U.S. Pepper Market Size, Share, Trends, and Growth Analysis Report, Segmented by Nature, Product Type, Application, Form, and Country – Industry Forecast From 2026 to 2034

U.S. Pepper Market Size

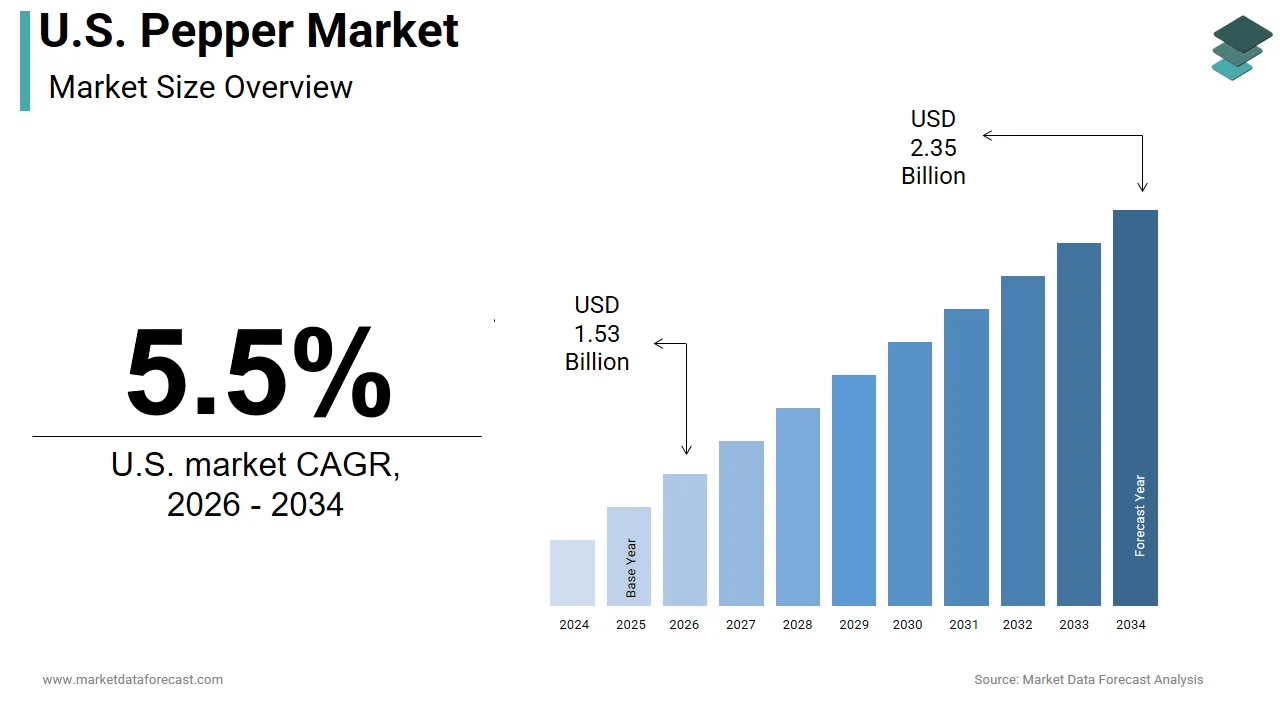

The U.S. pepper market was valued at USD 1.45 billion in 2025, is estimated to reach USD 1.53 billion in 2026, and is projected to reach USD 2.35 billion by 2034, growing at a CAGR of 5.5% from 2026 to 2034.

The pepper is the capsicum species, including bell peppers chili peppers and specialty varieties, such as jalapenos and habaneros. Peppers are valued for their nutritional content, particularly high levels of vitamin C and antioxidants, which align with contemporary health trends. The agricultural landscape for peppers is concentrated in states like California, Florida, and New Mexico, where climate conditions support year round or seasonal production. The total acreage dedicated to vegetable production has seen shifts towards high value crops including peppers due to their profitability. Consumer dietary patterns have evolved to include more ethnic cuisines, such as Mexican Asian and Mediterranean foods, which heavily utilize peppers for flavor and heat. The increased consumption of vegetables is encouraged to combat chronic diseases, further boosting demand. Import reliance remains significant particularly during off seasons with Mexico, being a primary supplier.

MARKET DRIVERS

Rising Popularity of Ethnic Cuisines and Flavor Profiles Drives Demand

The increasing popularity of ethnic cuisines, particularly Mexican, Indian, and Thai foods is bolstering the growth of the United States pepper market. These culinary traditions rely extensively on various types of peppers to provide heat depth and complexity to dishes. As per the study, ethnic flavors continue to dominate menu trends with spicy items gaining traction, among American diners. The widespread availability of international ingredients in mainstream grocery stores has made it easier for consumers to replicate these flavors at home. Bell peppers are staple ingredients in fajitas stir fries and salads while chili peppers are essential for salsas curries and hot sauces. The rise of food tourism and social media platforms has exposed consumers to diverse culinary experiences, fostering a willingness to experiment with spicier and more complex flavor profiles. According to the Specialty Food Association sales of hot sauces and spicy condiments have grown significantly reflecting this shift in consumer preference. The millennial and Gen Z demographics are particularly influential in this trend as they prioritize authentic and bold taste experiences.

Health Consciousness and Nutritional Benefits Boost Consumption

The growing health consciousness among consumers due to the high nutritional value is accelerating the growth of the United States pepper market. Peppers are rich in vitamins A and C, potassium and fiber by making them an attractive option for health focused individuals. As per the Centers for Disease Control and Prevention, only 1 in 10 adults meet the federal fruit or vegetable recommendations creating a substantial opportunity for growth in vegetable consumption. Peppers are low in calories and high in antioxidants, which help reduce inflammation and support immune function. The trend towards plant-based diets has further amplified the demand for versatile vegetables that can serve as main ingredients or flavorful additives. Bell peppers in particular are popular in keto and paleo diets due to their low carbohydrate content. According to the International Food Information Council consumer surveys indicate that a majority of Americans are actively trying to consume more vegetables for health benefits. The visual appeal of colorful peppers also contributes to their popularity in healthy meal preparation and social media sharing. Nutritionists and dietitians frequently recommend peppers as part of a balanced diet to prevent chronic diseases such as heart disease and cancer.

MARKET RESTRAINTS

Vulnerability to Climate Change and Extreme Weather Events

The climate change and extreme weather events by disrupting agricultural production and supply stability is hindering the growth of the United States pepper market. Peppers are sensitive to temperature fluctuations droughts and excessive rainfall, which can lead to reduced yields and poor quality. The frequency of severe weather events, such as hurricanes and heatwaves has increased in key growing regions like Florida and California. These events can cause immediate crop damage and long term soil degradation affecting future planting cycles. Drought conditions necessitate increased irrigation which raises production costs and strains water resources. The water scarcity issues in the West have forced some farmers to reduce acreage or switch to less water intensive crops. The unpredictability of weather patterns makes it difficult for growers to plan harvests and meet contractual obligations. Supply shortages resulting from weather related disruptions lead to price volatility which can dampen consumer demand. Importers may face similar challenges in source countries such as Mexico exacerbating supply chain instability. The financial risk associated with climate variability discourages investment in expansion and innovation.

Labor Shortages and Rising Production Costs Impact Profitability

The labor shortages and rising production costs by squeezing profit margins for growers is also to declining the growth of United States pepper market. Pepper harvesting is labor intensive as it often requires manual picking to ensure quality and prevent damage to the plants. The agricultural sector faces a chronic shortage of workers due to stricter immigration policies and an aging domestic workforce. This shortage leads to delays in harvesting which can result in crop loss and reduced marketable yield. The inability to secure sufficient labor forces growers to pay higher wages to attract workers which increases operational expenses. The increased costs are difficult to pass on to consumers who are price sensitive regarding fresh produce. Additionally, the cost of inputs such as fertilizers pesticides and fuel has surged due to global supply chain disruptions and geopolitical tensions. Small and medium sized farms are particularly vulnerable as they lack the economies of scale to absorb these costs. The combination of labor scarcity and input inflation threatens the economic viability of domestic pepper production.

MARKET OPPORTUNITIES

Expansion of Organic and Sustainable Pepper Cultivation

The expansion of organic and sustainable pepper cultivation to capture value conscious consumers is majorly to accelerate new opportunities for the growth of the United States pepper market. Demand for organic produce is growing as shoppers become more aware of the environmental and health impacts of conventional farming practices. Organic peppers command a premium price which can offset higher production costs and improve profitability for growers. Consumers are willing to pay more for products that are free from synthetic pesticides and genetically modified organisms. The federal government supports organic transition through cost share programs and technical assistance which lowers barriers for farmers. The number of certified organic operations continues to rise indicating a supportive ecosystem. Retailers are expanding their organic sections to meet this demand providing greater shelf space for organic peppers. Sustainability certifications such as Regenerative Organic Certified also offer differentiation opportunities for brands committed to soil health and carbon sequestration. The trend towards local and transparent supply chains further enhances the appeal of organic peppers grown domestically.

Innovation in Value Added and Convenience Products

Innovation in value added and convenience products to expand beyond fresh sales is another attribute to promote growth opportunities for the expansion of United States pepper market. Consumers are increasingly seeking ready to eat and easy to prepare food options due to busy lifestyles. Pre washed cut and packaged peppers, such as stir fry mixes and stuffed pepper kits cater to this demand for convenience. Processed pepper products, such as roasted peppers pepper jams and infused oils also provide avenues for product diversification. These items have longer shelf lives and can be marketed as gourmet ingredients for home cooking. The rise of e commerce and direct to consumer models allows brands to reach wider audiences with specialized pepper products. The online grocery sales have stabilized at higher levels post pandemic creating a durable channel for innovation. Manufacturers can leverage technology to develop novel packaging that preserves freshness and reduces waste. Collaborations with chefs and food influencers can help promote these value-added products and educate consumers on their versatility.

MARKET CHALLENGES

Supply Chain Disruptions and Logistics Bottlenecks

The supply chain disruptions and logistics hurdles by affecting the timely delivery and quality of products is one of the challenges for the growth of the United States pepper market. Peppers are perishable goods that require efficient cold chain management to maintain freshness from farm to table. According to the Federal Reserve Bank of New York, global supply chain pressures have caused delays in transportation and increased freight costs. Port congestion and trucking shortages can lead to spoilage and reduced shelf life for imported and domestic peppers. The reliance on imports from Mexico means that any disruption at the border or in transit can cause immediate supply shortages. Retailers face difficulties in maintaining consistent stock levels, which can lead to lost sales and customer dissatisfaction. The cost of refrigerated transport has risen due to fuel price volatility and equipment shortages further straining margins. Small growers and distributors are particularly affected as they lack the resources to mitigate these risks through diversified logistics networks. The complexity of coordinating multiple stakeholders in the supply chain increases the likelihood of errors and delays.

Intense Competition from Imported Peppers

The intense competition from imported peppers to domestic producers by exerting downward pressure on prices is additionally to inhibit the growth of United States pepper market. Mexico is the largest supplier of fresh peppers to the United States benefiting from lower labor costs and favorable climate conditions that allow for year-round production. The import volumes of fresh peppers have increased steadily over the past decade displacing domestic supply during off seasons. The lower cost of imported peppers makes it difficult for US growers to compete on price particularly in the commodity segment. Retailers often prioritize cheaper imports to maximize margins which limits shelf space for domestic products. Domestic producers face higher regulatory and environmental compliance costs which further erode their competitiveness. The seasonal nature of US production means that growers must maximize revenue during short windows making them vulnerable to price fluctuations. Efforts to promote local produce through marketing campaigns have had limited success against the sheer volume and affordability of imports.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Nature, Product Type, Application, Form, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | Everest Spices, MDH Spices, Nestlé S.A., Gupta Trading Company, SAIGON HANOI IMEXCO LTD., British Pepper & Spice Co. Ltd., McCormick & Company, Inc., Olam International, Intimex Group, and Others. |

SEGMENTAL ANALYSIS

By Nature Insights

The conventional segment was accounted in holding a prominent share of the United States pepper market in 2025 due to their widespread availability affordability and established supply chains. The dominance of this segment is driven by the high-volume production capabilities of conventional farming which meets the mass market demand for fresh and processed peppers. Lower production costs associated with conventional methods allow retailers to offer competitive prices which appeals to price sensitive consumers. The extensive distribution network for conventional produce ensures that peppers are accessible in grocery stores supermarkets and food service establishments across the nation. The familiarity of conventional peppers among consumers also contributes to their sustained popularity as they remain a staple ingredient in everyday cooking. Major food manufacturers and restaurant chains prefer conventional peppers due to their uniform quality and reliable sourcing.

The organic pepper segment is likely to witness a fastest CAGR of 8.5% during the forecast period with the increasing consumer awareness regarding health benefits and environmental sustainability. Shoppers are increasingly seeking produce free from synthetic pesticides and fertilizers, which drives demand for organic options. The sales of organic fruits and vegetables have consistently outpaced conventional produce growth reflecting a shift in consumer preferences. The younger people, particularly millennials and Gen Z are willing to pay a premium for organic products that align with their values. Retailers are responding by expanding their organic offerings and dedicating more shelf space to certified organic peppers. Government incentives and support programs for organic transition further encourage farmers to adopt sustainable practices. The perception of organic peppers as healthier and safer for consumption reinforces their appeal among health-conscious families.

By Product Type Insights

The black pepper segment was the largest by holding 58.4% of the United States spice market share in 2025 due to its universal usage as a fundamental seasoning in American cuisine. The versatility and presence in nearly every household and commercial kitchen is fuelling the growth of the segment. According to the Spice Trade Association black pepper remains the most widely consumed spice in the United States accounting for a significant portion of total spice imports. Its ability to enhance the flavor of a wide variety of dishes from meats to vegetables ensures steady demand. The industrial food sector also relies heavily on black pepper for processed foods ready to eat meals and snacks. The long shelf life of black pepper corns and ground powder makes it a convenient pantry item for consumers. Established supply chains from major producing countries such as Vietnam India and Brazil ensure consistent availability. The cultural ingraining of black pepper in Western culinary traditions solidifies its leading position.

The red pepper segment is deemed to grow at an fastest CAGR of 6.2% during the forecast period with the increasing popularity of spicy foods and global cuisines that utilize red pepper for heat and color. The demand for hot and spicy menu items has surged influencing consumer purchasing behavior in retail sectors. The rise of hot sauce culture and spicy snack foods that further boosts the consumption of red pepper variants. Health benefits associated with capsaicin the active component in red peppers, such as metabolism boosting and pain relief also attract health conscious consumers. The visual appeal of red pepper in culinary presentations enhances its usage in professional and home cooking. Social media trends showcasing spicy food challenges and recipes have amplified interest in red pepper products.

By Application Insights

The food and beverage application segment was accounted in holding a dominant share of the United States pepper market in 2025 with the extensive use of peppers as ingredients in culinary preparations and processed foods. According to the United States Department of Agriculture, the majority of pepper production and imports are directed towards human consumption either as fresh produce or processed ingredients. The versatility of peppers allows them to be used in a wide range of dishes from salads and stir fries to sauces and soups. The food service industry relies heavily on peppers for menu diversity and flavor enhancement. The processed food sector utilizes peppers in ready to eat meals snacks and condiments which expands their application beyond fresh consumption. The growing trend of home cooking and meal preparation kits also contributes to this dominance as consumers seek fresh and flavorful ingredients. The integration of peppers into mainstream dietary habits ensures a consistent and high-volume demand.

The personal care products application segment is likely to witness a fastest CAGR of 7.0% during the forecast period with the increasing incorporation of pepper extracts and essential oils in cosmetic and wellness products. Capsaicin and other compounds found in peppers are valued for their anti-inflammatory and circulation boosting properties which are beneficial in skincare and haircare formulations. The demand for natural and active ingredients in beauty products has risen prompting manufacturers to explore botanical extracts like pepper. Pepper infused products such as scalp treatments lip plumpers and body scrubs are gaining popularity among consumers seeking innovative solutions. The aromatherapy sector also utilizes pepper essential oils for their stimulating and warming effects. The perceived efficacy of pepper based ingredients in addressing issues such as muscle pain and skin dullness enhances their appeal.

By Form Insights

The powdered pepper segment was the largest by holding 34.6% during the forecast period with the convenience ease of use and long shelf life. The widespread availability of powdered pepper in various packaging sizes makes it accessible to a broad range of consumers from individual households to large scale food manufacturers. The consistency of flavor and texture in powdered form ensures predictable results in culinary applications. The processing of peppers into powder extends their usability and reduces waste compared to fresh forms. The industrial food sector heavily relies on powdered pepper for standardized formulation of processed foods and snacks. The ability to blend powdered pepper with other spices creates convenient seasoning mixes that appeal to busy consumers. Retailers prioritize powdered pepper due to its higher turnover rates and compact storage requirements.

The whole pepper segment is deemed to grow at an anticipated CAGR of 5.5% from 2026 to 2034 with the increasing consumer appreciation for freshness and aromatic quality associated with whole forms. The rise of gourmet cooking and home mixology trends has elevated the status of whole peppercorns as premium ingredients. Fresh whole peppers, such as bell and chili varieties are also gaining traction due to the farm to table movement, which emphasizes fresh and unprocessed produce. As per the United States Department of Agriculture sales of fresh vegetables have remained strong reflecting consumer desire for healthy and natural food options. The visual appeal of whole peppers in culinary presentations enhances their usage in high end dining and social media content. The perception of whole peppers as more authentic and less processed than powdered forms attracts health conscious consumers. Retailers are expanding their offerings of specialty whole peppers including heirloom and exotic varieties to meet this demand.

COMPETITIVE LANDSCAPE

The competition in the United States pepper market is characterized by a mix of large multinational corporations and specialized spice traders who compete on quality sourcing and brand recognition. The market structure is moderately fragmented with several key players holding influence over specific segments such as retail or industrial supply. Competitive intensity is driven by the need to differentiate through product purity origin stories and sustainability credentials. Innovation in packaging and convenience formats plays a vital role as firms seek to appeal to busy consumers. Regulatory compliance regarding food safety and labeling serves as a barrier to entry for smaller competitors. Established players leverage their extensive distribution networks to ensure widespread availability and consistent supply. Customer loyalty is maintained through transparent sourcing practices and educational marketing campaigns. Price competition remains intense in the commodity segment while premium segments focus on value added features.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. pepper market include

- Everest Spices

- MDH Spices

- Nestle S.A.

- Gupta Trading Company

- SAIGON HANOI IMEXCO LTD.

- British Pepper & Spice Co Ltd.

- McCormick & Company, Inc.

- Olam International

- Intimex Group.

TOP PLAYERS IN THE MARKET

- McCormick and Company is a global leader in the spice and flavoring industry with a dominant presence in the United States pepper market. The company offers a wide range of pepper products including black white and red varieties under its flagship brand. McCormick strengthens its position through continuous innovation in flavor profiles and sustainable sourcing initiatives. The company recently invested in digital platforms to enhance consumer engagement and provide recipe inspiration. Its robust supply chain ensures consistent quality and availability across retail and food service channels. McCormick, also focuses on strategic acquisitions to expand its portfolio of premium and organic spices. These efforts reinforce its reputation for reliability and quality in the global spice sector.

- Olam International is a major agribusiness player with significant involvement in the global pepper supply chain. The company sources processes and distributes high quality peppers from key producing regions such as Vietnam India and Brazil. Olam strengthens its market position by implementing sustainable farming practices and supporting smallholder farmers through training programs. The company recently expanded its processing facilities to improve efficiency and product consistency. Olam focuses on traceability and transparency to meet the growing demand for ethically sourced ingredients. Its integrated supply chain model allows for better risk management and cost control. These initiatives ensure that Olam remains a trusted supplier for global food manufacturers and retailers seeking reliable pepper solutions.

- Nestle S.A. participates in the global pepper market primarily through its culinary and seasoning brands such as Maggi. The company incorporates pepper into various ready to eat meals bouillons and spice blends catering to diverse consumer preferences. Nestle strengthens its position by focusing on health and wellness trends offering lower sodium and natural ingredient options. The company recently launched new product lines featuring bold and authentic flavors including spicy pepper variants. Nestle leverages its extensive distribution network to reach consumers in both developed and emerging markets. Its commitment to sustainability and responsible sourcing enhances brand loyalty. These strategic moves allow Nestle to maintain a strong presence in the competitive global seasoning and spice industry.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United States pepper market primarily employ strategies such as product diversification sustainable sourcing and digital engagement to strengthen their market position. Companies frequently expand their portfolios to include organic and specialty pepper varieties that cater to health conscious consumers. This approach allows them to capture niche segments and command premium pricing. Investment in sustainable farming practices is crucial for ensuring long term supply stability and meeting regulatory standards. Digital transformation is another key strategy as companies implement e commerce platforms and social media marketing to reach direct consumers. Strategic partnerships with retailers and food service providers help secure shelf space and build brand loyalty. Additionally, firms focus on supply chain resilience by diversifying sourcing locations to mitigate risks.

MARKET SEGMENTATION

This research report on the U.S. pepper market has been segmented and sub-segmented into the following categories.

By Nature

- Organic

- Conventional

By Product Type

- White Pepper

- Black Pepper

- Green Pepper

- Red Pepper

By Application

- Food and Beverage

- Snacks and Convenience Food

- Meat & Poultry Products

- Beverages

- Sauces & Dressing

- Bakery and Confectionery Products

- Frozen Products

- Personal Care Products

- Others

By Form

- Whole Pepper

- Powdered Pepper

By Country

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

What is the U.S. pepper market?

The U.S. pepper market includes fresh bell peppers, chili varieties, black pepper imports, and ground spices for cooking, food processing, and retail sales nationwide.

How does the U.S. pepper market function?

The U.S. pepper market functions through domestic farms, imports from Mexico and other countries, distribution to grocers, and processing for spices and ready meals.

What drives growth in the U.S. pepper market?

The U.S. pepper market grows from demand for fresh produce, organic options, processed foods, and year-round supply through imports and advanced farming.

Which pepper types lead the U.S. pepper market?

The U.S. pepper market features bell peppers, chili peppers, black pepper, and ground varieties popular in households and food manufacturing.

What role do imports play in the U.S. pepper market?

Imports sustain the U.S. pepper market by providing off-season bell peppers and steady black pepper supply from global producers.

How important are bell peppers in the U.S. pepper market?

Bell peppers drive the U.S. pepper market as fresh produce staples used in salads, cooking, and year-round consumer demand.

What is black pepper's place in the U.S. pepper market?

Black pepper anchors the U.S. pepper market as an essential spice import for seasoning, blending, and food industry applications.

How does domestic production fit the U.S. pepper market?

Domestic production supports the U.S. pepper market mainly through chili peppers grown in key states despite challenges in acreage.

What trends shape the U.S. pepper market?

The U.S. pepper market follows organic demand, clean-label preferences, premium spices, and expanded use in ready-to-eat foods.

What challenges face the U.S. pepper market?

The U.S. pepper market contends with declining domestic yields, import reliance, supply chain issues, and climate impacts on production.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com