, and holidays. The emotional connection associated with jewelry enhances its desirability as a gesture of love commitment or appreciation. Engagement and wedding related purchases further anchor the market with diamond rings representing a major segment of sales. The ritualistic nature of these exchanges ensures recurring revenue streams for retailers who tailor marketing campaigns to specific events. Additionally, the rise of milestone celebrations such as graduations and promotions expands the scope of gift giving beyond romantic contexts. This cultural imperative sustains baseline demand even during economic downturns as consumers prioritize sentimental purchases over other discretionary items.

MARKET RESTRAINTS

Volatility in Precious Metal Prices Impacts Affordability

The fluctuation in prices of gold silver and platinum impedes the growth of the United States jewelry market. This affects production costs and retail pricing stability. These precious metals are fundamental components of fine jewelry and their market values are subject to global economic conditions geopolitical tensions and currency fluctuations. As per the London Bullion Market Association gold prices have experienced considerable volatility reaching historic highs that increase the cost of raw materials for manufacturers. This instability forces retailers to adjust prices frequently which can deter price sensitive consumers and disrupt purchasing plans. According to the World Gold Council higher metal prices often lead to reduced consumer demand for heavier pieces as buyers opt for lighter alternatives or postpone purchases. The unpredictability of input costs complicates inventory management and profit margin forecasting for jewelers who must balance competitiveness with profitability. Additionally, rising prices may shift consumer preference towards fashion jewelry made from base metals or synthetic materials which offer lower price points. This substitution effect limits the growth potential of the fine jewelry segment particularly among middle income households. The inability to hedge effectively against metal price swings exposes smaller retailers to financial risk making it challenging to maintain consistent offerings. So, material cost volatility remains a persistent challenge that constrains market expansion and influences consumer behavior.

Ethical Sourcing Concerns Deter Conscious Consumers

Growing awareness of the ethical sourcing and environmental impact of mining activities is restraining the United States jewelry market. This is causing hesitation among socially conscious buyers. Consumers are increasingly scrutinizing the supply chain origins of diamonds and gemstones seeking assurance that their purchases do not support conflict or exploitation. According to research, approximately 90 percent of Millennial and Gen Z consumers prefer jewelry brands with transparent and certified ethical practices. The complexity of verifying supply chains and the prevalence of uncertified stones create trust deficits that hinder sales for traditional retailers. According to the Kimberley Process Certification Scheme, while the initiative has significantly reduced the trade of traditional "conflict diamonds," concerns regarding broader human rights violations in mining regions persist. This skepticism leads some buyers to avoid natural stones altogether in favor of lab grown alternatives or vintage pieces. The lack of standardized labeling and verification mechanisms across the industry further complicates consumer decision making. Retailers face increased pressure to implement rigorous due diligence processes which raise operational costs and compliance burdens. Failure to demonstrate ethical credibility can result in reputational damage and loss of customer loyalty in an era where values driven purchasing is paramount. These concerns act as a barrier to growth for companies that cannot adequately prove the integrity of their sourcing practices.

MARKET OPPORTUNITIES

Expansion of Lab Grown Diamond Segment

The rapid adoption of lab grown diamonds creates big potential for the United States jewelry market. This offers a sustainable and affordable alternative to mined stones. These chemically identical gems appeal to environmentally conscious consumers who seek ethical options without compromising on quality or brilliance. As per the Federal Trade Commission guidelines updates have clarified labeling requirements for lab grown diamonds enhancing consumer confidence and market transparency. The production cost of lab grown diamonds has decreased significantly making them accessible to a broader audience including younger buyers entering the engagement ring market. According to a study, the market share of lab grown diamonds in the US has surged with double digit annual growth rates driven by competitive pricing and marketing efforts. Major retailers are expanding their collections to include these stones catering to the demand for larger carat weights at lower price points. This segment allows jewelers to attract customers who previously could not afford natural diamonds thereby expanding the total addressable market. The ability to customize colors and cuts in a controlled laboratory environment offers unique design possibilities that differentiate products. Furthermore, the reduced environmental footprint of lab grown stones aligns with corporate sustainability goals enhancing brand image. Retailers can capture value from a growing demographic that prioritizes ethics and affordability by embracing this technology. This approach also maintains the emotional significance of diamond jewelry.

Digitalization and E Commerce Integration

The integration of advanced digital technologies and e commerce platforms offers a transformative opportunity for the United States jewelry market. This enhances customer experience and reach. Online sales channels allow retailers to showcase extensive catalogs to a global audience breaking geographical barriers and reducing overhead costs associated with physical stores. As per the US Census Bureau e commerce sales in the jewelry sector have grown substantially with consumers increasingly comfortable purchasing high value items online. Virtual try on tools augmented reality applications and high resolution imaging enable shoppers to visualize products accurately boosting confidence in digital transactions. According to Shopify data, jewelry brands utilizing immersive technologies like AR try-on report a 94 percent higher conversion rate and a 40 percent lower return rate compared to traditional online listings. Social media platforms serve as powerful marketing engines where influencers and user generated content drive discovery and engagement. Direct to consumer models facilitate personalized interactions and custom design services that foster loyalty and repeat business. The use of data analytics helps retailers understand consumer preferences and optimize inventory management efficiently. Additionally, omnichannel strategies that blend online convenience with offline expertise create seamless shopping journeys. By leveraging digital innovation, jewelers can tap into younger demographics who prefer digital-native experiences. This allows them to expand their market presence beyond traditional brick-and-mortar limitations.

MARKET CHALLENGES

Counterfeit Products and Intellectual Property Theft

The proliferation of counterfeit jewelry and intellectual property theft poses a critical challenge to the United States jewelry market. This undermines brand integrity and consumer trust. Fake products flooded with inferior materials deceive buyers and dilute the value of authentic luxury brands causing significant financial losses. As per the International Chamber of Commerce and the OECD, the trade in counterfeit goods affects the jewelry and watch sector extensively, with an estimated 25 billion dollars in lost revenue annually. The ease of replicating designs and selling them through unregulated online marketplaces makes enforcement difficult for legitimate manufacturers. According to the Jewelers Vigilance Committee identifying and combating fake certificates and misrepresented stones requires substantial investment in authentication technologies and legal resources. Consumers who inadvertently purchase counterfeits may lose confidence in the market overall leading to hesitation in future high value purchases. The lack of uniform global standards for hallmarking and certification exacerbates the problem allowing fraudulent items to circulate freely. Brand reputation suffers when counterfeit items fail to meet quality expectations associating negative experiences with the original label. Protecting intellectual property involves continuous monitoring and litigation which strains resources particularly for smaller independent designers. This pervasive issue distorts market dynamics by creating unfair competition and eroding the perceived exclusivity of genuine luxury jewelry. Addressing this challenge requires collaborative efforts among industry stakeholders regulators and technology providers to secure supply chains.

Supply Chain Disruptions and Raw Material Scarcity

Supply chain disruptions and scarcity of raw materials are a formidable obstacle to the United States jewelry market. This affects production timelines and product availability. Dependence on imported gemstones and precious metals exposes the industry to geopolitical instability trade restrictions and logistical bottlenecks. As per the US Geological Survey reliance on foreign sources for critical minerals like gold and colored gemstones creates vulnerabilities during international conflicts or export bans. Recent global events have highlighted the fragility of long distance supply chains leading to delays and increased transportation costs. According to the Gemological Institute of America fluctuations in mine output due to environmental regulations or labor strikes further constrain the availability of high quality stones. These shortages force manufacturers to compete for limited resources driving up input prices and squeezing profit margins. The inability to secure consistent supplies hampers the ability to fulfill large orders and meet seasonal demand peaks. Retailers face the risk of stockouts which can drive customers to competitors with better inventory management. Diversifying supply sources is complex and time consuming requiring extensive vetting and relationship building with new suppliers. Additionally, the push for ethical sourcing limits the pool of acceptable vendors adding another layer of complexity. Navigating these logistical and material constraints requires strategic planning and resilience to maintain operational continuity in an unpredictable global environment.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.16% |

| Segments Covered | By Product, Material, and Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities. |

| Regions Covered | US, Canada, and the Rest of North America |

| Market Leaders Profiled | Buccellati (Compagnie Financière Richemont SA), Cartier, LVMH Moët Hennessy Louis Vuitton, Chow Tai Fook Jewellery Company Limited, Damas Jewellery, Graff, Harry Winston Inc (The Swatch Group), HStern, Louis Vuitton Malletier SAS, Pandora A/S, Rajesh Exports Ltd., Signet Jewelers, Swarovski AG, Titan Company |

SEGMENTAL ANALYSIS

By Product Insights

The ring segment was the largest segment in the United States jewelry market in 2025. This prominence of the segment is driven primarily by its central role in marriage proposals and wedding ceremonies which constitute a significant portion of industry revenue. Engagement and wedding rings are considered essential purchases for couples marking this life milestone creating a consistent and high value demand stream. As per The Knot annual real weddings study the average cost of an engagement ring in the United States exceeds 5000 dollars reflecting the willingness of consumers to invest heavily in this specific product category. This cultural imperative ensures that rings remain the most purchased jewelry item by value despite fluctuations in other discretionary spending areas. According to the Natural Diamond Council and retail data, diamonds remain the dominant choice, featured in approximately 86 percent of engagement rings sold in the U.S. The emotional significance attached to rings fosters brand loyalty and encourages upgrades or additions such as anniversary bands and eternity rings. Furthermore, the rise of custom design services allows consumers to create unique pieces that reflect personal stories enhancing the perceived value. Retailers focus heavily on this segment through targeted marketing campaigns during peak proposal seasons. The durability of rings as heirlooms also supports secondary market activity and insurance sales. This combination of cultural necessity high average transaction value and emotional attachment solidifies the ring segment as the dominant force in the US jewelry landscape.

The earrings segment is anticipated to witness the fastest CAGR of 6.5% between 2026 and 2034 due to changing fashion trends and the popularity of multiple ear piercings. Consumers are increasingly viewing ears as a canvas for self expression leading to the accumulation of various styles from studs to hoops and huggies. As per retail and consumer data, the trend of multiple ear piercings has surged, with over 65 percent of young adults in the U.S. sporting more than one piercing per ear. This trend drives repeat purchases as buyers seek to mix and match metals shapes and gemstones to create curated looks. The versatility of earrings allows them to transition seamlessly from casual daytime wear to formal evening events making them a practical addition to any jewelry collection. According to Vogue Business fashion editors note that ear stacking has become a major style movement influencing retail assortments and marketing strategies. The lower price point of many earring styles compared to rings or necklaces lowers the barrier to entry encouraging impulse buys and frequent updates to personal collections. Social media platforms amplify this trend by showcasing innovative styling techniques and new designs. Additionally, the introduction of hypoallergenic materials and comfortable closures appeals to sensitive skin types expanding the potential customer base. This dynamic interplay of fashion accessibility and social influence propels the earrings segment ahead of other categories in terms of growth velocity.

By Material Insights

In 2025, the gold segment continued to lead the United States jewelry market because of its timeless appeal, intrinsic value, and versatility in design applications across various jewelry types. The metal's resistance to tarnish and ability to be alloyed into different colors such as yellow white and rose gold make it a preferred choice for both everyday wear and special occasions. As per the World Gold Council demand for gold jewelry in the US remains robust with consumers viewing it as a stable store of wealth amidst economic uncertainty. The cultural significance of gold in gifting traditions particularly during holidays and milestones sustains its dominance in the market. According to the US Geological Survey gold imports for jewelry manufacturing continue to account for a substantial portion of total gold consumption in the country. The malleability of gold allows artisans to create intricate designs that appeal to diverse aesthetic preferences from minimalist modern styles to ornate vintage inspired pieces. Furthermore, the rise of recycled gold initiatives appeals to environmentally conscious buyers who seek sustainable luxury options. Major retailers emphasize karat purity and craftsmanship to justify premium pricing and differentiate their offerings. The liquidity of gold also provides consumers with a sense of security knowing that their jewelry retains residual value. This combination of aesthetic flexibility financial stability and cultural relevance ensures that gold maintains its position as the primary material in the US jewelry sector.

The lab grown diamonds segment is likely to experience the fastest CAGR of 15.7% over the forecast period owing to ethical considerations and affordability advantages over mined stones. These synthetic gems possess identical physical chemical and optical properties to natural diamonds but are produced in controlled environments reducing environmental impact and human rights concerns. As per the Federal Trade Commission updated guidelines have standardized labeling for lab grown diamonds increasing consumer trust and market transparency. The cost advantage allows buyers to purchase larger or higher quality stones within their budget appealing to millennial and Gen Z consumers who prioritize value and sustainability. According to sources, lab grown diamonds now account for a significant double digit percentage of total diamond jewelry sales in the US reflecting rapid adoption rates. Major jewelry chains have expanded their offerings to include extensive collections of lab grown pieces catering to this shifting preference. The ability to customize colors and cuts without the rarity constraints of mining enables innovative designs that attract younger demographics. Marketing campaigns emphasizing eco friendliness and technological innovation resonate with socially conscious shoppers. Additionally, the consistency in supply and quality control offered by laboratory production reduces variability and enhances retailer confidence. This convergence of ethical alignment economic benefit and technological advancement positions lab grown diamonds as the most dynamic growth driver in the jewelry material landscape.

COUNTRY LEVEL ANALYSIS

United States Market Analysis

The United States was the dominant market for jewelry in the North American region and accounted for a 85.3% share in 2025. This dominance of the US market is driven by its high consumer spending power and established retail infrastructure. Its dominant position is also reinforced by a culture that places significant emphasis on gift giving and personal adornment as symbols of status and affection. As per the US Census Bureau retail trade data indicates that jewelry stores generate billions of dollars in annual sales reflecting the deep integration of this category into the national economy. The market is characterized by a mature ecosystem where global luxury brands coexist with independent artisans and direct to consumer startups. According to the Bureau of Labor Statistics, employment in jewelry manufacturing and retail supports approximately 140,000 direct jobs, contributing to local economies across various states. Consumer behavior in the US is marked by a high adoption of digital shopping channels alongside traditional brick and mortar experiences creating an omnichannel environment. The presence of major industry events such as JCK Las Vegas facilitates networking and trend setting that influences global markets. Regulatory frameworks enforced by the Federal Trade Commission ensure fair labeling and advertising practices protecting consumers and maintaining market integrity. High disposable income levels among American households enable sustained demand for both fine and fashion jewelry segments. The diversity of the population drives varied tastes and preferences encouraging innovation in design and material usage. This robust foundation ensures that the United States remains the central hub for jewelry consumption and trend dissemination in the region.

COMPETITIVE LANDSCAPE

The competition in the United States jewelry market is intense and fragmented characterized by a mix of large multinational corporations regional chains and independent artisans. Major retailers compete on brand reputation product variety pricing and customer service quality to capture market share. The rise of direct to consumer brands has disrupted traditional retail models by offering lower prices and transparent sourcing practices. Online platforms have lowered barriers to entry enabling smaller players to reach national audiences without significant physical infrastructure. Luxury brands differentiate themselves through exclusivity heritage and high craftsmanship while mass market retailers focus on affordability and accessibility. Price sensitivity among consumers drives promotional activities and discounting strategies particularly during holiday seasons. Innovation in design and material usage such as lab grown diamonds provides competitive advantages for early adopters. Customer experience remains a critical differentiator with personalized services and seamless omnichannel interactions driving loyalty. Regulatory compliance and ethical standards also influence competitive dynamics as consumers increasingly demand transparency. This complex landscape requires continuous adaptation and strategic innovation to maintain relevance and profitability.

KEY MARKET PLAYERS

A few of the market players that are dominating the United States jewelry market are

- Buccellati (Compagnie Financière Richemont SA)

- Cartier

- LVMH Moët Hennessy Louis Vuitton

- Chow Tai Fook Jewellery Company Limited

- Damas Jewellery

- Graff

- Harry Winston Inc (The Swatch Group)

- HStern

- Louis Vuitton Malletier SAS

- Pandora A/S

- Rajesh Exports Ltd.

- Signet Jewelers

- Swarovski AG

- Titan Company

Top Players In The Market

- LVMH stands as a global luxury powerhouse with its Watches and Jewelry division featuring iconic brands like Tiffany and Co and Bulgari. The conglomerate leverages its extensive retail network and marketing expertise to elevate brand prestige and drive international sales. Recent actions include integrating Tiffany into its high jewelry portfolio and launching exclusive collections that emphasize craftsmanship and heritage. LVMH focuses on enhancing customer experience through digital innovation and personalized services in flagship stores. The company invests heavily in sustainable sourcing initiatives to align with modern consumer values. By cross promoting jewelry lines within its broader luxury ecosystem LVMH strengthens brand visibility and attracts affluent clientele. Strategic expansions in key markets such as Asia and North America ensure continued growth. These efforts solidify its position as a leader in high end jewelry by combining artistic creativity with commercial acumen and operational excellence.

- Signet Jewelers operates as the largest retailer of diamond jewelry in the United States owning prominent banners such as Kay Zales and Jared. The company focuses on omnichannel strategies that blend physical store presence with robust e commerce capabilities to reach diverse customer segments. Recent initiatives involve expanding its private label offerings and enhancing digital tools for virtual consultations and custom designs. Signet prioritizes customer loyalty programs that drive repeat purchases and increase lifetime value. The firm actively promotes ethical sourcing standards to build trust and transparency with conscious consumers. By optimizing inventory management and leveraging data analytics Signet improves operational efficiency and responsiveness to market trends. Strategic partnerships with technology providers enable seamless online shopping experiences. These actions strengthen its market position by catering to evolving consumer preferences for convenience personalization and responsible luxury while maintaining its dominance in the mainstream jewelry sector.

- Chow Tai Fook Jewellery Group is a leading global jewelry retailer known for its extensive network of stores and strong brand recognition in Asia and increasingly in international markets. The company specializes in gold jewelry and diamonds offering a wide range of products that cater to various cultural preferences and occasions. Recent actions include expanding its retail footprint in North America and Europe to diversify its geographic revenue streams. Chow Tai Fook invests in innovative design collaborations and digital marketing campaigns to attract younger demographics. The group emphasizes quality control and craftsmanship to maintain its reputation for reliability and excellence. By adopting advanced manufacturing technologies and sustainable practices the company enhances production efficiency and environmental stewardship. Strategic acquisitions of complementary brands further broaden its product portfolio. These efforts reinforce its global presence and competitiveness by balancing traditional values with modern retail innovations and customer centric approaches.

Top Strategies Used By Key Market Participants

Key players in the United States jewelry market prioritize omnichannel retail strategies to seamlessly integrate online and offline shopping experiences for enhanced customer convenience. Companies focus on product differentiation through unique designs customizations and exclusive collections that appeal to specific demographic segments. Sustainability and ethical sourcing initiatives are prominently featured in marketing campaigns to build trust and align with consumer values. Brands leverage social media influencers and digital advertising to increase brand awareness and engage with younger audiences effectively. Investment in advanced technologies such as augmented reality for virtual try ons improves online conversion rates and reduces return risks. Loyalty programs and personalized services foster long term customer relationships and encourage repeat purchases. Strategic partnerships with designers and celebrities enhance brand prestige and visibility. These combined approaches allow firms to navigate competitive pressures and drive growth in a dynamic retail environment.

MARKET SEGMENTATION

This research report on the United States jewelry market is segmented and sub-segmented into the following categories.

By Product

- Necklace

- Ring

- Earrings

- Bracelet

- Others

By Material

- Gold

- Platinum

- Diamond

- Others

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Frequently Asked Questions

What is currently driving growth in the United States jewelry market?

Rising consumer spending on luxury goods and personal accessories is driving growth.

Why is jewelry demand increasing in the United States?

Consumers are seeking fashion, self-expression, and gifting options.

How would you explain the jewelry market in simple terms?

It involves the design, production, and sale of decorative accessories like rings and necklaces.

Where is jewelry most commonly purchased in the United States?

It is widely purchased through retail stores, online platforms, and specialty boutiques.

What makes jewelry important in consumer lifestyles?

It serves as a fashion statement, investment, and symbol of personal expression.

From a buyer’s perspective, is jewelry a valuable purchase?

Yes, it offers aesthetic value and, in some cases, long-term worth.

What challenges are affecting the United States jewelry market?

Fluctuating raw material prices and changing consumer preferences are key challenges.

How is e-commerce influencing jewelry sales in the United States?

Online platforms are increasing accessibility and convenience for buyers.

Which product segments contribute the most to jewelry demand?

Rings, necklaces, and bracelets are major contributors.

Is the United States jewelry market growing steadily?

Yes, it is expanding with rising disposable income and fashion trends.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com