U.S Pasta Market Size, Share, Trends & Growth Forecast Report - Segmented By Type, Raw Material, Distribution Channel, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S Pasta Market Size

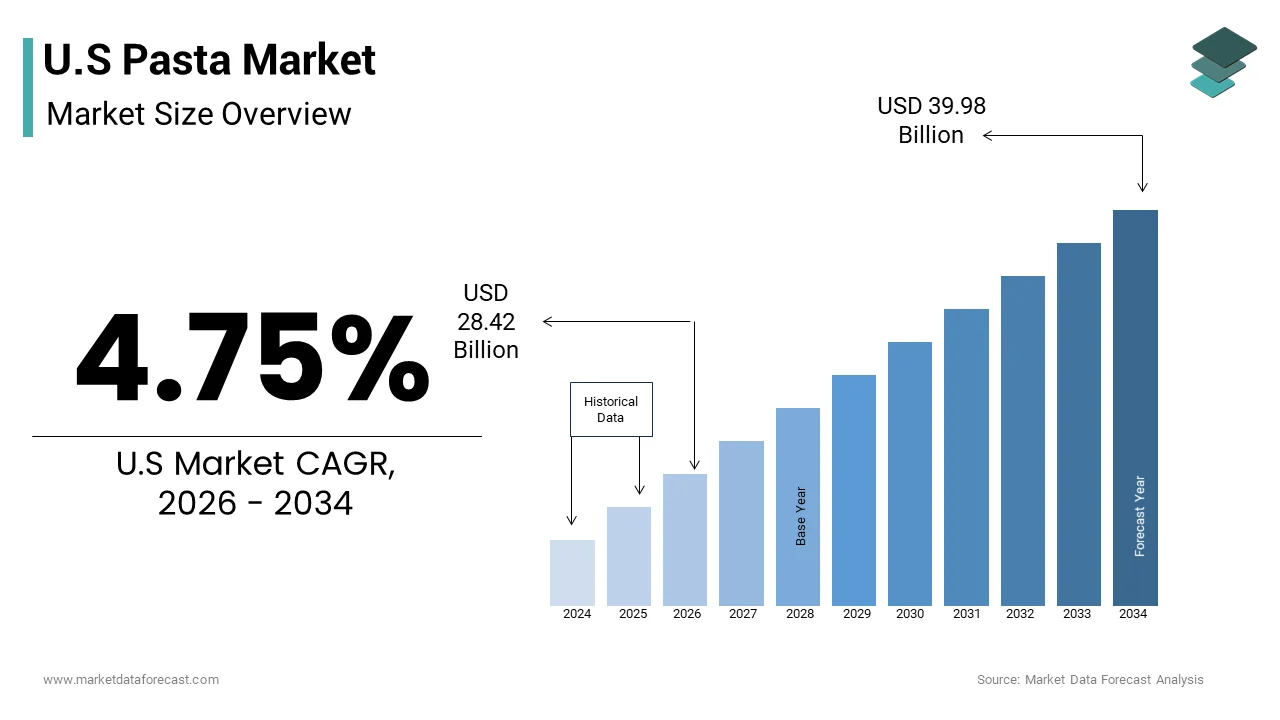

The U.S pasta market size was valued at USD 27.12 billion in 2025 and is anticipated to reach USD 28.42 billion in 2026 to reach USD 39.98 billion by 2034, growing at a CAGR of 4.75% during the forecast period from 2026 to 2034.

Introduction and Market Definition

The pasta is the versatility affordability and deep integration into American dietary habits. Pasta serves as a staple carbohydrate source for millions of households offering a convenient base for diverse culinary applications ranging from quick weeknight dinners to elaborate gourmet preparations. As per the National Pasta Association, the average American consumes approximately 20 pounds of pasta annually reflecting its entrenched position in household meal planning. The market encompasses a wide variety of shapes sizes and formulations including traditional semolina based products and innovative alternatives derived from legumes grains and vegetables. Consumer preferences have evolved to prioritize quality and nutritional value driving demand for organic whole wheat and gluten free options. The production infrastructure within the United States is robust with domestic manufacturers leveraging advanced extrusion and drying technologies to ensure consistent texture and cooking performance. Regulatory standards set by the Food and Drug Administration govern labeling and composition ensuring transparency for consumers regarding ingredients and allergens. The cultural acceptance of Italian cuisine has further solidified pasta as a mainstream food item rather than an ethnic specialty. Retail availability spans across supermarkets convenience stores and online platforms ensuring ubiquitous access.

MARKET DRIVERS

Resilience as an Affordable Protein and Carbohydrate Source

The enduring appeal of pasta as a cost-effective nutritional staple is majorly accelerating the growth of the United States pasta market. In periods of economic uncertainty or inflationary pressure consumers increasingly turn to affordable food options that provide satiety and versatility without compromising on taste. According to the study, food at home prices have experienced fluctuations prompting households to seek value oriented meals where pasta plays a central role. A single pound of dry pasta can feed a family of four making it an economical choice compared to meat centric dishes. The ability to pair pasta with inexpensive vegetables sauces and proteins enhances its budget friendly attribute. Nutritional awareness also contributes to this driver as enriched pasta provides essential nutrients such as iron and B vitamins which are critical for public health. The United States Department of Agriculture notes that grain consumption remains a significant component of the American diet with pasta offering a convenient way to meet daily grain recommendations. Furthermore, the long shelf life of dry pasta reduces food waste and allows for bulk purchasing which appeals to cost conscious shoppers. This economic resilience ensures that pasta maintains its volume sales even when discretionary spending declines.

Cultural Integration and Culinary Versatility

The deep cultural integration of Italian American cuisine and the inherent culinary versatility of pasta drive continuous consumption across diverse demographic groups. The cultural integration and culinary versatility is also boosting the growth of United States pasta market. Pasta has transcended its ethnic origins to become a universal comfort food accepted and loved by Americans of all backgrounds. As per data from the National Pasta Association, nearly 90% of American households include pasta in their regular meal rotation demonstrating its widespread acceptance. The adaptability of pasta allows it to fit into various dietary patterns including vegetarian vegan and Mediterranean diets which are gaining popularity. Consumers appreciate the ability to customize pasta dishes with endless combinations of sauces vegetables and proteins catering to individual taste preferences. The rise of home cooking trends particularly among younger generations has renewed interest in preparing pasta from scratch or experimenting with artisanal varieties. Social media platforms amplify this trend by showcasing creative recipes and cooking techniques that inspire consumers to try new shapes and flavors. Additionally, the convenience of pasta preparation aligns with busy lifestyles as it can be cooked quickly and paired with pre made sauces for rapid meal assembly. The emotional connection to pasta as a comforting and familiar food further reinforces its demand. Restaurants and food service providers also contribute by featuring pasta prominently on menus thereby influencing home cooking habits.

MARKET RESTRAINTS

Health Concerns Related to Carbohydrate Consumption

The growing health consciousness and the prevalence of low carbohydrate diets is hampering the growth of the United States pasta market. Many consumers associate refined carbohydrates with weight gain and blood sugar spikes leading them to reduce or eliminate pasta from their diets. According to the Centers for Disease Control and Prevention, obesity rates in the United States remain high prompting many individuals to adopt dietary strategies that limit carbohydrate intake. The perception of pasta as a high glycemic index food discourages health focused shoppers from purchasing traditional semolina based products. This shift in dietary behavior is particularly evident among millennials and Generation Z, who prioritize wellness and fitness. Nutritionists and health influencers often advocate for reducing refined grains further reinforcing negative perceptions. The stigma associated with carbs challenges manufacturers to reformulate products or educate consumers about the benefits of whole grain and enriched pasta. Despite efforts to promote balanced diets the prevailing narrative around carbohydrate restriction continues to dampen demand for standard pasta varieties.

Prevalence of Gluten Intolerance and Celiac Disease

The increasing diagnosis of celiac disease and non-celiac gluten sensitivity is additionally impeding the growth of United States pasta market. A growing segment of the population must strictly avoid gluten due to adverse health reactions limiting their ability to consume traditional pasta made from durum wheat. As per the Celiac Disease Foundation, approximately 1 in 100 people worldwide suffer from celiac disease with many more experiencing gluten sensitivity. This medical necessity drives these consumers away from standard pasta aisles toward specialized gluten free alternatives which often come at a premium price. The strict regulatory requirements for labeling gluten free products add complexity and cost for manufacturers who wish to cater to this niche. Cross contamination risks in facilities that process both wheat and gluten free ingredients necessitate separate production lines which can be prohibitively expensive for smaller brands. Consequently, the total addressable market for traditional pasta shrinks as more consumers identify with gluten free lifestyles. Even those without diagnosed conditions may choose gluten free options perceived as healthier or easier to digest. This trend fragments the market and dilutes the volume sales of conventional pasta. Manufacturers face the challenge of maintaining quality and texture in gluten free formulations which often differ significantly from wheat based counterparts.

MARKET OPPORTUNITIES

Expansion into Plant Based and Alternative Ingredient Formulations

The rising demand for plant based and alternative ingredient is an major factor is creating new opportunities for the growth of the United States pasta market. Consumers are increasingly seeking pasta made from legumes, such as chickpeas lentils and black beans, as well as ancient grains like quinoa and spelt. These alternatives offer higher protein and fiber content appealing to health conscious shoppers and those following vegetarian or vegan diets. According to the Plant Based Foods Association, sales of plant-based foods continue to grow outpacing overall food sales indicating strong consumer interest. Manufacturers can capitalize on this trend by introducing innovative blends that combine traditional semolina with nutrient dense ingredients to enhance nutritional profiles. The versatility of these alternative pastas allows them to be marketed not only as gluten free options but as superior nutritional choices. Retailers are dedicating more shelf space to these premium products reflecting their growing popularity. Online channels also provide a platform for niche brands to reach targeted audiences interested in specific dietary benefits. The opportunity extends to developing ready to eat meals featuring these alternative pastas which cater to convenience seekers.

Growth of Premium and Artisanal Pasta Segments

The emergence of premium and artisanal pasta for manufacturers to elevate brand value and appeal to discerning consumers is another attribute to fuel the growth of United states pasta market. Shoppers are increasingly willing to pay higher prices for pasta made with high quality ingredients such as organic durum wheat bronze cut techniques and slow drying processes. The premium pasta category has seen consistent growth as consumers seek restaurant quality experiences at home. Artisanal brands often emphasize traditional Italian methods and heritage which resonates with food enthusiasts looking for authenticity. The visual appeal of unique shapes and rustic packaging further enhances the perceived value of these products. Specialty grocery stores and high end retailers are key distribution channels for these premium offerings allowing brands to target affluent demographics. Limited edition releases and seasonal flavors can drive trial and excitement among adventurous cooks. Additionally, the gift market for gourmet food baskets includes premium pasta as a staple item expanding its usage occasions. By focusing on quality craftsmanship and storytelling manufacturers can command higher price points and build loyal customer bases.

MARKET CHALLENGES

Volatility in Durum Wheat Prices and Supply Chain Disruptions

The instability of durum wheat prices and supply chain disruptions is one of the major challenges for the growth of United States pasta market. Durum wheat is the primary ingredient for high quality pasta and its availability is subject to climatic conditions geopolitical tensions and global trade dynamics. These input cost increases squeeze profit margins for manufacturers who may struggle to pass these costs onto price sensitive consumers. Supply chain disruptions in transportation and logistics further exacerbate the issue by delaying raw material deliveries and increasing freight expenses. The reliance on imported durum wheat from countries like Canada and Italy exposes manufacturers to currency fluctuations and trade policy changes. Any disruption in these international supply lines can lead to shortages and production delays. Manufacturers must maintain strategic stockpiles and diversify sourcing strategies to mitigate these risks which requires substantial capital investment. The unpredictability of raw material costs makes long term pricing strategies difficult to implement. Additionally, the energy intensive nature of pasta production means that rising utility costs further compound financial pressures.

Intense Competition from Private Label and Store Brands

The intense competition from private label and store brands to national pasta brands is additionally to hinder the growth of the United States pasta market. Retailers have invested heavily in improving the quality and packaging of their own label pasta products offering consumers a cheaper alternative to name brands. Store brands often mimic the quality and appearance of leading national brands while undercutting them on price. This price pressure forces national brands to invest heavily in marketing and promotions to maintain brand loyalty and justify premium pricing. The differentiation between national and private label pasta has narrowed as manufacturing standards have improved across the board. Retailers leverage their shelf power to promote private labels through prominent placement and exclusive deals further disadvantaging national brands. The lack of brand attachment for a commodity product like pasta makes consumers more likely to switch to lower priced options. National brands must continuously innovate and emphasize unique selling propositions such as organic certification or special blends to retain customers.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.75% |

| Segments Covered | By Type, Raw Material, Distribution Channel, and Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities. |

| Regions Covered | US, Canada, and the Rest of North America |

| Market Leaders Profiled | Barilla Group (Italy), F.lli De Cecco di Filippo S.p.A (Italy), Ebro Foods, S.A (Spain), Nestlé S.A. (Switzerland), Unilever plc (U.K.), E. D. Smith & Sons Ltd (No Noodles Brand) / Or Private Label Leaders like TreeHouse Foods, Armanino Foods-Distinction Inc. (U.S.), The Kraft Heinz Company (U.S.), Banza Inc. (U.S.), Borges International Group, S.L.U. (Spain), 8TH Avenue Food & Provisions (U.S.) |

SEGMENTAL ANALYSIS

By Type Insights

The dried pasta segment was accounted in holding 43.5% of the United States pasta market share in 2025 due to its exceptional shelf stability and cost effectiveness, which align with household budgeting and storage preferences. The extended shelf life of dried pasta allows consumers to purchase in bulk and store it for long periods without spoilage reducing food waste and frequent shopping trips. This convenience is particularly valued by families and individuals seeking reliable meal solutions that do not require refrigeration. The production process for dried pasta involves low moisture content which inhibits microbial growth and ensures safety without the need for preservatives. Retailers favor dried pasta because it requires less complex logistics and lower energy costs for storage compared to chilled alternatives. The affordability of dried pasta makes it accessible to a broad demographic including low-income households who prioritize value. During economic downturns the sales of dried pasta often increase as consumers shift away from more expensive fresh foods. The versatility of dried pasta in various culinary applications from simple buttered noodles to complex casseroles further cements its dominance. Manufacturers benefit from economies of scale in producing dried pasta which allows for competitive pricing and widespread distribution.

The chilled segment is likely to grow at an anticipated CAGR of 10.6% during the forecast period with the increasing consumer demand for convenience and the perception of superior freshness. Modern lifestyles characterized by busy schedules have led to a rise in the purchase of ready to cook and ready to eat meals where chilled pasta plays a key role. Consumers associate chilled pasta with higher quality and restaurant like experiences at home which justifies the premium price point. The shorter shelf life of chilled pasta is offset by its immediate readiness which reduces preparation time significantly. Retailers are expanding their refrigerated sections to accommodate a wider variety of chilled pasta options including stuffed ravioli tortellini and gnocchi. The availability of fresh herbs and sauces in the same aisle facilitates one stop shopping for complete meal solutions. Younger demographics particularly millennials and Generation Z are driving this trend as they prioritize convenience without compromising on taste. The visual appeal of chilled pasta packaging which often highlights artisanal qualities also attracts attention in stores.

By Raw Material Insights

The wheat pasta segment was the largest by occupying 23.4% of the United States pasta market share in 2025 due to well established supply chains and deep rooted consumer familiarity with wheat based products. Durum wheat is the primary raw material for traditional pasta and its cultivation and processing infrastructure in North America are highly developed. According to the United States Department of Agriculture, the United States is a major producer of durum wheat ensuring a steady and reliable supply for domestic pasta manufacturers. This local sourcing reduces transportation costs and supports national agricultural industries, which appeals to policymakers and consumers alike. The taste and texture of wheat pasta are considered the standard by most Americans making it the default choice for everyday meals. Generations of consumers have grown up eating wheat pasta creating a strong habitual preference that is difficult to disrupt. The versatility of wheat pasta in absorbing sauces and maintaining structure during cooking makes it ideal for a wide range of dishes. Manufacturers benefit from the economies of scale associated with wheat production which keeps prices competitive and affordable for mass market consumers. The regulatory framework for wheat labeling is clear and understood by shoppers reducing confusion at the point of purchase. Furthermore, the enrichment of wheat pasta with essential nutrients such as iron and folic acid adds to its nutritional appeal.

The gluten free segment is esteemed to grow at an anticipated CAGR of 8.4% from 2026 to 2034 owing to the rising health awareness and the increasing prevalence of celiac disease and gluten sensitivity. Consumers are becoming more educated about the potential adverse effects of gluten leading many to adopt gluten free diets even without a medical diagnosis. The number of Americans diagnosed with celiac disease or non-celiac gluten sensitivity has increased significantly in recent years creating a larger addressable for gluten free products. This medical necessity drives consistent demand for high quality gluten free pasta alternatives made from rice corn quinoa and legumes. The improvement in taste and texture of gluten free pasta has also attracted non celiac consumers who perceive these products as healthier or easier to digest. Retailers are responding by expanding their gluten free sections and offering a wider variety of shapes and brands. The marketing of gluten free pasta as part of a wellness lifestyle appeals to health conscious shoppers who prioritize clean labels and natural ingredients. Social media and influencer endorsements further amplify the visibility of gluten free options encouraging trial among new customers.

By Distribution Channel Insights

The supermarkets and hypermarkets segment held a dominant share of the United States pasta market in 2025 due to the convenience of one stop shopping and the extensive variety of products offered. Consumers prefer purchasing pasta alongside other grocery items such as sauces vegetables and meats which simplifies meal planning and preparation. These retail giants offer a wide range of pasta types brands and price points catering to diverse consumer preferences and budgets. The prominent shelf placement of pasta in central aisles ensures high visibility and accessibility for shoppers. Promotional activities such as discounts bundle deals and loyalty program rewards further drive sales in this channel. Supermarkets also facilitate the launch of new products by providing ample shelf space and marketing support to manufacturers. The trust consumers place in established retail chains for product quality and safety reinforces their preference for purchasing pasta here. The ability to physically inspect packaging and compare prices empowers consumers to make informed decisions. Additionally, the presence of in store bakeries and delis often inspires meal ideas that include pasta. This comprehensive shopping experience combined with competitive pricing ensures that supermarkets remain the dominant channel for pasta distribution.

The online retail segment is deemed to witness a fastest CAGR of 7.6% during the forecast period with the widespread adoption of e commerce and the convenience of home delivery. The shift towards digital shopping has accelerated in recent years as consumers seek time saving solutions for grocery procurement. Online platforms offer an unparalleled selection of pasta brands including niche artisanal and specialty products that may not be available in local stores. The ability to compare prices read reviews and access detailed product information enhances the shopping experience and builds consumer confidence. Subscription services provided by online retailers allow customers to automate recurring purchases of staple items like pasta ensuring they never run out. The convenience of doorstep delivery is particularly appealing to busy professionals and families who value time efficiency. During periods of restricted mobility or health concerns online shopping became a essential lifeline for many households establishing lasting habits. Retailers have invested heavily in logistics and cold chain infrastructure to ensure timely and safe delivery of goods.

COMPETITIVE LANDSCAPE

The competition in the United States pasta market is characterized by a mix of established global brands and aggressive private label offerings from major retailers. National brands compete on quality heritage and innovation while store brands leverage price advantages and shelf dominance to capture value oriented consumers. The market is highly fragmented with numerous regional players contributing to intense rivalry. Differentiation is achieved through product attributes such as organic certification gluten free formulations and unique shapes that appeal to niche demographics. Price sensitivity remains a key factor influencing purchasing decisions particularly during economic downturns when consumers trade down to lower cost alternatives. Manufacturers invest heavily in marketing and packaging design to enhance brand visibility and emotional connection with shoppers. Supply chain efficiency and sourcing strategies are critical for maintaining margins amidst fluctuating raw material costs. Retailers exert significant power by negotiating favorable terms and promoting their own labels which pressures national brands to innovate continuously. The rise of e commerce adds another layer of competition as online platforms offer wider selections and convenience. Success depends on balancing cost effectiveness with product quality and brand storytelling.

KEY MARKET PLAYERS

A few of the market players that are dominating the U.S pasta market are

- Barilla Group (Italy)

- F.lli De Cecco di Filippo S.p.A (Italy)

- Ebro Foods, S.A (Spain)

- Nestlé S.A. (Switzerland)

- Unilever plc (U.K.)

- E. D. Smith & Sons Ltd (No Noodles Brand) / Or Private Label Leaders like TreeHouse Foods

- Armanino Foods-Distinction Inc. (U.S.)

- The Kraft Heinz Company (U.S.)

- Banza Inc. (U.S.)

- Borges International Group, S.L.U. (Spain)

- 8TH Avenue Food & Provisions (U.S.)

Top Players In The Market

- Barilla Group stands as a prominent entity in the United States pasta market leveraging its global reputation for quality and tradition. The company contributes significantly to the international landscape by exporting Italian culinary heritage and setting standards for sustainable production practices. It strengthens its position through continuous innovation in product formulations including whole grain and gluten free options that align with modern dietary preferences. Recent actions involve expanding its manufacturing capabilities in North America to enhance supply chain efficiency and reduce carbon footprints. The organization also invests heavily in digital marketing campaigns that emphasize family values and healthy eating habits. These efforts resonate with American consumers who prioritize transparency and nutritional benefits. The company focuses on enhancing retail partnerships to ensure widespread availability across diverse channels. Its dedication to quality and environmental stewardship solidifies its leadership role in the industry.

- De Cecco is renowned for its premium quality pasta products that appeal to discerning consumers seeking authentic Italian experiences in the United States. The company plays a vital role in the global market by maintaining traditional bronze die extrusion methods that ensure superior texture and sauce adherence. It strengthens its market position by targeting the high end segment with artisanal packaging and distinctive branding that highlights its heritage. Recent actions include expanding distribution networks to reach independent grocery stores and specialty retailers across the nation. The brand emphasizes its use of high quality semolina wheat sourced from select regions to guarantee consistent flavor profiles. Marketing initiatives focus on educating consumers about the benefits of slow drying processes and traditional craftsmanship. De Cecco also engages in culinary collaborations with chefs to showcase versatile recipe applications. These strategies enhance brand prestige and attract food enthusiasts who value authenticity. The company avoids mass market price competition by positioning itself as a luxury option.

- TreeHouse Foods serves as a major player in the United States pasta market primarily through its extensive private label manufacturing capabilities. The company contributes to the global sector by providing scalable production solutions for retailers seeking affordable and high quality store brand options. It strengthens its position by optimizing operational efficiencies and investing in advanced processing technologies that reduce costs and improve product consistency. Recent actions involve acquiring additional manufacturing facilities to expand capacity and meet growing demand for private label goods. TreeHouse Foods focuses on developing innovative pasta varieties such as protein enriched and vegetable based blends to cater to health conscious trends. The company leverages its broad distribution network to ensure products are available in major supermarket chains nationwide. Strategic partnerships with retailers enable customized product offerings that align with specific consumer preferences.

Top Strategies Used By Key Market Participants

Key players in the United States pasta market employ product diversification strategies to address evolving consumer dietary needs and preferences. Companies increasingly introduce gluten free organic and legume based pasta varieties to capture health conscious segments. Sustainability initiatives are central to corporate strategies as brands highlight eco friendly packaging and responsible sourcing practices to appeal to environmentally aware shoppers. Premiumization efforts involve launching artisanal lines with unique shapes and flavors that command higher price points and differentiate from standard offerings. Digital marketing and social media engagement are utilized to build brand loyalty and educate consumers on cooking techniques and nutritional benefits. Strategic partnerships with retailers ensure prominent shelf placement and promotional visibility for both national and private label brands. Cost optimization through supply chain enhancements and local sourcing helps maintain competitiveness against inflationary pressures. Innovation in convenience formats, such as ready to eat meals caters to busy lifestyles and drives incremental sales.

MARKET SEGMENTATION

This research report on the U.S pasta market is segmented and sub-segmented into the following categories.

By Type

- Dried

- Chilled

- Canned

By Raw Material

- Wheat

- Gluten-free

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail

- Others

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Frequently Asked Questions

What is currently driving growth in the United States pasta market?

Rising demand for convenient and affordable meal options is driving market growth.

Why is pasta a popular food choice in the United States?

It is versatile, easy to prepare, and widely accepted across different cuisines.

How would you explain the pasta market in simple terms?

It involves the production and sale of dried and fresh pasta products for consumption.

Where is pasta most commonly consumed in the United States?

It is widely consumed in households, restaurants, and food service outlets.

What makes pasta important in everyday diets?

It provides a convenient source of carbohydrates and can be prepared in many ways.

From a consumer perspective, is pasta a cost-effective food option?

Yes, it is affordable and suitable for a variety of meals.

What challenges are affecting the United States pasta market?

Changing dietary preferences and competition from alternative foods are key challenges.

How is health awareness influencing pasta consumption?

Consumers are increasingly seeking whole grain and healthier pasta options.

Which pasta types contribute the most to market demand?

Dried pasta and ready-to-cook varieties are major contributors.

Is the United States pasta market growing steadily?

Yes, it is expanding with consistent consumer demand.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com