U.S Mattress Market Size, Share, Trends & Growth Forecast Report - Segmented By Product, Mattress Size, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S Mattress Market Size

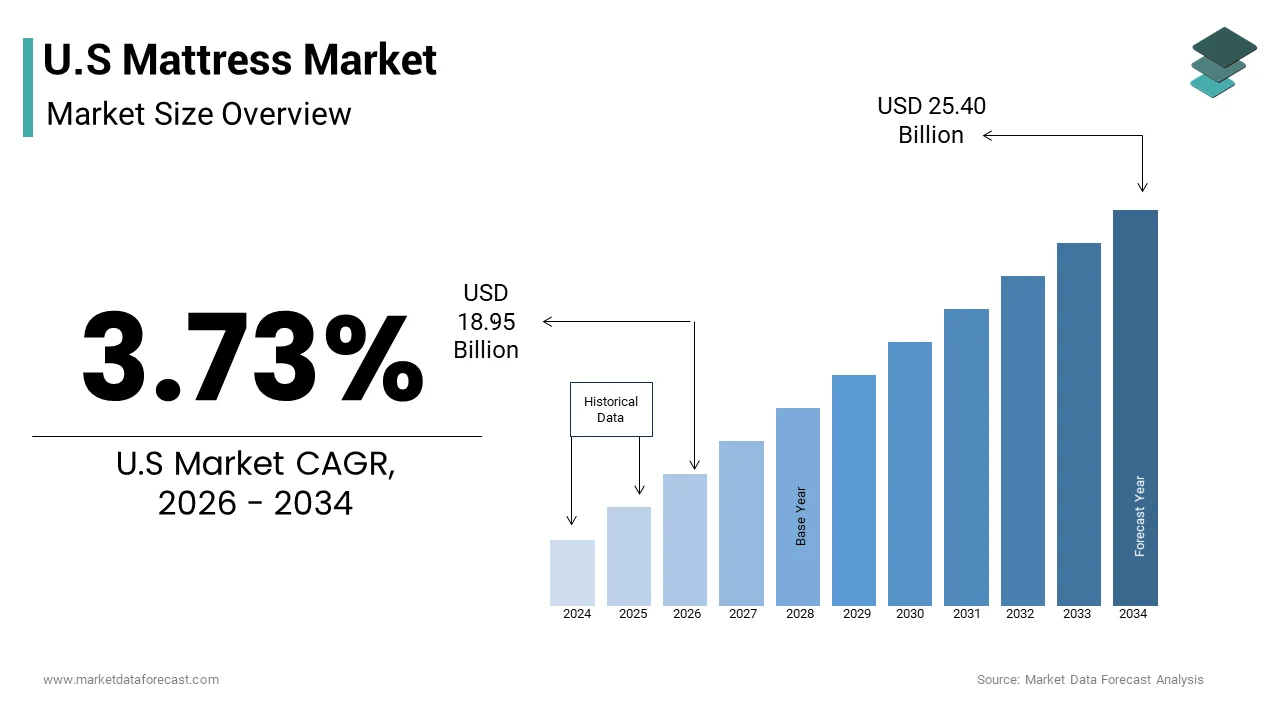

The U.S mattress market size was valued at USD 18.27 billion in 2025 and is anticipated to reach USD 18.95 billion in 2026 to reach USD 25.40 billion by 2034, growing at a CAGR of 3.73% during the forecast period from 2026 to 2034.

Current Market Overview and Definition

A mattress is a large, rectangular pad designed to support a person while they lie down or sleep. This market includes a diverse array of products including innerspring memory foam latex and hybrid constructions that cater to varying consumer preferences for comfort support and durability. The International Sleep Products Association (ISPA) recommends evaluating mattresses for replacement every 5 to 7 years, though actual consumer replacement cycles often extend to 8–10 years or longer. Industry forecasts identify housing turnover as a primary and reliable driver of mattress demand alongside replacement needs. The market is characterized by a significant shift from traditional brick and mortar retail to direct to consumer models which leverage digital marketing and compressed packaging logistics. According to the US Census Bureau, housing turnover strongly influences initial mattress purchases. However, the number of Americans moving annually has declined to approximately 26–27 million (based on 2022–2023 data), significantly lower than the historical high of 40 million. Consumer behavior is increasingly influenced by health consciousness with sleep quality recognized as a pillar of overall wellness. Data from the Centers for Disease Control and Prevention indicates that one in three US adults do not get enough sleep, a statistic frequently cited by the sleep products industry to contextualize the growing demand for ergonomic and therapeutic solutions. The industry also faces evolving regulatory standards regarding fire safety and chemical emissions which shape product development. Understanding this landscape requires analyzing the interplay between technological innovation in materials supply chain efficiency and the growing consumer expectation for transparency and sustainability in product sourcing and disposal.

MARKET DRIVERS

Rising Prevalence of Sleep Disorders and Health Awareness

The increasing awareness of sleep hygiene and the rising prevalence of sleep disorders are primary drivers for the United States mattress market. This transforms mattresses from mere furniture into health essential items. Consumers are actively seeking solutions for conditions such as insomnia back pain and sleep apnea which has elevated the importance of ergonomic support and pressure relief in purchasing decisions. As per the Centers for Disease Control and Prevention (CDC), approximately 33.2% of U.S. adults report getting less than the recommended seven hours of sleep per night, highlighting a public health crisis that drives product innovation. This health consciousness prompts individuals to invest in higher quality mattresses that offer specialized features such as zoned support cooling technologies and hypoallergenic materials. According to the National Sleep Foundation, annual surveys indicate that a significant majority of consumers consider mattress comfort critical to their overall health and well-being. The medical community increasingly prescribes specific sleep environments for patients with chronic pain further validating the therapeutic value of premium mattresses. Additionally, the integration of sleep tracking technology into smart mattresses allows users to monitor their sleep patterns and adjust settings for optimal rest. This convergence of health technology and consumer education creates a robust demand for advanced sleep solutions that promise improved physical and mental health outcomes thereby sustaining market growth.

Growth in Housing Market and Household Formation

The dynamics of the housing market and rates of household formation fundamentally fuel expansion of the United States mattress market. This is because new residences necessitate initial furniture purchases. Each new household typically requires multiple mattresses creating a direct correlation between real estate activity and mattress sales volume. As per the U.S. Census Bureau, approximately 1.527 million new housing units were completed at a seasonally adjusted annual rate as of early 2026, providing a substantial base for initial mattress installations. Furthermore, the trend of younger generations delaying marriage but forming independent households contributes to steady demand for entry level and mid range products. Data from the Joint Center for Housing Studies of Harvard University indicates that millennial and Gen Z cohorts are entering the housing market in significant numbers, driving renovation and furnishing activities. The rental market also plays a crucial role with millions of renters moving annually and requiring portable and affordable sleep solutions. Landlords and property managers frequently replace mattresses between tenants to maintain property standards ensuring a consistent replacement cycle. Additionally, the rise of remote work has led many individuals to upgrade their home environments including bedrooms to create comfortable living spaces. This structural demand from housing transitions ensures a baseline level of market activity that is less susceptible to short term economic fluctuations compared to discretionary spending categories.

MARKET RESTRAINTS

Volatility in Raw Material Costs and Supply Chain Disruptions

The volatility in raw material costs and ongoing supply chain disruptions hampers the growth of the United States mattress market. This squeezes profit margins and causes production delays. Key inputs such as polyurethane foam steel coils latex and wood frames are subject to global commodity price fluctuations and logistical bottlenecks. As per the Bureau of Labor Statistics producer price indices for foam and plastic materials have experienced double digit percentage increases in recent years forcing manufacturers to either absorb costs or raise prices. These price hikes can deter price sensitive consumers and slow down replacement cycles. According to the International Sleep Products Association supply chain inconsistencies have led to extended lead times for components affecting the ability of retailers to maintain adequate inventory levels. The reliance on imported materials exposes the industry to geopolitical tensions and trade policy changes which can abruptly alter cost structures. Transportation costs for bulky mattress items have also risen due to fuel price variability and driver shortages impacting final delivery expenses. Manufacturers face challenges in forecasting demand accurately amidst these uncertainties leading to inefficiencies in production planning. The inability to pass on all cost increases to consumers without risking demand erosion limits revenue growth. Consequently, the industry must navigate a complex web of logistical and financial pressures that constrain operational flexibility and profitability.

Environmental Regulations and Waste Management Concerns

Increasingly stringent environmental regulations and growing concerns regarding waste management hinder the expansion of the United States mattress market. This imposes additional compliance costs and operational complexities. Mattresses are bulky difficult to recycle and often end up in landfills where they take up significant space and decompose slowly. As per the Environmental Protection Agency millions of mattresses are discarded annually in the US with recycling rates remaining relatively low compared to other consumer goods. Several states have implemented extended producer responsibility laws that require manufacturers to fund and manage mattress recycling programs adding to operational expenses. According to the Mattress Recycling Council these initiatives while environmentally beneficial increase the cost of doing business for producers who must invest in collection infrastructure and processing facilities. Consumers are also becoming more discerning about the environmental footprint of their purchases preferring brands with sustainable practices which may require costly certifications and material substitutions. The transition to eco friendly materials such as organic latex and recycled steel often involves higher production costs and limited supplier availability. Compliance with varying state and local regulations creates a fragmented legal landscape that complicates national distribution strategies. Failure to adhere to these standards can result in fines and reputational damage. Thus, the burden of environmental stewardship acts as a financial and logistical constraint on market expansion.

MARKET OPPORTUNITIES

Expansion of Smart Mattress and Sleep Technology Integration

The integration of smart technology into mattresses opens up a pathway for the growth of the United States market. This appeals to tech savvy consumers seeking data driven insights into their sleep health. Smart mattresses equipped with sensors can track heart rate breathing patterns and movement offering personalized feedback and adjustments to improve sleep quality. As per the Consumer Technology Association the wearable and smart home health sectors are experiencing robust growth indicating a receptive audience for connected sleep solutions. These products often integrate with mobile applications and smart home ecosystems allowing users to automate lighting temperature and sound based on their sleep stages. According to sources, the global smart bedding landscape is projected to grow significantly, driven by increasing health consciousness and technological adoption. Manufacturers can differentiate their offerings by providing subscription based services for advanced analytics and coaching creating recurring revenue streams beyond the initial hardware sale. Partnerships with healthcare providers and insurance companies could further validate the therapeutic benefits of smart mattresses potentially opening new reimbursement channels. The ability to offer over the air updates ensures that products remain current with the latest software enhancements extending their lifecycle and value proposition. Mattress companies can transform a static product into an interactive health platform by leveraging the Internet of Things. This allows them to capture value in the burgeoning digital wellness economy.

Adoption of Sustainable and Eco Friendly Materials

The growing consumer preference for sustainable and eco friendly materials boosts prospects for differentiation and brand loyalty in the United States mattress market. Buyers are increasingly prioritizing products made from organic cotton natural latex and recycled components that minimize environmental impact and reduce exposure to harmful chemicals. Mattress manufacturers can capitalize on this trend by obtaining certifications such as Global Organic Textile Standard and CertiPUR US which verify the safety and sustainability of their materials. Brands that transparently communicate their supply chain practices and environmental commitments can build trust and attract conscientious buyers. The development of biodegradable foams and recyclable designs addresses end of life concerns aligning with circular economy principles. Retailers can highlight these attributes in marketing campaigns to appeal to millennials and Gen Z demographics who value ethical consumption. By innovating in material science and sustainable manufacturing processes companies can command higher price points and foster long term customer relationships based on shared values. This shift towards sustainability not only mitigates regulatory risks but also enhances brand equity in a competitive landscape.

MARKET CHALLENGES

Intense Competition from Direct to Consumer Brands

The surge of direct-to-consumer (DTC) mattress brands has intensified competition in the United States mattress market. This growth challenges traditional retailers with aggressive pricing and convenient shopping experiences. These online native companies bypass intermediaries allowing them to offer lower prices and streamlined logistics such as bed in a box delivery. Traditional brick and mortar retailers struggle to match the convenience and cost efficiency of these digital competitors leading to margin compression and store closures. According to research, the market has become saturated with numerous DTC entrants creating noise and confusion for consumers who face overwhelming choices. This saturation drives up customer acquisition costs as brands compete heavily for digital advertising space and influencer partnerships. The ease of market entry for new players means that established brands must continuously innovate and invest in marketing to maintain visibility. Price wars and promotional discounts erode profitability across the sector making it difficult for companies to sustain healthy margins. Additionally, the lack of physical trial opportunities for some online brands can lead to higher return rates which impose logistical burdens and costs. Navigating this hyper competitive environment requires strategic agility and strong brand differentiation to retain market share.

Complexity of Last Mile Logistics and Returns

The complexity of last mile logistics and the high cost of handling returns are serious barriers to the United States mattress market. This is due to the bulky and heavy nature of the products. Delivering mattresses to consumers homes requires specialized transportation and handling which increases shipping costs and the risk of damage. As per the Council of Supply Chain Management Professionals last mile delivery accounts for a significant portion of total logistics costs particularly for large items. The rise of the bed in a box model has mitigated some issues but returns remain a logistical nightmare as compressed mattresses often cannot be repackaged for resale. According to reverse logistics experts the cost of processing a mattress return can exceed the value of the product itself due to disposal fees and labor. Many companies offer generous trial periods to compete which inadvertently encourages higher return rates as consumers treat homes as showrooms. The environmental impact of disposing of returned mattresses also poses reputational and regulatory risks. Managing this reverse flow efficiently requires sophisticated logistics networks and partnerships with recycling facilities which add operational complexity. Failure to optimize these processes can lead to significant financial losses and customer dissatisfaction. Therefore, balancing customer friendly return policies with cost effective logistics management remains a critical operational hurdle for industry participants.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.73% |

| Segments Covered | By Product, Mattress Size, and Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities. |

| Regions Covered | US, Canada, and the Rest of North America |

| Market Leaders Profiled | empur Sealy International Inc., Serta Simmons Bedding LLC, Sleep Number Corporation, Purple Innovation Inc., Casper Sleep Inc., Resident (Home of Nectar, DreamCloud), Saatva Inc., Helix Sleep LLC, Brooklyn Bedding LLC, Avocado Green Brands LLC, Tuft & Needle (SSB), Ashley Furniture Industries LLC, King Koil Mattress Co., Spring Air International, The Original Mattress Factory, Leesa Sleep LLC, GhostBed (Nature's Sleep), Bear Mattress, Cocoon by Sealy, Zinus Inc. |

SEGMENTAL ANALYSIS

By Product Insights

The foam and memory foam segment held majority share of the United States mattress market in 2025. This supremacy of the segment is credited to its superior pressure relief capabilities and adaptability to various body types which appeals to a broad consumer base. Moreover, this material conforms closely to the sleeper’s contours reducing pressure points on hips and shoulders which is particularly beneficial for individuals with chronic pain or joint issues. As per the International Sleep Products Association (ISPA), innerspring and hybrid mattresses account for the largest share of unit shipments in the US, while foam mattresses remain a significant secondary category reflecting widespread acceptance among consumers seeking value. The versatility of foam allows manufacturers to create products at various price points from budget friendly options to premium luxury models ensuring accessibility for different income levels. According to Consumer Reports memory foam mattresses consistently receive high ratings for motion isolation making them ideal for couples where one partner moves frequently during sleep. The development of open cell foam technologies has addressed previous concerns about heat retention enhancing breathability and comfort. Additionally, the compatibility of foam with the bed in a box distribution model has facilitated its dominance in the online retail sector where compressed packaging reduces shipping costs and simplifies delivery. The ability to layer different densities of foam enables precise customization of firmness and support levels catering to diverse sleep preferences. This combination of therapeutic benefits affordability and logistical efficiency solidifies foam as the primary choice for American consumers replacing traditional innerspring constructions in many households.

The hybrid mattress segment is estimated to register the fastest CAGR of 8.5% over the forecast period owing to the demand for balanced support and comfort that combines the best features of innerspring and foam technologies. Hybrid mattresses feature a core of pocketed coils topped with layers of memory foam or latex providing the bounce and airflow of springs with the contouring and pressure relief of foam. As per Mattress Firm sales data hybrid models have become the top recommended category by sleep experts due to their ability to cater to a wide range of sleep positions and body weights. This segment appeals to consumers who find all foam mattresses too soft or lacking in edge support while traditional innersprings are too firm or prone to motion transfer. According to sources, the average selling price of hybrid mattresses is higher than pure foam or innerspring options contributing significantly to revenue growth despite lower unit volumes compared to budget foam models. The innovation in coil design such as zoned support systems and enhanced durability further distinguishes hybrids as premium products. Marketing efforts emphasize the longevity and comprehensive support of hybrids attracting buyers willing to invest in long term sleep health. The expansion of hybrid offerings by both direct to consumer brands and traditional retailers ensures widespread availability and consumer awareness. This strategic positioning as a superior all around solution drives the rapid adoption of hybrid mattresses across diverse demographic groups.

By Mattress Size Insights

The queen size mattress segment dominated the United States market in 2025. This dominance of the segment is driven by its optimal balance of space comfort and compatibility with standard bedroom dimensions in most American homes. It provides sufficient room for two adults to sleep comfortably without occupying excessive floor space making it the default choice for master bedrooms and guest rooms alike. As per the International Sleep Products Association (ISPA), queen size mattresses account for nearly 50 percent of total mattress unit sales in the US, reflecting their status as the industry standard. The prevalence of queen size beds in new housing developments and apartment complexes reinforces this demand as builders design bedrooms to accommodate this specific footprint. According to the U.S. Census Bureau, the average size of new single-family homes has contracted slightly since 2023, yet primary bedroom dimensions in most new builds continue to be designed with sufficient clearance for king-size mattresses. The affordability of queen size mattresses compared to king or California king options makes them accessible to a broader range of consumers including first time homebuyers and renters. Retailers stock the widest variety of styles and brands in queen size ensuring that consumers have ample choices regardless of their preferred material or brand. The ease of finding matching bedding and accessories for queen sizes further simplifies the purchasing process for consumers. This combination of spatial efficiency cost effectiveness and widespread availability ensures that the queen size segment remains the cornerstone of the US mattress market.

The king size mattress segment is anticipated to witness the fastest CAGR of 6.2% between 2026 and 2034 due to increasing consumer preference for spacious sleeping arrangements and the trend toward larger master suites in modern home designs. Living standards are rising, leading homeowners to invest more in renovations. These projects often prioritize maximizing personal comfort and minimizing sleep disturbance between partners. As per the National Association of Home Builders new custom homes increasingly feature expanded master bedrooms capable of accommodating king size beds and additional furniture such as seating areas or large dressers. This architectural shift facilitates the adoption of larger mattresses among affluent demographics who view sleep space as a luxury amenity. According to Better Homes and Gardens surveys indicate that a growing percentage of couples prefer king size beds to reduce the likelihood of waking each other during the night thereby improving overall sleep quality. The aging population also contributes to this trend as older adults often experience more sleep disruptions and benefit from the extra space to move freely. Additionally, the rise of work from home arrangements has led some individuals to use larger beds for both sleeping and daytime relaxation increasing the perceived utility of king size models. Manufacturers respond by offering premium king size options with advanced features appealing to consumers willing to pay for enhanced comfort. This convergence of lifestyle changes and housing trends propels the king size segment forward.

By End User and Distribution Channel Insights

The residential end user segment was the largest segment in the United States mattress market in 2025. Factors such as the fundamental necessity of sleep surfaces for every household and the regular replacement cycle associated with personal use are supporting the prominence of this segment. Every individual requires a mattress for daily rest making residential demand consistent and resilient to economic fluctuations compared to commercial sectors. The average replacement interval of seven to ten years ensures a steady stream of recurring purchases as older mattresses lose support and hygiene standards decline. Also, the emotional and health related motivations behind residential purchases often lead to higher willingness to invest in quality upgrades compared to bulk commercial buys. Trends such as the focus on wellness and home improvement further stimulate residential spending as consumers view their bedrooms as sanctuaries for relaxation and recovery. The diversity of residential needs ranging from twin beds for children to king sizes for couples creates a broad product landscape that supports various manufacturers and retailers. This vast and continuous demand base establishes the residential segment as the undisputed leader in the market.

The Business to Consumer retail distribution channel segment is likely to experience the fastest CAGR of 9.5% during the forecast period. This quick surge of the segment is propelled by convenience competitive pricing and innovative marketing strategies. The shift away from traditional brick and mortar showrooms towards digital platforms allows consumers to research compare and purchase mattresses from the comfort of their homes eliminating the pressure of in person sales tactics. The bed in a box revolution pioneered by digital native brands has streamlined logistics reducing shipping costs and enabling risk free trials with easy return policies that alleviate purchase anxiety. Moreover, the ability to offer transparent pricing and detailed product information online empowers consumers to make informed decisions based on reviews and specifications rather than salesman recommendations. Traditional retailers are responding by enhancing their own online presence and offering omnichannel services such as buy online pick up in store. This digital transformation expands market reach and lowers barriers to entry for new brands driving rapid growth in the B2C channel.

COUNTRY LEVEL ANALYSIS

United States Mattress Market Analysis

The United States remained in the lead in the toy market and captured a 85.1% share in 2025. This leading position of the US market is supported its high consumer spending power and established retail infrastructure. Its commanding position is driven by a culture that prioritizes comfort and wellness with sleep health recognized as a critical component of overall quality of life. As per the International Sleep Products Association the US mattress industry generates billions of dollars in annual revenue reflecting the deep integration of sleep products into the national economy. The market is characterized by intense competition between traditional legacy brands and agile direct to consumer startups driving continuous innovation in materials and distribution models. According to the US Census Bureau housing turnover and new construction rates directly influence mattress demand with millions of units sold annually to new homeowners and renters. Consumer behavior in the US is marked by a high adoption of e commerce channels with online sales growing faster than offline retail. The presence of major industry trade shows and associations facilitates knowledge sharing and standard setting that influences global trends. Regulatory frameworks regarding fire safety and environmental sustainability shape product development and compliance strategies for manufacturers. High disposable income levels among American households enable sustained demand for premium and luxury mattress segments. The diversity of the population drives varied preferences for firmness size and material encouraging a wide range of product offerings. This robust foundation ensures that the United States remains the central hub for mattress innovation and consumption in the region.

COMPETITIVE LANDSCAPE

The competition in the United States mattress market is intense and characterized by a mix of established legacy brands and agile direct to consumer startups. Major retailers compete on product innovation pricing and customer service quality to capture market share in a saturated landscape. The rise of online native brands has disrupted traditional retail models by offering lower prices and convenient home delivery options. Legacy manufacturers respond by enhancing their digital presence and adopting bed in a box formats to remain competitive. Price sensitivity among consumers drives frequent promotional activities and discounting strategies particularly during holiday seasons. Innovation in materials such as latex foam and hybrid constructions provides competitive advantages for early adopters. Customer experience remains a critical differentiator with personalized services and seamless return policies driving loyalty. Regulatory compliance regarding safety and environmental standards also influences competitive dynamics as consumers demand transparency. This complex landscape requires continuous adaptation and strategic innovation to maintain relevance and profitability in a rapidly evolving industry.

KEY MARKET PLAYERS

A few of the market players that are dominating the U.S mattress market are

- Tempur Sealy International Inc.

- Serta Simmons Bedding LLC

- Sleep Number Corporation

- Purple Innovation Inc.

- Casper Sleep Inc.

- Resident (Home of Nectar, DreamCloud)

- Saatva Inc.

- Helix Sleep LLC

- Brooklyn Bedding LLC

- Avocado Green Brands LLC

- Tuft & Needle (SSB)

- Ashley Furniture Industries LLC

- King Koil Mattress Co.

- Spring Air International

- The Original Mattress Factory

- Leesa Sleep LLC

- GhostBed (Nature's Sleep)

- Bear Mattress

- Cocoon by Sealy

- Zinus Inc.

Top Players In The Market

- Tempur Sealy International Inc is a global leader in the sleep industry known for its proprietary TEMPUR material and diverse brand portfolio including Sealy Stearns and Foster. The company leverages advanced pressure relieving technology to deliver superior comfort and support across various product lines. Recent actions include expanding its direct to consumer capabilities and enhancing digital marketing efforts to reach younger demographics effectively. Tempur Sealy focuses on sustainability initiatives by introducing eco friendly materials and reducing carbon footprint in manufacturing processes. The firm strengthens its market position through strategic partnerships with hospitality chains and healthcare providers to showcase product benefits. By investing in research and development the company continues to innovate in smart sleep technologies and adjustable bases. These efforts ensure sustained growth and brand loyalty in both residential and commercial sectors globally while maintaining high standards of quality and customer satisfaction.

- Serta Simmons Bedding LLC operates as a major entity in the global mattress landscape offering iconic brands such as Serta Simmons and Beautyrest. The company focuses on delivering innovative sleep solutions through continuous product development and enhanced distribution networks. Recent strategies involve integrating digital tools for personalized customer experiences and optimizing supply chain efficiency to reduce delivery times. Serta Simmons emphasizes sustainability by implementing recycling programs and using responsibly sourced materials in production. The firm expands its presence in the luxury segment through premium collections that feature advanced cooling and support technologies. Collaborations with retail partners and online platforms enhance accessibility and brand visibility for consumers. By prioritizing customer centric innovation and operational excellence Serta Simmons maintains its competitive edge. The company also invests in workforce training and community engagement to build strong corporate reputation and trust among stakeholders worldwide.

- Purple Innovation Inc distinguishes itself in the global market through its proprietary Hyper Elastic Polymer technology which offers unique comfort and support characteristics. The company focuses on direct to consumer sales models that provide convenience and transparency to customers seeking innovative sleep solutions. Recent actions include expanding retail partnerships with major brick and mortar stores to increase physical presence and allow product trials. Purple invests heavily in marketing campaigns that highlight the scientific benefits of its grid technology for pressure relief and temperature regulation. The firm diversifies its product line to include pillows sheets and adjustable bases creating a comprehensive sleep ecosystem. By leveraging data analytics Purple enhances customer engagement and personalizes recommendations effectively. The company prioritizes sustainable practices by designing durable products that minimize waste. These strategic moves strengthen its brand identity and drive growth in the competitive sleep industry while appealing to tech savvy and health conscious consumers.

Top Strategies Used By Key Market Participants

Key players in the United States mattress market prioritize omnichannel retail strategies to seamlessly integrate online and offline shopping experiences for enhanced customer convenience. Companies focus on product differentiation through proprietary technologies such as cooling gels and zoned support systems that appeal to specific health needs. Sustainability initiatives are prominently featured in marketing campaigns to build trust and align with environmentally conscious consumer values. Brands leverage social media influencers and digital advertising to increase brand awareness and engage with younger demographics effectively. Investment in advanced logistics and compressed packaging reduces shipping costs and improves delivery efficiency for direct to consumer models. Loyalty programs and extended trial periods foster long term customer relationships and encourage repeat purchases. Strategic partnerships with healthcare professionals and hospitality chains enhance brand credibility and visibility. These combined approaches allow firms to navigate competitive pressures and drive growth in a dynamic retail environment.

MARKET SEGEMENTATION

This research report on the US mattress market is segmented and sub-segmented into the following categories.

By Product Type

- Innerspring / Coil

- Foam (including memory foam)

- Latex

- Hybrid

- Other Mattress Types

By Mattress Size

- Single-size Mattress

- Double-size Mattress

- Queen-size Mattress

- King-size Mattress

- Custom & Specialty Sizes

By End User

- Residential

- Commercial

By Distribution Channel

- B2C/Retail

- Mass Merchandisers

- Specialty Mattress Stores (including exclusive brand outlets)

- Online

- Other Distribution Channels

- B2B/Project

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Frequently Asked Questions

What is currently driving growth in the United States mattress market?

Rising consumer focus on sleep quality and home comfort is driving market growth.

Why are consumers in the United States investing more in mattresses?

They are prioritizing better sleep health and overall well-being.

How would you explain the mattress market in simple terms?

It involves the production and sale of bedding products designed for sleep support.

Where are mattresses most commonly purchased in the United States?

They are widely purchased through retail stores, online platforms, and specialty outlets.

What makes mattresses important for daily life?

They provide comfort and support essential for quality sleep.

From a consumer perspective, is investing in a good mattress worthwhile?

Yes, it improves sleep quality and long-term health.

What challenges are affecting the United States mattress market?

High competition and fluctuating raw material costs are key challenges.

How is e-commerce influencing mattress sales in the United States?

Online platforms are making purchasing more convenient and accessible.

Which mattress types contribute the most to market demand?

Memory foam, innerspring, and hybrid mattresses are major contributors.

. Is the United States mattress market growing steadily?

Yes, it is expanding with increasing consumer awareness of sleep health.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com